Affluent targets DeFi's distribution bottleneck, embedding vault-based yield strategies directly into Telegram Wallet's native Earn tab for 1B+ users.

The three-role vault architecture (Owner / Guardian / Manager) constrains vault managers through code-enforced whitelists, leverage caps, oracle-verified RFQ execution, and a Guardian veto layer.

Affluent's correlation-aware risk model is technically differentiated, decomposing DeFi positions into underlying exposures and using a dual-metric system (Risk Ratio + Leverage) that prices correlated pairs more accurately than standard LTV.

V3 (Jan 2026) transitions the protocol from TON-native lending to cross-chain yield infrastructure, with the Sentora Vault bridging USDT to Euler/Morpho on Ethereum — the first of what the team envisions as a series of partnerships connecting Telegram's distribution to Ethereum's deep liquidity.

At ~$4.7M TVL, the protocol's path to scale depends on stablecoin yield partnerships, vault manager diversification, and sustained Telegram Wallet integration, which are variables that will determine whether Affluent's architecture finds its market before the embedded yield race is decided.

DeFi has a yield distribution problem. The infrastructure for earning 4-8% on stablecoins exists, and it's mature. Aave processes $27B+ in deposits. Morpho curates $6B across isolated markets. Pendle lets you strip and trade yield curves. The pipes are built. The problem is that the 99.9% of people who could benefit from these pipes have no idea how to connect to them, and wouldn't trust themselves to try.

This is the gap Affluent is designed to close. Not by building better yield infrastructure, but by embedding existing yield strategies directly inside Telegram Wallet, where 1B+ users already live.

To understand why that's a harder problem than it sounds, it helps to see how DeFi got here.

The history of DeFi yield is really a history of who you have to trust and how much you have to know.

Phase 1: Direct lending

Aave V1-V3 and Compound established the template. You deposit into a pool, borrowers pay interest, a smart contract handles the rest. Clean and transparent, but each V3 market is an isolated liquidity silo, and yield optimization means actively choosing which markets to supply, when to rebalance, and which collateral parameters to monitor. Most people can't do this, and the ones who can are already doing it.

Phase 2: Curated allocation

Morpho Blue introduced permissionless isolated markets with a vault layer on top, where professional risk managers (e.g. Gauntlet, Steakhouse, MEV Capital) allocate depositor capital across pools based on their own risk assessments. This solved the optimization problem, and it scaled to billions. But it introduced a new trust layer: you're trusting that the curator won't misallocate your capital, and you need enough DeFi literacy to evaluate whether they're good at their job.

Meanwhile, Aave V4 (testnet Nov 2025, mainnet planned 2026) is building its own answer, a Hub-and-Spoke architecture that unifies liquidity per chain while letting modular Spokes handle different risk profiles. The trend is clear: more sophisticated capital allocation, still targeting DeFi-native users.

Phase 3: Embedded yield

The insight driving this wave isn't a new yield source or a better risk model but rather the recognition that the next hundred million users aren't coming to DeFi. DeFi has to go to them.

Multiple protocols are converging on this simultaneously, but from different angles. Aave launched a consumer savings app in November 2025 (up to 9% APY, deposits from 12,000+ US banks, $1M balance protection) and now powers embedded yield inside MetaMask, Bitget Wallet's 80M users, and Latin American fintechs. Morpho reached $1B+ in Coinbase-originated loans. Frax is building its own consumer frontend with Visa card integration.

