What Happened?

On March 24, 2026, the New York Stock Exchange (NYSE) and Securitize, a tokenization infrastructure firm backed by BlackRock, signed a memorandum of understanding (MOU) for the development of a tokenized securities market. The core of this partnership is that Securitize has been selected as the first digital transfer agent on NYSE's blockchain-based securities market, the Digital Trading Platform, gaining the authority to issue corporate equities and ETFs directly on-chain.

Securitize's role extends beyond token issuance. As NYSE's core design partner, it will co-establish standards for tracking securities ownership and processing corporate actions on blockchain rails. Securitize Markets, the firm's broker-dealer subsidiary, will also participate as a trading participant on the platform.

The Digital Trading Platform that NYSE is building aims to fundamentally redesign the structure of traditional equity markets. The platform is designed to support 24/7 trading, instant settlement (T+0), dollar-denominated orders, and stablecoin-based funding. Its architecture combines NYSE's high-performance Pillar matching engine with a blockchain-based post-trade system, and includes multi-chain support for settlement and custody. Holders of tokenized equities will retain the same dividend and voting rights as traditional shareholders.

This announcement coincided with the House Financial Services Committee holding its first dedicated hearing on tokenization during the same week. Nasdaq had already received SEC approval on March 18 for a rule change enabling tokenized trading of Russell 1000 stocks and major index ETFs through a DTC pilot program. NYSE's Digital Trading Platform still requires SEC and FINRA approval, with a target launch by the end of 2026.

Researcher's Comment

The tokenization approach adopted by NYSE and Securitize is fundamentally different from Nasdaq's. Earlier this year in January, the SEC issued guidance on tokenized securities, classifying them into two categories: issuer-sponsored and third-party-sponsored. In the issuer-sponsored model, the issuer or transfer agent uses the blockchain as the official record of ownership, and token transfers themselves constitute changes to the issuer's shareholder registry. In the third-party-sponsored custodial model, a third party holds the underlying securities and issues tokens representing rights to those holdings.

Nasdaq's approach falls under the latter. In Nasdaq's tokenization pilot, clearing and settlement occur on T+1 through existing NSCC/DTC rails. If a buyer wants tokenized settlement, they set a tokenization flag at order entry, and DTC handles the tokenization and settlement. In other words, the existing complex infrastructure of brokers, NSCC, DTC, and transfer agents remains largely intact, with blockchain utilized only at the settlement layer. This is an incremental approach.

The NYSE-Securitize model is different. As explicitly stated on Securitize's official blog, what they are building is market structure for "issuer-sponsored tokenized securities." Issuers and transfer agents issue shares directly on-chain and manage the shareholder registry on-chain. In principle, this structure carries the potential to bypass central clearing and depository institutions such as NSCC and DTC, making it a far more radical direction than Nasdaq's path.

Practical constraints do exist. NYSE itself currently operates on DTCC infrastructure, so signing an MOU will not immediately lead to a market structure that bypasses DTCC. However, the fact that NYSE is building a separate Digital Trading Platform from the ground up, designed with instant settlement, stablecoin funding, and multi-chain settlement, signals a direction toward replacing existing clearing and settlement infrastructure.

Ultimately, Nasdaq and NYSE share the same vision: lower fees, instant settlement, 24/7 trading. But their playbooks differ. Nasdaq has already secured SEC approval through an incremental approach leveraging existing DTCC infrastructure, and has established a global distribution channel through its partnership with Kraken. NYSE chose to build a blockchain-native platform from scratch, bringing in Securitize as its design partner. Nasdaq's approach offers faster regulatory approval and lower switching costs for existing market participants, while NYSE's approach has the potential to more fully realize the structural benefits that tokenization promises: instant settlement, DTCC bypass, and programmable securities.

In the broader context, this week demonstrated that tokenized securities are moving beyond individual experiments into a structural transformation of U.S. capital markets. Nasdaq's SEC approval, the NYSE-Securitize MOU, and Congress's first dedicated tokenization hearing all occurred in the same week. With the world's two largest stock exchanges each beginning to build tokenization infrastructure in their own way, the question has shifted from "will equities be tokenized?" to "under what structure will they be tokenized?" Whether Nasdaq's incrementalism or NYSE's radicalism becomes the market standard will be a defining variable for the direction of tokenized finance over the coming years.

