This article is an excerpt from our report on stock tokenization. The full report can be found in “2026: The Year of Tokenized Stocks”

The year 2025 was an extremely encouraging one for the cryptocurrency industry, as it shed the stigma of its past and experienced active institutional adoption.

The Trump administration repeatedly emphasized that the United States should become the capital of cryptocurrency and rolled out a variety of initiatives to elevate the cryptocurrency and blockchain industry to a national strategic priority. For example, through an executive order in March, it established the “Strategic Bitcoin Reserve” and the “U.S. Digital Asset Stockpile,” both composed of Bitcoin and other cryptocurrencies seized by the Treasury Department. In addition, the “President’s Working Group on Digital Asset Markets,” which was officially established through an executive order in January, published an in-depth 166-page report containing regulatory recommendations in July.

The administration’s strong stance on the cryptocurrency industry was quickly conveyed to regulatory agencies as well. The SEC announced new regulatory framework initiatives such as Project Crypto, while the CFTC introduced Crypto Sprint.

In 2025, the U.S. Congress also produced a number of notable achievements. The GENIUS Act, the first piece of legislation aimed at regulating stablecoins at the federal level, was introduced in the Senate and ultimately signed by the President. Meanwhile, the CLARITY Act, which seeks to clarify market structure and supervisory authority across the entire cryptocurrency sector, and the Anti-CBDC Surveillance State Act, which prohibits CBDCs, both passed the House of Representatives.

These consistent yet rapid actions by the U.S. administration, regulatory bodies, and Congress led to greater regulatory clarity for cryptocurrencies. That clarity naturally resulted in increased cryptocurrency adoption by industry players. Across sectors such as big tech, banking, asset management, fintech, and retail, a large number of Web2 players have recognized the potential of cryptocurrency and blockchain as the financial technologies of the future and have recently been quick to adopt features such as stablecoins and AI agent payments.

If the Crypto Market Structure Bill, also known as the CLARITY Act, which is currently the subject of the most active discussion, is passed as well, the adoption of cryptocurrency by traditional finance will accelerate at a pace far greater than it is today.

As blockchain is fundamentally a technology designed for finance, financial use cases experienced unprecedented growth in 2025.

The first is stablecoins. In 2025, stablecoins achieved remarkable results across all dimensions, including regulation, real world usage, and onchain activity. The market capitalization of stablecoins has now reached approximately $300B, and following the passage of the GENIUS Act, a large number of traditional financial institutions and corporations have begun directly participating in the issuance and distribution of stablecoins.

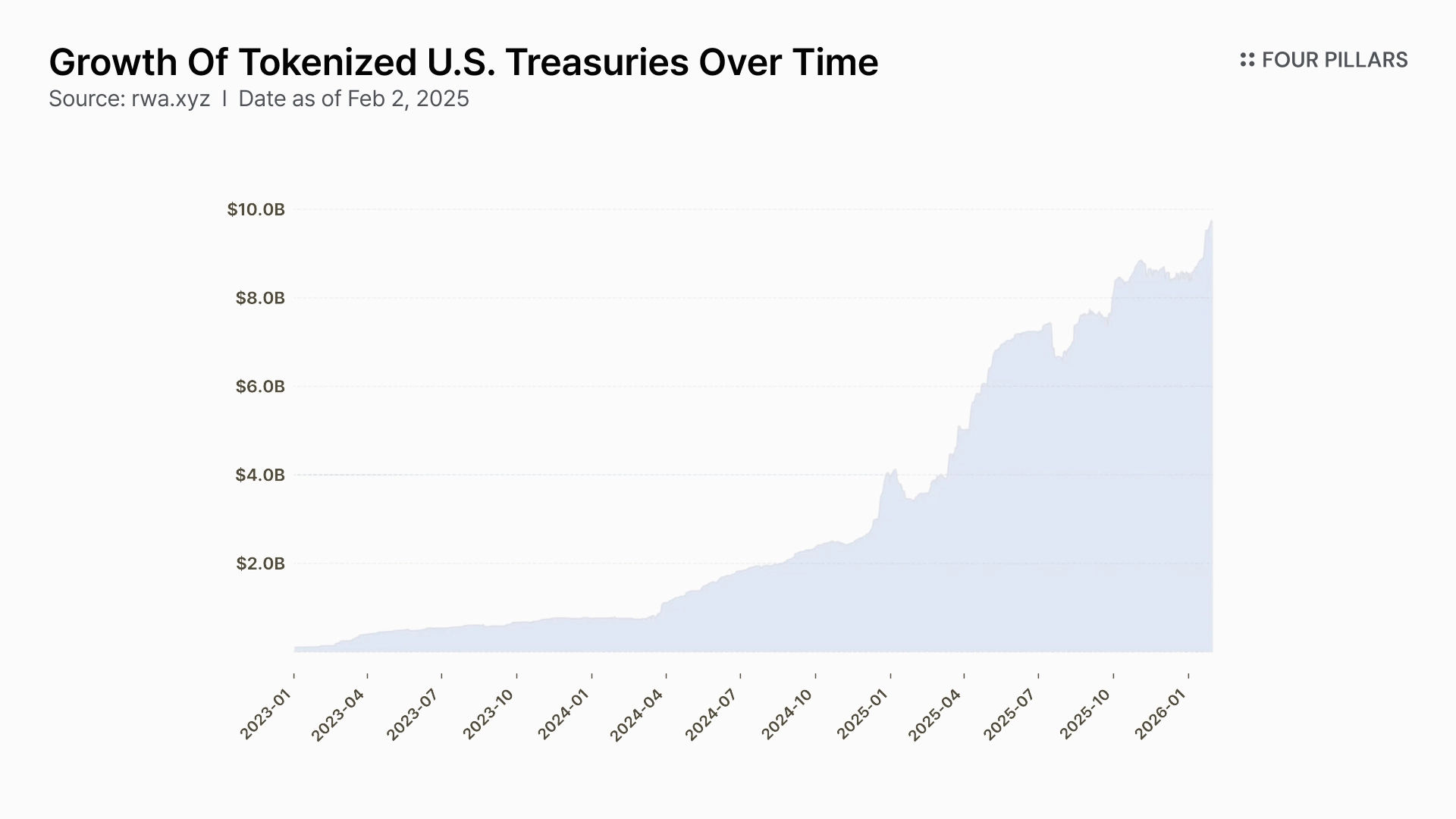

The second is the tokenization of U.S. Treasuries among RWAs. As stablecoin issuance grew rapidly, investors naturally began seeking investment opportunities that could generate stable returns using stablecoins, and the tokenization of short term U.S. Treasuries perfectly met that demand. The size of the tokenized U.S. Treasury market has increased by more than approximately 120% year to date, and tokens backed by Treasuries such as BUIDL and USTB have become core yield engines utilized by numerous DeFi protocols within the onchain ecosystem.

Then, within this massive trend of integration between traditional finance and onchain systems, what will be the key theme to emerge in 2026? Following stablecoins and U.S. Treasuries, the keyword that will undoubtedly attract attention in 2026 is tokenized stocks.

The total size of the global stock market is approximately $140T, and when including shares of private companies, the scale is significantly larger. Of this, the U.S. stock market accounts for approximately $72T, representing more than half of the global total. However, the size of the tokenized stocks market is still less than $1B. Considering that major figures such as BlackRock CEO Larry Fink and SEC Chair Paul Atkins have continuously emphasized the importance of tokenizing all assets, including equities, the upside potential of tokenized stocks is enormous.

But wait, why has the tokenized stocks market not grown as rapidly as the tokenized U.S. Treasury market so far? In the case of U.S. Treasuries, the characteristics of the assets and their yields are relatively standardized, making onchain liquidity and tokenization management easier and enabling rapid growth. In contrast, stocks have more diverse asset characteristics, a wider variety of associated rights, and building liquidity on a per stock basis is far from easy.

In addition, issues such as oracle challenges during off market hours and the existence of multiple tokenization approaches have kept the tokenized stocks sector relatively small so far. These topics will be examined in greater detail later on.

1.3.1 Why Tokenization Is Gaining Attention

In September 2025, Nasdaq submitted a proposed rule change to the SEC that would allow stocks and ETPs to be traded in the form of blockchain based tokenized securities. DTCC has continuously conducted various experiments, including tokenizing securities such as stocks onchain, using them as collateral, and testing settlement efficiency. Robinhood views tokenized stocks as a core part of its future vision and is already providing tokenized stock services to users in the EU.

It is no coincidence that not only Web3 protocols, but also traditional financial infrastructure providers and fintech companies, view tokenized stocks as highly important. This is because the infrastructure of the traditional stock market is inefficient and leaves significant room for improvement.