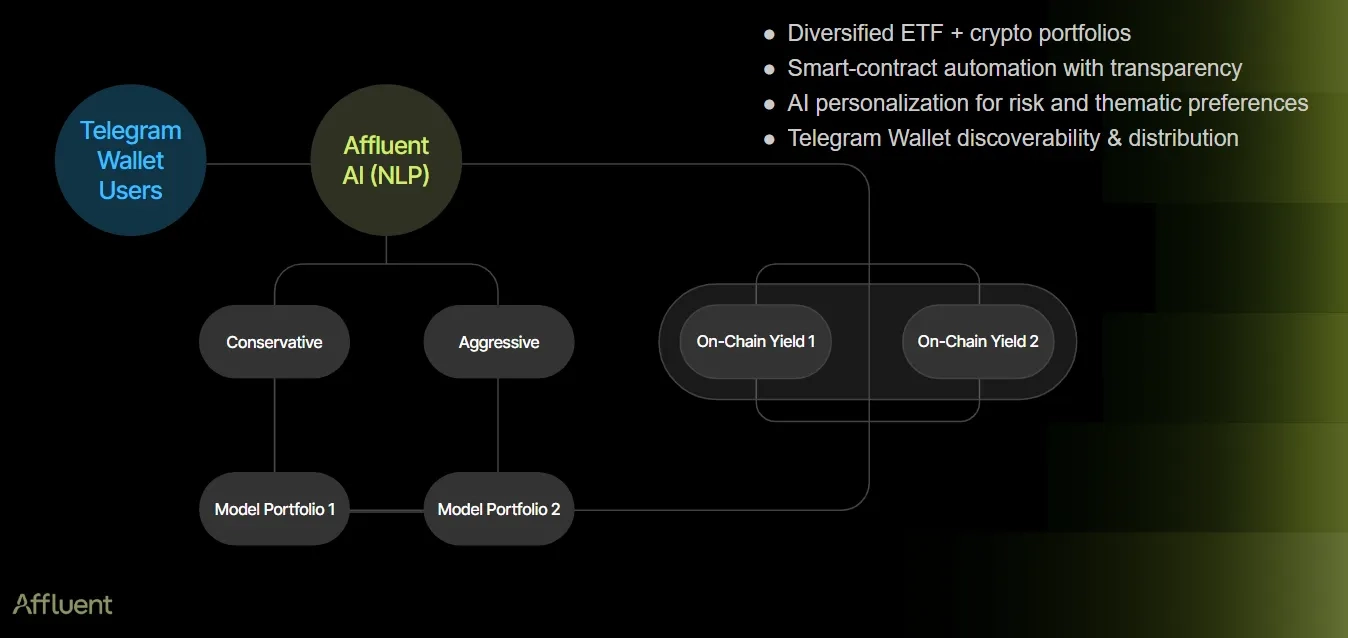

Affluent's approach is different from all of these. Rather than building a standalone app or partnering with wallets, it embedded directly inside Telegram Wallet's native Earn section, as part of the wallet's own UI. Users open Telegram, tap Wallet, tap Earn, and deposit. No wallet connection, no chain selection, no bridging.

Here's the thing about DeFi yield infrastructure: it's largely solved. The unsolved part is who gets access to it.

The numbers make the gap visible:

Aave: $27B+ deposits, 2.5M users, now embedding yield inside wallets and fintechs globally

Morpho: $6B TVL, $1B+ in Coinbase-originated loans

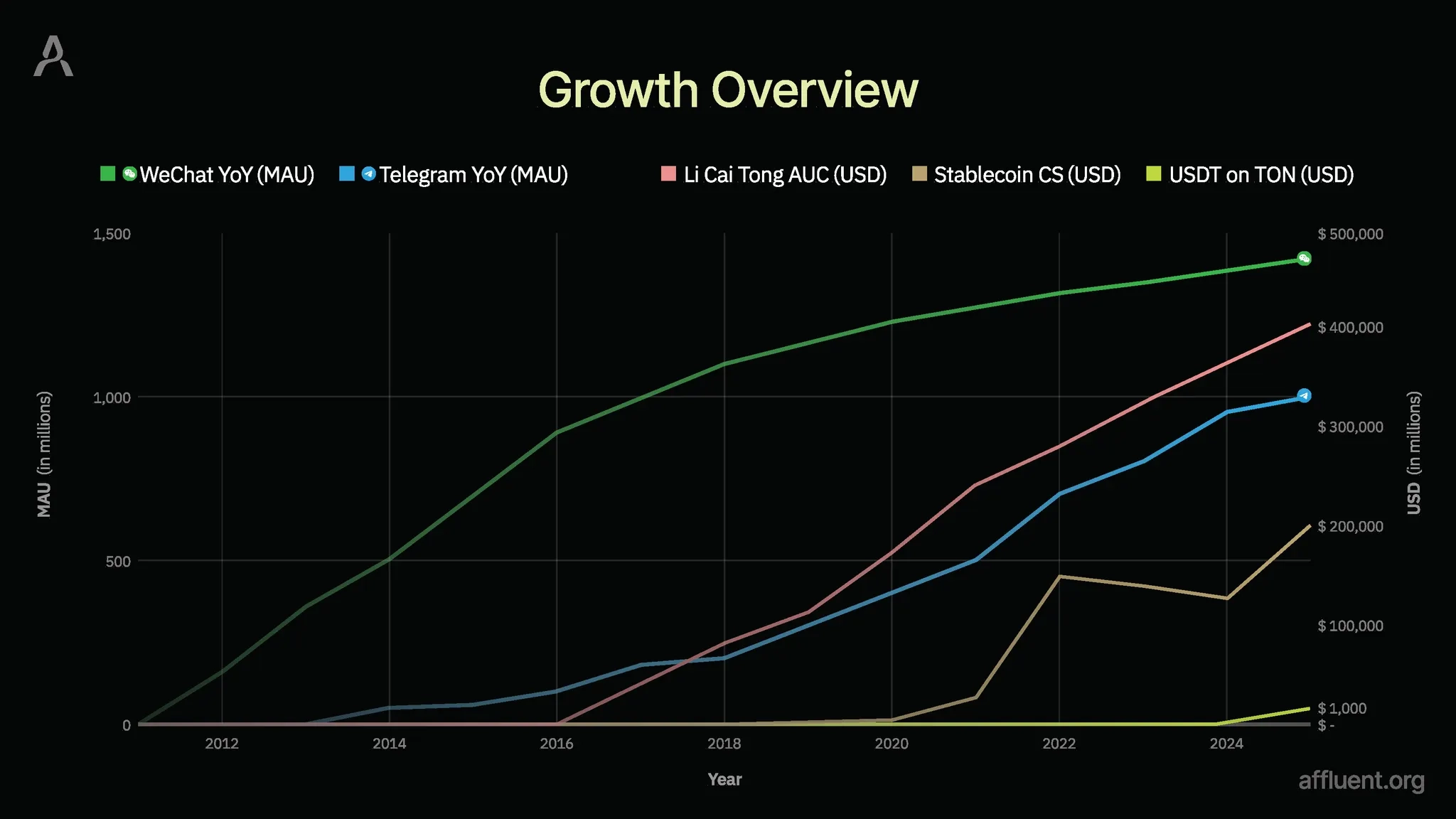

Yu'e Bao peak AUM (2017): $233B, built by embedding MMF yield in a payments app

That last number is the one that should change how you think about the embedded yield race. Yu'e Bao wasn't a technology breakthrough. It was a distribution breakthrough. The fund's returns were mediocre, roughly in line with comparable money market instruments.

