Japan is building regulated stablecoin infrastructure at scale. The three megabanks, MUFG, SMBC, and Mizuho, are collaborating on a shared issuance platform targeting ¥1 trillion in stablecoins by 2028. Circle's USDC became the first foreign stablecoin approved for Japanese exchanges. A Tokyo startup beat the banks to market with the country's first licensed yen stablecoin. And a parallel system of tokenized bank deposits is already live, settling environmental certificates and preparing to handle security token trades.

This report maps the infrastructure taking shape. Part 1 covers the regulatory foundation: the 2023 stablecoin framework that defines who can issue, how reserves must be held, and what licenses intermediaries need. plus the security token rules enabling ¥168 billion in tokenized assets. Part 2 examines the key initiatives: the megabank consortium and its cross-border settlement projects, SBI Holdings' multi-pronged distribution strategy spanning USDC, RLUSD, and a forthcoming yen stablecoin, the securities firms building tokenization platforms, JPYC's journey from prepaid workaround to regulated issuer, and DCJPY's tokenized deposit network now onboarding Japan Post Bank's 120 million account holders.

The thesis emerging from these initiatives: stablecoins and tokenized deposits as financial infrastructure, not speculative assets. Japan is testing multiple approaches simultaneously, trust-issued stablecoins, bank-issued stablecoins, and tokenized deposits .letting the market determine which settlement layer prevails for different use cases.

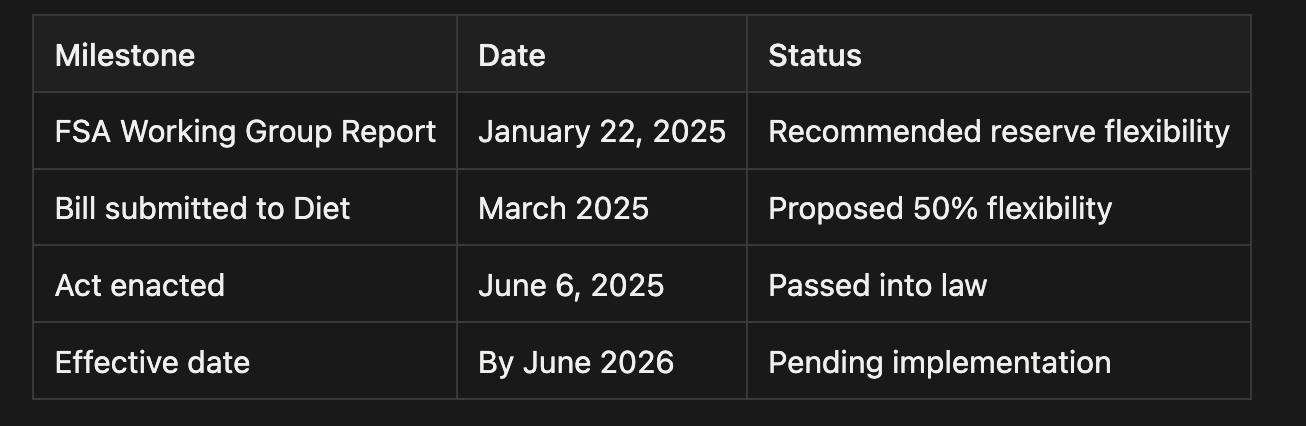

Japan became one of the first major economies to implement comprehensive stablecoin regulations when the revised Payment Services Act (PSA) took effect in June 2023. The legislation established clear rules for stablecoin issuance, intermediation, and foreign stablecoin entry.

Classification and Scope

Under Japanese law, stablecoins are classified as "Electronic Payment Instruments" (EPI), digital assets denominated in fiat currency and redeemable at face value. The framework distinguishes between two types:

Digital money-like type: Backed by fiat currency at 1:1 (e.g., USDC, yen stablecoins). Regulated as EPI under the PSA.

Crypto-asset type: Value maintained algorithmically or by crypto collateral (e.g., DAI). Falls outside the EPI framework; classified as crypto assets.

Only fiat-backed stablecoins have clear issuance and intermediation pathways under current regulation. Despite being legally permissible as crypto assets, no algorithmic or crypto-backed stablecoins are currently listed on registered Japanese exchanges.

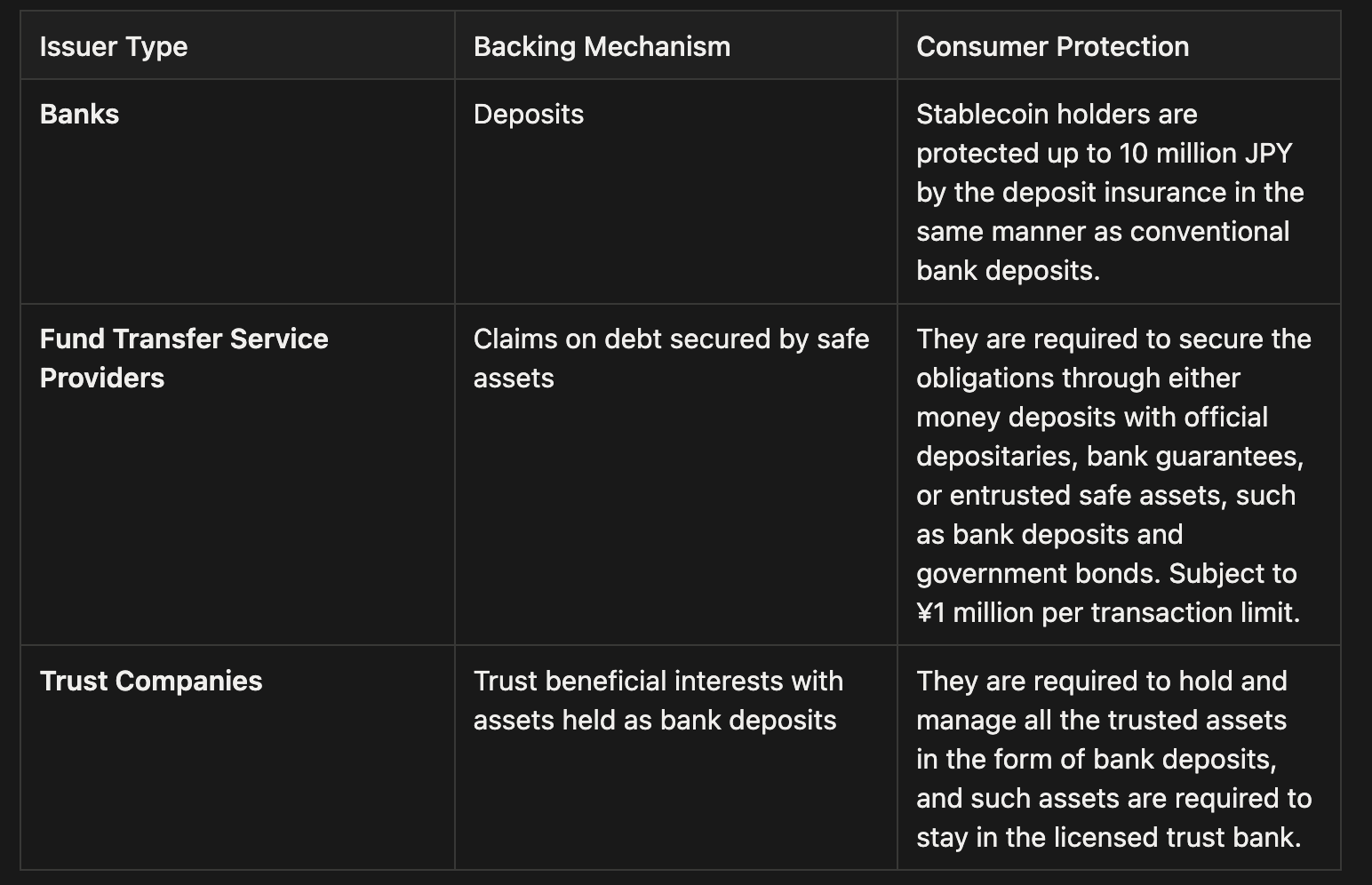

Who Can Issue

Stablecoin issuance is restricted to three types of licensed institutions:

Reserve Requirements for Trust-Type Stablecoins

When the Electronic Payment Instruments (EPI) framework took effect in June 2023, trust-type stablecoin issuers were required to hold 100% of backing assets in demand deposits. This conservative approach prioritized redemption liquidity but limited issuer profitability and competitiveness compared to global peers.

With the PSA Amendment Act in 2025, trust-type stablecoin issuers can invest up to 50% of backing assets in low-risk instruments:

Japanese Government Bonds (JGBs) with remaining maturity ≤3 months

US Treasury securities with remaining maturity ≤3 months (for USD-denominated stablecoins)

Early-cancellable term deposits (JPY or USD denominated)

If government bond prices fall due to market conditions, issuers are required to contribute additional trust funds to ensure full redemption at par value. Japanese stablecoins must also be non-interest bearing to holders. Issuers retain yield generated from reserve assets but cannot distribute it to token holders.

