Circle trades at 44x trailing EBITDA on a business that earns 96% of its revenue from interest rates. The sell-side has a 3x spread on price targets ($60 to $235) which I think reflects category confusion.

Coinbase receives 51% of Circle’s gross revenue under an agreement Circle cannot exit unilaterally. Faster supply growth makes the revenue mix more rate-concentrated, which is the opposite of what a platform re-rating requires.

The products the bull case needs generated 4% of revenue in FY25, guided to 6% in FY26. CPN and Arc look like important strategic defense but defense doesn’t earn a platform multiple.

At $98 as of Mar 26, three things have to happen simultaneously: supply grows, rates hold, and the market grants a VISA/Mastercard tier multiple despite 96% rate concentration.

CRCL dropped roughly 20% to $101 on March 24, its worst day since the NYSE listing. The CLARITY Act draft came out restricting passive yield on stablecoin balances (no interest, no deposit-equivalent rewards, only activity-based incentives survive) and the immediate read was that the USDC growth engine just got legislated away. Same day, Tether announced it had engaged a Big Four firm for its first full financial statement audit, not the quarterly BDO attestations it's been doing, but a real audit of assets, liabilities, and controls. If Tether cleans up transparency, Circle's institutional moat, "we're the one you can actually trust,” gets thinner.

The market split between dip-buyers (Bernstein maintained $190, Cathie Wood bought $16M worth the next morning) and bears. But I think the crash to $101 isn't the mispricing. The 44x trailing EBITDA that existed before the crash was. The stock has since fallen further to $98.

17~20 sell-side analysts cover CRCL, and their price targets range from $60 to $235. That’s a 3x spread on what is functionally a single-product company, and I think the disagreement itself might be the most honest signal in the coverage. Bernstein at $190 is pricing a payments network. H.C. Wainwright at $85 is pricing a rate-sensitive intermediary. Needham cut from $190 to $130 in a matter of months, which means the same team revised its own framework by 30% and still landed on a number implying 50% upside. When I see that kind of dispersion, my instinct isn’t to pick a side, but to ask what’s causing it.

