*Asia Stablecoin Alliance is launched by Heechang Kang and Jinsol Bok from Four Pillars, along with Alex Lim (Jongkyu Lim), the Korea lead at LayerZero, to accelerate stablecoin adoption across Asia and to serve as a research and community hub for establishing clear stablecoin strategy and technical infrastructure. (X Link, Substack Link)

Recently in Korea, there has been active discussion around various topics such as the issuer of KRW stablecoins and the management of reserves. One unfortunate reality is that while almost all stablecoins globally are issued on Ethereum without exception, there is still a lack of awareness in the Korean market about why KRW stablecoins must also be issued on Ethereum.

Compared to other networks, Ethereum offers overwhelming liquidity, a proven system, network effects, a high level of security, and strong decentralization. While it is possible to support native issuance on networks other than Ethereum, my argument is that the initial issuance must always begin with Ethereum at the center.

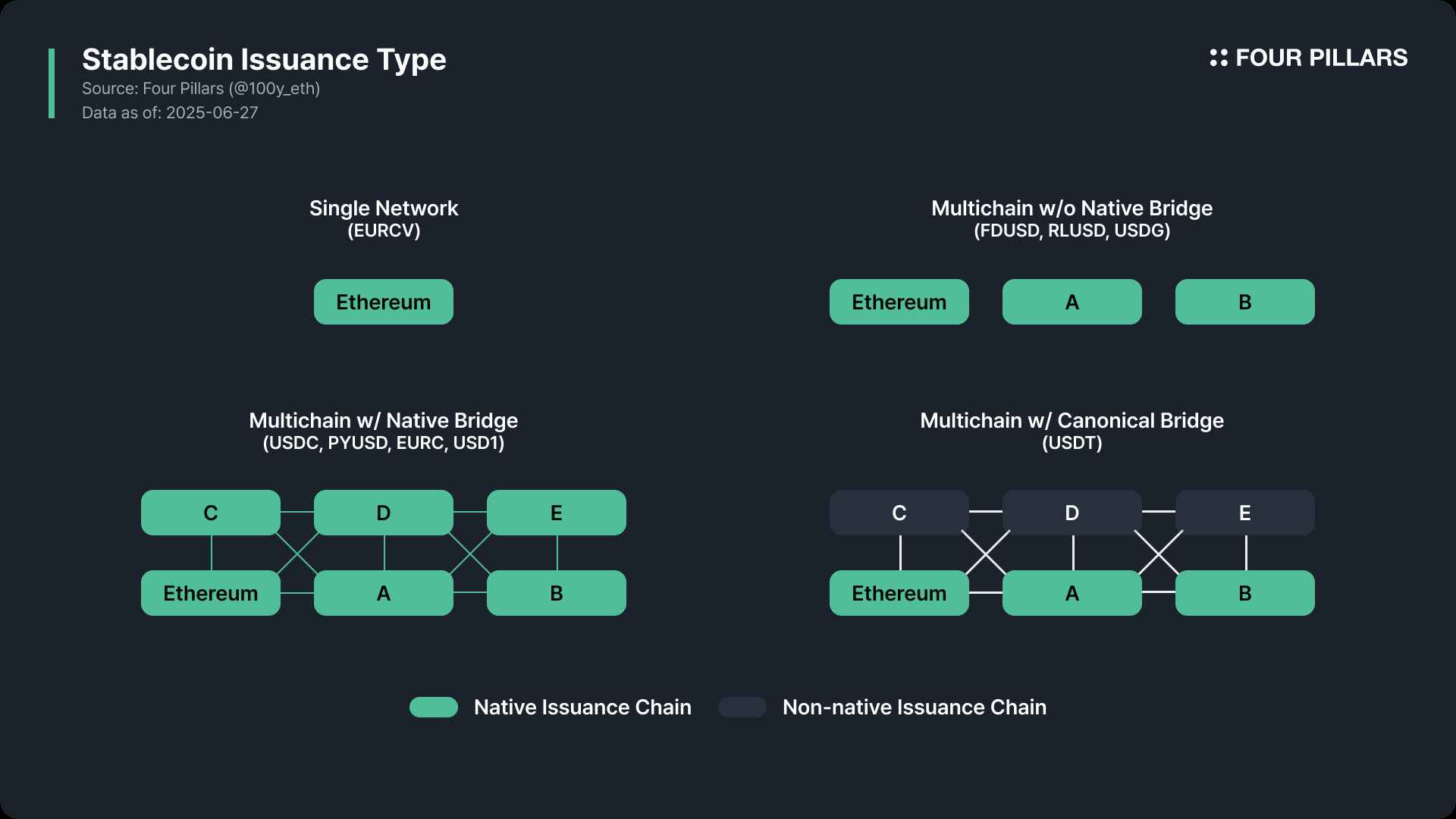

Global stablecoins typically support issuance through one of the following methods: 1) single network, 2) multichain without native bridge, 3) multichain with native bridge, and 4) multichain with canonical bridge.

Considering the unique nature of KRW stablecoins, they should be issued on the Ethereum network without exception. However, it may be worth strategically considering native issuance on a small number of chains. If multichain support is introduced, it will be essential to adopt a cross-chain solution.

For global readers, the idea that stablecoins are issued on Ethereum may seem like a given. However, the market situation in Korea is quite different. Recently, discussions around stablecoins have been progressing rapidly in Korea, and it is common for institutions, media, and communities to act as if stablecoins should only be issued on a specific network. As a result, public opinion is often misled. For example, Kaia and Avalanche are networks that are frequently mentioned in Korea.

It is desirable for KRW stablecoins to circulate across various networks such as Kaia, Avalanche, and Solana, and it is up to the issuer to decide whether to issue them on these networks. However, one thing that must be made clear for a successful stablecoin initiative is that KRW stablecoins must always begin with Ethereum as the primary issuance network.