Intermediary Licensing for Stablecoins

Japan's June 2023 Payment Services Act (PSA) amendments established a comprehensive licensing framework for entities that intermediate stablecoins. The framework distinguishes between full-service intermediaries requiring EPISP registration and a new lighter intermediary category (ECISB) introduced in 2025 for entities operating on behalf of licensed providers.

Electronic Payment Instrument Service Provider (EPISP)

To conduct stablecoin-related business in Japan, entities must obtain a stablecoin-related license by registering as an Electronic Payment Instrument Service Provider (EPISP). This requirement was introduced in the June 2023 revision of the PSA. In October 2024, JVCEA was certified by the FSA as the self-regulatory organization for EPISPs.

Business operators who engage in the business of buying, selling or exchanging EPIs (as well as in the intermediation of such activities), or in the management of EPIs for the benefit of others, are required to undergo registration as an EPISP.

Entities with a CAESP license that want to trade stablecoins will also need to apply to the FSA for a separate EPISP license. This means crypto exchanges must obtain dual registration (CAESP + EPISP) to offer both crypto assets and stablecoins. For example, SBI VC Trade, a cryptocurrency exchange subsidiary of Japan's SBI Holdings, became the first Japanese firm to be licensed as an EPISP. The license is required to handle offshore stablecoins such as Circle's USDC.

Foreign-issued stablecoins can enter Japan through licensed EPISPs that have entered into contracts with the issuer. This is how USDC became available in Japan. Circle partnered with SBI VC Trade, which obtained EPISP registration and signed an issuer contract with Circle.

Electronic Payment Instrument and Crypto-Asset Intermediary Service Business (ECISB)

On 6 June 2025, the Act to Partially Amend the Payment Services Act (PSA Amendment Act 2025) was enacted, which will come into force by June 2026. This will introduce a new regulatory framework for intermediaries acting solely for the benefit of another EPISP or CAESP by which they are retained.

An ECISB is an intermediary that connects customers to a licensed exchange. The ECISB helps facilitate the transaction, but the licensed exchange actually executes the trade and is responsible for regulatory compliance. Some potential examples are crypto affiliate/referral websites, fintech apps with crypto features, or financial advisors/brokers.

An ECISB must register with the JFSA as an Electronic Payment Instrument and Crypto-asset Intermediary Service Business Operator (ECISBO). Because ECISBOs do not accept deposits of users' property, they are not subject to financial requirements. AML/CFT obligations are handled by the principal EPISP/CAESP. ECISBOs must be affiliated with an EPISP or a CAESP, and the entrusting EPISP/CAESP is liable for any damages that the entrusted ECISBO causes to a user in connection with intermediation.

Japan established its security token framework through amendments to the Financial Instruments and Exchange Act (FIEA) passed in May 2019 and effective May 2020, making it one of the first major economies to create clear regulations for tokenized securities. Subsequent amendments in 2024 expanded the framework to cover real estate tokens, while regulatory relaxations have made it easier to launch trading venues.

Classification and Scope

Japan classifies securities into two tiers based on liquidity:

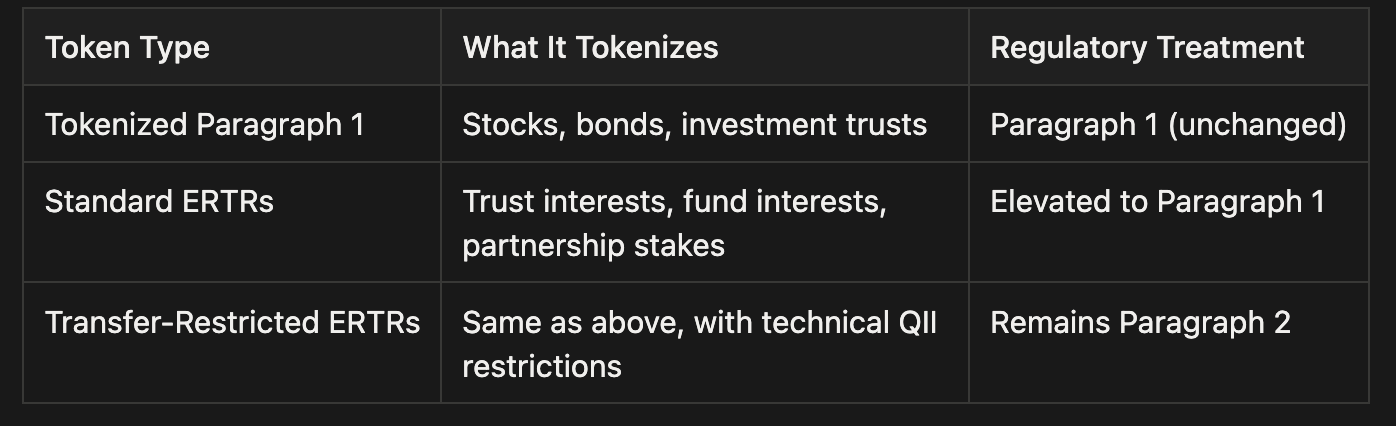

Paragraph 1 Securities: Highly liquid instruments such as stocks, corporate bonds, government bonds, and investment trust units. Subject to stricter disclosure requirements, prospectus obligations, and licensing rules.

Paragraph 2 Securities: Less liquid instruments including trust beneficiary interests, collective investment scheme interests, and partnership interests. Subject to lighter regulatory requirements due to limited transferability.

When securities are tokenized, the FIEA treats them as "Electronically Recorded Transferable Rights" (ERTRs), which are rights recorded and transferred using blockchain or distributed ledger technology.

The Elevation Problem

Tokenizing a Paragraph 1 security is straightforward: the token inherits Paragraph 1 treatment. But tokenizing a Paragraph 2 security creates a regulatory complication. Because blockchain makes these otherwise illiquid instruments easily transferable, the FIEA elevates them to Paragraph 1 treatment, triggering the full suite of disclosure and licensing requirements.

Issuers can avoid this elevation only by implementing technical transfer restrictions that limit circulation to qualified institutional investors. Without such restrictions, even a simple fund interest becomes subject to prospectus requirements and can only be distributed by Type I licensed operators.

Real Estate Tokens Join the FIEA Framework

Prior to November 2024, tokenized real estate fund interests occupied a regulatory gray zone. They were governed by the Act on Specified Joint Real Estate Ventures (ASJREV) but sat outside the FIEA's security token framework.

This changed with amendments that took effect November 1, 2024. Real estate security tokens are now classified as "rights representing electronically recorded transferable securities" under the FIEA. Operators of tokenized real estate funds must comply with both statutes: ASJREV for the underlying real estate operations and FIEA for the token distribution. Self-offerings and private placements now require Type II Financial Instruments Business registration.

Licensing Requirements

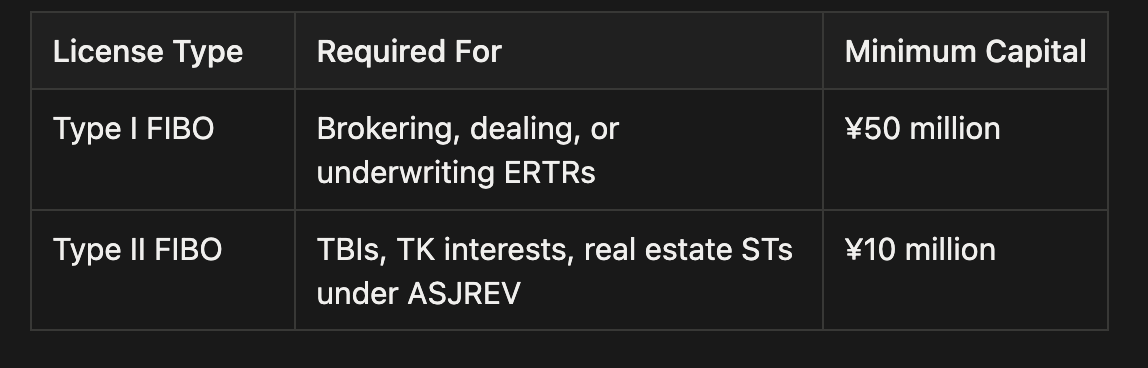

Handling security tokens requires registration as a Financial Instruments Business Operator under the FIEA. The license type depends on the nature of the tokens and the activities performed.

Type I FIBO is the same license category required for traditional securities firms. It covers brokering, dealing, and underwriting ERTRs, whether tokenized Paragraph 1 securities or elevated Paragraph 2 securities. The ¥50 million capital requirement is deliberately high, ensuring only established, well-capitalized institutions participate. Major securities companies such as SBI Securities, Nomura Securities, and Daiwa Securities hold Type I licenses and can handle security tokens.