1.3.2 How the Traditional Stock Market Operates

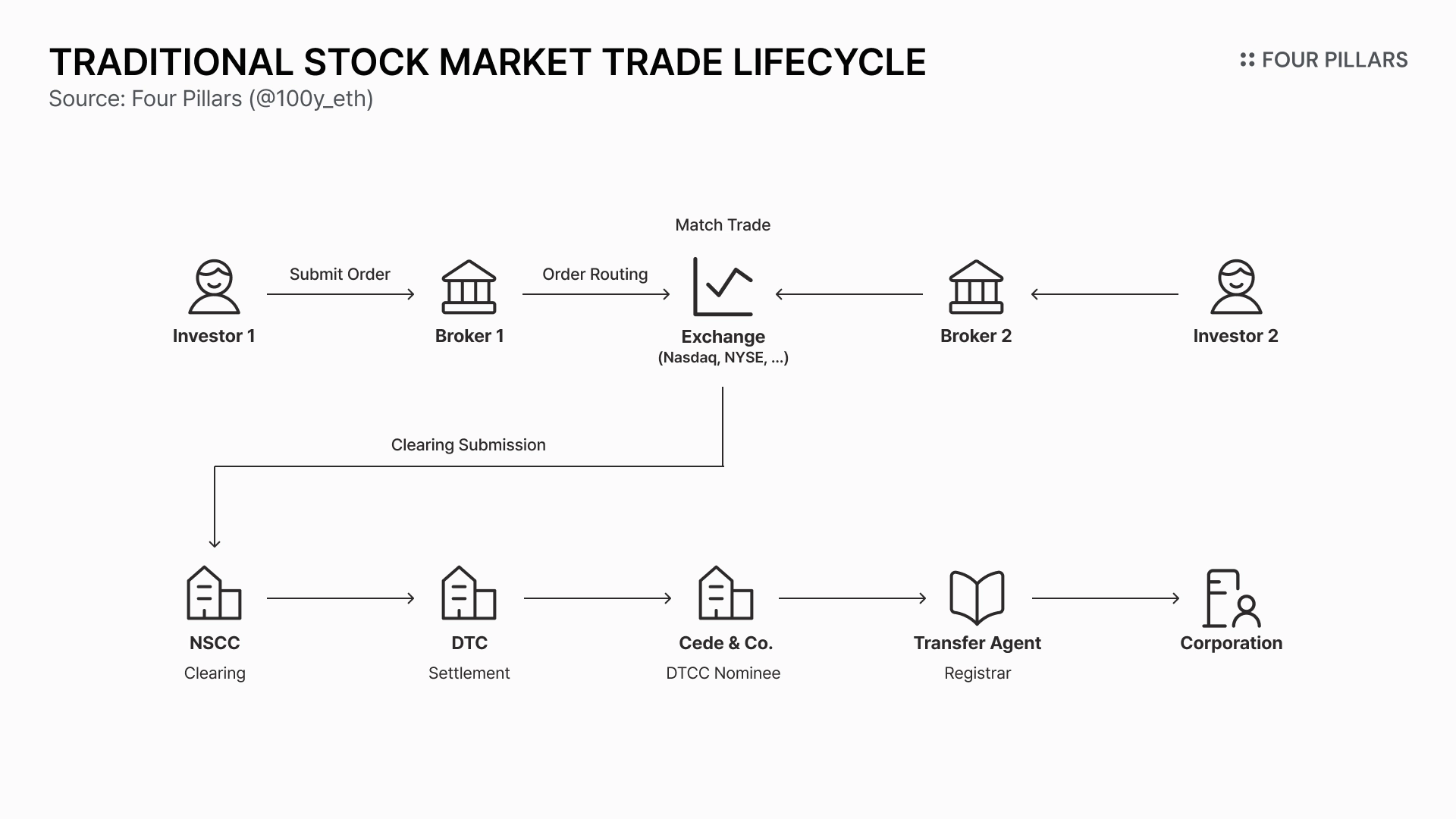

The actual process by which stocks are bought and sold in today’s stock market typically proceeds as follows:

An investor places a buy or sell order through a broker, such as Fidelity Investments or Robinhood.

The broker receives the order, conducts internal verification and review, and then forwards the order to an exchange, such as Nasdaq or the NYSE.

The order is entered into the exchange’s order book, and when matching buy and sell orders are found, the trade is executed. Immediately upon execution, a confirmation message is sent to both the investor and the broker.

The exchange collects all executed trade information and sends it to a clearinghouse, such as the NSCC.

The clearinghouse calculates how many shares and how much money must be exchanged between brokers.

Once clearing is completed, the settlement institution, such as the DTC, transfers the actual cash and shares between brokers.

Finally, the transfer agent updates the official record of the legal owners.

The shareholder register is not managed directly by the company itself, but is typically maintained by a transfer agent. In other words, the company’s official master shareholder register managed by the transfer agent is what governs actual ownership of shares. However, most U.S. stocks are not recorded under the names of individual investors, and the company’s official shareholder register usually lists only a single name, Cede & Co.

Cede & Co. is a special purpose entity that acts as the nominee of DTCC. While the legal ownership of shares remains under the name of Cede & Co., individual investors hold claims against Cede & Co. through their brokers, meaning they effectively hold ownership indirectly. This structure eliminates the need for the transfer agent to update the register for every transaction and allows stock settlement and transfers to be processed much more quickly.

1.3.3 Inefficiencies of the Traditional Stock Market

The ultimate goal of stock trading is to connect buyers and sellers of stocks and deliver cash and shares between them. However, as seen in the process above, numerous intermediaries such as brokerages, clearinghouses, and settlement institutions are involved, resulting in a highly complex system.

Even after a trade is executed, full settlement takes T+1 days in the United States and T+2 days in most other countries. Brokers, the NSCC, and the DTC all charge fees for their services. The final burden of these fees ultimately falls, directly or indirectly, on investors. In other words, complex processes create inefficiencies in both time and cost.

The reason today’s traditional stock market processes are so complex is ultimately to minimize credit risk. In the past, when stocks were exchanged in the form of paper certificates, it was not possible to process settlement and clearing safely and quickly, and back office failures were frequent. At that time, there was no technology capable of handling direct ownership and direct settlement at scale, so an indirect ownership model based on central depositories was adopted. As a result, intermediaries such as brokers, clearinghouses, and settlement institutions emerged, and a complex structure took shape.

In particular, as the number of intermediaries involved in stock trading increased, various laws and regulations such as SIPA, the Securities Acts Amendments of 1975, and the Securities Exchange Act of 1934 were introduced to control the risks of each intermediary. This ultimately led to the complete entrenchment of the complex structure of today’s stock market.

The traditional stock market suffers from issues such as slow settlement times, limited trading hours, high fees, low accessibility to foreign stocks, and indirect ownership, largely due to infrastructure limitations. There have been many attempts so far to address these problems.

1.4.1 Settlement Time

Settlement is the process in which cash and stocks are actually exchanged and a stock trade is finalized. Because settlement involves multiple steps such as clearing, ownership transfer processing, cash settlement, and risk management, all handled by multiple intermediaries, settlement does not occur immediately after a trade is executed.

Long settlement times themselves are problematic because they can lead to issues such as one party failing to deliver cash or shares on time, or increased liquidity risk caused by restrictions on reinvestment or withdrawals during the delay period. For these reasons, stock markets around the world have continuously worked to reduce settlement times.

For example, in the U.S. stock market, when stocks were traded in the form of paper certificates, the T+5 settlement cycle was used due to the burden of physical document processing. This was shortened from T+5 to T+3 in 1995, from T+3 to T+2 in 2017, and from T+2 to T+1 in 2024, reflecting continuous improvements in settlement time. In addition to the United States, Canada and Mexico also transitioned to a T+1 settlement cycle at the same time, while Europe still operates on T+2 but is planning to move to T+1 with a target of 2027.

However, there is still a limitation in that no market currently offers true instant settlement, or T+0, as enabled by blockchain technology.

1.4.2 Trading Hours

Traditional stock markets such as Nasdaq and the NYSE have limited trading hours. This causes significant inconvenience, especially for investors in different time zones. To address this, ongoing efforts are being made at both the service level and the infrastructure level.

Service Level

Source: Robinhood

The first approach is extending trading hours at the service level. Services such as Robinhood and Interactive Brokers provide the ability to trade stocks 24 hours a day, five days a week. For example, during regular trading hours they use markets such as Nasdaq and the NYSE, while during extended hours they route orders to Blue Ocean ATS, where trades are executed.

However, these 24 hour trading services are only supported for certain stocks and ETFs and only through limit orders. During overnight hours, they suffer from unavoidable limitations such as lower liquidity and higher volatility compared to regular hours, as well as reduced transparency because trading occurs on ATS platforms.

