Imagine what would’ve happened if Google had partnered with Coinbase to launch stablecoin

As seen in the cases of USDT and USDC, support as a quote currency on exchanges is a highly effective strategy for the early growth of a stablecoin.

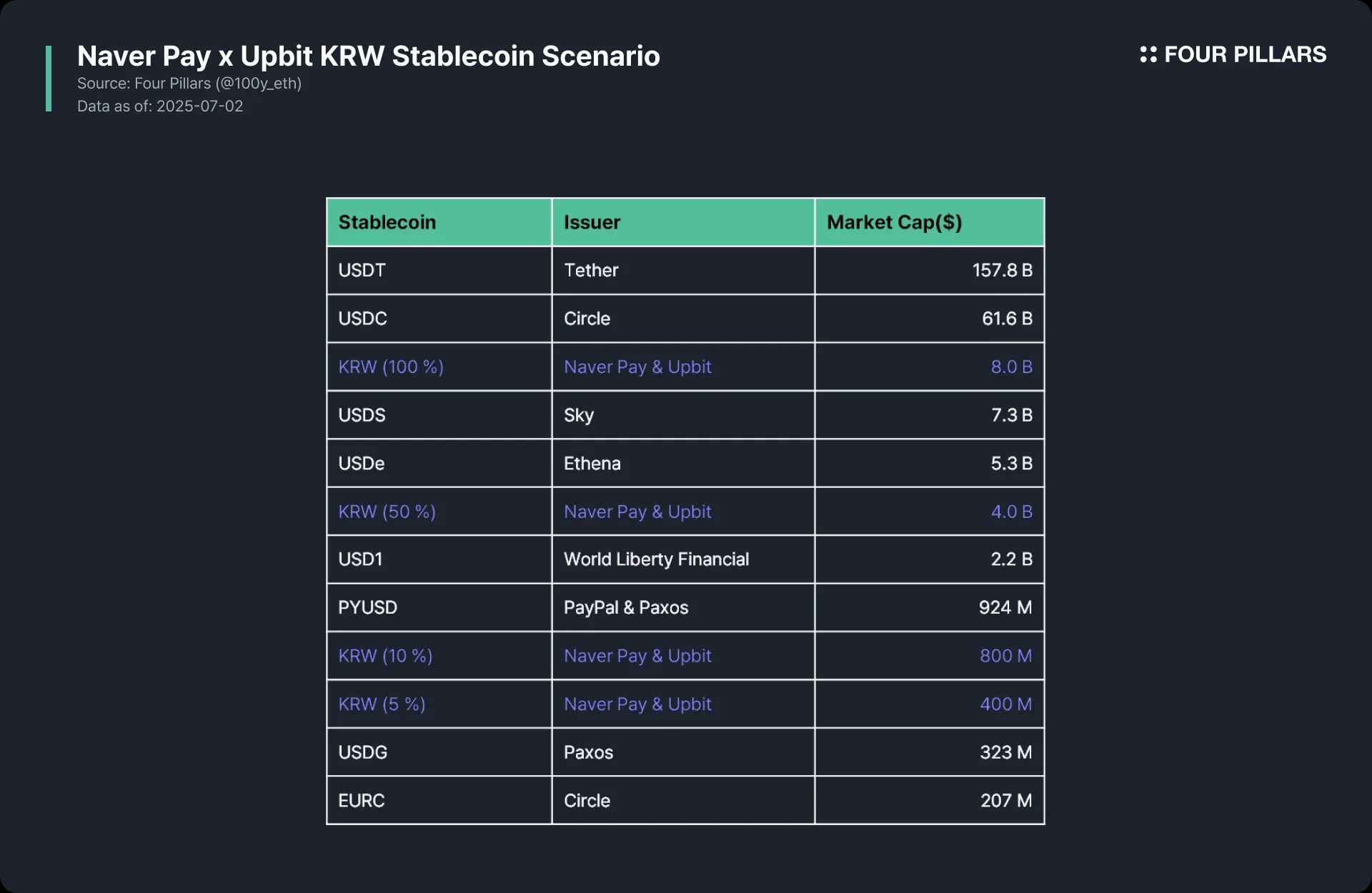

Naver Pay, the leading player in Korea’s simple payment market, and Upbit, the top crypto exchange in Korea, recently announced that they are pursuing a stablecoin issuance business through a consortium.

Based on customer deposit volumes of Upbit and Naver Pay, even if only about 5 percent is converted into KRW stablecoins, KRW has the potential to become the second-largest stablecoin in the world after the US dollar.