What Happened?

On March 24, Circle (CRCL), the stablecoin issuer, saw its stock price plunge 20% in a single day, marking its largest daily decline since its June 2025 NYSE listing. CRCL had rallied more than 170% since early February and fell to approximately $101 on the day. Coinbase (COIN) also dropped roughly 10% on the same day.

The immediate trigger was the leak of the latest draft of the CLARITY Act, the Crypto Market Structure Bill, to industry participants. According to reporting by crypto journalist Eleanor Terrett, the draft included provisions prohibiting platforms such as Coinbase and Kraken from offering interest on stablecoin holdings, whether directly or indirectly. However, it was designed to permit activity-based rewards tied to trading activity. Coinbase currently pays 3.5% interest to USDC holders, and concerns spread through the market that if the regulation materializes, the incentive to hold USDC could weaken significantly.

On the same day, Tether announced that it had signed a formal engagement with a Big Four accounting firm for its first independent financial statement audit, adding pressure on Circle. Tether had previously only published quarterly attestations through BDO Italia. This audit will be a comprehensive review of assets, liabilities, internal controls, and reporting systems for the entire $184 billion USDT reserve. Tether did not disclose the specific audit firm, though subsequent reports indicated that KPMG is conducting the audit. Tether CFO Simon McWilliams stated that the firm was selected through a competitive bid process and that Tether already operates at Big Four audit-level standards.

Circle has long maintained an advantage over Tether in terms of regulatory compliance and transparency within the stablecoin industry. However, the market's concern grew that this differentiator could weaken significantly if Tether secures a Big Four audit. One analyst commented that "if successful, this poses a structural competitive threat to Circle, which already operates on thinner margins."

Meanwhile, amid the broad sell-off, Cathie Wood's ARK Invest moved in the opposite direction. ARK purchased 161,513 shares of CRCL on March 24 across three ETFs (ARKK, ARKW, ARKF), totaling approximately $16.34 million. Circle is currently the third-largest holding in ARK's flagship fund ARKK, accounting for 5.48% of the portfolio. This purchase came just four days after ARK sold $5.9 million worth of CRCL shares on March 20, suggesting that ARK viewed the selloff as a buying opportunity.

Researcher's Comment

The CRCL selloff is an event in which the core tensions surrounding the stablecoin industry's revenue structure and regulatory framework surfaced simultaneously.

First, the market's initial reaction was likely excessive. What the CLARITY Act draft prohibits is platforms paying passive interest to users, not Circle's own reserve income. 96% of Circle's revenue comes from interest earned on the USDC backing portfolio, which is primarily composed of U.S. Treasuries. The CLARITY Act does not touch this revenue stream. As some analysts have pointed out, banning interest payments could actually remove the market pressure on Circle to share its reserve income externally. In effect, it could end up protecting Circle's revenue model through regulation.

However, the more fundamental issue lies on the demand side for USDC. The 3.5% interest reward that Coinbase offers is one of the key incentives for users to hold USDC. If this incentive disappears, users may shift from "holding" USDC to only "using" it when needed. As analyzed in a previous newsletter, stablecoin interest payments are a key catalyst for democratizing the deposit spread that banks have long monopolized. Banning them may be a short-term compromise to address banking industry concerns, but it could slow the growth of the stablecoin ecosystem in the long run.

The timing of Tether's Big Four audit announcement on the same day maximizes the pressure on Circle. Circle has maintained its differentiation through the narrative of "we are the transparent issuer with SEC registration, U.S. regulatory compliance, and regular audits." If Tether completes a Big Four audit, this differentiation is substantially neutralized. Between $184 billion in USDT and roughly $60 billion in USDC, the key question for Circle's future valuation is what competitive advantage it can claim once the transparency premium disappears.

