The crypto market is shifting focus from short-term price movements toward real business value and sustainable growth. This has sparked greater interest in protocols that demonstrate concrete results through metrics like user adoption and revenue generation.

Three areas have proven their market fit in the crypto industry: blockchain platforms, exchanges, and asset management services. Each sector requires its own specific evaluation framework due to their distinct success factors.

The link between protocol sustainability and token value has become crucial. In response, more projects are implementing strategies designed to convert protocol success into token value. These include buyback and burn models or expanding token utility through native chain launches

From the ICO boom of 2017, through the DeFi and NFT summer of 2021, to the memecoin frenzy of 2024, each market cycle has attracted enormous capital. Investors have boldly bet on the technological innovations and potential value these projects promised. Yet when each cycle ends, projects built on flashy marketing and empty roadmaps vanish, while only a few that create real value survive. As market cools down, we return to the fundamental question: "Does this token actually have value?"

As excitement fades, investors naturally turn their attention to fundamentals. Can the value investing principles championed by Warren Buffett apply to digital assets? The question of applying value assessment to crypto protocols reflects a fundamental concern about sustainability.

In the cyclical nature of the crypto market, we may need to shift from a "get rich quick" toward sustainable long-term growth. Just as companies like Amazon, Google, and Apple in traditional markets have continuously innovated and built substantial value over time, the crypto ecosystem increasingly needs protocols capable of creating similar long-term value. Only protocols with genuine business models and consistent revenue streams will build a foundation for true growth beyond speculation.

Traditional value investing involves finding undervalued assets where intrinsic value exceeds current price. The stock market uses standardized metrics like P/E ratios, book value, and dividend yields to evaluate companies. However, the crypto market lacks these established indicators, and its high volatility and speculative nature make it challenging to identify under or overvalued assets.

Measuring the intrinsic value of crypto assets presents several difficulties. Many crypto projects haven't established clear revenue models or mechanisms that directly link revenue to token value. Unlike traditional companies with defined balance sheets of tangible and intangible assets, crypto protocols often have little beyond treasury holdings, making Net Asset Value assessments problematic.

Despite these challenges, as the market matures, investors are increasingly focusing on fundamental metrics like cash flow, revenue, active users, and protocol fees. Protocols and foundations are also evolving, with many introducing mechanisms that connect token value to actual revenue and implementing buyback and burn models to return value to token holders.

In this article, we'll analyze blockchains and crypto protocols as businesses, applying comparative value analysis to notable projects. We'll focus on three key business models in the crypto industry—blockchains, exchanges, and asset management—examining each using appropriate evaluation metrics.

Our approach relies on comparative analysis between projects with similar characteristics. While this relative value assessment can't fully measure absolute intrinsic value, it provides a useful framework for determining which projects offer relative value within their sectors in the current market.

As the blockchain industry matures, more efforts are being made to evaluate crypto protocols as legitimate businesses. Since traditional financial valuation models don't directly apply, we need evaluation criteria specifically designed for the crypto industry's unique characteristics.

In the crypto space, three business models have clearly proven their product-market fit: blockchains (Layer 1 and Layer 2), exchanges, and asset management. While other sectors like gaming, social platforms, and DePIN exist, they generally lack examples with sufficient scale and profitability. This analysis therefore focuses on the three established business models that have been validated in the blockchain industry.

Each sector has different characteristics and competitive factors, resulting in varying value creation mechanisms across business models. Consequently, we need to apply tailored evaluation criteria to each business model. The following sections outline the selected metrics and rationale for each area.

1.1.1 Blockchains (Layer 1 or Layer 2)

Blockchains fundamentally function as platform businesses. Networks like Ethereum, Solana, and BSC provide the infrastructure for developers and users, with their value and utility growing exponentially through network effects as they attract more participants.

As highlighted in the Fat Protocol Thesis, the blockchain industry often values future potential over current performance. These base-layer protocols are valued higher than the applications built on top of them, because they function as both comprehensive platforms and base currencies, creating value at the protocol level rather than primarily in the applications.