It is now widely known around the world that discussions about issuing KRW stablecoins are actively underway in Korea. However, the messaging around KRW stablecoin issuance is currently coming top down from the government, and there are still no specific legal guidelines dedicated solely to KRW stablecoins.

As a result, practitioners in public institutions, financial institutions, banks, and companies are left with almost a blank slate when it comes to the blueprint for who should issue KRW stablecoins, how they should be issued, where they should be issued, and how they should be used or managed. This has led to many discussions in Korea regarding the issuance pipeline, including the issuer, reserve assets, risk management, issuance network, and use cases. This article focuses specifically on the “issuance network” of KRW stablecoins.

Recently in Korea’s finance and blockchain industries, there has been heated discussion about which network KRW stablecoins should be issued on. While various networks including Ethereum are being mentioned, two mainnets that are particularly popular in the Korean community are Kaia and Avalanche. Let’s take a closer look at why these two are being frequently discussed.

1.2.1 Kaia

Source: X (@seo_sangmin)

The most frequently mentioned network in Korea is by far Kaia. Kaia’s chairman, Sangmin Seo, recently expressed his strong commitment to KRW stablecoins by stating, “Justas we onboarded native USDT on KaiaChain, we will do our best to enable the issuance of a KRW wtablecoin on KaiaChain as well. Kaia’s Stablecoin Summer is just beginning.”

Kaia is a newly rebranded network formed from the merger of the former Klaytn and Finschia networks. Klaytn originated from GroundX, a blockchain subsidiary of Kakao, while Finschia originated from a former affiliate of LINE. Beyond this historical background, Four Pillars researcher Jaewon Kim (Ponyo) presented the following reasons as grounds for choosing Kaia as a potential issuance network for KRW stablecoins:

- Rapid regulatory responsiveness and operational efficiency: Kaia is a domestic Layer 1 network in which Kakao’s GroundX was involved from the design stage. This allows Kakao to quickly implement regulatory measures such as network changes, wallet limit settings, transaction suspensions, and on-chain reserve disclosures. This “immediacy of action” is a clear competitive advantage from a regulatory perspective.

