Issuer premium in stablecoins is compressing as value shifts toward distribution and usage control rather than issuance scale.

Circle’s margins no longer scale with USDC circulation, reflecting growing economic capture at the distribution layer.

CPN and Arc represent a strategic move up the stack to regain leverage over usage, routing, and settlement.

For $CRCL, the upside is stabilization of long-term economics rather than explosive growth.

Circle’s business used to be easy to describe. Issue USDC, hold reserves, earn interest, and scale with volume. For a long time, that model worked well enough that few people questioned it. It enabled Circle to grow rapidly, establish itself as a core stablecoin issuer, and ultimately list on one of the world’s largest public markets. Even today, Circle’s top line continues to show solid growth.

Beneath the surface, however, the limitations of this model are becoming more visible. While revenue continues to expand, growth is gradually approaching a ceiling, and margins are under sustained pressure. Left unchanged, the current structure risks capping long-term returns.

As stablecoins move from trading into payments, treasury, and embedded financial workflows, value is moving toward platforms that control usage and end users. Circle’s recent push into payments infrastructure and settlement should be read in that context. The company is responding to a market in which issuer premium is under pressure and control over distribution increasingly determines returns.

This memo lays out that dynamic and explains why Circle has chosen to build CPN and Arc as the next phase of its business.

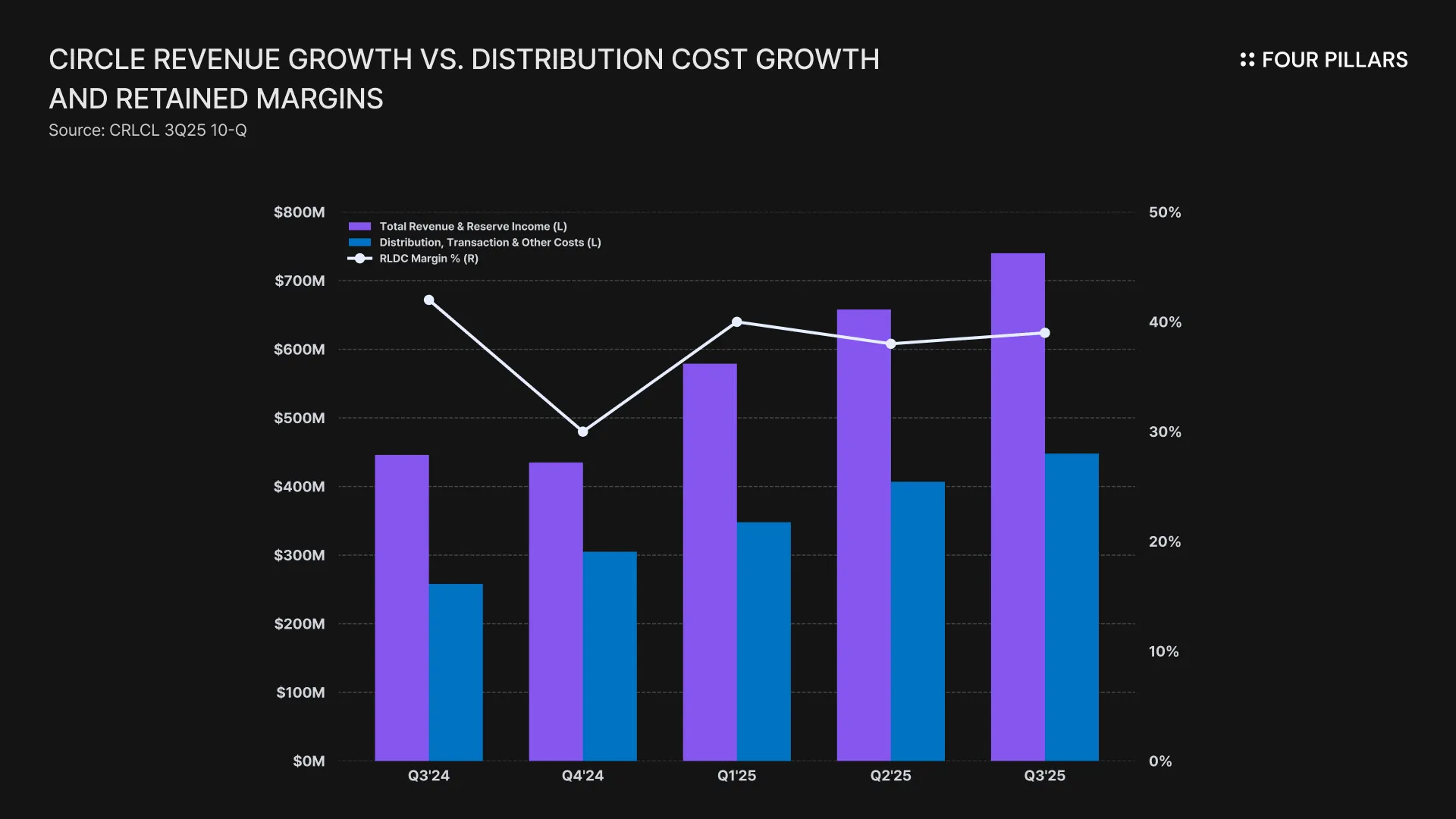

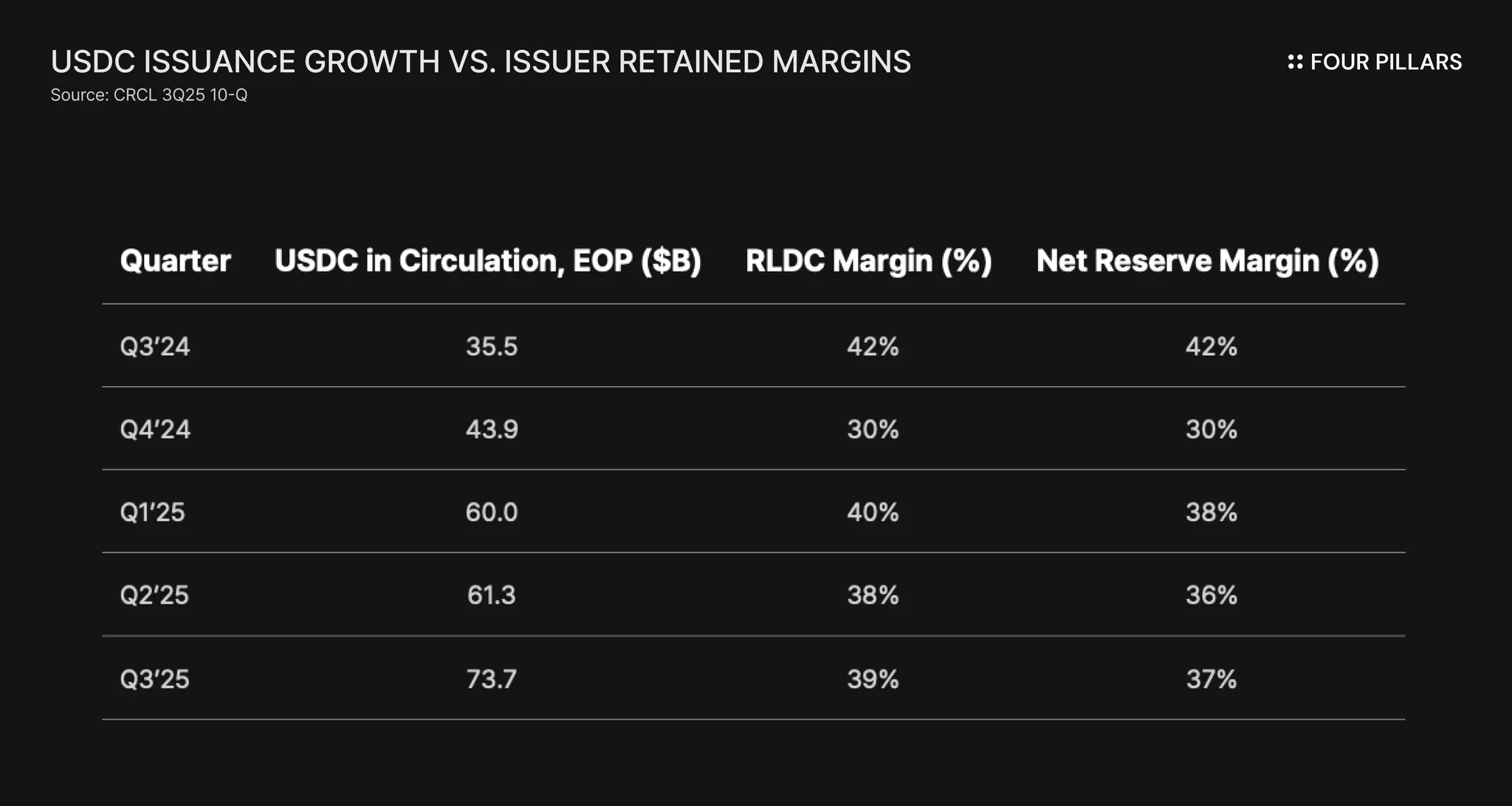

From Q4 2024~Q3 2025, Circle’s total revenue and reserve income increased from $435M to $740M. Over the same period, distribution, transaction, and other costs increased from $305M to $448M. Revenue grew quickly but distribution costs grew just as quickly, and in some quarters faster.

As a result, Circle’s revenue less distribution costs (RLDC) margin did not expand with scale. It moved from 42% in Q3 2024, down to 30% in Q4 2024, then back to 40% in Q1 2025 and 39% in Q3 2025. Margin outcomes were driven by distribution mix rather than issuance volume.

Distribution costs represent payments to platforms that control where USDC is held and how it is used. Coinbase is the clearest example. In 2021 and 2022, stablecoins were treated primarily as infrastructure and were not disclosed as a distinct revenue driver. By 2023, Coinbase began explicitly identifying stablecoins and USDC-related activity as a meaningful contributor to its subscription and services revenue, driven by rewards programs, payments usage, and balance retention.

That monetization accelerated through 2025. Stablecoin revenue increased from $297.5M in Q1 2025 to $332.5M in Q2 2025 and $354.7M in Q3 2025, totaling $984.7M over the first three quarters of the year. Quarter-on-quarter growth remained positive throughout the period, reflecting expanding usage across rewards, payments, and treasury-related products. Over the same period, Circle’s issuer retention under its distribution agreements remained measured in basis points.

Industry structure is moving in the same direction. Issuance is becoming easier and more modular, while differentiation concentrates in layers that manage usage. Stablecoin-as-a-service providers such as Paxos, Brale, Stably, and Agora abstract issuance for enterprises. Payment and API platforms such as Stripe, Shopify, and MoneyGram integrate stablecoins directly into existing commerce flows. Orchestration layers including Bridge, BVNK, and ZeroHash route payments, manage compliance, and connect stablecoins to banks and wallets.

Circle remains central to the stablecoin ecosystem, with scale, trust, and regulatory standing. At the same time, its financials show that issuance alone no longer guarantees margin expansion. Control over usage increasingly determines who captures value.

If issuer leverage is weakening, the obvious response is to move closer to usage.