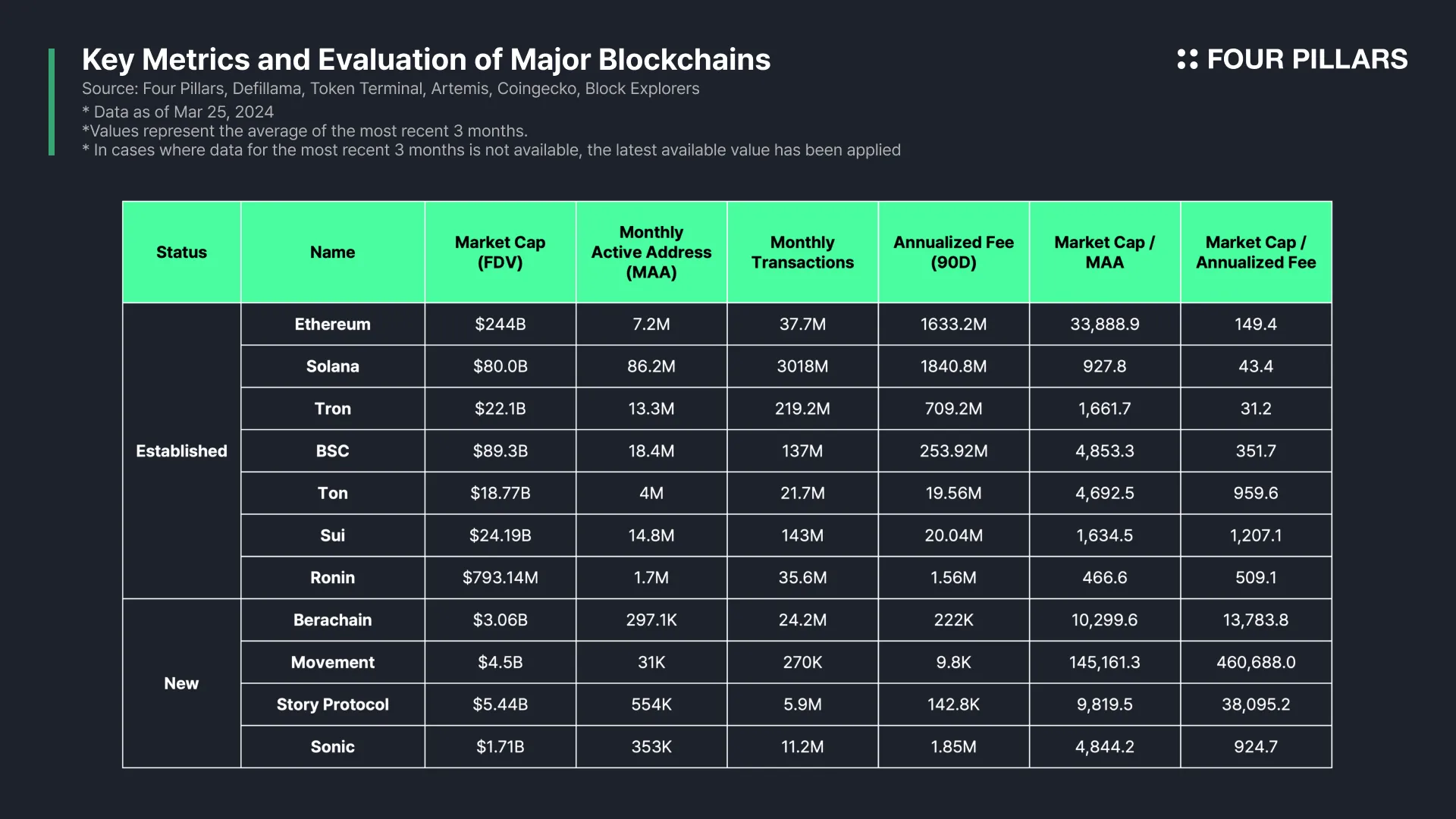

For evaluation of blockchains, active addresses and transaction counts serve as basic metrics of network activity. However, these metrics can be misleading—chains with lower fees and faster processing typically see more bot and spam activity. Total fees generated often provide a more direct indicator of demand for block space on the network.

Value can be assessed through ratios of activity metrics to market capitalization. Market Cap to Monthly Active Addresses (MC/MAA) shows the value assigned per user, with lower ratios suggesting potential undervaluation relative to the user base. Similarly, Market Cap to Fees (MC/Fee) resembles the traditional Price to Sales (P/S) ratio, where lower values indicate potential undervaluation relative to revenue.

1.1.2 Trading Platforms (Exchanges)

Exchanges have established the clearest product-market fit and revenue models in the blockchain industry. They're also among the most competitive areas, typically accounting for the majority of blockchain activity and trading volume.

Decentralized exchanges (DEXs) like Uniswap, Jupiter, and Curve provide the infrastructure and liquidity for token swaps, generating revenue through trading fees. This category also includes services like Banana Gun that don't directly provide liquidity but collect fees while offering user interfaces.

When DEXs and AMM-style exchanges first emerged, projects launched with various price discovery mechanisms, fostering experimentation and innovation. However, as the market matured, the technical differences between services have narrowed. Today, exchanges differentiate themselves primarily through liquidity, user experience, and access to speculative products like futures and meme coins.

Similar to blockchains, exchanges rely on network effects from users and liquidity for their long-term competitive advantage, measured by metrics like active addresses and trading volume. The total fees generated serve as both revenue and a direct indicator of user demand.

Market Cap to Volume (MC/Volume) indicates how the market values an exchange relative to its trading activity. MC/Fee compares market cap to revenue, similar to the traditional P/S ratio. Lower values in these ratios may suggest undervaluation compared to the exchange's activity or revenue generation.

1.1.3 Asset Management

Asset management protocols help users manage cryptocurrency assets and generate returns. This category encompasses most DeFi protocols outside of DEXs, including stablecoin issuers (Maker, Ethena), real-world assets (Ondo Finance), lending platforms (Aave), and liquid staking services (Lido).

In this sector, Total Value Locked (TVL) serves as the most critical metric, comparable to Assets Under Management (AUM) in traditional finance. TVL indicates not just scale, but also user trust and attractive risk-adjusted returns. Larger protocols typically benefit from better diversification and reduced systemic risk, making TVL more meaningful than just an indicator for its scale. Meanwhile, active addresses and transaction metrics are relatively less significant here, as securing substantial deposits from fewer high-value clients can be more advantageous.

Unlike the previous two business models, asset management protocols vary significantly in their operations and revenue generation methods. For example, Lido has a simple model that takes 10% of Ethereum staking rewards as fees, while Maker has multiple revenue streams including stability fees from DAI issuance, yield adjustment through DSR (DAI Savings Rate), and investment returns from held assets. Therefore, when comparing metrics or relative values between these services, it's important to consider their specific characteristics and differences.

For valuation, Market Cap to TVL (MC/TVL) shows a protocol's value relative to managed assets, similar to MC/AUM in traditional finance. Lower ratios may suggest undervaluation based on assets managed. Since protocols with similar TVL can have vastly different profitability, Market Cap to Revenue (MC/Revenue) helps identify potentially undervalued protocols based on their earning capacity.

The most notable observation is the valuation gap between established chains and recently launched newcomers. Movement, with the highest metrics, records a market cap to active address ratio that's over 100 times greater than Solana's. This suggests newer chains are being valued based on future potential rather than current performance. Conversely, Sonic, despite being a relatively recent blockchain, shows market cap to active address and transaction ratios similar to established chains, indicating a more reasonable valuation.

