If Hyperliquid wins, KNTQ wins more. Same macro thesis, 142x smaller market cap, with operating leverage that amplifies every dollar of HYPE appreciation.

sKNTQ yields 7-8% from actual protocol revenue. I'm using conservative assumptions that have meaningful upside baked in.

Equity perps are coming, Hyperliquid via HIP-3 is positioned to capture them, and KNTQ is currently the only liquid way to express that specific bet.

The market prices Kinetiq as an LST. I think it's HIP-3 infrastructure disguised as an LST, becoming the coordination layer for permissionless market deployment.

Path to $2B FDV (~17x): HYPE 5x, Markets at $1B/day, buyback % normalizes—$71M annual buybacks at 30x P/E.

I'm long KNTQ.

If Hyperliquid wins, KNTQ wins more. That's the entire thesis. Everything else in this paper supports that sentence.

Here's the thing. Most people expressing a Hyperliquid conviction just buy HYPE, and that makes sense. $6.4B market cap, $20.5B fully diluted, direct exposure to the highest-revenue L1 in crypto. Clean trade. I own HYPE too.

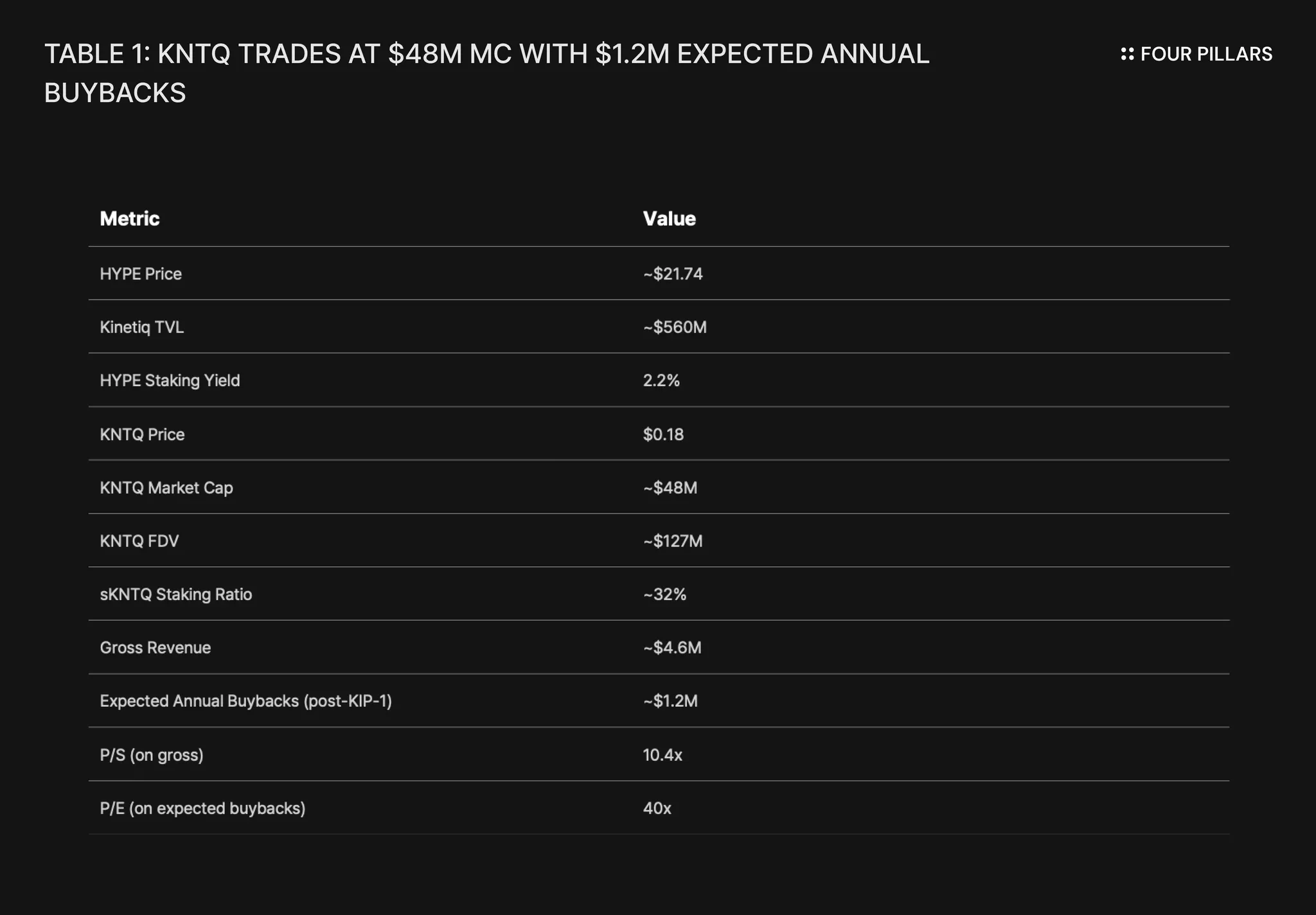

But I'm also taking a different position. KNTQ is sitting at $45M market cap (as of Jan 22 2026), $168M fully diluted, which makes it 142x smaller than HYPE. Same macro thesis, 142x cheaper.

Market cap leverage isn't the insight though. Anyone can do that math. The insight is that KNTQ isn't just a levered HYPE bet, it's the only liquid way to bet on HIP-3 specifically. On equity perps specifically. On the part of Hyperliquid's vision that I think gets wildly underpriced.

Let me be specific. HYPE is a bet on everything Hyperliquid does. The perps DEX, the L1, HyperEVM, the ecosystem broadly. When you buy HYPE, you're saying "this chain wins." Fine thesis. I agree with it.

But KNTQ is a concentrated bet on one mechanism. HIP-3 is the permissionless market deployment system that lets anyone launch a perpetual exchange for any asset, and Kinetiq is building the infrastructure layer for it. They own 46% of the liquid staking market. They run Markets.xyz, a live HIP-3 exchange that's already processing real volume. They're building Launch, which is infrastructure for teams deploying new HIP-3 markets without needing $17M+ in HYPE stake. Every product touches the same thesis: as HIP-3 scales, Kinetiq scales faster.

The setup is asymmetric in a way I find hard to ignore. Downside is correlated, because if Hyperliquid fails then KNTQ fails and I'm not pretending otherwise. But upside is amplified through a value accrual mechanism that actually works. Every revenue stream, whether from LST fees, Markets exchange, Launch infrastructure, or validator commissions, flows into KNTQ buybacks and gets distributed to sKNTQ stakers. And here's what closes the loop: to mint kmHYPE and use the Markets exchange, you need to stake KNTQ first. Product adoption creates direct token demand. Add operating leverage from TVL scaling with HYPE price, plus Launch optionality that isn't priced yet because it hasn't shipped.

This paper argues three things. First, that equity perps are the next trillion-dollar market for onchain derivatives. Second, that Hyperliquid via HIP-3 is positioned to capture it. And third, that KNTQ is the sharpest instrument to express this view.

If I'm wrong about equity perps, I lose. If I'm right about equity perps but wrong about Hyperliquid, I lose. If I'm right about both but Kinetiq loses market share, I still probably lose.

That's a lot of ways to be wrong. I'm long anyway.