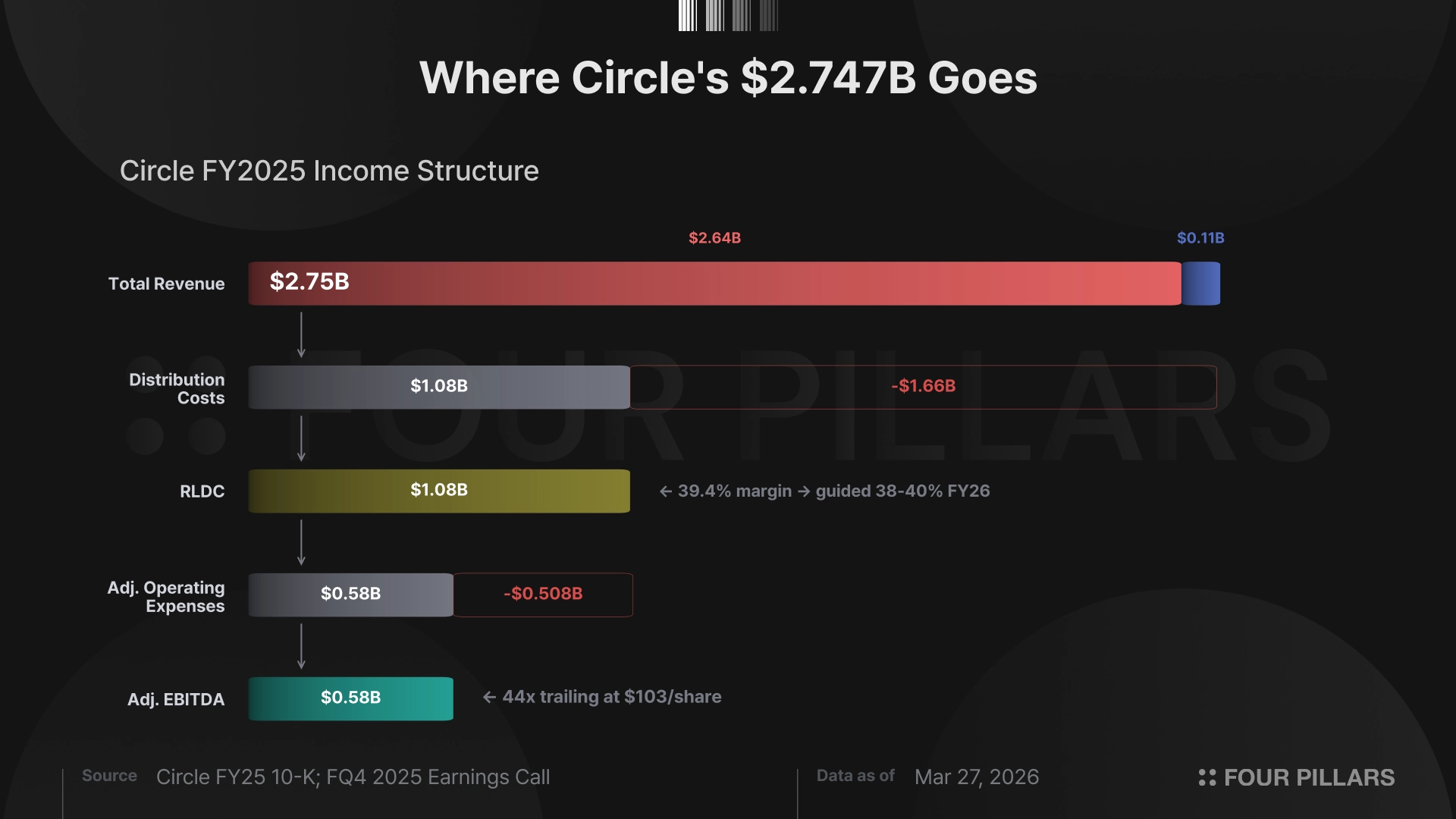

The way I read the 10-K, the answer is pretty clear. Circle generated $2.747B in total revenue in FY25. Of that, $2.637B was reserve income (interest earned on the USDC backing portfolio) which is 96% of the total. Distribution costs consumed $1.664B, or 60.6% of gross, leaving $1.083B in reserve-linked distribution cost (RLDC) at a 39.4% margin. Adjusted EBITDA came in at $582M. GAAP net loss was -$69.5M after $566M in stock-based compensation, $424M of which was a one-time IPO vesting event.

At $98 per share on 248M diluted shares, that puts the market cap around $24.3B and the trailing multiple at roughly 42x adjusted EBITDA. You can build a forward number around $700M if you assume 15% supply growth and flat rates, which gets you to about 35x. But the yield on Circle’s reserve portfolio already fell from 5.0% to 4.1% over FY25, and the forward estimate requires rates to stop declining at exactly the level they’ve been declining through.

The trailing multiple, meanwhile, asks you to believe that a business earning 96% of its revenue from short-duration fixed income deserves a framework designed for platform businesses with operating leverage. RLDC margin was 39.4% and management guided FY26 flat at 38-40%, which doesn’t suggest they expect the cost structure to improve.

The bull’s counter is that Circle has properties a money market fund doesn’t — CCTP, CPN, Arc, agentic payments, regulatory positioning, the USDC network effect. But businesses that aren’t generating meaningful revenue yet are more optionality than a valuation input.

