In March 2026, Mastercard acquired stablecoin infrastructure company BVNK for up to $1.8B. This is the largest stablecoin infrastructure M&A deal to date, surpassing Stripe's $1.1B acquisition of Bridge.

In 2025, stablecoin transfer volume reached $33T, roughly twice Visa's annual processing volume ($16.7T). While most of this is still trading settlement, cross-border remittances and B2B payments are expanding at a CAGR of 72%. Traditional card networks find their rationale for entering crypto in the need to absorb this payment flow.

Mastercard's crypto business is unfolding across three axes that cover the full spectrum of payment flows. First, it leverages its existing network of 150M merchant locations as a touchpoint for stablecoin payments through crypto wallet-linked cards. Second, it is building tokenized deposit settlement infrastructure for banks and institutions through its proprietary permissioned blockchain, Multi-Token Network (MTN). Third, through the BVNK acquisition, it secures public blockchain-based commercial payment infrastructure (stablecoin-to-fiat conversion, cross-border payouts, enterprise wallets).

The BVNK acquisition cannot be explained by technology alone. This deal brought in a license network spanning 130 countries, fiat banking partnerships, and an already-validated enterprise client base (Worldpay, Deel, Flywire, etc.) all at once. It shows that in the stablecoin infrastructure market, the moat is formed not only by the technology stack but also by the bundle of country-specific licenses and compliance.

Source: Mastercard

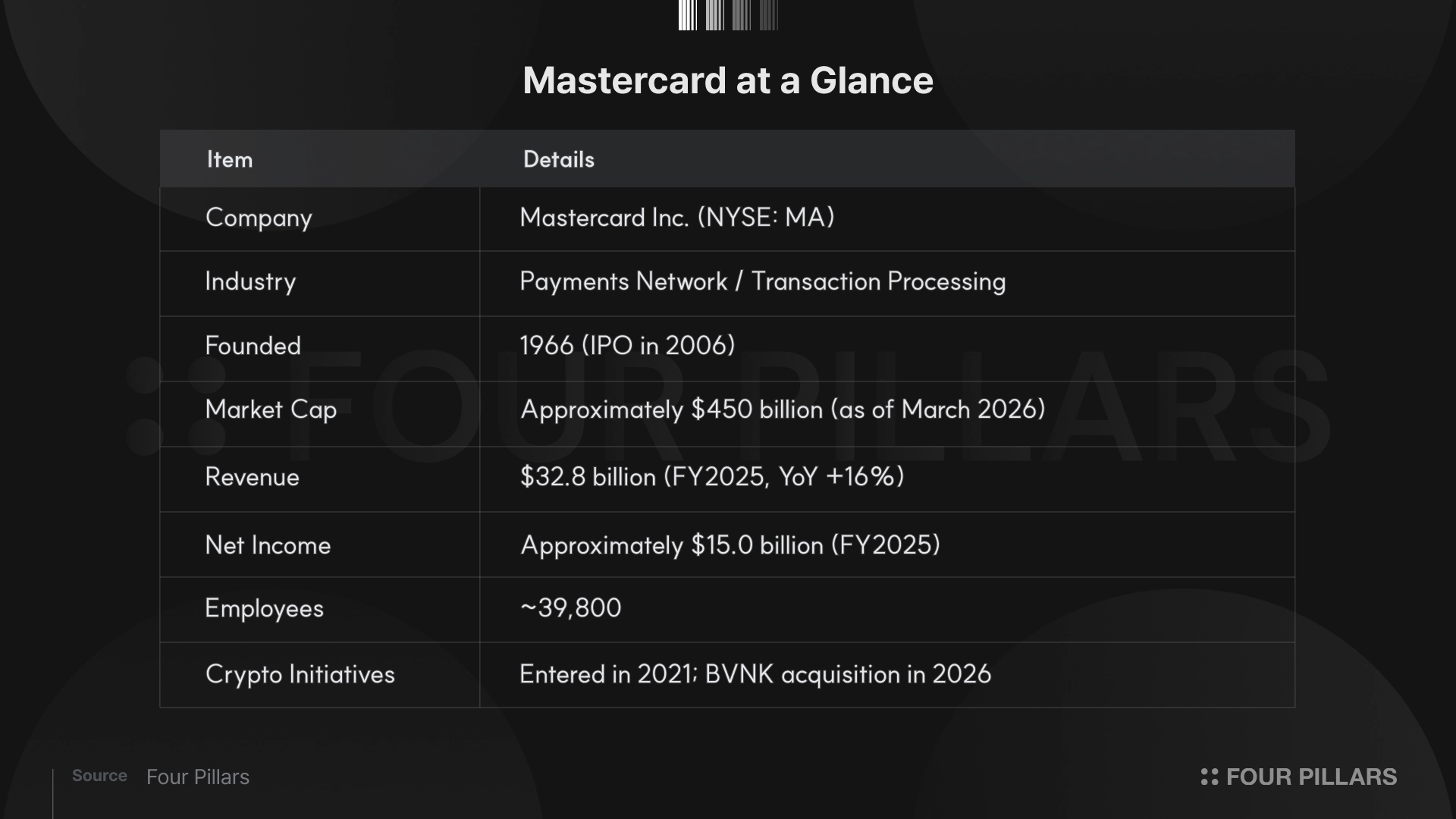

Mastercard is the world's second-largest payment network, founded in 1966, with over 3.5B cards in circulation across more than 200 countries. With FY2025 annual revenue of $32.8B and a market capitalization of about $450B, it ranks among the global top 20 by market cap. It maintains a net profit margin of 46% through a tollbooth model that intermediates transactions between card-issuing banks and merchant-side banks and collects fees.

Mastercard's crypto journey began in 2021 with the announcement of direct support for cryptocurrency networks. Since then, it has sequentially rolled out crypto cards, a proprietary permissioned blockchain (Multi-Token Network), and stablecoin network integration. As of 2025, it has moved beyond the exploration phase into execution. On March 17, 2026, it announced the acquisition of stablecoin infrastructure company BVNK for up to $1.8B.

This article analyzes Mastercard's crypto business strategy and the implications of the BVNK acquisition. It also draws lessons that companies considering crypto market entry can reference, particularly regarding the criteria for Build vs. Buy decisions and the meaning of the license moat.

Mastercard is a global network operator that connects payments across commerce worldwide.

Mastercard's market capitalization is about $450B as of March 2026, placing it second in the global payments industry behind Visa. It stands at roughly 85% of Visa's $540B market cap. However, Mastercard (+16%) has consistently outpaced Visa (+12%) in revenue growth, and its relatively smaller scale serves as a structural advantage in growth rate terms.

Mastercard holds a distinctive position in the payments industry. Its core business is operating the network that intermediates payments between card-issuing banks (Issuers) and merchant-side banks (Acquirers). Its net profit margin is about 46%, a global top-tier level. Through a platform model that collects per-transaction fees, it generates stable cash flows with every transaction processed.