What made it extraordinary was the conversion funnel: 700M+ Alipay users, idle balances sitting in a payment app, and a one-tap path to earning yield. Nobody downloaded a separate investing app. They just noticed their idle Alipay balance could earn interest, and tapped "yes." Ultimately, the fund grew from zero to world's largest in four years because the product was the placement, not the performance.

The embedded yield race in DeFi is now multi-front. Standalone consumer apps (Aave App), exchange integration (Morpho via Coinbase), wallet backends (Aave powering MetaMask and Bitget), and platform-native embedding (Affluent inside Telegram Wallet). Each model has different acquisition costs, different trust signals, and different lock-in dynamics.

Affluent's bet is that platform-native embedding (zero download, zero wallet setup, zero acquisition cost), creates a fundamentally different conversion dynamic than asking users to find and install something new. That's a bet on Telegram's distribution power, not on Affluent's architecture. Which is both the strength and the vulnerability of the thesis, as we'll see.

Source: Affluent

But distribution alone isn't enough. You also have to convince users that their money is safe, and in DeFi, "safe" means different things depending on how many humans stand between a depositor and their funds.

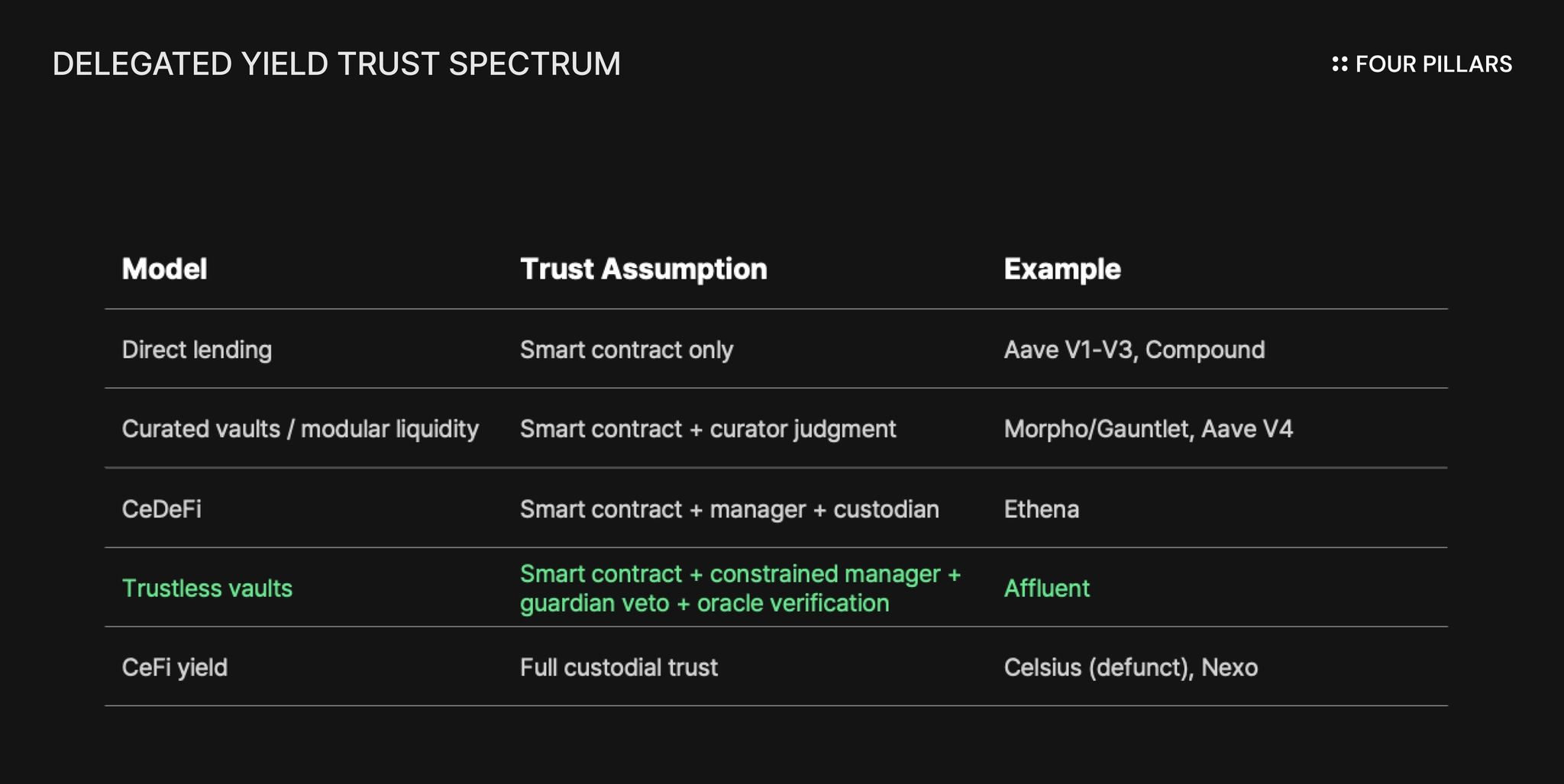

What's interesting about Affluent's position on this spectrum is the claim it's making. Most vault-based products (e.g. earn, Morpho curators, even Ethena) give their strategists relatively broad execution authority. The strategist decides what to do, and the smart contract ensures they can't steal the funds outright, but the range of permitted actions is wide. Affluent constrains its vault managers through code-enforced whitelists, leverage caps, oracle-verified swap execution, and timelocked parameter changes, with a separate Guardian role that can veto any risk-increasing action. It's a narrower corridor of permitted behavior than most DeFi vaults offer.

Whether that corridor is narrow enough to justify calling it "trustless," and whether the architecture holds up under stress at scale, is what the rest of this article examines.

Affluent started life as Factorial Finance, a modular lending protocol on TON with isolated pools and a Factory for permissionless market creation. The architecture mirrored Morpho Blue: each pool siloed, no cross-contamination, with a vault layer on top for UX abstraction. Standard playbook.

The rebrand in June 2025 signaled something more ambitious. The name changed, the positioning shifted from "lending protocol" to "infrastructure for trustless asset management," and the team behind it came into sharper focus: Justin Hyun, formerly a director at the TON Foundation, and Hyung Lee, an ex-TradFi options trader who co-founded B-Harvest, a validator and staking infrastructure firm. The combination of TON insider knowledge and derivatives market experience explains a lot about the design choices that followed.

