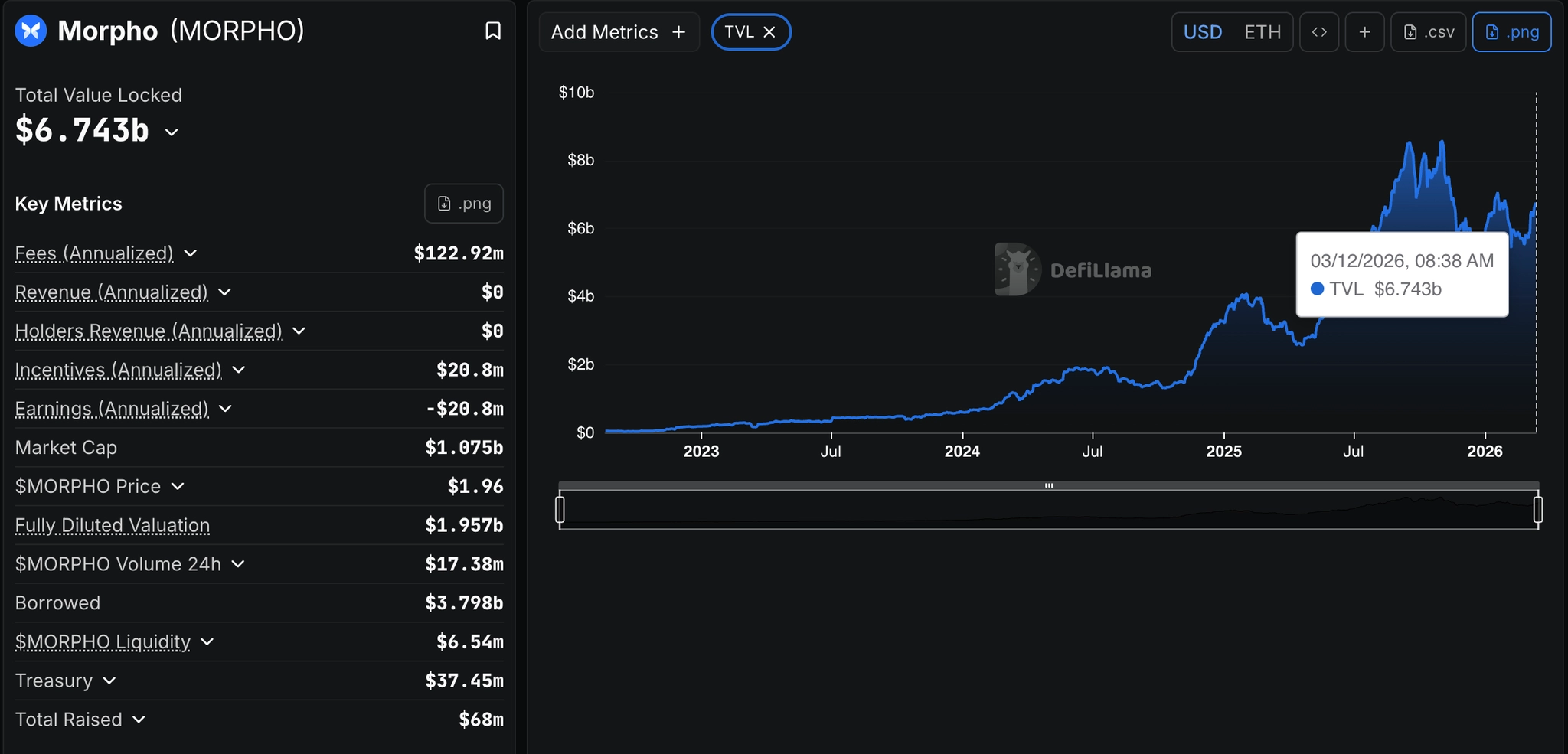

As of Mar 12, MORPHO trades at $1.96B FDV on zero tokenholder revenue, all-time. The fee switch that would change this has never been proposed in 128 Snapshot votes.