The history of retail speculation is a story of leverage getting easier to access. First it was margin accounts, then options, then crypto perps. Each step removed friction and the market expanded. We're about to see the next step, and most people aren't paying attention to what it means.

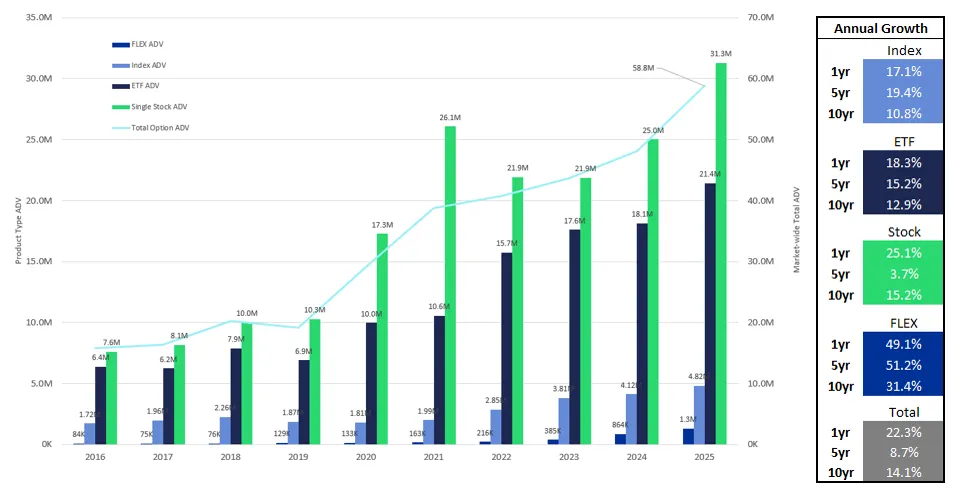

Start with what's already happened. Zero-day options on equities exploded over the past two years. 0DTE volume on SPX now accounts for over 60% of total options activity, up from essentially zero before CBOE introduced daily expirations in 2022. Retail traders discovered they could express a directional bet on the S&P with defined risk and massive leverage, and they couldn't get enough of it. The demand was always there. The product just finally matched it.

Source: CBOE

But options are complicated. You need to understand Greeks, manage time decay, think about implied volatility, and decide between strikes and expirations. Most retail traders don't actually want that complexity. What they want is something much more simple, which is leveraged exposure to price movement without getting liquidated on a wick. They want to go long or short with size, collect funding when they're right, and not think about theta bleeding their position while they sleep.

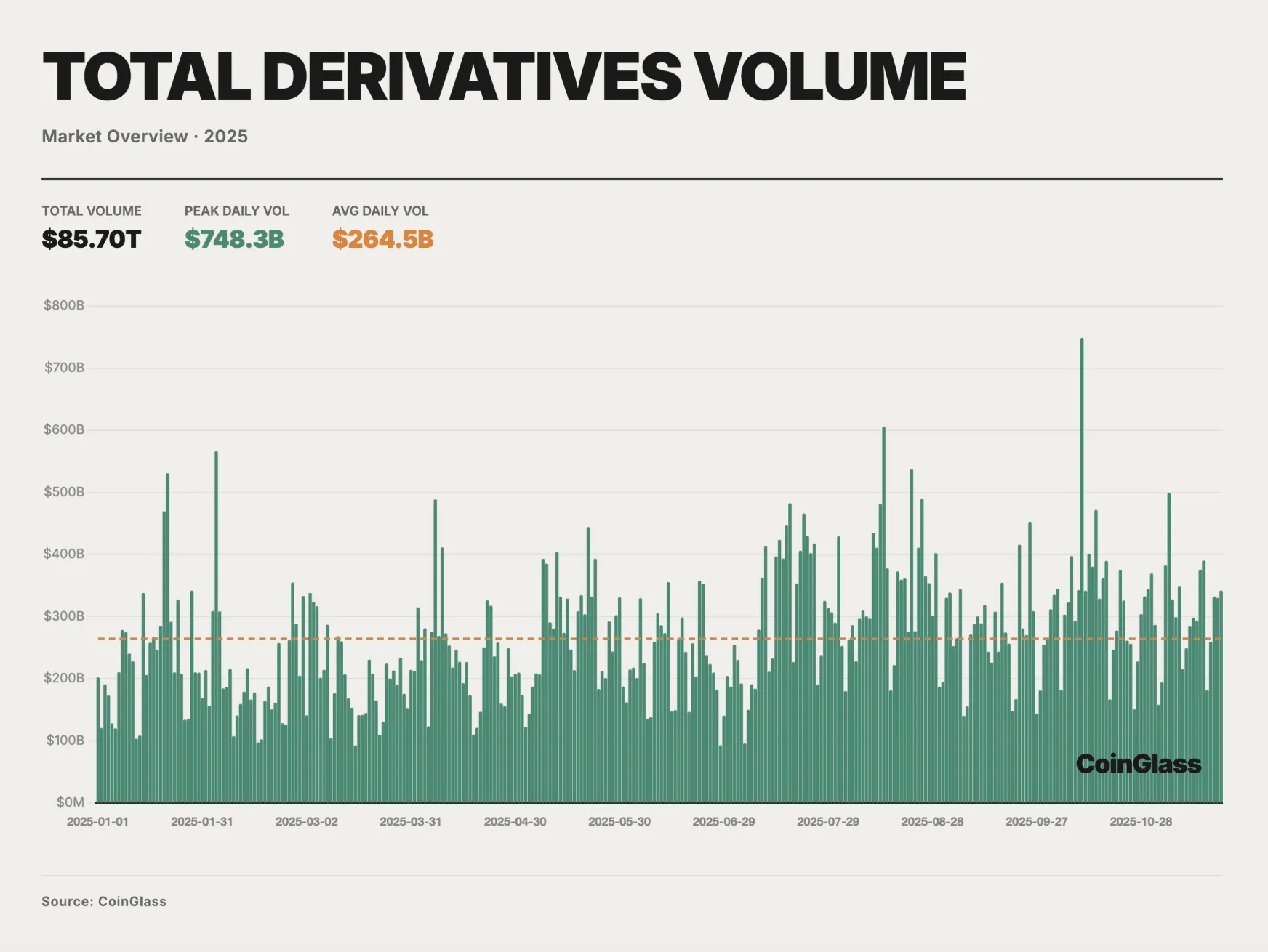

Perps are that product. No expiry, no Greeks, no strike selection. Just pick your direction and your leverage. Crypto proved the demand exists at scale. Binance, Bybit, and now Hyperliquid process hundreds of billions in daily perp volume because the product fits how retail actually wants to trade. In 2025, total crypto derivatives volume hit $85.7 trillion, with daily turnover averaging $264 billion.

Source: Coinglass

So the question isn't whether perps work, but rather what assets they'll expand to cover.

Equity perps are the obvious next market. The 0DTE explosion already proved that retail wants leveraged equity exposure, but right now their only options are complex derivatives or margin accounts with pattern day trading rules and minimum balance requirements. A 22-year-old in Lagos or Jakarta or São Paulo can't access US options markets, but they want exposure to Tesla and Nvidia and the S&P just as much as someone in New York does. Maybe more, because the asymmetry matters more when you're starting with less.