Today the protocol has three core components. The Affluent Market is the lending engine — supply, borrow, liquidate in isolated pools. The Factory enables permissionless market creation, though it's currently gated until the team considers it battle-tested. And the Strategy Vault is the differentiated product layer where professional managers operate under code-enforced constraints.

The Market is table stakes. The Factory is a promise. The Strategy Vault is the thesis.

Source: Affluent

Most lending protocols rely on a single loan-to-value ratio: borrowed value divided by collateral value. Simple, intuitive, and wrong in ways that matter.

The problem is correlation. When you borrow TON against tsTON (a liquid staking derivative of TON) the two assets move almost in lockstep. tsTON is TON plus a staking yield premium plus a thin layer of smart contract risk. A standard LTV model treats this position identically to borrowing TON against USDT, where the collateral and the borrowed asset have zero price correlation. The result is that correlated pairs get overcollateralized relative to their actual risk, locking up capital unnecessarily, while uncorrelated pairs may be undercollateralized relative to theirs.

Affluent replaces LTV with a dual-metric system. Both metrics must stay below market-defined thresholds simultaneously:

Risk Ratio = Σ(risk_factor × |net_asset_per_token|) / total_net_asset

Leverage = total_supply / net_asset

The key mechanism is decomposition. Instead of treating a DeFi position as a single opaque asset, the protocol breaks it down into its underlying exposures. tsTON isn't evaluated as "tsTON"; rather, the protocol decomposes it into underlying TON exposure, then adds a DeFi-specific risk premium (5% for smart contract and depeg risk) on top.

In practice: supply $100 tsTON, borrow $60 TON, and the system first nets the TON position ($100 − $60 = $40 net), applies the 40% TON risk factor to the net ($16), then adds the 5% tsTON premium on the gross supply ($5), yielding $21 total risk value against $40 net asset, a 52.5% risk ratio. The same position under a flat LTV model would simply read 60% borrowed against 100% collateral, missing the correlation entirely.

In practice, this means a user borrowing TON against tsTON gets meaningfully more favorable treatment than one borrowing TON against an uncorrelated stablecoin. The system recognizes that these are different risk profiles and prices them accordingly, which is closer to how a TradFi risk desk models a derivatives portfolio (decomposing complex positions into factor exposures).

The tradeoff is complexity. Every asset needs a calibrated risk factor. Every DeFi position type needs a decomposition rule. Parameter changes carry real consequences, and the protocol has limited historical data to validate these parameters under stress. The isolated pool structure contains the blast radius (a miscalibrated parameter in one market doesn't cascade into others) and the conservative initial parameterization gives the team room to refine as live data accumulates.