Solana demonstrates overwhelming activity metrics due to its low fees, fast transactions, and vibrant ecosystem. By monthly active address count, Solana records approximately 12 times that of Ethereum, and in transaction count, about 80 times more. Considering these figures represent a significant decrease from Solana's peak during last year's memecoin frenzy, it's clear that Solana maintains an exceptionally robust user base compared to all other chains. However, it's worth noting that chains with low fees and high transaction volumes, including Solana, may see inflated activity metrics due to bot operations.

Fee revenue for blockchains indicates demand for block space on that network. Unlike address count or transaction volume, fee revenue closely aligns with market capitalization rankings among these networks.

Blockchain fee revenue indicates demand for block space. Unlike address or transaction counts, fee revenue closely aligns with rankings of market cap across networks. However, low fee revenue doesn't necessarily indicate low demand for a blockchain. Affordable fees can serve as a competitive advantage for onboarding users and protocols. Particularly for Sui and Ronin, which show high transaction counts but relatively low fee revenue, this could indicate efficient block space utilization despite high user activity.

Overall, Solana, Tron, and Ronin networks appear undervalued relative to their activity metrics. Despite some decline after the meme coin boom, Solana's market cap to active address ratio remains much lower than other major chains. Its annualized fee revenue is among the highest of major chains, suggesting its market cap is undervalued compared to fee income.

Ronin has succeeded in attracting distinct users and ecosystem by focusing on the specific business area of onchain gaming, yet its market cap to active address ratio appears to be the most undervalued among major chains. However, its fee income is relatively low, placing its market cap to fee ratio in the mid-range.

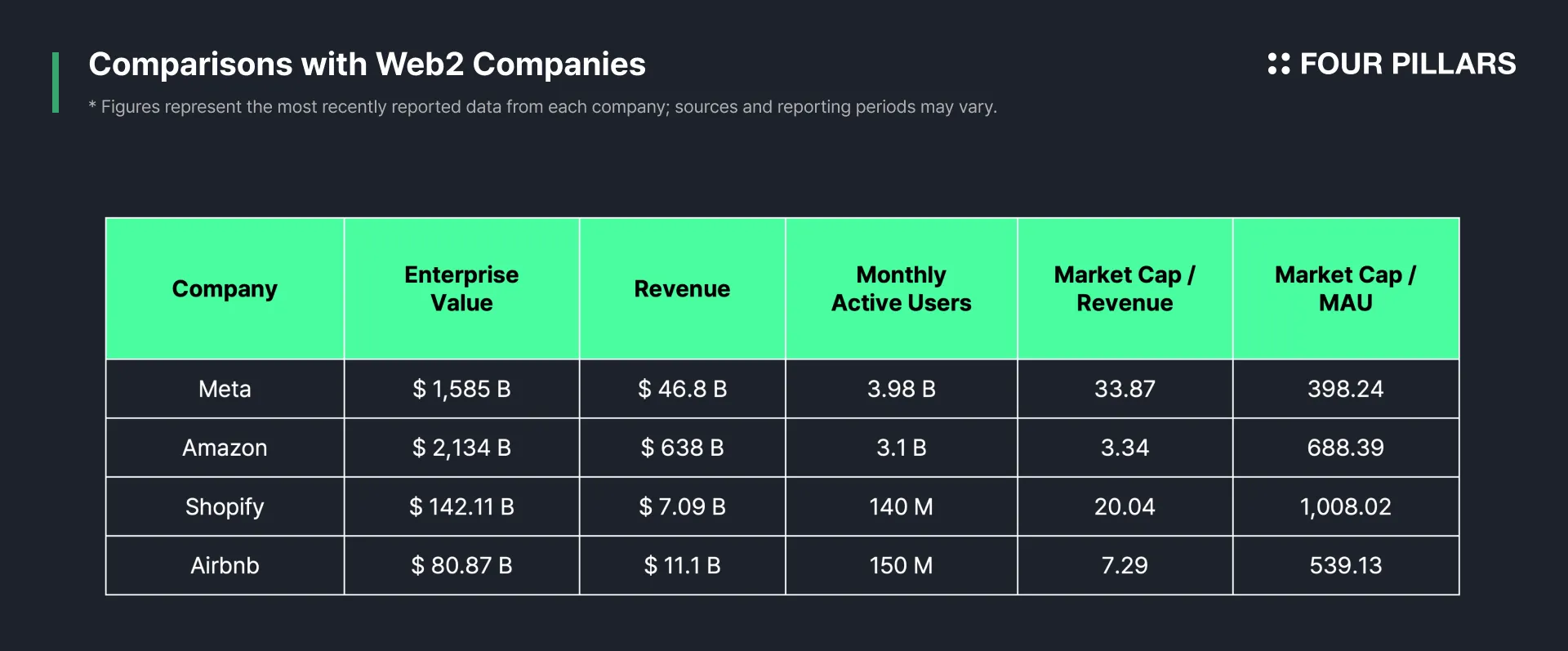

Comparing Web2 platforms with blockchains, their market cap to active user ratios aren't drastically different. Most major chains (except Ethereum) have monthly user to market cap ratios between 1,000 and 10,000. Large Web2 platforms like Meta and Airbnb have ratios around 500, while Amazon is at about 7,000 – lower than most of blockchains but reasonably different given service variations. However, active addresses in blockchain typically inflate actual number of user, meaning the real market cap per user gap is likely much larger.

The market cap to revenue ratio shows a significant gap between blockchains and Web2 platforms. While platform companies typically have ratios from under 10 to around 30, Ethereum shows approximately 150 times, and TON and Sui approach 1,000 times. Meanwhile, Solana and Tron show reasonable market cap to fee revenue ratios even compared to traditional companies.

