Approximately six months have passed since the election of a president who has been a strong proponent of Korean won (KRW) stablecoins. However, South Korea still lags significantly behind other Asian jurisdictions such as Hong Kong, Singapore, and Japan in terms of legislation and industry development related to stablecoins.

One of the primary reasons is that regulators, financial institutions, and companies view KRW stablecoins with more concern than optimism—focusing on regulatory burdens, governance issues, and demand uncertainty rather than potential benefits. Yet, when viewing stablecoins through the lens of financial-infrastructure evolution, the migration of traditional infrastructure to blockchain is an inevitable future. In preparing for that future, KRW stablecoins are not a matter of choice but a matter of survival.

That said, because the nature of the Korean won is very different from the U.S. dollar, there are many regulatory and industrial barriers to success. Accordingly, this article proposes eight conditions necessary for KRW stablecoins to succeed.

It has now been nearly six months since the inauguration of the new President, Lee Jae‑myung, in South Korea. Even prior to his election, President Lee strongly advocated for the rapid introduction of a KRW stablecoin, stating that delaying its progress would be akin to the isolationist policies of the late Joseon Dynasty.

Despite this strong support, progress on the KRW stablecoin front remains slow when compared to other Asian countries:

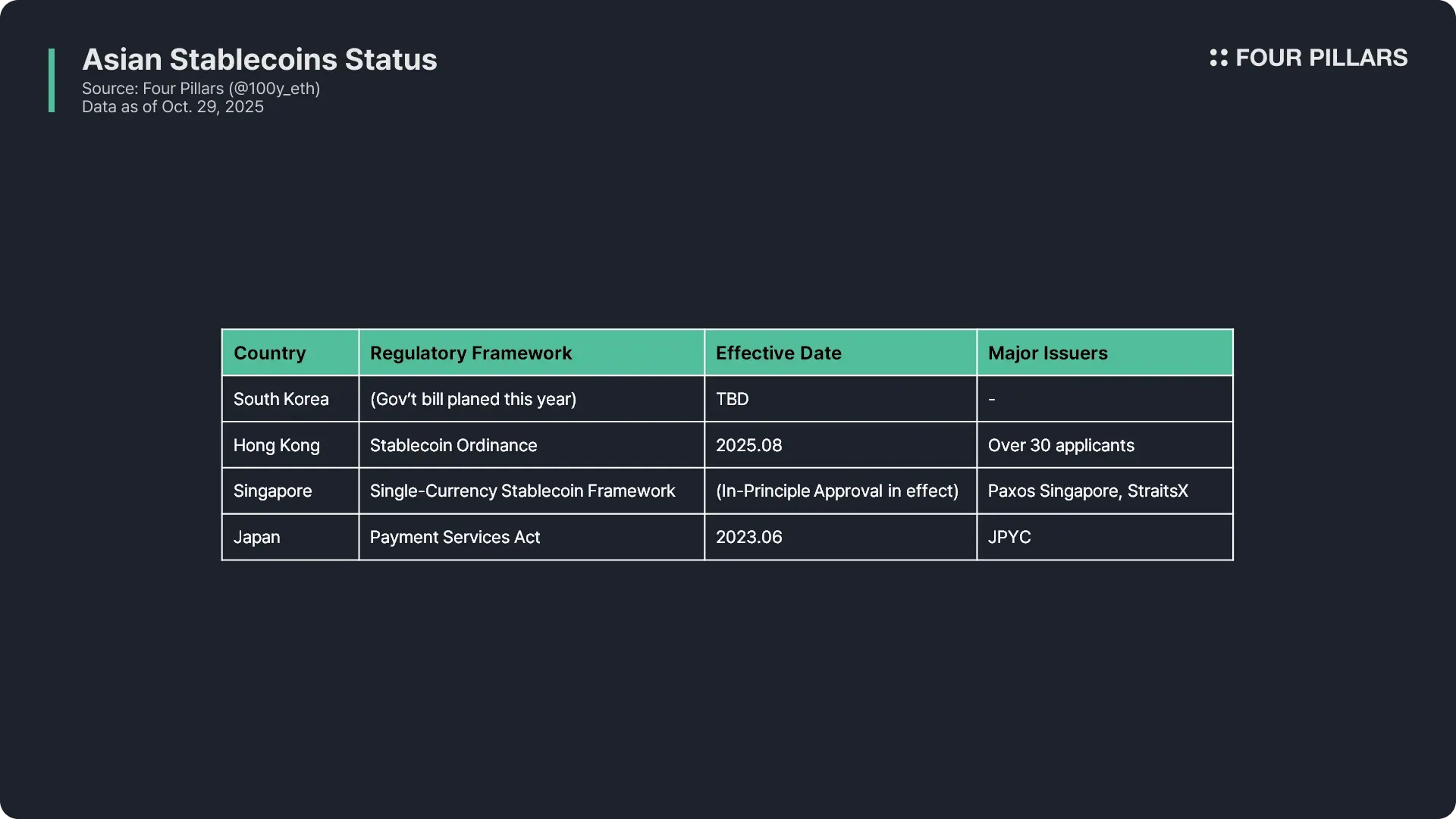

Japan: In June 2023, the revised Payment Services Act (PSA) came into force, and in August 2025, JPYC Inc. obtained an issuance licence for the first Japanese-yen stablecoin. The coin, named JPYC, was issued on October 27 across the Ethereum, Avalanche, and Polygon networks with ¥400 million each.

Hong Kong: In May 2025, the legislature passed the Stablecoin Ordinance and in August 2025 a licensing regime for stablecoin issuers came into effect. By the end of September, 36 formal licence applications had been submitted.

Singapore: The Monetary Authority of Singapore (MAS) announced in August 2023 the “Single-Currency Stablecoin Framework” regulating single-currency stablecoins. Although final details are still unfolding, firms such as StratisX and Paxos Singapore have obtained in-principle approvals (IPA) from MAS and initiated business plans.

In contrast, South Korea has seen six bills related to stablecoins introduced in the National Assembly by both the ruling Democratic Party of Korea and the opposition People Power Party. The Financial Services Commission (FSC) is expected to submit its own regulatory framework bill within the year. This means that, at present, no stablecoin legislation has yet been enacted in Korea.

