What FTX got wrong was not the direction but the execution. In its second year, the exchange posted $1B in revenue, proposed a non-intermediated clearing model to the CFTC, and listed tokenized stocks. The vision FTX laid out mirrors where the entire crypto industry is heading today. What collapsed was not the vision but customer fund misappropriation, Alameda favoritism, and the absence of transparency. QFEX takes that vision and rebuilds it from scratch.

QFEX's edge lies in its trader DNA. The entire team comes from HFT trading houses, and the exchange's microstructure reflects inefficiencies they encountered firsthand: (1) a 100ms speed bump neutralizes latency arbitrage, (2) careful tick size calibration strikes a balance between top-of-book liquidity, tight spreads, and genuine price discovery, and (3) price bands block cascading liquidations before they start.

The TAM for perpetual futures is not crypto. Perps now compete directly with infrastructure serving roughly 6.8M CFD retail traders, $9.6T in daily global FX volume, and over $600T in OTC derivatives notional outstanding. No-expiry leverage, zero rollover burden, and 24/7 access are things legacy instruments never offered.

Perpetual futures are rapidly being institutionalized, yet almost no exchange has been purpose-built for traditional assets from the ground up. Adding traditional assets to a crypto exchange is a different problem from building an exchange for traditional assets. QFEX is the latter. Adding exchange-listed products to a B-Book broker is a different problem from designing on a public order book from day one. QFEX is the latter there, too.

Source: FTX

FTX was actually pretty good. What FTX got wrong was not the direction but the execution. Founded in 2019, the exchange posted over $1B in revenue and more than $250M in operating income in 2021. Considering that Coinbase recorded $7.4B in revenue the same year and listed on Nasdaq, a two-year-old unlisted exchange reaching one-seventh of Coinbase's scale is striking. When you consider that Hyperliquid's annual revenue stands at $844M, widely regarded as one of crypto's most successful products, FTX's $1B figure is all the more impressive given it was recorded four years earlier.

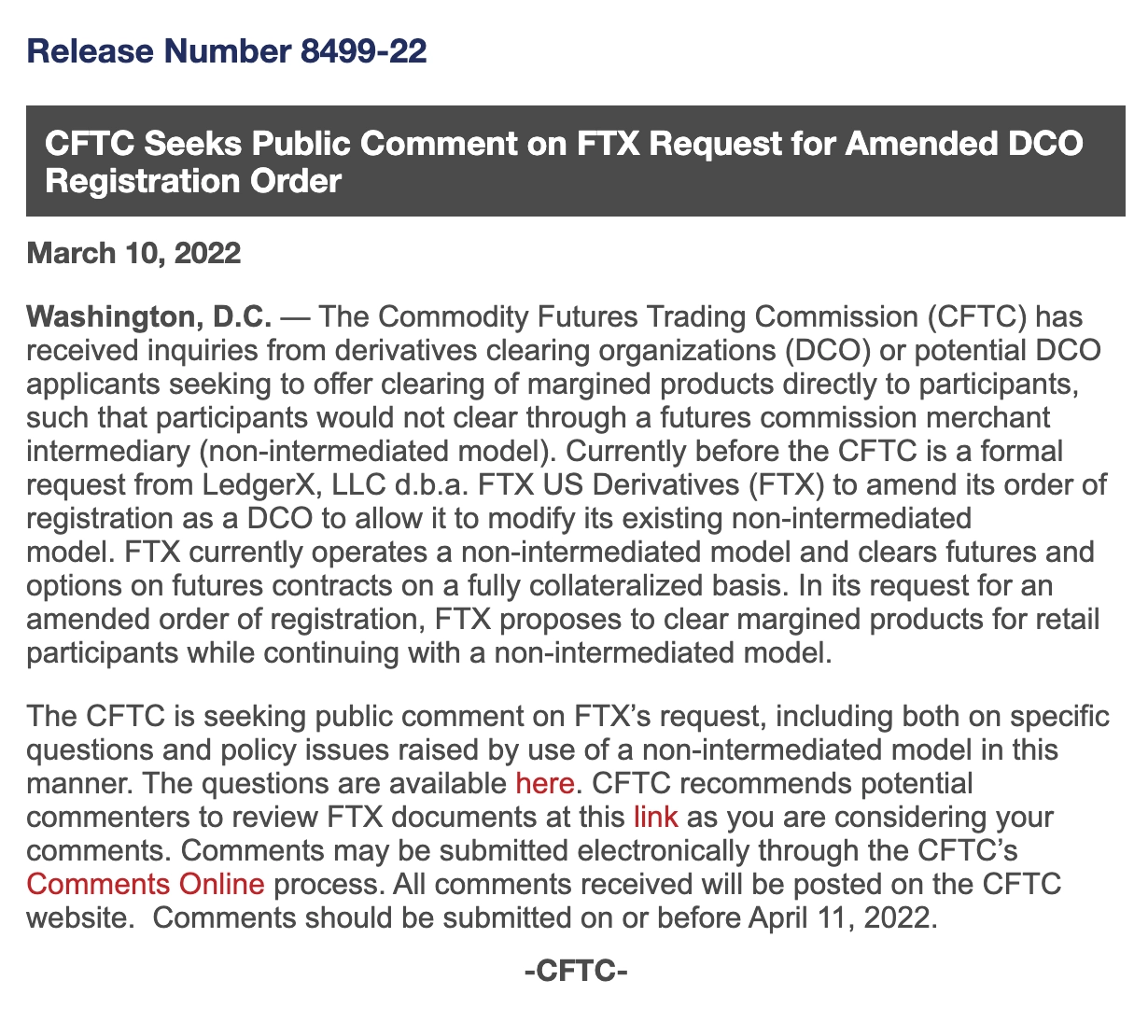

Source: CFTC

The numbers were not the only thing that stood out. FTX introduced several industry-first concepts. The exchange attempted to bring the integrated model that had already been working on crypto exchanges, where trade execution, margin management, and clearing all run within a single platform, into the traditional financial regulatory framework. To that end, it formally proposed a non-intermediated clearing model to the CFTC. Rather than the current structure where exchanges, clearinghouses, and brokers operate separately, the proposal envisioned retail investors depositing margin directly with the clearinghouse. The idea was ultimately blocked by pushback from the traditional finance industry, but it carried enough substance to warrant academic review.

"FTX was also the first crypto exchange to list tokenized equities such as TSLA and AAPL, brokering traditional asset trading on crypto infrastructure. It further pioneered pre-IPO markets and launched prediction markets for events such as U.S. elections early on. In the U.S., FTX acquired LedgerX, a CFTC-licensed derivatives exchange, in a push to enter the regulated market. It recruited a former CFTC commissioner and testified before Congress. In this way, FTX was the exchange that tried most directly to bridge traditional finance and crypto, much like the direction the crypto industry is heading today.