Type II FIBO covers handling of trust beneficiary interests (TBIs), tokumei kumiai (TK) silent partnership interests, and real estate security tokens under the ASJREV structure. The ¥10 million capital requirement reflects the narrower scope. Operators dealing with real estate-related tokens must also demonstrate personnel with professional knowledge in real estate and establish appropriate compliance systems.

Trust Beneficiary Interests (TBIs): Rights held by beneficiaries of a trust arrangement. In Japanese real estate securitization, property is typically placed into a trust with a trust bank, and investors receive beneficial interests entitling them to distributions from rental income or sale proceeds.

Tokumei Kumiai (TK): A Japanese "silent partnership" where an investor contributes capital to an operator's business in exchange for a share of profits. Unlike a standard partnership, the TK investor remains undisclosed to third parties and the operator conducts business in its own name.

Recent Regulatory Relaxations

Two developments in late 2024 and early 2025 have lowered barriers for market participants.

First, amendments effective November 21, 2024 allow Type I FIBOs to operate trading platforms for certain security tokens without obtaining full Proprietary Trading System (PTS) authorization, provided trading volumes remain within specified thresholds. Previously, launching a secondary market for security tokens required the same authorization as operating a full-scale alternative trading system.

Second, a new Simplified Type I FIBO registration category takes effect in May 2025. This provides a lower-barrier option for smaller firms seeking to participate in security token distribution with limited scope. The license is designed primarily for foreign asset managers distributing unlisted fund products to Japanese institutional investors, and restricts marketing to qualified institutional investors only.

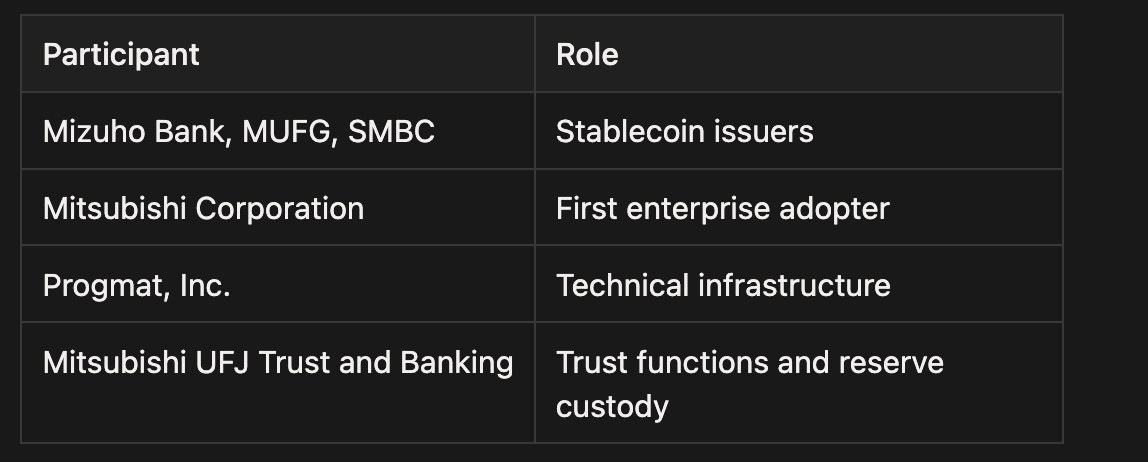

Japan's three largest banks, MUFG, SMBC, and Mizuho, are building shared stablecoin infrastructure designed to become the foundation for next-generation payment systems. The initiative combines regulatory backing, a purpose-built issuance platform, and enterprise adoption at global scale.

On November 7, 2025, the FSA announced its support for a proof-of-concept involving all three megabanks. The initiative falls under the newly established Payment Innovation Project (PIP), housed within the FSA's FinTech Proof-of-Concept Hub that has operated since 2017. This represents the first project under PIP and the eleventh overall under the FinTech PoC Hub, a signal that regulators view bank-issued stablecoins as ready for production testing rather than mere experimentation.

Pilot testing began in November 2025, with a full commercial launch targeted for March 2026. The scale is substantial:

Issuance volume: ¥1 trillion (~$6.6 billion) over three years

Corporate clients: 300,000+ across the combined megabank customer base

Supported blockchains: Ethereum, Polygon, Avalanche, Cosmos

Currency support: JPY at launch; USD planned for late 2026

Mitsubishi Corporation, Japan's largest trading company with over 240 subsidiaries worldwide, will serve as the proof case. It currently routes inter-subsidiary transfers through conventional banking rails, a process involving multiple correspondent banks, business-hour constraints, and significant FX costs. Target use cases include dividend distributions, acquisition settlements, and routine inter-company transactions. Stablecoin-based settlement offers instant finality and 24/7 availability.

Progmat: The Infrastructure Layer

At the center of this initiative is Progmat, MUFG's token issuance platform. Originally launched in February 2022, Progmat was restructured as a joint venture in October 2023 when Japan's major financial institutions formalized its role as national digital asset infrastructure.

Progmat Coin uses a trust-based issuance model that provides bankruptcy-remote protection:

A financial institution deposits fiat currency with MUFG Trust Bank

Progmat issues equivalent stablecoins on public blockchains

Reserve assets remain ringfenced within the trust structure

Monthly third-party audits ensure transparency

Critically, non-bank issuers can use this trust pathway without obtaining separate licenses, lowering barriers for corporates and fintechs that want to issue stablecoins without becoming banks.

The core platform runs on R3 Corda for internal coordination and settlement finality. Public blockchain deployment uses partnerships with Datachain. This architecture enables stablecoins issued on one chain to move seamlessly across ecosystems. In September 2023, Binance Japan signed an agreement with MUFG to act as both entrustor and intermediary for Progmat stablecoins, positioning the world's largest crypto exchange as a distribution channel within Japan's regulated framework.

SMBC's Parallel Track

While participating in the joint megabank project through Progmat, SMBC is simultaneously developing its own stablecoin on a separate technology stack. In April 2025, SMBC signed an MoU with Ava Labs, Fireblocks, and Japanese IT company TIS to explore stablecoin commercialization. Pilot testing is scheduled for Q4 2025 or Q1 2026, with commercial launch targeted for 2026 if trials succeed.

SMBC's approach signals that even within a cooperative megabank framework, individual institutions are hedging by maintaining independent technology options. The result is not fragmentation but redundancy, multiple paths to the same destination.

Project Pax: Cross-Border Payments

In September 2024, the three megabanks launched Project Pax, a cross-border payment platform developed jointly by Progmat, Datachain, and TOKI. The project targets the $182 trillion cross-border transfer market with a design principle called "rails abstraction", clients send standard SWIFT payment instructions while settlement happens on-chain invisibly in stablecoins (JPY, USD, or EUR).

The client never touches the stablecoin directly; they see only familiar SWIFT messaging and bank statements. More than ten domestic and international banks are participating in the prototype phase. By integrating with existing SWIFT infrastructure rather than replacing it, Project Pax lowers the barrier for banks that have already invested billions in correspondent banking relationships.

Atomic Settlement for Capital Markets

Beyond payments, Japan's institutions are building infrastructure for capital markets settlement. The problem is timing mismatch. When security tokens trade on Japan's secondary market today, the token transfer occurs instantly on-chain, but fund settlement happens separately via bank transfer, typically T+2 or longer. This separation creates:

Counterparty risk: One party may fail to deliver after the other has performed

Settlement delays: Days rather than seconds

Administrative burden: Manual reconciliation between blockchain and bank records

Project Trinity announced August 2025 uses stablecoins for Delivery versus Payment (DvP) settlement. Participants include SMBC (stablecoin issuer), Daiwa Securities, SBI Securities, Osaka Digital Exchange, BOOSTRY, Progmat, and Datachain/TOKI. The core technical challenge is blockchain fragmentation, SMBC's stablecoin on Avalanche, BOOSTRY's tokens on Quorum, Progmat's on Corda, solved via Datachain's IBC protocol for cross-chain atomic swaps.

The DCJPY pilot announced December 2025 tests the same atomic DvP concept using tokenized bank deposits rather than stablecoins. Participants include SBI Securities, Daiwa Securities, SBI Shinsei Bank, and DeCurret DCP. By running both pilots simultaneously, Japan allows the market to determine which settlement asset prevails for capital markets infrastructure.

Captive Demand

The ¥1 trillion target looks achievable, not because the technology is revolutionary, but because captive demand exists. Mitsubishi Corporation alone routes billions through its 240+ subsidiaries. If the pilot demonstrates even modest savings on FX and settlement timing, other trading companies will follow. The megabanks don't need to win new customers; they need existing ones to adopt new rails.