In practice, this legislative vacuum means that financial institutions and corporations in South Korea are still largely in the pre-research or proof-of-concept phase regarding KRW stablecoin projects. The expectation is that a government-proposed bill — as opposed to a legislator-proposed bill — has a higher likelihood of passing, but even that proposed bill remains unpublished in draft form.

As a result, the KRW stablecoin initiative in Korea remains largely dormant, especially when compared to the more advanced trajectories seen in neighbouring jurisdictions.

In my view, one of the major reasons the development of a KRW stablecoin has been slow is that regulators, financial institutions, and corporations are not particularly optimistic about the idea. This hesitancy is largely due to the fact that, unlike the U.S. dollar, the Korean won faces numerous regulatory and industrial constraints when issued as a stablecoin. To date, regulators, financial institutions, and businesses have asked me the following kinds of questions:

One of the key advantages of stablecoins is that they remove cross-border constraints. Given that South Korea has strict foreign exchange regulations, doesn’t that diminish the benefit of a stablecoin?

In the digital world, demand tends to favor the U.S. dollar — is there real demand for the Korean won in this context?

If a KRW stablecoin is issued, isn’t it essentially confined to domestic usage anyway?

Since Korea is already a financially advanced country, would the introduction of a KRW stablecoin lead to meaningful improvements in user experience?

If a KRW stablecoin is adopted, how would it improve upon existing services?

Aren’t stablecoins primarily a strategic tool in the U.S. (for example under Donald Trump) for reducing national debt? Does Korea need to follow the U.S.’s path?

If a stablecoin is used on a public network, wouldn’t citizens’ financial information be fully exposed?

All of these questions raise valid points and have some merit. However, in my opinion, adopting a defensive and conservative stance toward a KRW stablecoin simply because of these questions is the wrong approach.

1.3.1 South Korea

Source: KB

There are two main reasons why Koreans today can conduct various financial activities safely and conveniently. The first is the presence of multiple public intermediary institutions such as the Bank of Korea, the Korea Financial Telecommunications and Clearings Institute (KFTC), and the Korea Securities Depository (KSD). The second is the existence of the numerous payment and settlement systems managed by these entities, which together form the backbone of Korea’s financial infrastructure.

In Korea, financial infrastructure can be broadly categorized based on the purpose of payment or settlement into:

retail payment systems,

large-value payment systems,

securities settlement systems, and

foreign exchange settlement systems.