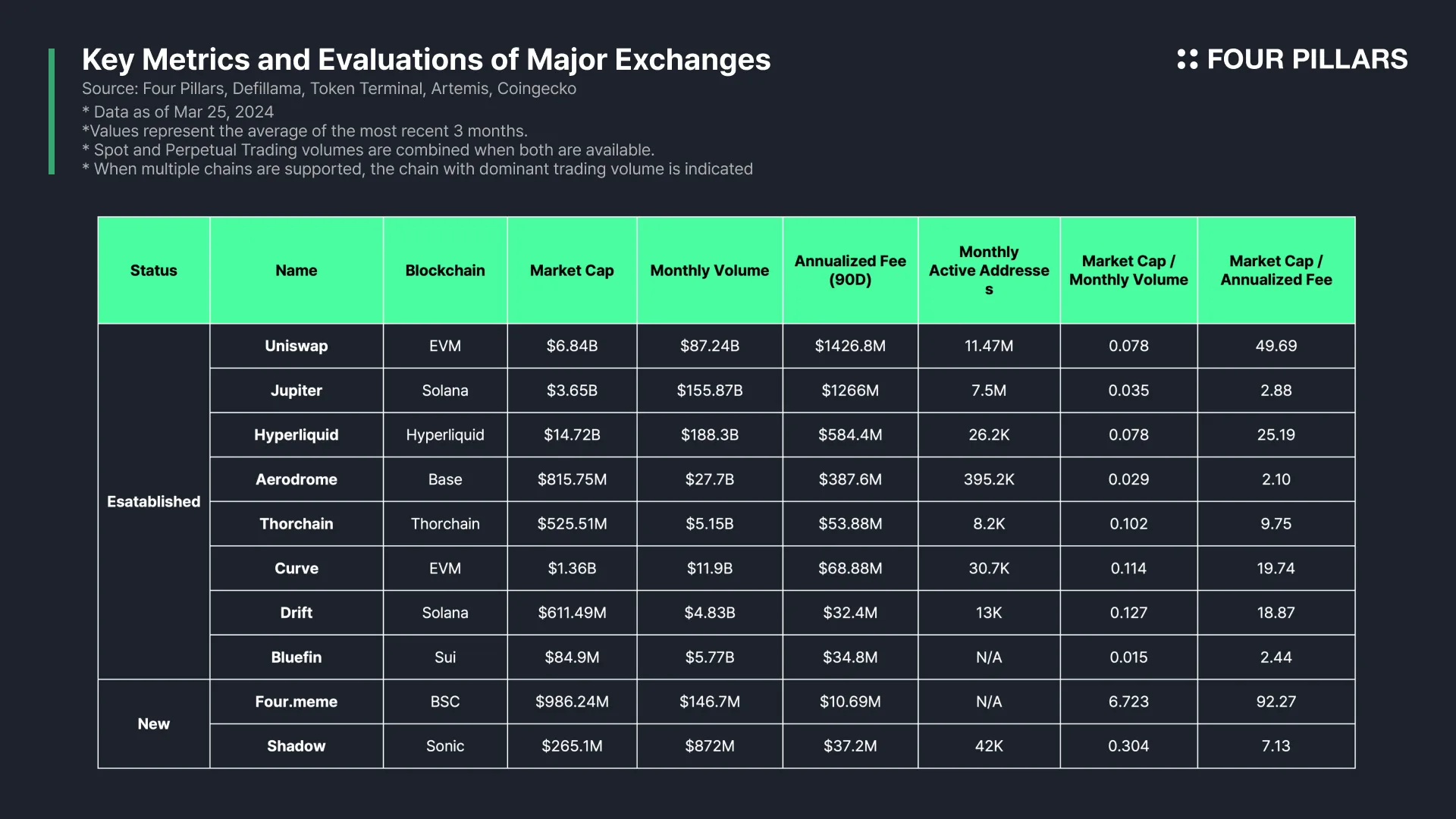

In the evaluation of decentralized exchanges, trading volume and fee revenue emerge as the most critical assessment metrics. A notable distinction exists between exchanges that offer futures trading and those limited to spot trading only. Hyperliquid stands out by achieving the highest trading volume despite having considerably fewer monthly active users compared to other platforms. This suggests that Hyperliquid's trading activity is dominated by a small group of professional traders executing large-volume transactions. By contrast, Uniswap—which focuses exclusively on spot trading and attracts predominantly retail users—generates only about half the trading volume of Hyperliquid or Jupiter, even though it maintains the largest user base. This indicates a significantly lower per-user trading volume on Uniswap.

When compared to the blockchain sector, the valuation disparities among exchanges appear relatively modest. Most exchanges maintain a market cap to monthly trading volume ratio between 0.03 and 0.1, with few outliers. This consistency likely stems from the straightforward and standardized nature of exchange businesses, which makes their performance more measurable and comparable. The existence of clear metrics such as trading volume and fee revenue enables markets to value exchanges with greater efficiency. Exchange business models rely on tangible factors like liquidity, user experience, and fee structures, rather than technical differentiation or potential monetary value—characteristics that make value assessment more accessible for investors compared to blockchain valuations.

For context with traditional financial companies, we can look at Coinbase as a comparable service. With monthly trading volume of approximately $100 billion, around 10 million users, and a corporate valuation of $44 billion, Coinbase provides an interesting benchmark. Leading Web3 DEXs such as Uniswap, Jupiter, and Hyperliquid match or exceed Coinbase's trading volumes, yet their token market capitalizations remain substantially lower than Coinbase's corporate value.

Following patterns similar to the blockchain market, newer trading platforms generally receive higher relative valuations than established exchanges, though this premium is less extreme. Four.meme, which functions as a meme coin launchpad on BSC, exhibits a remarkably high market cap relative to its monthly trading volume. While this might appear as overvaluation, the highly volatile nature of meme coin trading could potentially justify this premium if BSC experiences increased meme coin activity in the future. Meanwhile, Shadow, a prominent DEX on the emerging Sonic chain, demonstrates consistent growth in both users and trading volume despite its relatively recent launch. Its market cap to fee ratio compares favorably with established DEXs.

