This article is an excerpt from our report on stock tokenization. The full report can be found in “2026: The Year of Tokenized Stocks”

The "onchaining of assets" currently led by major firms such as Robinhood and Coinbase is more than a technical supplement to increase transaction speeds; it is a process of redesigning traditional financial infrastructure based on distributed ledger technology (DLT). While initial stages, such as BlackRock's BUIDL, focused on debt and Money Market Funds (MMF) for accredited investors to verify digital liquidity, extending this to the general stock market to combine with P2P trading and DeFi ecosystems represents a paradigm shift in impact.

This is because stock is an asset directly linked to corporate governance and capital structure, moving beyond simple debtor-creditor relationships. Therefore, innovation in stock ownership transfer presents technical and institutional challenges previously unseen in financial law, including:

Execution of voting and dividend rights via smart contracts.

Expansion of stock collateralization and its impact on financial system stability.

Real-time synchronization of shareholder registries based on distributed ledgers.

Internalization of regulatory compliance through whitelist policies.

This chapter reviews the legal and institutional responses of major countries aiming to move beyond mere "wrapping" of profit rights toward "native" tokens that fully realize intrinsic shareholder rights on a distributed ledger.

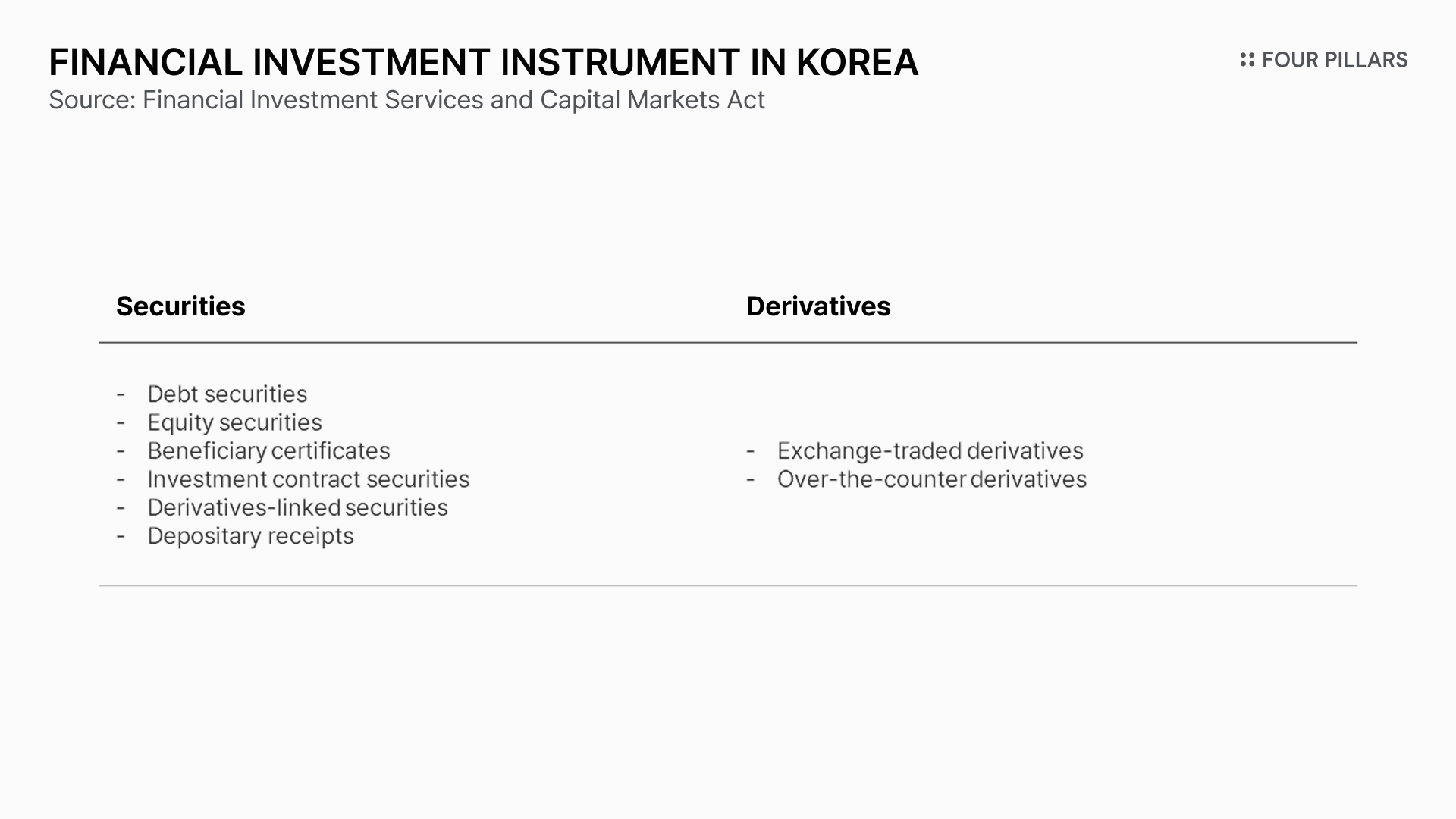

Republic of Korea regulates both "securities" and "derivatives" under the Financial Investment Services and Capital Markets Act (the "Capital Markets Act"). Unlike the U.S., which maintains separate systems like the Securities Act of 1933 and the Commodity Exchange Act of 1936, Korea manages these under a single, unified legal framework. The Act defines "financial investment instruments," which include the following:

Security tokens were first introduced in Korea through fractional investment. In 2019, Kasa utilized the Financial Regulatory Sandbox to issue Digital Asset Backed Securities (DABS) for commercial real estate.

The Financial Services Commission (FSC) defines fractional investment as a new investment form where two or more investors invest in and trade claims split from physical assets or rights with property value (Financial Services Commission, Guidelines on New Securities Businesses such as Fractional Investment).

In Korea, fractional investments are issued in the form of either investment contract securities or beneficial certificates of non-monetary trusts. At the time, although investment contract securities existed under the legal and institutional framework, there had been no actual cases of issuance.

Kasa received "Innovative Financial Service" designations for two regulations that were otherwise impossible under current law:

Non-monetary Trust Beneficiary Certificates: The Capital Markets Act only stipulated monetary trusts; a sandbox was needed to issue non-monetary certificates (Art. 110, Sec. 1).

Brokerage and Exchange Specialization: To avoid being classified as an unauthorized brokerage, Kasa received exemptions to operate both the issuance and distribution platforms (Art. 373, Art. 11).

In addition, securities recorded on a distributed ledger are not accorded the presumption of rights under the Act on the Electronic Registration of Stocks and Bonds. (hereinafter referred to as the “Electronic Securities Act”)—under which a holder in possession of a physical certificate is presumed to be a lawful holder and may transfer the security by delivery of the certificate, and a person registered in the electronic securities account registry is presumed to be the lawful right holder and may transfer the security through book-entry transfers. Accordingly, Kasa established a mechanism to ensure legal protection of investors’ rights by mirroring the distributed ledger and the Korea Securities Depository’s electronic securities system on a one-to-one basis.

In 2023, the FSC announced a plan to reorganize the token security framework, clarifying that token securities are legally "securities" and subject to investor protection under the Capital Markets Act. Key features include:

Recognition of the Presumption of Legal Rights for Distributed Ledgers (Amendment to the Electronic Securities Act)

Security tokens are accommodated under the Electronic Securities Act as a form of securities issuance recorded on a distributed ledger. Distributed ledger technology is recognized as a legally valid method of recordation in the statutory register for information concerning the creation, modification, and extinguishment of rights in securities. Through this recognition, securities issued on a distributed ledger are afforded the same level of legal protection as traditional securities.