Within the retail payment system alone, there are multiple sub-networks designed for different purposes, such as the Electronic Banking System, Interbank Transfer System, Cash Dispenser (CD) Network, Giro System, and Open Banking Network.

Most of these infrastructures were established during the 1980s and 1990s. Before that, cash was the primary means of payment between individuals and corporations. In the case of stock trading, transactions were conducted through the physical delivery of paper certificates and cash payments, a highly inconvenient and inefficient process.

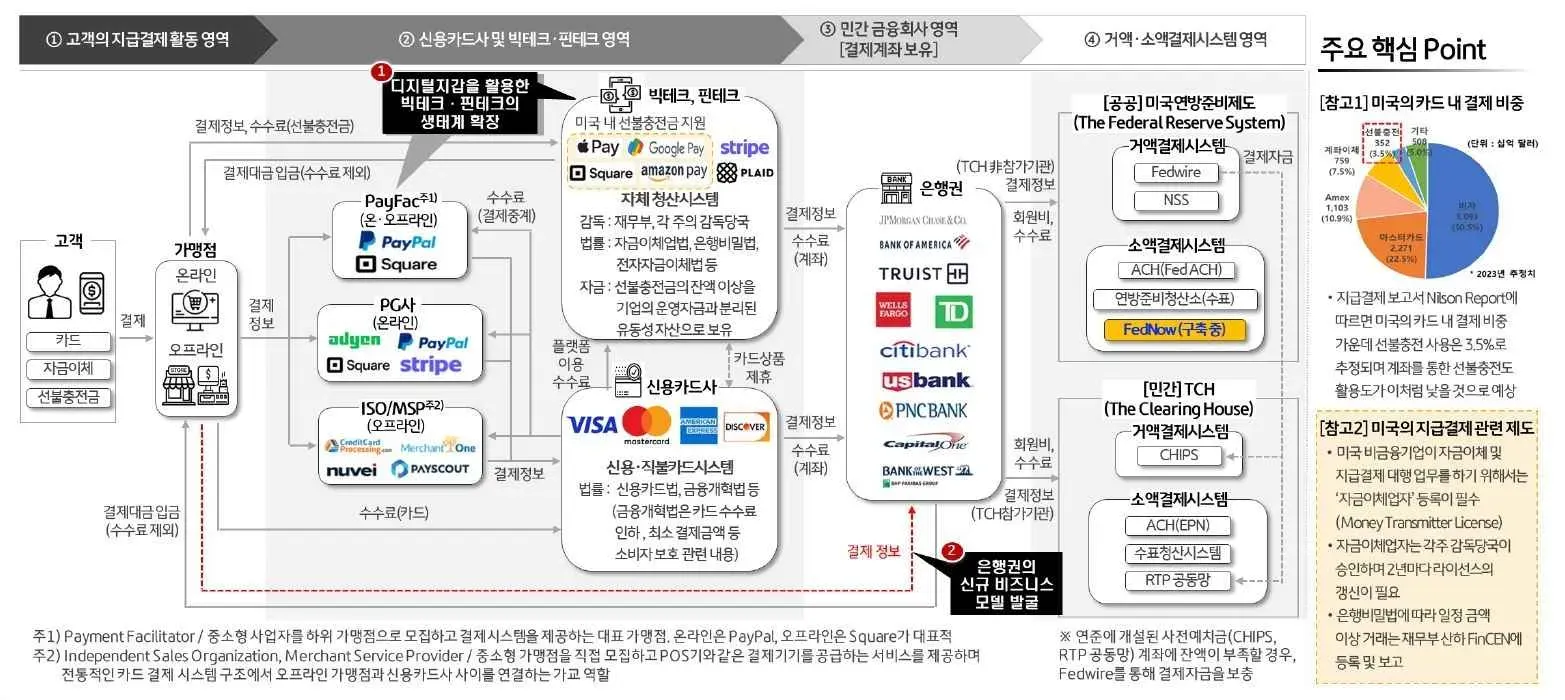

1.3.2 United States

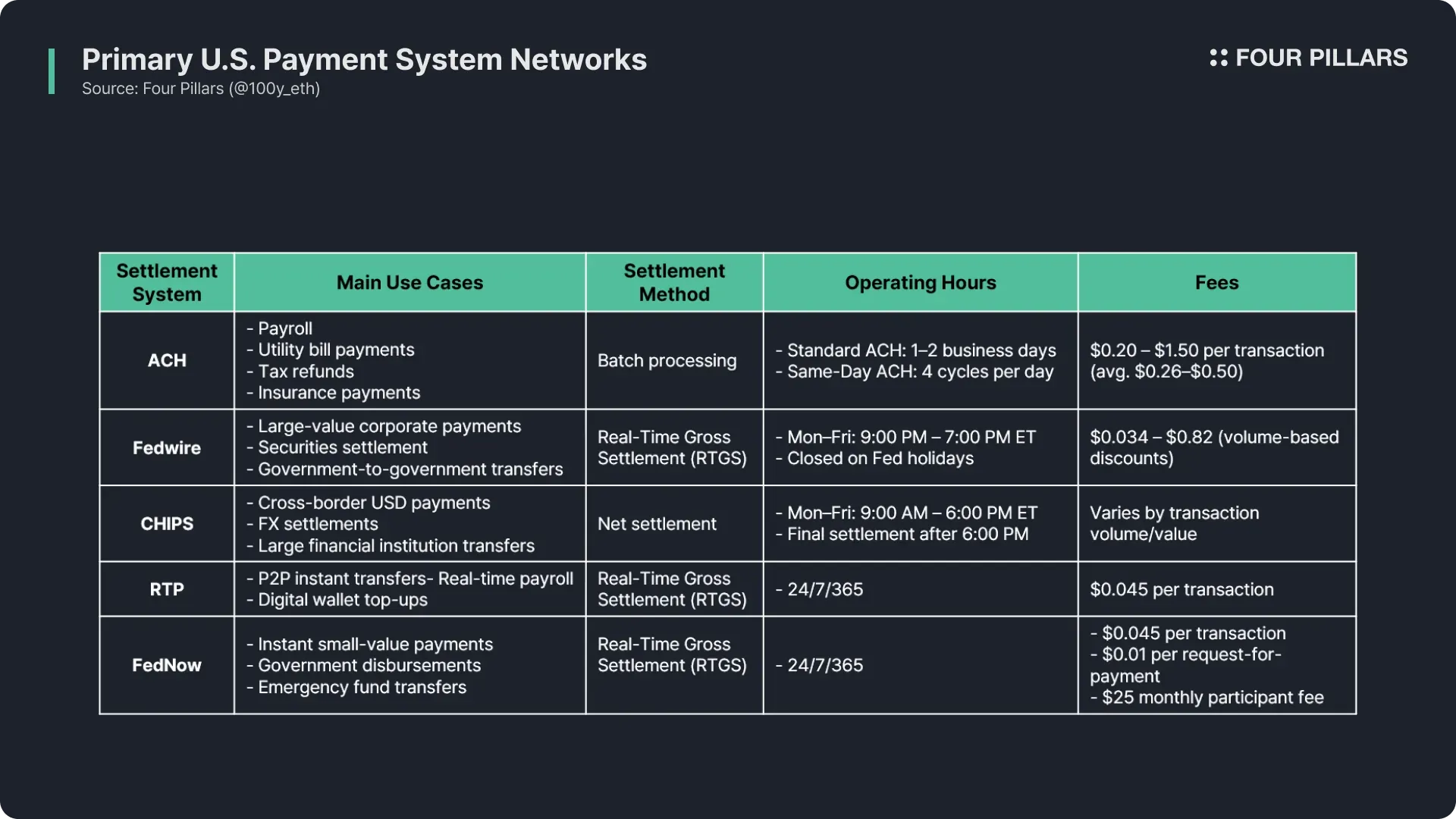

The same applies to the United States. Depending on the purpose of payment or settlement, there exist numerous financial networks such as Fedwire, CHIPS, ACH, and FedNow. For securities transactions, institutions such as the National Securities Clearing Corporation (NSCC) and the Depository Trust Company (DTC) serve as intermediaries that maintain the financial infrastructure.

1.3.3 Are Our Financial Infrastructures Outdated?

Today, people have easy access to a wide range of financial services, which gives the illusion that the financial backend is robust and modern. In reality, this accessibility is largely due to fintech companies that have abstracted the complexity of the backend systems and presented users with intuitive front-end interfaces. The underlying financial infrastructure, however, is decades old, deeply complex, and remarkably inefficient.