Of course, Tether's audit may take considerable time to complete, and Tether has a track record of failing to deliver on transparency-related commitments. In 2021, it reached a settlement with the New York Attorney General's office, and in 2024, it faced a DOJ investigation over anti-money laundering violations. A significant gap remains between announcing an audit and completing one.

This event is one in which Circle's structural dilemma was laid bare all at once. The era in which regulatory compliance served as a differentiator is passing. Tether is attempting to close that gap through an audit. And platform-based interest payments, which were Circle's core growth driver, face increasing regulatory restrictions. ARK Invest deploying roughly $16 million on the day of the crash reflects a judgment that these headwinds are already overpriced in. But Circle has reached a point where it needs to present the market with a value proposition beyond "the transparent stablecoin issuer."

Crypto

Institution

White House clears review of rule that could open path for crypto in $10 trillion 401(k) market

Bipartisan lawmakers introduce PREDICT Act to bar federal officials from prediction markets

NYSE parent ICE invests another $600 million in Polymarket, expanding bet on prediction markets

Tech

Investment

Digital asset manager ParaFi raises $125 million for new venture fund: Bloomberg

Circle Ventures leads Tazapay Series B extension, bringing the round to $36 million

Stablecoin startup Payy, focused on private transactions, raises $6 million in seed funding

Asia

Ripple joins Singapore central bank initiative to test RLUSD trade settlements

Startale Group closes $63 million Series A with investments from SBI Group and Sony Innovation Fund

CRCL fell 20% yesterday after the Clarity Act draft targeted passive stablecoin yield. Same day, Tether signed a Big Four audit.