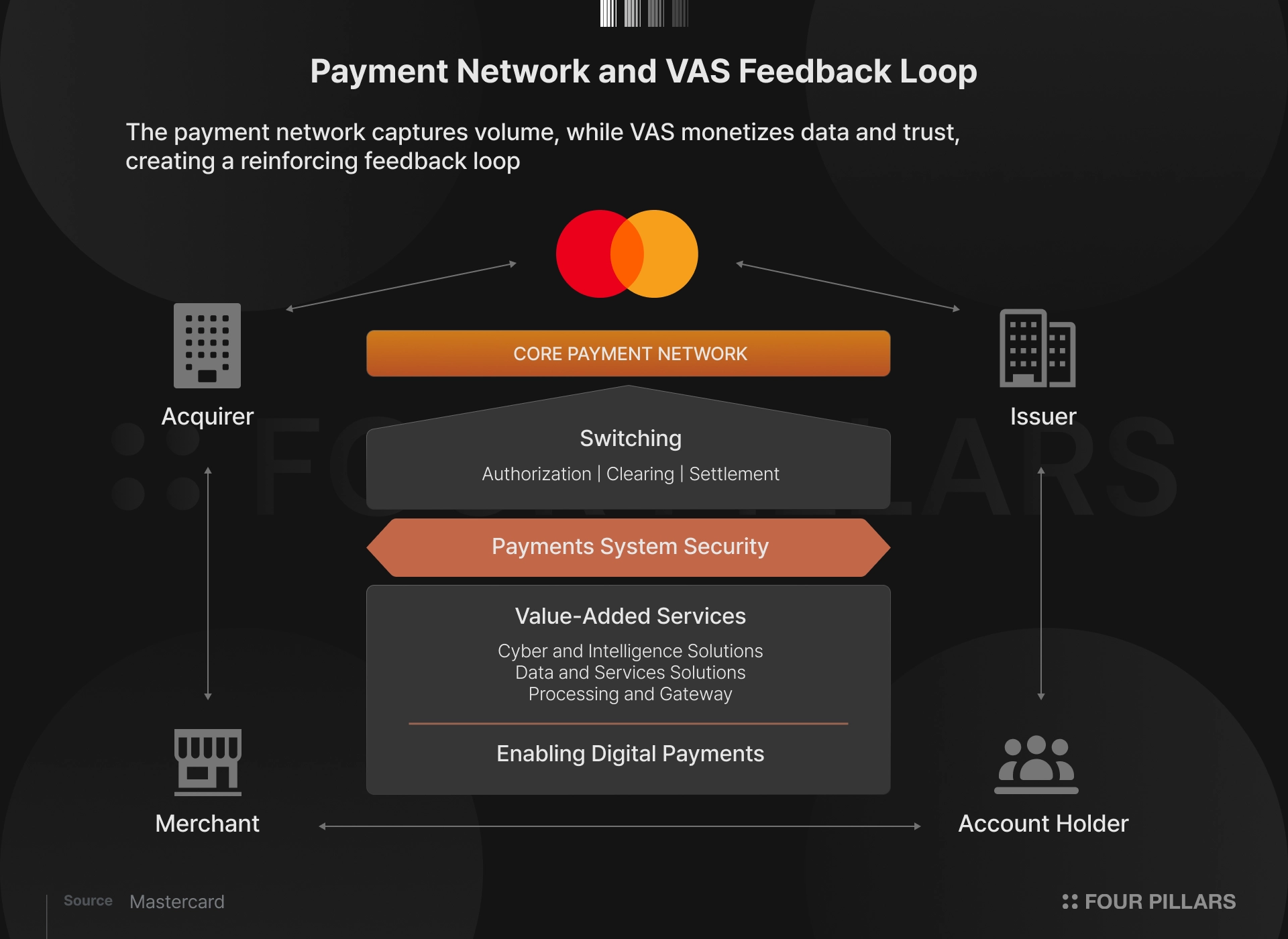

Mastercard's business, which generated annual revenue of $32.8B (FY2025), divides into two axes. One is the Payment Network at $19.5B in revenue, and the other is Value-Added Services (VAS) at $13.3B in revenue.

1.2.1 Payment Network: The Structure of the Tollbooth Model

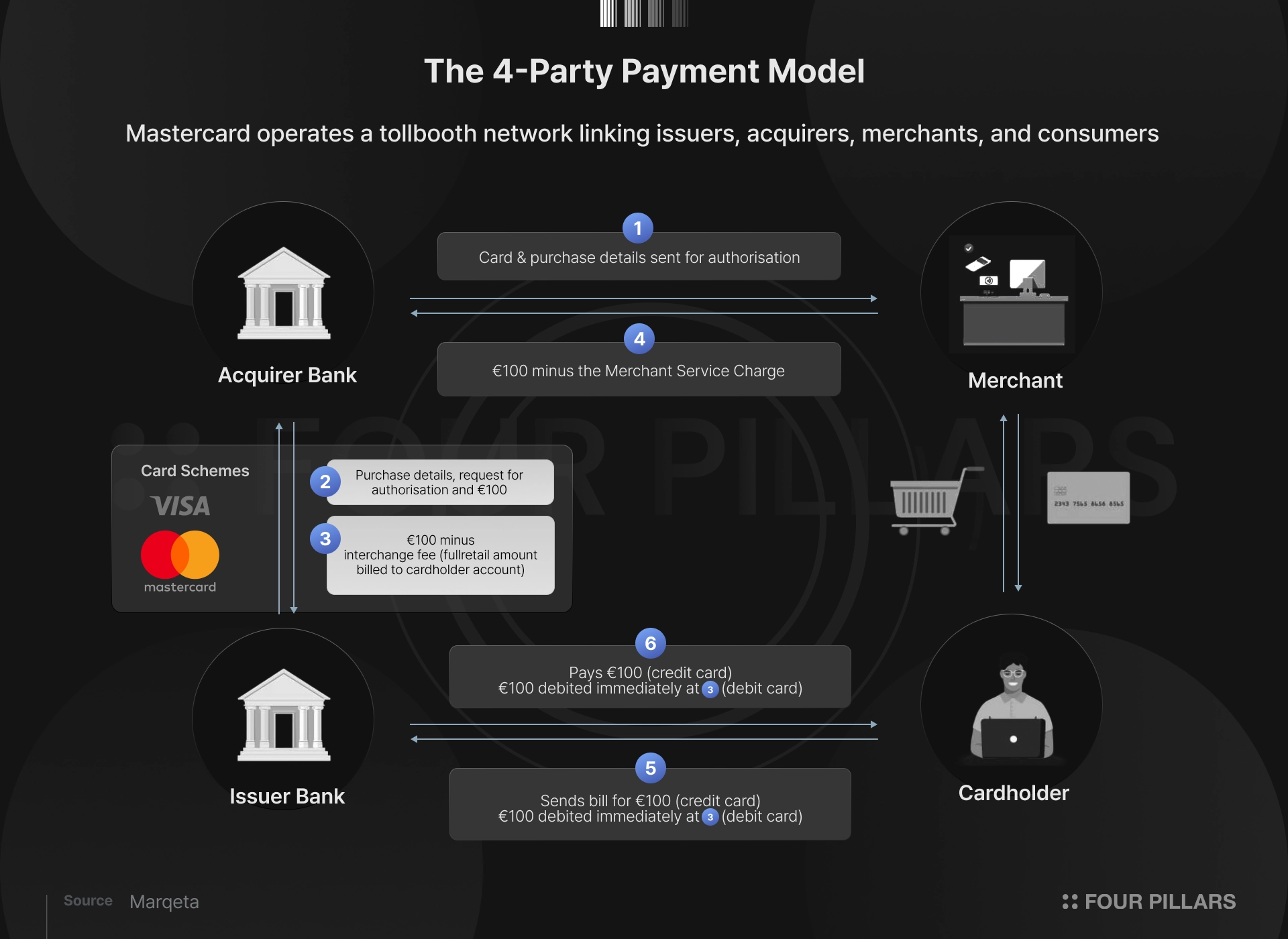

This is the most core network operations segment. Mastercard's specific role is to intermediate the four-party structure linking consumers, issuing banks (Issuers), acquiring banks (Acquirers), and merchants through its network.

When a consumer swipes a card, the Mastercard network processes three stages: Authorization, Clearing, and Settlement, collecting fees tied to transaction volume. As of 2025, total payment volume passing through the Mastercard network was $10.6T, with about 160B transactions processed annually. From these transactions, Mastercard generates roughly KRW 200T in revenue from network fees alone (net several bps) that it directly collects.

The payment network revenue consists of three components.

Domestic Assessment: Fees charged on Gross Dollar Volume (GDV) of Mastercard card payments within each country

Cross-Border Volume Fee: Fees charged on cross-border transactions where the card-issuing country and payment country differ. The per-transaction rate is higher than domestic payments, making this a significant contributor to overall profitability

Switching Fee: Per-transaction fees charged for the switching services that process authorization, clearing, and settlement of individual transactions

The key competitive strength of this structure is the two-sided network effect. The more merchants accept Mastercard, the more consumers choose it, and the more consumers use it, the more merchants accept it. Currently, over 3.5B Mastercard-branded cards are in circulation worldwide, and over 150M merchant locations accept Mastercard. Together with Visa, the two hold over 90% of the global card payment market in a duopoly structure built on this network effect.

