MoneyX is a conference representing the Asian finance and fintech industry, hosted by JPYC, Progmat, TV Tokyo, SBI Group, and CoinPost. It serves as a platform to discuss key issues shaping the next generation financial ecosystem, including digital assets, stablecoins, payment infrastructure, and regulatory environments.

Four Pillars participated in MoneyX as the exclusive research partner, and this article aims to share summaries of the sessions as well as various insights related to the Japanese market gained on site.

Contrary to common perceptions in the global market, Japan appears to be one of the most open markets toward the transition to onchain finance. Its approach, which emphasizes compliance first and internalization strategies, as well as a coexistence model for CBDCs, deposit tokens, and stablecoins, provides valuable examples that other countries may reference.

MoneyX is a conference that represents the Asian finance and fintech industry, where key issues shaping the next generation financial ecosystem are discussed, including digital assets, stablecoins, payment infrastructure, and regulatory environments. Japan in particular has presented an important benchmark in global stablecoin regulatory discussions by clarifying the legal definition and issuance and distribution framework of stablecoins through the enforcement of the revised Payment Services Act in 2023.

At the center of Japan’s stablecoin industry are major companies such as SBI Group, JPYC, CoinPost, and Progmat, which have come together to co host the MoneyX conference. Approximately 3,000 participants attended the event, including representatives from major Japanese financial institutions, fintech companies, blockchain projects, and regulatory authorities. They engaged in in depth discussions on the institutional adoption of stablecoins and their practical use cases.

Four Pillars participated in MoneyX as the exclusive research partner and published and distributed a proprietary research report providing an in depth analysis of the Japanese stablecoin market. The report covers the current state and growth trajectory of the Japanese stablecoin market, analysis of key issuers and infrastructure providers, a review of the regulatory framework based on the Payment Services Act, comparisons with global markets, and future outlooks.

On the day of the event, Four Pillars also operated its own booth on site and exchanged insights on market conditions and future prospects with Japanese financial institutions and industry participants. In this article, we will share the sessions during the event and the key insights that can be drawn from the Japanese market.

Speaker: Satsuki Katayama(Minister of Finance)

This session started from the premise that stablecoins and tokenized deposits must move beyond being merely “faster and cheaper” and become infrastructure that connects to real industrial processes. On that basis, it explored institutional design and use cases needed to make that shift happen.

Finance Minister Katayama, who could not attend in person due to official duties, delivered the keynote via a video message. She noted that the United States is tightening its federal regulatory framework for stablecoins as part of its push to strengthen digital finance leadership, and explained that tokenized deposits are also expanding rapidly, led by major commercial banks.

In response, she said Japan has already taken an early lead in building regulatory frameworks for crypto assets and stablecoins. As a result, the first yen-denominated stablecoin (JPYC) was issued in October of last year and surpassed a cumulative issuance of 1 billion yen in roughly three months. She also noted that, in November, a joint issuance proof-of-concept involving the three megabanks was announced.

She did not frame the core value of stablecoins and tokenized deposits as simple improvements in speed or cost reduction. Instead, she presented high-impact use cases: in trade finance, linking logistics, customs clearance, and payment data on chain, and in securities settlement, synchronizing the transfer of rights and the settlement of funds, thereby upgrading entire end-to-end operational processes.

She added that, alongside support for pilot projects through the Financial Services Agency’s PIP program, Japan would establish a dedicated organization for crypto assets and stablecoins this summer to strengthen its digital financial asset framework. The moderator then opened the session by explaining that MoneyX is a forum built around the shared theme of the evolution of money, bringing together discussions across technological innovation, institutional design, governance, risk, and social implementation.

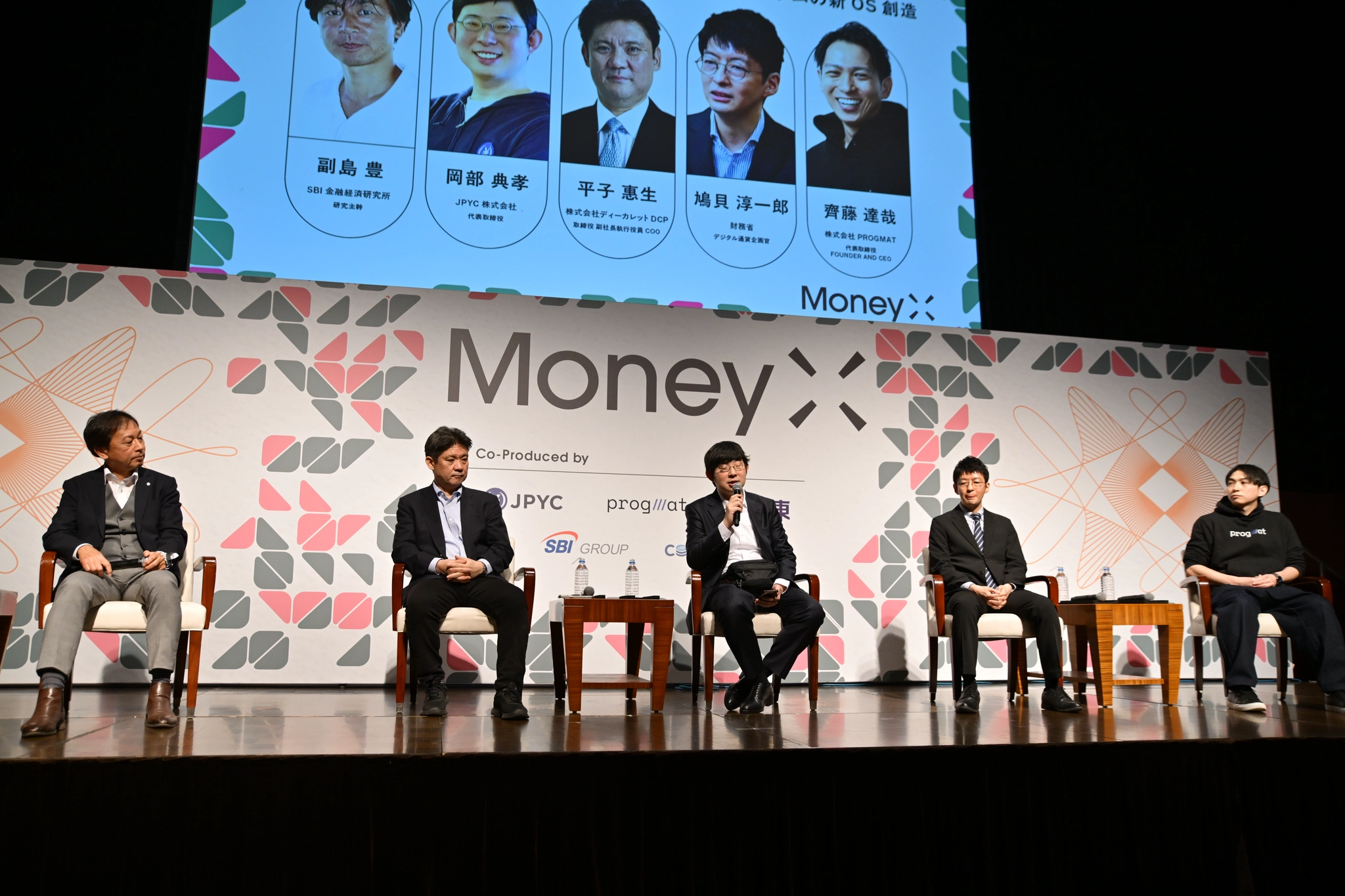

Panelist: Yoshio Hirako(DeCurret DCP Inc.), Junichiro Hatogai(Ministry of Finance), Tatsuya Saito(Progmat, Inc.), Noritaka Okabe(JPYC inc.) / Moderator: Yutaka Soejima(SBI Financial and Economic Research Institute)

This session operated on the premise that stablecoins, tokenized deposits, and CBDCs each have distinct roles but must be connected within a single system, and discussed who should design the standards and governance for that connectivity, and how.

