Since the approval of the BTC spot ETF, interest in blockchain within the financial industry has been rising, with numerous efforts to integrate blockchain into finance.

Numerous efforts, including KYC-enabled decentralized applications and private blockchains, have been explored; however, these approaches often result in the creation of siloed ecosystems.

Kinto, based on Arbitrum Orbit as an Ethereum L2, features enforced KYC and AA at the network level, allowing participants from the traditional financial industry to transact safely.

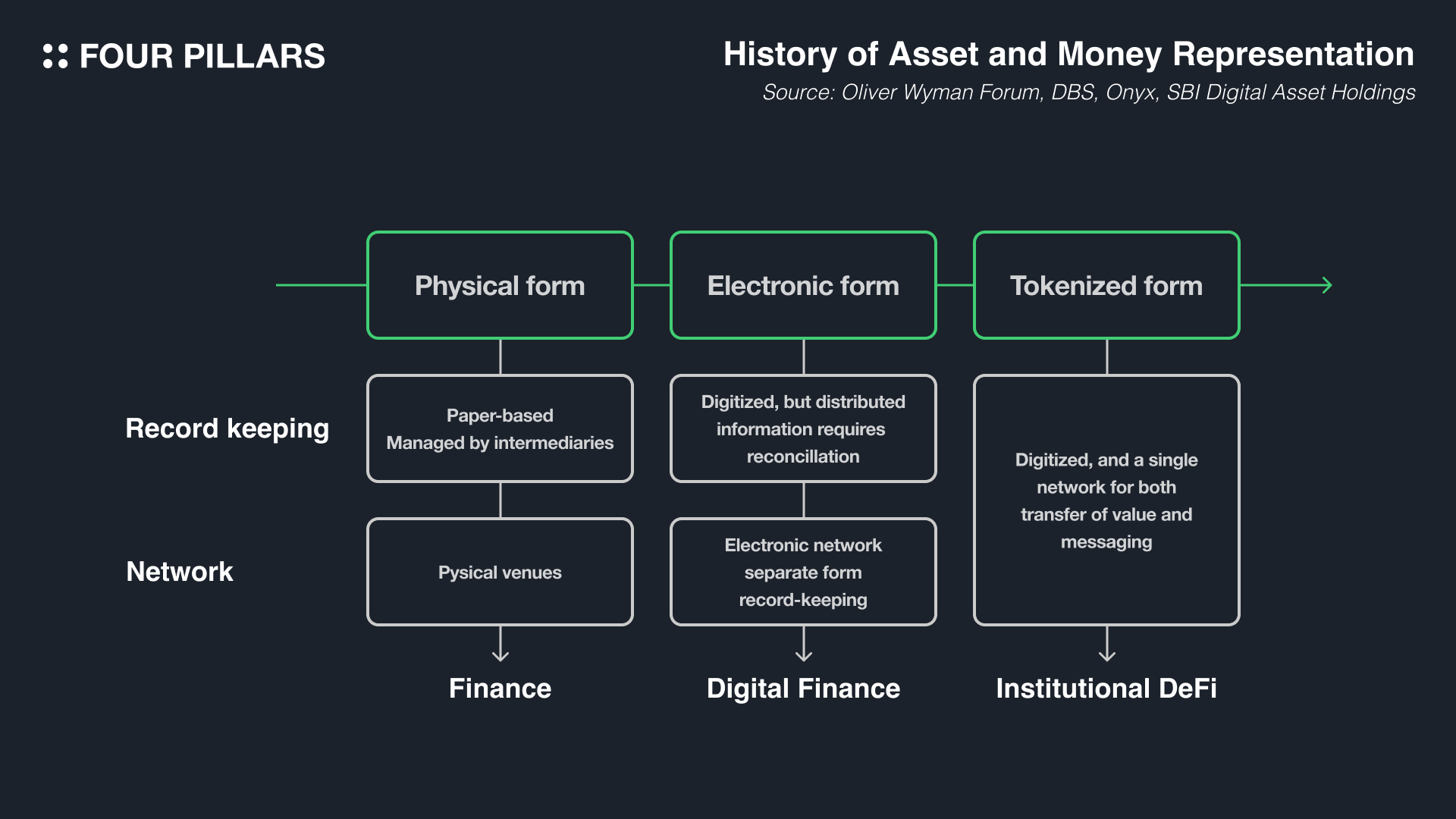

Blockchain technology possesses many characteristics suitable for the financial system. While networks like Bitcoin and Ethereum offer strong decentralization, providing a trustless environment that does not depend on any single entity, even centralized blockchains can bring significant benefits to finance, with efficiency being a primary advantage. Contrary to the general perception of blockchain as inefficient, its application in the financial industry can paradoxically lead to greater efficiency.