Project Pax is the wilder bet. Abstracting stablecoin settlement behind SWIFT messaging is clever, but it also means competing on pure cost against correspondent banking relationships that have worked (expensively) for decades. The real test is whether "invisible" blockchain settlement can deliver enough margin improvement to justify the integration effort.

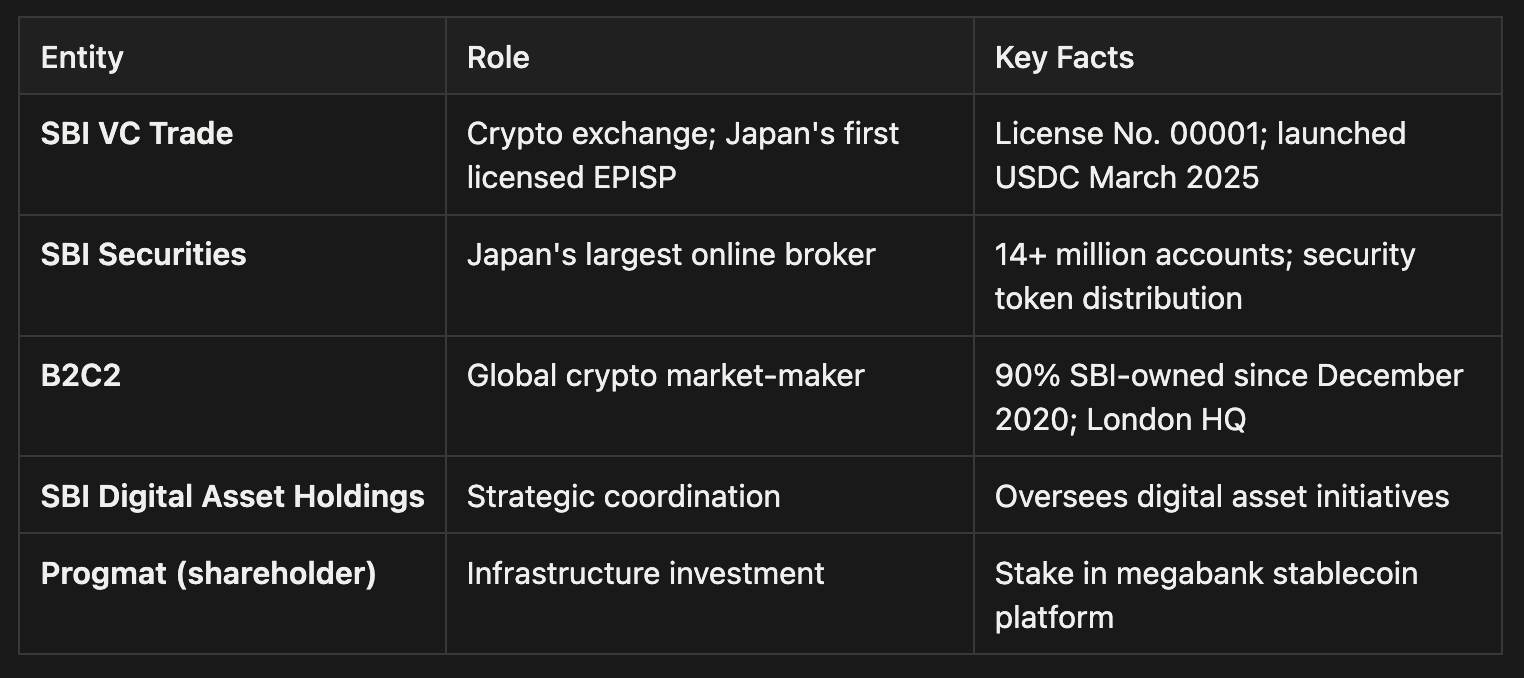

While the megabanks focus on stablecoin issuance, SBI Holdings has positioned itself as Japan's primary distribution channel for both foreign and domestic stablecoins. The conglomerate operates across the entire digital asset value chain, from exchange services to market-making to tokenized asset platforms, making it the natural gateway for stablecoin adoption in Japan.

The SBI Ecosystem

SBI's digital asset strategy spans multiple subsidiaries, each serving a distinct function in the stablecoin value chain:

This integrated structure allows SBI to capture value across issuance, trading, custody, and settlement. a strategic moat that pure-play crypto firms cannot easily replicate.

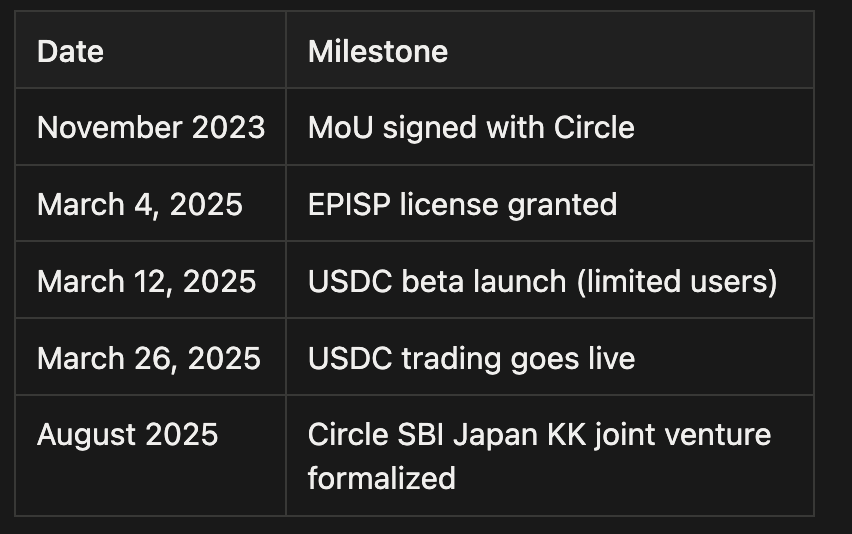

Japan's First Stablecoin License

On March 4, 2025, SBI VC Trade became the first company in Japan to register as an Electronic Payment Instruments Exchange Service Provider (EPISP), License No. 00001 from the Kanto Regional Financial Bureau. This license, created under the 2023 amendments to the Payment Services Act, authorizes handling of foreign stablecoins in Japan.

SBI VC Trade now holds three licenses enabling its full-stack crypto services:

Electronic Payment Instruments Business (License No. 00001): stablecoin trading

Crypto Asset Exchange Business (License No. 00011): cryptocurrency trading

Type 1 Financial Instruments Business (No. 3247): securities services

The EPISP license makes SBI the gatekeeper for any foreign stablecoin seeking Japanese market access.

Circle Partnership and USDC

The Circle partnership began with an MoU in November 2023 and accelerated through 2025.

SBI Holdings and Circle established Circle SBI Japan KK as a joint venture aimed at:

Developing digital financial services using USDC

Enhancing USDC's role in cross-border payments

Integrating stablecoins into Web3 ecosystems

To cement the strategic alignment, SBI Holdings and SBI Shinsei Bank jointly invested $50 million ($25 million each) in Circle's March 2025 NYSE IPO. This investment stake gives SBI ongoing influence over Circle's strategic direction.

Retail Payment Pilot

On December 25, 2025, SBI VC Trade and APLUS (an SBI consumer finance subsidiary) announced a proof-of-concept for in-store stablecoin payments launching in spring 2026. The initiative aims to capture demand from international visitors while advancing the "International Financial City OSAKA" project championed by local governments.

The pilot leverages digital wallet infrastructure developed during the Osaka-Kansai Expo 2025. The settlement workflow insulates merchants from crypto complexity:

Customer holding USDC in private wallet (e.g., MetaMask) scans merchant QR code

SBI VC Trade intercepts the transaction and converts USDC to yen

APLUS receives yen from SBI VC Trade

APLUS settles with retailer in local currency

This structure allows merchants to accept stablecoin payments without handling digital assets directly or bearing foreign exchange risk. International tourists pay with existing crypto holdings; retailers receive yen through familiar settlement channels.

Ripple Partnership and RLUSD

SBI's stablecoin strategy extends beyond Circle. The company has maintained a strategic partnership with Ripple since 2016, when SBI became one of Ripple's earliest institutional investors. Japan accounts for more than half of Ripple's global On-Demand Liquidity (ODL) volume, making it Ripple's most important market. On August 22, 2025, SBI and Ripple signed an MoU for RLUSD distribution in Japan.

The dual partnership reflects SBI's "bet on everything" approach. RLUSD offers a second dollar stablecoin option backed by US dollar deposits, short-term government bonds, and cash equivalents, with monthly third-party attestations, similar to USDC's reserve structure.