Infrastructure Level

Source: DTCC

The second approach is extending trading hours at the infrastructure level. DTCC, Nasdaq, and CBOE announced that, subject to regulatory approval, they plan to enable 24/5 stock trading starting on June 28, 2026. Unlike existing services that process overnight trades through ATS platforms, DTCC aims to immediately guarantee central counterparty clearing, or CCP, even for overnight trading.

However, this does not provide 24/7 trading. Approximately one hour of downtime per day is still required for system maintenance, risk calculations, and position reconciliation. In addition, margin management and risk management become significantly more complex for brokerages and other financial institutions. The fundamental reason for these limitations is that 24 hour trading is being implemented on top of an already complex existing system.

1.4.3 Trading Fees

Because stock trading involves numerous intermediaries such as brokers and DTCC, fees incurred at each stage are ultimately passed on to investors as trading fees. For example, DTCC charges usage fees to securities firms and financial institutions that participate in its infrastructure under the guise of transaction and clearing fees and asset custody services. Securities firms and financial institutions then charge fees to investors.

Source: The Measure of a Plan

The most representative service that promotes fee reduction is Robinhood. Robinhood users can trade stocks without explicit commissions, but hidden fees exist. Robinhood does not process customer orders directly, instead routing them through Citadel. In the process of handling customer trades, Citadel profits from the bid ask spread and pays rebates to Robinhood in the form of PFOF, or Payment for Order Flow. In other words, commission free trading is an illusion.

There is also a way to reduce fees at the trading infrastructure level rather than the service level. Investors can register shares directly in their own names on the shareholder register without going through DTCC, meaning without being registered under Cede & Co. This is known as the Direct Registration System, or DRS. While registering through DRS results in lower fees compared to holding stocks through a broker, it is not commonly used due to differences in accessibility, convenience, and ease of trading from the individual investor’s perspective.

1.4.4 Fundamental Inefficiencies Remain Unresolved

Although there have been many attempts to address the inefficiencies of the existing stock market, all of these efforts are merely stopgap measures built on top of the existing complex infrastructure and do not resolve the root causes of inefficiency. Ultimately, achieving 1) instant settlement, 2) 24/7 trading, and 3) extremely low fees requires an entirely new financial infrastructure.

Blockchain technology and tokenized stocks can solve this.

1.5.1 Advantages of Tokenized Stocks

Tokenized stocks refer to representing traditional stocks in the form of digital tokens on blockchain technology. The advantages that tokenized stocks can offer are listed below, and most of them stem from the inherent characteristics of blockchain technology:

Instant settlement: Transactions on a blockchain are finalized immediately.

24/7/365 trading: Blockchain infrastructure operates on decentralized networks around the clock, enabling these assets to be traded 24/7/365.

Low fees: Tokenized stocks significantly reduce the number of intermediaries involved, allowing investors to benefit from lower fees.

Fractional investment: Stock tokens can be held and traded in fractional units.

Global accessibility: Transactions conducted via blockchain are accessible to investors worldwide.

Direct ownership: Investors can hold stock tokens directly in their personal wallets.

Smart contracts: Beyond simply holding and trading stocks on a blockchain, investors can leverage stock tokens for a wide range of financial activities through smart contracts.

1.5.2 Misconceptions About Tokenized Stocks

A common misconception is that tokenized stocks solve all the shortcomings of the traditional stock market and fully deliver all of the advantages listed above. This, however, is not the case.

As will be examined in detail in the next section, there are many different ways in which stocks can be tokenized. The ownership itself can be tokenized, one or multiple rights associated with a stock can be tokenized, or claims on the company that holds the stock can be tokenized. Because there are various approaches to tokenized stocks, each comes with its own distinct advantages and limitations.

Following stablecoins and bonds, we are now approaching the inevitable evolution of financial infrastructure in the form of tokenized stocks. Since the tokenized stocks market is still at a very early stage, tokenization methods are diverse and not yet standardized. The purpose of this report is to improve understanding of tokenized stocks in the market and to examine the current tokenized stocks landscape, the regulatory environment in each country, and the future opportunities related to tokenized stocks.

2.1.1 Stablecoins and Tokenized Treasury Funds Are Easy. What About Stocks?

Stablecoins and U.S. Treasury funds, which have seen the most active development in tokenization, were able to grow rapidly with relatively limited regulatory and liquidity fragmentation because their tokenization approaches are relatively standardized.

Stablecoin issuance: An issuer that holds the necessary licenses in each jurisdiction custodies fiat currency and issues onchain stablecoins backed 1:1.

Tokenization of U.S. Treasury funds: Many people misunderstand this, but RWAs such as BUIDL, USYC, and BENJI are not the tokenization of Treasuries themselves. Rather, they are tokenized money market funds (MMFs) composed of Treasuries. In the United States, tokenization is carried out by having an SEC registered transfer agent manage the MMF shareholder register using a blockchain based system.

However, tokenized stocks are different. Unlike fiat currency or bonds, stocks come in many varieties, and the associated rights include not only ownership but also voting rights and dividend rights. As a result, it has been very difficult to tokenize stocks in a uniform way like fiat currency or bonds, and major tokenized stocks services such as Securitize, Backed, and Robinhood tokenize stocks using different approaches.

2.1.2 Four Types of Tokenized Stocks

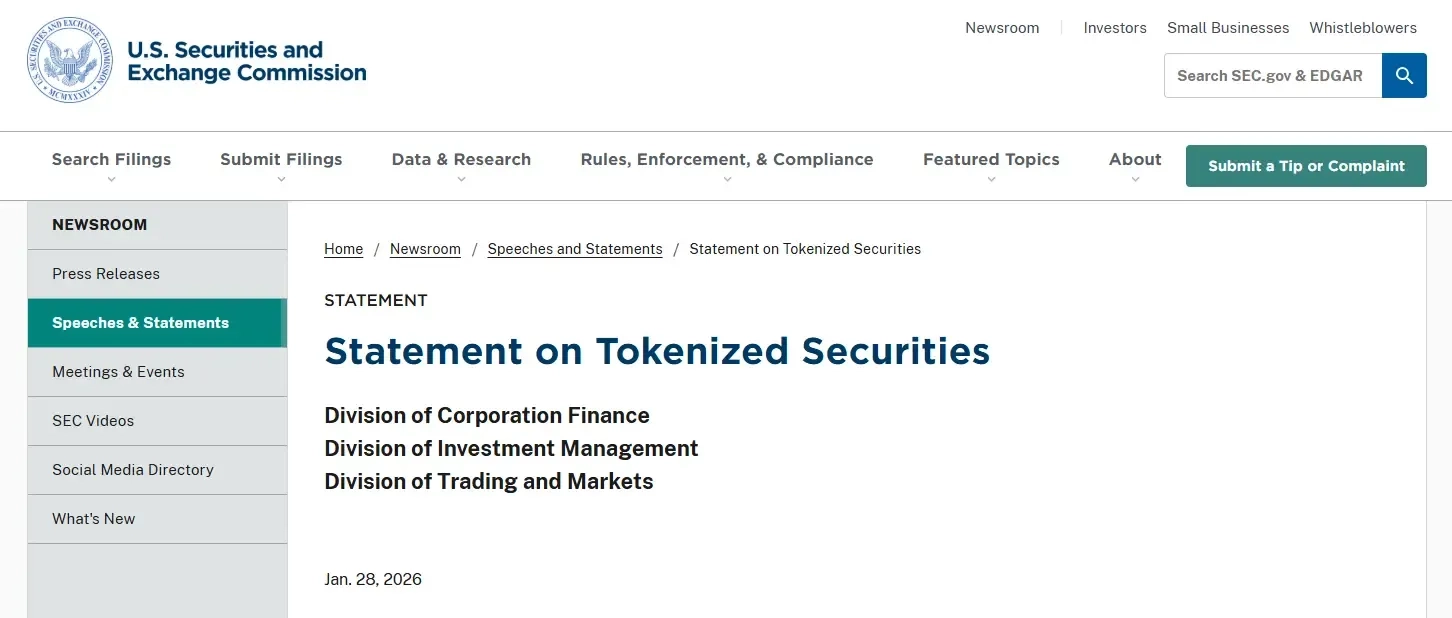

The SEC recently released a statement on tokenized securities. This statement is a highly important document in that it presents a classification framework for tokenized securities that exist in the market and the SEC’s views on them.

The SEC classified tokenized securities into the following four categories:

Issuer-Sponsored Tokenized Securities: An approach where the issuer/transfer integrates blockchain into the shareholder register that it previously managed in an off-chain database. The security itself is tokenized. Representative example: Securitize

Tokenized Security Entitlement: An approach where blockchain is integrated into a registry system managed by a third party. The rights that an investor holds indirectly through an intermediary or custodian are tokenized. Representative example: DTCC

Linked Security: An approach where a third party references another company’s security as an underlying asset and issues a new security in its own name. Investors only have rights to the security issued by the third party and have no rights of any kind to the referenced company.