On July 1, 2025, there was significant news in Korea’s KRW stablecoin landscape. Upbit announced a partnership with Naver Pay to enter the KRW stablecoin business. This meant that Korea’s top crypto exchange and the no.1 domestic payment platform would collaborate to issue a stablecoin.

Recently in Korea, various initiatives have emerged in the stablecoin space. Eight commercial banks are forming a consortium to issue stablecoins, and fintech companies and card issuers like Kakao Pay, Kakao Bank, and Shinhan Card have applied for trademarks related to stablecoin names. This shows growing interest in stablecoins among banks, financial institutions, and corporations.

In other words, the Korean market currently anticipates the issuance of various KRW stablecoins by multiple issuers. However, the author believes that if Naver Pay and Upbit indeed move forward with launching a stablecoin together, they are highly likely to dominate the KRW stablecoin market.

1.2.1 Exchange Support Was Key

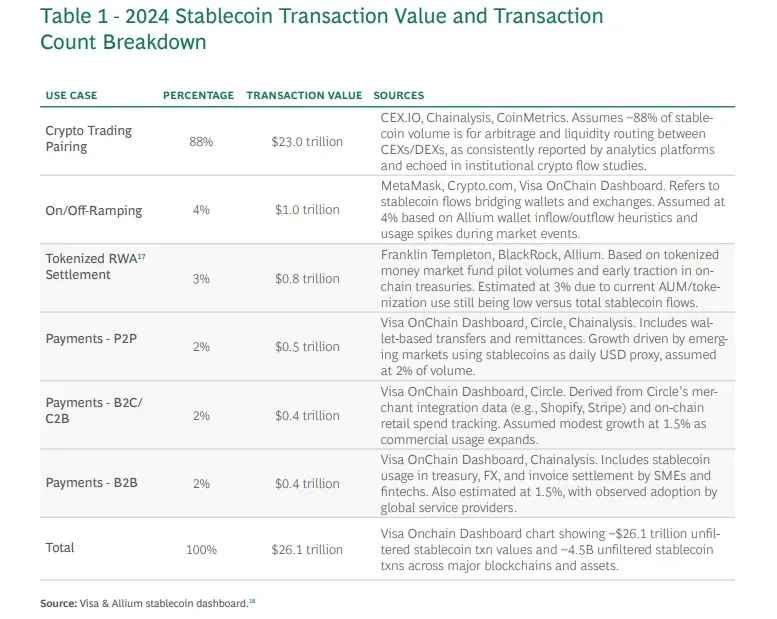

Source: BCG

According to BCG, a staggering 88 % of stablecoin transaction volume in 2024 originated from crypto trading. While payments, remittances, and interbank settlement are frequently cited as potential use cases for stablecoins, this data suggests that crypto trading still plays a critical role in stablecoin usage. From this perspective, using stablecoins in crypto trading is the most important way to bootstrap liquidity in the early stages. This can also be observed in the growth stories of USDT and USDC.

1.2.2 The Growth of USDT

USDT did not begin with the goal of creating a stablecoin. It originated from an idea by developer J.R. Willett that new cryptocurrencies could be created on top of the Bitcoin blockchain. This idea was implemented through a project called Mastercoin, which later became the Omni Layer, the technical foundation for USDT. USDT was first issued on the Omni Layer under the name Realcoin in October 2014, and was renamed Tether in November 2014.

USDT began full-scale circulation in January 2015 when it was adopted by the crypto exchange Bitfinex. This was because Bitfinex executives had established Tether Holdings Limited in the British Virgin Islands in 2014. From early 2017 to September 2019, USDT issuance surged from 10 million dollars to 2.8 billion dollars. This explosive growth was largely driven by Bitfinex users being forced to use USDT after the exchange lost access to USD deposits and withdrawals due to a shutdown of remittance services from local Taiwanese banks and Wells Fargo in April 2017.

Afterward, support from major global exchanges like Binance, Huobi, and OKX further fueled USDT’s growth. These developments helped Tether solidify its role as the de facto reserve currency of the crypto market.

1.2.3 The Growth of USDC

USDC was announced in May 2018 by the Centre consortium, founded by Circle and Coinbase, and officially launched in September of the same year. Like USDT, USDC’s early growth was largely driven by trading pair support from Coinbase and Kraken. Beyond crypto exchanges, USDC saw further expansion when it was adopted as the primary stablecoin on the Solana network, enabling significant onchain growth.