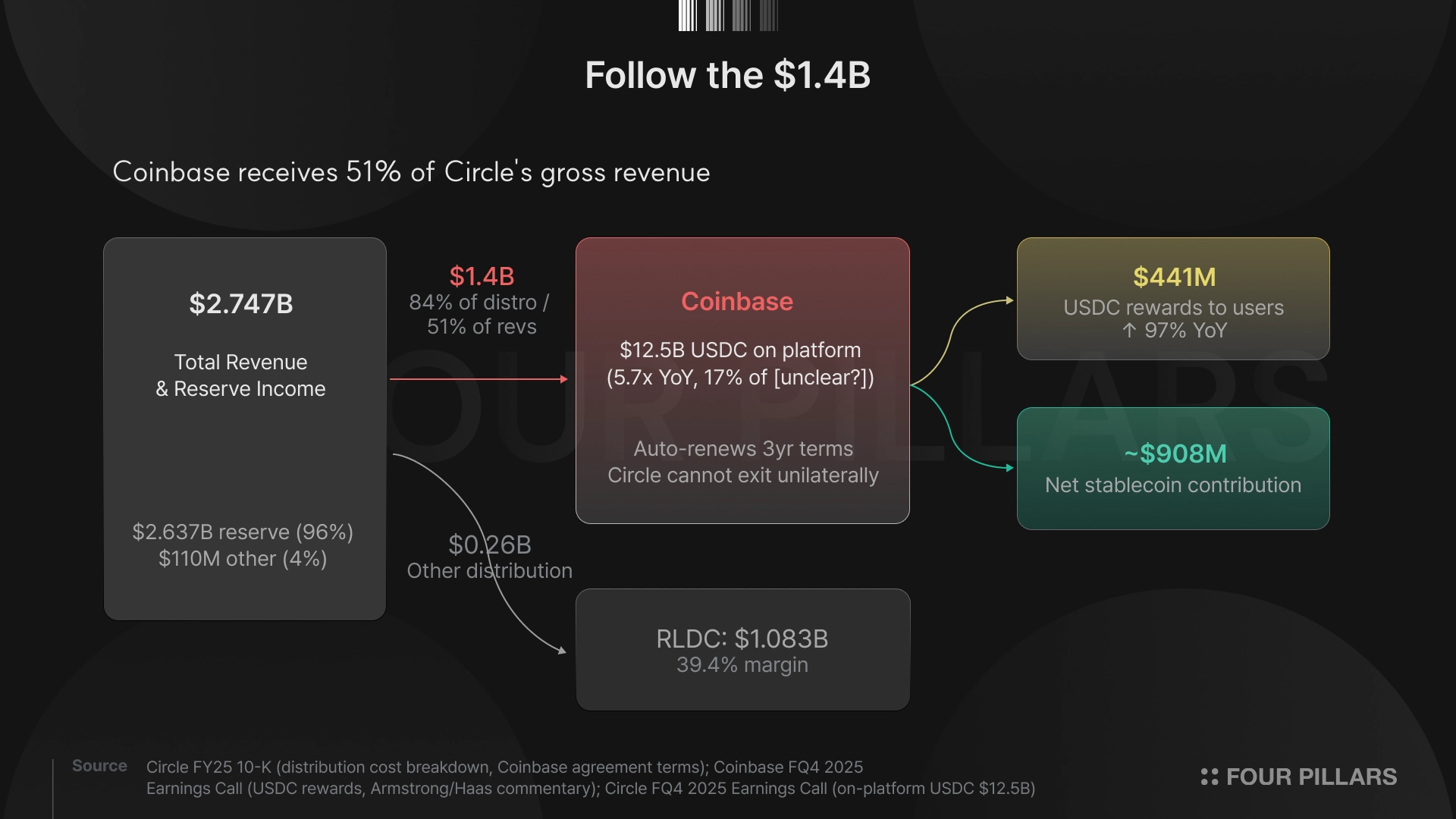

Circle earns reserve income on the USDC backing portfolio. It pays Coinbase roughly $1.4B in distribution costs — 84% of all distribution spend and 51% of gross revenue, up from $924.5M in FY24. Coinbase then voluntarily redistributes $441M of that as USDC rewards to users (up 97% YoY, the single largest contributor to Coinbase’s expense growth). Coinbase keeps the remaining ~$908M as net stablecoin contribution. The agreement auto-renews on 3 year terms, with Circle unable to exit unilaterally if Coinbase meets certain thresholds, and Coinbase receiving a platform share based on USDC held on its platform ($12.5B, up 5.7x from $2.2B) plus 50% of residual payment base.

That 5.7x growth in USDC on Coinbase happened because the partnership guaranteed distribution at scale, and distribution partnerships at this level are expensive precisely. Binance is now paying $60.3M upfront plus monthly incentive fees for a similar arrangement over four years. But growth generated under dependency isn’t quite the same as growth that survives without it, and some of the signals around this relationship are worth sitting with.

Armstrong on his own Q4 call said that if Coinbase were prohibited from paying USDC rewards, it would “ironically just make us more profitable.” Haas was more direct: “We partner with Circle on overall items, but we also compete with them. And our goal is to drive a payments vertical where we create the best place for businesses to come transact in USDC on Base.” Coinbase also took a $395M loss on strategic investments “which includes our investment in Circle” with no analyst follow-up and no mention of Circle’s IPO on its entire Q4 call.