The major problems with today’s financial infrastructure can be summarized as follows:

Inefficiency caused by outdated infrastructure

Inefficiency resulting from excessive intermediaries

Fragmentation of financial assets and transactions

Barriers created by national borders

Blockchain technology offers a solution that can address these issues simultaneously, representing a potential paradigm shift for the modernization of financial infrastructure.

1.4.1 The Shift of Traditional Financial Infrastructure Toward Blockchain

Regardless of whether one views stablecoins positively or negatively, from the perspective of financial infrastructure development, there is a clear trend toward blockchain technology supplementing or even replacing legacy systems. Several movements illustrate this transition:

Tokenization of Real-World Assets (RWA): Global asset managers such as BlackRock and Franklin Templeton are actively exploring RWA tokenization. Companies like Securitize are already providing tokenization services across multiple asset classes in full compliance with financial regulations.

Stock Tokenization (Corporate Initiatives): Companies such as Robinhood and Kraken are offering tokenized stock trading services, while others like Coinbase are preparing to launch similar platforms.

Stock Tokenization (Infrastructure Level): Recently, Nasdaq submitted a rule change proposal to the U.S. Securities and Exchange Commission (SEC) that would allow tokenized securities to be traded within existing exchange systems. The Depository Trust and Clearing Corporation (DTCC), which handles securities clearing and settlement in the United States, continues to test and deploy blockchain-based infrastructure.

Interbank Settlement: Since 2019, JPMorgan has provided efficient wholesale payment services between clients through the DLT-based JPM Coin on its Kinexys platform. Numerous financial institutions are now testing and adopting blockchain-based interbank settlement systems through initiatives such as Circle CPN and Project Pax.

Global Remittance: Companies including Venmo, MoneyGram, and Bitso are offering blockchain-based cross-border remittance services. Even traditional infrastructures like SWIFT are conducting various blockchain pilot programs.

Payments: Major payment companies such as Visa, Mastercard, Stripe, and PayPal are actively adopting blockchain and stablecoins for payments.

“Crypto and the Evolution of the Capital Markets”: In their paper, Tuongvy Le and Austin Campbell argued that if blockchain systems had existed earlier, today’s complex securities infrastructure would not have developed in its current form.

1.4.2 Stablecoins Are a Means, Not an End

The advantages that blockchain can bring over legacy financial systems are clear: trust and accessibility.

Blockchain enables transactions to be conducted with fewer intermediaries and without the constraints of borders, making it possible to manage all types of financial assets and activities on a single network. This could include deposits, stocks, funds, card payments, reward points, and remittances — all processed within one unified backend.

If, in the future, much of the financial infrastructure transitions to blockchain, there will inevitably be a need for a form of “money” that can operate within that environment. The entity that fulfills this role on the blockchain is the stablecoin.

In South Korea, there is a tendency to focus excessively on the issuance and management of stablecoins, often treating the KRW stablecoin as an end goal in itself. However, from the perspective of financial infrastructure evolution, stablecoins should be regarded as a means to an end — a tool that enables the modernization and integration of financial systems.

The KRW stablecoin is not a matter of choice but of survival. If South Korea continues to approach the issue conservatively, focusing solely on issuance and regulation, the country risks losing its competitiveness in the rapidly advancing global blockchain industry.

Up to this point, we have examined why the KRW stablecoin should be introduced. In this section, I present an opinion on how it can be implemented successfully.

South Korea possesses several favorable conditions to become a global leader in blockchain innovation. The population has a high level of digital literacy, and a large portion of citizens have had some exposure to blockchain or cryptocurrency in one form or another. While speculative activity is often viewed negatively in Korean society, a moderate level of speculation can actually energize an industry and serve as a catalyst for long-term growth. Moreover, Korean blockchain developers are globally competitive in both skill and innovation.

However, one of the main reasons why Korea’s blockchain industry, including stablecoins, remains largely speculative rather than innovative is its regulatory environment. When comparing countries where the blockchain sector thrives with those where it does not, regulation is the key differentiator. In Japan, India, and several European countries, stringent regulations have made it difficult for blockchain industries to flourish. As a result, capable teams frequently relocate to more favorable jurisdictions such as the United States, Hong Kong, Singapore, Malaysia, or the United Arab Emirates, where they can establish and build their businesses.