Considering that the stablecoins which achieved dominance in the dollar ecosystem all grew significantly through crypto exchanges in their early stages, collaborating with a crypto exchange seems essential for KRW stablecoins to gain market share. From this perspective, the fact that Korea’s number one payment service Naver Pay and the top crypto exchange Upbit are forming a consortium to enter the KRW stablecoin business is a major development in the Korean market.

Source: Naver Pay

Naver Pay is a simple payment service offered by Naver Financial that allows users to pre-register bank accounts and cards, and make payments or transfers using the registered methods. Naver is the most widely used web portal in Korea and provides a wide range of services including search, news, blogs, shopping, and maps.

The average daily transaction volume through simple payment services in Korea is about 1 trillion KRW. Of this, simple payments account for around 480 billion KRW. Among these, the big three services Naver Pay, Kakao Pay, and Toss Pay hold over 90 percent market share. Among the three, Naver Pay leads the market with revenue around 1.6 trillion KRW, roughly double that of the second and third players Kakao Pay and Toss Pay.

Korea is a country of crypto exchanges. The FIU, under Korea’s Financial Services Commission, published a 2024 second-half report on virtual asset service providers, which revealed some interesting statistics:

The daily average transaction volume reached 14.3 trillion KRW, exceeding the Korean stock market volume for the same period (10.8 trillion KRW).

KRW deposits totaled 10.7 trillion KRW.

Major crypto exchanges in Korea include Upbit, Bithumb, Korbit, Coinone, and Gopax. Among them, Upbit stands out as the dominant player with a market share of approximately 60 to 70 percent.

If Upbit and Naver Pay jointly issue a KRW stablecoin, where could it be used? For the sake of this discussion, let us assume they name the coin nKRW.

2.3.1 Expected Use Cases

The first use case is Upbit’s quote currency. Exchanges operating in regulatory grey areas such as Binance and Bybit cannot support fiat currencies. However, even fully compliant exchanges like Coinbase support both fiat USD and the USDC stablecoin as quote currencies. In fact, Coinbase integrates the USD and USDC order books to allow users holding either to trade within the same liquidity pool.

Likewise, if nKRW is adopted by Upbit, nKRW holders would be able to trade in the KRW market with the same liquidity as before. Previously, transferring KRW to Upbit required going through a banking process. But if Naver Pay is integrated, users could conveniently top up nKRW through Naver Pay and transfer it to Upbit. Additionally, unlike fiat KRW, nKRW is not subject to banking settlement hours, which offers operational advantages for exchanges.

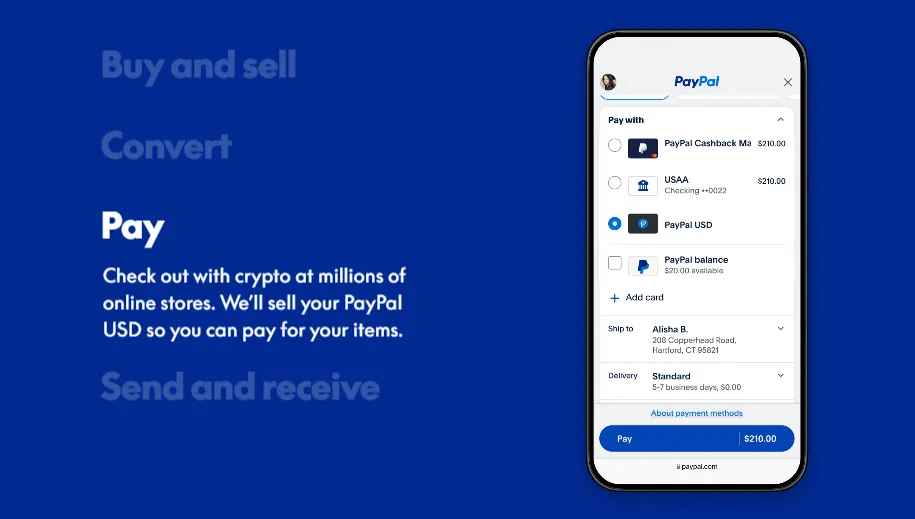

Source: Paypal

The second use case is payment currency within Naver Pay. A representative example of a fintech company using a stablecoin for payments is PayPal’s PYUSD. PayPal users can top up PYUSD using bank accounts or cards and hold it within the app for payments. Similarly, if nKRW is introduced, Naver Pay could support it as a fourth payment option in addition to bank accounts, cards, and Naver Pay Money.