1.2.2 Value-Added Services (VAS): The Second Axis Monetizing Data and Intelligence

VAS grew 44% in two years, from $9.2B in 2023 to $13.3B in 2025, with a 26% year-over-year increase in Q4 2025. Its growth rate consistently outpaces payment network revenue (+12-16%), and it accounts for about 40% of total revenue. As pressure on network fees intensifies, Mastercard's business center of gravity is shifting toward expanding the VAS revenue share.

The detailed composition of VAS is as follows:

Cybersecurity & Fraud: A major axis of VAS. Decision Intelligence Pro analyzesMs of data points per transaction within 50 milliseconds to determine fraud. In 2024, Mastercard acquired Recorded Future for $2.65B, adding cyber threat intelligence capabilities. AI-based fraud detection accuracy improved over 40% year-over-year.

Data Analytics & Consulting: Based on 160B annual transaction data points, it provides consumer spending insights, market analysis, and campaign performance measurement services to banks and enterprises. Mastercard Commerce Media, launched in October 2025, is a digital advertising network connecting 500M consent-based consumer data points with 25,000 merchant advertisers, reportedly delivering up to 22x return on ad spend.

Open Banking: Through the 2020 acquisitions of Finicity and Europe's Aiia, Mastercard built an open banking platform. It provides consumer-consent-based financial data sharing, account-based payment initiation, and transaction history analysis for credit assessment.

Commercial Payments (Commercial & New Payment Flows): A business targeting the B2B payments space. Virtual Card Number (VCN)-based enterprise spend management, Commercial Connect API (embedding payments in ERPs like SAP Concur), and Mastercard Move (cross-border payouts) belong to this segment.

Loyalty & Marketing: Provides reward program design for card issuers, merchant-linked benefits, and consumer engagement platforms.

If the payment network is a platform that generates fees tied to transaction volume, VAS is the layer that monetizes data and trust on top of that platform. The two businesses are mutually reinforcing. Fraud patterns are extracted from 160B annual transactions to build security services, those security services raise the network's trust level, and that trust in turn drives more transactions into the network.

Mastercard is moving aggressively into crypto because stablecoins threaten the very rationale of card networks while simultaneously opening new markets that cards could never reach. This threat and opportunity break down into three paths: the scenario where card rails are bypassed in retail payments, the scenario where AI agents transact outside card networks, and the opportunity in markets cards never accessed, such as cross-border remittances.

2.1.1 Retail Commerce Could Be Replaced by Stablecoins

The growth of stablecoin payment volume is confirmed by the numbers. Stablecoin transfer volume in 2025 reached $33T, a 72% increase year-over-year, roughly twice Visa's annual processing volume ($16.7T). Stablecoin transfer volume, which was just $3.3B in 2018, grew 10,000x in seven years.

However, interpreting this figure directly as a crisis for card networks is excessive. About 70% of stablecoin transaction volume in 2024 was bot activity, and 90% of stablecoin volume was reportedly exchange-to-exchange settlement and DeFi transactions. Payments for services (the domain Visa/Mastercard processes) accounted for only about 10% of the total.

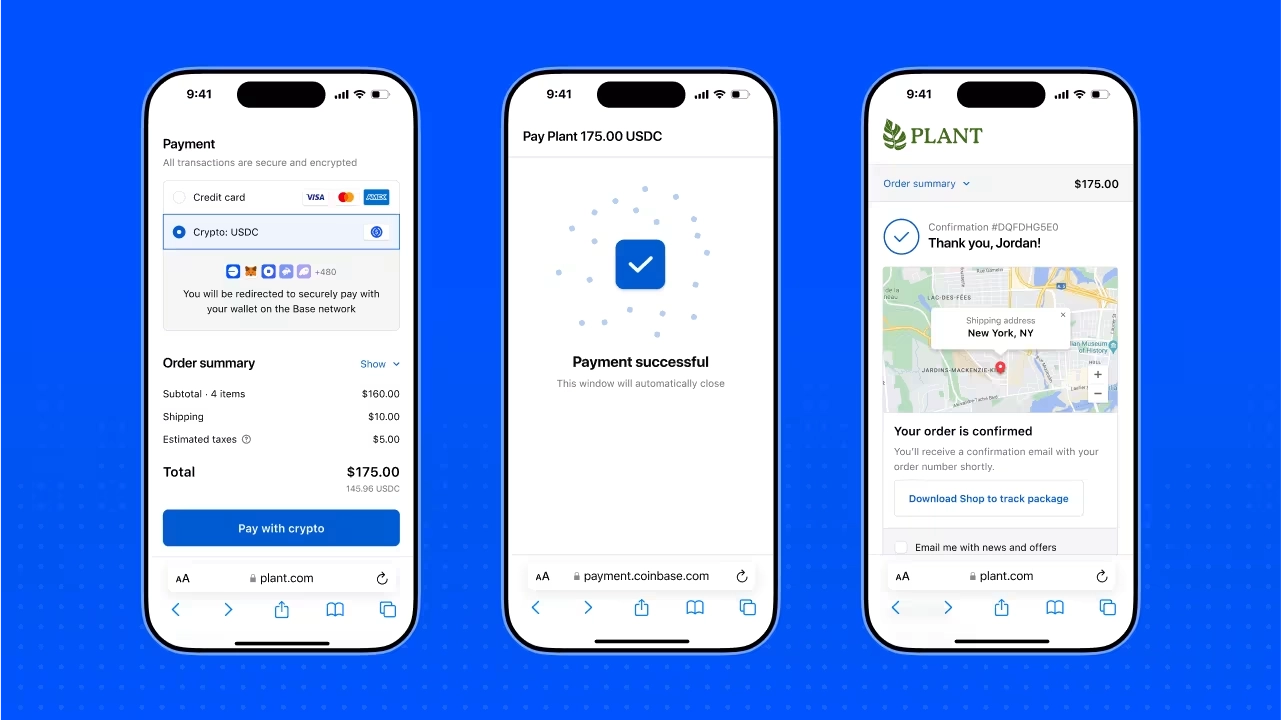

In the current transitional phase, card networks still function as intermediaries for stablecoin payments. When a user pays at a merchant with a crypto wallet-linked card, the Mastercard/Visa network processes authorization and settlement. The crypto balance is converted to fiat at the point of payment, and the merchant receives fiat just as before. In this structure, as stablecoin volume grows, transactions passing through the card network also grow. For card networks, this is a positive scenario.

However, the ultimate scenario is different. As stablecoin payments mature, a wallet-to-wallet structure becomes possible, where stablecoins transfer directly from the sender's wallet to the receiver's wallet. In this structure, card networks are not needed at all. From a purely technical standpoint, consumer protection, fraud prevention, and dispute resolution could also be replaced by smart contracts.

Source: Shopify

Coinbase Payments is the most direct example. Coinbase integrated with Shopify to enableMs of merchants to accept USDC payments directly without card networks. Settlement completes in about 200ms on Base, and the per-transaction cost is about 1 cent. Compared to card payments' 2-3% fees, this is a significantly cheaper rail. Coinbase also built an open-source Commerce Payments Protocol on top, implementing traditional payment features like escrow, refunds, and subscription payments through smart contracts.

All of these movements represent scenarios where the value of the payment network Mastercard and Visa have built over decades is being challenged. Ultimately, in the process of onchain reshuffling of commerce infrastructure that card networks once provided, the metric Mastercard should watch is not total stablecoin volume. It is how fast the share of stablecoin payments that bypass card rails is growing.