The part I keep coming back to is the re-rating paradox. If USDC supply grows 30% to roughly $100B and rates hold, gross reserve income climbs to approximately $4.1B. Other revenue stays at the guided ~$160M. The rate-dependent share of revenue moves from 96% to 97%.

Supply growth (the thing the bull case needs most) makes the revenue mix more concentrated in rate income, which makes it harder for the market to re-rate Circle away from money market fund comps. Maybe I’m wrong about this, but as far as I can tell, the bull case and the re-rating thesis pull in opposite directions.

The bull case for a platform multiple rests on three products and a narrative.

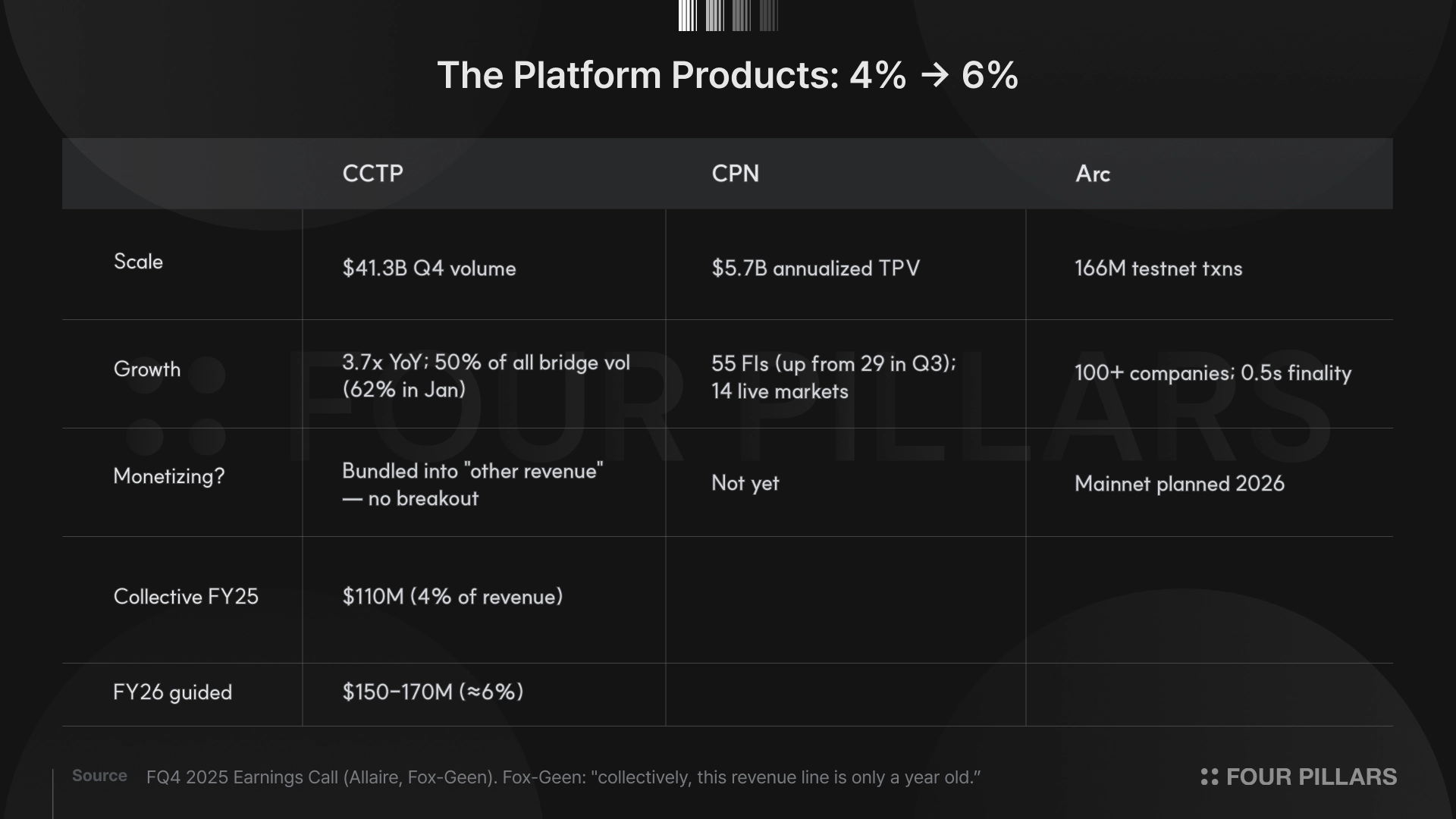

CCTP processed $41.3B in Q4 volume, up 3.7x year-over-year, across 19 chains. Allaire claimed 50% of all bridge volume at Q4 end and 62% in January. But Circle bundles CCTP revenue into “other revenue” without breaking out the contribution.

