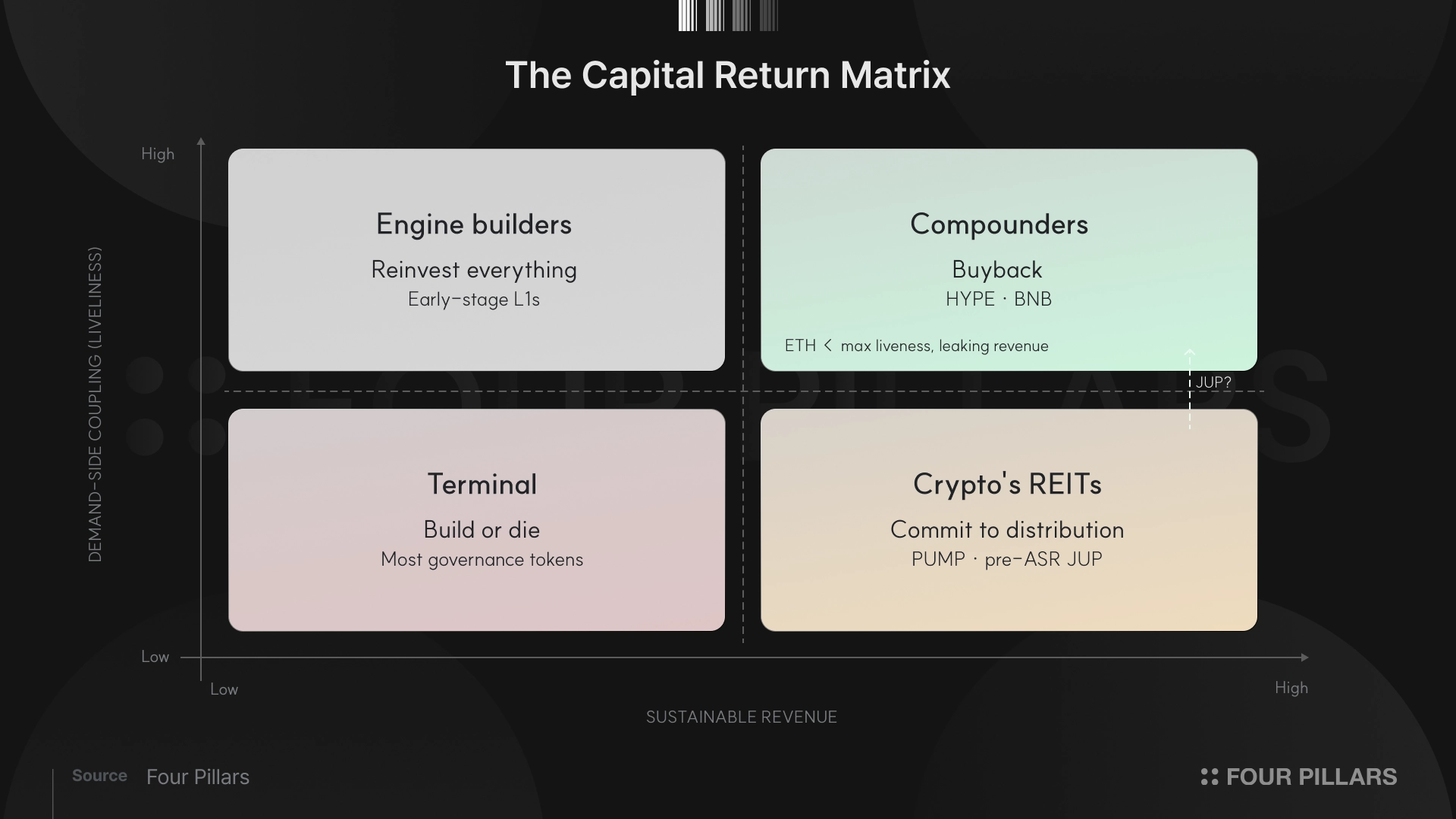

The right capital return mechanism depends on what kind of asset your token is. Buyback, fee switch, and reinvestment are each correct for different quadrants of a liveness/revenue 2x2 matrix.

Buybacks work for tokens that compound with protocol growth; tokens that don't need committed distribution.

Fee switch signals commitment and attracts stable capital, because the yield IS the thesis.