2.1.2 AI Agent Payments

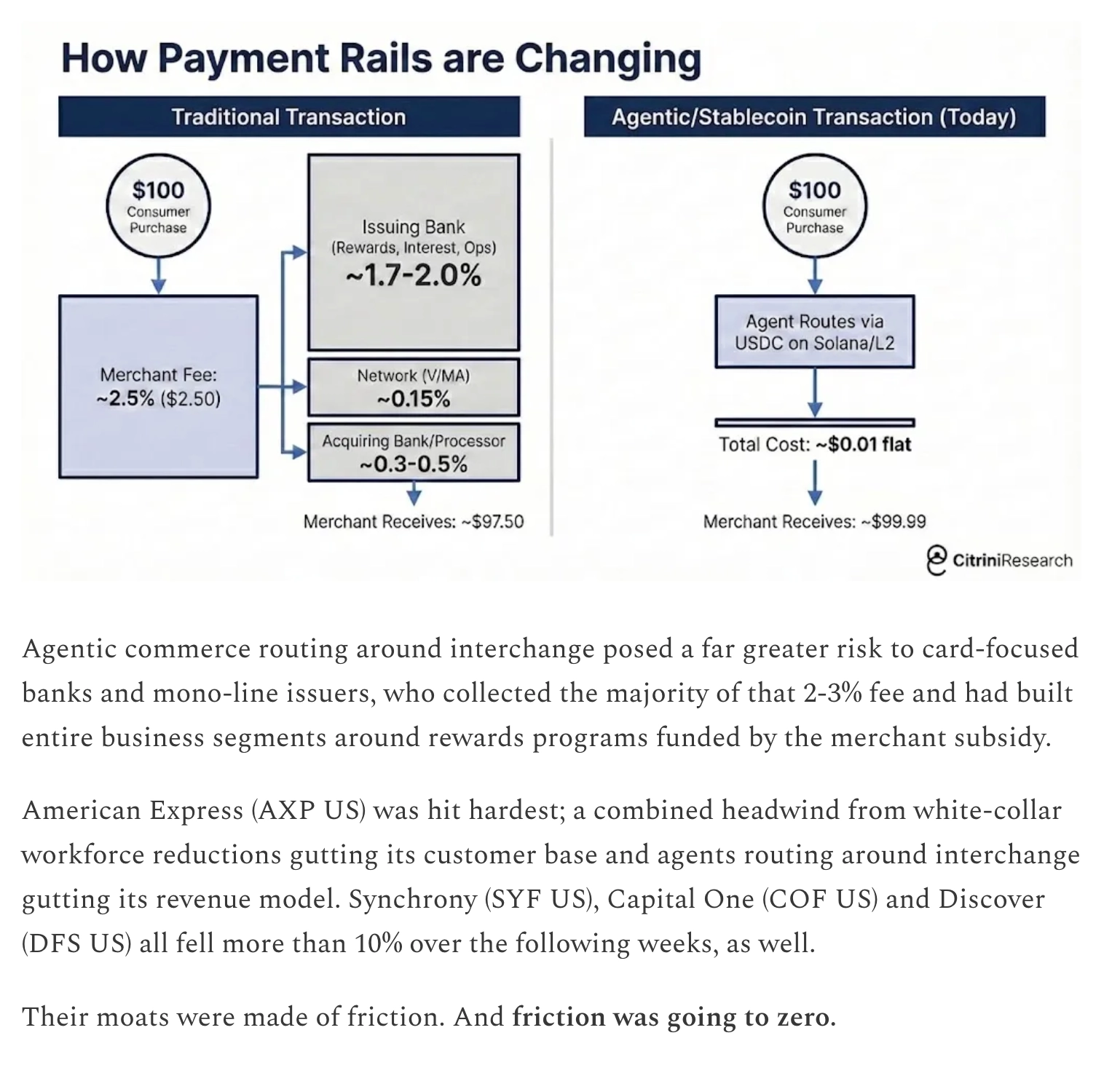

AI agent payments are also emerging as a new variable. The projection that AI agents will execute more transactions than humans no longer looks like an excessive forecast. AI agents cannot open bank accounts, but crypto wallets can be generated instantly with just a private key. Agent-to-agent transactions are mostly micropayments of a few cents per transaction, which card networks' minimum fee (about 30 cents) cannot handle. From the AI agent's perspective, card networks are not value-adding infrastructure but friction that only adds cost. Any rational agent would naturally bypass them.

Real products are already shipping. Coinbase's x402 protocol embeds stablecoin payments directly into HTTP requests, with Cloudflare, Circle, AWS, and Google supporting it. When an agent calls an API, payment executes simultaneously, making the card network's authorization-settlement process unnecessary.

Source: Citrini Research

The market is treating this scenario as credible. Citrini Research published a report titled "The 2028 Global Intelligence Crisis". It modeled a scenario where AI agents autonomously route payments to stablecoins on Solana/Ethereum L2 instead of card networks for cost optimization, diagnosing the inflection point as the moment Mastercard's Q1 2027 purchase volume growth decelerates from 5.9% YoY to 3.4%. As this report circulated, a sell-off of roughly $300B occurred, with Visa falling about 4%, Mastercard about 6%, and American Express about 8%.

Many assessments argue this reaction was excessive. The 2-3% interchange fee that AI agents would bypass is collected by the card-issuing bank, not by Visa/Mastercard. The card networks themselves take only a few bps per transaction, so the direct impact of stablecoin bypassing concentrates on issuing banks rather than on the networks. There is also a view that in the current stablecoin card structure where fiat conversion intervenes, card networks could be strengthened as the "last mile touchpoint" for stablecoins.

However, the question the market is asking remains valid. When the decision-making agent for transactions shifts from humans to software, the premises of existing business models must be re-examined.

2.1.3 New TAM: Markets Cards Never Reached

The picture is not all threat. There are also new markets that stablecoins open up. These are domains cards never accessed in the first place: cross-border B2B payments, overseas remittances, freelancer/creator payouts, and more.

These domains have always been handled by the SWIFT-based correspondent banking system, not by cards. Correspondent banks route transactions through 3-5 intermediary banks from the sender's bank to the receiver's bank, with each intermediary collecting fees and adding processing time. As a result, financial institutions collect an average of $20 in fees per cross-border payment, and settlement takes 3-5 days. Traditional banks tie up roughly $10T in accounts worldwide to support this system.

Stablecoins present the possibility of replacing correspondent banking in this domain. Real-time settlement (minutes), low fees (gas fee levels), programmable payment logic, and 24/7 operation make this possible.

For Mastercard, this domain is not a market being taken away by stablecoins. It is a new TAM that the existing card business could never address in the first place. Cards are infrastructure optimized for consumer-to-merchant payments, not a suitable tool for cross-border payments of $100,000+ between enterprises or payroll disbursements to thousands of overseas contractors. If Mastercard directly owns stablecoin rails, it can enter this market that was unreachable by cards. Among BVNK's clients acquired in this deal, Deel (global payroll), Worldpay (merchant cross-border settlement), and dLocal (emerging market payments) are players in precisely this TAM.

There are two reasons why Mastercard moved to fully operationalize its crypto strategy starting in 2025. One is that as the global regulatory environment became clear, the legal foundation was established for Mastercard's clients, banks and fintechs, to adopt stablecoin services. The other is that competitors like Stripe and Visa had already begun securing stablecoin infrastructure, creating competitive pressure that left Mastercard unable to remain on the sidelines. CEO Michael Miebach summarized the urgency of this transition by saying "the train is leaving the station."

2.2.1 The Turning Point in Regulatory Clarity

2025 was the year global stablecoin regulatory frameworks were formally established. As the US, EU, Hong Kong, and others finalized legal definitions for stablecoins, issuer requirements, and reserve regulations, companies moved from the stage of questioning the legality of stablecoin businesses to the stage of deciding which stablecoins to support and which partners to work with.

In the US, the GENIUS Act was signed in July 2025, establishing the first federal stablecoin regulatory framework. This law clarified three major points.

It defined stablecoins as a separate category of "payment stablecoins" rather than securities or commodities, removing them from SEC/CFTC jurisdiction. This allowed companies dealing with stablecoins to operate without the risk of securities law violations.

It opened pathways for both banks and non-banks to issue stablecoins through federal or state licenses.

It standardized issuer soundness standards by mandating 1:1 reserve requirements and monthly disclosure obligations.

The EU's MiCA and Hong Kong's Stablecoin Ordinance also came into effect around the same period. While the specific requirements differ, the direction converges in that all establish issuer authorization, reserve obligations, and disclosure frameworks. The meaning of this change is clear. Mastercard's clients, banks and fintechs, have moved past questioning the legality of stablecoin businesses to the stage of deciding which stablecoins to support and which partners to work with. If Mastercard has stablecoin infrastructure in place, it stands in a position to offer these clients immediately deployable, compliant solutions.

2.2.2 Competitive Pressure

Competitive pressure on Mastercard is coming from two directions simultaneously. One is Stripe from the PSP (Payment Service Provider) camp, and the other is Visa from the same card network camp. The nature of the threat differs between the two.