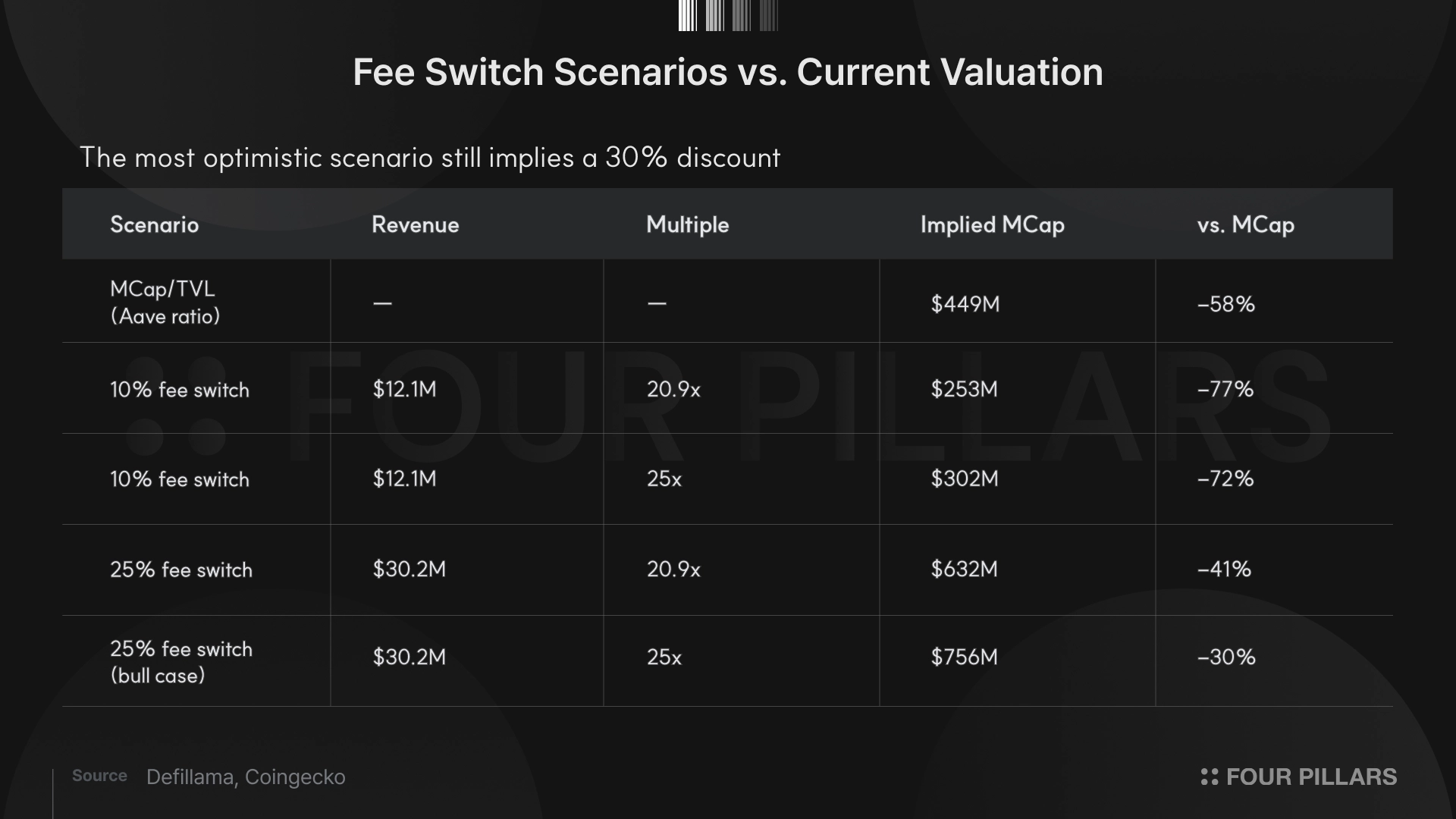

Governance is essentially a four-player game. Stake Capital, Gauntlet, NEMO Ventures, and leuts.eth hold the majority. They have little incentive to turn on the fee switch. Even if they did, the bull case (25% fee, 25x multiple) implies $756M: 30% below where the token trades today.