Introduction of the Issuer Account Management Institution (Amendment to the Electronic Securities Act)

Unlike traditional securities, which may be issued only through account management institutions such as securities companies, distributed ledger–based securities may be issued directly by the issuer acting as an account management institution, provided that the issuer satisfies certain statutory requirements. Where the issuer does not meet the requirements to qualify as an issuer account management institution, the securities must be issued through an existing account management institution, such as a securities company.

Introduction of the Over-the-Counter Brokerage Business (Amendment to the Capital Markets Act)

Security tokens issued using distributed ledger technology are to be traded and circulated through the Korea Exchange (KRX) and licensed over-the-counter (OTC) brokerage firms. OTC brokerage firms are required to meet certain quantitative thresholds and to satisfy prescribed physical and human resource requirements, as well as to establish internal control standards, including measures to prevent conflicts of interest.

In addition, in order to ensure the separation of issuance and distribution, securities and beneficial certificates that are issued, underwritten, or arranged by the brokerage firm itself or by its affiliates, as well as beneficial certificates for which such entities act as trustees or sponsors, may not be distributed through the same brokerage firm.

The amendment to the Enforcement Decree of the Capital Markets Act regarding the introduction of over-the-counter(OTC) brokerage entities were enacted and took effect in September 2025. Subsequently, the amendments to the Electronic Securities Act, along with additional revisions to the Capital Markets Act, passed the National Assembly plenary session on January 15, 2026.

The security token (STO) market in the Republic of Korea is scheduled for full-scale implementation in January 2027. In preparation for this rollout, the government will launch the Security Token Consultative Body in February 2026.

The consultative body will design detailed regulatory frameworks through three specialized working groups: (i) technology and infrastructure (including blockchain infrastructure), (ii) issuance framework (including securities registration statements), and (iii) distribution framework (including disclosure requirements for secondary trading and licensing regimes).

From a technological perspective, the use of smart contracts in connection with security tokens is expected to become fully operational. In particular, with a focus on investment contract securities, smart contracts are anticipated to enable the automation of contractual execution, including profit distribution, the provision of incentives, and the exercise of conditional rights. This development may lead to enhanced operational efficiency and improved transaction transparency in capital markets.

The remaining key challenge lies in the rational design of the permissible scope of infrastructure and licensing requirements. In particular, whether the current private blockchain–based framework should be expanded to permit the use of public blockchains constitutes a critical policy issue that will determine the scalability and international competitiveness of Korea’s security token ecosystem. In addition, ongoing domestic discussions on security tokens remain largely centered on fractional investment, and the limited scope of permissible underlying assets continues to function as a constraint on the expansion of viable business models.

Ultimately, legislation represents only a starting point. Over the next year, the design of subordinate regulations that can preserve investor protection while accommodating technological innovation will constitute a critical turning point in determining the international competitiveness of Korea’s security token market.

In the United States, even where assets take the form of digital tokens, existing securities regulations—namely the Securities Act of 1933 and the Securities Exchange Act of 1934—are applied if their economic function and substance qualify them as securities. This approach reflects the so-called “same function, same regulation” principle. Accordingly, a number of digital assets have been registered as securities, and in many cases, issuers have relied on registration exemptions under Regulation D. This approach generally permits securities offerings to be conducted as private placements, allowing sales only to accredited investors.

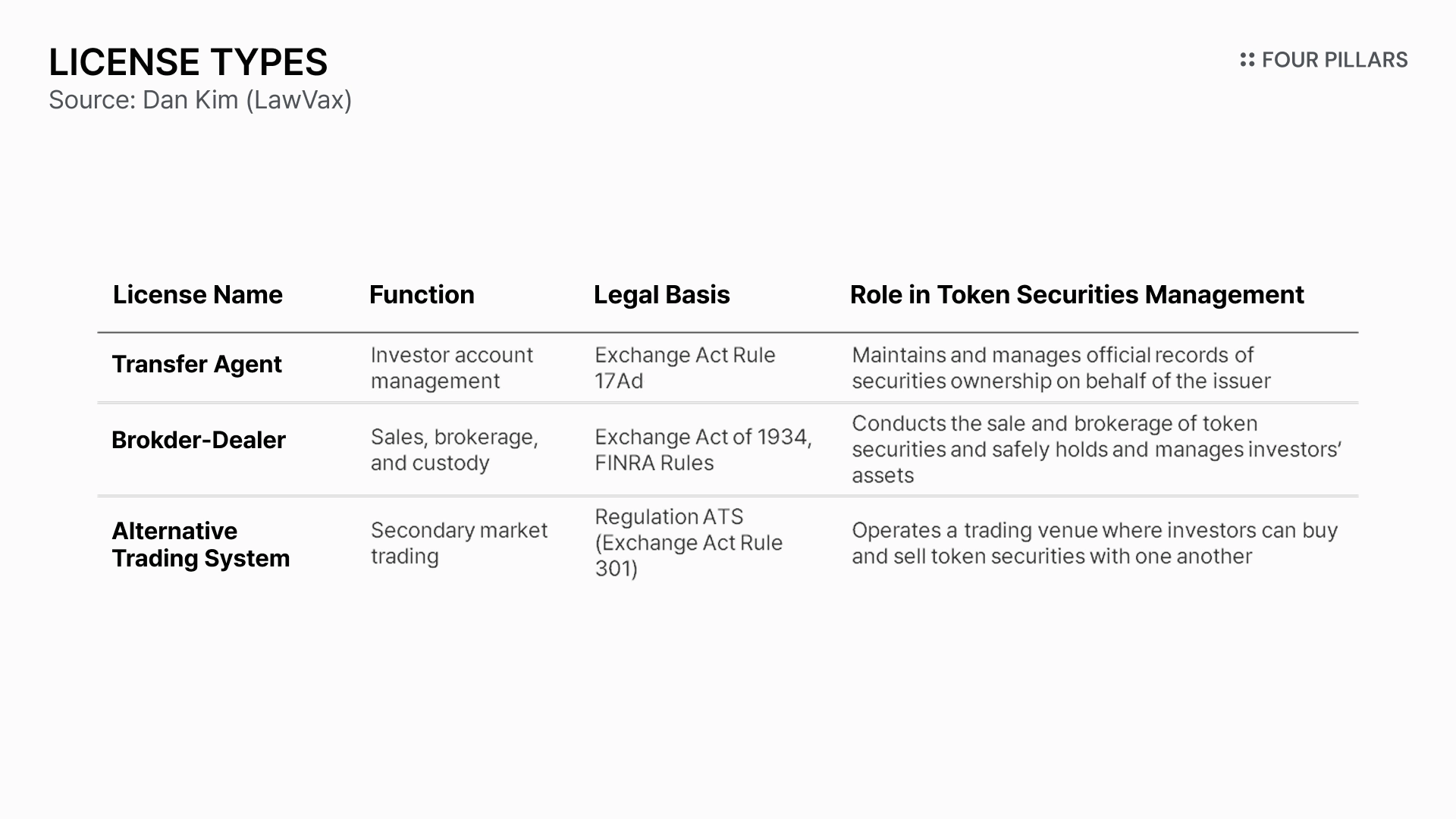

As discussed above, security token service providers in the United States operate their businesses based on existing licensing frameworks embedded in traditional financial infrastructure, rather than seeking to create an entirely new and separate regulatory regime. The issuance, custody, and distribution of security tokens are structured around established securities market licenses—namely transfer agents, broker-dealers, and alternative trading systems (ATSs)—with distributed ledger technology being utilized in a manner that supports and extends this existing framework.

Amendments to the UCC and the Exclusion from the Securities Exchange Act of 1934

The Uniform Commercial Code (UCC) has traditionally contemplated only certificated securities, represented by physical instruments, or uncertificated securities, recorded on the issuer’s books. As a result, distributed ledger technology—characterized by the absence of a centralized record-keeping authority—has faced limitations due to its ambiguous legal status within the existing legal framework.