Permissionless equity perps solve this. No KYC, no minimum balance, no PDT rules, no market hours. Just a wallet and a position. The infrastructure is already being built.

NYSE announced they're exploring 24-hour trading for US equities. Robinhood is pushing for extended hours. The traditional system is moving toward what crypto already has, which tells you something about where demand is pulling.

But here's the distinction that matters. Permissioned 24-hour equity trading serves American retail who already have brokerage accounts. Permissionless equity perps serve the other 7 billion people who don't. These aren't competing for the same users. They're expanding into different segments of the same underlying demand.

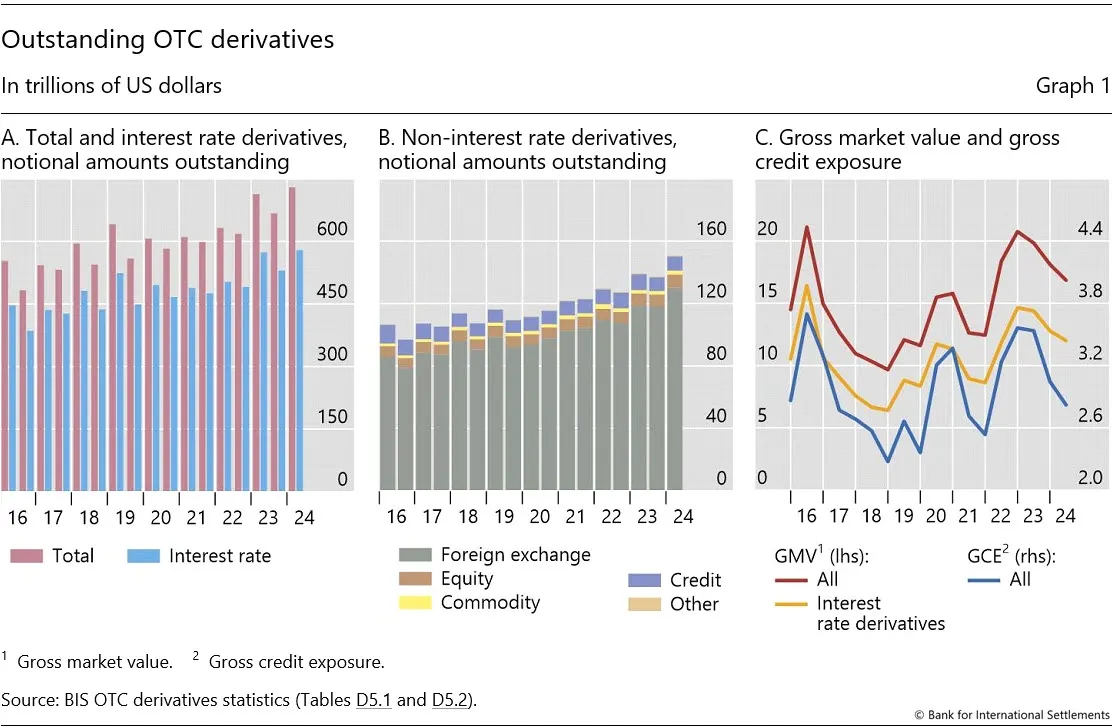

The TAM framing most people use for equity perps is wrong. They compare it to crypto perp volume and ask whether it can get that big. That's thinking too small. The right comparison is global derivatives notional value, which sits at nearly $700 trillion. Crypto perps proved the product works. Equity perps apply it to a market that's orders of magnitude larger.

Source: BIS

Hyperliquid is positioned to capture this because of HIP-3. The permissionless market deployment system means anyone can launch a perp market for any asset, whether that's Tesla stock, gold, a volatility index, or something nobody's thought of yet. The infrastructure doesn't care what the underlying is. It just provides the venue.

This is the macro thesis Kinetiq rides on. Not "LSTs are valuable" or "Hyperliquid has good UX," but something more fundamental: equity perps are coming, Hyperliquid will be the primary venue, and Kinetiq is building the infrastructure layer that makes it work.

If I'm wrong about equity perps becoming a massive market, the thesis falls apart. But every signal I can find, from 0DTE growth to NYSE announcements to global retail demand for leverage, points in the same direction.

If equity perps are the next trillion-dollar market, which venue captures it?

Hyperliquid was purpose-built for this. HyperCore is a deterministic execution environment built specifically for trading, where orderbooks, margin accounts, liquidation logic, and oracle pricing all live at the same layer. For a trading venue operating at scale, correctness, solvency, and latency matter more than general programmability. HyperEVM runs alongside it for permissionless smart contract deployment, but the core trading infrastructure is what makes Hyperliquid structurally different.