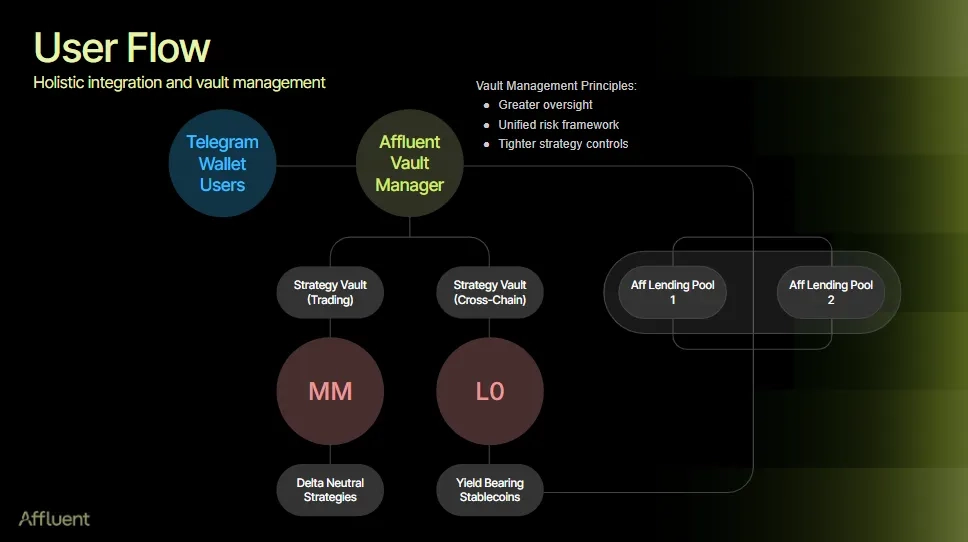

The Strategy Vault is where Affluent's "trustless" claim gets specific. The design separates three roles with distinct authority levels, each constrained by the one above it.

The Owner creates the vault and sets all parameters: which assets and markets the vault can touch (whitelists), the maximum leverage, the price deviation tolerance for swaps, the fee rate (capped at 2% of NAV), and the oracle configuration. Critically, most Owner actions are timelocked — any sensitive change (upgrading the vault, swapping the oracle, transferring ownership, changing the guardian, raising the leverage cap) sits in a pending state for a configurable period between 24 hours and two weeks before executing.

The Guardian exists for one purpose: to veto. It can cancel any pending timelocked action and block risk-increasing changes. It doesn't operate the vault, doesn't touch funds, doesn't set strategy. It watches the watchers. If the Owner's keys are compromised and an attacker tries to widen the leverage cap or swap the oracle to a malicious feed, the Guardian can kill the action during the timelock window.

The Vault Manager operates within the rails the Owner defined. It can swap between whitelisted assets (within the price deviation tolerance), interact with whitelisted Affluent Markets, and rebalance positions, but it cannot touch non-whitelisted assets, exceed the leverage cap, or bypass oracle verification. It must also maintain a cash buffer for depositor withdrawals. All vault balances are publicly queryable on-chain via getVaultData.

The trust gradient works like this: even a compromised Manager can't steal funds or take unauthorized risk; it's boxed in by whitelists and caps. Even a compromised Owner can't execute harmful changes instantly. The timelock creates a window for the Guardian to intervene. The only dangerous scenario is simultaneous compromise of Owner and Guardian, which is a fundamentally different (and much harder) attack than compromising a single key.

This is more restrictive than most Ethereum vault architectures. On Morpho, vault curators have broad discretion over which markets to allocate to and how to rebalance. On Yearn, strategists operate with significant latitude. Affluent's Manager is closer to a robot following a playlist than a fund manager making judgment calls.

The tradeoff is flexibility. If market conditions shift in a way the Owner didn't anticipate and whitelist for, the Manager can't adapt. Safety bought at the cost of agility.

Oracle-Verified RFQ

The most architecturally novel component is how vaults execute swaps.

When a Morpho vault or a Yearn strategy needs to swap assets, it routes through a DEX aggregator (e.g. 1inch, Paraswap, CowSwap). Every swap is exposed to MEV extraction, slippage on thin liquidity, and the smart contract risk of whichever DEX or aggregator handles the trade.

Affluent's vault managers don't touch DEXs at all. Instead, the protocol uses an Oracle-Verified RFQ (OVR) system. When a Manager needs to swap, it sends a Request for Quote to competing market makers. The market makers respond with prices. The protocol then verifies every quote against the oracle price within a pre-defined Price-Deviation Tolerance set by the Owner. If the best quote deviates beyond tolerance, the trade auto-rejects.

Market makers handle the actual execution, including swaps, minting, burning, and cross-chain bridging. This means the vault's funds never interact with external smart contracts at all.

The cost is that you need active market makers competing on quotes. At $4.7M TVL, the volume isn't enough to attract deeply competitive market making. As the protocol scales (if it scales), this becomes a genuine structural advantage. At current size, it's an elegant solution looking for sufficient demand.

In January 2026, Affluent shipped its V3 upgrade — the feature set that makes the team's strategic intent unmistakable. Affluent chose TON as the infrastructure layer to access Telegram's distribution, not as an ecosystem to build within. V3 is the proof: rather than deepening TON-native DeFi, the protocol built bridges outward to access Ethereum's liquidity depth from Telegram's user layer.

Three features define the upgrade:

Cross-Chain Accounts. Proxy accounts deployed on external chains act as agents following commands from the TON-based vault, communicating via LayerZero messaging. The vault issues instructions (supply to this Euler market, mint this Morpho vault token) and the proxy executes on the target chain. Strict whitelist management, price deviation tolerance, and integrity verification (anti-forgery, anti-replay) protect against cross-chain message tampering.

RWA Market Collateralization. A Market Freeze function that suspends all risk-increasing transactions (e.g. new loans, collateral withdrawals) until the oracle can provide trustworthy data. Conservative, but appropriate for assets that don't trade 24/7.