However, the 2022 amendments to the UCC introduced Article 12, which establishes the concept of "controllable electronic records." Under this framework, a person is deemed to have “control” where the electronic record itself, a record attached to or logically associated with it, or the system in which it is recorded: (i) confers upon the person the power to avail itself of substantially all of the benefits of the electronic record; (ii) grants the person exclusive power, subject to statutory exceptions, to prevent others from availing themselves of substantially all of such benefits and to transfer control of the electronic record to another person, or to cause another person to obtain control of a different controllable electronic record as a result of such transfer; and (iii) enables the person to readily identify itself as holding such powers, including through a name, identifying number, cryptographic key, office, or account number. By defining control in this manner, the amendments allow transactions conducted through distributed ledger technology to be accorded legal effect.

In addition, the U.S. Securities and Exchange Commission (hereinafter, the “SEC”) expressed a forward-looking interpretive position in its staff FAQs regarding the broker-dealer obligation to maintain possession or control of securities under Rule 15c3-3 of the Securities Exchange Act of 1934. Although the rule is premised on the existence of physical certificates, the SEC indicated that even in the case of digitally native, uncertificated assets such as crypto asset securities, the possession or control requirement may be deemed satisfied where such assets are held at a qualified control location.

These legislative developments are regarded as having laid the legal groundwork for recognizing distributed ledger records themselves as native securities records capable of evidencing the attribution and transfer of rights.

Transfer Agent: Legal Ownership Records for Security Tokens

A transfer agent is a key entity that, on behalf of the issuer, maintains and administers the official records of securities ownership. Within a security token structure, the transfer agent is responsible for managing investor accounts and recording transfers and changes in ownership of security tokens. Such records serve as authoritative evidence consistent with the legal register and are accorded a strong presumption of legal validity.

Broker-Dealer: Distribution, Intermediation, and Custody

A broker-dealer is responsible for the sale and intermediation of security tokens, as well as the custody and management of customer assets. In this process, distributed ledger–based security tokens are subject to the same customer asset protection obligations applicable to traditional securities. However, as discussed above, security tokens are exempted from the requirement of physical possession and control of securities.

Alternative Trading System (ATS): Secondary Market for Security Tokens

Secondary trading of security tokens is conducted primarily through alternative trading systems (ATSs). While ATSs operate under a more flexible structure than national securities exchanges, they function as regulated trading platforms subject to Regulation ATS and are overseen by the U.S. Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA).

Traditional financial market infrastructure (FMI) has been operated efficiently for decades; however, distributed ledger technology (DLT) is presenting new benchmarks in terms of settlement speed and operational efficiency. Against this backdrop, core U.S. financial market infrastructures—including Nasdaq and the Depository Trust & Clearing Corporation (DTCC)—are seeking to incorporate DLT in order to shorten settlement cycles within existing centralized systems and to enhance transparency in asset management.

DTCC Case Study: Digital Expansion of the Central Securities Depository System

The Depository Trust & Clearing Corporation (DTCC) is the central securities depository of the U.S. capital markets and a core institution responsible for the safe custody and settlement of securities transactions. In December 2025, DTCC obtained a no-action letter from the U.S. Securities and Exchange Commission (SEC). Pursuant to this relief, DTCC is permitted, over a three-year period, to provide custody and assurance services for tokenized stocks and other real-world assets (RWAs) recorded on pre-approved distributed ledgers. DTCC is expected to launch its new tokenization-related services in the second half of 2026.

Nasdaq Case Study: Overcoming Temporal Constraints of Centralized Exchanges

Nasdaq, as a leading U.S. national securities exchange, seeks to address the temporal constraints and inefficiencies inherent in traditional securities trading through the adoption of distributed ledger technology. Specifically, Nasdaq plans to build a system enabling 24-hour trading, five days a week, extending beyond the existing limited trading hours, with a target launch in the second half of 2026.

In addition, Nasdaq is focusing on the potential of distributed ledger technology to enable real-time settlement. By significantly shortening the settlement cycles that are currently standard in securities markets—such as T+2 or T+1—Nasdaq aims, over the longer term, to establish infrastructure capable of supporting same-day settlement (T+0).

To facilitate this system transition, Nasdaq has already submitted a proposed rule change to the SEC. If approved, Nasdaq—operating as a regulated central securities exchange under the SEC’s formal supervision and authorization—will be able to offer security token trading utilizing distributed ledger technology within the existing regulatory framework.

Securitize demonstrates the practical feasibility of an issuer-led, native token model that embraces blockchain innovation while complying with U.S. securities regulation, without relying on exemptions from existing securities laws. Leveraging its status as an SEC-registered transfer agent, a FINRA-member broker-dealer, and an operator of a licensed alternative trading system (ATS), Securitize operates the entire lifecycle of security tokens within the regulated framework—from issuance to secondary market trading and custody-related support.

In particular, by working directly with issuers to issue native tokens in which the issuer’s shareholder register directly reflects beneficial ownership, Securitize ensures that investors are granted the same voting and dividend rights as those associated with traditional securities, thereby providing legal certainty throughout the entire asset lifecycle.

The core driver of Securitize’s regulatory compliance lies in its smart contract technology based on the DS Protocol. This protocol enables the whitelisting of investor wallets and performs real-time onchain verification of anti-money laundering (AML) compliance and investor eligibility (KYC). In addition, by synchronizing smart contracts with an off-chain master securities record, the system allows, in cases of token loss or theft, for the affected tokens to be burned and reissued at the issuer's instruction.

This architecture overcomes the anonymity traditionally associated with digital assets and the vulnerabilities of bearer securities, and may be regarded as presenting a modern custody model that is consistent with FINRA’s customer protection rule (Rule 15c3-3).

Furthermore, Securitize integrates Regulation NMS, a core normative framework of traditional stock markets, into the onchain environment. By utilizing price oracles to ensure execution within prevailing market price ranges, the platform faithfully fulfills its best execution obligations. This robust risk management framework clearly differentiates Securitize from wrapped tokens or permissionless DeFi models that operate in regulatory blind spots.

While embracing the asset efficiency of DeFi—such as stablecoin-based settlement for security token purchases, onchain lending and borrowing, and the use of tokens as collateral—Securitize simultaneously achieves the financial system stability required by regulators, thereby positioning itself at the forefront of a global standard for compliant tokenization.