Ethereum proves you need both axes. Maximum liveness (gas, staking, collateral) but L2s captured 95% of the economics. Liveness alone doesn’t translate to value capture.

JUP is an interesting case study because it’s actively trying to change quadrants. Zero emissions, ASR, Offerbook, Lend, prediction markets are all liveness-building moves.

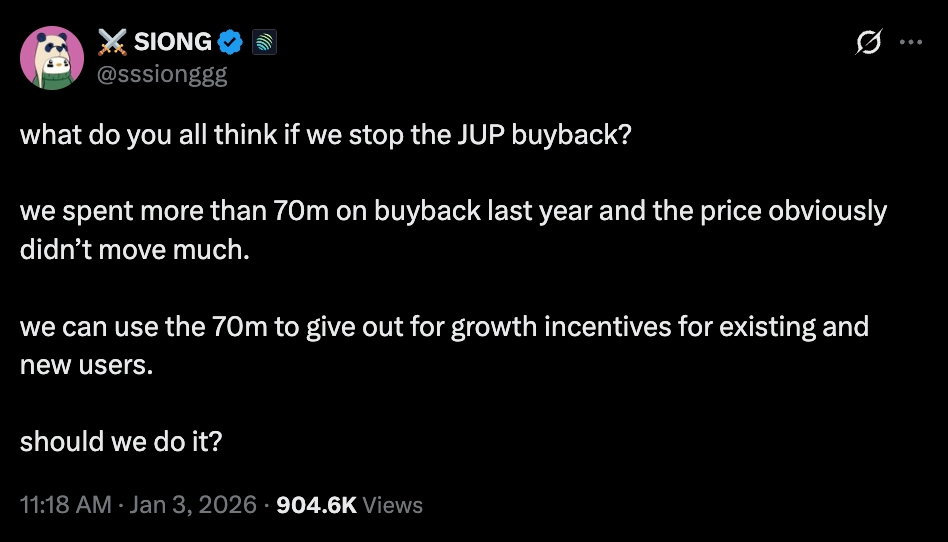

Siong, Jupiter's co-founder, publicly floated killing JUP's $70M annual buyback earlier this year. Within hours, three of the sharpest voices in crypto weighed in with contradictory advice.

Helius CEO Mert said copy Binance (make power users stake JUP for fee discounts, build mechanical demand) and stop the buyback, because buybacks are a pessimistic signal.

Sigil Fund CIO Fiskantes said the quasi-equity signaling matters since buybacks tell the market this token has real claims on cash flows.

Solana Co-Founder Anatoly said deploy capital into products, build the moat, growth over distribution.

All three were right. Watching the replies roll in, what struck me was that they weren't even debating the same question. Mert was answering 'what should an early-stage growth asset do with cash?' Fiskantes was answering 'how does a cash-flow claim signal commitment?' Toly was answering 'what do you do when the moat isn't finished?'

Each answer is correct for a different kind of token, and the fact that all three made sense simultaneously is what made me think the real question isn't 'which mechanism,' but 'what kind of asset is this token?'”

The way I think about it, there are two questions that matter.

Does your protocol generate revenue?

And does your token mechanically benefit from protocol growth?

The second question is the one I find more interesting. I'll call it demand-side coupling: if your protocol's usage doubled tomorrow and nothing else changed (e.g. no new narrative, no listing, no CT thread) would your token price move? Not because of sentiment, but mechanics. Because protocol activity creates direct, on-chain demand for the token itself.

HYPE is the clearest example. Perp volume generates fees that fund the Assistance Fund (AF) buyback. Validators stake HYPE for network security. Gas is paid in HYPE. HIP-1 auction spots require HYPE. HIP-3 requires staking 500K HYPE. Every layer of Hyperliquid's usage feeds back into token demand through distinct channels. Double the volume, and the buyback accelerates, staking yields increase, gas consumption rises. The token compounds with the protocol.

Pre-ASR JUP fails the same test just as cleanly. Swap volume on Jupiter generated USDC fees that flowed to the DAO treasury. The JUP token had governance rights and staking rewards, but the link between "more people swap on Jupiter" and "JUP price goes up" ran through pure sentiment.

Once I started thinking in these two dimensions, four buckets fell out pretty naturally, each with a different correct answer to the mechanism question.