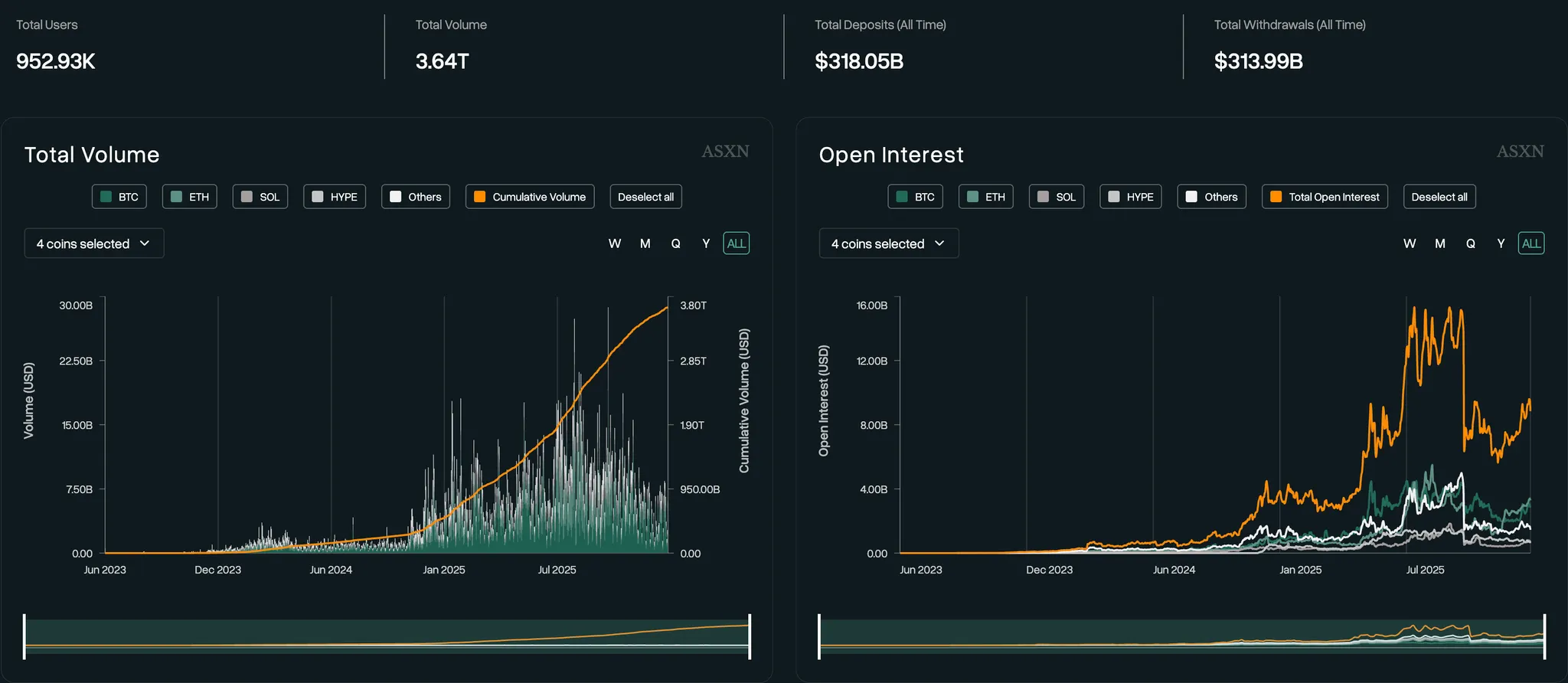

The numbers speak for themselves. Hyperliquid has processed $3.6 trillion in cumulative volume across nearly 1m users. Current open interest sits at $9 billion. In the last 30 days alone, perp volume hit $156 billion, putting Hyperliquid at #1 among all perp DEXs by a wide margin. More telling is the comparison against centralized exchanges: Hyperliquid now commands roughly 5% of global perp market share including CEXs, running at about 35% of Bybit's volume and 11% of Binance's. An onchain venue competing at that scale against the largest centralized exchanges in the world is unprecedented.

Source: ASXN

But what makes the economics unusual is the margin structure. 99% of perp fees flow to the Assistance Fund for HYPE buybacks and burn. That's not a typo. In traditional finance, exchanges keep the vast majority of trading fees as profit. Hyperliquid routes nearly all of it back to token holders. The result: $54 million in holder revenue over the past 30 days, $13.78 million in the past week, ranking #1 across all protocols by this metric.

Then there's HIP-3. Permissionless market deployment means anyone can launch a perpetual exchange for any asset. The infrastructure doesn't care what the underlying is. For decades, the scarce resource in market structure was infrastructure: who could build the matching engine, the risk systems, the liquidation logic. HIP-3 commoditizes that. The scarce resource becomes rallying capital and demand around a market worth trading.

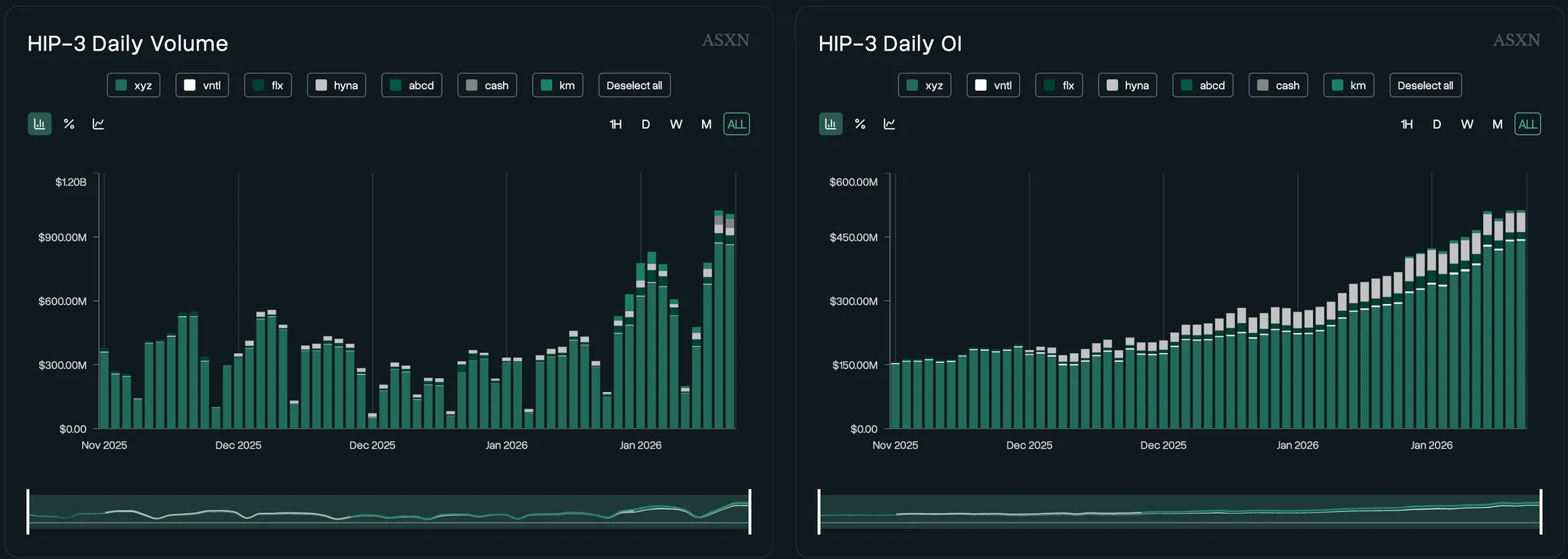

HIP-3 markets have already processed $226 billion in cumulative volume with $512 million in open interest. On January 22nd alone, daily volume crossed $1 billion. The markets are live: XYZ100 leading with $120M OI and $351M daily volume, silver at $79M OI, gold at $56M OI, and a growing roster of equity perps including TSLA, NVDA, GOOGL, INTC, and PLTR. The thesis is being tested in production right now.

Source: ASXN

This creates a flywheel. More markets mean more volume. More volume means more fees. More fees mean more buybacks, which support HYPE. Higher HYPE attracts more builders and capital, which leads to more markets. The cycle compounds.

The question for this paper isn't whether Hyperliquid wins. I think it probably does, and if you disagree you should stop reading here because everything else depends on that assumption. The question is how to express that view with the sharpest risk-reward.

If Hyperliquid wins, staked HYPE becomes the most structurally demanded asset in the ecosystem. This isn't about yield farming or speculative staking, but rather about multiple compounding forces that all pull HYPE supply in the same direction.

Start with native staking. Currently 434.8 million HYPE is staked across +38 validators, representing 43.5% of total supply locked for network security at roughly 2.2% APY. That's the baseline.

Then there's the Assistance Fund. Remember that 99% fee capture mentioned earlier? The Assistance Fund currently holds 39.2 million HYPE worth $852 million, and it keeps growing with every trade on the platform. It's a perpetual buyback machine funded by real trading activity.

HIP-3 adds another layer of structural demand. Deploying a new perp market requires staking a minimum of 500,000 HYPE, which at current prices means north of $17 million just to launch. Every new HIP-3 market that goes live locks more HYPE into the system. It’s a functional stake that the network requires to operate. Scale that to 100 new markets and you're looking at 50-75 million additional HYPE locked into infrastructure.

Then there's the DATs. Hyperion DeFi (NASDAQ: HYPD) holds roughly 1.7 million HYPE and operates as a yield-generating business through staking, validator commissions, and DeFi monetization. Hyperliquid Strategies Inc. is merging onto NASDAQ with initial contributions of 12.6 million HYPE plus $305 million in cash, backed by Paradigm, Galaxy, Pantera, and D1 Capital. HSI has filed to raise up to $1 billion more for additional HYPE accumulation.