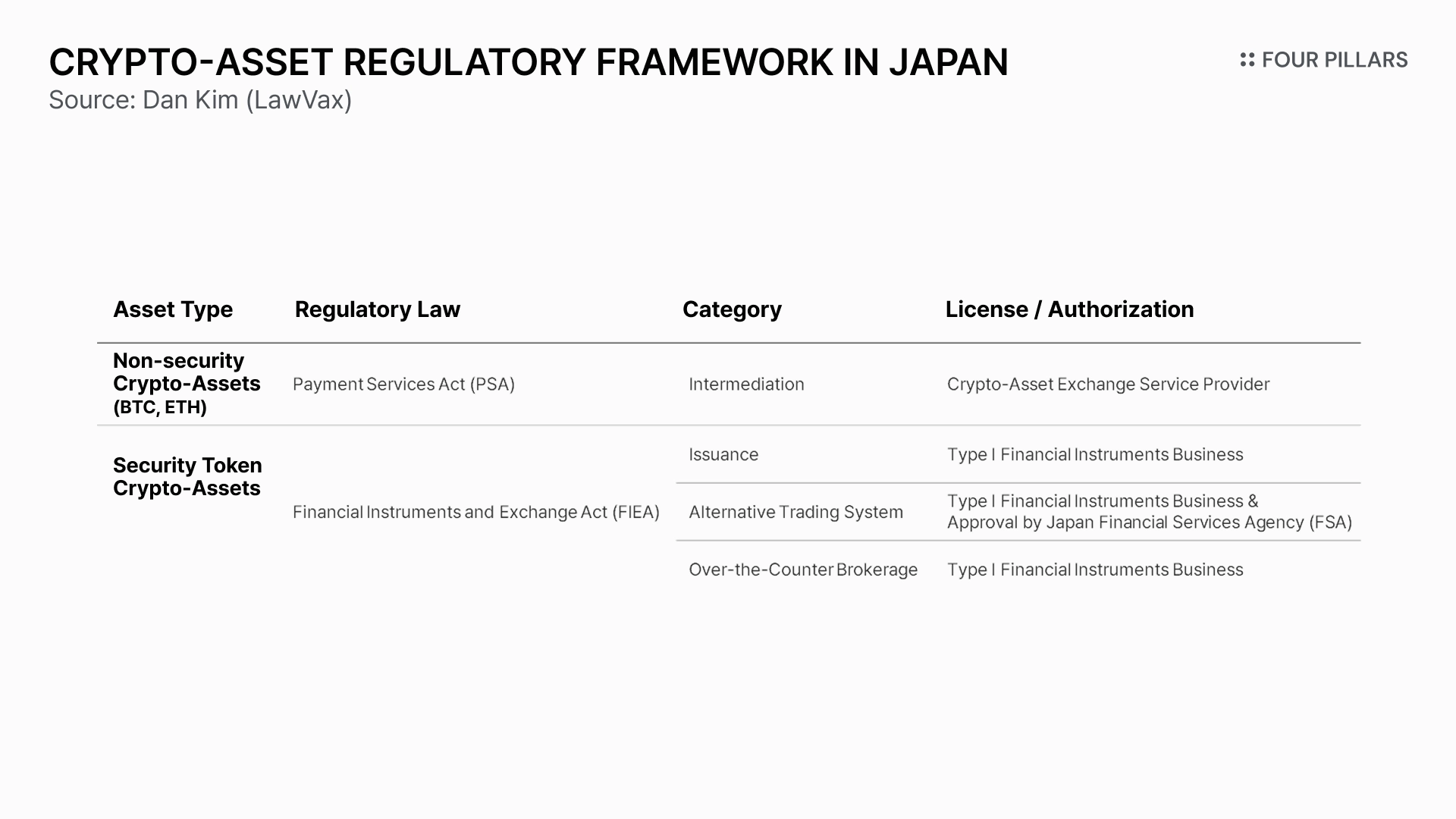

Unlike Korea or the European Union, which have enacted separate regulatory regimes for digital assets, Japan regulates digital assets by defining and governing them within its existing financial laws.

Under the Financial Instruments and Exchange Act (FIEA), security tokens are defined as Electronically Recorded Transfer Rights, which are regarded as securities rights recorded in a digital form.

Electronically Recorded Transfer Rights are subject to the same regulatory framework as securities listed in Article 2, Paragraph 1 of the Act (Article 2, Paragraph 3 of the Financial Instruments and Exchange Act).

Accordingly, any entity engaging in businesses involving such rights is required to obtain a Type I Financial Instruments Business license pursuant to Article 28 of the Financial Instruments and Exchange Act.

However, pursuant to Guideline 2-2-2 under the Financial Instruments and Exchange Act and related guidelines, where the registration (recordation) of the holder(s) of rights or the number of such rights, which are contractually or in practice managed by the issuer or other relevant party, and the transfer of such rights are carried out in an integrated and continuous manner on an electronically recorded ledger (including any ledger that is linked to such ledger), the relevant rights shall constitute Electronically Recorded Transfer Rights.

Conversely, where the electronic ledger is merely created for internal administrative purposes within the issuer or similar entity, and the transaction parties or intermediaries are unable to access or refer to such electronic ledger, the rights recorded therein shall not be deemed Electronically Recorded Transfer Rights.

In conclusion, Electronically Recorded Transfer Rights are not merely internal electronic records, but a system that grants legal effect to the transfer of rights through a transparent and consensus-based electronic ledger.

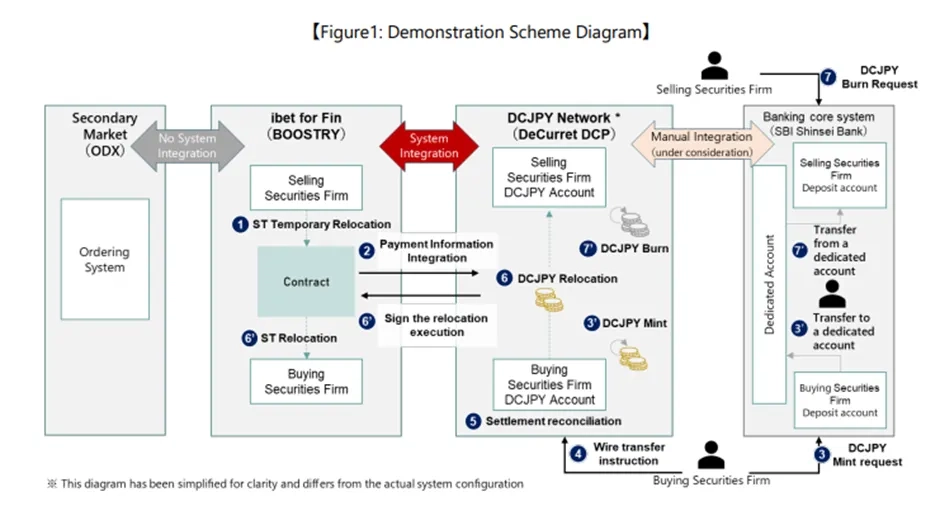

The SBI Group utilizes security tokens as a primary mechanism to overcome the limitations of traditional stock market structures, pursuing a strategy to establish an integrated digital infrastructure that encompasses the entire lifecycle of issuance, distribution, and settlement.

Secondary Market via Proprietary Trading Systems (PTS), the Osaka Digital Exchange (ODX)

Japan has adopted a distinct distribution structure centered on Proprietary Trading Systems (PTS) rather than listing security tokens on the Tokyo Stock Exchange (TSE). To engage in these operations, entities are required to obtain a Type I Financial Instruments Business license under the Financial Instruments and Exchange Act (FIEA).

In 2021, SBI Holdings and Mitsui Sumitomo Financial Group established the Osaka Digital Exchange (ODX) through a joint venture, successfully institutionalizing an independent distribution channel for security tokens within the formal regulatory framework. "START," operated by ODX, is Japan’s first secondary market dedicated to security tokens authorized to handle "Electronically Recorded Transfer Rights." It currently serves as the core infrastructure for Japan's security token distribution model.

Digitalization Strategy for Securities Settlement and Clearing Infrastructure Using Stablecoins and Deposit Tokens

Securing Stablecoin Distribution Licenses by the SBI Group

Japan recognizes crypto-assets as a legitimate means of payment. The institutional foundation was finalized through the 2023 amendment of the Payment Services Act, which explicitly defined stablecoins as "Electronic Payment Instruments" and established a new licensing system for "Electronic Payment Instrument Exchange Service Providers

In connection with these regulatory developments, SBI VC Trade became the first entity in Japan to obtain the "Electronic Payment Instrument Exchange Service Provider" license in March 2025. By securing the authority for the legal distribution and payment processing of USDC within Japan, the group has established a leading position in the market.