HYPE ($39.32, $9.4B mcap) and BNB ($644, $87.8B mcap) both sit here. Growth compounds through the token, so you don't pull capital out of a compounding engine. You accelerate it.

HYPE buyback reinforces a flywheel that already exists mechanically: more volume, more fees, more buybacks, tighter float, higher prices, more traders. It's defense amplifying offense. BNB runs the same structural play with quarterly burns funded by Binance profit, stacked on exchange fee discounts and Launchpad allocations (centralized rather than on-chain, but the logic is identical). Apple didn't pay dividends for decades because growth compounded through the equity. You don't cut a check when the reinvestment rate is that high.

PUMP live here. Real protocol revenue, no mechanical feedback loop through the token. Nothing wrong with that, but it changes everything about how you return capital.

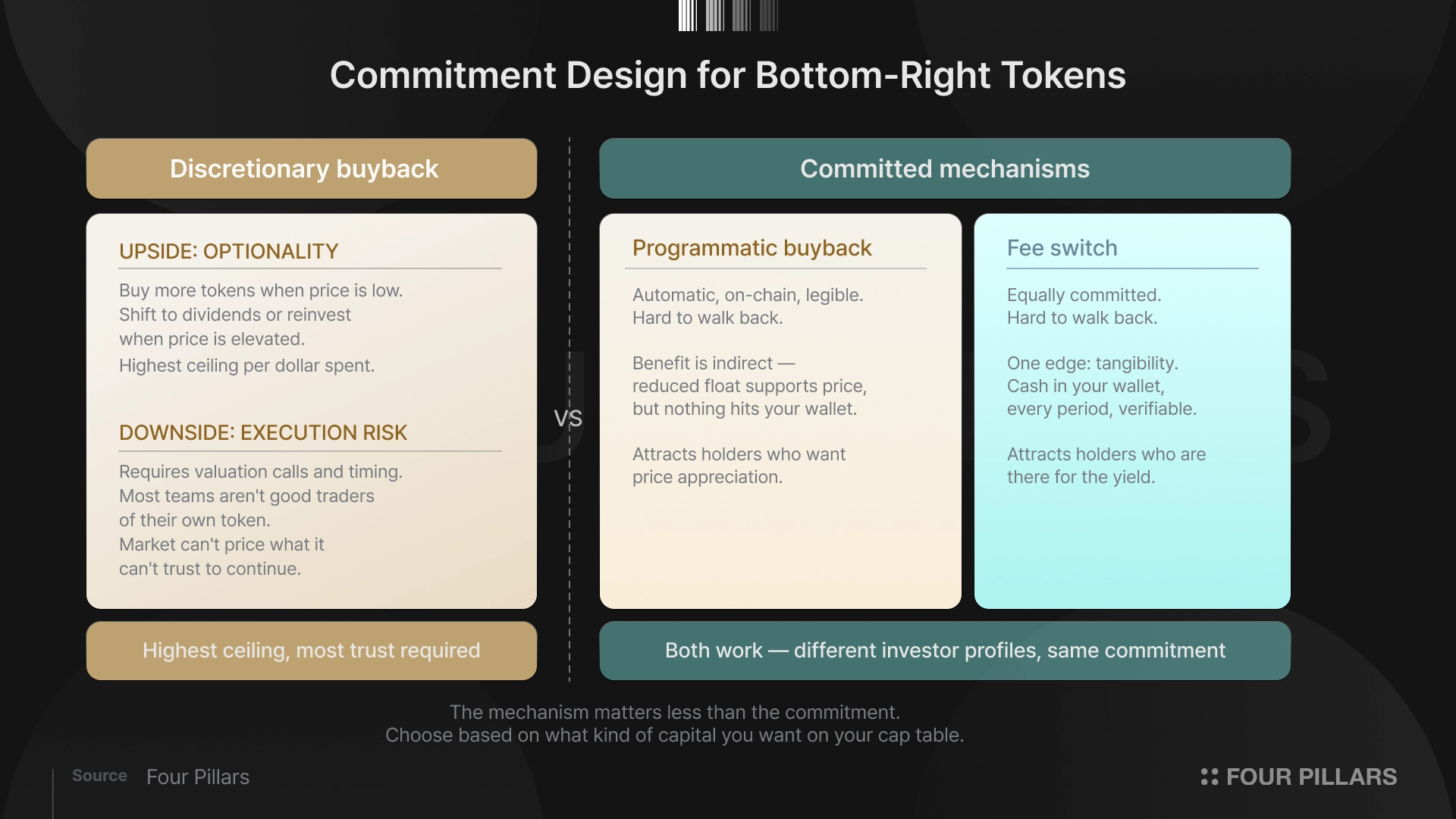

For bottom-right tokens, the buyback is the entire connection between protocol revenue and the token. That makes the commitment design critical, more than the specific mechanism. Programmatic buyback or fee switch both work. A discretionary buyback has the weakest signal, since the team controls timing and size with no automatic forcing function. The market can't price what it can't trust to continue.

That said, discretionary buybacks do have the optionality edge. A well-executed discretionary program can buy more tokens when prices are depressed and shift to dividends or reinvestment when prices are elevated (i.e. better economics per dollar spent). But that optionality comes at a cost. Someone has to make valuation calls and get the timing right. You're turning your capital return program into an active management problem, and most teams aren't equipped to be good traders of their own token. The upside of discretionary is the highest ceiling; the downside is that it requires the most trust and the most skill to execute.