- Policy leverage through domestic blockchain usage: Operating KRW stablecoins on a domestically developed chain aligns with the policy and political narrative of emphasizing financial sovereignty. It also minimizes concerns about dependency on foreign Layer 1 networks, which could result in favorable assessments from the National Assembly and the Financial Services Commission.

- USDT onboarding: In May 2025, Tether issued 100 million USDT natively on Kaia, and major exchanges such as Bitfinex and MEXC supported deposits and withdrawals. This indicates that Kaia has the basic infrastructure and operational capabilities to handle large-scale stablecoins.

- User acquisition potential via messaging platforms: After the merger, LINE NEXT onboarded Kaia minidapps to the LINE miniapp portal. If the Kaia wallet is later integrated into KakaoTalk, the KRW stablecoin could be used immediately across a single on-chain network connecting KakaoTalk (about 50 million users in Korea) and LINE (about 200 million users in Japan and Southeast Asia). This early user base is a unique advantage that foreign Layer 1s cannot easily replicate.

That said, in my personal opinion, the Kaia Foundation is currently established in Abu Dhabi and operated out of Singapore, and it no longer has direct connections to Kakao or LINE. Therefore, the claims of “rapid regulatory responsiveness and operational efficiency” and “domestic blockchain usage” may not hold much practical value. Still, considering Kaia’s DNA and the large number of personnel with backgrounds at Kakao and LINE, it is difficult to completely dismiss these advantages.

Additionally, GroundX, the former operator of Klaytn and a Kakao subsidiary, previously participated in the Bank of Korea’s CBDC pilot project. Currently, various affiliates of Kakao and LINE such as LINE NEXT, Kakao, Kakao Pay, Kakao Entertainment, and LINE Genesis are participating in Kaia as validators. These factors support the case for Kaia being adopted as the issuance network for KRW stablecoins.

1.2.2 Avalanche

Although it has not yet been widely mentioned in the retail community, Avalanche is starting to gain attention within Korea’s blockchain and finance sectors. The following reasons support its potential selection as a KRW stablecoin issuance network:

Experience in institutional collaboration: Avalanche has a history of collaborating with public and financial institutions around the world, including Singapore’s MAS and Japan’s SMBC, by providing blockchain technology support.

Institutional-grade product offerings: Avalanche offers solutions like Evergreen, which allow enterprises and financial institutions to easily build their own blockchains. These solutions support KYC/KYB enforcement, geographic access restrictions, validator permission settings, and more, enabling various degrees of customization between public and private networks.

One of the main advantages of stablecoins over traditional currencies is that they can be used in more functions and across more countries. To fully capitalize on this advantage, it is crucial for stablecoins to circulate and be utilized across various networks.

However, the question of “where should KRW stablecoins be circulated” and “on which network should KRW stablecoins initially be deployed” are two different issues. That is, regardless of who it will be, the bank, fintech, or company that will eventually take on the role of issuing KRW stablecoins must consider “which networks should our KRW stablecoin be natively supported on.”

In this respect, I want to emphasize that if KRW stablecoins are issued, they must be issued on Ethereum without exception, and I argue that issuance and distribution on networks such as Kaia, Avalanche, and Solana should be left to the discretion of the stablecoin issuer.