Another issue is the limited understanding and often conservative attitude of Korean regulators and policymakers toward blockchain technology. In the United States, for instance, the White House has led a Crypto Working Group to set strategic directions for industry growth. The Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC) have responded promptly with corresponding initiatives, demonstrating strong institutional understanding and policy agility. Furthermore, many prominent U.S. policymakers and regulators, including Cynthia Lummis, Gary Gensler, Paul Atkins, and Hester Peirce, possess a deep comprehension of the crypto sector.

As Korean regulators and especially members of the National Assembly work to establish critical regulatory frameworks for blockchain and stablecoins, it is essential that they approach the topic with genuine understanding rather than as a political tool to gain public support. Properly designed regulation will be key to nurturing a healthy and globally competitive ecosystem for the KRW stablecoin.

For stablecoins, utilization is more important than issuance. The broader the range of use cases, the greater the demand for issuance. One of the most crucial factors for the widespread adoption of stablecoins is providing issuers with appropriate incentives.

Tether and Circle, the issuers of USDT and USDC respectively, generate substantial revenue through large-scale collateral assets such as U.S. Treasury bills and repurchase agreements (repos). These profits, in turn, enable them to expand use cases and partnerships. Without returns from their collateral, their growth would have been far more limited.

In contrast, the situation in Korea is quite different. The Bank of Korea advocates for a deposit-based model for the KRW stablecoin. It is important to clarify that such deposits would not be interest-bearing or loaned out; they would be fully backed by cash reserves held in custody. In the United States, some stablecoin issuers hold a portion of their collateral as cash deposits, while in Europe, regulations require a significant portion of reserves to be maintained in deposits. However, because these are fully reserved accounts, they generate minimal income.

If a KRW stablecoin were to adopt a similar deposit-centric model, the issuer would have little incentive to expand issuance, which could also limit its utility and adoption. Therefore, Korea should, like the United States, Hong Kong, Singapore, and parts of Europe, permit the use of highly liquid financial instruments such as short-term government bonds and repos as collateral to enable yield generation.

Another important consideration is whether the Korean short-term bond market is large enough to support such collateralization. Unlike the United States, Korea’s short-term bond market is relatively small. Consequently, it may be prudent to consider other high-quality foreign assets, such as U.S. Treasury securities, as part of the collateral base. Hong Kong provides an instructive example: although the Hong Kong dollar (HKD) is nearly pegged to the U.S. dollar, issuers are allowed to hold USD-denominated assets such as U.S. Treasuries as part of their stablecoin reserves.

As emphasized in a previous article, cryptocurrency exchanges play a crucial role in the early growth of any stablecoin. USDT’s success was largely due to its early adoption by exchanges like Bitfinex, while USDC continues to maintain close partnerships and revenue-sharing agreements with major platforms such as Coinbase and Bybit to secure exchange-based use cases.

The stablecoin market is a battle of scale. Sustained utility requires maintaining a large supply, and the only practical way to achieve rapid issuance growth in a short time frame is through adoption by major cryptocurrency exchanges.

South Korea is one of the most active crypto trading markets in the world. Even partial integration of a KRW stablecoin across the nation’s top five exchanges could make it the second-largest stablecoin globally, after the U.S. dollar-based ones.

In this regard, the potential alliance between Dunamu (operator of Upbit) and Naver represents one of the strongest candidates for success. If these two companies were to issue a KRW stablecoin together, they could secure initial issuance worth several trillion won through Upbit while leveraging Naver’s ecosystem to build a large-scale network of KRW stablecoin use cases across digital payments, commerce, and financial services.

In the Korean market, there is still little recognition of the need to issue the KRW stablecoin on a public blockchain. Even when issuance is considered, there are frequent questions as to why Ethereum should be the preferred choice. In reality, none of the major global stablecoins exist outside the Ethereum ecosystem. Even Japan’s recently launched JPYC was issued on the Ethereum network.

If Korea allows the issuance of a KRW stablecoin on a public network, Ethereum should be the essential choice when considering its security scale, liquidity depth, system stability, and degree of decentralization. For a more detailed discussion, refer to this previous article.

According to Korea’s STO (Security Token Offering) guidelines, distributed ledger systems must consist of at least 51 percent public or financial institutions. In effect, this means that the use of private networks is being encouraged.

Likewise, once the KRW stablecoin is legalized, there is a strong likelihood that its issuance will be restricted to private networks. The Bank of Korea, for example, has already expressed strong support for private-network-based implementations.