Security-Based Swap: A swap type contract in which a third party provides synthetic exposure that tracks the price of another security. Unlike a Linked Security, this is not a security but a derivatives contract, so regulatory requirements are stricter. Representative example: Robinhood

At a time when there had been no official classification framework for tokenized securities, the SEC’s framework can serve as an excellent reference. Based on this, and after analyzing real products, we were able to classify tokenized stocks, the subject of this report, as follows.

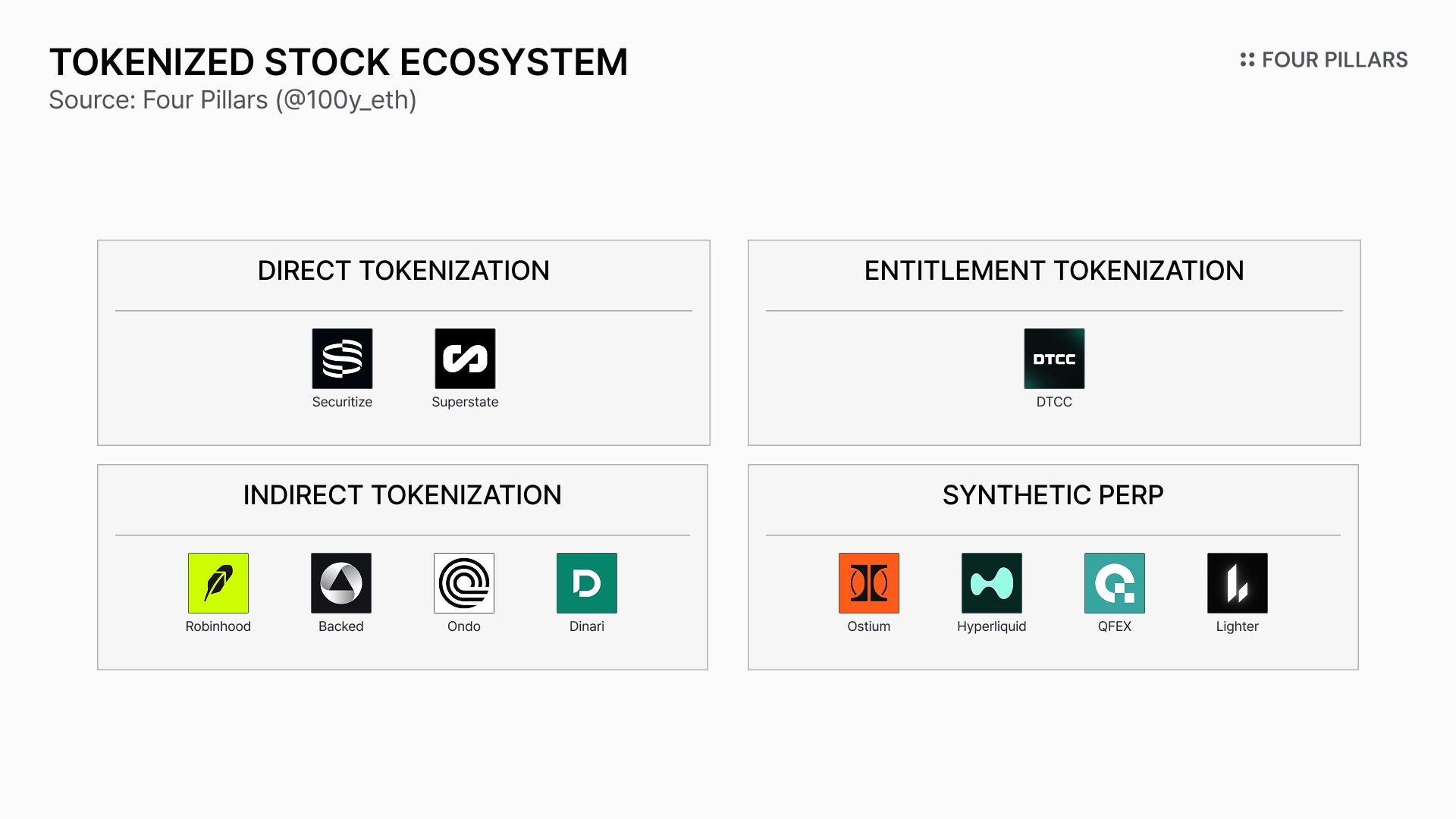

So far, tokenized stocks services in the market tokenize stocks through the following four methods:

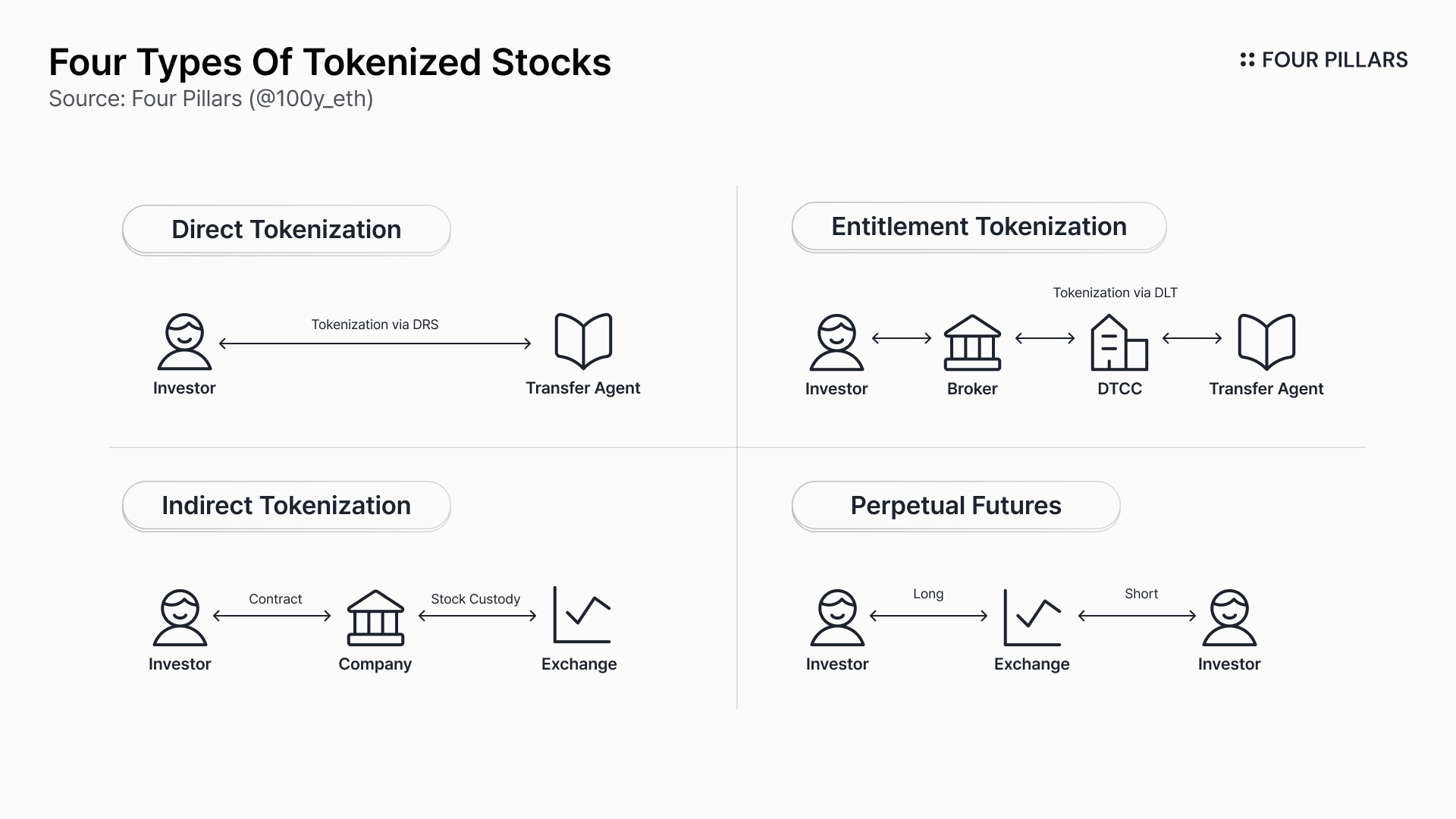

Direct Tokenization: A method that directly tokenizes stock ownership (e.g., Securitize, Superstate). This corresponds to Issuer-Sponsored Tokenized Securities in the SEC’s classification framework.