Yutaka Soejima (SBI Financial and Economic Research Institute) opened the session by framing its core question: not whether one form of money replaces another, but how different forms of money connect, where final settlement occurs, and who bears what responsibility. He added that this coordination requires the public sector to provide a minimum foundation (accessibility, regulation, interoperability, settlement finality) while fostering private-sector innovation.

Junichiro Hatogai (Japan's Ministry of Finance) elaborated on the role of the public sector. He argued that while the private sector drives innovation, the public sector should build the foundation that ensures interoperability and accessibility. He also emphasized the importance of filling gaps in payment accessibility where low profitability prevents the private sector from providing sufficient coverage.

Yoshio Hirako (DeCurret DCP) placed particular emphasis on interoperability. DCJPY, a tokenized deposit, is designed to reduce the complex operations of corporate payments (login, two-factor authentication, manual verification, ERP clearing) through onchain automation. He stressed that what matters in corporate payments and settlement is not which token is used, but the connectivity that allows CBDCs, tokenized deposits, and stablecoins to move safely within a single system, exchange with each other through pre-defined rules, and redeem into fiat payment rails when needed.

The remaining two panelists shared perspectives from the industry. Okabe (JPYC Inc.) introduced JPYC as Japan's first licensed yen stablecoin, noting that within approximately four months of issuance, cumulative issuance reached 1.3-1.4B yen, with about 81,000 holders and an average holding of roughly 110,000 yen per person. He noted that the primary users of digital money are not necessarily limited to humans, and that AI agents and robots may also participate in economic activity. He emphasized that public-chain-based programmable money in a form directly usable by programs, like JPYC, will become necessary.

Saito (Progmat) stressed that for tokenized deposits and stablecoins to be used in actual financial systems, a standardized management infrastructure covering issuance, administration, and redemption is needed, going beyond mere token issuance. He explained that to meet institutional compliance requirements (permission management, transfer restrictions, record-keeping and auditability), compliance must be designed as a structure embedded at the infrastructure level, not as a feature of individual services. The point is that on top of such infrastructure, various use cases including corporate payments, settlement automation, and programmable finance can realistically expand.

The consensus emerging from this session is that Japan's digital money ecosystem is heading toward a structure where multiple forms of digital currency coexist, rather than converging on a single form. Given that CBDCs, tokenized deposits, and stablecoins are each assumed to serve distinct roles at different layers, the task Japan's market has set for itself is orchestrating these inherently fragmented forms of money into a single operating system.

This multi-money structure is not something the market created organically. It is a result of regulatory design. Japan established a stablecoin regulatory framework relatively early, in June 2023, by amending the Payment Services Act to create a new legal category called "Electronic Payment Instruments (EPI)." The key is that while issuers are classified into three types (deposit-type for banks, trust-type for trust companies, and funds transfer-type for funds transfer service providers), a 100% yen reserve requirement is imposed across all types.

In March 2025, this was relaxed for trust-type issuers only, allowing up to 50% of reserve assets to be invested in government bonds with a remaining maturity of three months or less. The 100% reserve principle itself remains intact.

As a result of this framework, Japan's digital money started not from a single issuance model but from a structure where different financial entities issue within their own regulatory frameworks and share responsibilities. The problem is that these three tracks of digital money inherently carry fragmentation by design. This is why expressions like "digital island" and "walled garden" appeared repeatedly in the session, warning against fragmentation.

This concern is shared across the industry, and the session's discussion focused on coordinating the roles and positions of each economic actor. The panel composition itself reflects this: a financial policy research institute (SBI Financial and Economic Research Institute), government (Japan's Ministry of Finance), tokenized deposit infrastructure (DeCurret DCP), a stablecoin issuer (JPYC), and a tokenization infrastructure company (Progmat) were assembled in one place.

At the same time, this suggests that the Japanese market is progressing these discussions at a pace and in a manner suited to its industry structure. It illustrates the current stage of the Japanese market, where the center of gravity has shifted from "who will issue" or "which token becomes the standard" to how different digital currencies and infrastructures will be connected.

Panelist: Yam Ki CHAN(Circle), Seker(Binance) / Moderator: Takehiko Koyanagi(Nikkei Inc.)

Koyanagi opened with the framing numbers: stablecoin market cap crossed $300 billion after the U.S. Genius Act, but 99% is dollar-denominated, and real economic transactions are just 0.02% of gross volume. The question isn't growth — it's whether a multi-currency system is actually forming.

Chan laid out Circle's full-stack evolution beyond stablecoin issuance. USDC sits at $75 billion in circulation with $11 trillion in Q4 on-chain transactions. The product stack now includes Arc (a Layer-1 with known validators and sub-second finality), StableFX (an institutional FX engine for 24/7 stablecoin pair settlement), and the Circle Payments Network. He described the current model as a "stablecoin sandwich" — fiat in, stablecoin intermediary, fiat out — with local stablecoins eventually replacing the fiat edges. He noted 75% of Asian trade invoices are still dollar-denominated and that Arc's known-validator design was built to satisfy financial regulators.

Seker pushed back on multi-currency timelines. Non-USD stablecoin volumes remain tiny even on Binance, which holds ~40% of global stablecoin reserves. His argument: domestic ecosystems need sufficient scale to sustain local stablecoin adoption, and for smaller economies, tight on/off-ramps to dollar stablecoins may be more practical.

Chan confirmed this isn't just about issuing USDC in Japan. SBI invested $50 million in Circle at IPO and USDC launched through SBI VC Trade in March 2025 — the only licensed USD stablecoin in the Japanese market. That gave Japan something no other Asian market has: a compliant on-ramp for the world's second-largest stablecoin alongside a domestic yen alternative.

What I didn't fully appreciate until this session is the infrastructure play underneath. Arc with StableFX, combined with the Circle Partner Stablecoins program (which already includes JPYC), means Circle is positioning itself to own the on-chain FX layer between USD and every regional stablecoin that joins. The yen accounts for roughly 17% of global FX volume. Having both currencies as compliant on-chain instruments creates the foundation for on-chain FX with actual depth. If it's going to happen anywhere, USD/JPY is probably where it starts.

But Seker's skepticism is the honest counterweight. Euro stablecoins under MiCA have negligible adoption despite regulatory clarity. The 99% USD dominance Koyanagi opened with is a liquidity gravity well that every non-dollar stablecoin has to escape.

Panelist: Colin Payne(Financial Conduct Authority (FCA), UK), Alan Lim(Monetary Authority of Singapore), Carole House(Former White House Advisor, Penumbra Strategies) / Moderator: Prof. Chia Tek Yew(NUS - Asian Institute of Digital Finance)

Three regulators, three jurisdictions, one subtext: the global regulatory landscape is fragmenting, not converging.

Lim from MAS framed Singapore's approach as policy principles (fairness, accountability, transparency) combined with industry-led operationalization through consortia like Mindforge. His sharpest point: regulators need to examine how much stablecoin volume actually supports real economic activity versus crypto-to-crypto trading in a stablecoin wrapper.

Payne from the FCA revealed that the first sterling stablecoins are live in the UK's digital sandbox, with the crypto-asset authorization gateway opening August 2026. He stressed this isn't soft-touch — the FCA blocked FTX — and framed Brexit as a regulatory flexibility dividend. The UK isn't bound by MiCA and can carve its own path.