An analysis of market cap to annualized fees ratios reveals Jupiter, Aerodrome, and Bluefin as potentially the most undervalued exchanges. Jupiter particularly stands out by generating the highest fee revenue while maintaining a market cap merely half that of Uniswap. Despite Jupiter's commanding market share within the Solana ecosystem, the market appears reluctant to fully acknowledge its value—possibly due to its position as an aggregator without proprietary liquidity.

Similarly, Aerodrome displays a notably low market cap to fee ratio, suggesting undervaluation relative to its substantial fee revenue. This discounting likely results from its considerably weaker brand recognition compared to Uniswap (the flagship decentralized exchange across EVM chains) and its dependence on the Base chain alone for trading volume and user acquisition, which complicates the reflection of its potential value.

Lastly, Bluefin—a comprehensive spot and futures exchange operating on the Sui chain—presents perhaps the most undervalued market cap when measured against either monthly trading volume or annualized fees. Given that it represents virtually the only futures exchange on the promising Sui chain while also capturing significant spot trading market share, Bluefin's token value appears particularly underappreciated by the market.

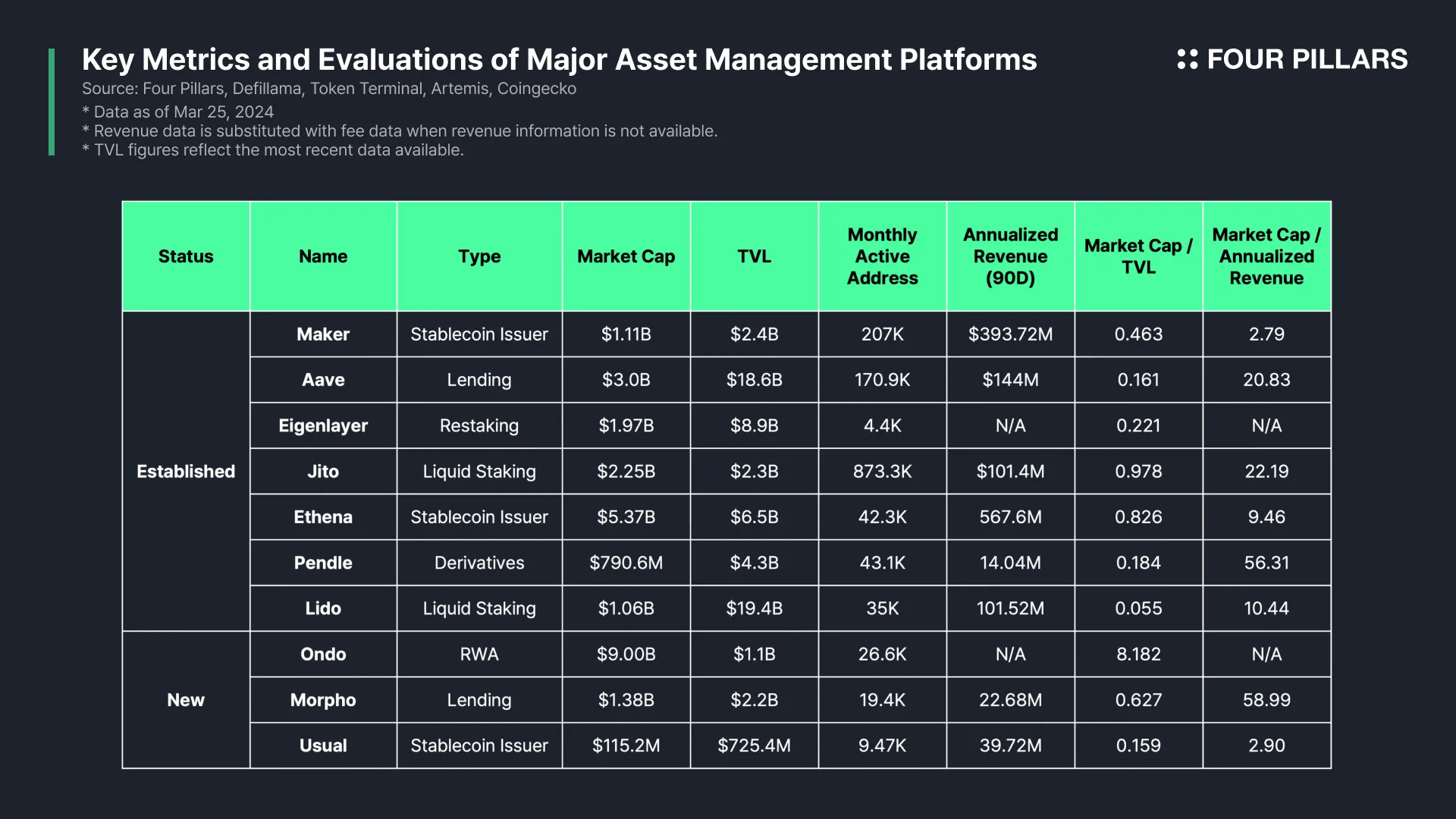

Unlike chains or trading platforms, asset management protocols show more evenly distributed market capitalizations. This reflects their longer history in blockchain applications and clearer service characteristics and revenue models, resulting in less speculative valuation. For this reason, even newly launched protocols in this category rarely display the extremely high valuations seen with new chains or exchanges.

Looking at active address counts, most protocols have similar levels of active users, with Solana-based protocols like Jito being exceptions. Leading services like Maker and Aave record relatively high user numbers, but most protocols typically have tens of thousands of active users. This consistency reflects the financial nature of these services, which target specific user segments, resulting in similar user groups across multiple protocols.

Among asset management categories, stablecoin issuance shows the highest profitability. Ethena, Maker (Sky), and Usual all generate substantial revenue and maintain high yields relative to TVL. This indicates consistent market demand for stablecoins and efficient fee models. Ethena particularly stands out, having achieved high market share and profitability through its innovative business model despite its relatively short operational history.