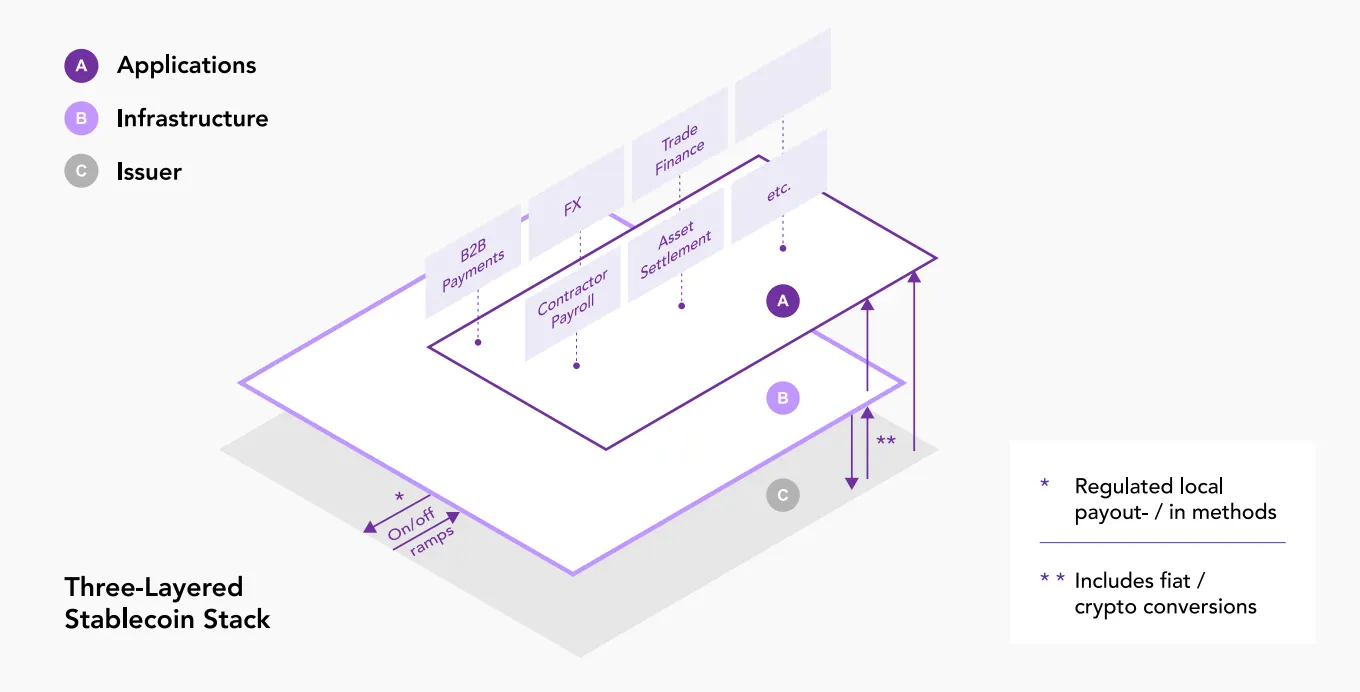

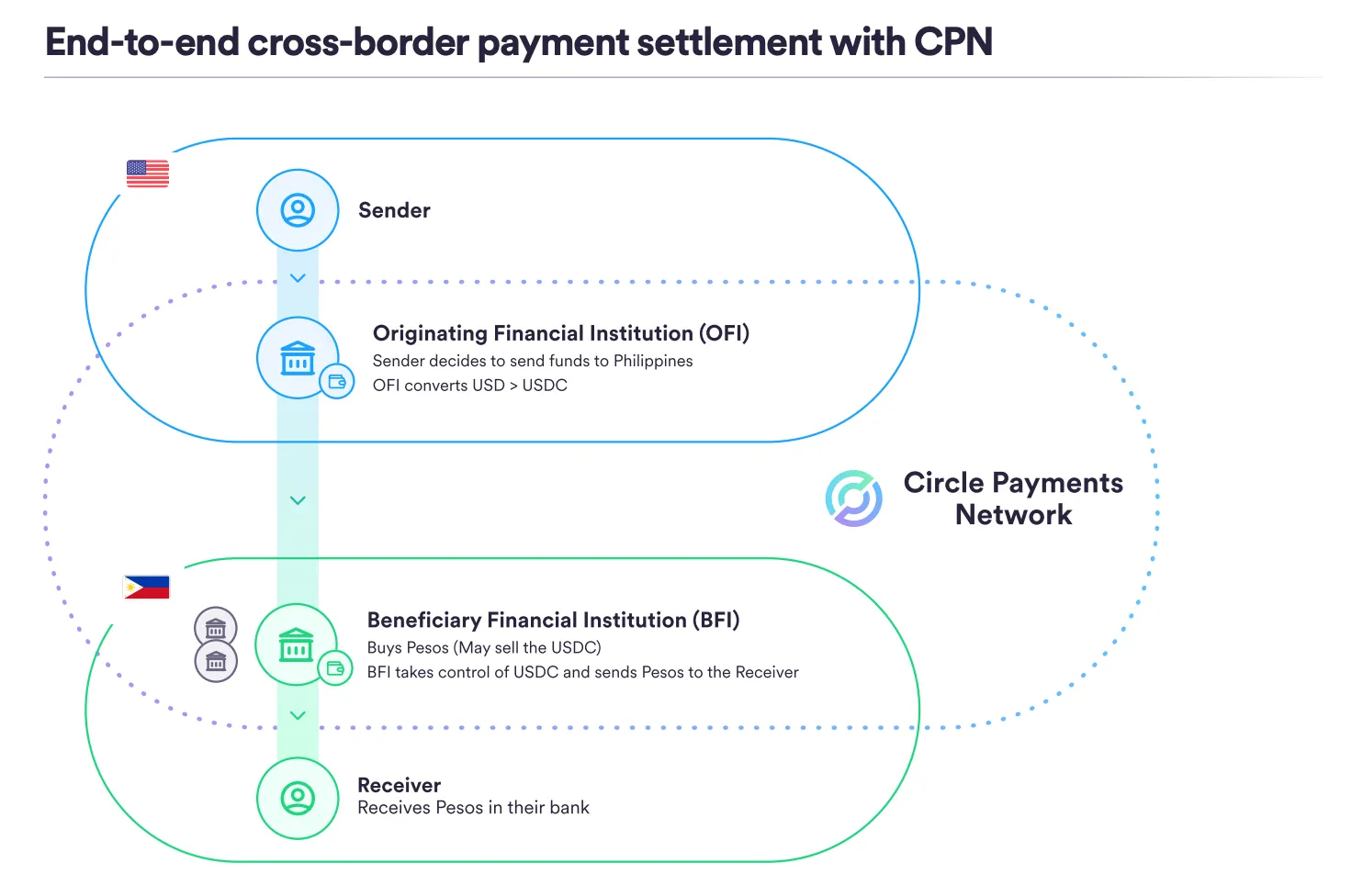

Circle’s answer is Circle Payments Network (CPN). CPN is a global network of partners, including banks, payment service providers (PSPs), virtual asset service providers (VASPs), and enterprises, who enable consumer, business, and institutional payments with 24/7 real-time settlement via stablecoins like USDC and EURC.

Source: Circle Payments Network Whitepaper

Thus CPN is not a consumer payments app and it is not a replacement for banks. It does not custody funds and it does not sit in the flow of money. Instead, it coordinates how stablecoin payments are routed, settled, and reconciled across financial institutions.

At a practical level, CPN provides three things Circle does not get from issuance alone:

It provides counterparty discovery. Financial institutions can find each other inside a shared framework rather than negotiating bespoke bilateral integrations. Originating institutions and beneficiary institutions interact through a common set of rules.

It provides compliance orchestration. AML, sanctions screening, and Travel Rule data are handled at the network level. That matters because compliance is one of the main frictions preventing stablecoins from being used outside crypto-native environments.

It provides routing and orchestration. Payments, FX conversions, and cross-border flows can be coordinated across multiple blockchains and fiat rails without each institution needing to build custom logic.

Source: Circle Payments Network Whitepaper

The closest analogies are SWIFT for coordination and CLS for FX settlement logic. Circle consistently describes CPN as a platform for upgrading payments, emphasizing partner onboarding, corridor expansion, and institutional adoption. Its value lies in shaping how stablecoins are used across payments, treasury, and enterprise workflows, rather than in generating meaningful fees in the near term.

By mid-2025, CPN had launched multiple live payment corridors and reported over 100 additional partners in the pipeline. The specific corridors matter less than the direction. Circle is inserting itself into the payment workflow rather than remaining upstream as a balance-sheet provider.

At the same time, CPN has a clear limitation. It still settles on other people’s rails. Today, final settlement occurs on public blockchains and through existing payment infrastructure. That means Circle does not control finality, latency, or fee behavior at the point where value actually moves. Those properties are inherited from the underlying chains and systems.

That gap explains why CPN alone is not sufficient as a response to weakening issuer leverage. It also sets up the role of Arc in the broader strategy.

Circle’s decision to build Arc looks unnecessary if viewed through the lens of blockchain competition. L1s like Ethereum, Solana, Tron, Plasma and other L2s already support stablecoins at scale. Settlement is fast, liquidity is deep, and institutional tooling continues to improve. From that perspective, adding another chain appears redundant.

But the problem is not access to settlement infrastructure. It is the lack of control over settlement conditions in a business where leverage is already moving away from the issuer. As USDC usage expands into payments, treasury, and enterprise workflows, finality, fee predictability, timing certainty, and accountability become technical concerns because they determine whether stablecoins can replace existing financial rails in regulated contexts.