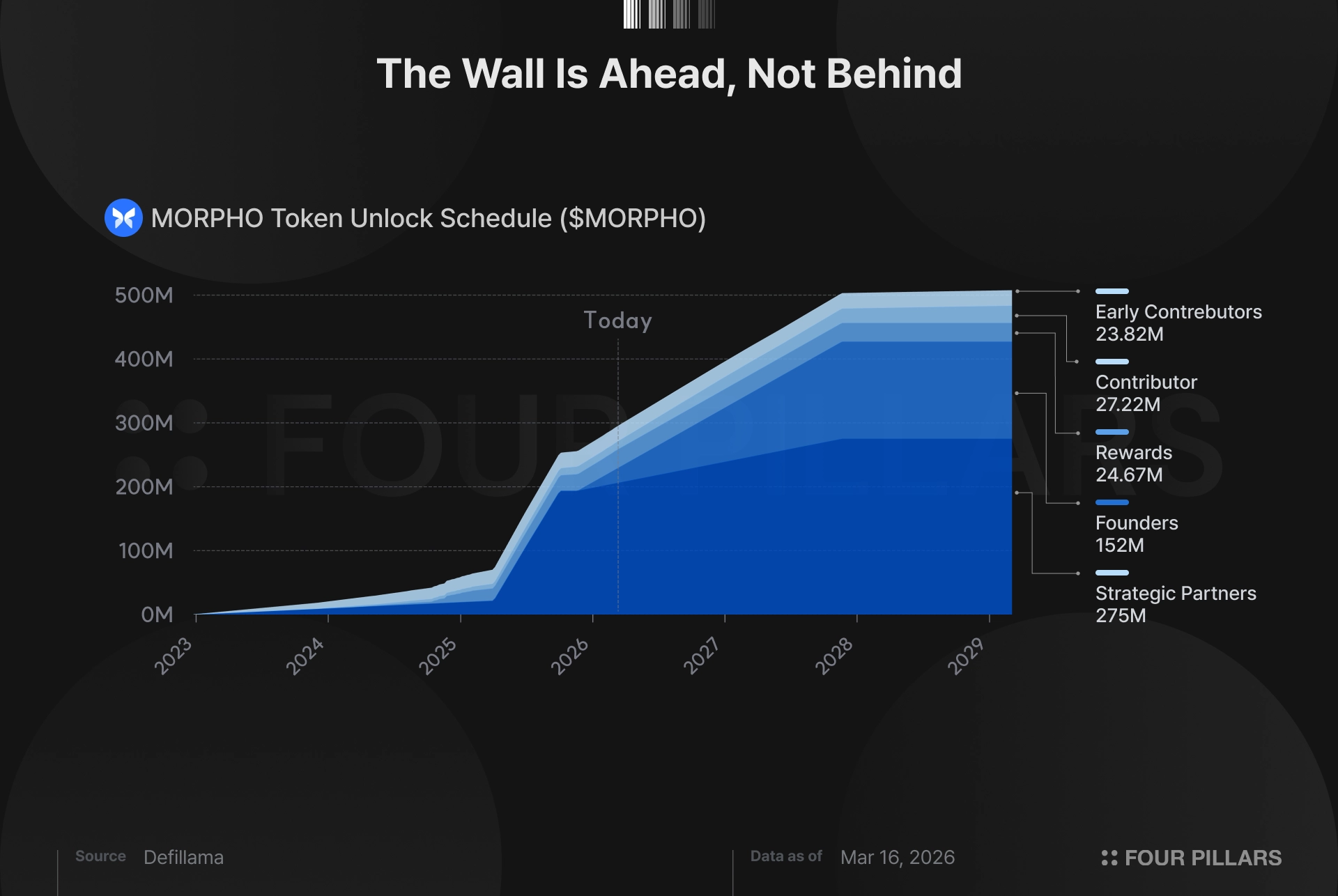

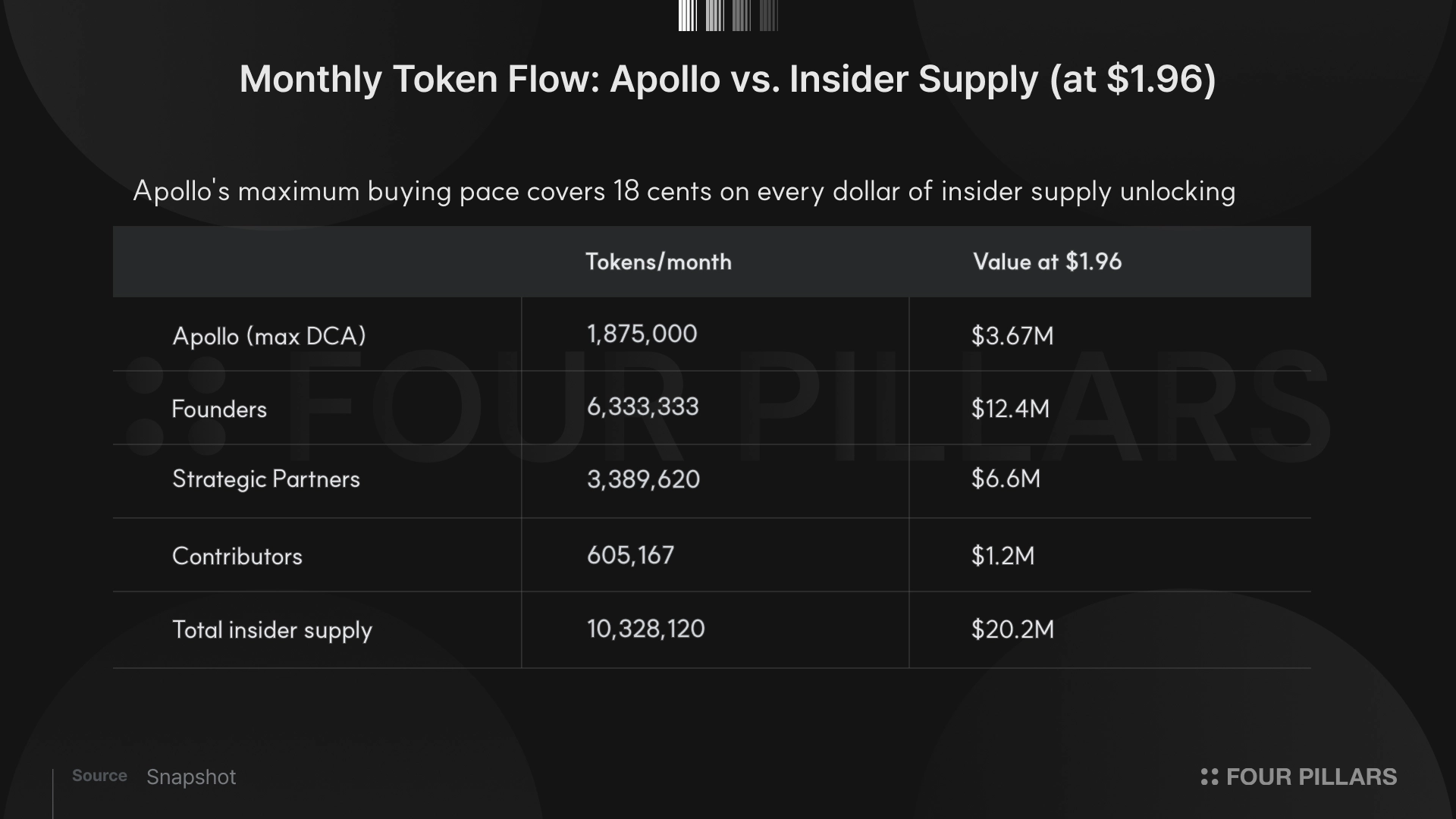

123.9M tokens unlock over the next 12 months, a 22.6% increase in circulating supply (per Coingecko). Apollo covers 18 cents on every dollar of that at maximum pace, and almost certainly via OTC, not open market.

Morpho can be the dominant lending protocol and MORPHO can be a bad token at the same time, because protocol moats and token value accrual are different questions entirely.