Meanwhile, the one edge a fee switch has over a programmatic buyback is tangibility. A buyback's benefit is indirect. You hope the reduced float supports price, but nothing shows up in your wallet. A fee switch is cash in your wallet every period, verifiable on-chain. For a token where the yield IS the thesis, that explicitness matters. It's the difference between "this token has a claim on cash flows" and "this token has a claim on cash flows, and here's the deposit."

There's also a self-selection effect worth thinking about. Buybacks attract holders who want price appreciation. Fee switches attract holders who are there for the yield, closer to the income capital that anchors dividend stocks in TradFi. Neither profile is better, but they're different, and the mechanism you choose shapes who shows up on your cap table.

REITs distribute 90% of taxable income because the growth is capped, but that doesn't make them an inferior investment. Bottom-right tokens are crypto's REITs.

This is Toly's playbook and it's correct for early-stage L1s building utility before monetization. The coupling exists but there's nothing to distribute. Distributing now is burning runway before the airport is built.

Most tokens. No revenue, no liveness. Whether you buy back, fee-switch, or reinvest is irrelevant; the answer is build liveness or build revenue, preferably both.

If liveness were sufficient by itself, Ethereum would be the most valuable asset in crypto by an even wider margin.

ETH's liveness credentials are unmatched. Gas token for the largest smart contract platform. Over $50B in staking deposits. Primary collateral across DeFi; Aave, Sky, Morpho, nearly every lending protocol denominates risk in ETH. If demand-side coupling were all that mattered, ETH would be the permanent top-right king.

But liveness alone didn't translate to value capture.