House delivered the session's sharpest critique: the U.S. push for dollar dominance through stablecoins contradicts its simultaneous rollback of enforcement, effectively forfeiting oversight of the largest USD-denominated peer-to-peer money transfer system in the world. She also flagged quantum computing as an existential risk — most cryptocurrency cryptography is vulnerable to quantum computers, and migration to safe standards will take five to ten years.

What makes Japan unusual isn't that it has stablecoin rules (the EU has MiCA, Hong Kong has its sandbox, and now the UK is opening its gateway) but that Japan's rules are already producing live products. The PSA amendments classified fiat-pegged stablecoins as "electronic payment instruments" with a licensing regime requiring 100% reserves in yen deposits or JGBs and segregated custody. No algorithmic experiments, no unbacked tokens.

Here's the regulatory architecture the panelists didn't discuss: the FSA is moving crypto assets from the PSA to the FIEA (Japan's securities law) while keeping stablecoins under the PSA. That's a deliberate split; stablecoins get a lighter, payments-focused touch while exchange-traded tokens get the heavier investor-protection framework. This matters because it means stablecoin issuers aren't burdened with securities-grade compliance overhead.

House's enforcement contradiction validates my bear case from a different angle. The FSA's January 2026 consultation on reserve bond eligibility (foreign bonds need credit ratings of 1-2+ and minimum outstanding issuance of ¥100 trillion) signals a regulator that moves methodically. That's the tradeoff Japan has chosen: slower velocity, but a framework where every actor (JPYC, the megabanks on Progmat, Circle via SBI) competes on the same licensed playing field. Whether "methodical" becomes "too slow" depends on the UK and Singapore timelines. Payne's August gateway is the one to watch.

Panelist: Noritaka Okabe(JPYC inc.), Hailey Yang(Kaia), Toshiyuki Kurihara(LINE NEXT Inc.) / Moderator: Takahito Kagami(CoinPost inc.)

The headline: LINE NEXT launched "Unifi," a Web3 wallet on LINE integrating JPYC as its primary stablecoin. The onboarding model is gamified micro-rewards — 10 JPYC for missions, 200 JPYC for game stages — building familiarity before graduating to financial use cases like lending. If LINE is installed, the stablecoin experience should feel invisible.

Okabe surprised the room by announcing JPYC is considering deployment on Kaia, the Layer-1 built by LINE and Kakao. Most expected Base or Arbitrum next, but the logic is distribution-first: the fastest path to Asian mass adoption runs through messaging platforms with hundreds of millions of users, not DeFi-native chains. JPYC is already on Ethereum, Polygon, and Avalanche, and will deploy on Circle's Arc at mainnet. The Kaia play connects LINE (Japan, Thailand, Taiwan) and Kakao (Korea) into a single yen stablecoin rail.

Yang from Kaia added concrete traction: stablecoin POCs with a Korean megabank, ¥3 billion in tokenized Indonesian shipping assets, and a vision of stablecoins converging with RWA and AI agents. The most forward-looking discussion: Okabe described a live POC where AI agents handle restaurant reservations and settle payments in JPYC, agent to agent. Merchants already offer 2% discounts for JPYC because settlement fees undercut credit cards.

Set this against the numbers. JPYC registered with the FSA in August 2025 and began issuing on October 27th. The business model mirrors Circle's: waive fees at launch, earn yield on JGB reserves. The ambition is ¥10 trillion in circulation within three years (~$65 billion). Current reality is ¥2.6 billion circulating, market cap ~$17 million, fresh off an $11.9 million Series B. That's 0.026% of the way there.

What Unifi and Kaia do is make the distribution strategy legible. The question was always how JPYC gets from $17 million to $65 billion. The answer isn't DeFi liquidity mining, but instead embedding into platforms where 100 million people already live. LINE's user base, the points economy (Ponta → JPYC → au PAY is already live), and AI agent commerce are distribution vectors that don't require users to understand what a stablecoin is. Meanwhile the megabank track runs in parallel — MUFG, SMBC, and Mizuho on Progmat targeting March 2026 deployment, with Mitsubishi Corporation as first user testing blockchain settlement for cross-border corporate payments.

The tax reform completes the demand picture — crypto capital gains dropping from up to 55% to a flat 20% for ~105 tokens on registered exchanges, with three-year loss carryforward (effective date probably 2027-2028; staking and lending stay at 55%). Japan is building the most complete regulated stablecoin stack in the developed world (startup speed, institutional credibility, and global liquidity under one legal framework) and the pieces are connecting faster than most people outside Japan realize. The regulatory infrastructure is no longer the bottleneck. For the first time, it might actually be the enabler.

In this session, SWIFT, the Bank of Japan (BOJ), and the Ministry of Finance clearly stated their respective positions on what role existing infrastructure will play in the era of digital money.

SWIFT's Kayahana rejected the 'slow legacy' framing of SWIFT and presented a notable argument about the bottleneck in cross-border payments. 75% of cross-border remittances already reach the receiving bank within 10 minutes, and the real bottleneck lies not in transmission speed but in the 'last mile' from the receiving bank to final deposit. In other words, final account crediting, country-specific AML/KYC processing, and timezone-driven operating hour mismatches are the true bottlenecks causing remittance delays. At the same time, he revealed a strategy to add a blockchain-based ledger on top of the existing messaging layer as a complement. This reads as a declaration that SWIFT intends to remain the foundational layer of cross-border payments even in the tokenization era.

BOJ's Sugimura defined the central bank's role as guaranteeing the finality of value transfers. He explained that the future of cross-border payment infrastructure will not be determined by a single technology, but will evolve through a combination of multiple options: improvements to interbank transfers, linkage of cross-border instant payment systems, non-bank payment instruments, and stablecoins. He introduced BIS-led Project Agora as a key example. The structure places private commercial bank deposits and central bank deposits on the same shared ledger to achieve atomic settlement. He described it as an experiment demonstrating that central banks can remain the infrastructure providing settlement finality even in a digital asset environment.

Hatogai of Japan's Ministry of Finance distinguished between wholesale and retail CBDCs, presenting use cases for each and explaining their policy implications. For wholesale, he argued that as tokenized assets and DLT-based financial transactions expand, the need for settlement finality grows, and so does demand for tokenized central bank money. For retail, he offered the view that rather than in cities where various payment methods already exist, retail CBDCs could function as a supplementary public payment infrastructure in depopulating areas or regions with low financial accessibility. This shows that CBDCs are not envisioned as replacing existing payment methods, but as sharing roles across different payment rails and coexisting in the future.

The three institutions in this session spoke from different positions, but converge on one point. Each is seeking not to be replaced in the digital money era, but to redefine and solidify its own position.

SWIFT is the most proactive of the three. The crypto industry has pushed the "replace SWIFT" narrative for over a decade, but SWIFT's position is different. In September 2025, SWIFT announced the addition of a blockchain-based ledger to its own infrastructure, with over 30 financial institutions participating in the design. In November of the same year, it began integrating with Chainlink CCIP, opening a blockchain access pathway for over 11,000 institutions. The strategy is not to compete with blockchain, but to absorb it as part of the stack.

BOJ's positioning is taking concrete form through Project Agora. Currently, cross-border payments separate messaging (payment instructions) from fund movement, and correspondent banks in between independently repeat AML/KYC checks, generating delays and costs. Agora aims to solve this through tokenization. The structure places tokenized commercial bank deposits and tokenized central bank money on a single unified ledger, executing atomic settlement via smart contracts. Both sides either execute simultaneously or neither does, eliminating the settlement delays and counterparty risk inherent in traditional correspondent banking. Seven central banks including BOJ and 41 private institutions are now participating, having entered the testing phase in January 2026, with a first-half report forthcoming.