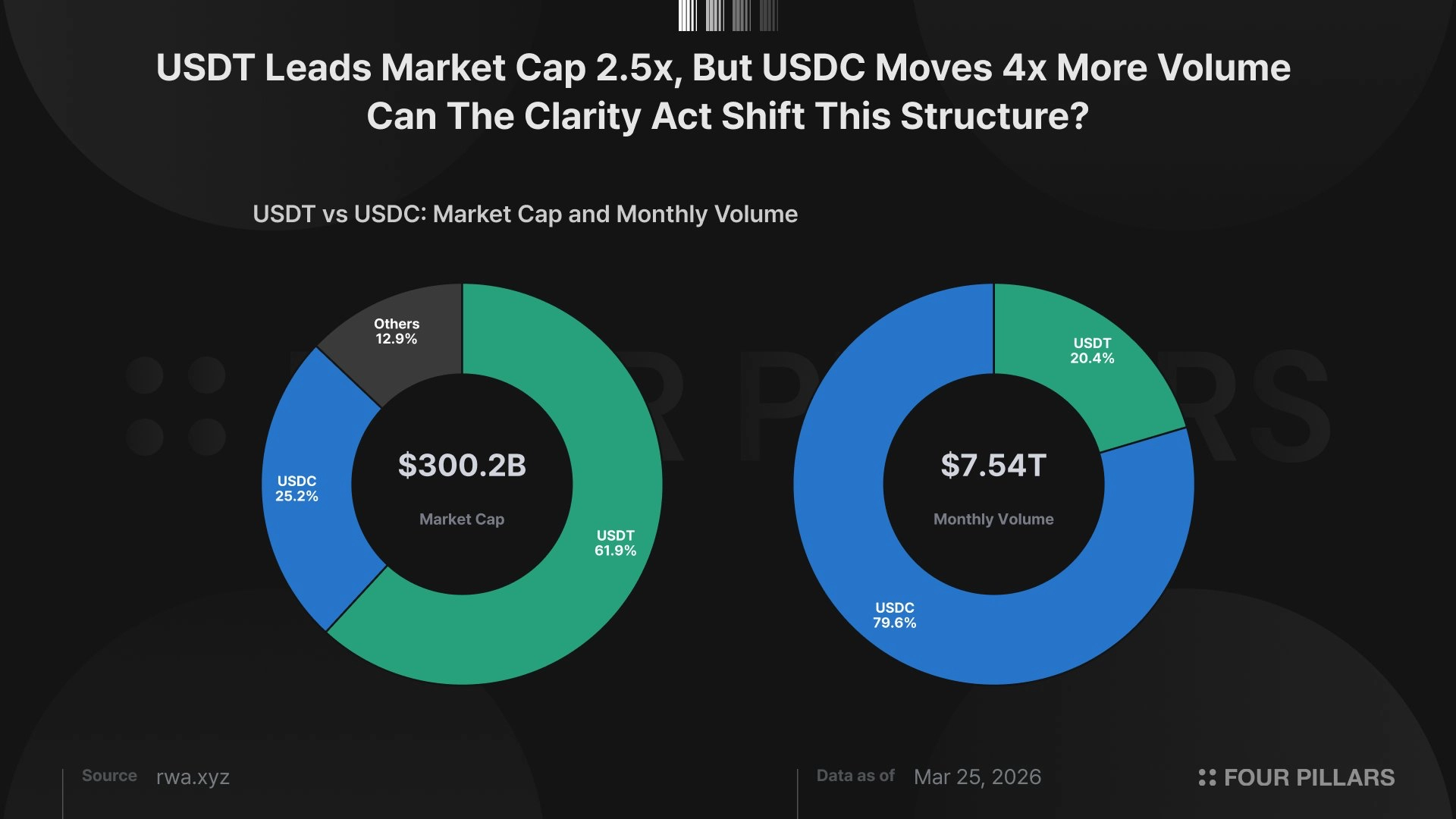

USDT holds 62% of stablecoin market cap ($185.7B) but only 19% of monthly transfer volume ($1.54T). Whereas, USDC holds 25% of market cap ($75.7B) but 81% of volume ($6T). Capital efficiency: USDC 107x/month vs USDT 10x.

Coinbase's ~4% USDC reward has likely contributed to this volume gap. The Clarity Act bans passive yield but permits "activity-based rewards," with final definitions due in 12 months. Tether meanwhile unveiled USAT (US-focused stablecoin), plans to hire 150 staff, and has Commerce Secretary Lutnick's support for US expansion.

If USDC rewards get restricted, the 4x volume advantage over USDT could narrow. Whether Coinbase's program qualifies as "activity-based" under the final rules remains the main issue.