Stripe is a PSP, meaning it handles payment processing between merchants and consumers. It sits at a different layer in the payment stack from card networks. However, when Stripe acquired stablecoin infrastructure company Bridge for $1.1B in October 2024, it signaled that a PSP was beginning to build its own independent payment rail that bypasses card networks.

Stripe subsequently launched its own blockchain Tempo and began offering Stablecoin Financial Accounts in over 100 countries, pursuing vertical integration of stablecoin payments. If Stripe'sMs of merchants can directly accept stablecoin payments without card networks, the transactions passing through the Mastercard network could decline.

Visa is a card network like Mastercard, but it has moved one step ahead in the crypto space. It began USDC-based onchain settlement in 2023, and in 2025 expanded Solana/Ethereum-based stablecoin settlement to US banks.

Visa also holds over 90% market share in crypto card volume, with crypto-native card issuers like Rain and Reap building most of their programs on Visa rails. Visa was also the first to invest in BVNK. While Mastercard initially approached through exchanges like Binance and Bybit, Visa partnered with crypto-native card issuers first, gaining an edge in physical payment volume.

Had Mastercard not moved, a scenario could have formed where Stripe preempts stablecoin infrastructure in online payments while Visa completes crypto integration first within the card network domain. Given that network effects in the payments industry are difficult to reverse once formed, the importance of timing was no less significant than the maturity of the technology.

Mastercard's initial recognition of payment opportunities in crypto came relatively early. After an exploration phase centered on partnerships and pilots from 2021 onward, it transitioned to full-scale execution starting in 2025.

Mastercard does not maintain a separate legal entity for its crypto business, but the Blockchain & Digital Assets division operates under the direct reporting line of CPO Jorn Lambert. This division oversees the strategy and execution of all Mastercard crypto products. In 2025, Mastercard created a senior product role, Director of Crypto Flows, to consolidate three key mandates under a single position: stablecoin-linked card issuance, DeFi payment rail expansion, and Mastercard network acceptance of Web3 transactions.

Source: Mastercard

This organizational restructuring indicates that crypto has been elevated within Mastercard from an experimental initiative to a core product. From 2021 to 2024, crypto initiatives were conducted on a per-partnership and per-pilot basis, but from 2025, the company restructured leadership and organization to enter a phase of full-scale business execution. In March 2026, the Crypto Partner Program, which brings together over 100 crypto-native companies, payment processors, and financial institutions to co-design product direction for onchain payments, and the BVNK acquisition announcement were made in the same week. This reads in the same context.

3.1.1 2021-2024: The Exploration Phase

Mastercard's crypto business started with the February 2021 announcement that it would directly support crypto assets on its payment network. The crux of the announcement was a positioning focused solely on "digital assets for payment purposes." The plan was to integrate digital currencies with price stability and regulatory compliance into the network, not speculative crypto assets.

Subsequent early moves focused on broadening touchpoints with the crypto ecosystem.

2021: Partnered with Bakkt to lay the foundation for providing crypto services to all banks and merchants on the network

2022: Launched Crypto Source (crypto trading infrastructure for banks) with Paxos and entered an NFT payment partnership with Coinbase. Crypto Secure (AI-based onchain fraud detection) also launched in the same year

2023: Announced the Multi-Token Network (MTN) and started its first pilot in Hong Kong. Crypto Credential, which verifies counterparty identity in blockchain transactions and replaces wallet addresses with human-readable aliases, was also unveiled during this period

2024: Completed tokenized deposit and carbon credit trading pilots with Standard Chartered, and launched the first live P2P transaction of Crypto Credential for cross-border remittances between Latin America and Europe

During this period, Mastercard was centered on partnerships and pilots. Rather than deeply integrating crypto into its own network, it was in the phase of exploring where opportunities lay through various experiments.

3.1.2 2025: The Turning Point

2025 was the year Mastercard's crypto strategy shifted from exploration to execution, with several major initiatives running simultaneously.

Stablecoin End-to-End Support Declaration: In April 2025, Mastercard announced End-to-End stablecoin payment functionality enabling consumers to pay from crypto wallets and merchants to settle directly in stablecoins. Multiple stablecoins including USDC, PYUSD, USDG, and FIUSD were integrated into the network.

MTN Institutional Integration Acceleration: In 2025, MTN was integrated with JP Morgan Kinexys to support 24/7 enterprise-to-enterprise payments, and connected with Fiserv's Digital Asset Platform. Ondo Finance's tokenized US Treasuries (OUSG) were also onboarded to MTN, expanding beyond tokenized deposits into the RWA domain.

Paxos Stablecoin Consortium Participation: Mastercard joined the Paxos-led stablecoin consortium to build 24/7 settlement infrastructure supporting multiple stablecoins on MTN. In March 2026, it partnered with SoFi to support SoFiUSD, the first public blockchain-based stablecoin issued by a US-licensed bank, as an MTN settlement instrument.

All of these movements converged in March 2026. The Crypto Partner Program announcement and the BVNK acquisition announcement were made in the same week, as years of exploration culminated in the acquisition of the most critical infrastructure.

Mastercard's crypto products are divided into three layers: consumer-facing, infrastructure/protocol, and security/compliance. Each layer operates independently, but when combined, they form a structure that covers the full spectrum from consumer payments to institutional settlement.

3.2.1 Consumer-Facing

This segment leverages the 3.5B cards managed by existing card infrastructure as crypto touchpoints. Through partnerships with MetaMask, OKX, Kraken, Crypto.com, Bybit, Exodus, and others, it issues crypto wallet-linked cards and enables stablecoin payments at over 150M merchant locations. Crypto purchases via Mastercard are also supported on major exchanges including Binance, Bybit, and Coinbase.

The collaboration with Monavate (formerly Baanx) deserves particular attention. Monavate is a Crypto-as-a-Service (CaaS) platform building crypto card programs for major self-custody wallets, including MetaMask Card, Exodus Card, and 1inch Card, on Mastercard rails. When a user pays directly from a MetaMask wallet, Monavate converts stablecoins to fiat in real time and sends authorization to the merchant through the Mastercard network. Users maintain self-custody of their assets until the point of payment, and merchants settle in fiat just as with regular card payments.

3.2.2 Infrastructure/Protocol

This layer constitutes the foundational infrastructure for stablecoin payments. While the consumer-facing layer enabled crypto usage on top of card networks, the infrastructure layer is designed to cover payment flows beyond card networks.

Four products currently comprise this layer.

Multi-Token Network (MTN): Mastercard's proprietary permissioned blockchain, specialized for tokenized deposit and RWA settlement between institutions. It is designed so that banks can participate in tokenized payments through existing interfaces (cards, APIs) without building separate blockchain infrastructure. JP Morgan Kinexys, Fiserv, and Ondo Finance are integrated, and app developers such as Coadjute (real estate escrow automation) and Pairpoint (IoT payments) are also building services on MTN

Crypto Credential: Infrastructure that verifies counterparty identity and qualifications in blockchain transactions. It enables the use of human-readable aliases (e.g., user.mastercard) instead of wallet addresses and automatically confirms whether the receiving wallet supports the relevant digital asset and blockchain

Mastercard Move (Stablecoins): Added instant remittance functionality to stablecoin wallets on top of the existing cross-border payout platform

BVNK Acquisition: A stablecoin infrastructure platform covering the full range of payment domains, including on/off-ramps, cross-border payouts, and enterprise wallets

3.2.3 Security/Compliance

For stablecoin payments to scale, security and regulatory compliance at the level of existing card payments must be guaranteed. Mastercard is directly applying decades of accumulated capabilities in this area to crypto.

Crypto Secure: A tool extending Mastercard's cybersecurity and fraud prevention capabilities to onchain transactions. It enables partners to assess the risk of blockchain transactions in real time and proactively block suspicious transactions. The core design retrains machine learning-based fraud detection models previously used for card payments on onchain data.

Mastercard Threat Intelligence: A service combining Recorded Future's cyber threat intelligence with Mastercard's payment network data to proactively detect cybersecurity risks at banks and merchants. Through this, Mastercard is strengthening security capabilities not only for stablecoin payments but also for traditional payments, with AI-based fraud detection technology recording over 40% improvement in fraud detection rates year-over-year. The 2024 acquisition of Recorded Future for $2.65B was also a decision to strengthen security.