Hatogai of the Ministry of Finance linked the need for wholesale CBDCs to the growth of tokenized assets. The logic is that as more assets are traded onchain, demand for central bank money to guarantee final settlement of those transactions also grows. This is already being demonstrated domestically in Japan. Japan's security token market, starting from digital bonds in 2020, surpassed 270 billion yen in cumulative public offerings as of November 2025, and six firms including SBI Securities and Daiwa Securities have begun DVP settlement testing using DCJPY. As real demand for tokenized assets is confirmed, the positioning of CBDCs as instruments that can provide settlement finality under the central bank is also taking shape.

Speaker: Yoshitaka Kitao(SBI Holdings)

This session delivered the message that on-chain finance is no longer an experimental domain but is shifting into a tangible trend that can replace traditional financial infrastructure. It argued that, for Japan not to fall behind, private-sector speed and government-led institutional reform must move forward in parallel.

Kitao summarized the drivers behind the evolution of on-chain finance into three factors: regulatory and legal reforms, technological advancement, and the accelerating convergence of traditional finance and decentralized finance. He strongly criticized Japan’s regulatory environment for continuing to hold the market back, citing restrictions on eligible stablecoin issuers, caps on foreign-currency stablecoins, delayed tax reforms, and slow progress on ETFs. In contrast, he said the United States is rapidly advancing stablecoin legislation and market structure bills to reduce legal uncertainty. He repeatedly emphasized that crypto assets can no longer be treated as a peripheral asset class, noting that Japan already has 14 million crypto asset accounts and total balances exceeding 5 trillion yen, and reiterating the message that “if something is good, it should be changed quickly.”

On the technology side, he explained that Layer 2 progress has largely addressed transaction speed and fee issues, and that the market is now entering a phase where AI agents can interact directly with wallets, enabling chain abstraction and natural-language execution. He also projected that individuals will gain more direct access to on-chain finance through AI agents, without intermediaries.

As evidence from the United States, he pointed to tokenized money market funds and tokenized stocks, along with 24/7 trading and instant DVP (delivery versus payment) settlement. Citing moves by major players such as the NYSE, Nasdaq, Robinhood, and WisdomTree, he argued that traditional financial infrastructure itself is being redesigned on chain.

He then outlined SBI’s strategy: supporting USDC through collaboration with Circle as well as Ripple’s USD, expanding crypto asset-backed lending, pursuing a multi-chain approach across Ripple, Canton, Solana, and Ethereum, establishing and investing in a joint venture with Startale, and transitioning a private trading system (PTS) onto an on-chain model. The core idea, he said, is not to concentrate on a single chain, but to build an architecture where customers can choose the chain that best fits the functions they need.

He concluded by warning that, in the era of AI agents, on-chain finance will become essential infrastructure, with stablecoins and tokenized assets serving as its payment layer. He said Japan risks falling behind the rest of the world again unless it accelerates now, urging the private sector to increase execution speed and the government to pursue bolder institutional reform

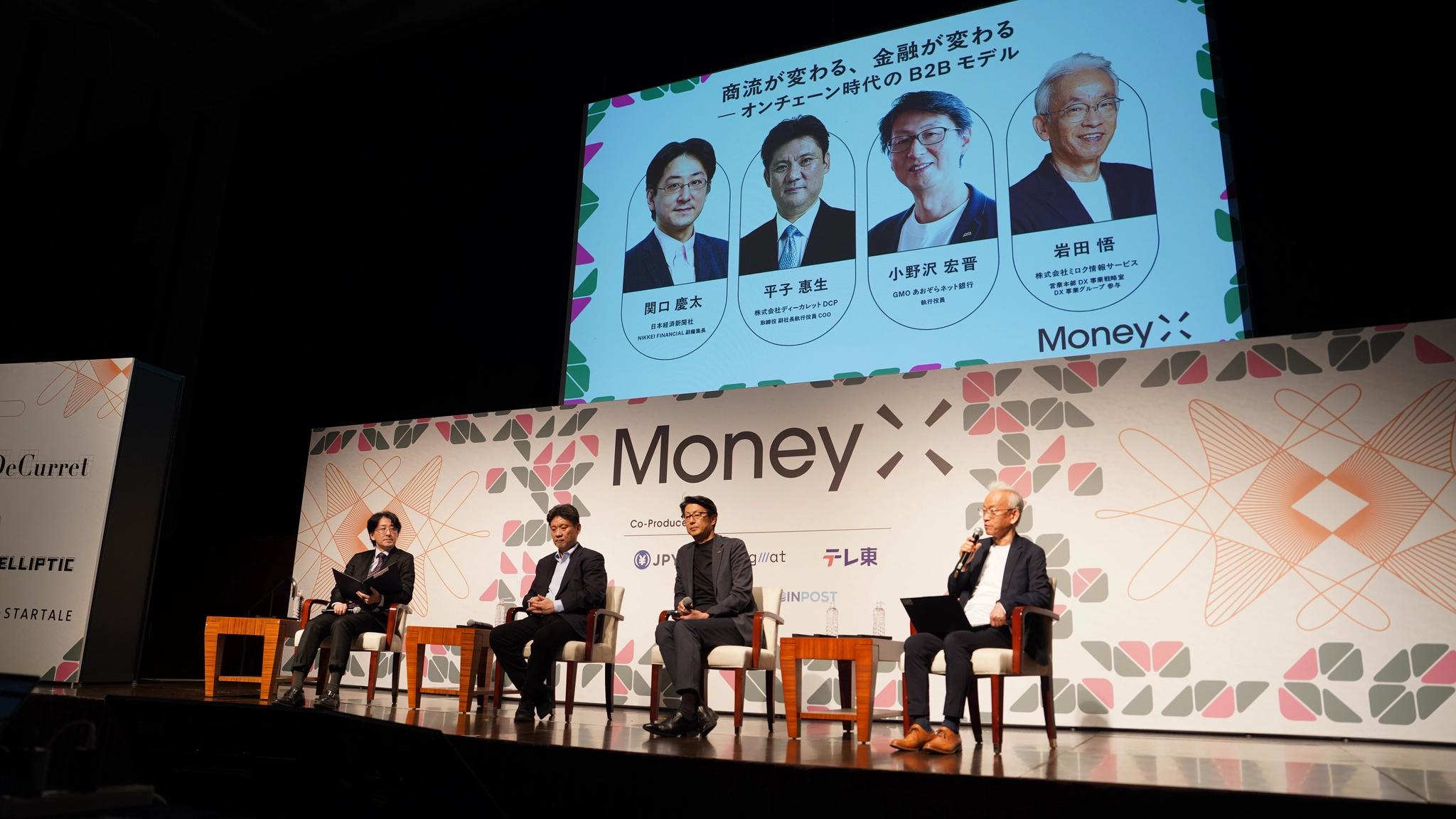

Speaker: Yoshio Hirako(DeCurret DCP Inc.), Hirokuni Onozawa(GMO Aozora Net Bank, Ltd), Satoru Iwata(MIROKU JYOHO SERVICE CO., LTD.) / Moderator: Keita Sekiguchi(NIKKEI Inc.)

This session centered on whether the relationship between deposits and stablecoins should be viewed as competition or substitution, or understood as a structure where each differentiates into distinct roles, within the context of a changing interest rate environment.

Nikkei's Sekiguchi set the starting point of the discussion with the question of how to understand the relationship between deposits and stablecoins amid a changing interest rate environment. He pointed out that while digital money discussions tend to focus on technology and token structures, in the actual financial system, macroeconomic financial conditions such as interest rates, capital flows, and the stability of bank deposits act as more significant variables. In this context, he explained that the core topic of this discussion is not whether stablecoins replace deposits, but what roles different forms of digital money will play in coexistence amid a changing interest rate environment.