Entitlement Tokenization: A method that tokenizes stock related rights within existing infrastructure (e.g., DTCC). This corresponds to Tokenized Security Entitlement in the SEC’s classification framework.

Indirect Tokenization: A method where a company buys and holds stocks on behalf of users and tokenizes the beneficial interest in them (e.g., Robinhood, Backed, Ondo, Dinari). This corresponds to Security-Based Swap in the SEC’s classification framework.

(Additional) Perpetual Futures: A perpetual futures market that tracks a stock’s price without spot trading (e.g., Hyperliquid, QFEX)

The processes differ significantly across tokenization methods, and for this reason, factors such as global accessibility, onchain usability, the types of rights being tokenized, and trading hours also vary greatly by method. Let us examine one by one how each method works in detail and what characteristics it has.

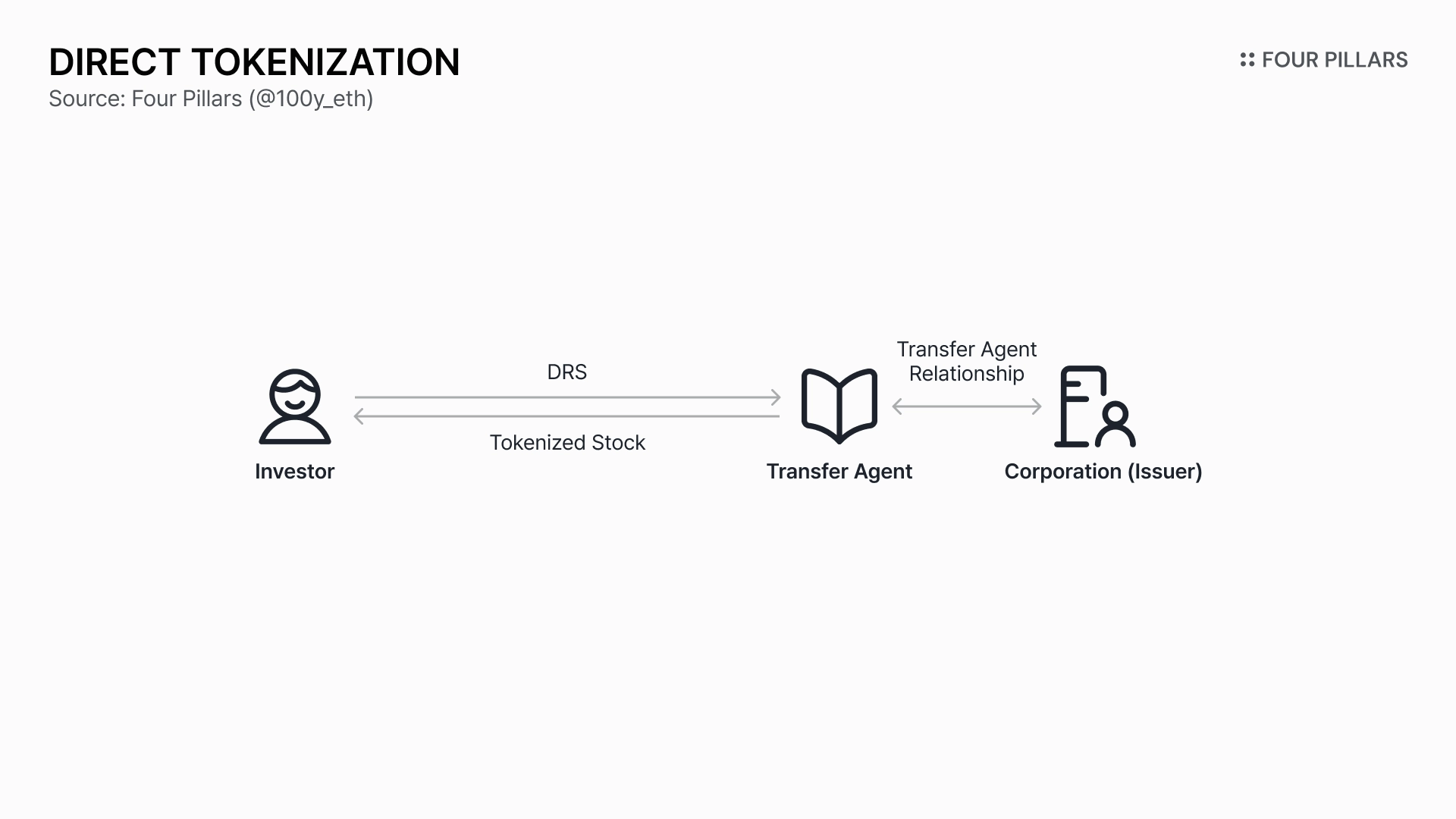

Direct Tokenization refers to fully tokenizing stock ownership onchain. Under the traditional system, even when investors purchase stocks through a brokerage, ownership of those stocks is registered under Cede & Co., and investors are recognized not as direct owners but as beneficial owners. In contrast, investors who hold stock tokens tokenized through direct tokenization are recognized as the direct owners of the stocks and are entitled to all rights associated with the stock, including dividend rights, voting rights, and ownership rights.

How is direct tokenization possible? This is related to the Direct Registration System, or DRS, discussed in the introduction of this report. DRS allows investors to be registered directly under their own names on the shareholder register, rather than through DTCC and Cede & Co. Platforms that support direct tokenization of stocks, such as Securitize and Superstate, manage stock registers through DRS and can issue onchain stock tokens to investors registered via DRS. This approach is almost identical to the way money market funds such as BUIDL are tokenized.

Direct tokenization is the tokenization method that most closely aligns with the direction pursued by the tokenized stocks sector. By tokenizing the stock itself and enabling investors to directly own it, this method offers the following advantages:

Instant settlement: Tokenized stocks are settled immediately when traded between investors.

Trading availability: Tokenized stocks are always tradable onchain.

Fewer intermediaries: Unlike the traditional model, which involves numerous intermediaries such as the NSCC, DTC, brokerages, and transfer agents, the direct tokenization approach involves no intermediaries other than the transfer agent.

Global accessibility: Any investor registered on the tokenization platform can access stock tokens.

Self custody: Investors directly hold their stocks.

Onchain liquidity: Because only a single token representing the stock can exist onchain, liquidity fragmentation is less severe compared to other tokenized stocks approaches.

Full inheritance of rights: All rights associated with the stock, including ownership, voting rights, and dividend rights, are fully tokenized.

In other words, direct tokenization is an extremely powerful approach that captures nearly all of the advantages commonly associated with tokenized stocks. However, direct tokenization also comes with the following drawbacks:

Liquidity fragmentation with traditional stocks: There is liquidity fragmentation between stocks already traded on Nasdaq or the NYSE and stocks that are directly tokenized onchain. Converting tokenized stocks back to trading on Nasdaq or the NYSE, or tokenizing stocks purchased on Nasdaq or the NYSE, involves complex processes and additional costs.

Limitations on onchain usage: For stocks tokenized through direct tokenization, peer to peer transfers among users registered on the platform are generally unrestricted. However, using these tokens within DeFi protocols such as AMMs or lending platforms is still limited. If stocks tokenized through direct tokenization were to interact permissionlessly with a wide range of AMM or lending pools, this could conflict with regulatory requirements.

Entitlement tokenization is a tokenization approach that allows investors to be granted all rights associated with stocks while largely preserving the existing stock market system. This is made possible by replacing internal ledgers used in traditional securities infrastructure to record ownership of rights with a blockchain based ledger.

As a result, entitlement tokenization can capture the advantages of existing centralized infrastructure while also benefiting from the operational advantages of blockchain technology.

Trading availability: This approach can serve as a foundation to expand beyond the 24/5 trading support that DTCC is preparing this year and eventually enable 24/7 trading.

Liquidity concentration: By leveraging DTCC’s existing infrastructure, this approach can benefit from deep, concentrated liquidity.

Regulatory continuity: This is the most regulation friendly approach within existing regulatory frameworks.

Compatibility with existing systems: The only change from existing systems is that rights records are maintained on a blockchain rather than internal ledgers, making this the most compatible tokenized stocks approach.

Full inheritance of rights: All rights associated with stocks, including ownership, voting rights, and dividend rights, are fully tokenized.

Smart contract based automation: Smart contracts can be used to automate the recording and management of rights.

However, inheriting the existing system almost entirely brings significant drawbacks along with its advantages:

Inheritance of existing system structure: The many intermediaries involved in the current system, such as brokerages, DTC, and NSCC, remain unchanged.

Indirect ownership: Investors still hold stocks indirectly, with ownership still registered under Cede & Co.

Limited global accessibility: Access is limited to existing investors who can already access the U.S. stock market.

Limitations on instant settlement: Because many intermediaries still exist, instant settlement may remain difficult, although the movement of stock collateral could become easier.