Payment Network Rules Update: The operational rules (dispute resolution, consumer protection, chargebacks, etc.) that banks, merchants, and partners participating in the Mastercard payment network must follow are being revised to accommodate onchain transactions. Through this, Mastercard's clear direction is to provide the same level of consumer protection for stablecoin payments as card payments.

Crypto business revenue is not yet reported as a separate line item. Mastercard reports crypto-related revenue within the Value-Added Services (VAS) segment and does not disclose the crypto share within VAS.

Of FY2025 annual revenue of $32.8B, VAS accounted for $13.3B, about 40% of the total. This is a 44% increase from $9.2B in 2023 in just two years, with Q4 2025 recording 26% year-over-year growth. VAS consists of cybersecurity, fraud prevention, data analytics, consulting, digital authentication, open banking, and more. About 60% of VAS revenue is payment network-linked revenue (authentication, fraud detection, tokenization tied to transaction volume), and the remaining 40% is non-network revenue such as consulting and marketing.

Current crypto-related revenue within this is estimated to be small. Credential licensing, MTN platform fees, and crypto card surcharges are the main sources, but it is realistic to view their share of total VAS revenue of $13.3B as low single-digit percentages. However, once the BVNK acquisition closes, BVNK's estimated annualized revenue of about $40M will be consolidated, and new revenue sources including stablecoin-to-fiat conversion fees and cross-border B2B settlement fees will be added.

Source: X(@Mastercard)

In March 2026, Mastercard made its biggest bet in five years of crypto business. It agreed to acquire London-based stablecoin infrastructure company BVNK for up to $1.8B ($300M in performance-linked earnouts included). This was the largest stablecoin deal ever, surpassing Stripe's Bridge acquisition ($1.1B).

The deal went through several twists. Coinbase negotiated with BVNK at roughly $2B in the second half of 2025 but the talks collapsed in November over profitability concerns. Mastercard also considered acquiring Zerohash but that fell through, and it ultimately secured BVNK. An interesting point is that BVNK's existing investors included Visa Ventures, a competitor. In effect, Mastercard took infrastructure that Visa had invested in and partnered with. This illustrates the intensity of competition between payment networks over stablecoin infrastructure.

4.2.1 BVNK Overview

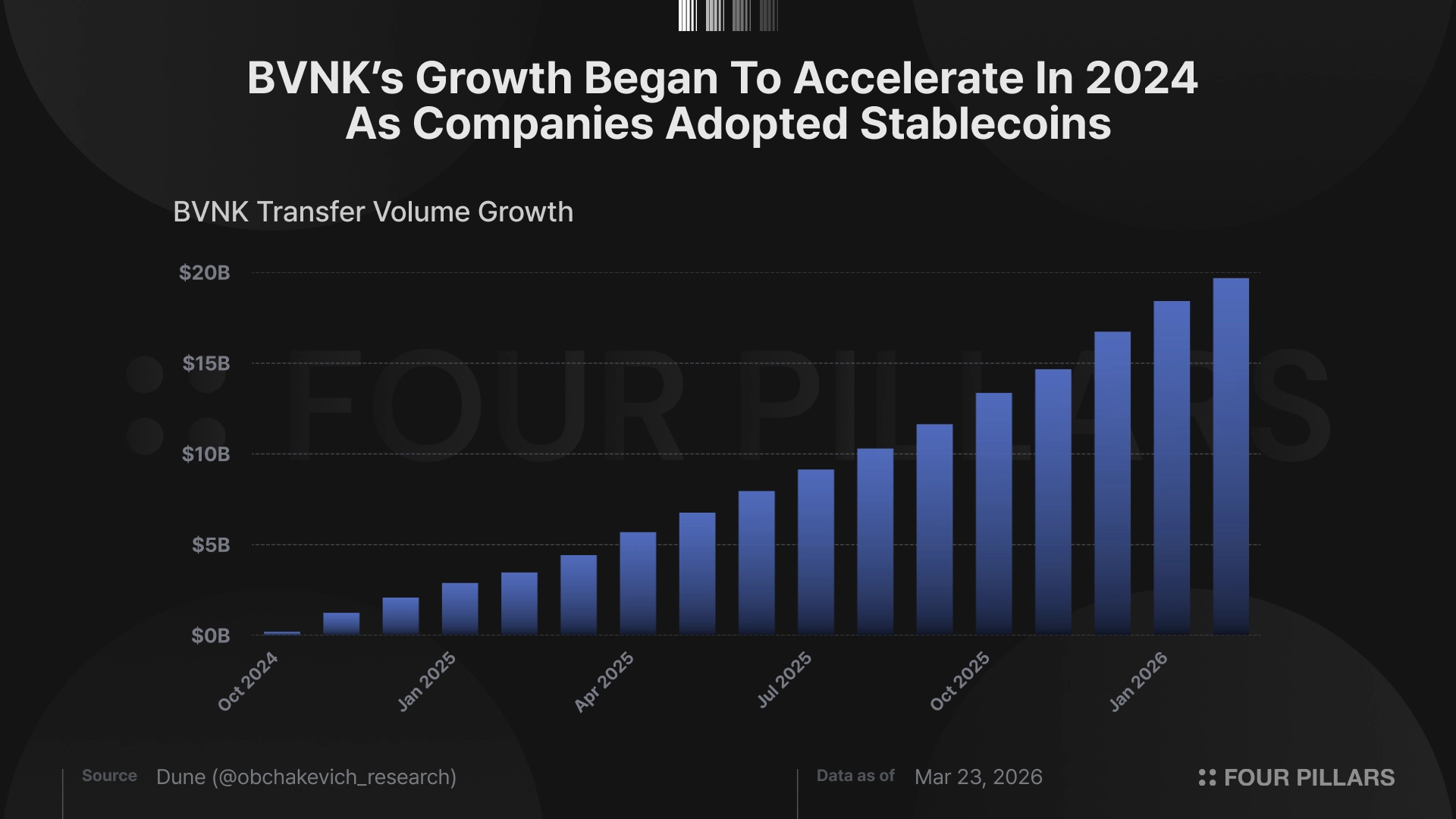

What kind of company is BVNK that Mastercard bet $1.8B on and other competitors coveted? BVNK is a stablecoin payment infrastructure company founded in London in 2021. At the time of founding, stablecoins were actively used in DeFi and on exchanges, but enterprise-grade payment infrastructure with licensing, compliance, and orchestration was absent. BVNK built full-stack infrastructure that processes fiat and stablecoins on a single platform, and in four years it secured annual processing volume of $30B, coverage in over 130 countries, and 226 enterprise clients.

The valuation trajectory from $340M in 2022 to $750M at Series B (December 2024) to an $1.8B acquisition in 2026 shows the market recognizing BVNK as a leader in this space.