Together, these two DATs already anchor roughly 6% of circulating supply in long-duration, institutional ownership. And they're just the beginning. The structural logic is that HYPE has limited CEX availability, so institutions that want exposure need compliant vehicles. DATs provide that access while simultaneously removing supply from circulation.

Add it up. Native staking takes 43.5%. The Assistance Fund holds another 39 million and growing. HIP-3 deployment will lock tens of millions more as markets scale. DATs are accumulating with institutional capital and have barely started. DeFi on HyperEVM needs liquid staked HYPE as collateral, creating yet another demand sink.

This is a supply squeeze that compounds as the ecosystem grows. Every new HIP-3 market needs stake. Every new DeFi protocol needs collateral. Every yield-seeking user needs liquid staking. Every institution that wants exposure needs a DAT wrapper. The more Hyperliquid succeeds, the more pressure there is on available supply. And unlike speculative demand that comes and goes with sentiment, this is structural demand baked into how the system functions.

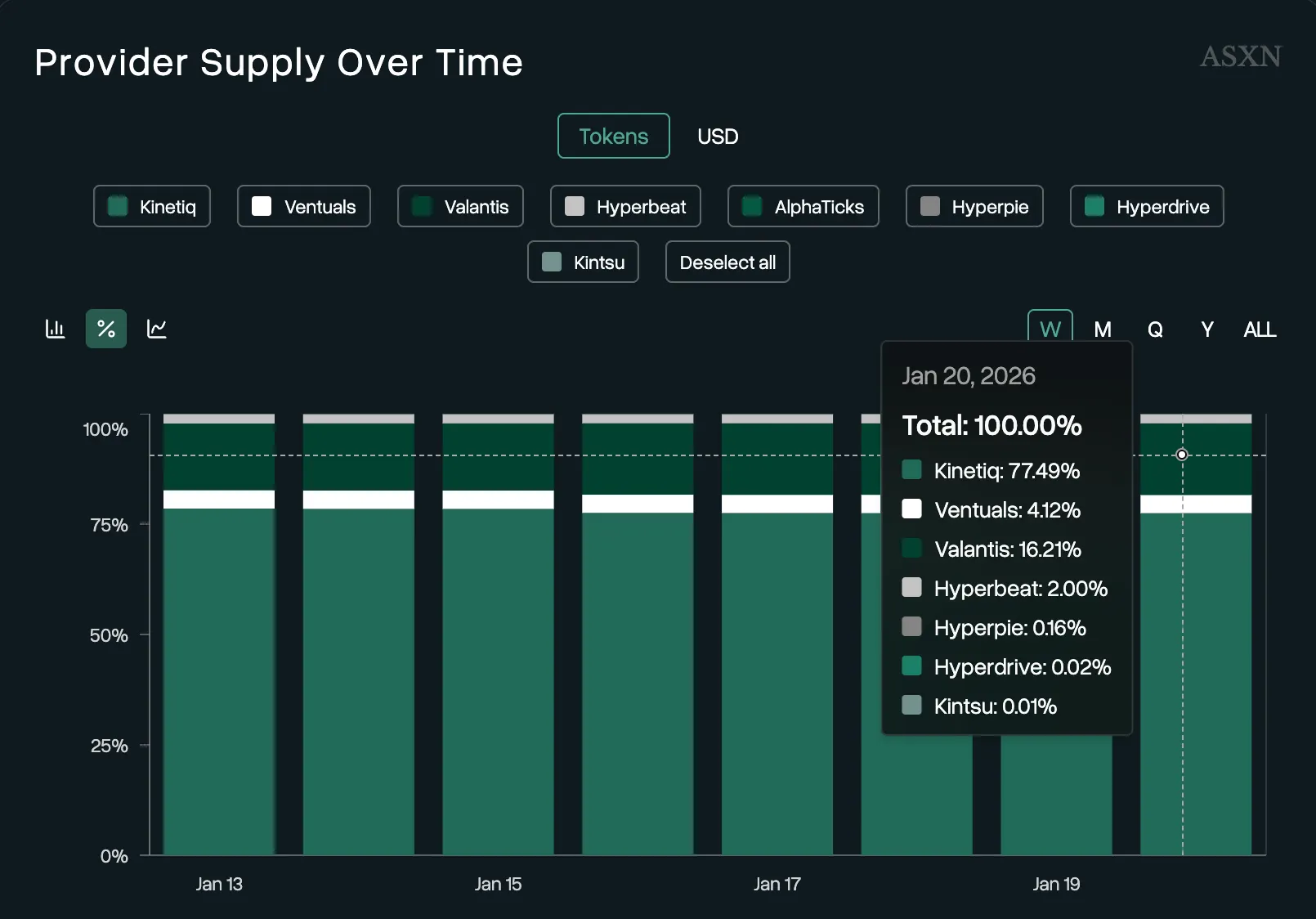

Kinetiq controls 77% of the liquid staking market.

Source: ASXN

This is the part most people miss when they look at Kinetiq as "just an LST protocol." The position isn't about market share in a commodity service. Instead, it’s about controlling the coordination layer for how staked HYPE gets deployed across an ecosystem with compounding structural demand.

If you believe Hyperliquid wins, you can buy HYPE. That's the obvious trade. But KNTQ is a different instrument. It's a concentrated bet on one specific mechanism: HIP-3 and the infrastructure layer that makes permissionless market deployment possible. Kinetiq owns 77% of the liquid staking market. They run Markets.xyz, a live HIP-3 exchange already processing real volume. They're building Launch, which is infrastructure for teams deploying new HIP-3 markets. Every product touches the same thesis, and the thesis is simple: as HIP-3 scales, Kinetiq scales faster.

There's no equity perps index. No HIP-3 ETF. No other liquid token that captures this specific exposure. KNTQ is the closest thing that exists right now, which is part of what makes the timing interesting. As HIP-3 matures and more infrastructure gets built, that could change. But today, this is the sharpest instrument available.

The market cap differential matters here. HYPE sits at roughly $6.4 billion, while KNTQ is around $45 million. That's 142x smaller. Same macro thesis, 142x cheaper entry point. But mc leverage alone isn't the insight because anyone can do that math. The insight is in how sKNTQ specifically accrues value.

Here's the mechanism. sKNTQ takes inspiration from the Assistance Fund model but adds a twist: instead of burning bought tokens, purchased KNTQ gets distributed to sKNTQ stakers, effectively increasing their ownership percentage of the protocol over time.

The revenue sources feeding this are specific:

Markets revenue: 100% of Kinetiq's disposable Markets income goes to KNTQ buybacks. This includes a minimum 10% of deployer share plus builder code revenue.

Launch revenue: 100% of Launch fees go to buybacks, fixed at 10% of deployer share.

Staking revenue (KIP-2): 70% of the 10% fee on staking rewards goes to buybacks. The other 30% funds operations.

Validator commissions: 100% of commission share from Kinetiq active set validators. These are validators who opt-in to splitting 50% of their commission from net new Kinetiq stake.

All acquired KNTQ flows to the sKNTQ staking contract and gets distributed proportionally to stakers.

And here's what closes the loop: kmHYPE minting is gated by sKNTQ staking tiers. To participate in Markets, you need to stake KNTQ first. Product adoption creates direct token demand. As Markets grows, KNTQ demand grows structurally.