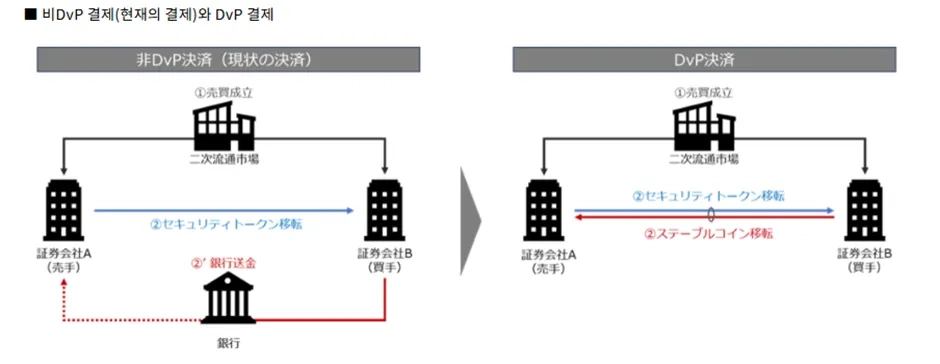

Real-time DVP Structure Linking Security Tokens and Stablecoins

In August 2025, the Osaka Digital Exchange (ODX) announced a project for Delivery Versus Payment (DVP) utilizing security tokens and stablecoins. In this framework, the transfer of securities and the payment of funds are conditionally linked and executed automatically via smart contracts.

Notably, this system adopts a "gross settlement" structure, where settlement occurs on an individual transaction basis, rather than the traditional method of aggregating transactions for collective netting.

If this structure is formally established, it is anticipated that the transfer of securities and payment of funds will occur instantaneously and simultaneously on the blockchain. In the long term, this is expected to resolve the settlement lag (T+N) inherent in traditional securities settlement systems, as well as the accompanying clearing risks.

Furthermore, global investors will be able to utilize internationally recognized stablecoins, such as USDC, to facilitate rapid investment and capital repatriation regarding security token assets within Japan. Consequently, this is highly likely to reduce friction costs associated with cross-border payments and capital movements, ultimately establishing a more 'seamless' international investment environment.

Source: odx

Infrastructure Strategy Extending to Deposit Token-Based Stock Settlement Proof-of-Concept

The SBI Group is conducting proof-of-concept (PoC) experiments for an stock DVP (Delivery Versus Payment) settlement structure utilizing not only stablecoins but also DCJPY, a form of deposit token. This initiative is evaluated as a strategic move that transcends the mere tokenization of shares; it represents a comprehensive effort to redesign the entire financial infrastructure—encompassing transfer, settlement, and clearing systems—on a distributed ledger foundation.

Source: SBI Shinsei Bank

Inclusion of Distributed Ledger in the Definition of 'Financial Instruments'

The EU has amended the existing MiFID II to explicitly include instruments issued via Distributed Ledger Technology (DLT) within the definition of "financial instruments." Through this amendment, tokens issued and circulated on a distributed ledger have obtained formal legal status as "financial instruments" (MiFID II, Art. 4(1)(15)).

Temporary Recognition of Distributed Ledger Records as 'Book-entry'

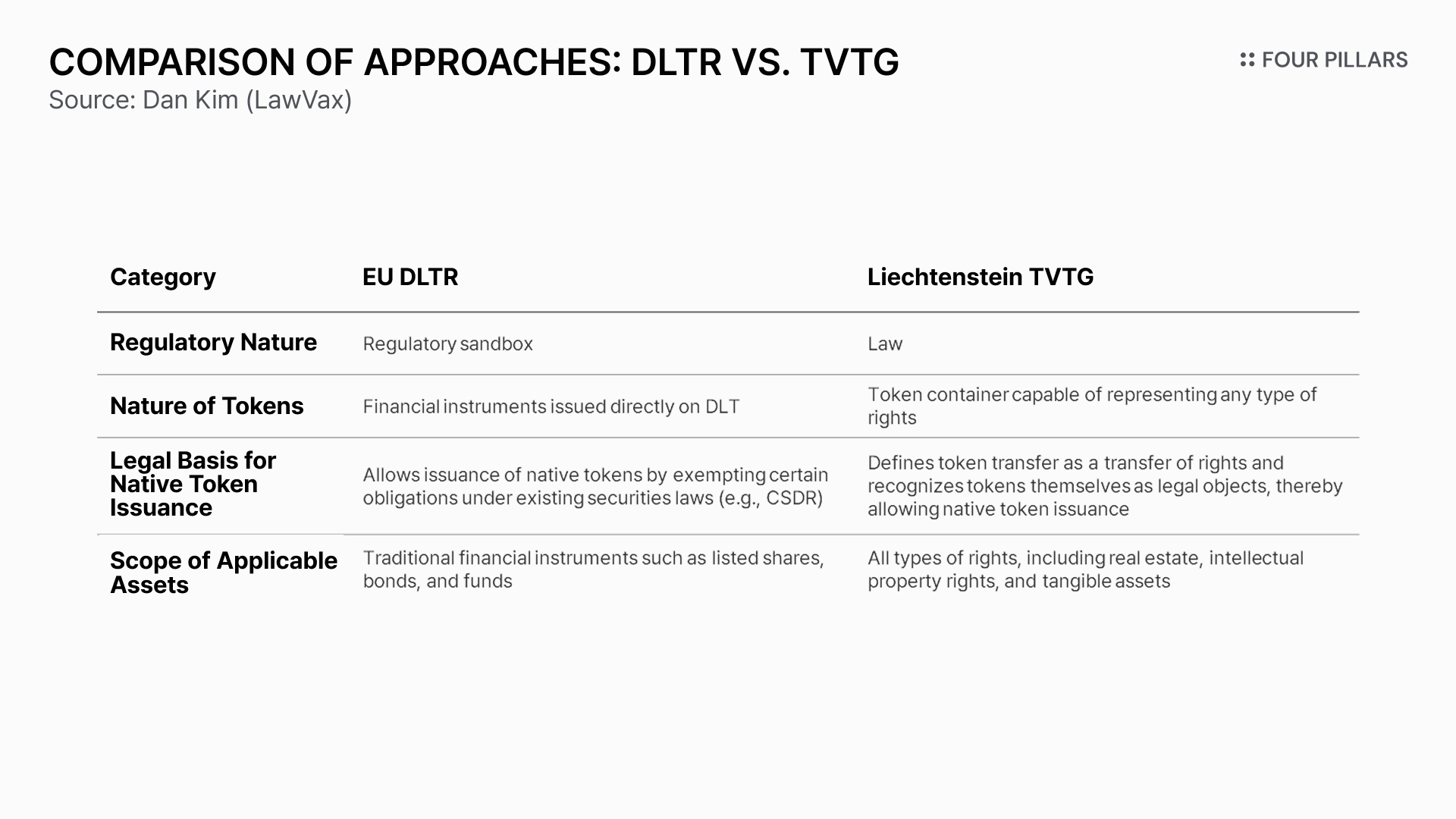

Under the EU Central Securities Depository Regulation (CSDR), listed securities must be recorded in the form of book-entry at a Central Securities Depository (CSD) to obtain formal legal recognition (CSDR Article 3). However, the DLT Pilot Regime (DLTR) provides a temporary exemption from this requirement to support technological innovation.

Under the DLT Pilot Regime (DLTR), operators of DLT Settlement Systems (DLT SS) and DLT Trading and Settlement Systems (DLT TSS) are permitted to use a distributed ledger in place of the traditional Central Securities Depository (CSD) ledger. This allowance is granted provided that the operators demonstrate that traditional book-entry methods are incompatible with distributed ledger technology and implement compensatory measures to ensure investor protection and market stability.

Furthermore, the DLTR permits a temporary settlement structure in which the delivery of securities and the payment of funds are completed solely through onchain data movement, by mandating that the transfer of tokens on a distributed ledger be regarded as a legally valid 'settlement'.

Establishment of New DLT Market Infrastructures

The DLT Pilot Regime (DLTR) has defined three new forms of infrastructure based on distributed ledger technology.