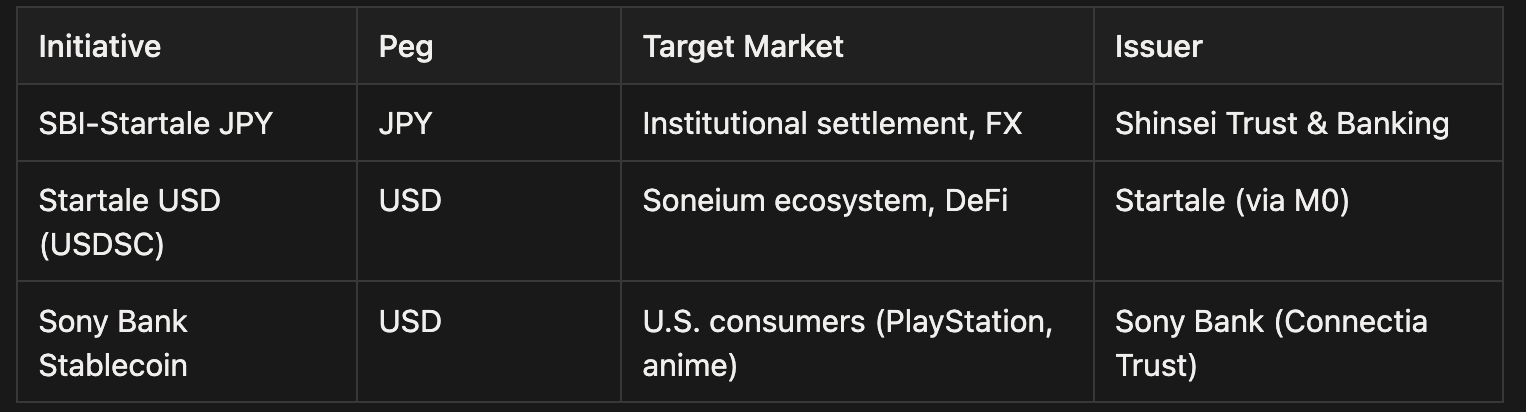

SBI-Startale & Sony: The Soneium Ecosystem

On August 22, 2025, SBI Holdings and Startale Group announced a joint venture to build an on-chain trading platform for tokenized stocks and real-world assets. On December 16, 2025, they followed up with an MoU for a yen-denominated stablecoin launching in Q2 2026.

Startale operates Astar Network, Japan's largest public blockchain, and co-develops Soneium, an Ethereum Layer-2 network created through a joint venture with Sony Group Corporation. The Soneium ecosystem is building a multi-currency stablecoin stack:

The SBI-Startale JPY stablecoin uses a trust-based structure as a "Type 3 Electronic Payment Instrument," exempting it from the ¥1 million limit on domestic remittances. This makes it suitable for institutional and wholesale use cases. USDSC launched December 3, 2025 as Soneium's native dollar stablecoin. Sony Bank is separately pursuing a U.S. dollar stablecoin for PlayStation purchases and anime subscriptions, applying for a U.S. national trust charter through Connectia Trust in October 2025.

The Toll Collector

SBI's strategy is less about picking winners than positioning to profit from whoever wins. USDC, RLUSD, the Startale yen stablecoin, SBI distributes all of them. B2C2 provides liquidity. SBI Securities offers the brokerage accounts. The conglomerate structure that looks sprawling is actually a moat: no pure-play crypto firm can replicate it.

The Osaka retail pilot will reveal whether stablecoin payments have genuine consumer demand or remain a solution looking for a problem. Expo 2025 provides ideal conditions, international visitors, digital wallet infrastructure already deployed, merchants willing to experiment. If adoption disappoints even in this setting, the retail thesis needs revisiting.

Stablecoins enable programmable money; security tokens enable programmable assets. Japan's securities firms are building the infrastructure to issue, distribute, and trade tokenized securities, with stablecoins as the intended settlement layer.

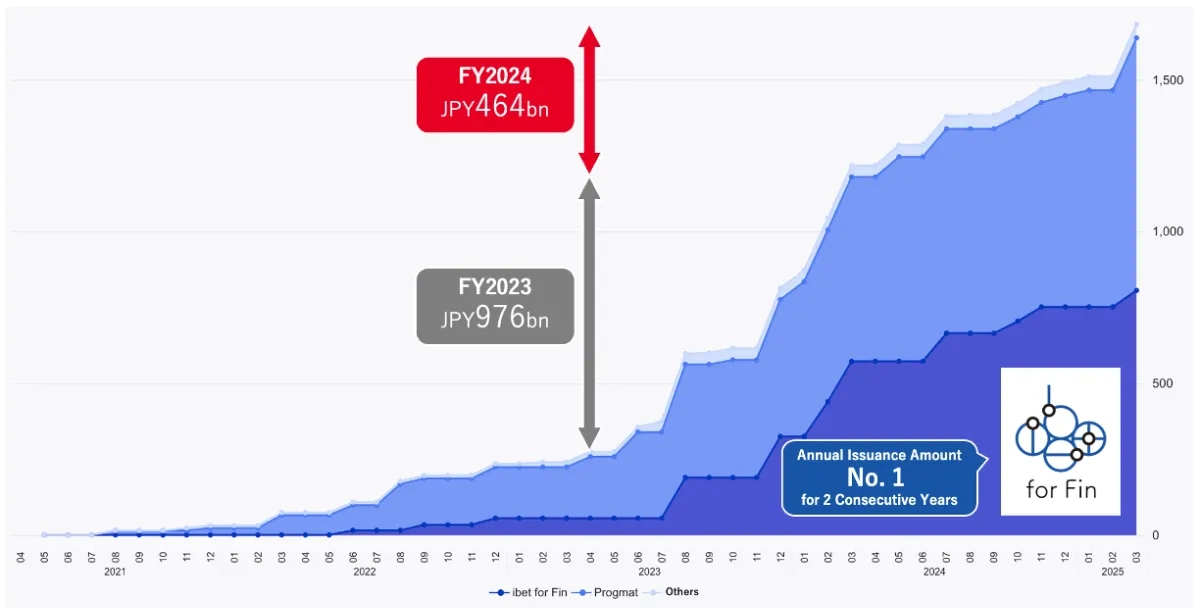

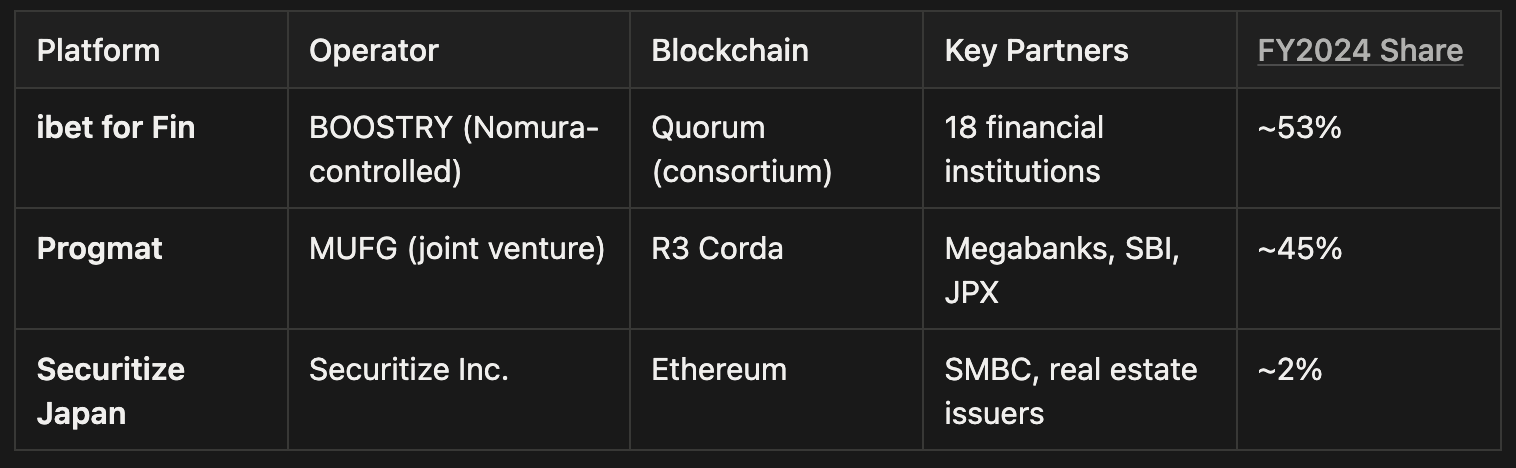

By the end of FY2024, cumulative public security token offerings reached ¥168.2 billion (~$1.1 billion), with real estate dominating issuance. FY2024 issuance totaled ¥46.4 billion, about 47% of the prior year's ¥97.6 billion, as many financial institutions paused offerings to assess the operational impact of tax reforms affecting beneficiary certificate trusts. With December 2024's tax reform proposals providing clarity, the issuance is expected to accelerate significantly in FY2025.