Source: Coindesk

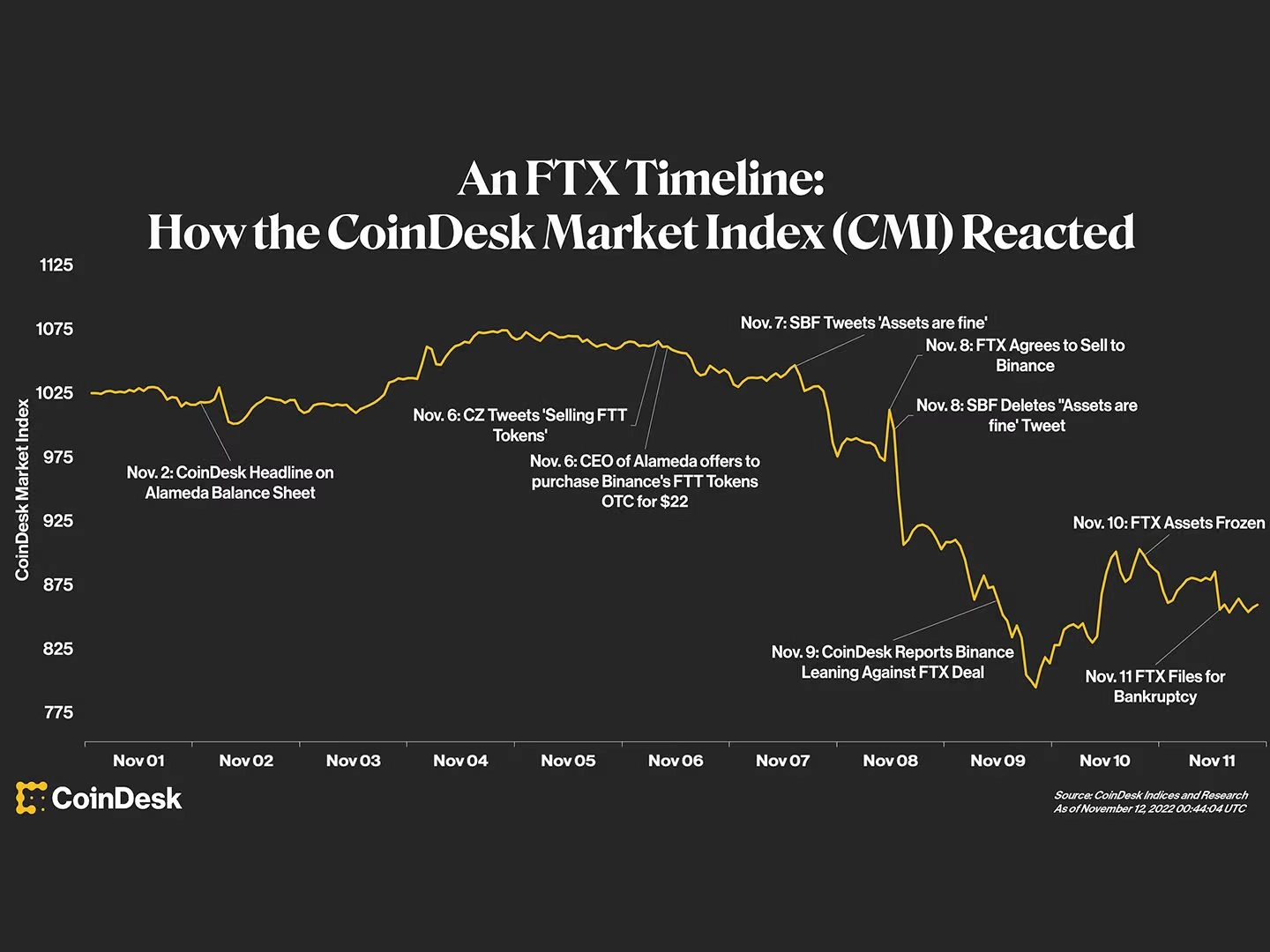

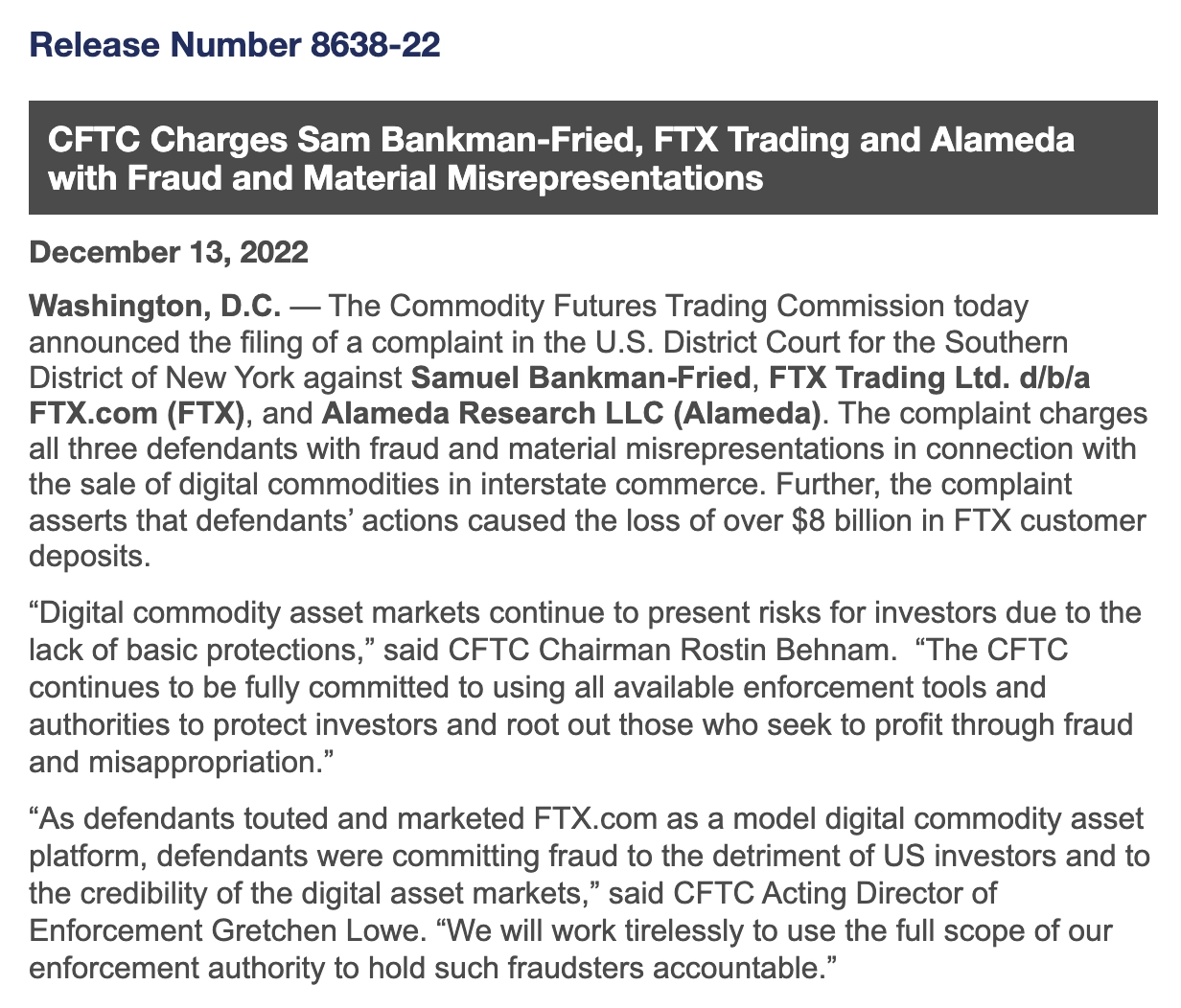

But everyone knows how this exchange ended. None of these efforts prevented $8B in customer asset misappropriation, the exchange's bankruptcy, or CEO Sam Bankman-Fried's 25-year prison sentence. It began when CoinDesk reported a document revealing an outsized FTT concentration on Alameda's balance sheet, triggering a mass withdrawal. Customer deposits had been diverted to fund Alameda's trading, and Alameda had been expanding positions on effectively unlimited credit. When FTT prices fell, collateral values eroded rapidly, and insolvency followed in the absence of sufficient liquidity.

Source: QFEX

FTX collapsed. Despite faster growth and higher profitability than virtually any other exchange, the combination of customer fund misappropriation, entanglement with Alameda, and a structure that leveraged a self-issued token as collateral left it as one of the largest bankruptcies on record. And yet, there is an exchange that wants to rebuild FTX. QFEX is also a centralized exchange. It carries forward the vision of replacing traditional financial infrastructure by unifying exchange, clearinghouse, and broker into one, the focus on traditional assets such as equities and commodities, and the trader DNA, while redesigning from scratch the structures that brought FTX down.