4.2.2 Key Products

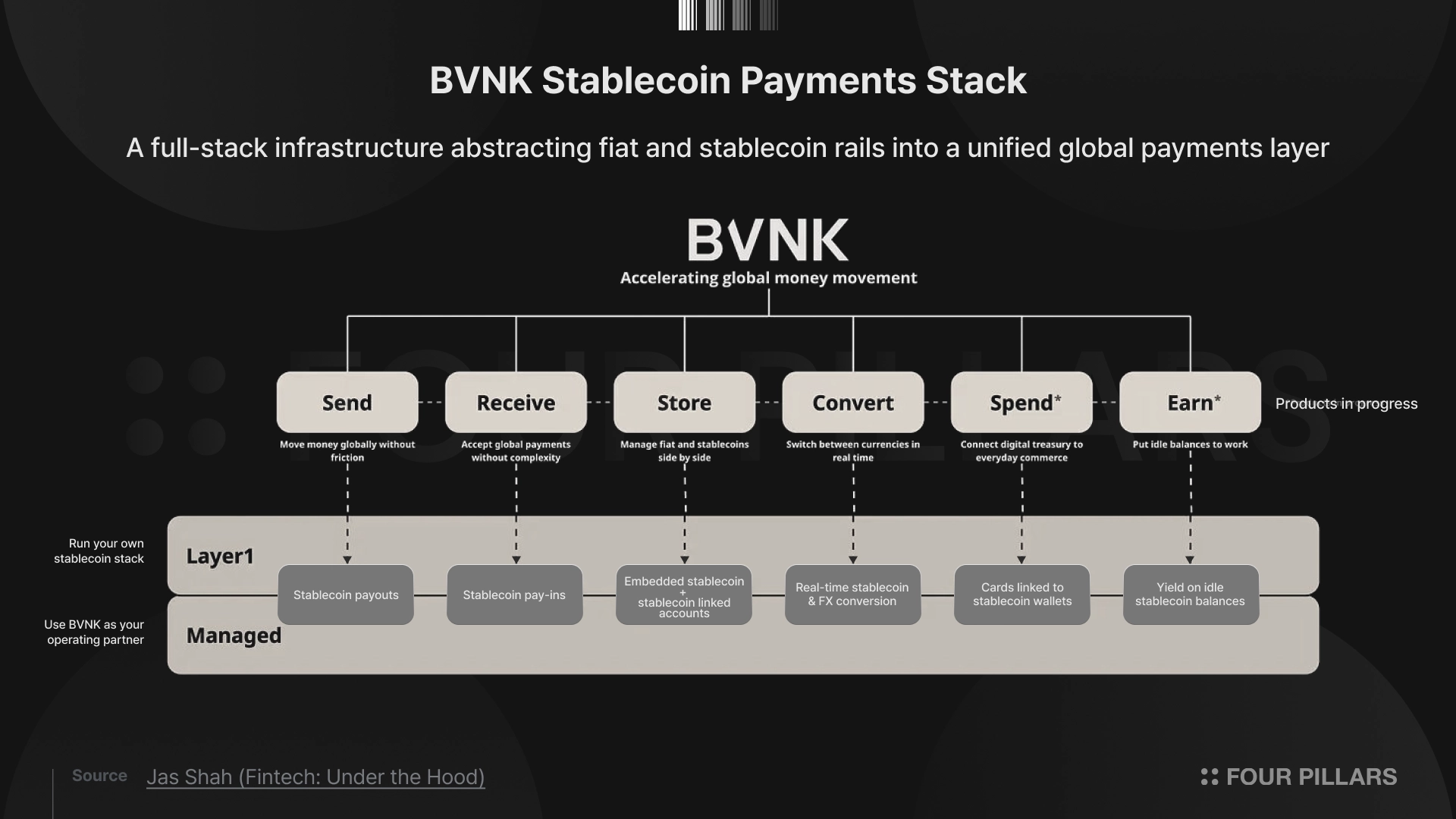

Managed Payments: A turnkey solution that enables enterprises to rapidly adopt stablecoin payments using BVNK's licenses, custody, and compliance infrastructure. BVNK handles KYB/KYC, fund custody, and payment execution, while client enterprises provide services under their own brand

Embedded Wallet: A product that unifies fiat and stablecoins in a single wallet. It holds USD, GBP, EUR fiat balances alongside stablecoin balances in one wallet, with simultaneous access to traditional payment rails like SWIFT, ACH, SEPA and blockchain networks like Ethereum, Tron, and Solana. It also supports automatic conversion of stablecoins to fiat upon receipt or conversion of fiat to stablecoins at payout time

Layer1: Infrastructure that enables large enterprises and financial institutions to operate stablecoin payments in-house by connecting their own licenses and custody partners. Enterprises hold wallet keys directly and BVNK provides only the infrastructure, making it suitable for large financial institutions that must fulfill custody requirements internally

Smart Treasury: An AI/ML-based liquidity management system that predicts liquidity demand across blockchain networks, exchanges, and wallets and automatically moves funds. It was designed to address the limitations of manual treasury management in 24/7 blockchain environments

Spend & Earn: A new product planned for Q1 2026 launch that integrates the ability to use stablecoins for everyday payments (Spend) with the ability to earn returns on balances based on low-risk assets such as short-term Treasuries (Earn)

4.2.3 Business Status

BVNK processes stablecoin transactions across major blockchains including Ethereum, Tron, Solana, Polygon, and BNB Chain in over 130 countries. Annual processing volume was $30B (as of 2025, 2.3x year-over-year growth), with 2.8M transactions processed, showing consistent growth. Monthly transaction volume surged from about $180M in October 2024 to $2.1B in December 2025, coinciding with the point when enterprise stablecoin adoption began in earnest.

As BVNK's position as commercial payment infrastructure for enterprises strengthened, it onboarded 226 new clients in 2025 alone. Key clients include not only Worldpay, Deel, Flywire, and dLocal, but also Rapyd, Thunes, and Bitso. These are operators providing global payment processing, cross-border settlement, and fintech infrastructure, leveraging BVNK's stablecoin-based orchestration layer to complement existing payment rails.

A key factor behind this client acquisition was BVNK's regulatory alignment, secured through country-specific licenses accumulated over years. BVNK holds US-wide MSB registration (NMLS ID 2531294), comprehensive authorization across the EU, and a Spain VASP license, and has obtained ISO 27001 and SOC 2 Type II certifications.

The strategic significance of the BVNK acquisition extends beyond adding one more piece of stablecoin infrastructure. Combined with the MTN that Mastercard had been building internally, the coverage of payment flows changes fundamentally.

4.3.1 Complementarity of MTN and BVNK

Mastercard was already operating the Multi-Token Network (MTN) as an institutional digital asset platform connecting traditional currencies and tokenized assets. MTN is a permissioned network specialized for tokenized deposit settlement between banks and institutions.

BVNK covers a different layer. It is public blockchain-based infrastructure that processes commercial payments for PSPs and enterprises like Worldpay, Flywire, and dLocal in over 130 countries. With MTN as the wholesale layer and BVNK as the commercial payment layer, the combination of the two platforms covers the full spectrum of payment flows onchain, from institutional settlement to cross-border B2B and freelancer payouts.

4.3.2 License and Compliance Bundle

BVNK's value lies in operating assets accumulated over five years, more so than the technology itself.

A license network spanning 130 countries, fiat partner bank relationships, and a large client base like Worldpay and Deel are assets that would take years to build organically. Country-specific license acquisition is the most time-consuming and complex process in stablecoin payment infrastructure. Even after the GENIUS Act, the US requires money transmitter licenses in each of 49 states, and the EU, UK, and Asia each require separate authorizations.

Looking at how much time and cost it takes to acquire these licenses from scratch makes the acquisition logic clear. In the US alone, money transmitter licenses must be obtained individually in 49 states. New York's BitLicense takes up to 2 years, and major states like California and Texas take 6-14 months. First-year direct costs alone run $1M to $3M, with annual maintenance costs exceeding $225,000. EU MiCA comprehensive authorization, Hong Kong HKMA license, and Singapore and UAE authorizations are each separate reviews. There is no mutual recognition between jurisdictions, so this process must be repeated by region for global services.

In effect, Mastercard secured the licensing portfolio BVNK built over five years in a single acquisition, advancing its market entry timeline by at least 2-3 years.

4.3.3 Direct Response to the Card Crisis Scenario

Even in the scenario where card rails are bypassed, infrastructure that handles stablecoin-to-fiat conversion and compliance across 130 countries with different currencies and regulatory environments is still necessary. BVNK's Embedded Wallet performs precisely this role. A fiat bridging rail fills the space left by card rails.

For the cross-border B2B remittance market that cards never accessed, BVNK provides Mastercard with immediately available infrastructure and client base already operating in global payroll, B2B cross-border settlement, and emerging market payments.

As a result, this acquisition performs defense and offense simultaneously. It secures an alternative rail to remain within payment flows even in a future where card rails are bypassed, while entering markets cards could never reach through stablecoin rails. Regardless of which future materializes, Mastercard has built a position to remain a payment infrastructure provider.

Over five years of crypto business, Mastercard built key infrastructure like MTN, Crypto Credential, and Crypto Secure in-house. It has invested in blockchain R&D since 2015, holding over 1,800 registered patents and over 5,000 filed patents globally. This means it did not buy BVNK solely because it lacked internal technical capabilities. Yet it still paid $1.8B. Why does the same company build some things and buy others? Examining the reasoning behind this decision reveals lessons for crypto market entry.

4.4.1 Buy: Why It Acquired BVNK

The blockchain industry can no longer be viewed solely as a technology industry. As of 2025, it has fully transitioned into a regulated industry. With major jurisdictions, including the US GENIUS Act, EU MiCA, and Hong Kong's Stablecoin Ordinance, simultaneously introducing issuer authorization and reserve obligations, stablecoin infrastructure operations now require compliance comparable to banking. The GENIUS Act includes a provision prohibiting circulation of stablecoins from unauthorized issuers after a three-year grace period, making licenses a prerequisite for business.