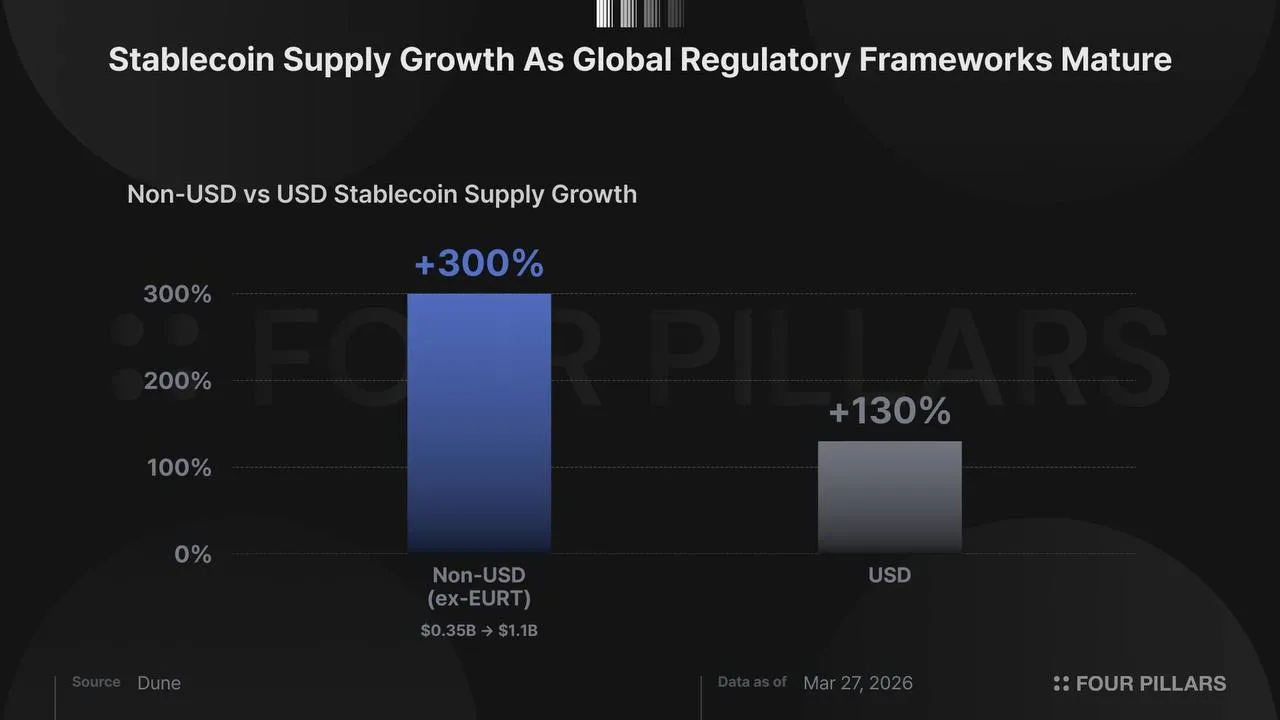

Non-USD stablecoin supply grew +300% over 3 years (ex-EURT, $0.35B to $1.1B), outpacing USD stablecoins at +130%. Per the Dune x Visa "Beyond Dollarization" report.

The EURT adjustment matters. Tether's euro stablecoin collapsed from $400M to $50M in Nov 2024 after failing MiCA compliance. Excluding it, the remaining non-USD stablecoins tripled. EURC (Circle) captured the gap, growing 138% post-MiCA license.

Supply grew 3x, but distribution grew faster. Holders: 30x (40K to 1.2M). Senders: 22x (6K to 135K). Volume: 16x ($600M to $10B monthly). Non-USD stablecoins are mainly used as operational money for payments and settlement, not DeFi yield.

Japan (JPYC, 3 mega-bank consortium), Brazil (BRL volume nearing $1B annual), Singapore (XSGD via Grab) are each scaling with local regulatory backing. Adoption appears to track regulatory maturity more closely than macro volatility.

The right capital return mechanism depends on what kind of asset your token is. Buyback, fee switch, and reinvestment are each correct for different quadrants of a liveness/revenue 2x2 matrix.

Buybacks work for tokens that compound with protocol growth; tokens that don't need committed distribution.

Fee switch signals commitment and attracts stable capital, because the yield IS the thesis.

Ethereum proves you need both axes. Maximum liveness (gas, staking, collateral) but L2s captured 95% of the economics. Liveness alone doesn’t translate to value capture.

JUP is an interesting case study because it’s actively trying to change quadrants. Zero emissions, ASR, Offerbook, Lend, prediction markets are all liveness-building moves.

Despite being known as cash-dependent, Japan went from 13% to over 42% cashless in a decade. Stablecoins are next, backed by a comprehensive legal framework enacted in 2023, which was ahead of most major economies.

Japan's three megabanks are building stablecoin infrastructure through Progmat, JPYC launched the first legally recognized yen stablecoin in 2025, and SBI Holdings plans to launch its own L1 aimed at institutional trading.

Stablecoins represent a shift from institutional trust (banks) to programmable trust - money that settles instantly, runs 24/7, and integrates with smart contracts and tokenized assets.

MoneyX is the convergence point. Produced by SBI, JPYC, Progmat, and CoinPost, the conference unites megabank executives, regulators, and builders to align Japan's stablecoin strategy amid global competition from the US, EU, and Asia.

Japan is building regulated stablecoin infrastructure at scale. The three megabanks, MUFG, SMBC, and Mizuho, are collaborating on a shared issuance platform targeting ¥1 trillion in stablecoins by 2028. Circle's USDC became the first foreign stablecoin approved for Japanese exchanges. A Tokyo startup beat the banks to market with the country's first licensed yen stablecoin. And a parallel system of tokenized bank deposits is already live, settling environmental certificates and preparing to handle security token trades.