CPN has 55 institutional participants (up from 29 in Q3) and $5.7B in annualized volume across 14 live markets, and it is not monetizing yet. Allaire’s own framing: “as this starts to get to more meaningful scale, we can start to monetize this.” CPN provides counterparty discovery and compliance orchestration for cross-border USDC payments, which is strategically important work, but the function right now is positioning Circle closer to where usage value concentrates rather than extracting revenue from that position.

Arc is on testnet with 100+ companies and 166M total transactions at 0.5-second finality, with mainnet planned for 2026. What strikes me about Arc is that it gives Circle a settlement surface it controls, which matters because Coinbase is explicitly building a USDC payments vertical on Base. Arc is leverage in that negotiation, not a standalone revenue product, and it’s competing with Base for the same use case.

Collectively, these products generated $110M in FY25, roughly 4% of total revenue. Management guided $150-170M for FY26, or about 6%. Fox-Geen offered fair context on the Q4 call: “collectively, this revenue line is only a year old.” I don’t want to dismiss that. But 4% after a year, guided to only 6%, doesn’t feel like a platform transition. Rather, it feels like important groundwork that hasn’t earned the multiple the market is applying.

Lastly, there’s the AI narrative. Allaire’s dominant talking point on the Q4 call was agentic payments. “99% of agentic payments measured have been in USDC,” Circle Gateway on testnet at $0.001 per transaction, the x402 standard. The structural positioning is that USDC is programmable, compliant, and liquid, and process of elimination probably does land you there for machine-to-machine payments.

But the revenue implication on any timeline this stock price cares about is close to zero. I published an assessment of these products for Four Pillars on January 2026, and even granting every benefit of the doubt, CPN and Arc look like strategic positioning to prevent Circle from being subordinated as value migrates to distribution platforms. That’s valuable and necessary work, but it’s defense, not offense, and defense doesn’t earn a platform multiple.

At 42x trailing and roughly 32x on generous forward estimates, you need USDC supply to keep growing (it's at ~$79B, up 72% YoY, 25% of the $314.6B stablecoin market), you need rates to hold, and you need the market to grant a platform multiple despite 96% rate concentration. All three have to happen together.