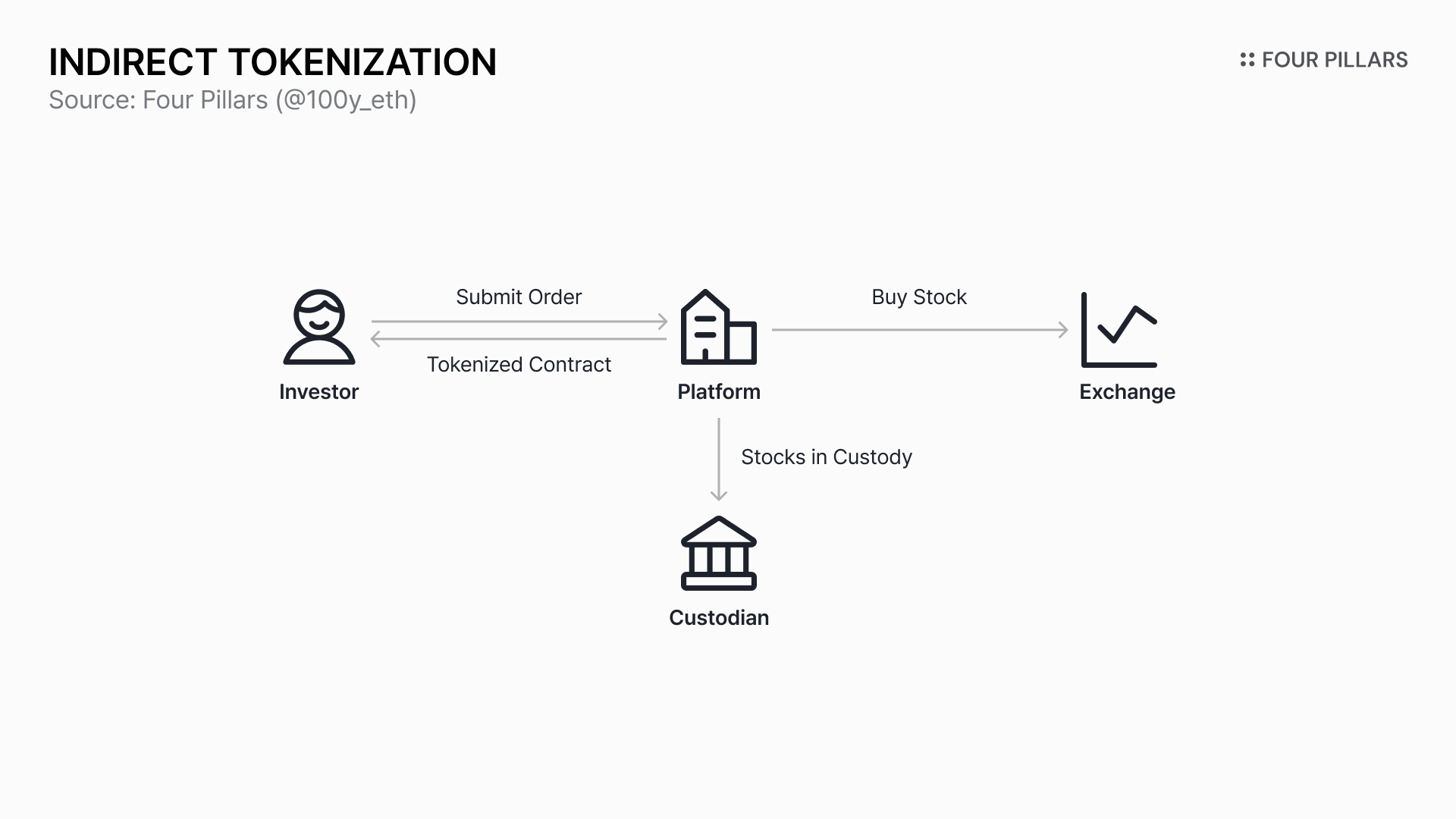

Indirect tokenization is fundamentally different from the direct tokenization and entitlement tokenization approaches discussed above. While the two approaches described earlier tokenize the stock itself or all rights associated with the stock, indirect tokenization, strictly speaking, does not tokenize the stock or the rights attached to it.

Indirect tokenization typically operates as follows:

A user places a stock purchase order on a tokenization platform.

The tokenization company purchases the stock on behalf of the user through a broker.

The purchased stock is held under the name of the tokenization company at a regulated institution such as a custodian or broker.

The company delivers a tokenized entitlement based on the stock to the user.

An important point to note is that the tokenized stock is not actually a stock, but rather a derivative contract between the user and the tokenization company. From the user’s perspective, they receive tokenized exposure in the form of claims and economic rights to the stock held by the tokenization company.

The advantages of indirect tokenization include the following:

Trading availability: Indirect tokenization platforms that directly issue and redeem stock tokens typically support 24/5 trading, while trading of tokenized stocks on blockchain networks is possible 24/7/365.

Global accessibility: Any investor registered on the tokenization platform can access stock tokens.

Optional onchain accessibility: On some tokenization platforms such as xStocks or Ondo Global Markets, even users without KYC can access tokenized stocks onchain.

Optional onchain usability: As an extension of onchain accessibility, stock tokens from certain tokenization platforms can freely interact with onchain DeFi protocols, allowing anyone to easily engage in a wide range of financial activities based on stocks.

However, because indirect tokenization involves companies holding stocks on behalf of users and tokenizing only the associated claims, it comes with many drawbacks:

Indirect ownership: Ownership of the stock or stock related rights belongs entirely to the tokenization company, not the user.

Rights limited to economic returns: Rights such as voting are held entirely by the tokenization company, and users can only access rights related to stock price appreciation and dividends.

Liquidity fragmentation: Even for the same stock, liquidity is not interoperable across different indirect tokenization platforms. For example, although the underlying stock may be the same TSLA, liquidity and regulatory conditions for Backed’s xTSLA and Ondo’s TSLAon are all fragmented.

Inheritance of existing system structure: The many intermediaries involved in the existing system, such as brokerages, DTC, and NSCC, remain in place. Moreover, because stocks are bought and sold using this system and separate contractual agreements are created for tokenization, the overall structure becomes even more complex.

The perpetual futures approach technically falls outside the scope of this report. In the cases of direct tokenization, entitlement tokenization, and indirect tokenization, there is still a one to one backing by actual stocks in some form in order to tokenize stocks. In contrast, the perpetual futures approach merely provides a trading venue that tracks the price of a stock and does not hold the stock itself as an underlying asset. As a result, the perpetual futures approach operates in a fundamentally different way from the three methods above and comes with a distinct set of advantages and disadvantages.

The primary mechanism used by perpetual futures exchanges to create products that track stock prices is the funding fee. This acts as an incentive system that encourages futures prices to track spot prices. For example, if the futures price falls below the spot price, holders of short positions can be required to continuously pay funding fees to holders of long positions in order to incentivize long positions and push the futures price back toward the spot price.

The advantages of the perpetual futures approach are as follows:

Trading availability: While the three tokenization methods discussed earlier cannot be considered fully 24/7/365 due to issuance and redemption processes for stock tokens, the perpetual futures approach enables truly 24/7/365 trading.

Global accessibility: Although this can vary by regulatory jurisdiction, overall global accessibility is significantly higher compared to other tokenized stocks approaches.

Asset diversity: Because stocks are not actually purchased and tokenized, a wide variety of assets can be listed and traded as long as sufficient liquidity is available.

However, because this approach differs significantly from other tokenized stocks methods, it also has the following drawbacks:

Limited rights: Since there is no backing by actual stocks, no rights of any kind can be obtained, including dividend rights.

Liquidity challenges: Unless the perpetual futures market reaches sufficient scale, issues such as widened spreads during off market hours and shallow liquidity are very difficult to resolve, given that trading volume in traditional stock markets remains dominant.

No underlying asset: The perpetual futures approach lacks an underlying asset that can guarantee price integrity.

Lack of onchain composability: Products traded in perpetual futures markets are not tokens. As a result, they cannot be transferred onchain or integrated with other DeFi protocols.

Source: SEC

What, then, is the SEC’s position on each tokenization method? This can be confirmed through the statement released by the SEC.

First, the SEC considers the direct tokenization approach to be safe. In this model, the only change is that the shareholder register managed by the stock issuer, or the company, moves from an internal database to a blockchain. The fundamental nature of the security remains unchanged, and this approach does not violate existing securities laws in any way.

Second, the SEC has taken a conditionally permissive stance toward the entitlement tokenization approach. DTCC seeks to integrate blockchain alongside internal databases for recording stock entitlements, and the SEC recently issued a conditional no action letter allowing this initiative.