DLT multilateral trading facility (DLT MTF) : A multilateral trading facility that only admits to trading DLT financial instruments

DLT settlement system (DLT SS) : A settlement system that settles transactions in DLT financial instruments against payment or against delivery

DLT trading and settlement system (DLT TSS) : A DLT MTF or DLT SS that combines services performed by a DLT MTF and a DLT SS

Direct Trading Based on DLTR and the Acceptability of Non-Custodial Wallets

In traditional financial markets, transactions were required to be conducted through "intermediaries." However, the DLT Pilot Regime (DLTR) allows natural persons to participate directly in DLT market infrastructure as participants without an intermediary.

In this regard, the European Securities and Markets Authority (ESMA) stated in its DLT Pilot Regime report that "direct transactions between investors using non-custodial wallets that they control directly, with no interposition of a third-party, could be considered OTC trading, while exchanging an asset between two counterparties through the interposition of an DLT MI, where the infrastructure also offers the custodial wallet to the two counterparties, could be considered on-venue trading". By providing this interpretation, ESMA has effectively opened up the possibility for the P2P transfer of tokenized financial instruments via non-custodial wallets.

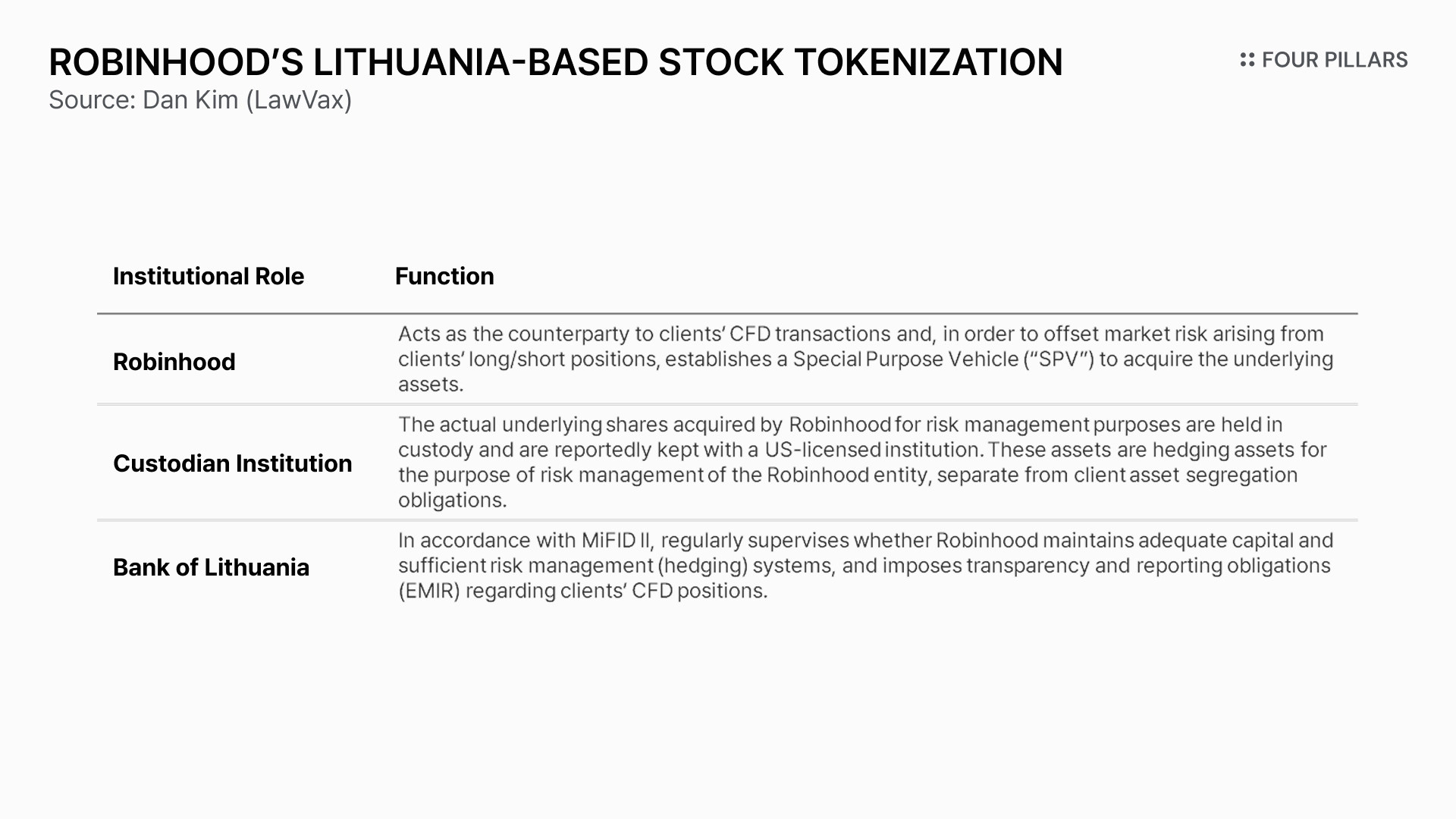

Robinhood has obtained a Category A financial brokerage firm license in Lithuania, an EU member state and a Crypto Asset Service Provider (CASP) license to expand its services across more than 30 countries in the European Economic Area (EEA). This model utilizes tokenization technology within the regulatory framework of MiFID II.

Robinhood’s Products: OTC Derivatives, Not Securities

Robinhood’s security tokens are legally classified not as "securities," but as over-the-counter (OTC) derivatives with the characteristics of Contracts for Difference (CFD) regulated under MiFID II. In other words, investors do not directly hold the underlying shares; instead, they enter into a 1:1 contractual relationship where gains or losses resulting from price fluctuations are settled in cash.

Under this structure, Robinhood does not act as an intermediary; instead, it functions as the direct counterparty to its users. Based on its Category A financial brokerage license in Lithuania, Robinhood exectues trades via an over-the-counter(OTC) model.

In such an OTC structure, unlike listed securities, there is no mandatory requirement to record transactions in the Central Securities Depository (CSD) ledger. Consequently, it is possible to utilize a distributed ledger as a means of contract recording and management without the need for separate regulatory exemptions, such as those provided by the DLT Pilot Regime (DLTR).

Furthermore, since typical rights associated with shares, such as the entry in the register of shareholders or the granting of voting rights, are not required, this model is characterized by a relatively low implementation burden in terms of service design and operation

Division of Institutional Roles and Asset Custody

To manage the risks associated with the CFD contracts executed with investors and to satisfy regulatory requirements, hedging and asset custody are performed.

Liechtenstein enacted the Token and Trustworthy Technology Service Provider Act (commonly referred to as the TVTG) in 2020. By doing so, it became the first jurisdiction in the world to introduce a comprehensive legal framework governing the transfer of rights via distributed ledger technology.

The core of the TVTG lies in its adoption of the 'Token Container Model,' which directly links legal rights to tokens on a distributed ledger. Under this model, existing legal rights—such as stocks, bonds, real estate, intellectual property, and physical assets—are encapsulated within a digital container called a 'token' to be transferred on a distributed ledger. Consequently, the transfer of the token itself is legally recognized as the transfer of the underlying right.

This is evaluated as a more advanced approach than the EU’s DLT Pilot Regime (DLTR) implemented later, in that it does not merely digitize existing rights for record-keeping on a distributed ledger, but rather recognizes the legal status of the digital certificate itself as the embodiment of the right. While the DLTR posits the distributed ledger as a substitute for traditional 'ledgers,' the TVTG recognizes the token as the legal object itself through which rights are manifested.