This article maps the infrastructure taking shape. Part 1 covers the regulatory foundation: the 2023 stablecoin framework that defines who can issue, how reserves must be held, and what licenses intermediaries need. plus the security token rules enabling ¥168 billion in tokenized assets.

Part 2 examines the key initiatives: the megabank consortium and its cross-border settlement projects, SBI Holdings' multi-pronged distribution strategy spanning USDC, RLUSD, and a forthcoming yen stablecoin, the securities firms building tokenization platforms, JPYC's journey from prepaid workaround to regulated issuer, and DCJPY's tokenized deposit network now onboarding Japan Post Bank's 120 million account holders.

In March 2026, Mastercard acquired stablecoin infrastructure company BVNK for up to $1.8B. This is the largest stablecoin infrastructure M&A deal to date, surpassing Stripe's $1.1B acquisition of Bridge.

In 2025, stablecoin transfer volume reached $33T, roughly twice Visa's annual processing volume ($16.7T). While most of this is still trading settlement, cross-border remittances and B2B payments are expanding at a CAGR of 72%. Traditional card networks find their rationale for entering crypto in the need to absorb this payment flow.

Mastercard's crypto business is unfolding across three axes that cover the full spectrum of payment flows. First, it leverages its existing network of 150M merchant locations as a touchpoint for stablecoin payments through crypto wallet-linked cards. Second, it is building tokenized deposit settlement infrastructure for banks and institutions through its proprietary permissioned blockchain, Multi-Token Network (MTN). Third, through the BVNK acquisition, it secures public blockchain-based commercial payment infrastructure (stablecoin-to-fiat conversion, cross-border payouts, enterprise wallets).

The BVNK acquisition cannot be explained by technology alone. This deal brought in a license network spanning 130 countries, fiat banking partnerships, and an already-validated enterprise client base (Worldpay, Deel, Flywire, etc.) all at once. It shows that in the stablecoin infrastructure market, the moat is formed not only by the technology stack but also by the bundle of country-specific licenses and compliance.

SDEV’s $134M capital raise decomposes to $76M in external capital, 943.6M SKY from the Foundation, and roughly 30% of typical governance polling turnout.

Sky runs a $12.57B lending business that flipped positive. Annualizing the two-month run rate gives ~$166M in earnings (~10x P/E), normalizing over six months gives ~$110M (~15x P/E).

Governance cut the buyback by 87.5%, emissions by 16.2%, and SSR by 25bp in three weeks. The same actions that narrowed the pipe to tokenholders accelerated surplus accumulation by ~$96M per year.

The math for SKY stakers and non-stakers diverges.

Lido's Community Staking Module (CSM) has spent the past 1.5 years since its 2024 launch proving that permissionless staking can work at scale. CSM currently accounts for roughly 7.5% of Lido's total stake, meaningfully contributing to the decentralization of Ethereum's validator set.

CSM v3, proposed through LIP-33, introduces native support for the 0x02 validators at the heart of Ethereum's Pectra upgrade. It adopts a dual-instance architecture, deploying a new instance separate from the existing one. This allows permissionless participation to grow beyond 15% while keeping the total validator count at or below current levels.

The CSM v3 codebase also serves as the foundation for Curated Module v2 (CM v2), which manages approximately 90% of Lido's total stake. A module that began as a permissionless experiment has come to define the architecture of the entire protocol, marking a notable turning point in Lido's approach to module design.

Circle trades at 44x trailing EBITDA on a business that earns 96% of its revenue from interest rates. The sell-side has a 3x spread on price targets ($60 to $235) which I think reflects category confusion.

Coinbase receives 51% of Circle’s gross revenue under an agreement Circle cannot exit unilaterally. Faster supply growth makes the revenue mix more rate-concentrated, which is the opposite of what a platform re-rating requires.

The products the bull case needs generated 4% of revenue in FY25, guided to 6% in FY26. CPN and Arc look like important strategic defense but defense doesn’t earn a platform multiple.

At $98 as of Mar 26, three things have to happen simultaneously: supply grows, rates hold, and the market grants a VISA/Mastercard tier multiple despite 96% rate concentration.

Dive into 'Narratives' that will be important in the next year