In liquid staking, there's a notable valuation difference between Ethereum's Lido and Solana's Jito. Though offering similar services, Jito's market cap to TVL ratio is nearly 20 times higher than Lido's. Jito gained this premium as Solana's leading staking platform during last year's rapid growth. Despite the TVL size difference, Jito generates revenue comparable to Lido, reflecting higher profitability through MEV revenue.

When examining market cap to TVL ratios, Lido (0.055), Aave (0.161), and Usual (0.159) show the lowest values. Lido's market cap represents only about 5.5% of its massive TVL. Among newer protocols, Usual has a relatively low $115.2M market cap compared to its $725.4M TVL, suggesting undervaluation despite being recently launched. However, considering traditional asset managers are typically valued at about 1% to 3% of AUM, crypto protocols still trade at a premium relative to total deposited assets.

Looking at market cap to revenue ratios, Maker (2.79) and Usual (2.90) appear most undervalued. Both focus on stablecoin issuance and show stable profitability. Maker generates the second-highest annualized revenue after Ethena, yet its market cap is low relative to earnings. Similarly, Usual has recorded high revenue despite being an early-stage project but shows a low market cap relative to both its TVL and profitability. This may reflect lower speculative interest or specific tokenomics affecting their market valuations.

As our analysis shows, blockchain services with established histories and proven product-market fit have developed clear business models and performance metrics. However, unlike the stock market where shareholder value is fundamental, in crypto, a protocol's success doesn't automatically translate to higher token value. Many projects with excellent products, active user bases, and steady revenue still struggle to see these strengths reflected in their token prices, creating one of crypto's persistent challenges.

With market maturation, many projects are now working to bridge this gap. We're seeing major protocols either 1) implementing token buybacks and burns to directly return value to token holders, or 2) launching their own blockchains to expand their tokens' utility. Both strategies represent efforts to strengthen the connection between protocol success and token value.

Buybacks and burns have been standard shareholder value return mechanisms in traditional markets for decades. In crypto, MakerDAO and Aave stand out as notable examples using burn mechanisms effectively.

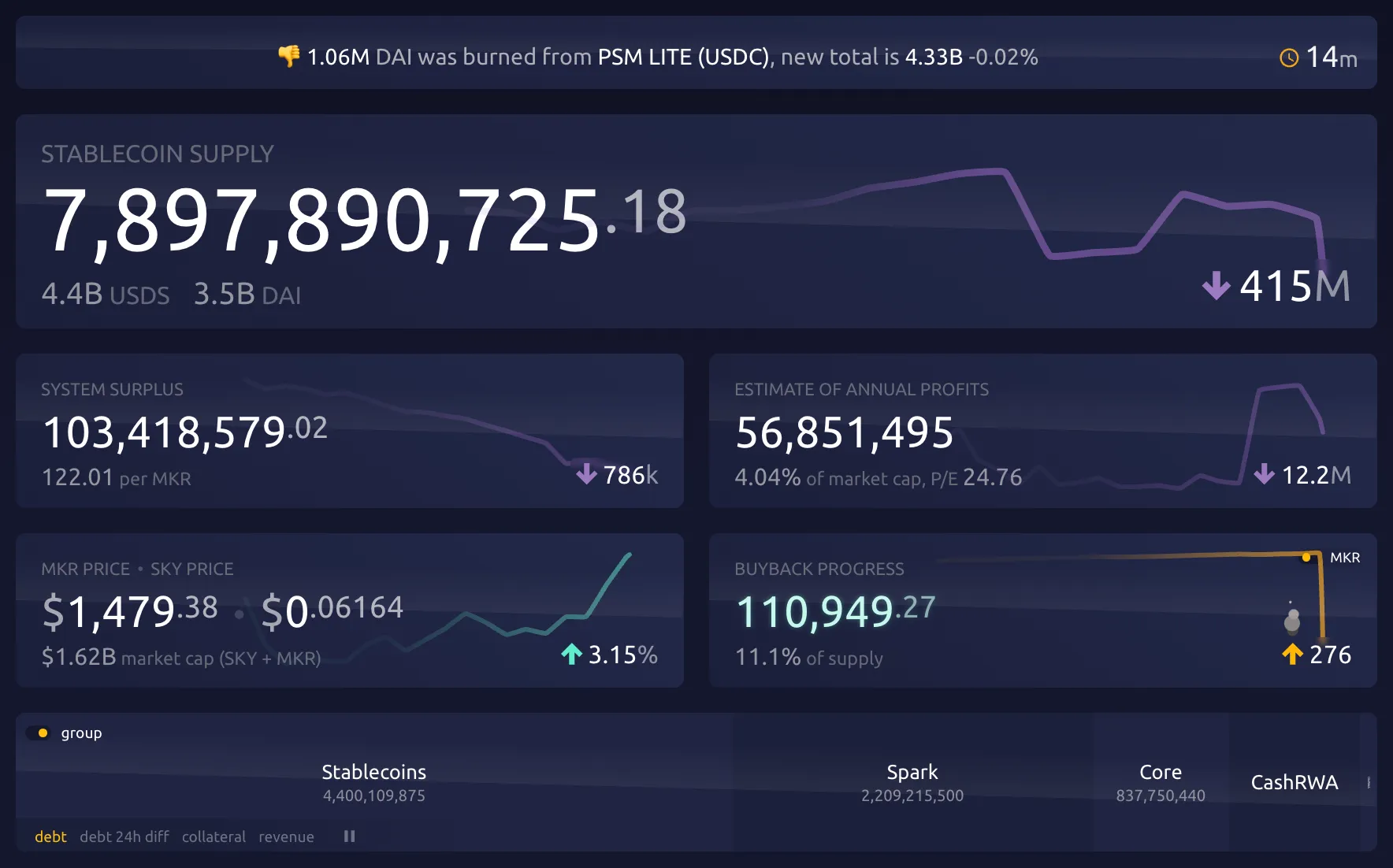

Source: Maker Burn

MakerDAO (now Sky) allocates a portion of its protocol revenue to purchase and burn MKR tokens through its Smart Burn Engine. This system activates whenever the protocol's surplus buffer exceeds $50 million, using excess DAI stablecoins to buy MKR tokens from Uniswap pools. These purchased tokens are permanently burned, reducing the circulating supply. According to Maker's founder Rune, the current mechanism results in daily SKY token burns worth approximately 1 million USDS.