"Replacing the $100B exchange and clearinghouse industry and rebuilding FTX" sounds radical. But the team's track record in trading engine design and high-frequency trading is clear. What market QFEX is targeting, and what kind of exchange it has designed to serve that market, is what follows.

In November 2022, when FTX collapsed, QFEX CEO Annanay Kapila was on the crypto team at Tower Research Capital. Working the trading desk, he watched in real time as FTX withdrawals froze, the API buckled under load, and liquidity evaporated.

Tower Research was processing significant volume on FTX at the time, so the team felt the shock directly. Colleagues scrambling to extract funds through any available channel, the moment when normal market making became impossible and counterparty risk materialized in real time.

The FTX collapse sent shockwaves across the entire crypto industry, but those who felt it most acutely were the HFT (High Frequency Trading) firms that had been using FTX as a trading venue. In an interview, Annanay recalled that even after FTX went down, there was a shared consensus in the HFT industry that "FTX's innovativeness deserved recognition." Tower Research, Jump Trading, and Jane Street knew from daily practice that FTX's product-level innovations, such as the Quant Zone for automated strategies, the ability to use USDC and USDT jointly as margin, and the breadth of listings, were in a different league from other crypto exchanges.

"We're building FTX without the fraud" is QFEX's vision, and it emerged from this context. What QFEX learned from FTX, and what it deliberately did not carry forward, deserves a closer look.

2.1.1 FTX's Customer Asset Misappropriation

In a traditional futures trade, a single retail order travels through CME (exchange) to CME Clearing (clearinghouse) to an FCM (futures commission merchant) such as Goldman Sachs, and finally to the customer. Retail cannot access the clearinghouse directly and must go through an FCM. Each is a separate legal entity, each charges fees, and margin passes through the FCM to the clearinghouse.

FTX and other crypto exchanges proved that collapsing this structure into one platform enables real-time margin, instant clearing, 24/7 operation, and the elimination of intermediary fees. As noted, FTX formally proposed this non-intermediated clearing model to the CFTC, seeking to bring a structure already functioning on crypto exchanges into the U.S. regulated futures market.

However, the BIS (Bank for International Settlements) classified FTX and similar integrated entities not as novel financial infrastructure but as "crypto conglomerates" combining exchange operations, token issuance (FTT token), and proprietary trading. In traditional finance, even when an exchange, clearinghouse, custodian, and prop trading arm sit within the same group, each is required to maintain separate governance and legal functional separation.

This is to prevent losses in one division from eroding customer assets in another, and to block the prop trading arm from exploiting exchange operational information. The underlying premise of traditional financial regulation is that separation protects customers better than integration.

2.1.2 QFEX's Fund Segregation

In hindsight, the BIS was right. FTX lent customer deposits to Alameda, and Alameda used them for venture investments, real estate, and FTT-collateralized loans. Decision-making records were managed through auto-deleting messengers, and basic systems for accounting, cash management, and cybersecurity were absent. Pursuing integration without transparency, independent audits, asset segregation, or internal controls is what led to granting a subsidiary exemption from liquidation and misappropriating customer assets.

QFEX carries forward the integration thesis but embeds the safeguards that FTX lacked. Customer funds are held in segregated custody at BitGo Bank & Trust, National Association, a national bank chartered under the OCC (Office of the Comptroller of the Currency). BitGo Bank is legally required to separate customer assets from exchange operating funds, making it structurally impossible for the exchange to access or misappropriate customer capital.

With conflicts of interest blocked, the efficiencies of integration can be fully realized. Matching, clearing, and risk management run within a single software stack, so trades settle at the moment of execution without an intermediary broker, and margin is recalculated in real time. The T+1 settlement delay, inter-institutional margin transfer costs, and 24/7 operational complexity that are unavoidable when exchanges and clearinghouses are separated are eliminated in the integrated model.

Trader DNA is where FTX and QFEX share the most direct lineage. FTX was famously built by Jane Street alumni SBF and Gary Wang. That background produced per-second real-time margin calculation, cross-margin pooling BTC, ETH, and stablecoins into a single collateral pool, and 24/7 blockchain-based deposits and withdrawals that could meet margin calls within minutes. These features did not exist on other crypto exchanges at the time, and this level of detail is why the HFT industry acknowledged FTX's superiority.

QFEX was built by Annanay Kapila, who was on Tower Research's crypto trading desk, and Joshua Wharton, a Citadel alumnus. The rest of the team comes from Jump Trading, Hudson River Trading, Optiver, Jane Street, and other global trading houses.

This background is reflected in HFT-grade market microstructure design embedded throughout the exchange. These are granular components of the trading engine that are invisible to most users, but they govern how trades are executed: order matching priority, time precedence between orders, and how tick size affects liquidity competition. This structure is what ultimately determines market maker participation incentives, the spreads end-users experience, and execution quality.

100ms speed bump: HFT firms place orders tens to hundreds of times faster than ordinary traders to front-run price movements, a practice known as latency arbitrage. QFEX imposes a uniform 100ms (0.1 second) delay on all limit orders, neutralizing this speed advantage. Cancellations and liquidity-adding orders are exempt, so market makers can update quotes quickly without interference. This follows the same design philosophy as IEX (Investors Exchange), which received SEC approval for a 350-microsecond (0.00035 second) speed bump addressing the same problem in U.S. equities.

Dynamic tick size: QFEX recalibrates tick sizes weekly. Tick size is the minimum price increment between quotes. If the tick size is $0.01, the next quote after $100.00 is $100.01. When this interval is too wide relative to volatility, market makers cannot compete by offering better prices and are forced into pure speed competition at the same price level. Only the one or two fastest firms survive, creating a monopoly structure. Most traditional exchanges rarely update tick sizes. QFEX recalibrates weekly to match changes in volatility, maintaining fair competition among market makers.

Price bands: Orders beyond equity ±10%, index ±5%, and FX ±2% are automatically rejected at the matching engine level. This differs from a circuit breaker. Circuit breakers halt trading after a crash has already occurred. Price bands reject orders that could cause a crash before execution. The May 2010 Flash Crash, when the Dow Jones dropped roughly 1,000 points (9%) in minutes, is the classic example. A single order at an extreme price punched through the order book, triggering liquidations that filled at extreme prices and triggered further liquidations in a chain reaction. Price bands cut the first link of that chain.

Identity verification: Most crypto perp exchanges allow trading with nothing more than a wallet connection, no KYC required. Accessibility is high, but it also means attackers can create unlimited accounts. In Hyperliquid's JELLYJELLY incident, the attacker executed self-liquidations across multiple accounts precisely because of this.

QFEX blocks this attack vector, but not through traditional document ID verification + KYC. With advances in AI, document-based ID verification is proving easier and easier to bypass. Instead, QFEX uses an advanced vendor solution that combines digital fingerprinting, transaction analysis, usage pattern analysis, and wallet blockchain data within an AI model. This enforces compliance policies strictly and enforces single-user-per-account on a best-effort basis, programmatically blocking the multi-account attack vectors that underpin most DEX exploits. Institutional traders undergo a separate, extensive KYB process.