The Apollo announcement gave MORPHO holders a 75% pump in a bear market. MORPHO at $1.96 per token gives you a $1.08B market cap and $1.962B fully diluted valuation on a protocol that has generated exactly zero dollars in protocol revenue (+holder revenue) since launch. Not trailing, not annualized. All-time zero.

The protocol runs $6.7B in TVL across 33 chains and processing $10.1M in fees over the past 30 days (~$121M annualized) as of Mar 12, 2026. The fees are real and the lending activity is real, but every dollar of interest generated flows to the vault suppliers and tokenholders takes none of it.

Source: Defillama

Start with the simplest comp. Apply Aave's MCap/TVL ratio (6.63%, from $1.67B market cap against $25.19B TVL) to Morpho's $6.78B TVL and you get an implied market cap of $449M, or $0.82 per token against a $1.96 market price, a 58% discount on a single-metric basis.

Let's walk through the fee switch math. Morpho Blue has a governance-controlled fee parameter (setFee() in the smart contract) that can take up to 25% of interest before it reaches depositors. A 10% fee switch generates $12.1M in annual protocol revenue ($121M annualized interest × 10%). Lending protocols trade at roughly 20-25x protocol revenue; at Aave's current multiple (20.9x, derived from $1.67B market cap against ~$80M annualized revenue) that's $253M implied market cap, stretch to 25x and you reach $302M (as of March 12). Either way, 72-77% below current market cap.

Maximum 25% fee switch produces $30.2M in revenue. At 20.9x, implied market cap is $632M — 41% below market cap. Push to 25x and you reach $756M, still underwater on every combination you can reasonably construct.

Note that these aren't bear-case numbers with punitive assumptions. They're the bull case — maximum revenue extraction at generous multiples.

Ask any bull and you'll hear the same objection — Morpho is early, the fee switch exists, TVL is growing, the protocol will monetize eventually. Reasonable on its face, but the problem with MORPHO isn't the absence of revenue in the system. Revenue already exists, and it routes around tokenholders on every path.

Start with that annualized interest figure. Every dollar flows to vault depositors, the people supplying capital to Morpho's lending markets. That's by design and it's what makes the product competitive, because depositors comparing Morpho, Aave, and Spark are comparing yields. Offering 100% of interest to lenders is how the protocol grew from zero to its current TVL in roughly three years.