CPN allows Circle to influence how stablecoin flows are coordinated across institutions. Today, settlement inherits the properties of the underlying chain or rail. Fee behavior, congestion, reorg risk, and governance decisions sit outside Circle’s control. For many use cases, that tradeoff is acceptable. For others, particularly large-value payments and institutional flows, it introduces uncertainty that traditional financial systems are explicitly designed to avoid.

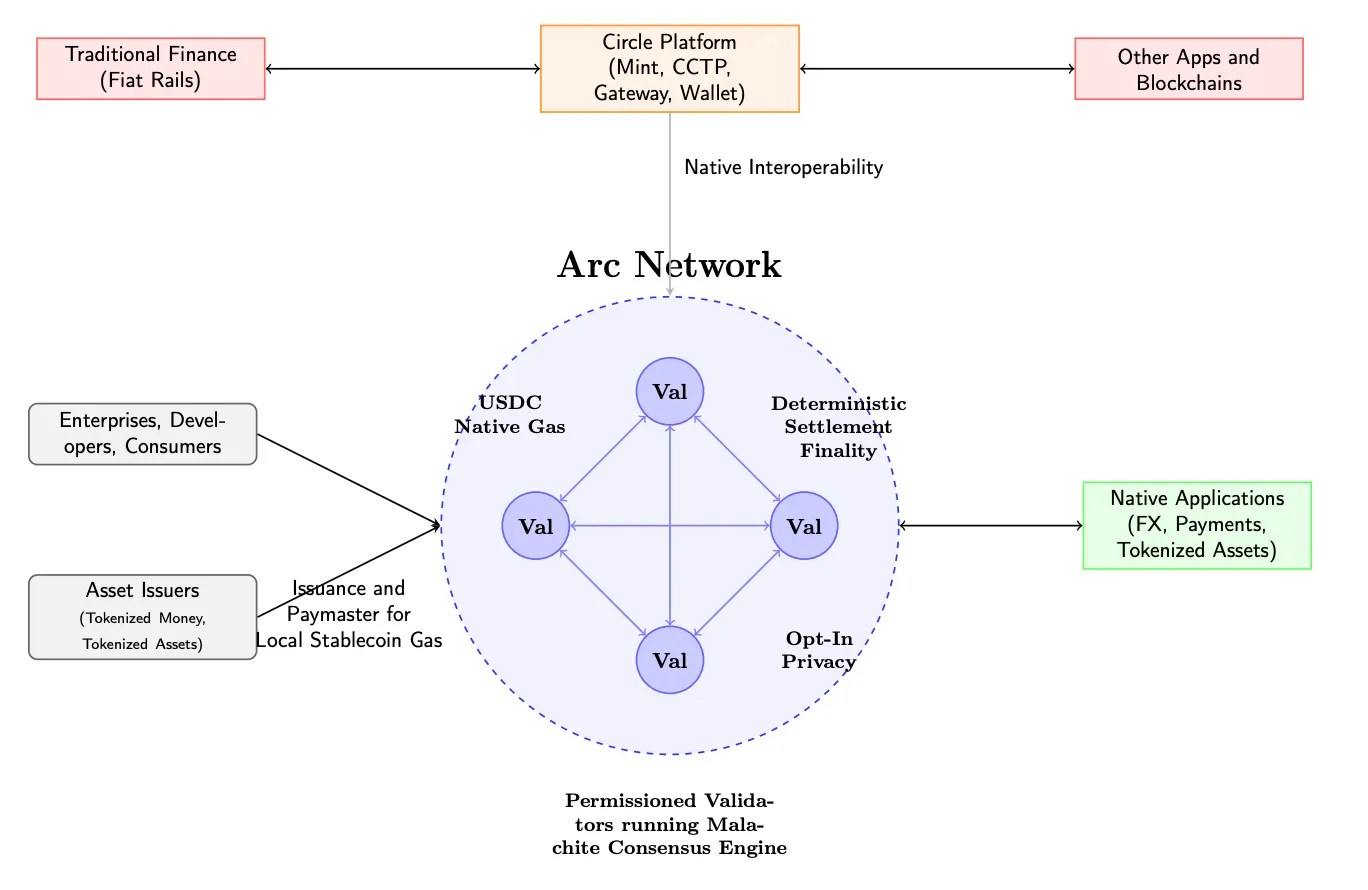

Arc is Circle’s attempt to address this problem. Arc is designed to provide a controlled settlement environment for flows that require determinism and accountability. Deterministic finality removes ambiguity around settlement completion. Stable, dollar-denominated fees reduce operational uncertainty for enterprises. A permissioned validator set introduces identifiable operators and governance rather than maximum openness. Privacy is implemented as a compliance feature.

Source: Arc Litepaper

None of these features are unique in isolation. Similar capabilities exist elsewhere. What differentiates Arc is that these properties are bundled into a settlement environment operated by the same entity that issues USDC, manages reserves, and coordinates payment flows through CPN. That integration matters because it allows Circle to offer institutions a consistent set of guarantees across issuance, routing, and settlement.

Arc does not need to handle the majority of USDC volume to serve its purpose. Most retail and crypto-native activity can continue to settle on existing chains.

Arc’s role is narrower. It gives Circle a place to route flows where settlement certainty is a requirement and provides Circle leverage in negotiations with distributors and counterparties by removing absolute dependence on third-party rails.

Source: Circle 3Q 2025 Earnings Presentation

The risk is that Arc sees limited adoption. Institutions may decide that existing settlement infrastructure is sufficient. In that case, Arc remains a lightly used component of Circle’s stack.

But the more important risk is the alternative. Without any settlement layer it controls, Circle’s role becomes structurally confined to issuance and compliance. In a market where usage and distribution increasingly determine economics, that is a position with limited long-term leverage.

For $CRCL stockholders, the core question is whether these initiatives can slow or reverse the drift of value away from the issuer and toward distributors.

Circle’s recent financials provide a useful baseline. Across recent quarters, revenue and reserve income scale with USDC circulation, but retained margins do not expand proportionally as seen in section 1.