Most crypto perp exchanges allow trading with nothing more than a wallet connection, no KYC required. Accessibility is high, but it also means attackers can create unlimited accounts. In Hyperliquid's JELLYJELLY incident, the attacker executed self-liquidations across multiple accounts precisely because of this. Rather than relying on traditional document-based ID verification, which AI advances are making increasingly easy to bypass, QFEX uses an advanced vendor solution that combines digital fingerprinting, transaction analysis, usage pattern analysis, and wallet blockchain data within an AI model. This enforces compliance policies strictly and enforces single-user-per-account on a best-effort basis, programmatically blocking the multi-account attack vectors that underpin most DEX exploits. Institutional traders undergo a separate, extensive KYB process."

These features, the speed bump, dynamic tick size, price bands, and KYC trading, look like individual functions but share a common design direction. They block speed-based monopolies, promote fair competition among market makers, and prevent the system from becoming self-destructive under extreme scenarios. All of them reflect experience from market making and high-speed trading, where the team directly identified and exploited market inefficiencies, now embedded into QFEX's trading engine.

The fact that FTX's tokenized equities were a facade also came to light around the time of its collapse. Annanay mentioned this anecdote directly in a podcast. An acquaintance who held Tesla stock tokens on FTX attempted to redeem them and physically visited the office of the Swiss entity in Zug that was designated as the custodian. The door was locked. The office was empty. The claim of 1:1 physical backing had never been real.

2.3.1 Why QFEX Chose Perpetual Futures

Source: QFEX

FTX was one of the earliest examples of listing traditional assets on a crypto exchange. It offered tokenized trading in equities such as TSLA and AAPL through an indirect tokenization model where the underlying asset is physically backed 1:1, similar to today's Backed Finance or Ondo Finance. This approach was advanced enough to remain in use today. The broader direction of listing high-demand blue-chip assets beyond crypto on an exchange is something QFEX has carried forward directly. QFEX currently supports 15 U.S. single stocks (NVDA, TSLA, etc.), 2 U.S. indices (S&P 500, Nasdaq 100), 5 commodities (natural gas, gold, etc.), and 2 FX pairs (GBP/USD, EUR/USD).

Setting aside the fact that FTX did not actually hold the physical assets, tokenization is structurally distant from the kind of trading QFEX is built for. In high-frequency, two-way leveraged trading, the transaction costs inherent in a tokenization structure are prohibitive.

When a tokenized stock's price diverges from the underlying asset, arbitrageurs must mint or redeem tokens to converge the price. The mint/redeem fee paid to the issuer runs 0.1% to 1% of the transaction amount. Price divergences below this cost threshold are not corrected because arbitrage cannot turn a profit. The result is a spread floor of 0.1% to 1% for tokenized equities. Compared to spreads below 0.01% for the same stocks on the NYSE or Nasdaq, this is tens to hundreds of times wider.

This is why QFEX delivers traditional asset trading through perps rather than tokenization. Perps require no ownership or custody of the underlying asset, so mint/redeem mechanics do not exist. Price convergence is maintained through the funding rate mechanism. No backing costs, no backing audits, no backing-absence risk. In theory, any asset can support a leveraged position as long as price indexing is secured. Perps preserve 24/7 crypto-native accessibility while eliminating the structural costs of tokenization, making them the most fitting instrument for QFEX.

2.3.2 Price Sourcing and Funding Rates for Traditional Assets

Unlike crypto assets, traditional asset perpetual futures face additional design challenges. Price sourcing and funding rates are the two primary examples.

First, price sourcing for traditional assets presents problems that crypto does not have. Crypto trades 24/7 across exchanges like Binance and OKX, so a reference price always exists. Traditional assets must pull prices from external legacy exchanges, and off-hours when markets close create windows with no reference price at all.

Most exchanges, including those built on HIP-3, route underlying prices through oracle networks such as Pyth Network or Chainlink. Exchange-origin data passes through an oracle, then through a relayer, and finally arrives onchain. Each additional relay stage introduces latency, and data quality at each stage depends on the oracle provider's infrastructure.

QFEX bypasses oracle networks entirely, sourcing primary market data directly for each asset class. With no intermediate layer between the exchange's original feed and QFEX's matching engine, price latency and third-party infrastructure dependency are minimized. During periods when external prices go completely dark, such as weekends, QFEX reduces risk exposure by capping positions at 10% of normal levels rather than relying on an internal oracle.

Equities: Real-time feeds from the NYSE and Nasdaq are used as the base. This covers U.S. equity regular and extended trading hours. Outside these hours, overnight data comes from Blue Ocean ATS, an alternative trading system that provides trading in major U.S. equities during U.S. overnight hours, ensuring access to external data based on actual executed prices even at night.

Indices: S&P 500 and Nasdaq 100 prices are derived from CME E-mini futures. While the cash index is calculated only during regular hours, CME futures trade nearly 24 hours from Sunday evening to Friday afternoon, enabling underlying price tracking overnight.

FX/Commodities: ECN (Electronic Communication Network) feeds are used. An ECN is an electronic trading system that directly matches buy and sell orders from banks, brokers, and institutional investors without a central exchange. Because FX and precious metals liquidity is distributed across multiple ECNs rather than a single exchange, QFEX aggregates quotes from the most liquid ECNs to calculate optimal prices.

Funding rates are a more demanding area. In crypto perps, the underlying asset trades 24/7, so funding rate design is relatively straightforward. Equity markets, however, are open only 6.5 hours a day and shut entirely on weekends. Perps trade 24/7 while the underlying is closed. How to handle price divergence during these hours is the central challenge for traditional asset perpetual futures. Crypto-proven funding rate formulas cannot be applied as-is. Funding intervals, interest rate structure, and closed-market handling all need to be redesigned for traditional asset characteristics. QFEX addresses this with several solutions.

1-hour funding intervals: Most crypto exchanges charge funding every 8 hours. QFEX uses 1-hour intervals. Traditional assets have lower volatility than crypto, and an 8-hour interval is too slow to correct price divergence. Shorter intervals improve price tracking accuracy.

Zero funding during market close: Funding rates work by charging the side whose position diverges from the underlying, pushing the price back toward convergence. But when markets close, the underlying price stops updating. Perps keep trading while the reference stands still. Trade.xyz (HIP-3) charges funding during closed hours based on the last closing price. When the perpetual price moves away from the close, the diverging side pays, effectively anchoring the price near the close.

The problem arises when a market-moving event actually occurs during closed hours. If a geopolitical shock hits on a Friday night, equities should gap down at Monday's open. But if weekend funding kept the perpetual anchored to Friday's close, the price adjustment and a wave of liquidations all hit at once when markets reopen. QFEX sets funding to zero during market close. It does not force a reference when no reference exists. Traders can freely form prices reflecting real expectations even while markets are closed, and if a gap occurs at the open, the perpetual has already moved in that direction, distributing the shock.

Source: CFTC

The entity that absorbed liquidation positions the market could not handle on FTX was Alameda Research. FTX described this role as the BLP (Backstop Liquidity Provider) mechanism, but according to the CFTC complaint, the primary participant in the BLP was Alameda.

As the sole backstop, Alameda had exclusive visibility into the size and timing of liquidation flows, which translated directly into a trading edge. Former Alameda CEO Caroline Ellison testified in court that this structure had been profitable for an extended period but exacted catastrophic costs during events like the Terra collapse. A single backstop is efficient in normal conditions, but in extreme market stress, the backstop itself becomes the systemic risk.

More critically, Alameda's account had an "Allow Negative" flag set in the code. It could trade with a negative balance, and automatic liquidation was disabled. The risk engine operated strictly for every other user, but the affiliate running the largest positions on the platform was granted an exception.