Issuance Platforms

Japan Security Token Market Report (FY2024)

Two platforms dominate Japan's security token issuance market, each backed by competing megabank ecosystems:

ibet for Fin operates as Japan's only consortium-type security token network, jointly governed by 18 major financial institutions including Nomura, SMBC, Mizuho Trust, and SBI Securities. As of April 2024, the platform handles beneficiary certificate trusts and corporate bonds, with BOOSTRY serving as secretariat.

Progmat focuses on trust beneficiary interests and has expanded into stablecoin issuance (Progmat Coin). Its shareholder structure, encompassing all three megabanks, JPX, and SBI, positions it as national infrastructure.

Securitize Japan brings the global Securitize platform to Japan, partnering with SMBC for real estate and credit card receivables tokenization. In 2025, Securitize released new features aimed at improving investor experience and streamlining issuer operations.

Secondary Markets

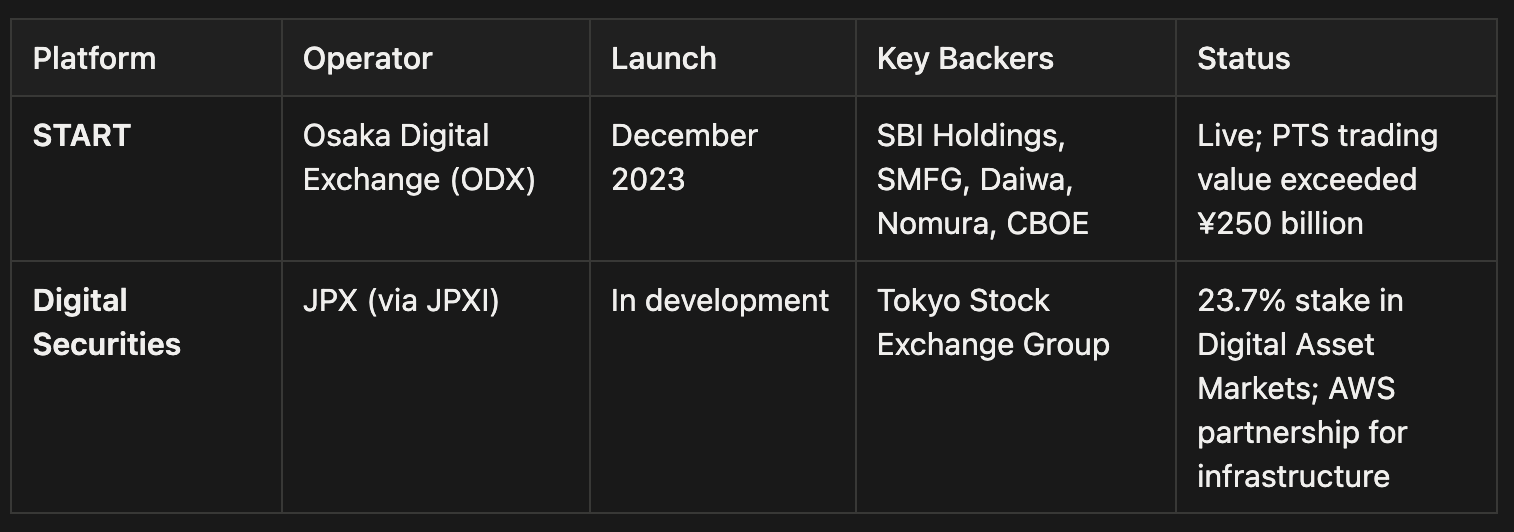

The Osaka Digital Exchange (ODX) launched START, Japan's first proprietary trading system (PTS) for security tokens, on December 25, 2023. Founded by SBI Holdings and SMFG, with backing from Daiwa Securities, Nomura, and CBOE, ODX received FSA approval on November 16, 2023. The platform launched with two real estate tokens: Kenedix Realty Token and Ichigo Residence Token.

Japan Exchange Group (JPX), operator of the Tokyo Stock Exchange, is also positioning digital securities as a growth area through its subsidiary JPX Market Innovation & Research (JPXI). JPX holds a 23.7% stake in Digital Asset Markets (DAM), the sole distributor of Zipangcoin (a gold-backed token from Mitsui & Co). Its Medium-Term Management Plan 2027 designates digital assets infrastructure as a revenue diversification priority.

The Stablecoin-Security Token Connection

Security tokens become significantly more useful when paired with stablecoins for settlement. Currently, when tokens trade on ODX, the token transfer occurs on-chain but fund settlement happens separately via bank transfer (typically T+2). This separation creates counterparty risk and administrative burden.

The megabank initiatives covered in Section 2.1, particularly Project Trinity and the DCJPY pilot, aim to solve this through atomic DVP settlement: the security token and payment move simultaneously in a single transaction. If one leg fails, both fail. As this infrastructure matures through 2026, security token markets will gain a native on-chain settlement layer, enabling true 24/7 trading with instant finality.

Waiting for DVP

The FY2024 slowdown was a pause, not a reversal. Tax reform uncertainty froze issuance decisions; with December 2024 reforms providing clarity, the pipeline should reopen. Real estate tokens dominate today, but corporate bonds are the larger opportunity, Japan's bond market dwarfs its real estate securitization market.

Everything hinges on atomic DVP. Security tokens that settle T+2 via bank transfer are only marginally better than traditional securities. Security tokens with instant on-chain settlement against stablecoins or DCJPY are genuinely different infrastructure. The 2026 pilots will determine which version of the market emerges.

While megabanks build institutional infrastructure and SBI assembles distribution networks, a Tokyo-based startup has quietly captured a different position: first mover.

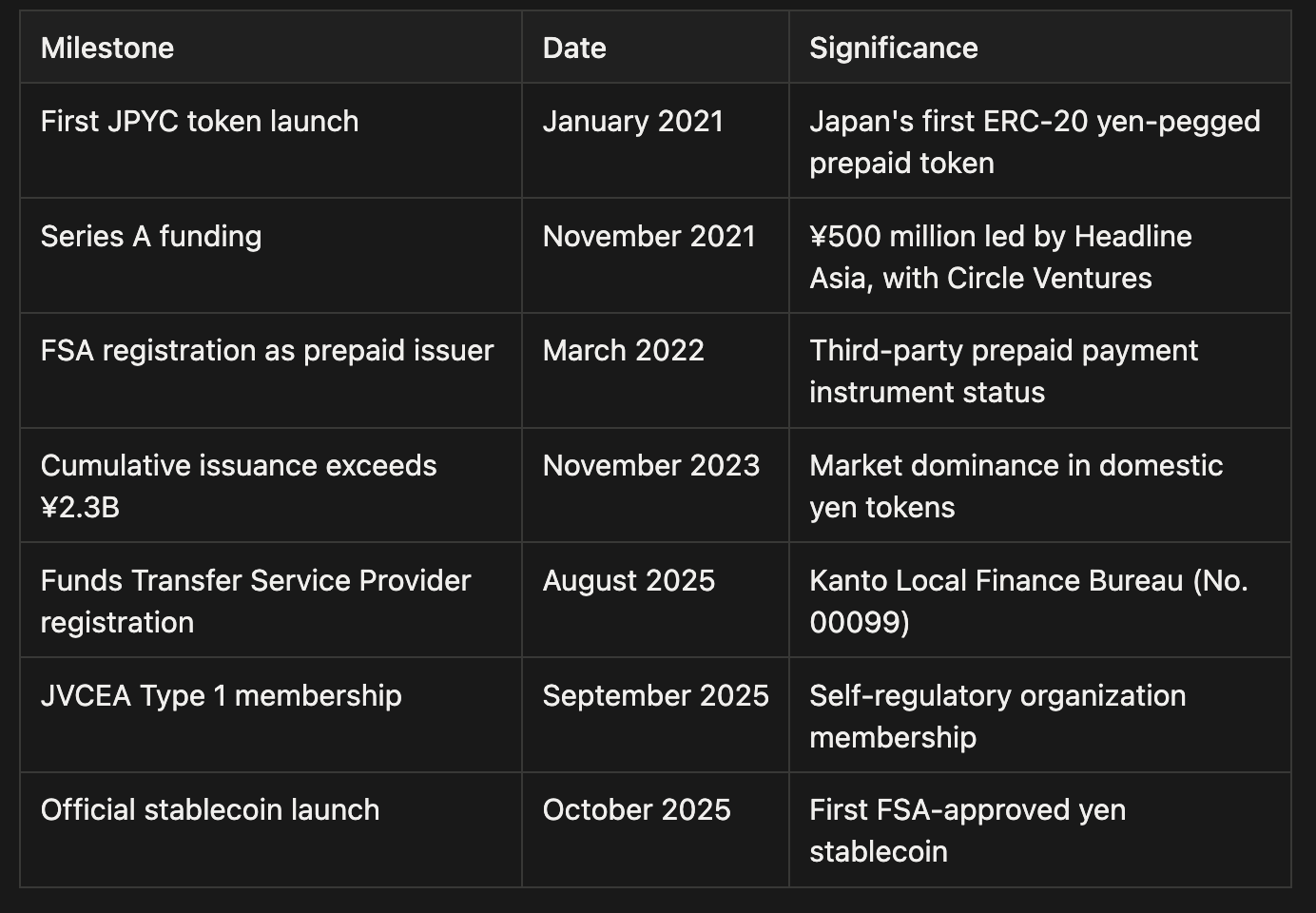

JPYC Inc. launched Japan's first domestically regulated yen-pegged stablecoin in October 2025, beating the megabank consortium to market and establishing a template for how nimble fintech players can navigate Japan's demanding regulatory landscape.