The math creates an interesting asymmetry. Kinetiq's TVL scales with HYPE price because the underlying asset is staked HYPE. If HYPE doubles, Kinetiq's TVL roughly doubles even with zero new deposits. That means revenue scales, which means buyback pressure scales, which means the yield on sKNTQ scales. But if KNTQ's market cap stays flat while all this happens, the implied yield becomes absurdly high, which forces a price adjustment. Operating leverage works in your favor when the underlying asset appreciates.

Then there's Launch, which isn't priced at all because it hasn't shipped yet.

The problem Launch solves is capital efficiency. HIP-3 requires a minimum 500,000 HYPE bond to deploy a market, which at current prices means $17 million or more. Most teams building interesting products shouldn't have to lock that much capital just to launch.

Launch solves this through permissionless LST creation and stake crowdfunding. It works like a cross between Shopify and Kickstarter but for sourcing stake. A community can choose to launch an LST of its own, or stakers can back an HIP-3 deployer they believe in, drastically lowering the technical and capital requirements to ship. If stakers opt in, these LSTs can convert into full HIP-3 DEXs. Kinetiq's take rate on Launch hasn't been finalized, but based on the Markets fee structure, something in the range of 10% of deployer economics seems reasonable.

Every market that launches through Launch adds another revenue stream flowing back to the protocol. And because Kinetiq already has the largest pool of staked HYPE, they're the natural coordination point for teams that need stake but can't afford it independently.

Put it together. KNTQ gives you levered exposure to Hyperliquid's success through the 77% liquid staking position. It gives you direct value accrual through buybacks that compound into staker ownership. It gives you operating leverage as TVL scales with HYPE price. And it gives you optionality on Launch, which isn't priced because it doesn't exist yet but could become a meaningful revenue stream as HIP-3 adoption accelerates.

If Hyperliquid wins, KNTQ wins more.

0xomnia is a Hyperliquid OG. He's been building in crypto since 2013 and was among the earliest believers in what Hyperliquid could become, positioning Kinetiq as core infrastructure before the ecosystem had proven itself.

In our experience covering Hyperliquid, 0xomnia has demonstrated sharp product intuition and disciplined capital allocation. When VCs offered $10 million at a $250 million valuation, he turned it down. Whatever the reasoning, that's capital many founders would take.

His team of 18 contributors has executed consistently. Kinetiq launched kHYPE as the dominant liquid staking solution, capturing 77% market share. They shipped vkHYPE through a collaboration with Veda Labs, creating the largest vault on HyperEVM. They built iHYPE for institutional access, enabling publicly-traded companies like Hyperion DeFi to get compliant HYPE staking exposure. And they deployed Markets.xyz, making history as the first HIP-3 LST with guaranteed revenue share to stakers, sourcing 888,888 kHYPE from token holders in under 90 minutes.

The results speak for themselves. Kinetiq has become the largest protocol on Hyperliquid, operating as both an application and infrastructure layer. Four audits plus a $5 million bug bounty demonstrate commitment to security over speed. The protocol generates real revenue that flows directly to token holders rather than accumulating in a foundation treasury.

In an ecosystem where many projects have optimized for short-term extraction (paid KOL campaigns, promises that never materialize, quick pivots to other chains) Kinetiq has consistently chosen the slower path. No paid promotions. Organic growth only. Value returned to stakers. That pattern of behavior over 18 months is what gives me confidence that the team will continue building rather than extracting as the opportunity scales.

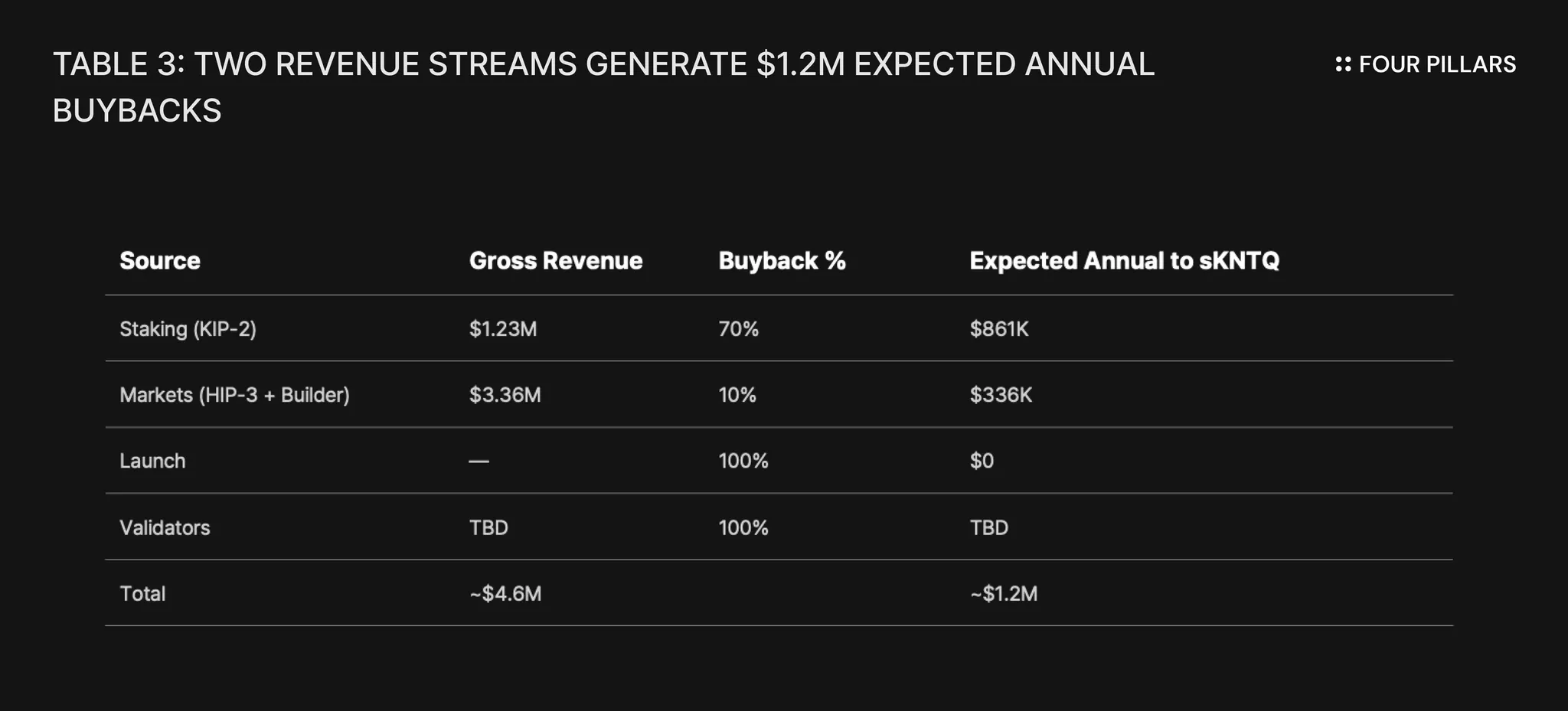

The thesis is qualitative until you run the numbers. So let me be specific about what sKNTQ is expected to earn once KIP-1 goes live.

Important note: At time of writing, KIP-1 (sKNTQ) has been announced and completed but is pending launch. The buyback flows described below are forward-looking projections based on the announced tokenomics, not current reality. You're buying the expectation of future yield once the mechanism activates.