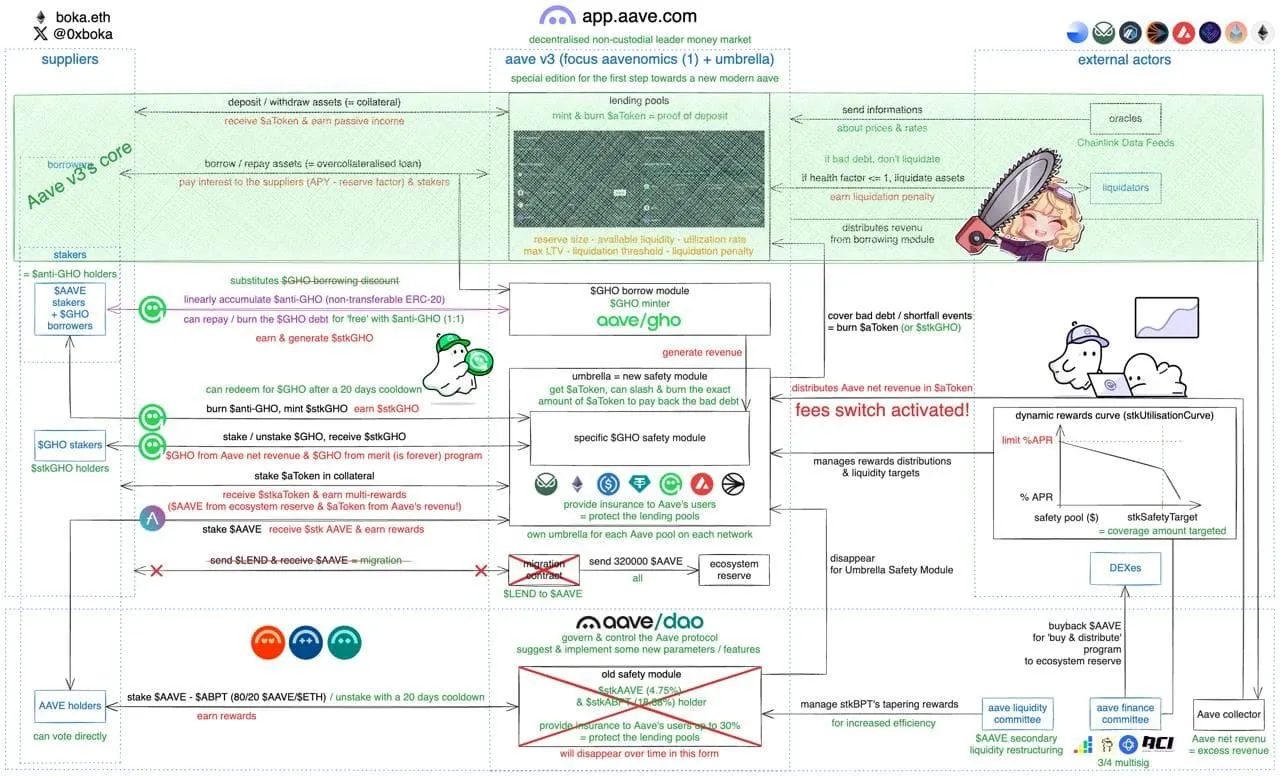

Source: [ARFC] Aavenomics implementation: Part one

Aave has recently introduced a more sophisticated buyback mechanism through its "Aavenomics" governance proposal. Under this plan, the Aave Finance Committee will purchase $1 million worth of AAVE tokens from the market every week during the first six months. This initiative is funded through the protocol's surplus revenue, creating token scarcity and upward price pressure. The community strongly supported this proposal, and AAVE's price increased by 21% following the announcement.

These buyback and burn mechanisms create a direct link between protocol success and token value, forming an aligned incentive structure where token value grows alongside the protocol. However, for early-stage projects that haven't achieved sufficient decentralization, buyback mechanisms might be interpreted as having security-like characteristics. Additionally, conducting buybacks during periods of overvaluation can destroy value rather than create it. Therefore, buybacks and burns work best for protocols that have already reached significant scale and established stable revenue models. In regulatory environments where direct dividends face securities law challenges, buybacks offer a practical alternative to return value to token holders while minimizing legal risks.

Another approach to increasing token value involves protocols launching their own blockchain networks and positioning their tokens as native assets within these ecosystems. This strategy significantly expands a token's utility beyond governance, creating fundamental demand. Recent notable examples include Unichain and Jupiter Network. Both protocols share the common characteristic of being dominant DEXs in their respective ecosystems—Ethereum and Solana.