Deposit caps and withdrawal fees. V3 added per-token deposit caps to ensure stability of vault operations and withdrawal fees as a bank-run friction mechanism, protecting remaining depositors' NAV when a vault faces heavy redemptions.

The Sentora Vault, launched alongside V3, is the proof of concept, and the architectural template for everything Affluent wants to do next. Users deposit USDT on TON. The vault bridges to Ethereum, mints Euler RLUSD and Morpho PYUSD vault tokens, bridges the vault tokens back, and returns yield to depositors. All abstracted behind a one-click Telegram Wallet interface.

This is where the stablecoin thesis meets the distribution thesis. PayPal, Ripple, and other global institutions are pouring resources into the stablecoin race, each issuing yield-bearing stablecoins designed to capture future payment rails. But issuing a stablecoin is only half the problem; the other half is getting it into users' hands. Affluent's partnership with Sentora, a risk curator operating across Morpho and Euler, is the first concrete expression of a broader strategy: sourcing institutional-grade stablecoin yield on Ethereum and routing it to Telegram's distribution layer.

Architecture is one thing. What's actually running is another.

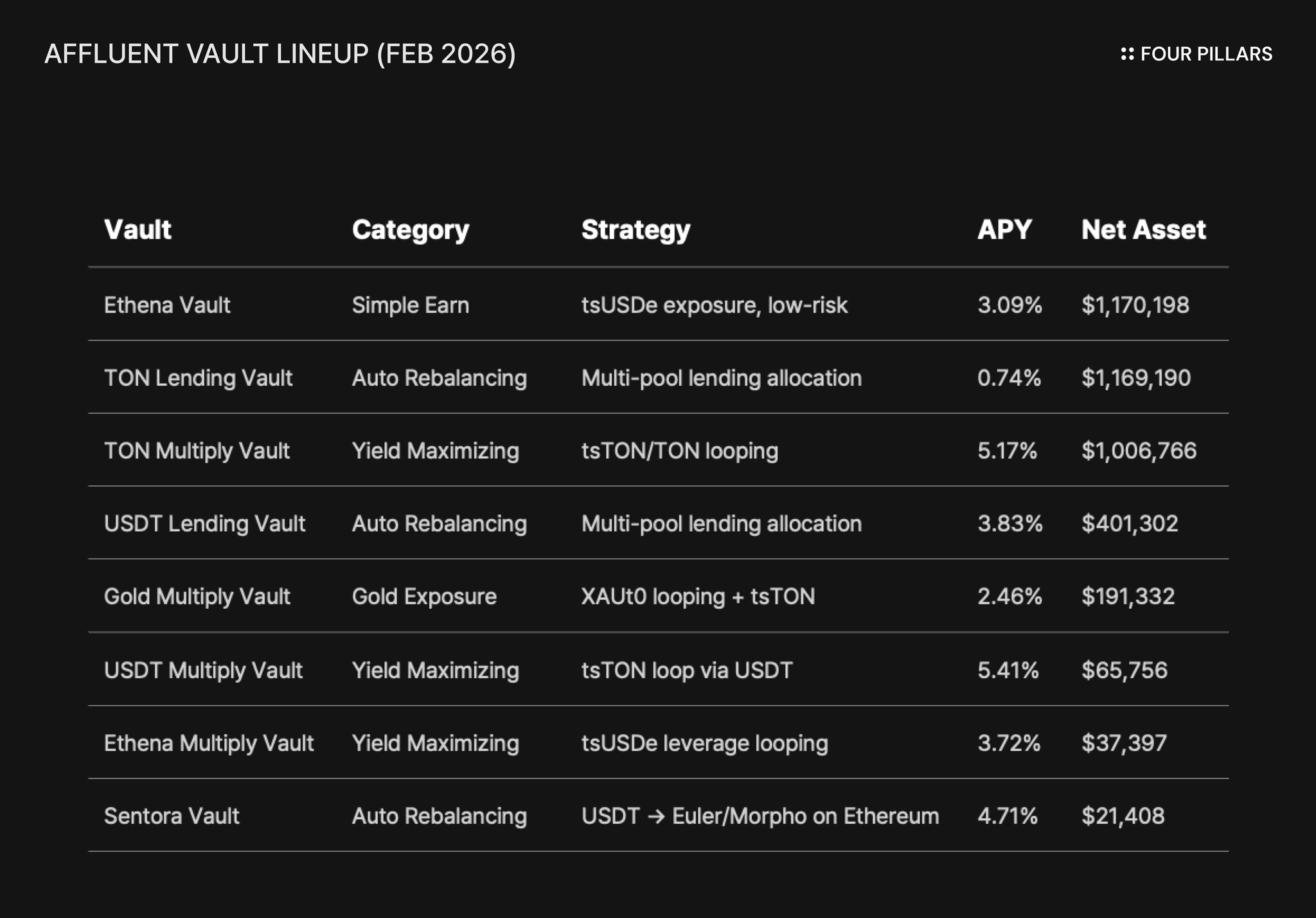

As of February 10, 2026, Affluent operates eight vaults across three categories:

The distribution is instructive. The two largest vaults by net asset are the Ethena Vault ($1.17M, tagged "Simple Earn, Low Risk") and the TON Lending Vault ($1.17M). The highest-APY vaults (TON Multiply at 5.17%, USDT Multiply at 5.41%) sit in the middle of the pack by assets.