10.4x P/S on gross revenue looks reasonable for a protocol with multiple scaling levers. 40x P/E on expected buybacks is high, but it's pricing zero growth in a thesis that depends entirely on growth.

Revenue Stream 1: Staking (KIP-2)

Kinetiq takes a 10% fee on staking rewards passing through kHYPE. Of that fee, 70% flows to sKNTQ buybacks and 30% funds operations. At current TVL of ~$560M earning 2.2% staking yield, gross protocol revenue comes to ~$1.23M annually, which means ~$861K expected to flow to sKNTQ once KIP-1 activates.

This scales linearly with HYPE price since TVL is denominated in staked HYPE. If HYPE doubles, TVL roughly doubles, staking rewards roughly double, and the buyback flow roughly doubles even with zero new deposits.

Revenue Stream 2: Markets.xyz

This is where the fee structure gets specific. Markets.xyz earns revenue through two separate channels, and they stack.

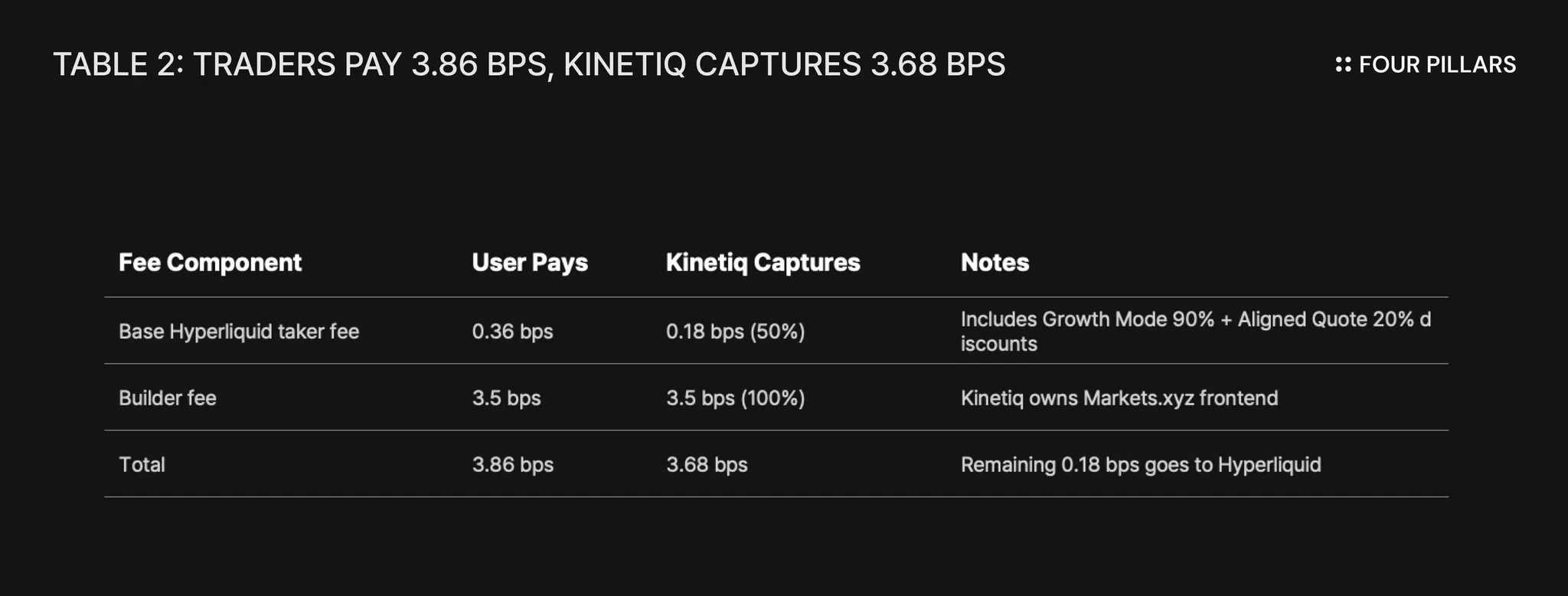

The first channel is HIP-3 deployer revenue. Kinetiq deployed the HIP-3 markets (USTECH, US500, BABA, USBOND, etc.) and earns 50% of the base Hyperliquid fee on all volume, regardless of which frontend the trader uses. The second channel is builder code revenue. Kinetiq owns the Markets.xyz frontend, and traders who use that interface pay an additional builder fee on top of the base fee.

One important caveat: The builder code fee only applies to volume routed through the Markets.xyz frontend. If someone trades Kinetiq's HIP-3 markets directly on hl.exchange, Kinetiq still earns the 0.18 bps deployer fee but not the 3.5 bps builder fee. I'm assuming most volume flows through Markets.xyz since it's Kinetiq's own product with better features, but this is an assumption worth flagging.

Markets.xyz launched January 12, 2026 and averaged ~$38M daily volume in its first 10 days. I'm using $25M/day as a conservative baseline since early volume tends to be inflated by launch excitement. At that volume, Markets generates ~$3.36M gross annually.

How much flows to sKNTQ?

Per KIP-1, 100% of Kinetiq's "disposable" Markets income flows to buybacks, with a guaranteed minimum of 10% of deployer share plus builder code revenue. The majority gets reinvested during growth phase into trader rebates, oracle feeds, and liquidity incentives.

I'm modeling at the 10% floor because that's what's contractually guaranteed. This is a conservative assumption with meaningful upside as Markets matures and reinvestment needs decrease.

At 10% to sKNTQ: $3.36M × 10% = $336K/yr expected

Revenue Stream 3: Launch

Fixed at 10% of deployer share, with 100% flowing to buybacks. Not live yet, so current contribution is zero.

Revenue Stream 4: Validator Commissions

Kinetiq active set validators opt into splitting 50% of their commission from net new Kinetiq stake. 100% of that commission share flows to buybacks. Depends on validator adoption, not quantified yet.

At current staking ratio of ~32%, this implies roughly 7-8% real yield once KIP-1 goes live.