From Prepaid to Stablecoin

JPYC's journey began with a regulatory workaround. When the company launched its first yen-pegged token in January 2021, Japan had no legal framework for stablecoin issuance. Founder Okabe structured JPYC as a prepaid payment instrument under the Payment Services Act, essentially a digital gift card that could be purchased with yen but not redeemed back to cash. This gave JPYC a legal foundation to operate on public blockchains while competitors waited for regulatory clarity.

The June 2023 PSA revision created a path to full stablecoin status. After over a year of preparation, JPYC transitioned to the EPI framework in June 2025, with FSA registration as a Funds Transfer Service Provider following in August.

Technical and Reserve Architecture

The new JPYC operates as an Electronic Payment Instrument under the Payment Services Act, fundamentally different from its prepaid predecessor. Unlike the prepaid token, the new JPYC is fully redeemable: users can convert JPYC back to yen through the JPYC EX platform after completing identity verification via Japan's My Number (JPKI) card system.

JPYC operates under a Type II Funds Transfer License, which currently limits issuance and redemption to ¥1 million per user per day. Wallet-to-wallet transfers have no such restriction, allowing high-value transactions once tokens are in circulation. The company is pursuing a Type I license to remove the daily cap entirely.

JPYC EX operates as "open financial infrastructure" requiring no merchant contracts, any developer or business can integrate JPYC freely using the provided SDK released on GitHub. This positions JPYC for broad ecosystem adoption rather than controlled distribution.

Integration Ecosystem

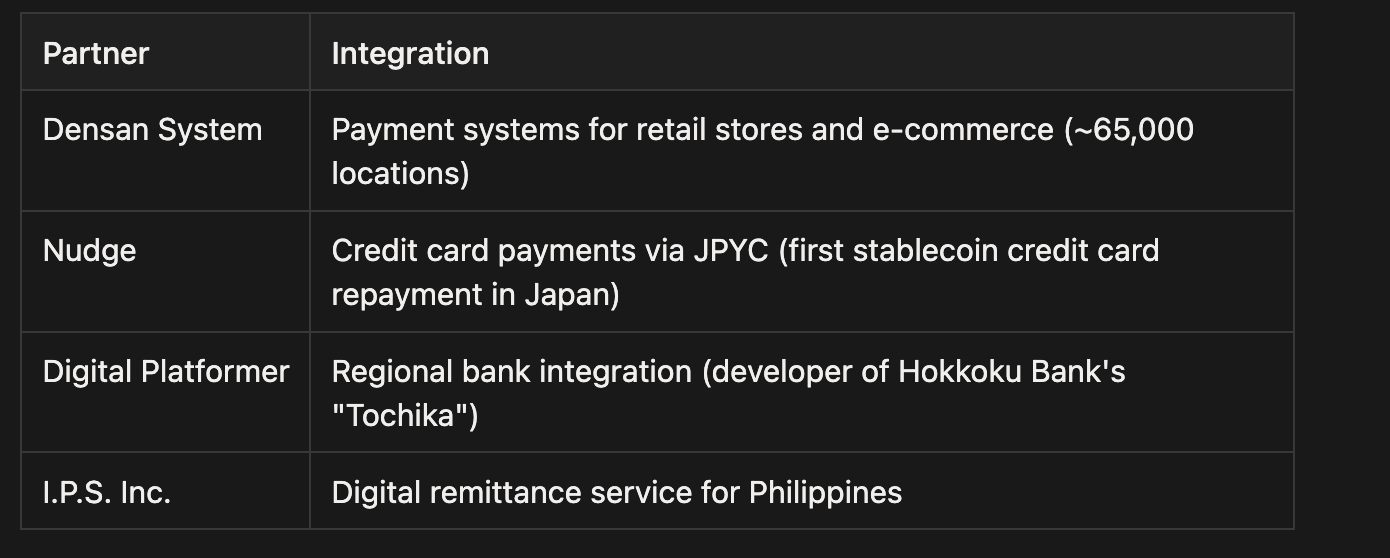

JPYC launched with commitments from multiple Japanese technology and financial companies to integrate the stablecoin into their services.

Densan System's integration is particularly notable: the fintech firm operates payment infrastructure spanning approximately 65,000 retail locations across Japan, focusing on familiar interfaces, QR codes, barcodes, and touch terminals, while incorporating stablecoin settlement. Target applications include small-amount high-frequency transactions, billing operations, local government services, and tourism.

Nudge became the first service to accept JPYC for credit card balance repayments in October 2025, users can transfer JPYC to a designated wallet address to settle their Nudge Card bills. This effectively enables JPYC payments at approximately 150 million VISA merchant locations globally.

Digital Platformer (developer of Hokkoku Bank's "Tochika" deposit-backed token) launched a joint study to integrate JPYC with regional banks, focusing on issuance/redemption models, payment infrastructure, and cross-bank coordination. Multiple regional banks have inquired about JPYC integration, suggesting demand beyond the megabank ecosystem.

I.P.S. Inc. partnership, announced one day after the stablecoin launch, targets Philippines remittances. The Philippines receives approximately $40 billion annually in remittances, much of it from Japan. A yen stablecoin offering lower fees and faster settlement than traditional remittance channels addresses a concrete market need. and signals JPYC's cross-border ambitions.

More recently, LINE NEXT signed an MoU to integrate JPYC into a stablecoin wallet accessible via LINE Messenger, targeting payments and loyalty programs for LINE's massive Japanese user base. Separately, Sumitomo Mitsui Card Company and MynaWallet piloted touch-based JPYC payments using Japan's My Number Card as a hardware wallet which users tap their government ID on payment terminals while blockchain settlement occurs invisibly in the background, addressing the UX friction that limits stablecoin adoption among non-technical users.

Onchain Presence

Unlike bank-issued stablecoins designed primarily for institutional settlement, JPYC operates natively in decentralized finance ecosystems.

As of January 2026, JPYC has approximately ¥331 million in circulationacross 85,000 holder addresses on Ethereum, Polygon, and Avalanche. The token trades on Uniswap v4 and Trader Joe, enabling on-chain JPY/USD trading pairs without centralized intermediaries.

Secured Finance launched a JPYC product suite in November 2025 aimed at bringing "the yen yield curve on-chain," including fixed-rate lending markets, JPYC borrowing collateralized by WBTC or ETH, and an on-chain yen benchmark rate. PAO TECH Labs has announced plans for JPYC lending markets on Morpho and Euler Finance.

The Partnership Path

JPYC's path forward runs through the partnerships, not the DeFi integrations. The 85,000 wallet holders are nice validation, but ¥331 million in circulation is rounding error at institutional scale. Densan System's 65,000 retail locations and the Nudge credit card integration matter more, they create utility for people who don't know what a blockchain is.

The Type I license is the unlock. At ¥1 million daily limits, JPYC can serve retail and crypto-native users but not corporate treasury. Removing that cap opens B2B payments, positioning JPYC as a nimble alternative for mid-market companies that find megabank relationships too heavy.