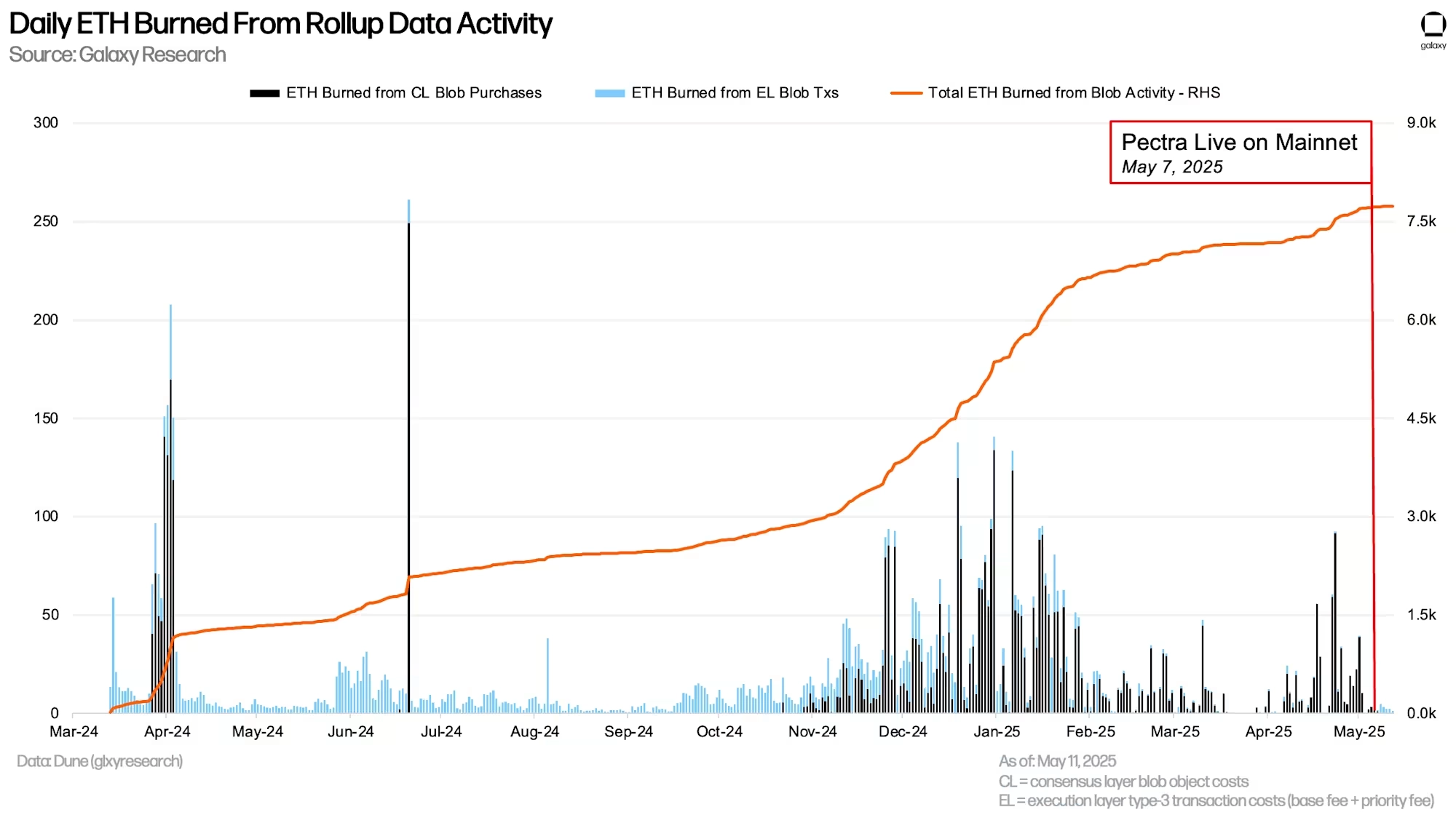

In Q4 2025, L2s paid just $766K in settlement fees back to L1, a 94% year-over-year collapse. For the full year 2024, L2s generated $277M in revenue and paid $113M back to Ethereum. By 2025, that ratio collapsed ($129M in L2 revenue, roughly $10M back to L1, less than 8%). After the Pectra upgrade in May 2025, ETH burned via blobs fell 71%, from 11.22 ETH per day to 3.26 ETH per day.

Source: Galaxy Digital

The L2 roadmap that was supposed to scale Ethereum's economics instead gave away over 90% of them. Vitalik himself acknowledged in February 2026 that "the original L2 model no longer makes sense."

Source: X (@VitaikButerin)