The financial industry did not start as a unified system worldwide but grew differently in each country based on strict regulations. As a result, international transactions involve various stakeholders and systems, leading to complexity, and even domestic transactions can take two days to settle with the T+2 system. For this reason, the U.S. SEC plans to implement a T+1 system starting May 2024 to alleviate some of these inconveniences.

Blockchain operates essentially as a decentralized database with a timestamp server, allowing all transactions to be executed and settled in real time. This characteristic has the potential to revolutionize the cumbersome and complex systems of the traditional financial industry. For instance, JP Morgan has settled daily transactions worth $1B through its JPM Coin system, and DTCC has developed a pilot for a blockchain-based settlement system, Project Ion, demonstrating blockchain's potential synergy with the financial sector.

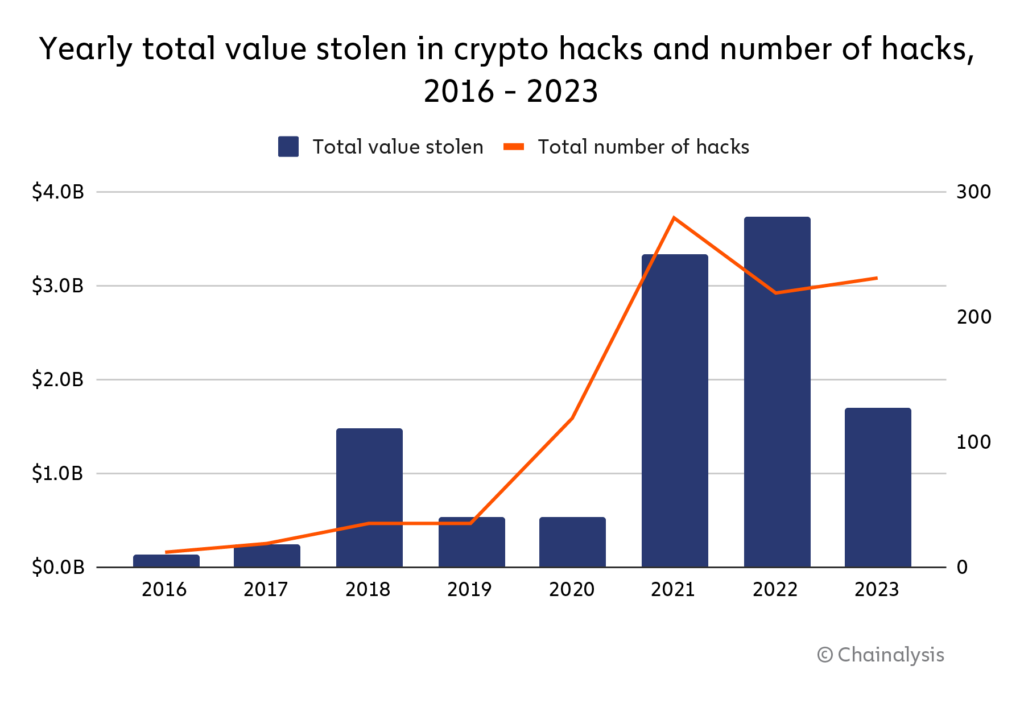

Source: Chainalysis

Despite the recent approval of a Bitcoin spot ETF in January, attracting significant funds into ETFs and garnering more interest from financial institutions in blockchain, there are still considerable constraints for the traditional financial industry to adopt blockchain networks. The first is anonymity; the anonymous nature of blockchain networks complicates tracking and penalizing asset owners, making compliance with KYC/AML essential. The second concern is the risk of hacking; public blockchain networks have seen significant thefts, with $3.7B in 2022 and $1.7B in 2023, indicating that the exposure of assets to potential attackers makes public blockchains unsuitable for the financial industry.

Compared to the Web3 ecosystem, the traditional financial industry possesses considerable liquidity. If the blockchain sector can adequately prepare systemically and regulatorily to absorb this liquidity, it could be a game-changer. According to a report by JP Morgan, for blockchain to integrate with traditional finance, it must meet the following criteria:

KYC/AML compliance must be enforced for all participants interacting with the blockchain.