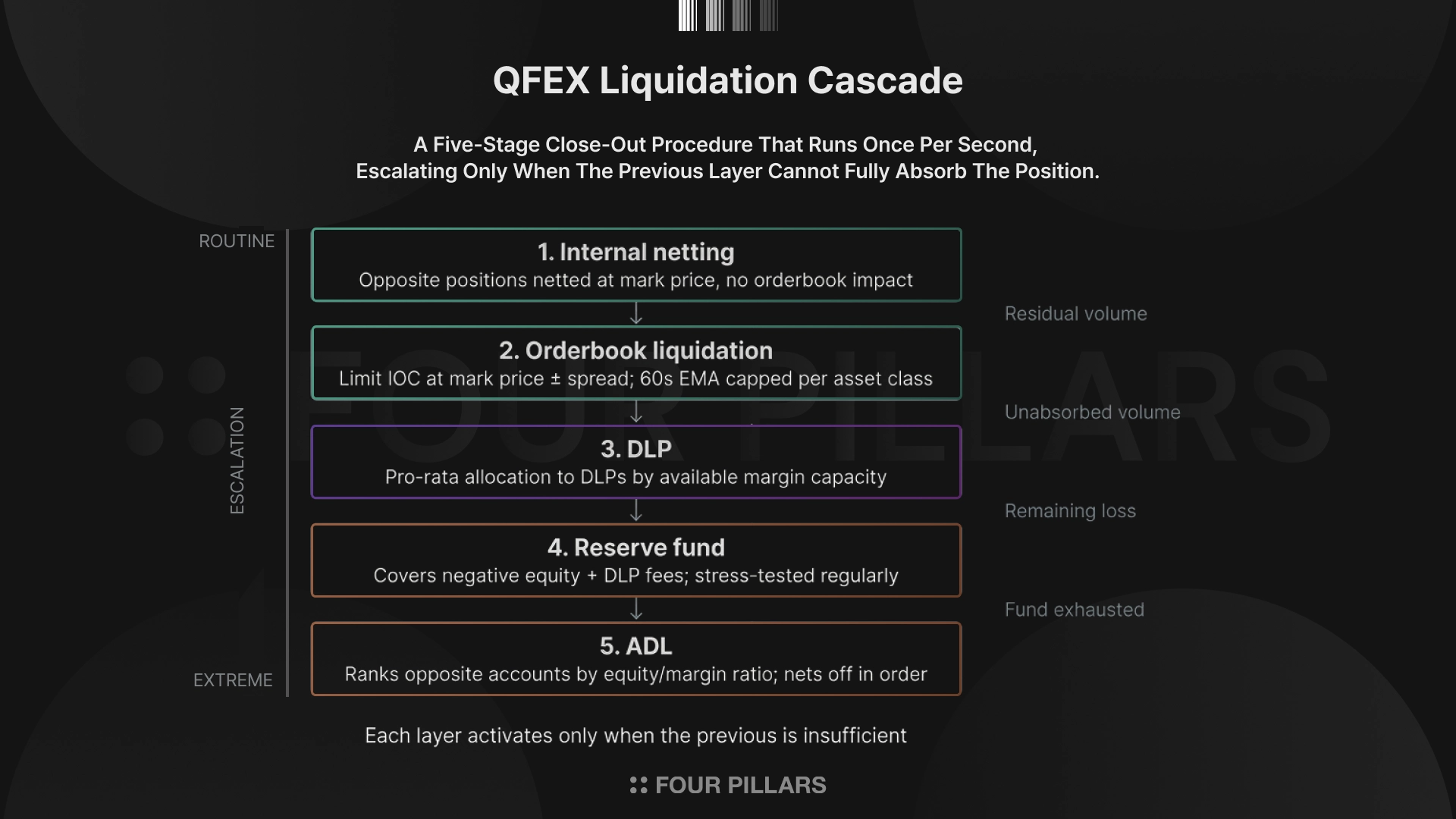

To prevent this type of failure, QFEX first distributed the single backstop structure into a 5-stage sequential liquidation (cascade) process:

Internal netting: When liquidation positions exist in opposite directions simultaneously, they are offset at the Mark Price without hitting the order book. Liquidation volume is absorbed internally before reaching the order book, preventing market price impact.

Order book liquidation: Liquidation volume is released into the order book based on a 60-second EMA (Exponential Moving Average), capped at time-of-day limits (regular hours $100K, overnight $50K, weekends $10K). The EMA prevents liquidation volume from flooding the order book at once and crashing prices.

DLP (Designated Liquidity Provider): An opt-in program for qualified market makers. When the order book cannot absorb liquidation volume, participating market makers take on liquidation positions on a pro-rata basis according to available margin. The pro-rata allocation prioritizes DLPs whose absorption of the liquidation would reduce their overall risk exposure on the exchange, derisking the system as a whole. Under this structure, a single entity monopolizing the backstop, as Alameda did, is structurally impossible.

Reserve Fund: Funded by residual collateral and excess margin from liquidations, with additional contributions at QFEX's discretion. Its purpose is to prevent customer account balances from going negative. DLP fees are also paid from this fund.

ADL (Auto-Deleveraging): A last-resort safety mechanism activated only when the Reserve Fund is exhausted. Positions on the opposite side with the largest profits are reduced sequentially.

As this liquidation mechanism shows, QFEX prioritizes risk management above all. No matter how robust the liquidation process, if the incoming liquidation volume overwhelms the system, no structure can hold. Leverage settings typically determine that volume.

FTX used up to 101x leverage as a marketing point, and DEXs trailing Hyperliquid continue to offer 50x or higher on BTC/ETH in a leverage arms race. Higher leverage attracts users more easily, but the risk of cascading liquidations under market stress scales proportionally.

QFEX offers comparatively lower leverage: 10x on single stocks, 30x on gold/indices, 50x on FX. Overnight, positions are capped at 50% of normal levels; on weekends, 10%. This structurally suppresses the scenario of large-scale cascading liquidations during thin-liquidity hours when the underlying market is closed. Rather than raising leverage to acquire users, QFEX chose to build a risk framework that institutions and professional traders can trust.

The Allow Negative flag on FTX-Alameda accounts is a problem of a different order. The moment a risk engine exception is granted to a specific account, trust in the entire risk management system collapses. QFEX's liquidation rules apply identically to every account, and account-level exceptions do not exist at the architecture level. The goal is to make it impossible for the exchange operator to selectively override its own rules.

What position can QFEX carve out as it enters the market? At first glance, perps look like a market where competition has already ended. On the CEX side, Binance maintains a 29.3% market share with $25T in annual volume, followed by OKX and Bybit at roughly 21% each. On the DEX side, Hyperliquid commands more than half of onchain perps volume. Both revenue and open interest share confirm the dominance on each side.

This view, however, rests on the assumption that perps competition plays out only within crypto. As the efficiency of perps as a trading format is increasingly proven, that assumption is breaking down.

The CEX vs DEX distinction no longer holds meaning. Coinbase's vision of the "Everything Exchange" captures it well. Not just Coinbase, but every exchange is trying to become an exchange for every asset. Fintechs trade crypto. CEXs list equities. DEXs list gold and the S&P 500. Legacy exchanges adopt blockchain rails. Neither asset type nor onchain vs. offchain serves as a dividing line anymore.

Fintechs are trading crypto: Robinhood acquired Bitstamp for $200M in 2025, expanding aggressively into crypto exchange operations. Crypto trading revenue hit $680M in the first nine months of 2025, up 154% year over year. In the EU, it offers crypto perps and over 1,000 tokenized equities under a MiFID license.

CEXs are trading traditional assets: Binance listed tokenized U.S. equities in partnership with Ondo Finance. Coinbase launched stock perpetual futures covering every Mag7 name.

DEXs are listing traditional assets on their order books: Hyperliquid offers gold, silver, and S&P 500 perpetual futures onchain. HIP-3-based Trade.xyz secured an exclusive S&P 500 index license from S&P Dow Jones Indices and listed an officially licensed S&P 500 perpetual futures contract onchain.