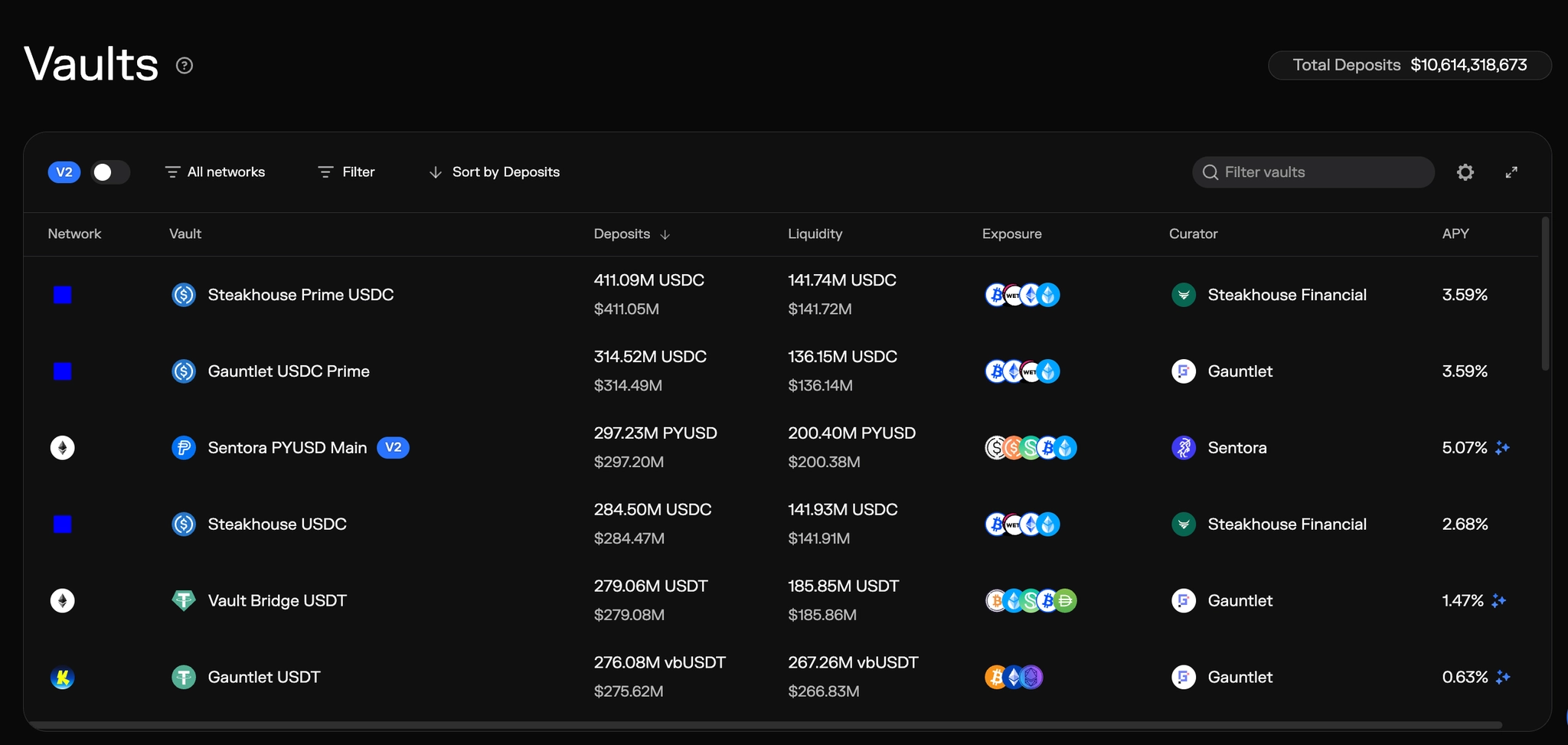

Curators sit on top of this layer. Gauntlet, Steakhouse Financial, Sky, Sentora and others manage vault strategies and earn a performance fee on the yield they generate for depositors. The fee varies by curator. Gauntlet charges 0-5% depending on the vault, Steakhouse ranges from 0% ~ 25%. Assuming an average performance fee of 5-10% across total depositor interest, curators collectively earn roughly $6-12M per year, which is real money for each major curator, but an order of magnitude less than the full interest figure that sometimes gets misattributed to them.

Source: Morpho App

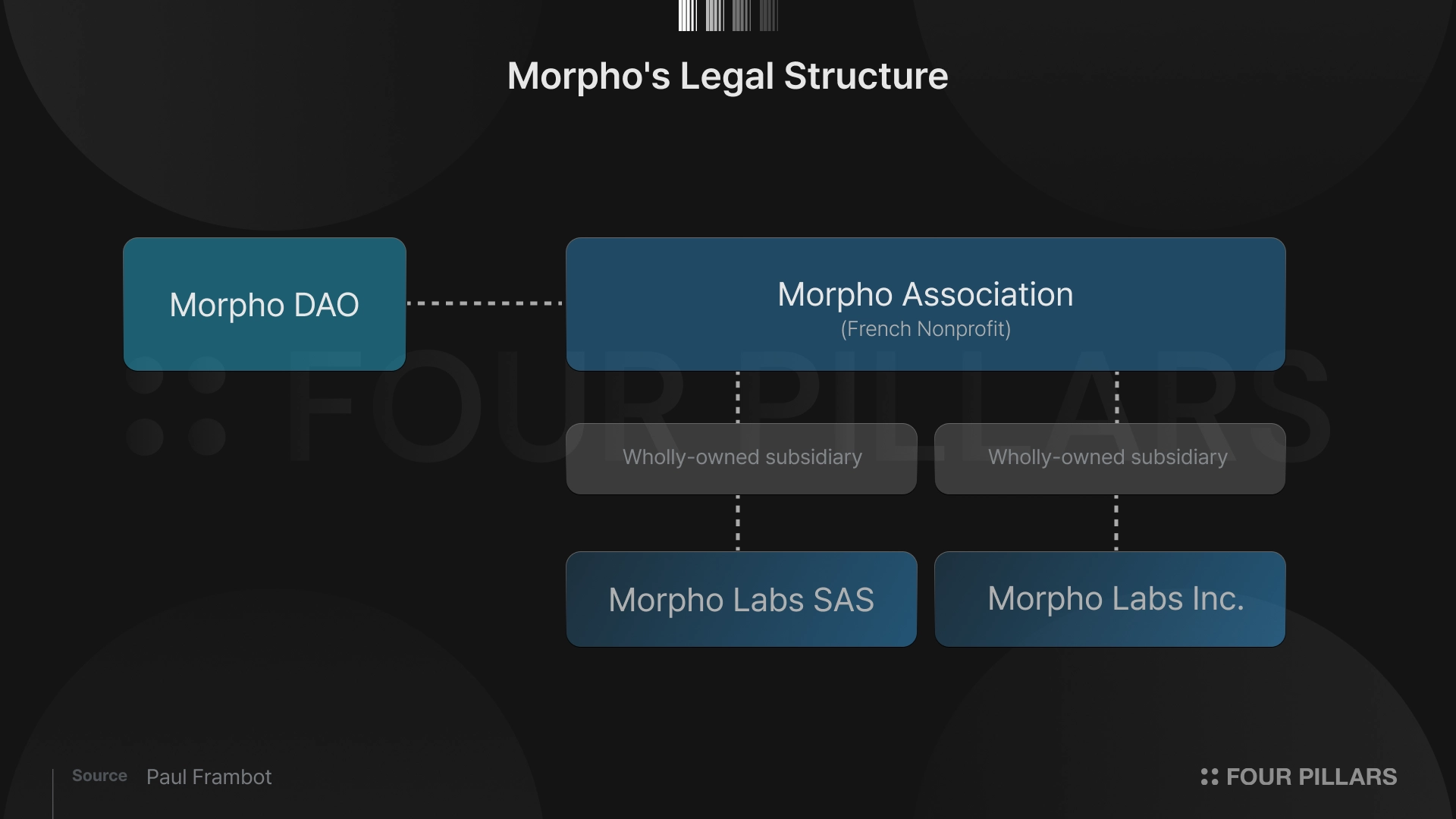

Now consider the Morpho Association, because this is where the cash flow divergence between "Morpho succeeds" and "MORPHO holders benefit" becomes explicit. The Association is a French loi 1901 nonprofit (registration W751263773) that controls Morpho Labs SAS as a wholly owned subsidiary following a June 2025 share transfer — the same leadership directing both entities, with no external equity holder able to challenge either. The share transfer permanently eliminates external equity extraction, which concentrates control in the nonprofit rather than distributing anything to tokenholders.