DeCurret DCP's Hirako identified the key issue as how bank deposits will be reconfigured in a digital environment. Introducing DCJPY, he explained that when transaction data and payments are processed on the same system in corporate payment and settlement workflows, operational automation becomes possible. This is not about competing with stablecoins, but an evolutionary path for bank deposits to remain a payment foundation in the digital economy.

Onozawa of GMO Aozora Net Bank stated that stablecoin adoption does not immediately lead to deposit outflows. He emphasized that as the interest rate environment shifts, the driver of fund movement lies in interest rates and yield structures rather than payment convenience. Bank deposits provide stability and regulatory protection, while stablecoins provide usability within the digital asset ecosystem. He sees the two as likely to coexist in a parallel structure with different roles, not as substitutes.

Iwata of Miroku Information Service pointed out from a corporate practitioner's perspective that the value of digital money lies in business process automation rather than in a new form of asset. Corporate accounting, tax, and payment operations still rely on manual processes, and he argued that introducing a structure where payment data connects directly to accounting systems would significantly improve internal operational efficiency. His diagnosis was that the spread of digital money is more directly connected to changes in corporate operational infrastructure than to consumer payment innovation.

The session framed the relationship between tokenized deposits and stablecoins as role differentiation, not substitution. Concerns over deposit outflows are not unique to Japan. In the U.S., Coinbase is offering USDC holders a base yield of around 4%, intensifying tensions with traditional banks. Led by the American Bankers Association (ABA), over 40 banking groups sent a joint letter to Congress, warning that such yield programs could siphon bank deposits and undermine lending capacity.

In this context, Onozawa of GMO Aozora Net Bank explicitly stating that "stablecoin expansion does not equal deposit outflows" stands out. While this cannot be taken as representative of all Japanese banks, his position was clear: bank deposits serve stability and regulatory protection, stablecoins serve usability in the digital asset ecosystem, and the two coexist in a parallel structure rather than as competitors.

Where, then, do Japan's tokenized deposits fit within this structure? The consensus emerging from the session narrows to B2B operational automation, not consumer payments. Hirako described the essence of DCJPY as "reducing the complex operations of corporate payments, such as login, two-factor authentication, manual verification, and ERP clearing, through onchain automation." This diagnosis carries weight when measured against how Japanese corporations actually operate.

In Japan, order confirmation, delivery inspection, invoice issuance, reconciliation, ERP registration, and accounting entries are each handled by separate systems or manual processes, and the cloud SaaS adoption rate among SMEs is only 34%. When the qualified invoice system was implemented in 2023, 91% of companies cited 'increased operational burden' as their top concern. This shows a structure where even minor regulatory changes shake the ground floor, because invoicing and settlement processes are manual at their core.

Tokenized deposits are an attempt to bridge this disconnect. The primary use case being presented is one where smart contracts atomically execute invoicing, payment, clearing, and accounting entries at the point of delivery confirmation. The value proposition of tokenized deposits is not lower payment fees. It is the automation of the operational processes that surround payments.

Panelist: Shinsuke Sato(SLASH VISION), Gen Adachi(NETSTARS Co., Ltd.), Seihaku Yoshida(HashPort Inc.) / Moderator: Genki Oda(Japan Virtual and Crypto assets Exchange Association)

Shinsuke Sato of Slash Vision Labs opened his segment by pulling out an actual Slash Card for the audience to see. The card is a Visa card issued with Orient Corporation (Orico), a long-established Japanese credit company, serving as the BIN sponsor. Users load USDC onto the card, and from there it works at any Visa merchant in the world, just like a regular card. Merchants are settled in yen once or twice a month, exactly as they always have been, so they never need to know that a stablecoin was involved in the transaction. Sato called this the closest thing to real-world implementation currently available. Japan already has a mature cashless ecosystem built around the yen, he pointed out, so there is no reason to rebuild it. Instead, the focus should be on something that was not possible before: letting people spend foreign currencies freely in Japan, using blockchain as the bridge. USDC is the starting point, but the plan is to expand into yen-denominated stablecoins, bank-issued stablecoins, and tokenized deposits as they become available.

Gen Adachi of NETSTARS explained how his company is layering stablecoins on top of existing QR payment infrastructure through its payment gateway, StarPay. NETSTARS was the first company to introduce QR payments in Japan back in 2015, and today it operates as the country's largest QR payment aggregator, offering roughly 60 cashless brands, including PayPay, Alipay, and Visa, to merchants through a single contract.

NETSTARS added USDC as a payment option to its existing QR terminals and ran a pilot program at Haneda Airport's Terminal 3 from January through February 2026. According to Adachi, the volume of transactions far exceeded expectations, and a steady stream of inquiries from merchants has followed. For merchants, the appeal is straightforward: their existing QR readers work as-is, and settlement is entirely in yen, so nothing in their operations needs to change. Adachi noted that during the first two days, most users were Japanese early adopters, but the mix quickly shifted to predominantly Western tourists for the remainder of the pilot.

Seihaku Yoshida of HashPort shared that the company's wallet originally served as the official payment app for the 2025 Osaka-Kansai Expo before being rebranded as HashPort Wallet. Downloads have since topped 1.16 million. What stood out most, though, was his thinking on the business model. Yoshida explained his decision to set payment fees at zero by pointing to the models behind WeChat Pay and Alipay. Both services charge no fees on transfers and payments under 3,000 yen. Instead, they keep funds parked inside the wallet and generate revenue by managing that money and layering financial services on top of it. Yoshida said he intends to follow the same playbook, building a service where leaving funds in the wallet as stablecoins feels more convenient than withdrawing yen to a bank account.

He also raised the issue of monetary sovereignty. In an era where AI agents choose their own payment methods, if dollar-denominated stablecoins are the only convenient option, the yen risks being sidelined in the emerging digital economy. This, he said, is precisely why HashPort is concentrating on yen stablecoins, even as it operates as an equity-method affiliate of KDDI (au) and counts SMBC among its investors.

All three presenters in this session follow the same design principle. Merchants are settled in yen. Users get a payment experience indistinguishable from what they already know. The stablecoin stays hidden in the background. To understand why this strategy works especially well in Japan, you need to look at the dual structure of the country's payments market.

Japan's cashless payment ratio reached 42.8% in 2024, surpassing the government's 40% target ahead of schedule. But beneath that headline number, cards and QR payments play very different roles. Visa, Mastercard, and JCB account for the bulk of cashless spending by value, while QR payments have grown rapidly in transaction count but remain far smaller in monetary terms. PayPay surpassed 70 million registered users as of July 2025 and commands roughly two-thirds of Japan's QR payment volume. In choosing to ride Visa's rails, Slash Card tapped into the dominant infrastructure by value. In choosing QR rails, NETSTARS tapped into the dominant infrastructure by volume. Neither had to build a new network.

Adachi described the Haneda pilot only as "beyond expectations" during the session, but the actual structure is worth a closer look. The pilot ran from January 26 to February 28, 2026, at two locations inside Haneda's Terminal 3: the Edo Food Hall and the Edo Event Hall. Partner company WEA JAPAN handled the QR code development, while NETSTARS simply connected USDC as an additional payment method through its existing StarPay gateway. Rather than building stablecoin payments as a standalone business, the company treated it as an extension of its existing gateway. In a separate interview, NETSTARS' Saori Okuyama put it plainly: the real challenge for stablecoins is not the technology, but creating places where people can actually use them. It is an honest acknowledgment of where the bottleneck sits today.