If the KRW stablecoin is initially limited to private networks, it would retain some advantages of blockchain technology—such as 24/7 operation, instant settlement, and the use of smart contracts. However, its accessibility to global liquidity and its utility in international markets would remain severely constrained.

The ideal case would therefore be the use of a public blockchain. Nevertheless, even if the issuance of the KRW stablecoin is mandated to occur on a private network, there remains one viable model that could still support moderate growth of the ecosystem: the establishment of a single, unified Korean private blockchain that hosts all financial assets and services.

The worst-case scenario would be multiple institutions developing and launching their own separate private networks. Such fragmentation would essentially recreate the inefficiencies of the legacy financial system. To realize even the basic advantages of blockchain, there must be only one unified private blockchain, supporting all types of financial activities—such as remittances, savings, loans, securities trading, and loyalty points. Even this level of integration would achieve a key benefit of blockchain technology: the unification and efficiency improvement of complex legacy financial infrastructure.

Stablecoins enable use cases that traditional financial systems cannot easily support, such as micropayments and AI agent-based transactions. Unlike card networks that rely on fixed transaction fees, blockchain allows transactions with minimal costs, even at second-level intervals. This capability makes microtransactions economically viable, paving the way for a new subscription-based microeconomy.

For example, KRW stablecoins could be adopted in usage-based billing models for K-content streaming services or fan engagement platforms for K-pop idols, where payments are tied to individual interactions or content consumption.

Moreover, stablecoins are becoming essential infrastructure for payments between AI agents. Coinbase recently introduced the x402 standard, a stablecoin-based protocol that allows AI agents to pay for online resources without creating complex accounts, verifying identities, or managing API keys. Major technology companies such as Cloudflare, Google, AWS, and Anthropic have already begun implementing this model.

As AI agent-based economies and commerce evolve, it is likely that many agents will pay for Korean-based services, data, or APIs. Accepting KRW stablecoins for such transactions would naturally create new demand for the currency in the digital ecosystem.

Why are Koreans able to transfer money so seamlessly between different banks? The answer lies in the daily clearing and settlement process that takes place near midnight. For example, KRW deposited in Shinhan Bank can be viewed as ShinhanKRW, while KRW in Nonghyup Bank can be seen as NonghyupKRW. When funds are transferred from Shinhan to Nonghyup, it effectively represents a 1:1 exchange between ShinhanKRW and NonghyupKRW. The reason this parity is maintained is because banks settle their accounts with one another every night.

The same logic applies to stablecoins. Once KRW stablecoins are legalized, there will likely be numerous issuers. Already, dozens of companies have filed for trademarks or licenses related to KRW stablecoin issuance. As multiple versions of KRW stablecoins emerge, liquidity fragmentation could occur, necessitating a mechanism to guarantee 1:1 parity and redemption between them.

While such conversions could theoretically occur through exchange order books or on-chain automated market makers (AMMs), these mechanisms are vulnerable to slippage and liquidity shortages, meaning they cannot ensure stable 1:1 exchange rates. Therefore, a clearing and settlement infrastructure dedicated to stablecoins will be essential.

A notable international example is Ubyx, a startup that connects multiple issuers and financial institutions, enabling stablecoins to be redeemed and settled at nominal value. The company has attracted investments from leading firms such as Galaxy Digital, Coinbase Ventures, Founders Fund, Paxos, and VanEck.

However, given the enormous liquidity required for such a system, it would be more appropriate for this function to be managed by a public institution or a jointly owned subsidiary of major commercial banks, rather than by a private company. This approach would provide greater regulatory oversight and stability.

Humanity is entering a critical transition period in the evolution of financial infrastructure. Considering the trajectory of technological development, the gradual transformation of legacy financial systems into blockchain-based infrastructure is only just beginning, and stablecoins serve as the foundation for this financial future.

Thus, the question “Can the KRW stablecoin succeed?” is fundamentally misplaced. The current approach in Korea—viewing the KRW stablecoin as something that may fail and therefore must be introduced cautiously—is flawed. The proper question should be how to introduce it effectively, not whether to introduce it at all.

Although Korea currently lags behind neighboring countries, it still has significant potential for growth in the blockchain industry. With the establishment of a sound regulatory environment, successful implementation, and the expansion of practical use cases, Korea can once again position itself as a leading global financial power in the digital era.

Dive into 'Narratives' that will be important in the next year