The Association published a "Mission & Structural Alignment" statement making three claims worth engaging directly:

First, that a nonprofit can't distribute profits to its members, which is legally true but practically meaningless for tokenholders. The Association can spend everything it receives on salaries, contractors, conferences, and "mission-aligned" activities with zero obligation to return value to anyone holding MORPHO. It consumed 195M MORPHO of its initial 200M allocation and then requested another 120M from the DAO reserve in MIP 69 (June 2024), again, without publishing annual reports, budget breakdowns, or any financial disclosures.

Second, that the Labs SAS share transfer "permanently eliminates external equity extraction." It does, but the beneficiary of that elimination is the Association, not tokenholders. Locking out external investors protects the Association's position; it distributes nothing downward.

Third, that "token holders and entities contributing to Morpho share the same incentives." The Berachain deal tells a different story. The Berachain Foundation's original MIP 83 proposal explicitly described "a license fee paid to the Morpho DAO" totaling low seven figures in USDC and BERA, the counterparty themselves proposed DAO payment. The Association then posted MIP 94 to reroute those fees to itself, citing "tax risk for tokenholders in various jurisdictions.” The same proposal noted in passing that the identical issue applies to future fee switch activation, with work "not yet complete." That was February 2025. Multiple community members asked for the actual fee amount before and after the vote. It was never disclosed. For the Apollo cooperation agreement, no governance vote was held at all; the Association executed it directly as counterparty.

The structural result is commercial revenue (performance fees, license deals, institutional partnerships) flowing to curators and the Association. The entities that do the work capture the cash. MORPHO tokenholders fund the development and govern a protocol they don't economically participate in.

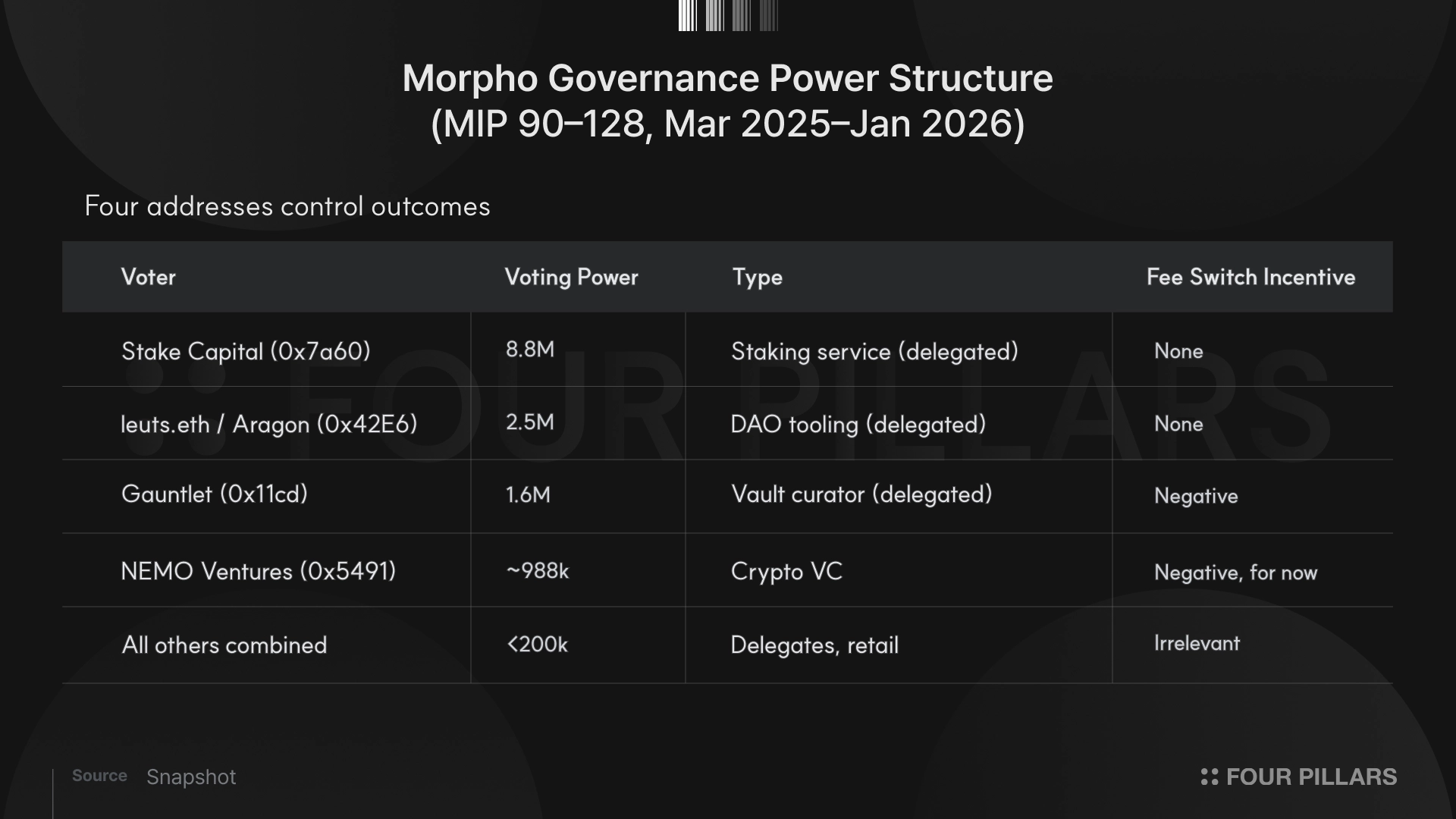

Morpho governance runs on Snapshot executed by a 5/9 multisig with no on-chain governor and no timelock. A separate 4/7 Guardian multisig retains unilateral upgrade authority. The quorum is 500,000 MORPHO, which is 0.05% of total supply or roughly $990K in tokens to pass any proposal.