Notably, the vaults that have attracted the most capital (the Ethena Vault and the Gold Multiply Vault) share a common feature: they're the products currently embedded in Telegram Wallet's Earn section. This is the distribution thesis in miniature. The Sentora Vault, which routes USDT cross-chain to Euler and Morpho on Ethereum, is next in line for Telegram Wallet Earn integration. If historical patterns hold, the placement itself will be the inflection point for that vault's TVL.

The Multiply Vaults use looping strategies (deposit collateral, borrow against it, swap back into collateral, redeposit), amplifying yield exposure up to 4x leverage. The Gold Multiply Vault is notable as the first yield-bearing gold product on TON, backed by Tether Gold's XAUt0 (1:1 physical gold, LBMA "London Good Delivery" bars, Swiss vault custody).

Separate from the vaults, Affluent operates eight isolated lending markets where users can directly supply and borrow.

A note on how these numbers relate: vault deposits flow into the markets. The $6.85M in total market supply includes both vault-deployed capital (~$4.06M across eight vaults) and direct depositors who supply and borrow in the markets without using a vault. These aren't additive; the vaults are a subset of market activity, not a separate pool.

Two things stand out. First, the Storm and Tradoor markets accept perp DEX LP tokens (SLP and TLP) as collateral, making Affluent a composability layer for derivatives infrastructure. A Storm Trade LP can deposit their LP tokens, borrow against them, and loop for amplified yield. Second, the Vault Market accepts USDT-LV and TON-LV (Affluent's own Lending Vault tokens) as collateral, enabling recursive leverage on top of vault positions.

The markets exist independently of the vaults. Users can supply and borrow directly without going through any vault layer. The vaults are a convenience and optimization layer that operate on top of these markets, allocating depositor capital across them according to their respective strategies.

The more useful competitive frame for Affluent isn't protocol rankings on a single chain; rather, it's the broader embedded yield race across DeFi.

Affluent's positioning is distinct along two axes. On architecture, it offers tighter vault constraints than Morpho curators or Yearn strategists, trading flexibility for verifiable safety guardrails. On distribution, it's embedded natively inside a messaging super-app rather than a wallet or exchange, which means zero acquisition cost per user but total dependency on a single channel partner. The risk concentration is worth stating plainly. Aave hedges its distribution by powering yield across MetaMask, Bitget, and its own consumer app simultaneously. Morpho routes through Coinbase. Affluent routes through Telegram. If Telegram deprioritizes Web3 financial products or changes its Wallet integration terms, Affluent loses its primary user funnel. That's a strategic dependency. Every embedded yield product depends on its distribution partner; Affluent's dependency is just more concentrated than most.

The counterargument is that Telegram's commitment appears to be deepening, not retreating. The Wallet launched US services in late 2025 and is reportedly expanding into payments infrastructure. Affluent's tight collaboration with the Telegram Wallet team (the Earn tab integration, the progressive addition of vaults to the native UI) suggests an active partnership rather than a passive listing.

The Telegram Wallet integration is Affluent's most differentiated strategic asset, and the architectural comparison to Yu'e Bao is structurally apt — zero-friction access inside a super-app, invisible infrastructure, no separate download.

The integration has been live for three months. For calibration: a conversion rate of 0.001% of Telegram's monthly active users, each depositing $100, would produce roughly $950M. The current TVL figure suggests the integration is in its earliest adoption phase, with the vast majority of Telegram's user base yet to engage.

This is consistent with how platform-embedded financial products typically develop — gradually, then suddenly, as trust compounds and awareness spreads. The thesis remains a coherent long-term proposition. In the near term, the data provides more questions than confirmation, and the timeline for meaningful conversion is an open variable.

Several features of the current architecture are worth monitoring as the protocol scales.

The multiply vaults (which represent a significant share of deposits) run variations of leveraged asset loops. A single directional move in the underlying collateral affects multiple vaults simultaneously through the same risk factor. The vault count offers product variety, not exposure diversification in the traditional sense. The Ethena Vault and Sentora introduce genuine differentiation through independent yield sources; the multiply strategies move largely in concert.

RedStone provides oracle services across all markets and vaults — standard for the current oracle landscape, but a single-provider dependency in an infrastructure layer where redundancy is the norm on more mature chains. The permissionless Factory for third-party vault creation exists in the architecture; its activation would meaningfully broaden operational resilience. Until then, vault management remains concentrated.

The Guardian role is well-designed. Its effectiveness depends on operational independence between Guardian and Owner, a dimension that would benefit from greater public clarity. Transparency here would strengthen the trust framework the protocol's entire value proposition rests on.

It's worth being precise about Affluent's relationship to TON. The protocol built on TON because TON is Telegram Wallet's native chain, the technical prerequisite for embedding directly into the Earn tab. This is a distribution-driven infrastructure choice, not an ecosystem bet.