Legacy exchanges are going onchain: Nasdaq is building a 24/7 tokenized securities trading system pending SEC approval. DTCC (Depository Trust & Clearing Corporation) is piloting blockchain-based real-time settlement. 24/7 operation, instant settlement, and blockchain rails are no longer unique to crypto exchanges.

The only remaining difference is who delivers the same asset on what infrastructure. Labels like CEX, legacy exchange, fintech, and DEX tell you where a platform started. They no longer describe what it offers.

What remains is a single competitive axis: who delivers the same asset on faster, cheaper, and safer infrastructure. From this perspective, it is worth revisiting the legacy instruments that have been providing leverage on traditional assets.

3.2.1 CFD (Contract for Difference)

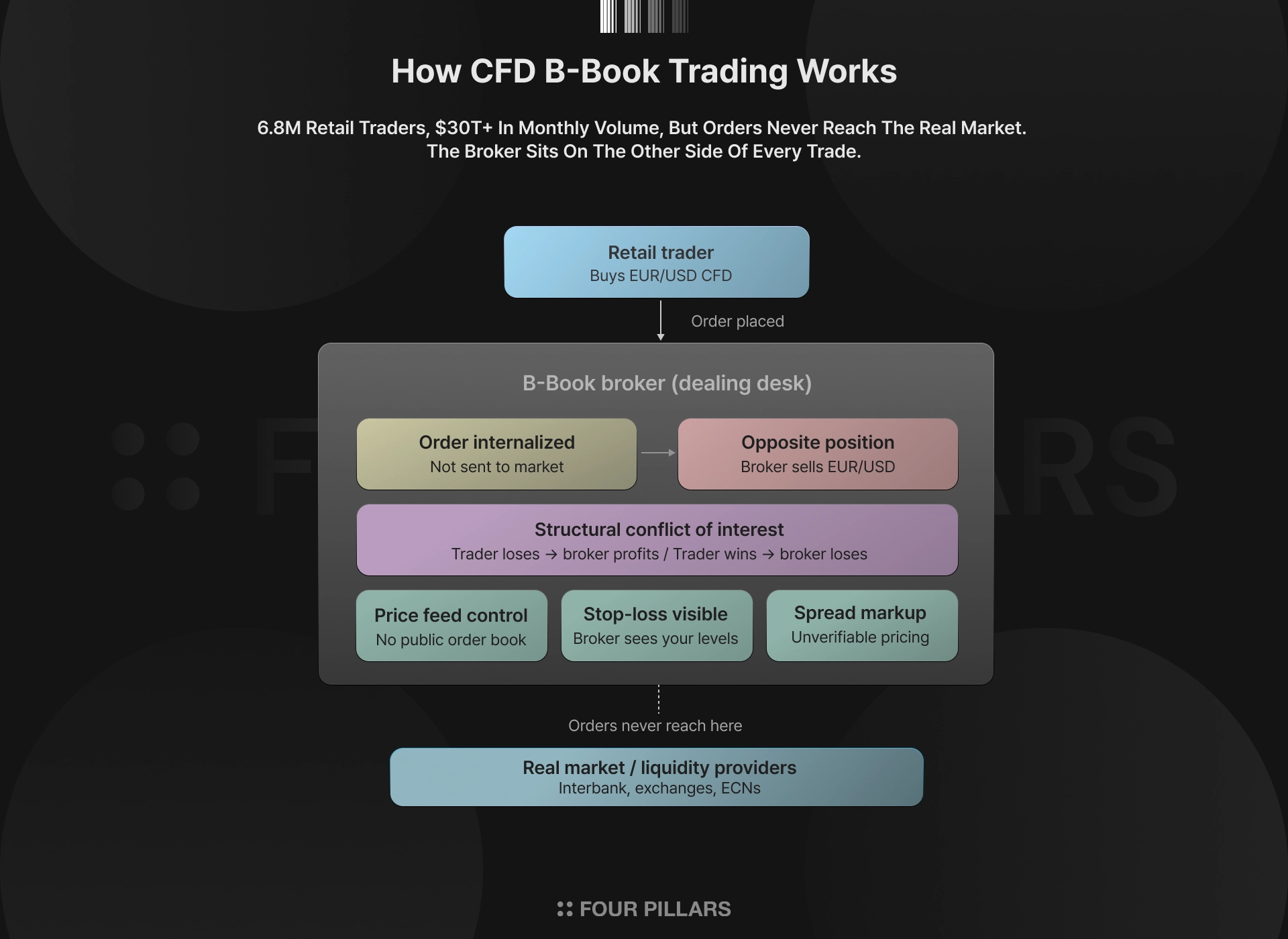

Roughly 6.8M retail traders worldwide trade CFDs, with monthly volume exceeding $30T. It is the most common leveraged trading instrument, but it carries a critical structural flaw: the B-Book model.

B-Book brokers do not route customer orders to the market. They process them internally. The broker takes the opposite side of the customer's position, so when the customer loses, the broker profits. There is no public order book, so there is no way to verify whether the broker's quoted price reflects the market. The broker can see customer stop-loss levels, controls the price feed, and profits from these advantages. The conflict of interest is embedded in the structure.

3.2.2 Expiring Futures

Expiring futures are the standard instrument for traditional leverage, but they carry structural inefficiencies. CME's futures market was originally designed around physical delivery dates, the arrival of a grain harvest or an oil tanker. That is why expiration dates exist. Yet physical delivery now accounts for a negligible fraction of futures trading volume. The vast majority is speculation and leverage. Users who have no need for expiration are forced into an expiration structure. Four inefficiencies stem from this:

Rollover operational burden: Expiring futures reach maturity every quarter. To maintain a position, the trader must close the current contract and buy the next one before expiration. This process is called a rollover. Traders holding long-term positions must repeat this every quarter, and missing the rollover window can mean unintended position closure or entry into the next contract at an unfavorable price.

Transaction costs: Every rollover involves two trades: closing the existing position and entering the new one. Each carries fees and spread costs, so long-term holders pay these repeatedly every quarter.

Liquidity fragmentation: The March, June, September, and December contracts each have separate order books. Even for the same crude oil or gold, liquidity is split across multiple expiries. Liquidity concentrates in the front month contract approaching expiration, while the rest trade at wider spreads.

Front-running: As expiration approaches, large rollover flows pile up in a predictable direction. Market makers and HFT firms detect this flow in advance and trade ahead of it. Traders who must roll have no choice over timing and are forced to transact at prices already moved against them.

CME recognizes these limitations. In June 2025, CME launched "spot-quoted futures," a no-expiry hybrid product for major indices including the S&P 500 and Nasdaq 100, as well as BTC/ETH. Positions can be held for up to five years without rolling, and quotes are based on spot prices. However, CME's fixed daily clearing cycle is incompatible with the continuous funding rate mechanism of true perpetual futures, making this a compromise rather than a full perpetual.

3.2.3 Options

Options remain a core hedging tool for institutions, but they fail to deliver the simple leverage most retail traders want. Say you are convinced NVDA will rise next week and buy a call option. Even if NVDA actually climbs 3%, the option price can fall if market volatility drops over the same period. Option prices are simultaneously affected by five variables (Greeks): time decay (theta), volatility changes (vega), rate of price change (gamma), and others beyond the underlying's direction. Unlike perpetual futures, where getting the direction right is sufficient, options require the trader to be right on direction, speed, timing, and volatility all at once.

The order book structure is another barrier. For a single underlying asset, hundreds to thousands of separate contracts exist across combinations of strike prices and expiration dates. AAPL options alone span weekly, monthly, and quarterly expirations, each with dozens of strikes, splitting the order book into over 2,000 fragments. Liquidity is dispersed, so most contracts trade at wide spreads, and getting filled at a desired price is difficult.