Naver Pay is used in a wide variety of locations in Korea. In addition to Naver’s own shopping platform, it is accepted by major online retailers and offline stores. Therefore, introducing nKRW would immediately enable broad utility and adoption across many channels.

Moreover, Naver Pay currently offers a card linked to Naver Pay Money. Extending this, it could also issue a card that supports payments using nKRW balances. Using stablecoins for payments has several benefits. Like prepaid funds, they bypass card networks and issuers, lowering intermediary fees. They can also significantly reduce settlement time compared to the traditional system.

2.3.2 Impact

Considering the current transaction volumes of Naver Pay and Upbit, the potential impact of adopting a KRW stablecoin can be estimated. The table above assumes Upbit’s KRW deposits total 10.7 trillion KRW (based on the second half of 2024) and Naver Pay’s prepaid balances total 150 billion KRW (as of January 2025). It then projects their share of the global stablecoin market depending on what percentage of these funds is converted to KRW stablecoins.

In the most optimistic scenario where all KRW on both platforms is converted into stablecoins, the Naver Pay and Upbit stablecoin could immediately become the third largest in the world after USDT and USDC. While this is unlikely in reality, even converting just 5 to 10 percent into stablecoins would put nKRW on par with PayPal’s PYUSD in terms of scale.

If various banks and companies enter the KRW stablecoin issuance market, it seems unlikely that they will be able to surpass the consortium of Naver Pay and Upbit. Upbit could lead the initial distribution and growth of the stablecoin based on its massive liquidity, and once a certain economy of scale is achieved, Naver Pay could leverage it for services like remittances and payments, enabling long-term growth.

But wait a moment, who exactly will issue the KRW stablecoin? Initially, USDC was issued by Circle under the governance of Centre, which was jointly founded by Circle and Coinbase. However, in August 2023, the Centre consortium was dissolved, and all governance and issuance rights were consolidated under Circle. In the case of PayPal’s PYUSD, PayPal participates in branding and distribution, but actual issuance is handled by Paxos.

One might simply assume that if Naver Pay and Upbit issue a KRW stablecoin, Naver Pay could take the role of Circle and Upbit the role of Coinbase, thus separating issuance and distribution. However, the reality is not that simple. According to the current “Virtual Asset User Protection Act,” “trading or other transactions involving virtual assets issued by oneself or related parties” is prohibited. In other words, a model where a fintech company issues and distributes a stablecoin may face legal challenges. However, lawyer Hyo Bong Kim from the law firm Bae, Kim and Lee mentioned that if this clause is interpreted as applying only to trading within crypto exchanges, it may open the possibility for fintech companies to issue and distribute stablecoins, depending on the legal interpretation.

Therefore, depending on how the law is interpreted, Naver Pay might be able to directly serve as the KRW stablecoin issuer. If that proves unfeasible, a third-party bank or private issuer would need to join the consortium and handle the issuance.

Given the existing deposit volume and distribution channels, a KRW stablecoin issued by Naver Pay and Upbit has a high potential to grow into a top 10 global stablecoin. But would it naturally expand into onchain DeFi? My answer would be that it will be difficult at the outset.

The first reason is Korea’s strict foreign exchange regulations. Since the 1997 IMF crisis, Korea has implemented very stringent foreign exchange laws. If KRW stablecoin legislation advances, the stablecoin is likely to be granted quasi-legal tender status, which could make onchain transfers more difficult. Under current laws, remitting, receiving, or converting amounts equivalent to $10,000 automatically triggers reporting and requires a complex documentation process. This makes outbound onchain transfers highly restricted.

The second reason is the low global demand for KRW. One of the main goals for DeFi protocols is to secure deposits. In the case of USD stablecoins, global demand is high, and most global onchain users treat them as a de facto reserve currency. If a DeFi protocol were to adopt a KRW stablecoin, its user base would likely be limited to a small group of Korean onchain users. Nevertheless, if the KRW stablecoin itself grows to a scale comparable to other global stablecoins, even this level of demand could be a significant benefit to global DeFi protocols.

KRW holds less than 0.2 percent of global payment market share and is not even ranked within the top 20 currencies in terms of payment volume. However, as roughly estimated above, if just 5 percent of the existing deposits on Naver Pay and Upbit were converted into KRW stablecoins, the resulting stablecoin could surpass the size of EURC, the representative euro-denominated stablecoin.

Let us watch to see whether the consortium of the number one fintech firm and the number one crypto exchange can succeed, and how other players in Korea will respond with new strategies.

Dive into 'Narratives' that will be important in the next year