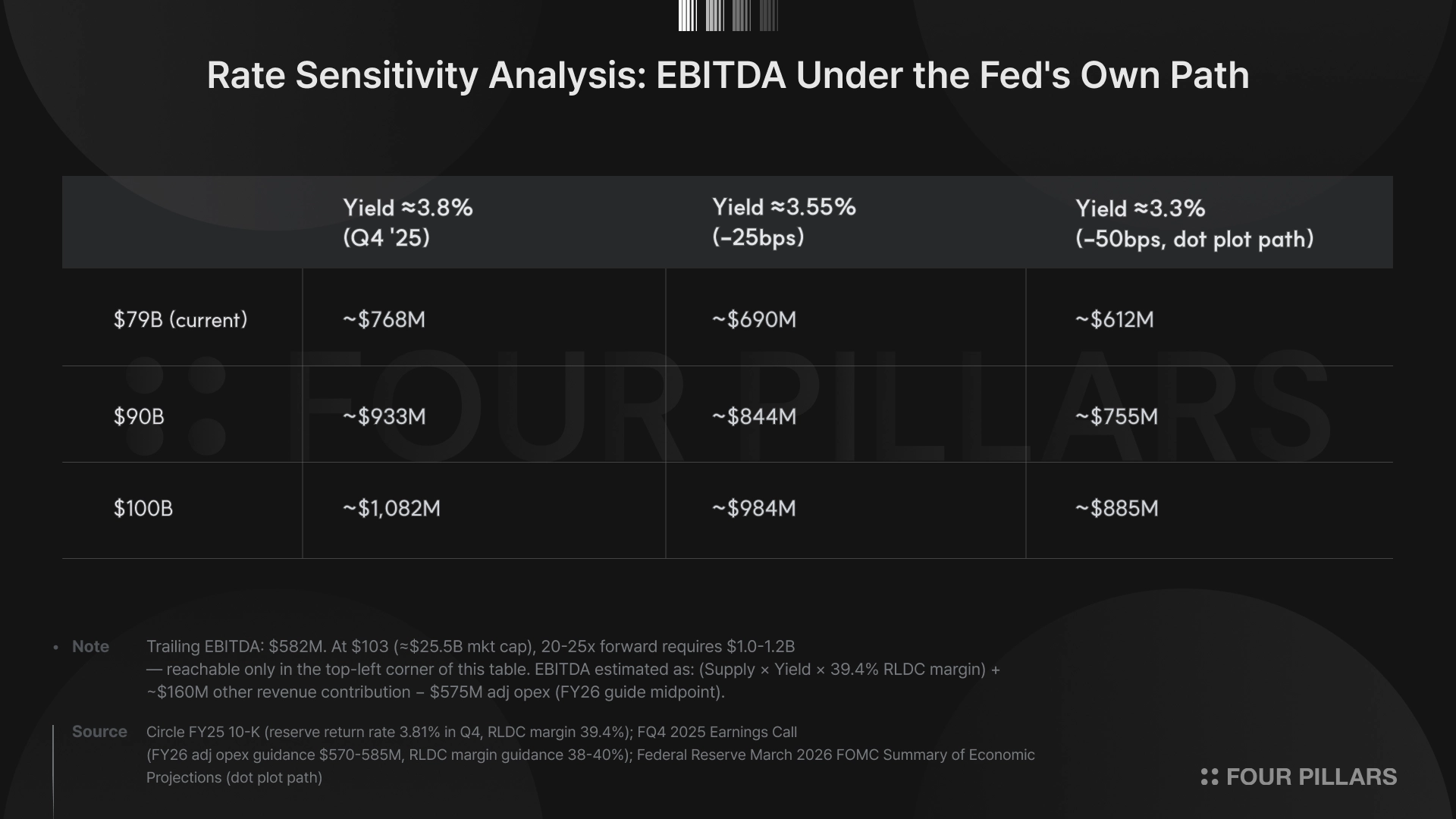

Even in the bull case (supply crosses $100B, rates hold near current levels) EBITDA reaches roughly $1.1B. But $98 per share on that EBITDA still requires a 20-25x multiple, which is payment network territory (Visa, Mastercard). Payment networks operate at 60%+ EBITDA margins with near-zero marginal cost per transaction. Circle has 39.4% RLDC margins guided flat, reserve income that moves with SOFR(Secured Overnight Financing Rate), and a cost structure where growing supply makes the Coinbase share larger, not smaller. The platform analogy requires a cost curve that isn't visible in the filings.