Yoshida's reference to WeChat Pay and Alipay as models hits differently if you know the recent history of Japan's payment wars. PayPay seized the market through SoftBank's massive cashback campaigns, and the ultimate goal of that battle was never payments per se. It was about pulling users into other services within the ecosystem. PayPay has since evolved into a full-scale financial super app spanning cards, banking, brokerage, and insurance. When Yoshida said that wallet dwell time is the real battleground, he was signaling his intent to follow exactly this precedent. The question is whether HashPort Wallet can retain funds on an ongoing basis, rather than riding a one-time wave of attention around the JPYC launch, given that PayPay already commands 70 million users and a well-established financial ecosystem.

Panelist: Noritaka Okabe(JPYC inc.), Pina Hirano(Asteria Corporation) / Moderator: Iwao Nakayama(Asteria Corporation)

Pina Hirano of Asteria opened the session by asking the audience for a show of hands.

"How many of you believe there will come a day when on-chain payments are taken for granted?"

About half the room raised their hands. Hirano traced Bitcoin's origins back to the very first line of Satoshi Nakamoto's white paper, "A Peer-to-Peer Electronic Cash System," then noted that price volatility turned out to be a fundamental barrier, preventing Bitcoin from ever gaining wide adoption as a payment method and making it unusable in corporate accounting. This was what led him to establish the Japan Blockchain Promotion Association (BCCC) in 2016 and to begin stablecoin proof-of-concept testing in 2017. But he was also clear that the arrival of stablecoins alone does not automatically lead to enterprise adoption.

Hirano laid out seven barriers that companies face when trying to adopt stablecoins: wallet management, approval authority, counterparty management, gas fees, integration with legacy systems, on-site usability, and auditing and internal controls. JPYC Gateway, he explained, is an attempt to resolve all of these through a single piece of infrastructure. The idea is to connect JPYC to Asteria's data integration middleware, Warp, so that JPYC becomes accessible from anywhere within a company's ERP, accounting, or treasury management systems.

Then Hirano went further. He announced that Asteria would hold one billion yen worth of JPYC, roughly one-third of the company's three billion yen in cash, and use it for actual payments and receipts. The session moderator, Nakayama, Asteria's CXO, half-jokingly asked, "As an employee, I'm a little worried. One billion out of three billion, is that really okay?" Hirano's response was that JPYC is not algorithmic; it is properly backed by reserves, so the risk is manageable. He then pointed out that whenever a CFO at a Japanese company evaluates a new technology, the first question is always, "Is anyone else using it?" Japanese companies almost never volunteer to go first. His intention, therefore, was to create the very first case of a Tokyo Stock Exchange Prime-listed company holding a third of its cash reserves in stablecoins.

Noritaka Okabe of JPYC said that market sentiment changed completely once the company received its official registration. Hirano echoed this, recalling that despite having championed stablecoins since 2017, he kept hearing "How much longer are you going to keep doing this?" from shareholders. But after JPYC obtained its registration and began issuance, the atmosphere shifted entirely. Government officials, Hirano noted, now bring up stablecoins every chance they get. Okabe also disclosed that JPYC had raised approximately 1.78 billion yen in a Series B round led by Asteria. The investor roster was notably diverse, including CVC arms from regional banks, JR West Innovations, a Meiji Yasuda Life Insurance-affiliated fund, bitFlyer Holdings, and fundnote, spanning banking, insurance, railways, crypto exchanges, and venture capital.

Okabe presented a striking figure: yen-denominated stablecoins currently account for just 0.01% of the global stablecoin market. Unless that share can be pushed to at least 10%, he said flatly, Japan is finished in the next economy. With China's stablecoin adoption stalled by capital outflow concerns, Japan stands as the Asian country that has moved fastest on regulation, accounting, and tax frameworks, positioning it to become a stablecoin hub. In discussions with the Financial Services Agency, he added, scenarios projecting Japan capturing up to 25% of the global market have been floated.

The second half of the session turned to the AI agent economy. Okabe shared that on Moltbook, an AI agent social network that has been gaining attention, instances of AI agents paying for services in JPYC have already appeared. He suggested that stablecoins might reach mainstream usage in AI agent ecosystems before they do among humans. Hirano picked up on Circle CEO Jeremy Allaire's prediction that billions of AI agents will transact in stablecoins, then pushed the vision even further. He forecast that the number of AI agents will exceed the human population, running transactions around the clock and generating an economy ten to a hundred times the scale of the human one.

To properly read Hirano's declaration that Asteria will hold one billion yen in JPYC, you first need to understand what kind of company Asteria is. Asteria Warp is a middleware product that has held the number one market share in Japan's EAI/ESB market for 19 consecutive years, enabling no-code data integration between disparate systems. When Hirano built the JPYC Gateway on top of Warp, the implication was not that a blockchain startup was getting into stablecoins. It was that an established enterprise middleware vendor was stepping into stablecoin distribution. Companies can now plug JPYC into their existing ERP and accounting systems without a single blockchain engineer, using no-code tools. The distribution channel and the self-holding announcement only become meaningful when taken together. A declaration that one company will use stablecoins is not enough on its own. The message has to be, "We are already using it, so you can too," delivered to a customer base of over 10,000 companies. That is how decisions actually get made in Japanese corporate culture.

One variable that this session did not address, but which directly shapes the presenters' strategies, is the movement of Japan's megabanks. MUFG, SMBC, and Mizuho are jointly preparing to issue stablecoins, with a target of one trillion yen in issuance within three years. The platform is MUFG's Progmat, supporting Ethereum, Polygon, Avalanche, and Cosmos. SMBC's Chief Digital Innovation Officer, Akio Isowa, has stated publicly that the banks want to avoid the fragmentation that plagued the early days of cashless payments, a remark that clearly references the QR payment wars of 2018 and 2019, when dozens of services flooded the market before PayPay ultimately captured most of it. From the banks' perspective, there is an urgency to establish a jointly governed standard before non-bank issuers like JPYC lock in a first-mover advantage.

This means that the strategy pursued by Asteria and JPYC is, at its core, a race against time. Securing Asteria Warp as a distribution channel is a strong opening move. But when a megabank consortium backed by 300,000 corporate clients and direct FSA support enters the field, the remaining question is how a non-bank issuer defends its position.

On the AI agent economy, the path to realization is not yet concrete enough, given that we are still at the experimental stage. Large-scale use cases for agentic payment protocols like x402 have yet to materialize. That said, the recognition that existing payment infrastructure lacks the speed and programmability to handle machine-to-machine transactions appears to be shared widely, across both banks and non-banks alike. The problem itself is real.

Panelist: Hajime Ikeda(Nomura Holdings, Inc./Senior Managing Director), Atsushi Itaya(Daiwa Securities Co. Ltd.), Mitsunori Yuasa(Franklin Templeton Japan), Yuki Tanaka(BlackRock) / Moderator: Tatsuya Saito(Progmat, Inc.)

This session approached onchain finance not as an alternative financial system emerging from crypto, but as a shift toward redesigning existing securities and asset management infrastructure on blockchain. Under the premise that the intersection of cross border payments and securities settlement represents the core of onchain finance, the discussion focused on the structural differences between the Japanese and US markets and how Japan is approaching the transition to onchain finance.

Yuki Tanaka of BlackRock explained the development of tokenized money market funds (MMFs) in three stages. The first stage is as a yield generating alternative that absorbs liquidity from stablecoins that do not provide returns. The second stage is their use as collateral assets in DeFi. The third stage is their use in trading and settlement within traditional financial systems. He emphasized that the foundation of all these stages is the currency used for settlement, namely stablecoins. For onchain capital markets to function, not only assets but also settlement instruments must exist onchain.