Reviewing legacy leverage instruments through this lens, the structural advantage of perps becomes clear. Perpetuals have no expiration. No expiration means no rollover burden, no roll transaction costs, no front-running, and no per-expiry liquidity fragmentation. A single underlying has a single order book, so liquidity concentrates. No Greeks to calculate like options. No broker sitting on the other side like CFDs. Get the direction right, and the position pays. A simple structure.

3.3.1 Perpetual Futures Volume Rush

The market is already choosing no-expiry leverage. Annual volume across the top 10 perps exchanges reached $93T in 2025, and fixed-expiry futures' share of BTC volume has fallen below 5%. In Q4 2025, BTC dropped more than 40% from its peak and spot volume was halved, yet perpetual futures volume over the same period rose 64.6%. Perps have established themselves as infrastructure that operates independently of the crypto cycle.

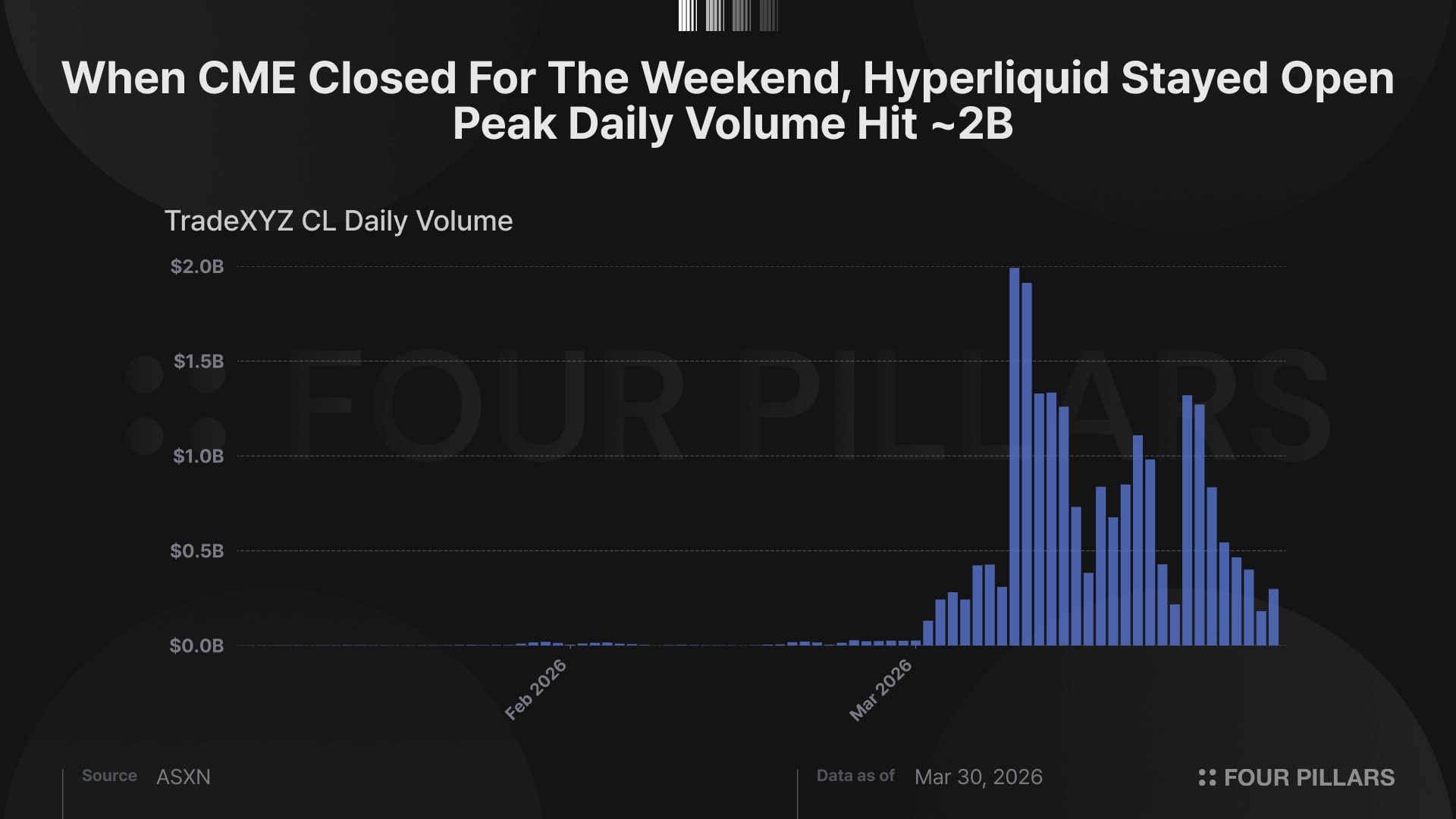

Recent events make this trend even more visible. In March 2026, U.S.-Israeli airstrikes on Iran escalated Middle East tensions, and WTI crude prices surged more than 30% in a single week. The most active crude oil trading venue during this period was not CME. It was Hyperliquid. While CME was closed for the weekend, Hyperliquid's crude oil perpetual (CL-USDC) continued trading around the clock, posting peak daily volume of $1.7B and open interest approaching $300M.

During the same period, combined daily volume for crude oil and silver perpetuals exceeded $900M, far outpacing large-cap crypto assets like SOL and XRP. The moment when traditional asset perpetuals trade more volume than crypto asset perpetuals arrived sooner than expected.

3.3.2 Institutional Adoption

The users of perpetual futurues have changed. As of 2025, institutional investors account for roughly 42% of total crypto derivatives trading volume. Three years ago, this market was dominated by retail. Ethena issues over $10B in synthetic dollars (USDe) using perps short positions, capturing funding rate yield through basis trades. SGX (Singapore Exchange) listed BTC/ETH institutional-only perpetual futures in November 2025, the first case of a traditional exchange offering perpetuals with exchange-based clearing. All of this points to perps transitioning from a retail speculation tool into institutional infrastructure.