Although Liechtenstein is not a member of the European Union (EU), it belongs to the European Economic Area (EEA) and adopts a significant portion of the EU's single market regulations. Accordingly, the Markets in Crypto-Assets Regulation (MiCA) is implemented and applied as part of Liechtenstein's domestic law.

However, the TVTG and MiCA are not designed to be mutually exclusive; rather, they are structured to coexist with clearly demarcated regulatory scopes. MiCA governs the overall crypto-asset market—including crypto-assets like Bitcoin and Ethereum, as well as stablecoins—by regulating the licensing of Crypto-Asset Service Providers (CASPs), white paper disclosure requirements, and market abuse. In contrast, the TVTG addresses legal issues concerning NFTs, security tokens, and tokenized rights, granting legal effect so that the transfer of a token constitutes the transfer of the underlying right according to the Token Container Model.

Ultimately, while MiCA functions as a financial regulatory framework for the crypto-asset market, the TVTG serves as the comprehensive legal infrastructure governing the ownership and transfer of rights embodied in tokens. These two systems operate in a complementary manner.

The UK Financial Conduct Authority (FCA) does not treat tokenized shares as a distinct asset class; rather, it classifies them as "Specified Investments," identical to traditional financial instruments.

According to the FCA guideline PS 19/22 (Guidance on Cryptoassets), if the rights inherent in traditional securities—such as stocks or bonds—are implemented in a tokenized format, they are categorized as security tokens. Consequently, they are subject to the same financial regulatory framework as conventional securities.

As a result, any entity seeking to issue or distribute tokenized shares must ensure that both the issuer and intermediaries obtain financial business authorization under the Financial Services and Markets Act (FSMA) and MiFID. Furthermore, they must strictly comply with the same regulations applicable to traditional securities, including the preparation of prospectuses and continuous disclosure obligations.

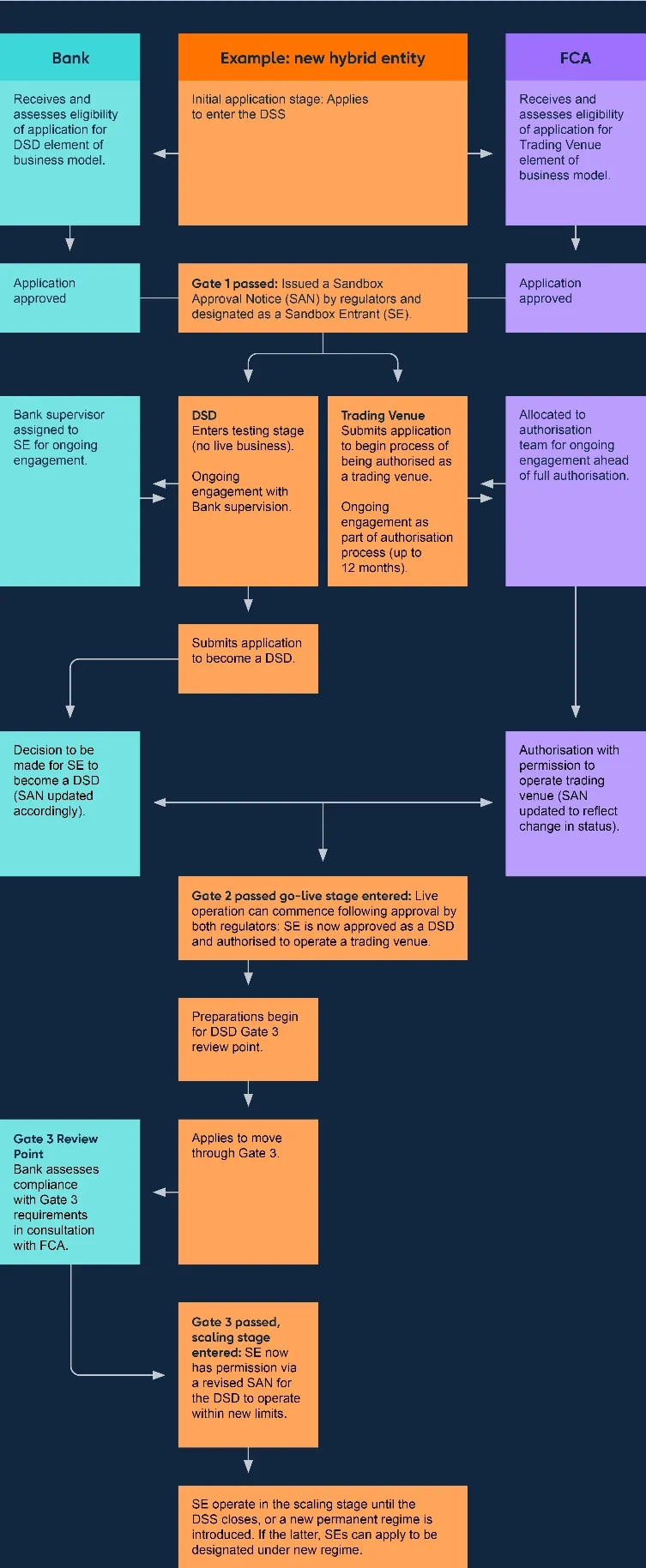

The UK operates the Digital Securities Sandbox (DSS) to facilitate the introduction of security tokens, where participating entities are subject to joint supervision by the FCA and the Bank of England. The UK is designing its system based on a hybrid model, where a single legal entity can perform both trading venue functions and settlement/custody functions, the latter being referred to as a Digital Securities Depository (DSD).

Applicants must submit their respective entry applications for the DSS to both the FCA and the Bank of England, after which they proceed through the following stages:

Gate 1: Application to become a sandbox entrant and begin non-live testing and preparation. Concurrently, the applicant undergoes the FCA’s exchange authorization process, which may take up to 12 months.

Gate 2: Approval to begin live activities in the DSS.

Gate 3: Application to increase limits and scale up activity.

Gate 4: Approval for operating outside DSS under a possible new permanent regime.

This sandbox model is scheduled to conclude in December 2028, and the empirical results obtained therein will serve as the legislative basis for the future digital securities regulatory framework. The UK utilizes the regulatory sandbox not merely as a temporary experiment, but as a phased implementation pathway leading toward formal institutionalization.

Source: Bank of England

4.7.2 Law Commission Report: Digital Assets

Similar to Liechtenstein’s "Token Container Model," the UK is pursuing legislative reforms to grant direct legal effect to tokens. In 2023, the UK Law Commission recommended the necessity of recognizing digital assets as a "third category" of personal property, distinct from the traditional categories of "things in possession" (tangible objects) and "things in action" (claims or rights).

This recommendation reflects the critical awareness that DLT-based tokens are not sufficiently encompassed by the existing property law framework. If this recommendation is adopted, it is expected to provide a robust legal foundation to protect the possession and ownership of tokens under UK law.

Through the "Federal DLT Act" enacted in 2021, Switzerland has fully integrated distributed ledger technology into its existing legal framework, including the Civil Code (specifically the Code of Obligations). A key innovation is the concept of "Registration Agreements," which allows the transfer mechanism of tokens to be designed flexibly according to the parties' agreement—such as smart contract logic and terms of use—rather than being uniformly prescribed by law. This structure does not fix the distributed ledger as a static technical infrastructure; instead, the law provides only the minimum requirements for the establishment of rights, leaving the specific transaction mechanisms to the autonomy of market participants.

Furthermore, Switzerland has established a secondary market for security tokens via distributed ledgers by introducing the "DLT Trading Facility License," which allows for the integrated performance of trading, settlement, clearing, and custody functions. The SIX Digital Exchange (SDX) stands as a representative case where Switzerland’s DLT-based securities regulation has been realized as actual market infrastructure. Under this legal foundation, Swiss corporations are now able to conduct "native issuance," where shares are issued in digital form from the very beginning.