Mitsunori Yuasa of Franklin Templeton explained that tokenized MMFs will eventually expand into the tokenization of various funds and financial assets. Investors will be able to manage assets from multiple financial institutions more transparently within a single wallet, and asset information that has traditionally been fragmented across financial institutions may become interconnected on a shared infrastructure.

Hajime Ikeda of Nomura described the distinctive feature of the Japanese tokenization market as its retail oriented approach centered on real estate. He noted that an important change was opening access to private assets, which were previously available only to institutional investors, to individual investors. However, he explained that tokenization aimed at upgrading the entire trading and settlement infrastructure of existing financial products, as seen in overseas markets, is only now beginning to develop in Japan.

Atsushi Itaya of Daiwa Securities characterized the difference between Japan and the United States not as a matter of speed but as a structural difference in the market. In the United States, securities account for a large share of household financial assets, which has led tokenization to develop first as a means of improving capital market efficiency. In Japan, however, participation in asset management has historically been lower, so the early development of tokenization has focused on fractionalizing investment assets such as real estate to broaden retail investor access.

In the latter part of the session, participants shared the view that many aspects of onchain finance are still close to the experimental stage. Questions remain about which settlement tokens are most suitable for securities settlement, how operational and redemption structures should be designed, and how to address issues such as 24 hour market operations and AML and KYC compliance. These challenges are currently being explored through various pilot implementations. It was also noted that in addition to dollar denominated stablecoins, infrastructure for yen denominated stablecoins will need to be developed for Japan’s financial sector to play a meaningful role in global onchain networks.

Overall, the session emphasized viewing onchain finance not as a technology that replaces traditional finance but as an infrastructure shift that expands the available set of financial options. If records of assets are stored on public blockchains, they can become a single and reliable source of truth, potentially enabling assets that were previously difficult to trade to connect with broader markets. The overall message was that onchain finance is not about displacing existing financial systems but about expanding the scope and depth of financial markets.

The key insight from this session is that onchain finance represents an important technological foundation that can expand the capabilities of traditional finance. There is often a misconception that onchain finance will radically replace existing financial systems, and in some cases traditional financial institutions, particularly in the United States, have resisted the development of onchain finance in order to protect existing structures.

However, the transition toward onchain finance is ultimately an inevitable trend. Blockchain technology has the potential to replace outdated financial infrastructure. Rather than taking business opportunities away from traditional finance, it can provide opportunities to expand financial activities across time and geography.

The session also discussed the gap between the United States and Japan in the development of onchain finance. Japan introduced regulatory clarity for security tokens in 2020 and for stablecoins in 2022, demonstrating relatively advanced regulatory progress not only within Asia but also globally. From a regulatory perspective, the gap with the United States is therefore not necessarily large. However, in terms of industry scale, there remains a significant difference between the two markets. It is therefore an important moment to observe whether blockchain technology can be effectively integrated in Japan to significantly expand the scope of its existing financial system.

Panelist: Akio Isowa(SUMITOMO MITSUI FINANCIAL GROUP), Nobuhiro Kaminoyama(Mizuho Financial Group, Inc.), Takayuki Noro(Mitsubishi UFJ Financial Group, Inc.) / Moderator: Tomohiro Miura(Financial Services Agency)

This session focused on how Japan’s three megabanks are responding to technological shifts such as stablecoins, blockchain, and AI. The discussion began from the premise that the overall direction of change has already been established. The key question is no longer whether new technologies will emerge, but how financial institutions prioritize them and embed them into actual financial operations through organizational structure and strategy.

Tomohiro Miura of the Financial Services Agency opened the discussion by asking how megabanks view the future of finance amid rising interest rates, demographic decline, and accelerating digital transformation. While Japan’s financial system has maintained a relatively stable structure for a long time, the panel acknowledged that multiple structural changes are now occurring simultaneously.

Akio Isowa of SMBC explained that in the past, existing payment infrastructure such as the Zengin network was so strong that blockchain did not significantly disrupt the core of financial services. Recently, however, the combination of AI and blockchain has begun to make the concept of programmable money more realistic. Within SMBC, dozens of experimental projects centered on AI have been conducted. These include AI systems trained on the president’s speeches, AI powered call centers, and company wide data restructuring efforts that are now moving from experimentation to practical deployment.

Nobuhiro Kaminoyama of Mizuho explained that his title changed from CDO to CDTO because organizational transformation is more important than digitalization itself. He emphasized that the most serious challenge is not technology but demographics. With an aging workforce and the prospect of large scale employee departures, he warned that if operational models are not transformed within the next five years, the current business model may become unsustainable. AI is viewed as a key tool for productivity transformation, although applying it to customer facing operations is much more difficult than expected.

Takayuki Noro of MUFG suggested that the identity of banks may gradually shift from financial service providers to financial infrastructure providers. Stablecoins and tokenized deposits can serve as strategic tools to defend against deposit outflows, provide trust layers such as KYC and AML, and enable 24 hour services and programmable finance. He referenced the experience of underestimating the early expansion of QR payments and having to catch up later, emphasizing that the bank does not intend to miss the next transformation in payment infrastructure.

In the latter part of the session, regulatory developments and pilot experiments were also discussed. Demonstration projects related to stablecoins, legal amendments, tax policy changes, and the introduction of crypto asset brokerage services all indicate that the institutional environment surrounding digital assets is actively evolving. Panelists emphasized that optimizing a single technology alone is insufficient. Financial innovation requires alignment between customer convenience, provider efficiency, and infrastructure stability.

An especially interesting topic raised during the discussion was the emergence of an AI agent economy. Observations were shared that in some stablecoin transactions, AI agents are already more active than human participants. This raises questions because current legal, tax, and consumer protection frameworks are largely designed around transactions between humans. As AI agents increasingly become participants in contracts and payments, policymakers may need to address how such activities should be regulated.

The overarching message of the session was that bank innovation should not be about showcasing technology, but about maintaining trust and intermediation within the financial system. Stablecoins and blockchain are not necessarily threats that replace banks, but rather catalysts that push banks to redefine their role within a new infrastructure environment. The discussion concluded with a shared view that a hybrid strategy, upgrading existing financial rails while simultaneously experimenting with new ones, represents the most realistic approach.

This session brought together representatives from Japan’s three largest banks. What was particularly striking was that, contrary to the common perception that Japanese megabanks are highly conservative, the themes of change and AI appeared repeatedly throughout the discussion.

Blockchain represents an entirely new form of financial infrastructure. If traditional financial institutions fail to adopt it, they risk falling behind. The discussion showed that even Japan’s large and traditionally conservative banks are well aware of this reality and recognize the need to adapt to emerging technological trends. MUFG, for example, is actively involved in the development of the Progmat platform.

Another interesting aspect is that Japan is one of the few countries simultaneously pursuing both stablecoins and tokenized deposits. While stablecoins are often perceived as a channel that could accelerate deposit outflows, Japanese banks are taking a more proactive approach. They are exploring the issuance of bank backed stablecoins and the development of tokenized deposits as a way to defend and retain deposits within the banking system.

The rise of AI is another development that deserves close attention. Given the current trajectory, there is little doubt that an AI agent economy will operate on blockchain based infrastructure. All three banks clearly recognize the organizational and industrial changes that AI may bring, and they expressed a strong view that the role of banks may evolve from providing financial services toward operating financial infrastructure.