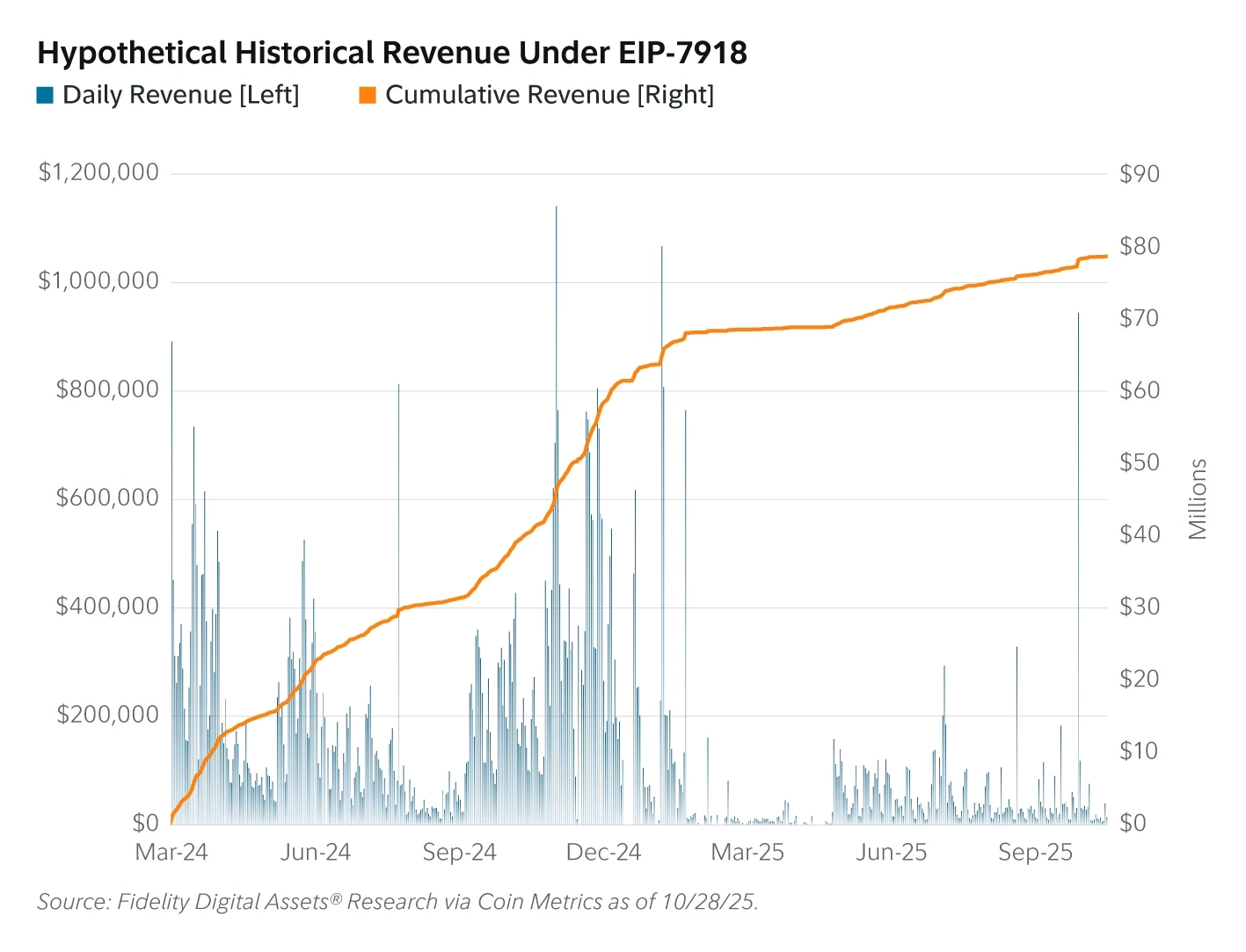

EIP-7918 in Fusaka tries to fix this with a blob fee floor tied to L1 gas cost. Fidelity estimates roughly $78.6M in additional revenue had the floor been active since Dencun. But current blob utilization sits at roughly 29% of the 14-blob target.

Source: Fidelity

Ethereum routes less than 6% of L2 economics back to L1. Meanwhile Hyperliquid routes 100% of protocol fees through the Assistance Fund to buybacks and validator rewards. Same liveness architecture in principle but opposite revenue routing choices. The two axes matter independently, both equally as important. That's what Ethereum's L2 experience suggests, at least at this scale.

JUP is the most interesting test case because it's actively trying to move from bottom-right to top-right. Zero emissions as of February 2026. ASR staking creating lockup incentives. Offerbook, Lend, and prediction markets all building new surfaces where JUP could develop mechanical demand. Every move is a liveness-building move.

What I'm watching for is whether demand-side coupling actually emerges from these features, or whether they're product expansions that generate revenue without routing it through the token mechanically. Most tokens with genuine liveness (HYPE, BNB, ETH) were designed that way from inception. The coupling was architectural, not retrofitted. JUP is trying to retrofit it, and I can't name three tokens that have pulled that off. It's not impossible, but it is rare, and the rarity is itself a data point.

So the next time someone tells you buybacks are always better than fee switches, or that fee switches are always better than buybacks, ask them this question: what kind of asset is this token?

Dive into 'Narratives' that will be important in the next year