Distribution and transaction costs absorb a growing share of gross economics, and RLDC margins fluctuate based on platform mix rather than improving with size. This makes Circle increasingly sensitive to the behavior of large distributors and partners, particularly those that control end-user balances and payment interfaces.

In that context, CPN and Arc should be viewed as tools to reshape Circle’s bargaining position rather than as standalone profit centers. CPN gives Circle a role in the coordination layer of stablecoin usage. By sitting closer to payment routing, counterparty discovery, and compliance workflows, Circle increases its relevance in transactions that extend beyond simple issuance and redemption. Even if CPN fees remain modest, the network creates a surface where Circle can influence standards and reduce reliance on bilateral agreements with dominant distributors.

Arc addresses a different part of the problem. Settlement is where economic leverage ultimately resolves. As long as Circle depends entirely on external rails for finality, it remains exposed to changes in fee structures, governance decisions, and technical constraints it does not control. Arc provides Circle with an internal settlement option for flows where certainty and accountability matter more than neutrality or liquidity depth.

That option does not need to dominate volume to be valuable. Its existence alone changes the negotiation dynamics with partners who would otherwise assume Circle has no alternative.

From an equity perspective, the upside of this strategy is incremental. There is no credible path where Arc meaningfully displaces existing public chains or where CPN becomes a high-margin payments network in the near term.

The more realistic benefit is stabilization. If Circle can modestly increase the share of activity routed through infrastructure it controls, it can reduce margin volatility and slow the erosion of issuer economics as USDC usage grows.

CPN and Arc should be understood as strategic necessities to reposition Circle within the stablecoin stack rather than as standalone growth bets. They are tools designed to prevent Circle from being locked into a subordinate position in the stablecoin economy.

Without any effort to move up the stack, Circle’s role narrows over time. Issuance becomes a low-leverage function, and value concentrate at the distribution layer. Margins remain volatile as usage grows.

Viewed through that perspective, CPN and Arc is more about preserving long-term leverage. They reflect Circle’s recognition that issance alone is no longer sufficient, and that control over usage increasingly determines economic outcomes.

Dive into 'Narratives' that will be important in the next year