At the same time, as regulations became clear, bank and institutional clients began actively evaluating stablecoin infrastructure adoption, and the market itself rapidly materialized. Entry is impossible without licenses, but those equipped with licenses can immediately pursue the market.

In this environment, there was a more specific pressure behind Mastercard's choice of acquisition over in-house development. CPO Lambert explained this directly on the day of the acquisition announcement: "BVNK invested years in securing not just the technology but licenses across multiple regions. Building the same capability internally would require considerable time, but acquiring it allows significantly faster market entry."

Time pressure: Stripe closed the Bridge acquisition in February 2025 and launched Stablecoin Financial Accounts in over 100 countries within three months. At a point when regulatory frameworks were finalized and institutional clients were beginning to select infrastructure partners, a 2-3 year gap required for in-house development is fatal.

Capability absorption: Mastercard has decades of experience operating permissioned networks, but no experience operating multi-chain payments on public blockchains. The know-how of abstracting blockchain-specific tech stacks into a single API was accumulated by BVNK over five years while processing $30B in real payments.

Valuation timing: BVNK's valuation surged from $340M in 2022 to $750M in 2024 to $1.8B in 2026. As regulations become clearer, the value of the license portfolio and client base increases. The longer the wait, the higher the acquisition cost.

4.4.2 Build: Why It Built MTN In-House

In contrast, MTN, the representative internally built infrastructure, was a domain where there was no reason to acquire externally. MTN is a permissioned blockchain network with a closed structure where only verified participants can access. Designing who can participate, what roles and responsibilities they have, and how disputes are resolved is the core, and this is essentially the same work Mastercard has done for decades in card networks. Mastercard has also stated directly that it establishes the framework governing interactions among MTN participants based on its experience designing rules for card and real-time payment networks.

The business alignment runs deep. MTN was designed so that banks can participate in tokenized payments through existing interfaces (cards, APIs) without separate blockchain infrastructure. The 22,000+ banks already connected to Mastercard's settlement network are the potential MTN participants.

JP Morgan Kinexys, Standard Chartered, and others chose MTN not because of blockchain technology superiority but because of trust in Mastercard as a counterparty. This kind of trust is not an asset that can be secured through acquisition. If anything, acquiring an external company for this domain would have carried greater risk of its operating philosophy conflicting with the compliance expectations of existing bank clients.

4.4.3 Lessons: Build vs. Buy Decision Criteria in Regulated Industries

The Build vs. Buy framework typically divides into three criteria: (1) Strategic importance: does it provide a core competitive advantage, (2) Capability availability: does the organization have the technical capability to build it internally, (3) Economic efficiency: is it cost-effective. The basic logic is that Build is favorable when the capability provides core competitive advantage and internal technical capacity is sufficient, while Buy is rational when it is not a core competitive differentiator or when time is constrained.

In Mastercard's case, the domain BVNK covers was strategically important, and Mastercard partially possessed blockchain technical capabilities. Looking at just those two axes, Build would be the right call. Yet it chose Buy because on the third axis, economic efficiency, the cost of Build was not conventional development cost. In regulated industries, the cost of in-house development is measured not in development expenses but in the time required to secure licenses, that is, the loss of market preemption opportunity. The judgment was that a 2-3 year gap is more expensive than the $1.8B acquisition premium.

Mapping Mastercard's choices to this framework sharpens the boundary between Build and Buy.

MTN, where Build was chosen, was a domain where core business capabilities directly transfer, Mastercard's trust itself functions as a moat, and no separate external licenses are required.

BVNK, where Buy was chosen, met the Build conditions on strategic importance and technical capability, but the moat was formed by assets that can only be accumulated over time: 130-country licenses, banking partnerships, and client networks. In a situation where the market was rapidly reshuffling after regulatory finalization, the 2-3 year in-house development timeline was unaffordable.

The general lesson derived here is that in regulated industries, the Build vs. Buy decision is not fixed. The economic efficiency calculation flips depending on the regulatory environment. When regulations are uncertain, Build or wait-and-see may be rational. However, the moment regulations are finalized, the market materializes and competition begins, and the time cost of in-house development exceeds the acquisition premium. BVNK's valuation rising from $340M to $1.8B demonstrates this. Companies need to consider that the Build vs. Buy decision for the same capability can reverse entirely depending on regulatory timing.

Mastercard's crypto strategy simultaneously performs defense and offense, and accordingly, risks are also two-sided. Internalizing stablecoins provides access to new TAM, but at the same time, the potential for conflict with the existing network fee business also grows. Regulatory clarity is an opportunity, but specific implementation rules remain undetermined.

The GENIUS Act passed, but specific implementing regulations are scheduled to be developed by January 2027. Reserve composition requirements, capital buffer standards for non-bank issuers, and conditions for foreign issuers' US market access remain undetermined. Depending on these rules, BVNK's operating scope and cost structure could change significantly.

The dual federal-state regulatory structure has been flagged as potentially triggering a regulatory race to the bottom. If states compete to attract stablecoin issuers by lowering regulatory standards, compliance levels could be driven down, and the moat of the license portfolio BVNK has built would become shallower. Conversely, if rules are set too strictly, operating costs for non-bank infrastructure companies like BVNK could surge, making profitability even harder to achieve. Either direction directly impacts Mastercard's crypto business TAM.

Even if Mastercard provides stablecoin rails, the structural reality that the per-transaction take rate is lower than card rails is a risk. In card payments, network fees, interchange, and processing fees combine for a merchant burden of about 2-3% per transaction, of which Mastercard collects a portion (several bps) as network fees.

In stablecoin payments, this fee structure itself does not hold. Even when processed through BVNK, the structure is one of adding margin on top of blockchain gas fees, so per-transaction revenue is significantly lower than card payments. If the same transaction migrates from card rails to stablecoin rails, even if Mastercard remains within the payment flow, per-transaction revenue declines. Whether the new TAM (cross-border B2B, remittances) captured through stablecoin rails can offset this self-cannibalized revenue loss is the critical question.

The prevailing market view has been that stablecoins would weaken card networks. However, Mastercard's moves point in a different direction. Rather than merely defending against scenarios where card rails are bypassed, it is taking an offensive frame, entering markets like cross-border B2B remittances that cards could never access through stablecoin rails.

With the BVNK acquisition securing commercial payment infrastructure in 130 countries, Mastercard aims to build a structure where it remains an infrastructure provider even if the payment instrument changes. Whether this strategy actually works can be verified at several upcoming checkpoints.

BVNK Acquisition Closing and Integration: Regulatory approval within the year is the first checkpoint. After closing, the key indicators determining integration success will be how BVNK's 130-country infrastructure connects with Mastercard's existing payment network and whether BVNK's existing clients (Worldpay, Deel, etc.) are retained post-acquisition.

Crypto-Related VAS Revenue Disclosure: Currently, crypto revenue is aggregated within VAS and not separately reported. If crypto revenue is reported as a separate line item in the H2 2026 earnings, this will be the first point to confirm the actual scale of the business. If the crypto share within VAS exceeds 10%, it can be read as a signal of entering the revenue contribution phase.

Visa's Response: Visa was also an investor in BVNK. Whether Visa acquires an alternative infrastructure player like Zerohash or accelerates its own in-house development following Mastercard's acquisition will determine the competitive dynamics between payment networks. If Visa announces a similar acquisition in the near term, it amounts to the internalization of stablecoin infrastructure by traditional payment networks becoming an industry standard.

GENIUS Act Implementation Rules Finalized (January 2027): Once capital requirements and foreign issuer access conditions are finalized, Mastercard's crypto business TAM will be recalibrated. If conditions for foreign issuers are strict, BVNK's US license portfolio value increases. If they are lenient, global competition intensifies.

Real Payment Stablecoin Volume: The growth trajectory of real payment volume, excluding trading and DeFi settlement, is the barometer for Mastercard's crypto strategy. If this volume accelerates, the justification for crypto investments including the BVNK acquisition strengthens. If it stagnates, ROI questions will be raised.

Dive into 'Narratives' that will be important in the next year