Third, the SEC has urged caution with respect to the indirect tokenization approach. This is because the rights involved vary depending on the specific structure used within indirect tokenization, and investors do not hold any direct rights related to the stock itself. Instead, they only hold rights derived from contractual relationships with intermediaries. This is also the reason why companies that fall under the indirect tokenization category are unable to offer services in the United States.

From a personal perspective, I also view indirect tokenization as a transitional approach. As the tokenized stocks ecosystem emerges and regulatory clarity remains limited, platforms that have not obtained licenses appear to adopt indirect tokenization as a way to offer tokenized stocks services. It will be interesting to see whether indirect tokenization platforms, led by Robinhood, grow large enough to become too big to fail, or whether their market share declines as regulations become clearer.

As an aside, which of the categories above do Security Token Offerings, or STOs, in Korea fall under? One of the most important aspects of the Korean STO framework is that issuance, distribution, and ownership information recorded on a blockchain is legally recognized as an electronic registration ledger. In Korea, there is an institution called the Korea Securities Depository, which plays a role similar to that of DTCC. Whereas only the databases of such central clearing institutions were previously recognized as official ledgers, blockchain records are now also legally recognized as official ledgers.

In this sense, the Korean approach is very similar to DTCC’s tokenization model, but there are also many differences. Unlike DTCC, which grants indirect ownership, ownership of electronically registered shares at the Korea Securities Depository is recorded directly under the final investor. As a result, the benefits gained from tokenizing stocks within the existing Korean stock system are not particularly large. In addition, when migrating the electronic registration ledger of currently listed stocks from internal databases to blockchain, shareholder consent is required. For this reason, scenarios in which stocks are tokenized in Korea are, in the short term, almost impossible to expect. A far more realistic approach would be to choose blockchain as the electronic registration ledger from the outset when establishing a company and registering its shares.

Another important aspect of Korean STOs is the introduction of the issuer account management institution system. This system allows securities issuers to directly register and manage tokenized securities on a blockchain without going through securities firms, making it very similar to the direct tokenization approach. However, this model also has its limitations. In Korea, STOs are likely to be permitted only on blockchain networks where more than 51% of the nodes are operated by financial institutions. If this happens, even under the same direct tokenization approach, platforms like Securitize would be restricted in Korea to issuing and circulating security tokens only on private blockchains, unlike their use of public blockchains such as Ethereum.

For these reasons, I believe that Korea’s STO framework represents only a partial tokenization regime. In my view, it needs further improvement to align with global regulatory standards and move closer to genuine financial innovation. For an overview of global regulatory developments, please refer to Part 4 of this report.

3.1.1 Securitize

Securitize is the world’s largest tokenization platform, having tokenized more than $2.5B worth of RWAs. It is also well known for collaborating with the world’s largest asset manager, BlackRock, to issue BUIDL, the BlackRock USD Institutional Digital Liquidity Fund, which is a tokenized money market fund. For reference, excluding gold and stablecoins, BUIDL is the largest RWA token by market size, with a scale of approximately $1.7B.

Securitize provides tokenized stocks through the direct tokenization approach. Among the stocks currently tokenized on Securitize is the blockchain software company Exodus Movement Inc. (EXOD). Stocks scheduled for future tokenization include FG Nexus, which offers merchant banking services and employs an ETH DAT strategy.

Using Exodus Movement Inc. as an example, in order for an investor to hold the stock in tokenized form and trade it on Securitize Markets, which is the ATS provided by Securitize, the investor must directly register the EXOD shares held in their brokerage account via DRS with Pacific Stock Transfer, which is Exodus’s official transfer agent, through Securitize. The detailed process is as follows:

The investor creates an account on Securitize and completes KYC.

The investor contacts their brokerage and requests that their EXOD shares be directly registered via DRS with Pacific Stock Transfer.

Once Pacific Stock Transfer and Securitize confirm that the shares have been transferred, the EXOD shares are reflected in the investor’s Securitize account.

The investor can trade EXOD on Securitize Markets or withdraw the EXOD tokens on Algorand and transfer them to an Exodus wallet.

Securitize plans to tokenize FG Nexus shares in a similar manner, first tokenizing the common shares FGNX and later tokenizing the Class A Preferred shares FGNXP. Notably, FGNXP is a dividend paying publicly listed preferred stock, and once tokenized, it will become the first case of a stock distributing dividends onchain.

For reference, Securitize uses a smart contract called the DS Protocol to enforce compliance related to the issuance, management, distribution, trading, and dividend payments of RWA tokens directly onchain. This serves as a powerful technical foundation for tokenized stocks. Readers interested in learning more about the DS Protocol can refer to my previously written article, “The Infrastructure of Tokenized Securities: How Securitize Powers the RWA Market.”

3.1.2 Superstate

Superstate is a tokenization platform known for issuing USTB, a short term T-Bills fund token, and USCC, a basis trade fund token. Through a service called Opening Bell, Superstate also provides tokenized stocks services. Currently supported tokenized stocks include Galaxy Digital Inc. (GLXY), SharpLink Gaming, Inc. (SBET), and Forward Industries, Inc. (FWDI).

Like Securitize, Superstate adopts the DRS approach to tokenize stocks. After tokenization, it enables issuers to manage shareholder registers and to use smart contracts to distribute dividends, conduct airdrops, or directly sell stocks to shareholders.

3.1.3 (For reference) WisdomTree

As an aside, WisdomTree also offers RWA token products related to stocks. However, unlike Securitize and Superstate discussed above, WisdomTree does not tokenize the stocks themselves. Instead, it tokenizes mutual funds that invest in stocks.

Therefore, WisdomTree’s case is not directly related to this section. Nevertheless, since it still represents a tokenized product that invests in stocks and its tokenization approach resembles direct tokenization, it is mentioned here as an aside to prevent potential confusion among readers.

Source: RWA.xyz

3.2.1 DTCC

In practice, the entitlement tokenization approach relies almost entirely on the existing stock market infrastructure. Because core functions such as clearing, settlement, and custody of traditional stocks are centered around DTCC, this is effectively a tokenization method that cannot be implemented by any entity other than DTCC.

DTCC has long shown interest in handling stocks on blockchain technology. Recently, there was major news in the blockchain industry when DTC, a subsidiary of DTCC and the central institution responsible for settlement, clearing, and custody of securities in U.S. financial markets, received a no action letter from the SEC. This approval allows DTC to officially provide services that tokenize U.S. securities using blockchain technology.

Source: SEC

It is important to note that this approval does not immediately allow all assets and all methods. Instead, DTCC was permitted to operate securities tokenization for a three year period under limited assets and conditions. Nevertheless, this provides DTCC with a foundation to begin real world tokenization in a controlled environment without regulatory risk.

DTCC chose a direction that largely preserves the existing stock system while moving the recording of stock entitlements from DTCC’s internal ledger to a blockchain. In other words, by using blockchain to record which investor holds which stock entitlements, all types of rights associated with stocks, including ownership rights, dividend rights, and voting rights, can be tokenized.

Projects that follow the indirect tokenization approach are very similar in that they purchase stocks on behalf of users, custody them at regulated institutions, and issue tokens representing economic rights. However, depending on the regulatory jurisdiction, there are significant differences in who can access the tokens and whether the tokens can be used onchain.