Panelist: Nischint Sanghavi(Visa), Fernando Vazquez(Chainlink Labs), Hitoshi Harada(Alpaca) / Moderator: Angelina Kwan(Stratford Finance)

This session began by defining the “scaling” of DeFi not simply as an increase in total value locked (TVL), but as the process of becoming mainstream financial infrastructure equipped with regulation, licensing, governance, and risk management. The moderator opened the discussion by asking what is already functioning in practice and what factors are still preventing DeFi from reaching larger scale.

Nischint Sanghavi of Visa identified onramps and offramps as the key drivers of expansion. Onramps refer to the pathways that allow users to move from traditional fiat currencies into stablecoins or crypto assets, while offramps enable users to spend their crypto holdings at Visa merchants. Visa has been gradually building the infrastructure for this transition through card integrations, stablecoin settlement mechanisms, and payment network connectivity. According to Sanghavi, true scaling occurs when these processes are integrated into the payment experience to the point where users do not even need to be aware that they are using crypto.

Fernando Vazquez of Chainlink emphasized the conditions necessary for DeFi to connect with traditional finance. Early DeFi systems did not place strong emphasis on elements such as privacy, regulatory compliance, or investor suitability. However, attracting traditional financial institutions such as banks and broker dealers requires compliance engines and privacy preserving structures. He also highlighted the importance of interoperability across blockchains and the development of integration layers that allow legacy financial infrastructure and blockchain systems to operate together.

Hitoshi Harada of Alpaca noted that stablecoins are already functioning in real financial use cases. There are emerging examples of stablecoins being used in US securities trading, and tokenized stocks and tokenized assets are no longer theoretical concepts but are actively being tested in real markets. In this process, the boundaries between securities firms and crypto companies are gradually becoming less distinct.

The discussion also highlighted several concrete examples of DeFi expansion, including tokenized equities, tokenized funds, securities lending markets, the use of stablecoins within bank accounts, and B2B transfers between large corporations. As the number of blockchain networks grows, simple bridging mechanisms alone are no longer sufficient. Infrastructure that connects transfer agent functions and compliance logic across chains will be required.

In the latter part of the session, panelists repeatedly emphasized that the main bottleneck for DeFi expansion is not technology but regulatory compliance and legal interoperability. Technical interoperability across chains is gradually improving, but navigating differing legal frameworks across jurisdictions remains significantly more difficult. The panel suggested that common standards, reserve asset requirements, regulatory harmonization, and automated compliance engines will become critical components of future financial infrastructure.

Finally, the panel emphasized that the expectations of digitally native generations for instant and seamless experiences are increasingly shaping financial services as well. Adoption may accelerate faster than expected, and the ultimate success of DeFi will depend on the alignment of regulatory compliance, user experience, and connectivity with existing financial rails. The session concluded with the view that a future in which stablecoins are naturally used for everyday payments and peer to peer transfers is entirely plausible.

DeFi is increasingly expanding into the regulatory domain. One example is Visa, which processed approximately $4.5 billion in stablecoin payments in 2025. Securitize has tokenized roughly $3.3 billion worth of assets, while Chainlink provides compliance focused infrastructure such as ACE (Automated Compliance Engine), which enables compliance features to be embedded directly into smart contracts, as well as CCID (Cross Chain Identity), an onchain identity verification system.

While onchain finance has so far expanded primarily through retail driven adoption, the participation of financial institutions is likely to accelerate the growth of the onchain ecosystem at an unprecedented pace. Compliance will be the most critical factor in this transition. As mentioned during the session, the main bottleneck for the growth of onchain finance is not technology but regulation. Many financial institutions and onchain platforms are currently developing initiatives that allow smart contracts to comply with national legal and regulatory frameworks. However, these systems remain fragmented across jurisdictions and platforms.

Going forward, the onchain financial ecosystem will likely see more examples of platforms such as Securitize and Canton that integrate regulatory compliance natively into their infrastructure. At the same time, existing crypto native players such as Uniswap, Chainlink, and Aave are also expected to increasingly offer institution focused onchain financial services.

Speaker: Ryo Sakai(WebX)

The closing of the event was delivered by Ryo Sakai of CoinPost. He began by noting that he may not possess the same level of detailed technical knowledge as many of the experts in the industry, but the direction of change that digital currencies and stablecoins will bring is becoming increasingly clear. He emphasized that this transformation will not be created by a single company or a small group of experts, but by the people gathered at the conference working together through execution and collaboration.

Sakai pointed out that the stablecoin market has grown nearly seventyfold compared with about six years ago, explaining that what is happening now is not simply a passing trend but a structural transformation of the financial system itself. As the industry grows, new challenges and issues inevitably emerge, which is why it is important to maintain forums where these discussions can continue.

He also outlined the future direction of CoinPost. CoinPost began as a media platform in 2018 and launched the large scale conference WebX in 2023. Going forward, the organization plans to expand the industry ecosystem by operating both online media and offline events together.

The next event was also announced. WebX will be held again at the same venue from July 13 to July 14, 2026. Sakai expressed hope that the discussions and business ideas that emerged during MoneyX will continue to develop into more concrete initiatives at that event. He concluded by expressing his hope that the conference encouraged participants to view new technologies and business opportunities with a more forward looking perspective, closing the event with a commitment to grow the industry together.

As a research firm based in Korea, Japan is both geographically close and psychologically distant. While the two countries are located very near each other, Japan’s blockchain industry has often appeared somewhat removed from the broader dynamics of the global blockchain market.

However, through Four Pillars participating in MoneyX as the exclusive research partner, it became clear that in terms of the intersection between traditional finance and onchain finance, the Japanese market is moving along a trajectory similar to the global market. In some aspects, it may even be ahead.

Based on the discussions across the sessions above, several key insights about the Japanese market can be identified:

Multi money coexistence: The prevailing consensus in Japan’s financial market is that CBDCs, tokenized deposits, and stablecoins will not compete as substitutes but will instead play complementary roles. This concept was described using the term “connected money.” The key competitive question therefore shifts away from which form of digital money will dominate, toward how different types of digital currencies can be interconnected and how final settlement will ultimately be defined.

Production phase: The Japanese market has now moved beyond a stage where regulation primarily restricts activity and into a stage where actual products are emerging. In other words, the environment is no longer defined only by regulatory frameworks. Real world implementations such as JPYC and Progmat have begun to appear.

Compliance first approach: Unlike the global onchain ecosystem, which initially grew in regulatory gray areas, Japan has attempted to embed compliance directly into onchain systems from the beginning. The main bottleneck to institutional adoption is widely recognized as compliance rather than technology. As a result, there is a clear direction toward building standardized infrastructure that integrates compliance throughout the entire lifecycle of issuance, management, and redemption.

Focus on UI and UX: Japan has traditionally been strong in attention to detail. The goal is not simply to introduce stablecoins into payment systems. Instead, there is a clear focus on designing retail payment experiences where users may not even realize that stablecoins or blockchain technology are being used behind the scenes.

Allowance of dollar stablecoins: Unlike many other jurisdictions, Japan is showing signs of actively allowing not only yen denominated stablecoins but also dollar stablecoins such as USDC. If this combination becomes established, Japan could gain a strategic advantage not only in domestic payments but also within the emerging onchain foreign exchange layer.

AI agent economy: Similar to trends in the global market, Japan is also considering the AI agent economy as one of the strongest reasons for adopting stablecoins.

Progressive banking sector: Japan’s megabanks do not view stablecoins primarily as a threat but rather as an opportunity. By internalizing stablecoin related capabilities, they are exploring a strategic transformation of financial infrastructure.

The time for execution has arrived. The key question now is whether Japan’s large financial system can successfully transition onto onchain infrastructure on the basis of clear regulatory frameworks.

Dive into 'Narratives' that will be important in the next year