The distinction matters because Affluent's growth trajectory is tied to Telegram Wallet's financial utility maturing, not to the growth of TON's broader DeFi ecosystem. The V3 cross-chain upgrade makes this explicit: rather than waiting for deep liquidity to develop natively on TON, Affluent bridges outward to Ethereum's Morpho and Euler markets where the liquidity already exists. The partners the team is currently engaging (stablecoin issuers, RWA tokenizers, risk curators) are almost entirely outside the TON ecosystem.

That said, the base layer dependency is real. Affluent's smart contracts, vault logic, and user-facing transactions all execute on TON. Any degradation in TON's infrastructure, validator set, or bridge security directly impacts Affluent's operations. Cross-chain architecture reduces the liquidity dependency on TON but doesn't eliminate the execution dependency. Readers evaluating Affluent are underwriting a view on Telegram's distribution power and, to a lesser but non-trivial extent, TON's continued reliability as an execution environment.

Affluent's roadmap has sharpened considerably since launch, moving away from earlier explorations (TON-native Bitcoin wrapping, tokenized Telegram bonds) toward a clearer thesis: become the primary channel connecting institutional-grade stablecoin and RWA yield to Telegram's distribution layer.

The stablecoin market is undergoing a supply-side explosion. PayPal (PYUSD), Ripple (RLUSD), and a growing roster of institutions are issuing yield-bearing stablecoins, each competing for distribution. Affluent's pitch to these issuers is straightforward: access to Telegram's user base through a single vault integration. Whether that pitch lands depends on whether issuers view Telegram as a distribution channel worth building for, a question that the Sentora partnership begins to answer but doesn't yet resolve. The Sentora Vault, routing USDT to Euler and Morpho on Ethereum, is the first live expression of this model. The pipeline includes additional stablecoin yield sources and risk curators, with Sentora's integration into the Telegram Wallet Earn tab as the near-term catalyst.

This is where the partnership model comes into focus. Affluent isn't building yield strategies in isolation; it's partnering with specialized players at each layer. Sentora handles risk curation across Morpho and Euler. Stablecoin issuers provide the yield substrate. Telegram Wallet provides the distribution. Affluent is the connective tissue, the vault infrastructure and compliance layer that makes the whole stack addressable from a single Earn tab.

The honest caveat: the "yield channel" thesis is early. The most mature proof point is the USDT Earn product (the Ethena Vault embedded in Telegram Wallet's Earn tab), which has accumulated roughly $1M in TVL across ~3,850 depositors at an average yield around 4%. The deposit profile is worth noting — an average deposit size of roughly $260 suggests genuine retail distribution rather than a handful of whales inflating the number. That's directionally consistent with the Yu'e Bao analogy: many small balances, low friction, organic discovery through the native UI.

Beyond stablecoins, the team is broadening the asset base through cross-chain integrations. Bridged versions of cbBTC and wETH are already live, opening the door to BTC and ETH yield strategies accessible from Telegram. The more ambitious expansion is into tokenized equities (xStocks) and broader RWA products, a bet that Telegram's global user base includes meaningful demand for investment products that traditional brokerages either don't serve or haven't reached. That demand is assumed, not yet observed at any meaningful scale through Affluent's existing products, but the thesis is at least directionally consistent with how fintech adoption has played out in markets where mobile-first platforms leapfrogged traditional financial infrastructure.

The progression follows a legible logic: stablecoin yield first (low complexity, high trust), then crypto-native assets (BTC/ETH yield), then RWAs (equities, treasuries). Each step requires deeper infrastructure and more sophisticated compliance, but each step also meaningfully expands the addressable market.

The most significant variable in Affluent's trajectory may be Telegram Wallet's own evolution. The Wallet team is reportedly expanding into payments infrastructure, which would transform Telegram from a messaging app with a wallet into something closer to a financial super-app. If that transition materializes, Affluent's position as the native yield layer becomes significantly more valuable — idle payment balances earning yield is exactly the Yu'e Bao playbook.

The team has also noted the possibility of leveraging Telegram's AI capabilities (Cocoon) as a future interface layer, though this remains exploratory rather than committed.

A handful of observable signals will indicate whether the roadmap is progressing:

TVL trajectory post-Sentora Earn integration. The Telegram Wallet Earn tab has been live since November 2025. The Sentora Vault's integration into the Earn tab, expected in early March 2026, will be the first test of whether cross-chain yield products convert at the same rate as simpler native offerings. The direction matters more than the absolute number.

Vault manager diversification. A single external manager deploying on the permissionless Factory would signal ecosystem maturation more convincingly than any new asset integration. Currently, all strategy vaults are managed by a single entity.

Stablecoin partnership cadence. Additional stablecoin yield sources and risk curators beyond Sentora would validate the "yield channel" thesis. The pipeline is reportedly active, but the conversion to live products is what counts.

Telegram Wallet's own trajectory. Payments expansion, regulatory approvals, and user growth in new markets all directly compound Affluent's distribution advantage.

Source: Affluent

Affluent has built institutional-grade infrastructure and distributed it through a channel with unmatched reach but early-stage conversion. The architecture is sound. The distribution positioning is unique. The stablecoin and RWA pipeline gives the protocol a growth vector that doesn't depend on any single ecosystem's DeFi activity. The question is whether the partnerships, the channel, and the capital arrive on a schedule that the infrastructure can wait for.

Dive into 'Narratives' that will be important in the next year