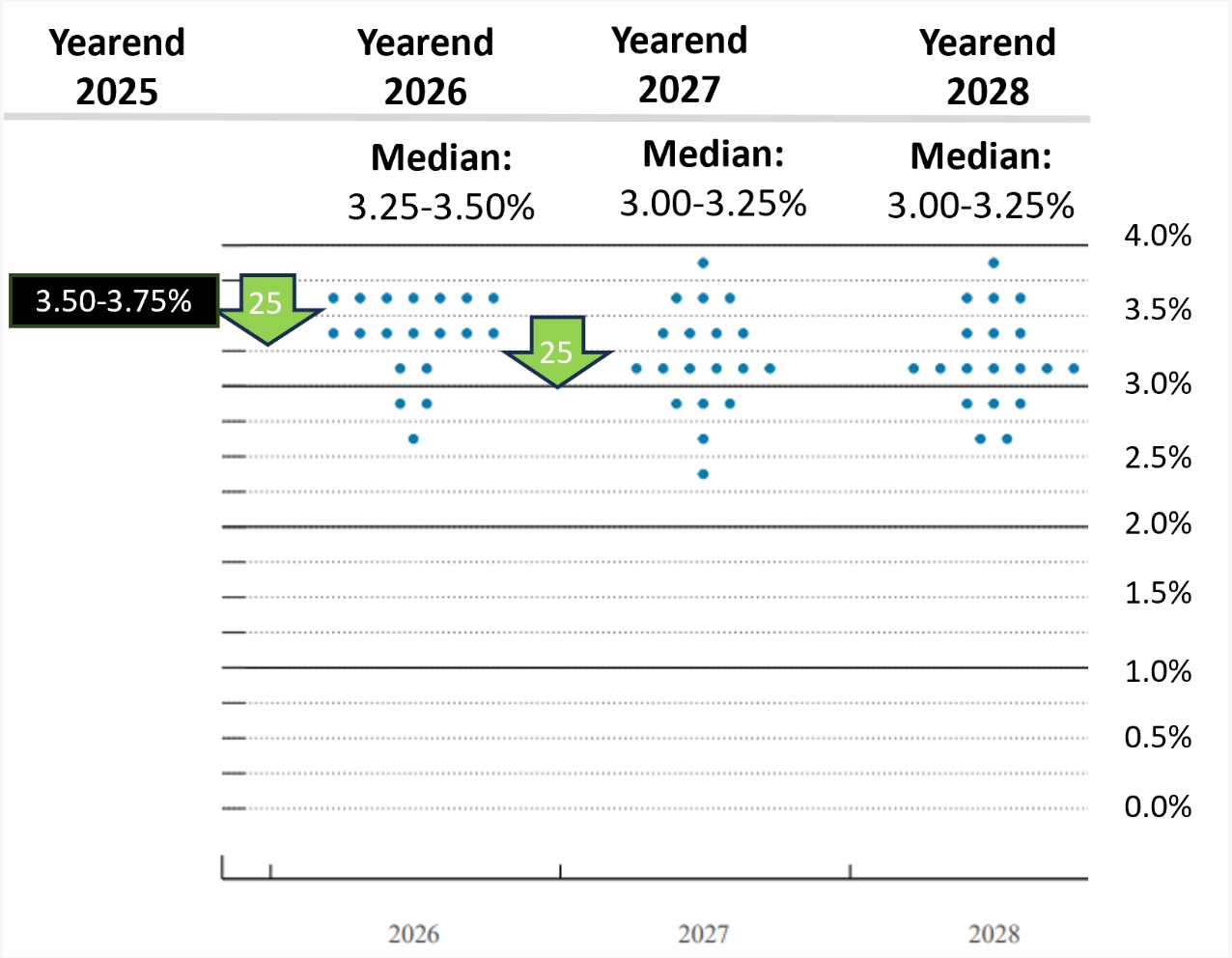

The downside isn't symmetric either, and the base case is already erosive. The fed funds rate sits at 3.50-3.75%, down from 4.25-4.50% when Circle filed its S-1, and the Fed's own dot plot projects another 25bps by year-end and 50bps total through 2027.

On roughly $75B in reserves, 50bps of additional cuts wipes approximately $375M in gross reserve income, which flows through at Circle's 39.4% RLDC margin to roughly $150M in lost contribution, about a quarter of trailing EBITDA. Current supply plus the dot plot path gives you $612M, barely above trailing. The stock doesn't need a rate shock to reprice. It needs rates to merely follow the path the Fed is already telegraphing.

Source: March 18, 2026 FOMC Summary of Economic Projections and Bondsavvy calculations

To steelman the bull on a longer horizon, Fox-Geen guided "40% CAGR over a multiyear through cycle" for USDC. If stablecoins compound at that rate from today's $316B and Circle holds its 25% share, USDC supply reaches roughly $300B by 2030. At a 3.0% reserve yield, the Fed's own longer-run neutral estimate and where the dot plot is already heading, that implies roughly $3.2B in EBITDA, putting today's $98 at about 8x forward. That's cheap. But you're paying 42x trailing today for an outcome four years away that requires sustained hypergrowth, no market share loss to Tether or new entrants, and the Coinbase relationship to not deteriorate.

USDC the product is winning — $79B in supply, 25% market share. I don’t have a bear case on the stablecoin itself. But product winning and equity winning are different questions with different answers, and at $98 the price seems to assume an escape from rate dependency that the product strategy isn’t designed to deliver and the cost structure isn’t configured to allow.

Dive into 'Narratives' that will be important in the next year