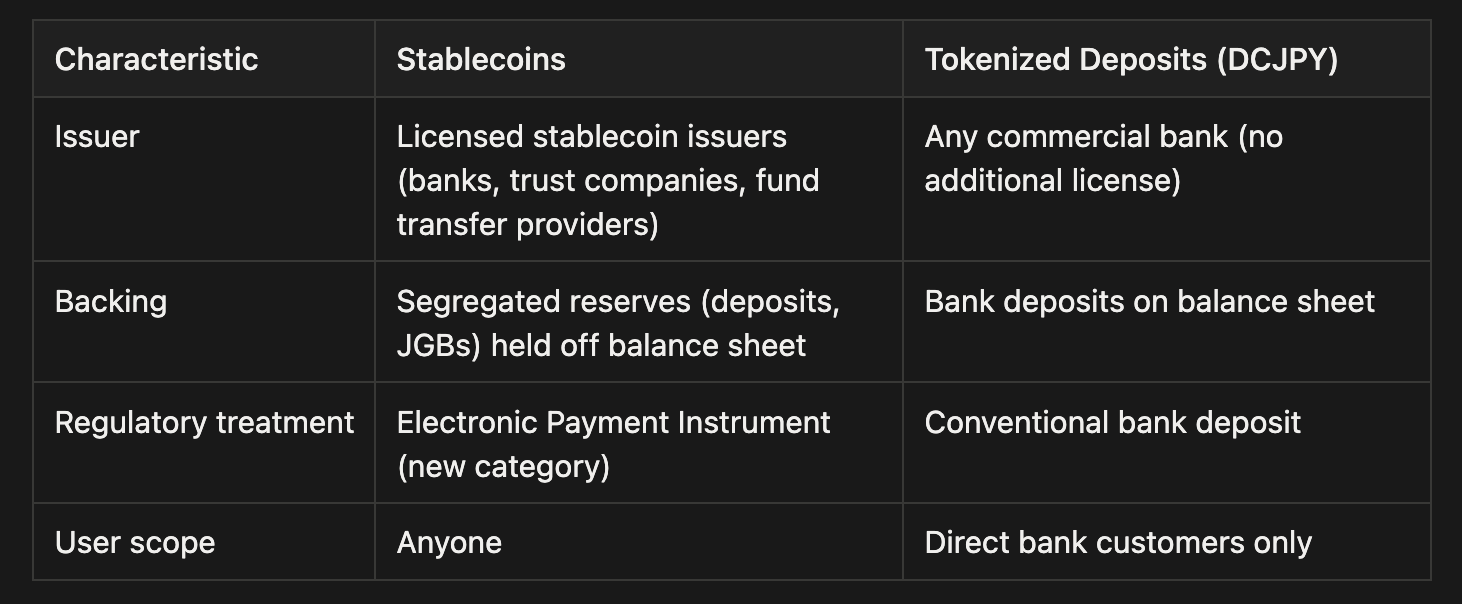

While JPYC and the megabank consortium race to launch stablecoins, a parallel infrastructure has quietly gone live: tokenized bank deposits. DeCurret DCP's DCJPY platform represents a fundamentally different approach to programmable money, one that operates entirely within existing banking regulation rather than creating new licensing categories.

The distinction matters for institutional adoption. A stablecoin represents a claim on segregated reserves held off balance sheet; a tokenized deposit represents the deposit itself, simply recorded on a distributed ledger rather than in a centralized database. When DCJPY transfers between parties, the underlying fiat balances at the issuing bank move accordingly. The blockchain becomes a settlement layer, not a new asset class.

This architectural choice explains why Japan's megabanks invested heavily in DeCurret despite simultaneously backing Progmat's stablecoin infrastructure. The two approaches serve different use cases: stablecoins for retail, Web3 integration, and cross-border payments; tokenized deposits for institutional settlement, securities DVP, and enterprise treasury operations where regulatory certainty is paramount.

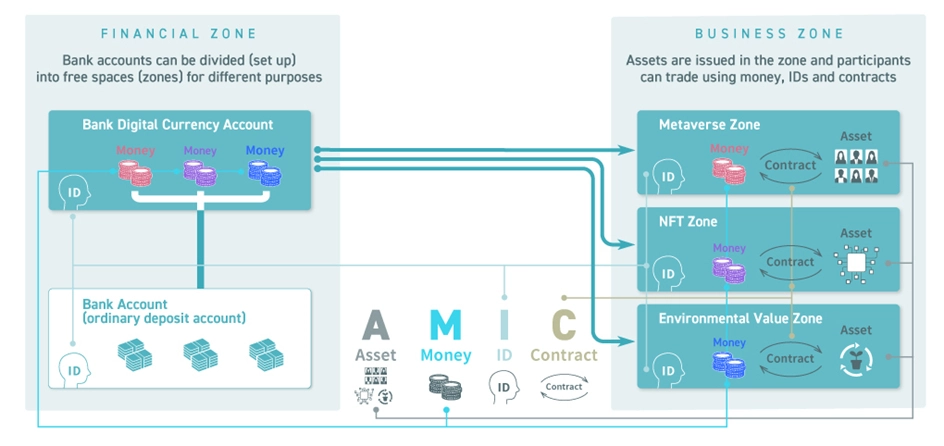

Technical Architecture: The Two-Zone Model

Source: Publishing a White Paper laying out a vision of the Digital Currency DCJPY|DeCurret DCP Inc.

DCJPY operates on a two-zone architecture that separates payment settlement from business logic through Financial Zone which handles the core payment and settlement functions, and Business Zone which hanles application specific logic and workflows.

This separation allows banks to maintain control over monetary operations in the Financial Zone while enabling innovation in the Business Zone. A retail loyalty program, an environmental certificate trading system, and a securities settlement application can each operate in their own Business Zone while sharing the same underlying payment infrastructure.

The issuance flow works as follows:

Customer requests DCJPY from their bank

Bank transfers equivalent fiat to a segregated DCJPY account

Platform mints corresponding DCJPY tokens

Tokens credited to customer's wallet

Critically, DCJPY is fully interoperable between banks. A DCJPY token issued by GMO Aozora Net Bank can be transferred to a Japan Post Bank customer, with the underlying interbank settlement handled automatically. This prevents the fragmentation that plagued earlier digital money experiments.

Live Use Cases

IIJ Environmental Value Trading marked DCJPY's first production deployment in August 2024. DeCurret's corporate parent uses DCJPY to settle renewable energy certificate trades. IIJ procures non-fossil certificates through JEPX, tokenizes them in the Business Zone, and sells to data center clients who pay with DCJPY minted by GMO Aozora Net Bank. Settlement occurs instantly on-chain, demonstrating atomic settlement of tokenized assets using tokenized deposits.

BOOSTRY Security Token Settlement represents the most significant institutional use case. A consortium including SBI Securities, Daiwa Securities, SBI Shinsei Bank, BOOSTRY, and Osaka Digital Exchange completed system design and workflow validation by August 2025, with formal announcement in December 2025. The integration connects DCJPY to BOOSTRY's ibet for Fin platform which immediately creating settlement infrastructure for a substantial portion of the market.

Japan Post Bank announced in September 2025 that it will begin issuing DCJPY in fiscal year 2026. With 120 million account holders and ¥190 trillion in deposits, Japan Post Bank's participation transforms DCJPY from a niche B2B solution into potential mass-market infrastructure. Initial applications target security tokens, NFTs, and real estate payments.

Partior Cross-Border Integration extends DCJPY beyond domestic settlement. SBI Shinsei Bank and DeCurret signed an MoU with Partior, the multi-currency wholesale platform used by DBS, J.P. Morgan, Standard Chartered, and Deutsche Bank. The partnership aims to connect DCJPY's domestic network to international rails for real-time cross-border settlement, targeting the same correspondent banking modernization market as Project Pax.

The Japan Post Wildcard

Japan Post Bank changes everything. 120 million accounts and ¥190 trillion in deposits, no stablecoin can match that domestic reach. The open question is what those account holders will actually do with tokenized deposits. Security token settlement and environmental certificates are live use cases, but they're B2B. Consumer applications haven't been announced.

The deeper tension is whether Japan needs both DCJPY and megabank stablecoins for domestic settlement. Banks may prefer tokenized deposits (no new regulatory category, familiar balance sheet treatment). Corporates wanting cross-chain flexibility may prefer stablecoins. The market will sort it out, but some redundancy seems inevitable.

The architecture emerging is layered: issuers (megabanks, trust companies, fund transfer providers) at the base, infrastructure operators (Progmat, BOOSTRY, Datachain) in the middle, and distributors (SBI, securities firms, fintech apps) at the top. Multiple settlement assets compete, trust-issued stablecoins, bank-issued stablecoins, tokenized deposits, each optimized for different use cases. Cross-border projects like Project Pax aim to abstract these rails entirely, letting corporates send SWIFT messages while settlement happens invisibly on-chain.

This layering reflects a broader truth: stablecoins reward position in the stack, not novelty. Control the interface, the flow, or the settlement layer and stablecoins enhance your economics. Issue a token without distribution and you compete in a market that naturally consolidates. Japan's incumbents understand this: the megabanks aren't launching stablecoins to compete with USDC, they're embedding programmable settlement into existing corporate relationships. SBI isn't betting on one token winning; it's positioning to profit from whichever tokens flow through its rails.

What remains is adoption. Infrastructure without users is just technology. The institutions are committed, the regulations exist, the technology works. Whether Japan's bet on institutional infrastructure over retail speculation pays off depends on whether enterprises find enough value in programmable money to change how they move it.

Dive into 'Narratives' that will be important in the next year