The security tokens issued by Backed Finance and Ondo Finance are securities structured as "Tracker Certificates," designed to allow investors to track the performance of underlying assets on a 1:1 basis without requiring direct ownership of those assets. Under the MiFID II framework, these instruments are classified as "Transferable Securities".

Backed Finance and Ondo Finance adopted Swiss law—which explicitly codifies the legal status and transfer of rights for DLT-based securities—as their governing law. Simultaneously, they established a strategic "multi-jurisdictional regulatory integration" model to overcome the limitation of Switzerland not being a member of the European Economic Area (EEA). Specifically, these entities obtained approval from the Financial Market Authority (FMA) of Liechtenstein, an EEA member state, in accordance with the EU Prospectus Regulation. By linking this approval with the Passporting system, they completed a legal structure that enables the lawful issuance of securities to qualified investors across the EU, including Germany and France.

The distribution of Backed Finance’s xStocks within Europe is conducted based on the investment firm license (No. 342/17) held by PEDSL (Payward Europe Digital Solutions (CY) Limited), which is regulated by the Cyprus Securities and Exchange Commission (CySEC). In this framework, PEDSL does not act as an intermediary but serves as the direct counterparty to the transactions.

Unlike Robinhood’s stock tokens—which are derivatives and cannot be transferred out of the application—the security tokens of Backed Finance and Ondo Finance are capable of onchain circulation. In non-custodial environments such as Bitget or MetaMask, this allows users to hold and transfer tokens directly via their own wallets, effectively functioning as peer-to-peer (P2P) transactions rather than exchange-based trades managed by the service provider.

Meanwhile, Ondo Finance is accelerating its entry into the U.S. tokenized stock market, extending its reach beyond Europe. To facilitate distribution within the United States, Ondo Finance is establishing an infrastructure that strictly adheres to the U.S. securities regulatory environment. Specifically, the firm utilizes Oasis Pro Markets—an SEC-registered broker-dealer and Alternative Trading System (ATS) operator—to conduct brokerage activities. Furthermore, by appointing Oasis Pro Transfer Agent as its transfer agent, Ondo Finance is developing a tokenized stock distribution system that maintains rigorous compliance with the institutional regulations of the U.S. capital markets.

In November 2023, the Hong Kong Securities and Futures Commission (SFC) outlined its regulatory direction for security tokens through the "Circular on Intermediaries Engaging in Tokenised Securities-Related Activities." Hong Kong maintains a technology-neutral stance, asserting that tokenized securities are identical to traditional securities in terms of their legal and economic substance, regardless of the underlying technical implementation. Consequently, existing securities regulations apply directly to equity tokens. While the SFC theoretically permits both public and private blockchains, it emphasizes rigorous controls over transfer restrictions, minting and burning mechanisms, and procedures for transaction reversal or redemption when utilizing public blockchains.

Regarding the issuance structure, Hong Kong currently recognizes the legal effect of records on a distributed ledger primarily through contractual arrangements. To institutionally recognize "native issuance," where rights are established directly via distributed ledger records, further legislative reforms are required to introduce the concept of "possession" for electronically transferable records. Meanwhile, to provide brokerage or trading services for security tokens or virtual assets, an entity must either (1) be a platform operator holding Type 1 (Dealing in Securities) and Type 7 (Providing Automated Trading Services) licenses under the Securities and Futures Ordinance (SFO), or (2) obtain a Virtual Asset Trading Platform (VATP) license under the Anti-Money Laundering Ordinance (AMLO).

By leveraging the principle of freedom of contract within the existing Common Law framework prior to formal legislative amendments, Hong Kong has opened a practical path for the industry. This serves as a significant pragmatic regulatory model that ensures market innovation is not stifled during legislative lacunae.

One of the key implications of Hong Kong’s 2023 guidelines is the abandonment of the blanket practice of classifying all security tokens as “complex products.” Previously, tokenized products were automatically deemed complex solely by virtue of being tokenized, which effectively restricted their sale to retail investors. The guidelines clarify the principle that, where the underlying asset itself is non-complex, the mere fact of tokenization does not justify classification as a complex product.

By dismantling regulatory barriers that had limited investor access on purely technological grounds, the guidelines have opened the door to the activation of a retail-oriented security token market.

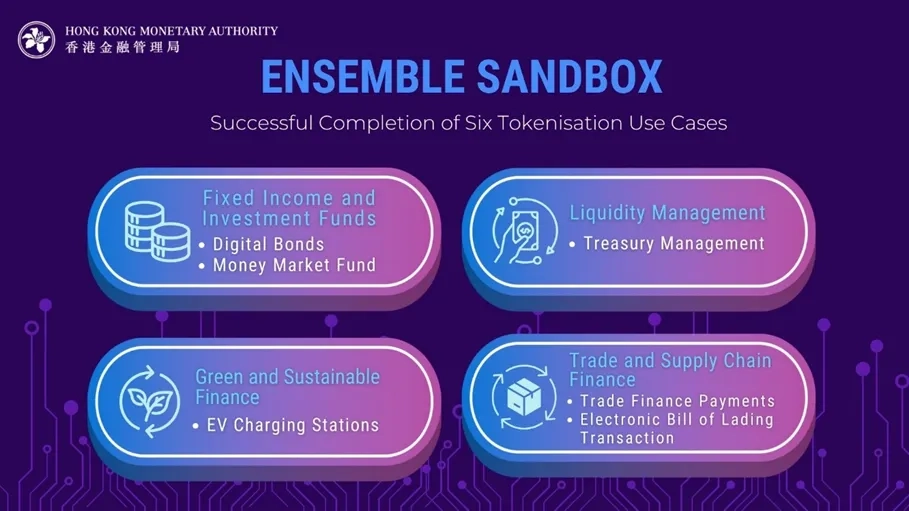

Project Ensemble, led by the Hong Kong Monetary Authority (HKMA), is an initiative aimed at piloting a next-generation financial market infrastructure (FMI) tailored for transactions in tokenized assets. A central focus of the project is the implementation of an interbank real-time settlement architecture leveraging wholesale central bank digital currency (wCBDC). The project conducts proof-of-concept testing to validate the technical interoperability among tokenized assets, tokenized deposits, and wCBDC.

By implementing a system in which assets and money are settled on a single ledger, the project presents a reference model for addressing long-standing inefficiencies in traditional securities markets, including settlement delays and counterparty risk. In this respect, the initiative represents a significant technological milestone, as it goes beyond mere asset tokenization toward the full digital integration of the monetary system and capital markets.

At present, in many jurisdictions, security tokens are being incorporated into existing securities law frameworks and are designed to be subject to the same level of regulation and investor protection as traditional securities. However, the significance of security tokens extends beyond the mere digitization of record-keeping.

The realization of instant settlement through distributed ledger technology, together with an integrated structure encompassing trading, clearing, and settlement, has the potential to fundamentally enhance the operational efficiency of capital markets and to accelerate the velocity of capital circulation. Furthermore, by enabling exchanges with stablecoins and interoperability with DeFi protocols, security tokens are expected to function as boundary assets that connect traditional finance with decentralized finance, thereby facilitating convergence with the onchain financial ecosystem.

The emergence of such new financial infrastructure should, from a regulatory perspective, be approached not as a matter of simple permission or prohibition, but as a challenge of building systemic resilience to ensure the stable functioning of the financial system in a transformed market environment. While preserving the principles of prudential regulation and investor protection that have been accumulated under existing securities regulation, it is essential to design a sophisticated regulatory framework that can institutionally accommodate the programmability and cross-border interoperability enabled by distributed ledger technology.

Ultimately, future regulatory strategies should focus not on ex ante controls that suppress innovation, but on flexible and phased regulatory reforms capable of managing risks while responding to changes in market structure.

Dive into 'Narratives' that will be important in the next year