Privacy protection for participants' transaction histories and positions, akin to how client and trade information is safeguarded by brokers in traditional finance.

Enhanced security measures for cross-chain bridges, private keys, and oracles.

Mature governance processes and token distribution.

A recourse mechanism for operational errors, as all financial systems are susceptible to them.

What efforts have been made in the blockchain ecosystem so far?

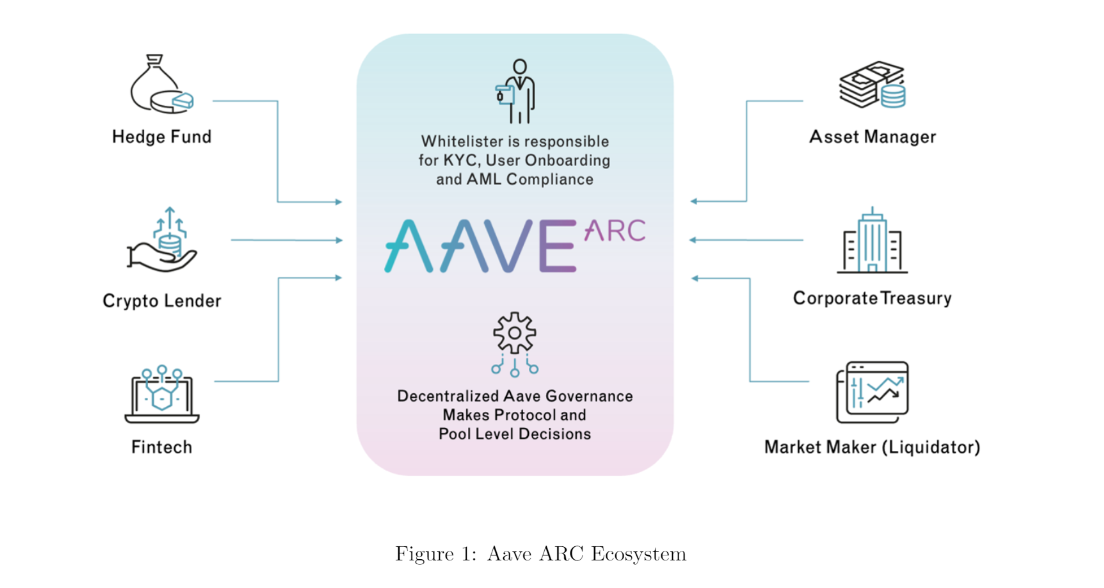

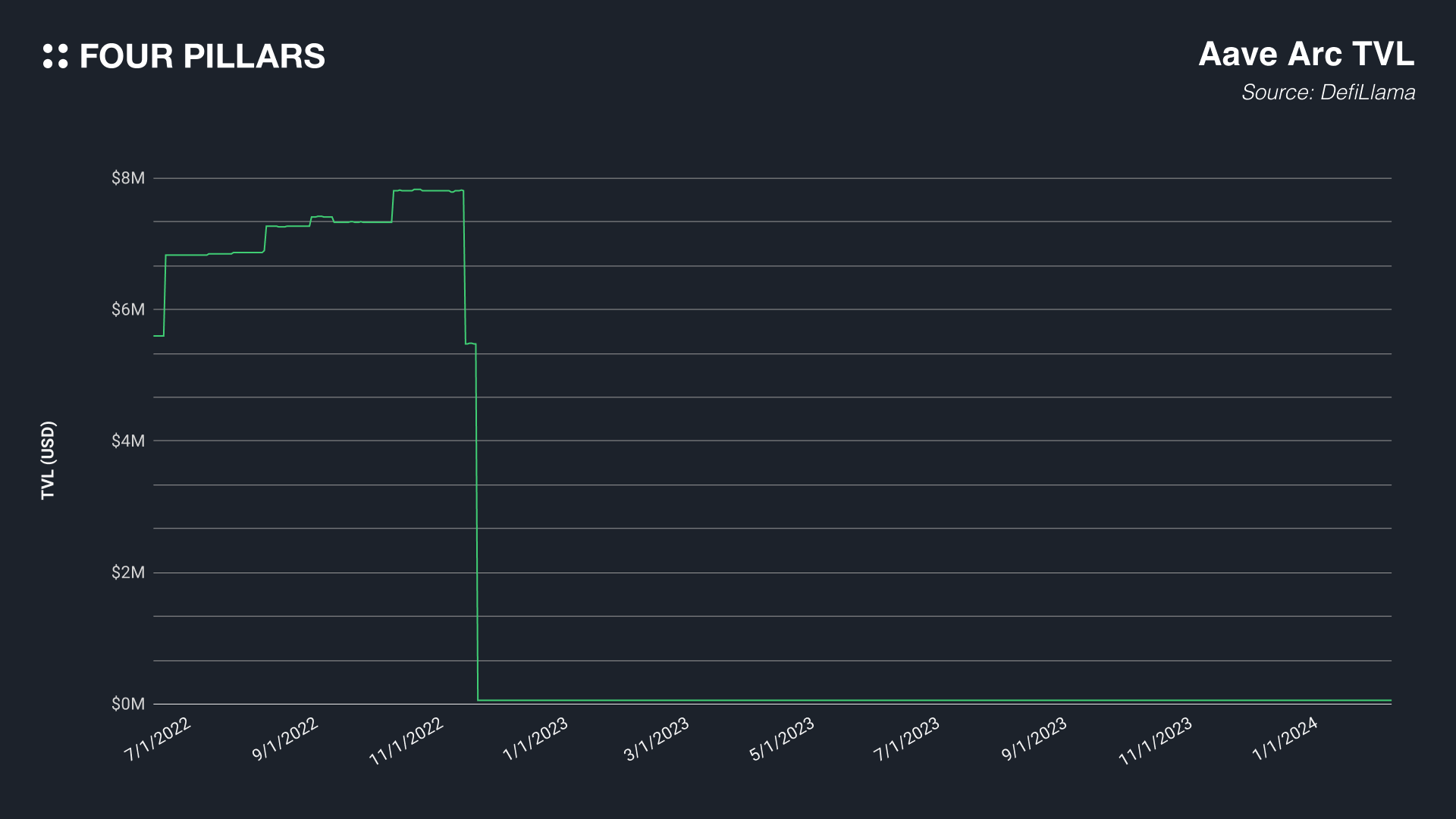

2.2.1 KYC’d DeFi - Aave Arc

The first attempt involves KYC’d DeFi services, allowing only KYC-verified users to access the DeFi protocol, with Aave Arc launched in 2021 as a notable example. Aave is one of the largest lending protocols in the Ethereum ecosystem. Although some smaller institutions can directly use Aave on the public network, most institutions cannot engage in transactions with non-KYC'd counterparties, making direct use impractical. Aave introduced Aave Arc to address this issue.

Source: Aave

Aave Arc operates as a permissioned liquidity pool based on Aave V2, incorporating additional smart contracts for whitelisting users. Only those who have undergone KYC or KYB can interact with Aave Arc, with processes like KYC, AML, and CFT conducted by Aave Arc's whitelisters. Fireblocks was the first whitelister, granting whitelist access to 30 trading firms, including GSR, Celsius, and Wintermute.