Source: Snapshot

The participation data across the past twelve months (MIP 90 ~ MIP 128) reveals something more specific than low turnout: a three-tier power structure assembled almost entirely from delegated votes. At the top sits Stake Capital with 8.8M voting power, a staking infrastructure provider that accumulated nearly 10x its prior weight between March and July 2025 as clients delegated MORPHO rather than manage governance themselves. When they participate, they take 73-82% of the vote unilaterally.

Below them, four entities run everything else. leuts.eth (Anthony Leutenegger of Aragon) holds 2.5M voting power. Gauntlet holds 1.6M. NEMO Ventures rounds out the operational core at ~988k, present on nearly every vote. Everyone else (DAOplomats, SEEDGov, PGov, CalBlockchain, boardroomgov.eth) never exceeds 2% combined. The 404 Gov delegate program shut down entirely in January 2026.

MIP 76, which authorized token transferability with obvious personal financial stakes for every holder, drew 141 voters. Voter turnout has been declining steadily since, with the most recent cluster of proposals (MIP 123–128) drawing 8–12 voters each. A November 2025 governance research brief by INCA documented the result: "a single actor with a few millions can secure enough voting power to push through last-minute changes," with the estimated cost to sway critical votes at approximately 2% of treasury assets. Across 128 proposals, no one has ever proposed activating the fee switch.

The silence makes sense. Two of them (leuts.eth and Gauntlet) control outcomes with delegated tokens that aren't theirs. Gauntlet earns millions annually managing $1.2B+ in vault TVL — the fee switch compresses depositor yields, reduces TVL, and directly hits their management revenue. Their abstain on the MORPHO Reward Rate Reduction in January 2025, the one proposal that would benefit token holders at the expense of emissions-fueled growth, was an early tell.

NEMO Ventures is a crypto VC. Fee activation is eventually good for token price but timing matters. Right now MORPHO trades on narrative optionality, and optionality lets the market assign whatever multiple it wants because there's no real number to contradict the story. Activation would make the valuation legible, and legibility is the enemy of the current premium. Turn the switch on and maximum revenue against a $1.96B FDV gives you a 65x multiple, which screams overvalued against Aave's 20.9x and lending protocol averages of 12-20x. The ambiguity of unexercised optionality is worth more to the current price than the reality of the arithmetic.

Stake Capital's business scales with ecosystem activity, not protocol cash flows. They have every incentive to vote for proposals expanding Morpho's reach (their July 2025 appearances were all cross-chain deployments and rewards expansion) and no incentive to compress the yields that attract the deposits their clients stake.

Declining TVL makes the fee switch less attractive exactly when you'd most want it. A shrinking deposit base means less interest to distribute, making the per-holder yield argument weaker at the moment governance pressure would theoretically peak. The rational response to TVL pressure is always more emissions, not less. And even at $6.78B, Morpho is still 3.7x behind Aave's $25.19B. The "growth first" rationale doesn't expire until that gap closes, and the same governance bodies that benefit from the current regime are the ones who decide when the gap is close enough.

Moreoever, the fee switch silence isn't just about curator economics. Morpho's founder has been explicit about it. In a June 2025 post, Paul Frambot stated that the Association "advocates for reinvesting protocol fees rather than distributing them" and that "all revenue should be reinvested back into growth." That's the founder on record stating the fee switch will not be used for distributions.