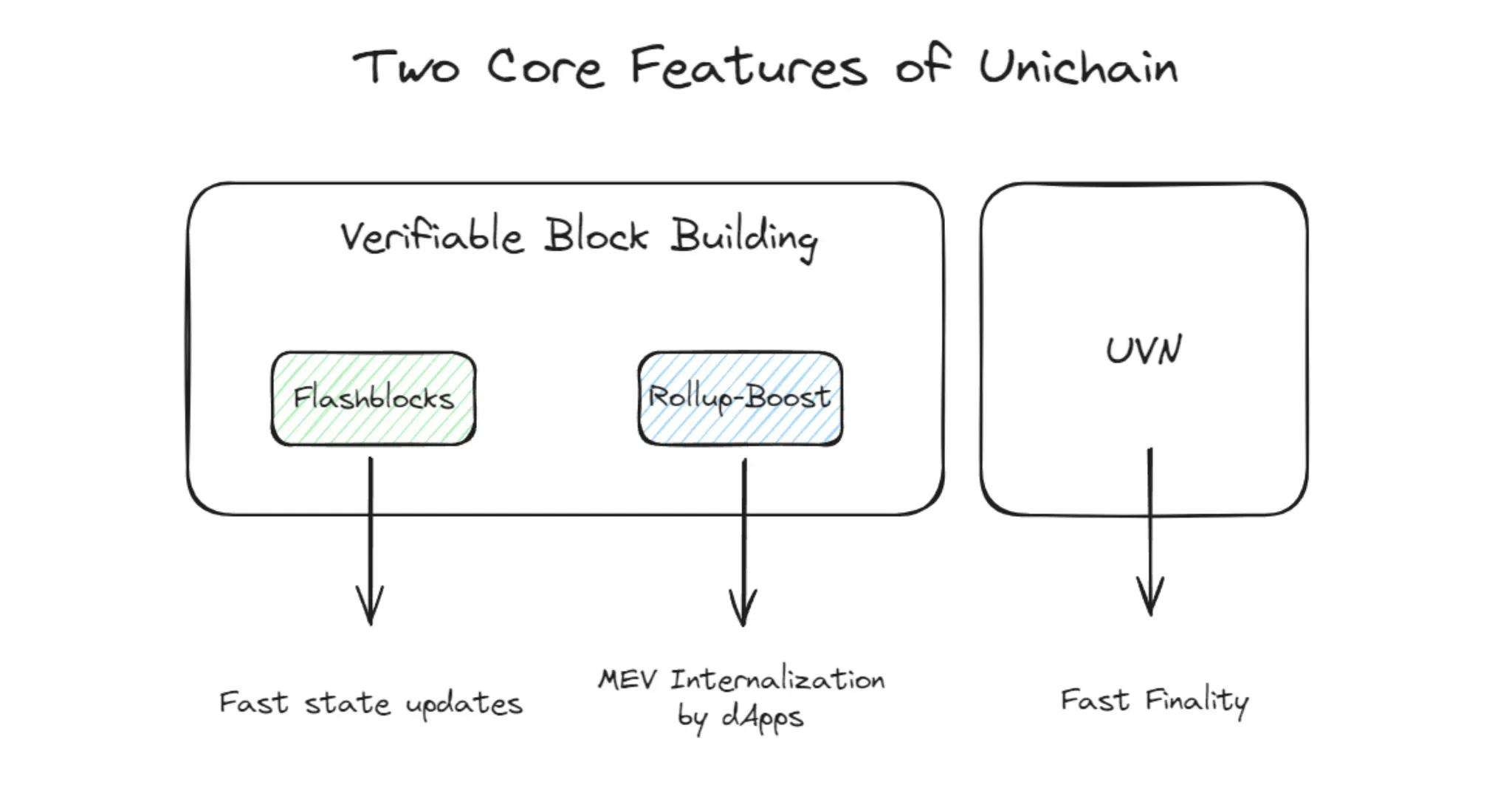

Source: Uniswap, Flashbots, and OP-Stack: The Trinity Behind Unichain

Uniswap recently transformed the UNI token's utility by launching Unichain, a Layer-2 solution. Released in February 2025, Unichain redirects approximately $360 million in fees that previously went to Ethereum validators, sending them instead to Uniswap Labs and potentially to UNI token holders.

From a tokenomics perspective, the key advantage of this chain launch strategy is the fundamental transformation of the UNI token itself. UNI can now validate transactions through the Unichain validator network or be staked to earn sequencer fees. This creates inherent demand beyond speculative value or governance rights. The market responded positively to this initiative, with the UNI token price rising by 12% after the announcement.

Jupiter is also expanding beyond its role as a Solana DEX aggregator by announcing Jupnet, a multi-blockchain network. Announced in January 2025, Jupnet consists of three core components: the DOVE network (a decentralized oracle service), an omnichain distributed ledger network supporting seamless cross-chain transactions, and an aggregated distributed identity system that enhances user accessibility.

Source: X(@JupiterExchange)

Interestingly, Jupiter implements a dual value accumulation strategy that combines both a native chain and buyback mechanisms. Jupiter allocates 50% of protocol fees to JUP token repurchases and holds these repurchased tokens for three years, creating a sustained supply reduction effect. Based on current revenue streams, annual buybacks exceeding $100 million are anticipated, with the first buyback already recovering JUP tokens worth $3.33 million.

The native chain transition strategy offers several important advantages. Most significantly, when a token functions as the base currency of a chain, its fundamental utility expands dramatically. Additionally, by capturing fee revenue within the chain, value that would otherwise flow to external systems remains preserved within the ecosystem. This can generate greater long-term value for both the protocol and its token holders.

However, operating a dedicated chain requires substantial technical expertise and resources. Activating and maintaining a new blockchain network presents much greater challenges than simply building on existing ecosystems. Issues with cross-chain compatibility and security also remain ongoing concerns, making this strategy—similar to buyback and burn mechanisms—more appropriate for protocols that have already validated their product-market fit and are ready for expansion rather than early-stage projects still finding their footing.

The crypto market is steadily moving beyond speculative waves toward valuations based on real business fundamentals. This evolution happens naturally as the market matures and investors increasingly prioritize sustainable value creation over short-term gains.

Our comparative analysis of key metrics across different business models offers a practical framework for spotting potentially undervalued or overvalued protocols in today's market. However, these evaluations reflect current performance and might not fully capture future growth potential or the unique attributes that make each protocol special.

We're also seeing growing attention to the mechanisms that connect protocol success with token holder benefits. Strategies like buybacks, burns, and launching native chains are increasingly important in creating alignment between protocols and their token holders, establishing tokenomics models that support long-term growth.

In the end, the most valuable protocols in crypto will be those combining sustainable business models with engaged user communities and clear paths for translating protocol success into token value. These projects will create lasting value beyond market speculation and build the foundations for sustainable growth in the years ahead.

Dive into 'Narratives' that will be important in the next year