Unfortunately, despite initial significant fund utilization, the TVL in Aave Arc plummeted following the bankruptcy of FTX in November 2022 and the impact on many institutions. The sharp rise in U.S. interest rates in 2022 also contributed to the declining demand for DeFi. Currently, only about $58k is deposited in Aave Arc, which seems like no one is using now.

2.2.2 Permissioned Network - Onyx Digital Assets, Avalanche Evergreen

The second approach involves permissioned networks, where only approved participants can interact with the network. This is a common method for accessing traditional financial markets, with Onyx Digital Assets and Avalanche Evergreen as prominent examples.

Onyx Digital Assets, operated by JP Morgan's blockchain subsidiary Onyx, is a blockchain for asset tokenization. Institutions can tokenize and trade various assets through Onyx Digital Assets. The JPM Coin System, allowing JP Morgan's clients to trade and settle quickly, is based on Onyx Digital Assets.

Avalanche Evergreen is a modified Subnet service by Avalanche, tailored for the traditional financial industry, offering appchain services compliant with KYC/KYB standards and customizable features like gas tokens and virtual machines. The Spruce Subnet created with Avalanche Evergreen has been used as a testnet by T. Rowe Price Associates, Wisdom Tree, Wellington Management, and Cumberland to explore blockchain usage.