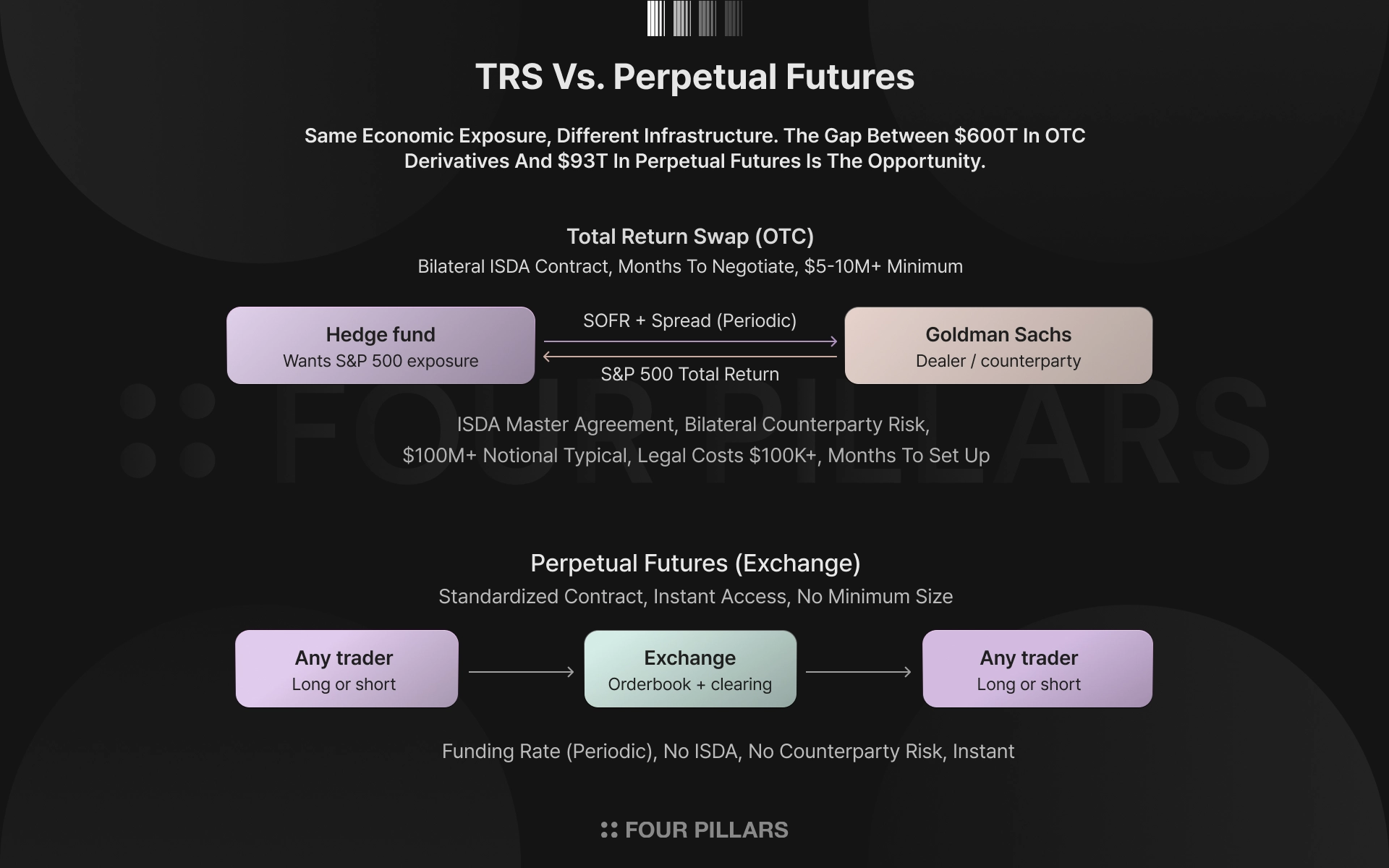

Institutional investors have in fact been trading the same structure as perpetual futures long before crypto existed, under the name of swaps. When a hedge fund wants $100M in synthetic exposure to the S&P 500, it enters a Total Return Swap (TRS) with Goldman Sachs. No ownership of the underlying, only price exposure. No expiration. Funding costs are periodically settled at SOFR (the risk-free reference rate) plus a spread. The mechanism is essentially identical to a perpetual futures funding rate. The difference is that TRS is executed as a bilateral ISDA (International Swaps and Derivatives Association) contract, while perps are standardized contracts that anyone can trade instantly on an exchange.

The efficiency gap this difference creates is large. Entering a TRS requires months of ISDA negotiation, hundreds of thousands of dollars in legal fees, and a minimum notional of $5 to $10M or more. Perps remove every one of these barriers. The global OTC derivatives market has a notional outstanding exceeding $600T. If even a fraction of this market migrates to perps, a market of incomparable scale emerges on top of the current $93T crypto perps market.

3.3.3 Regulatory Clarity

Regulation is moving in the same direction. In July 2025, Coinbase listed BTC/ETH perpetual futures in the U.S. through CFTC self-certification. ESMA (European Securities and Markets Authority) issued an official statement that "perpetual futures are likely to fall within the existing CFD regulatory framework."

Most notably, CFTC Chairman Mike Selig publicly stated in March 2026 that he would "unveil a crypto perpetual futures framework within weeks." The institutionalization of perpetual futures has moved past the discussion stage and into execution.

Perpetual futures have unquestionably been elevated in status. They are no longer a crypto-internal derivative but infrastructure competing directly with traditional finance leverage instruments.

QFEX's addressable market must be reassessed accordingly. Roughly 6.8M CFD retail traders, $9.6T in daily global FX volume, and over $600T in OTC derivatives notional outstanding are all markets that perps can absorb. Even if only a fraction of demand in each market, the portion seeking no-expiry leverage and 24/7 access, migrates, the resulting volume matches the entire crypto perpetual futures market today.

At this juncture, many exchanges have started offering traditional asset perpetual futures, but almost none have been purpose-built for traditional assets from the ground up. Users across CFD, DEX, and CEX already have sufficient structural reasons to leave their current platforms, and what they need upon departure differs. QFEX targets this gap.

CFD: Roughly 6.8M retail traders are transacting on top of the B-Book's misaligned incentives. The broker sits on the other side of the customer, controls the price feed, and can see stop-loss levels. What these users need upon migration is a public order book where brokers do not intervene, transparent price formation, and the absence of asymmetric funding.

QFEX's CLOB structure means all trades are executed on an order book between external market makers and traders. Funding rates settle directly between longs and shorts, eliminating CFD's asymmetric overnight funding. The incentive for this user base to move to perps is the clearest.

DEX: As ESMA and the CFTC formalize perpetual futures regulatory frameworks, the market landscape is expected to shift significantly once more. KYC-free platform access is likely to be restricted. As perps expand into traditional assets, the tolerance for discretionary intervention, such as validators force-settling positions by consensus or unilaterally halting markets, narrows.

QFEX secures a compliance foundation through mandatory KYC for all users and eliminates discretionary governance with a 5-stage liquidation cascade. The prerequisites for institutional participation are also in place. Customer assets are held in segregated custody at BitGo Bank (OCC-chartered), making exchange access to funds impossible. A 100ms speed bump and dynamic tick sizes block HFT speed monopolies, creating a fair competitive environment for market makers.

CEX: Kraken, OKX, and Coinbase have all launched traditional asset perpetual futures, but each takes the approach of layering traditional assets on top of crypto infrastructure. Price tracking for assets whose markets close, time-of-day risk calibration, and overnight/weekend liquidity management are problems that cannot be solved simply by extending a crypto matching engine.

QFEX designed its matching engine from the ground up for traditional asset trading cycles: real-time feeds from the NYSE and Nasdaq combined with Blue Ocean ATS overnight data, leverage limits differentiated by regular hours, overnight, and weekends, and zero funding during market close.

Adding traditional assets to a crypto exchange and building an exchange for traditional assets are different problems. QFEX is the latter. Adding exchange-listed products to a B-Book broker and designing on a public order book from day one are different problems. QFEX is the latter there, too.

With the CFTC chairman signaling a framework within weeks, CME listing spot-quoted futures, and Coinbase launching traditional asset perpetuals, the institutionalization of perpetual futures is already underway. The scenario in which perpetual futures as a trading format extends into traditional finance's $600T OTC derivatives market looks increasingly plausible. The remaining question is who will provide the optimal infrastructure.

Source: QFEX

QFEX brings HFT-grade microstructure, regulatory compliance, and risk management into a single exchange. Behind it is a $9.5M seed round (at a $95M valuation) led by General Catalyst and Y Combinator, with Paul Graham participating as a personal investor. The investor composition alone tells a story: it is not centered on crypto-native VCs but on backers who have bet on fintech and financial infrastructure startups. This lends credibility to QFEX's stated goal of targeting not crypto but the traditional financial infrastructure beyond it.

Even so, QFEX is still at a very early stage. Hyperliquid and HIP-3-based DEXs entered the market first and have established dominance. CEX positions remain strong. Yet the current $93T perpetual futures market represents only a sliver of the potential TAM, and QFEX is designing its trading engine to capture this expansion phase. That "We're building FTX without the fraud" and the goal of replacing the $100B exchange, clearinghouse, and brokerage industry sound quite bold, yet still come across as credible, is the point.

Dive into 'Narratives' that will be important in the next year