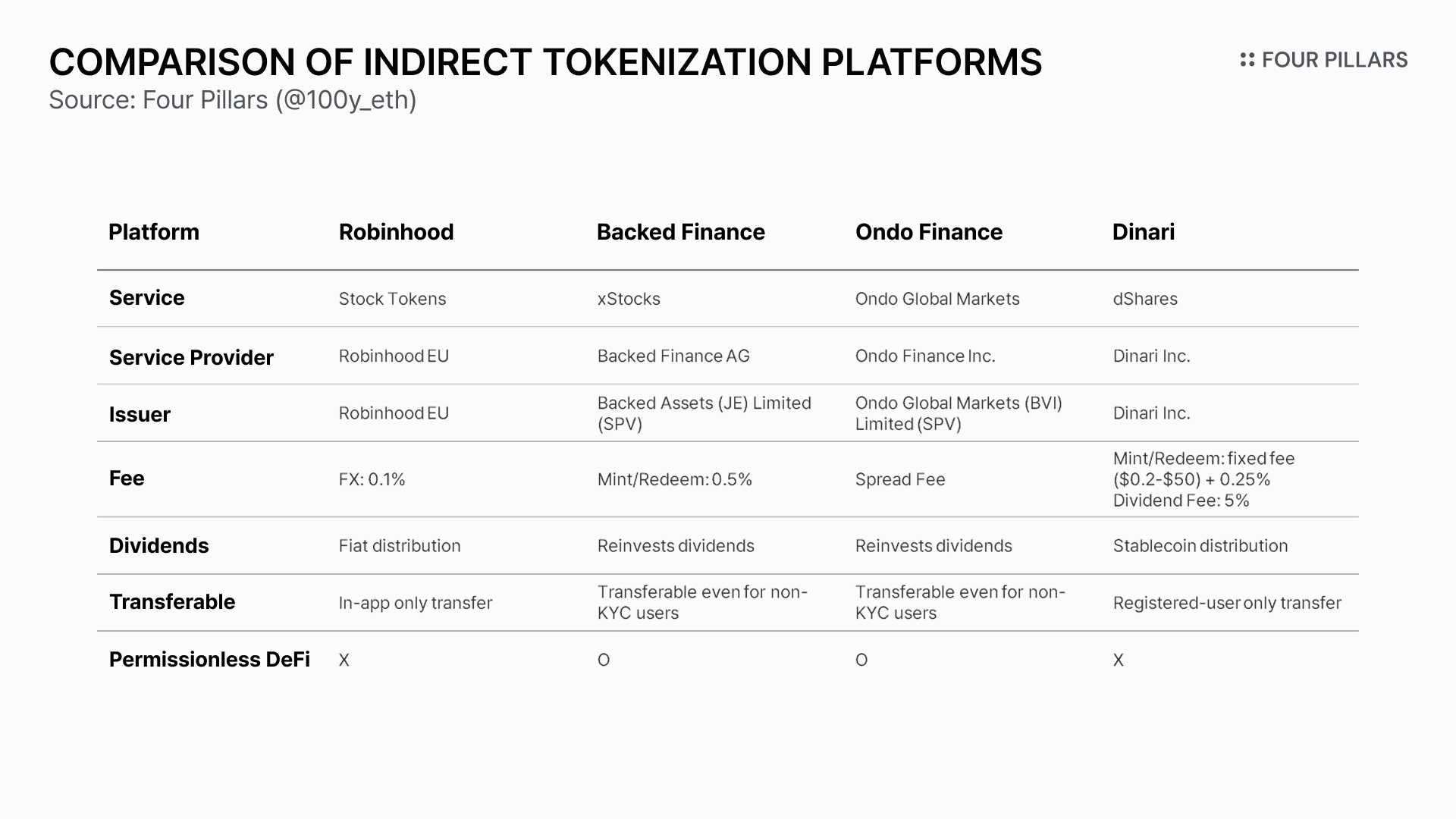

3.3.1 Robinhood

Robinhood is the largest financial super app in the United States. On June 30, 2025, it began offering a tokenized stocks and ETF service for EU customers. Through Robinhood’s Stock Tokens service, European users can trade tokens that track the prices of U.S. listed stocks and ETFs on a 24/5 basis.

The mechanism works as follows. When a user purchases a stock token through the Robinhood app, Robinhood EU buys the underlying stock through a U.S. broker. The stock that serves as collateral for the contract is custodied under the name of Robinhood EU at a regulated U.S. institution. A derivative contract based on that stock is then tokenized and delivered to the user.

Robinhood’s Stock Tokens are not stocks. They are OTC derivatives that track stock prices on a one to one basis, and the derivative contract is entered into between the user and Robinhood EU. These are not simple blockchain tokens, but regulated derivatives under the EU MiFID II regulatory framework. In other words, investors hold a contractual claim against Robinhood EU.

There are no issuance or redemption fees for Stock Tokens. Only a 0.1 percent FX fee is charged. Dividends generated by the underlying stocks are paid to users by Robinhood in fiat currency. Stock Tokens can only be traded within the Robinhood app.

Currently, Robinhood’s Stock Tokens are tokenized and traded on the Arbitrum blockchain. However, Robinhood plans to operate Stock Tokens in the future on its own Layer 2 network built on Arbitrum Orbit.

3.3.2 Backed Finance

Backed Finance is a tokenized stocks platform founded in early 2021. On June 30, 2025, it launched its tokenized stocks service called xStocks. xStocks is accessible to users of major centralized exchanges such as Kraken, Bybit, and Gate, and offers more than 70 stocks and ETFs.

The structure operates as follows. Backed Finance consists of Backed Finance AG, a Swiss headquarters responsible for platform provision, technical support, and strategy, and Backed Assets (JE) Limited, an SPV created for the issuance and redemption of xStocks. On behalf of users who wish to tokenize stocks, Backed Assets (JE) Limited purchases stocks through brokers and custodies them at regulated Swiss financial institutions.

xStocks are not stocks. They are bearer debt securities issued between the user and Backed Assets (JE) Limited. Because Backed Assets (JE) Limited is an issuer registered with the Jersey Financial Services Commission, it is legally permitted to issue securities. In addition, because it holds an EU approved prospectus, xStocks can be legally distributed in European markets under the EU and EEA financial regulatory framework. Notably, Switzerland has a blockchain related regulation known as the DLT Act, under which xStocks can be recognized as proof of securities ownership.

Issuance and redemption of xStocks incur a 0.50 percent fee. There is currently no management fee, but documentation notes that a management fee of 0.25 percent per year may be introduced in the future. This represents relatively high fees compared to other platforms. Dividends from the underlying stocks are reinvested into the stocks and reflected in an increased multiplier applied to the tokens, which raises the effective value of the tokens. While KYC and investor eligibility requirements must be met for direct issuance and redemption, once issued, xStocks can be freely traded and used onchain.

3.3.3 Ondo Finance

Ondo Finance is another representative tokenization platform, best known for U.S. Treasury based tokens such as USDY and OUSG. On September 3, 2025, Ondo Finance launched a tokenized stocks service called Ondo Global Markets, supporting the tokenization of more than 100 U.S. stocks and ETFs.

The mechanism is similar to Backed Finance. Ondo Finance operates an SPV called Ondo Global Markets (BVI) Limited, created solely for issuance purposes. This SPV purchases stocks on behalf of users through a broker, Alpaca, custodies them at regulated financial institutions, and issues stock tokens representing claims on those stocks. Tokenized stocks issued by Ondo Global Markets can also be recognized as proof of securities ownership under Switzerland’s DLT Act.

There are no issuance or redemption fees for Ondo Global Markets tokenized stocks. However, similar to the PFOF structure between Robinhood and Citadel, Ondo Finance can earn spread revenue while processing users’ stock orders. Dividends generated by the underlying stocks are reinvested into the stock tokens, which can result in the actual stock price being higher than the price of the tokenized stocks. As with xStocks, Ondo Finance’s tokenized stocks can be freely traded and utilized onchain.

3.3.4 Dinari

Dinari issues USD+, a U.S. Treasury based stablecoin, but its core product is a tokenized stocks service called dShares. Compared to other tokenized stocks platforms, dShares launched relatively early on August 27, 2024, and currently offers more than 200 stocks and ETF tokens.

The operating model is almost identical to Robinhood’s Stock Tokens. In this context, Dinari Inc. effectively plays the role that Robinhood EU plays in Robinhood’s structure.

dShares carry a relatively high number of fees. During issuance and redemption, a fixed network fee is charged, with $50 on Ethereum and $0.2 on other networks. In addition, depending on issuance size, an order fee of 0.25 to 0.50 percent is charged by network. When dividends are generated, Dinari takes 5 percent of the dividend amount. Dividends from dShares are paid to users in the form of the USD+ stablecoin. As with Robinhood, Dinari’s tokenized stocks can only be transferred among users registered on the Dinari platform.

Historically, finance has always evolved in a direction that improves accessibility. The advancement of finance means enabling more people to engage in a wider range of activities with a broader variety of assets. From this perspective, blockchain is a system that can resolve the inefficiencies and fragmentation of existing financial systems and ultimately emerge as the next generation financial infrastructure.

Humanity currently stands at a critical turning point in financial history. Fiat currencies have already been tokenized at massive scale in the form of stablecoins, and the tokenization of securities such as bonds and stocks is also progressing rapidly. However, because we are in a transitional period where financial infrastructure is being fundamentally reorganized, tokenization methods for stocks, which have complex rights structures, have not yet been standardized and are being attempted in various forms. The fact that, regarding the same legislation, Coinbase CEO Brian Armstrong argues that it effectively bans tokenized stocks, while Securitize and Superstate evaluate it as providing regulatory clarity for tokenized stocks, clearly illustrates how early stage the tokenized stocks market still is.

Tokenized stocks represent an inevitable trend. To realize more efficient stock trading, close collaboration among a wide range of participants across infrastructure, regulation, and the broader industry is essential. With this perspective, this report has examined the major implementation methods of tokenized stocks, the overall ecosystem landscape, global regulatory conditions, and the resulting business opportunities. Amid the complex and rapidly evolving tokenized stocks ecosystem, it is our hope that this report serves as a useful guide for readers.

Dive into 'Narratives' that will be important in the next year