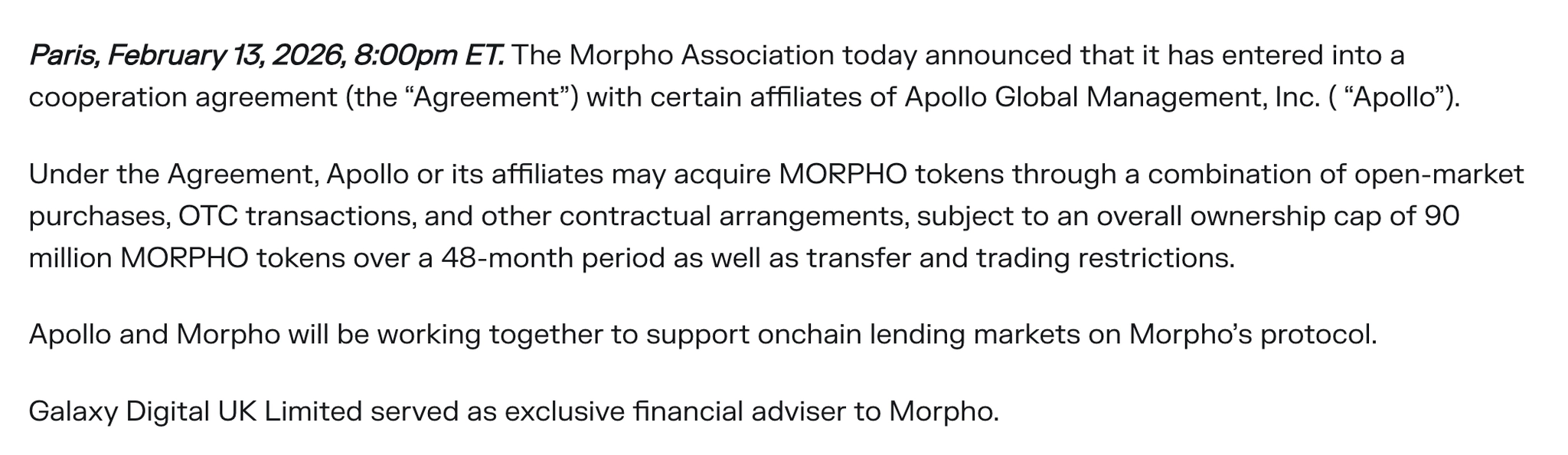

On February 13, the Morpho Association announced that Apollo Global Management had signed a cooperation agreement to acquire up to 90 million MORPHO tokens. The market heard "90 million tokens from a $938B AUM manager" and repriced accordingly — from $1.12 on February 12 to $1.96 by Mar 13, a 75% rally on volume that spiked from a $15M daily baseline to $62M at peak.

Source: Morpho Blog

Read the terms. Up to 90M MORPHO over 48 months through open-market purchases, OTC transactions, and other contractual arrangements, with Galaxy Digital UK as adviser — no disclosed price, no minimum commitment, no on-chain wallet identified. The counterparty is the Morpho Association, not the DAO.

An asset manager with $938B in AUM does not size governance positions through Uniswap. "Other contractual arrangements" almost certainly means direct allocation from the Association — tokens at a negotiated discount. If Apollo is sourcing tokens OTC from the Association's treasury, their purchases provide minimal open-market bid support. The demand floor holders are pricing in likely doesn't exist in the order book at all.

Apollo also isn't buying because they think MORPHO is undervalued. They're buying because 90M tokens is more than enough to control the protocol — at 7.5x to 30x the typical total voting power on any recent proposal, they can set the governance agenda unilaterally. The cooperation agreement's governance restrictions remain undisclosed. This is a control acquisition dressed in institutional credibility.

The supply dynamics matters too. Currently 549.5M tokens are circulating, and over the next 12 months 123.9M additional tokens enter circulation — a 22.6% increase. Founders contribute 76M (6.3M per month on smooth daily linear vesting that started late November 2025, no cliff), strategic partners add 40.7M, and contributors add 7.3M.

There's a useful asymmetry in the unlock profile. Strategic partners are already 75% through their vesting (206M of 275M), so most of that cohort's sell pressure is behind us. Founders are only 15.5% unlocked (23.5M of 152M), which means the wall is ahead, not behind, and concentrated in the single largest allocation.

Let's say Apollo exercises the full 90M over 48 months at maximum pace. That's 1.875M tokens per month ($3.67M at $1.96) against $20.2M per month in insider supply unlocking at the same price. Apollo covers 18 cents on every dollar of insider supply, even at maximum pace, even assuming they're buying in the open market rather than privately. The cooperation agreement provides narrative cover while the founders vest behind it.

None of this is a critique of what Morpho has built. Morpho grew to its current TVL faster than any lending protocol in DeFi history. The permissionless vault architecture produces fast product velocity. The codebase carries years of audit history with zero exploits, which matters when you're asking institutions to trust smart contracts with billions. Apollo, a $938B AUM manager, chose Morpho over every alternative for tokenized credit.

So yes, the moats are real, and they deserve respect. That TVL creates liquidity depth a fork starts at zero trying to replicate. Curator relationships run deep, with billions under management, representing years of trust-building and shared risk management. Integrations across aggregators and protocols create embedded switching costs.

I take all of this seriously, and the protocol is genuinely good at what it does. But every single one of these moats protects the protocol, not the token. TVL depth, curator relationships, audit history all ensure people keep using Morpho Blue. None of them ensure a dollar of that activity reaches MORPHO tokenholders.

The one mechanism that could change this is the fee switch, and the permissionless design that attracted that TVL is the same design that makes pulling it dangerous. Activating the fee switch compresses depositor returns, and depositors move to better yields. Curators can fork the GPL code (live since January 1, 2026) and deploy identical markets without the protocol-level fee. Gauntlet has its own brand, its own risk models, its own depositor relationships. The curator relationships that constitute Morpho's moat belong to the curators, and pulling the switch risks triggering the defection that dissolves it.

Protocol moats and token value accrual are different questions with different answers.

The February 2026 numbers make the protocol's trajectory hard to dispute. Coinbase loans powered by Morpho have crossed $2B originated. Anchorage Digital, Taurus, and Ledger Enterprise are embedding Morpho access for institutional custody clients. Bitwise, Sky, and SG Forge have joined the curator ecosystem. RWA.xyz is calling Morpho the prime brokerage layer of onchain finance.

The question this report asks is narrower: does the current valuation reflect what MORPHO tokenholders actually own today? The live variable is Morpho Markets V2 — the architectural shift that externalizes rate pricing entirely, letting markets rather than the protocol set rates, and potentially opening monetization structures the current design forecloses.

Morpho Vaults V2 shipped in September 2025. Markets V2 remains the team's core execution priority for 2026 and has not yet launched.

Dive into 'Narratives' that will be important in the next year