Despite all the examples provided being blockchain-based services that comply with KYC/AML regulations, making them safe for financial institutions to use, they share a common drawback: each operates within its isolated ecosystem. While utilizing blockchain technology does enhance the efficiency of the traditional financial system despite these isolated ecosystems, it's a missed opportunity not to leverage the inherent characteristic of blockchain technology, which is its pursuit of an open ecosystem. If it were possible to enjoy the benefits of a large ecosystem's user base and liquidity, such as that of the Ethereum network, within the boundaries of regulatory compliance, it would represent an ideal solution.

Source: Kinto

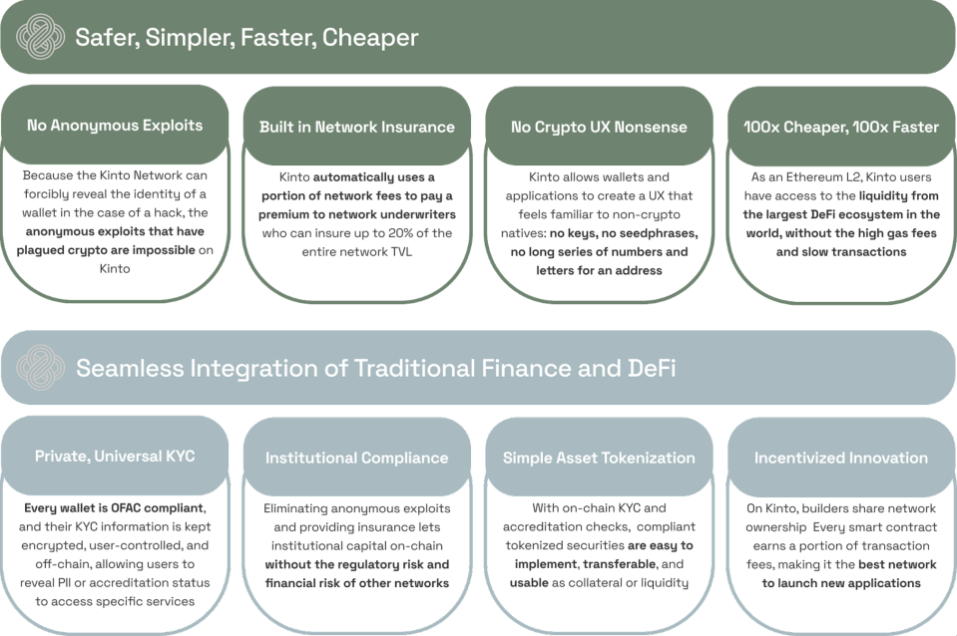

Kinto is an Ethereum Layer 2 solution based on Arbitrum Orbit, notable for mandating KYC for all network participants. This structure minimizes regulatory and financial risks while still capitalizing on the benefits of blockchain and DeFi, and even absorbing the user base and liquidity of the Ethereum ecosystem. It represents the first attempt among blockchain services specialized in the traditional financial industry to establish an open ecosystem instead of an isolated one. To date, Kinto has secured $5M in funding from investors including Kyber Capital, SALT, Spartan, and Parafi.

Kinto distinguishes itself from other networks in several ways:

KYC/AML at the Chain Level: All users and developers must undergo a KYC process before interacting with Kinto, ensuring transactions are safe from scams and hacking.

Data Privacy: Personal KYC data is encrypted and stored securely, not disclosed without the user's consent.

Smart Contracts Wallets Only: The network enforces account abstraction, requiring all users to use the Kinto Wallet. This smart contract wallet offers benefits like non-custodianship, gas fee sponsorship, and key recovery.

Sybil Resistance: Enforced KYC at the chain level provides resistance to Sybil attacks.

Dev Incentive: Developers receive a payback from 10% of sequencer revenue for the applications they build, offering an additional economic incentive.

Insurance Pool: 10% of sequencer revenue is allocated to a Safety Module insurance pool to prepare for potential future incidents.

Kinto is expected to enable various on-chain financial activities previously unfeasible in the blockchain ecosystem. These include trading tokenized ETFs through AMMs like Uniswap or Curve, linking wallets and accounts for payroll use, or managing a company's treasury on-chain, thus leveraging the benefits of on-chain finance within the traditional financial industry.

3.2.1 Modular Blockchain Approach

Kinto employs a modular blockchain architecture to enhance scalability. As an L2 built on Arbitrum Orbit, its execution layer operates similarly to the Arbitrum Nitro Stack. Ethereum serves as the settlement layer, while Celestia is used for data availability (DA). Initially utilizing a single sequencer, Kinto plans to transition to a decentralized sequencer system through a collaboration with Expresso Systems in the future.