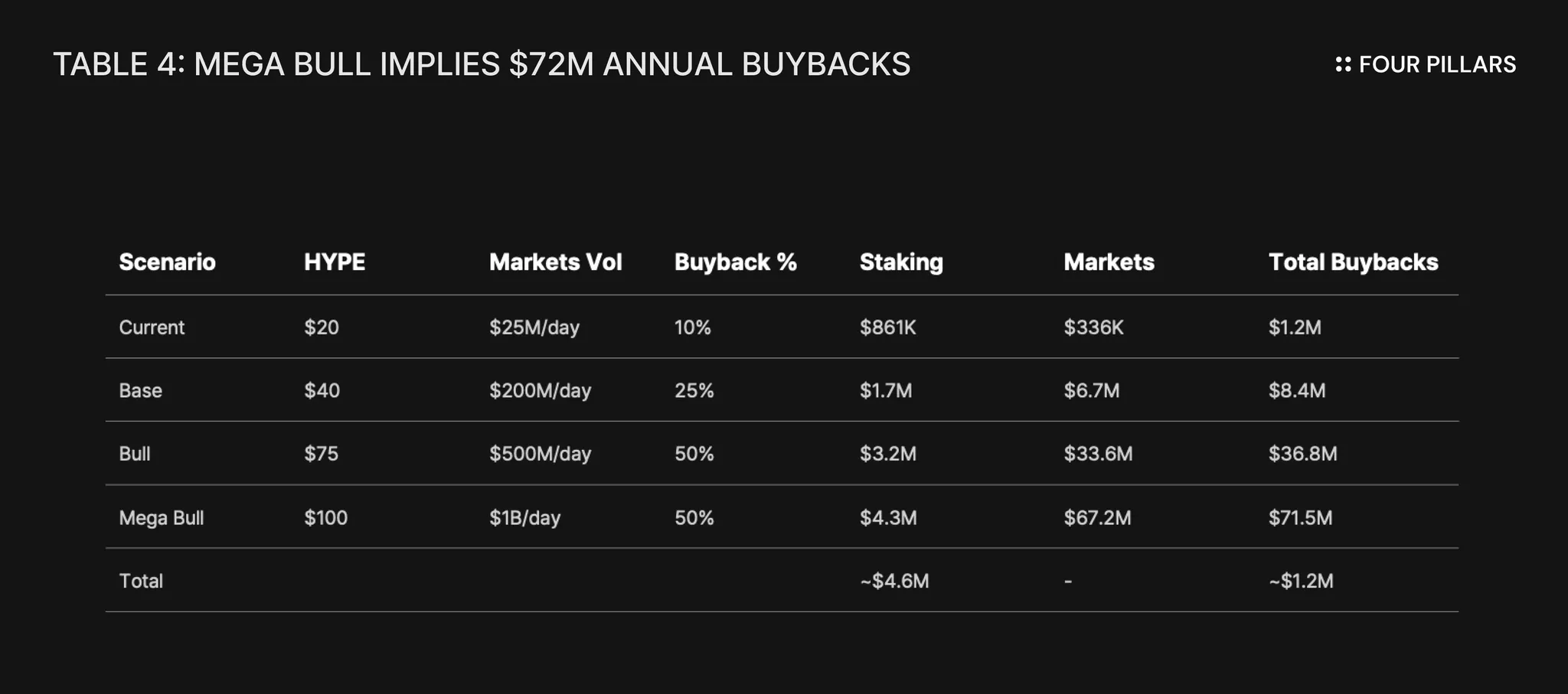

The numbers above assume everything stays constant: HYPE price flat, Markets volume at $25M/day forever, Growth Mode never ends, Launch never ships. If you believe Hyperliquid wins, none of those assumptions hold.

Let me walk through what moves the numbers.

HYPE price drives staking revenue. TVL is denominated in staked HYPE, so appreciation flows straight through. HYPE at $100 means TVL at $2.8B, which means $4.3M in staking buybacks alone.

Markets volume drives exchange revenue. At $200M/day, Markets gross revenue hits $26.9M. At $500M/day, it hits $67.2M. At $1B/day, it hits $134.3M. For context, Hyperliquid already does $5B+ daily in perp volume. $1B/day on Markets.xyz is 20% of current Hyperliquid volume—aggressive but not absurd if equity perps take off.

Growth Mode exit increases deployer fees. When the 90% discount goes away, HIP-3 deployer share jumps from 0.18 bps to 1.8 bps. That's a 10x on the deployer portion, though builder code (3.5 bps) stays the same. Total Kinetiq take goes from 3.68 bps to 5.3 bps.

Buyback % matures as reinvestment needs decrease. The 10% floor is for growth phase. At steady state, "disposable" income should be 25-50% based on typical protocol margins. Going from 10% to 50% is a 5x on the same gross revenue.

These aren't independent variables, but correlated bets on the same thesis: Hyperliquid wins, HIP-3 scales, equity perps become a real market.

Launch revenue and validator commissions not included in any scenario. Both are 100% to buybacks when live.

The Mega Bull case assumes HYPE 5x's from here to $100, Markets becomes the dominant equity perps venue at $1B/day (20% of current Hyperliquid volume in a world where that volume 3-5x's), and buyback % normalizes to 50% as growth mode ends. At 30x P/E, that's $2.15B FDV.

Is that aggressive? Yes. Is it absurd? No. Binance does $50B+ daily in perp volume. Hyperliquid already does $5B+. If equity perps become a real market and Hyperliquid captures it, $1B/day on Markets.xyz is 2% of Binance's current volume.

A 60x increase in buybacks translates to a 17x in FDV because multiples compress at scale. But 17x from a $127M FDV is still $2.15B.

The kmHYPE demand loop where Markets usage requires sKNTQ staking tiers. Launch optionality entirely since it hasn't shipped. Validator commission flow that scales with active set adoption. The fact that only 32% of KNTQ is currently staked, meaning yield will compress as more stake but also supply gets removed from circulation.

And the most obvious thing: I'm using a 10% buyback floor on Markets revenue because that's what's guaranteed. If "disposable" income at maturity is 50%, the Markets contribution to sKNTQ roughly 5x's at the same volume.

I've spent this entire paper making the bull case. Let me be honest about what kills it.

Non-substantial Markets.xyz volume. The first 10 days averaged $38M daily volume. I'm modeling $25M conservatively, but there's no floor. If volume drops to <$10M/day and stays there (it did, on Jan 18 2026), the Markets revenue thesis falls apart. HIP-3 deployer fees at 0.18 bps don't move the needle without builder code revenue, and builder code revenue needs traders using the Markets.xyz frontend specifically.

Growth Mode is a double-edged sword. I'm modeling at the 10% buyback floor because that's what's guaranteed during growth phase. But growth phase also means 90% of fees are being reinvested into rebates and liquidity. If that reinvestment isn't actually driving sustainable volume growth, Kinetiq is just subsidizing traders with no return. The bull case assumes reinvestment converts to retention.

LST market share could erode. Kinetiq has 77% of liquid staking on Hyperliquid today. That's dominant, but it's not a moat. If a competitor launches with better yields, better integrations, or just better marketing, that share compresses. Staking revenue is 70% of current buyback flow. Losing half of LST share means losing a third of sKNTQ yield.

Launch might not matter. I'm treating Launch as pure optionality, but the optionality might be worth zero. If HIP-3 deployers can raise $17M+ on their own, they don't need Launch. If they can't, maybe their markets aren't worth deploying anyway. The Shopify analogy assumes a long tail of small deployers who aggregate into meaningful volume, but that might not materialize.

Hyperliquid concentration risk. Every revenue stream depends on Hyperliquid succeeding. If Hyperliquid gets hacked, regulated out of existence, or simply loses to a competitor, KNTQ goes to zero. I'm making a concentrated bet on a concentrated bet.

A year from now, one of two things will be true. Either equity perps became a real market, Hyperliquid captured it, Kinetiq scaled with it, and this thesis looks obvious in hindsight. Or some combination of those bets failed, and I'm the analyst who published his conviction at the top.

I don't know which one it is. Neither do you. That's what makes it a bet.

What I do know is that I'd rather be wrong in public than right in private. The analysts who never commit, who hedge every statement, who write "this could go either way" at the end of every piece—they're protecting their reputations at the cost of being useful. I’m not interested in that game. I'm long KNTQ.

Dive into 'Narratives' that will be important in the next year