3.2.2 KYC Process

Source: Kinto

On the Kinto network, KYC verification is conducted by designated KYC Providers. These providers authenticate user identities and perform ongoing AML/PEP screenings. Users verified by KYC Providers receive a Kinto ID (a soulbound token) in their Kinto Wallet. Applications on Kinto are accessible only to users possessing a Kinto ID.

Despite the necessity of storing personal data due to KYC requirements, user wallet addresses are not stored, ensuring on-chain privacy protection. KYC Providers are curated through governance, with current providers including Plaid, Persona, Stripe Identity, and Parallel Markets.

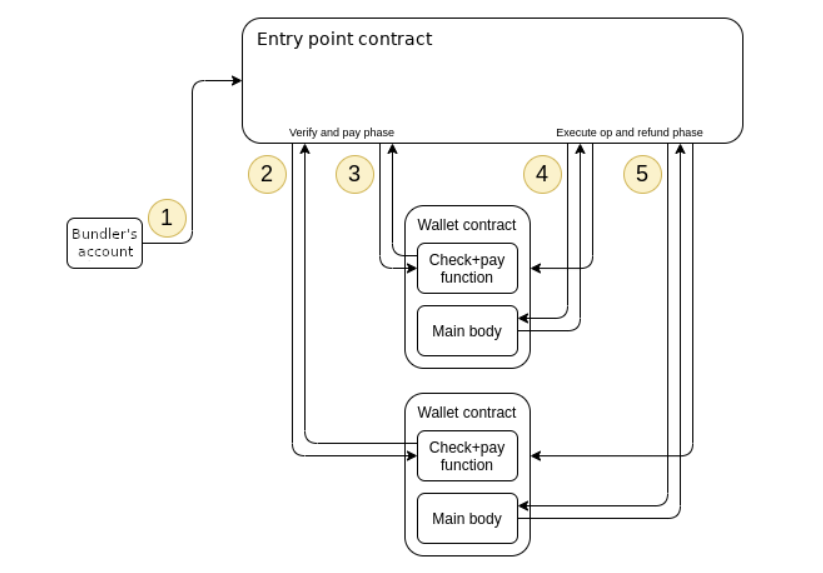

3.2.3 Account Abstraction

Source: Kinto

To improve user experience, Kinto introduces account abstraction based on EIP-4337. All users utilize a non-custodial smart contract wallet (Kinto Wallet), eliminating concerns over losing seed phrases or paying transaction fees. Due to the mandatory KYC on Kinto, slight modifications to EIP-4337 include:

Wallet Factory: A contract that creates and manages Kinto Wallets. Only users who have completed the KYC process can create AA wallets in Kinto.

Entry Point: Checks whether a wallet sending a transaction belongs to the Wallet Factory.

Sponsor Paymaster: In Kinto, end contracts pay gas on behalf of users, removing the need for users to pay transaction fees.

Wallet: A Kinto Wallet requires at least one cloud non-custodial signer (Turnkey) and can have up to three signers.

Kinto has established partnerships with various entities to synergize traditional finance with on-chain finance:

rwa.xyz: Track RWA activities on the Kinto network through rwa.xyz.

backed: Infrastructure for RWA.

collar: Enhances capital efficiency by enabling high LTV loans.

centrifuge: Easy access to Centrifuge's liquidity pools using Kinto ID.

t protocol: Provides short-term US T-bills.

adpat3r: Offers short-term bonds.

truefi: Provides products for institutional investors, such as US bonds.

opdefi: Detects and mitigates risks in on-chain activities.

gas.zip: A tool for multi-chain transactions, with Kinto support planned.

Polytrade: A marketplace showcasing RWA across various networks, including Kinto support.

Larry Fink, CEO of BlackRock, the world's largest asset manager, has stated that the approval of Bitcoin spot ETFs is just the initial step in the technological revolution of finance, with the tokenization of real assets to follow. As blockchain technology begins to address the complex pain points of the financial system one by one, the transition of the financial industry to blockchain will likely accelerate. Blockchain infrastructure prepared for this transition will be essential, with private blockchains expected to dominate in the short term. However, looking at the longer term, there is potential to connect to public blockchain ecosystems that can attract a broader user base and greater liquidity than isolated private blockchain environments. From this perspective, Kinto, an Ethereum L2 network enforcing KYC, represents a noteworthy effort worth paying attention to.

Thanks to Kate for designing the graphics for this article.

Dive into 'Narratives' that will be important in the next year