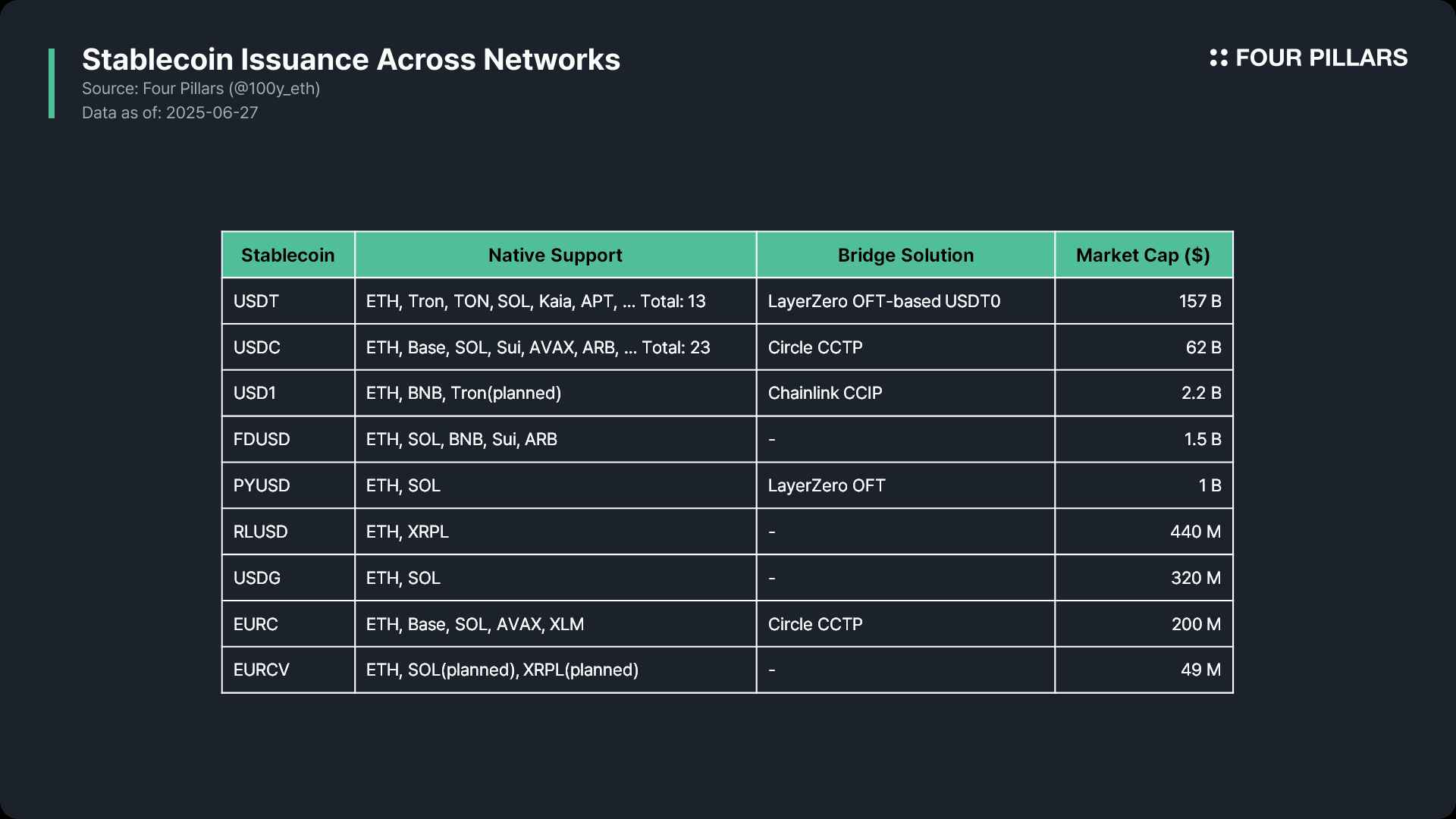

2.2.1 Tether USDT

Native issuance supported on: Ethereum, Tron, TON, Solana, Aptos, Avalanche, Kava, Celo, Kaia, Vaulta (formerly EOS), Liquid, Polkadot, Tezos

Bridge solution: USDT0 powered by LayerZero

USDT, the stablecoin with the highest market capitalization, currently supports native issuance on 13 networks. Interestingly, through USDT0, which leverages LayerZero’s technology, USDT can be used on major networks such as Arbitrum, BeraChain, Unichain, Optimism, Sei, and Ink even without native support, without liquidity fragmentation, just like a native asset.

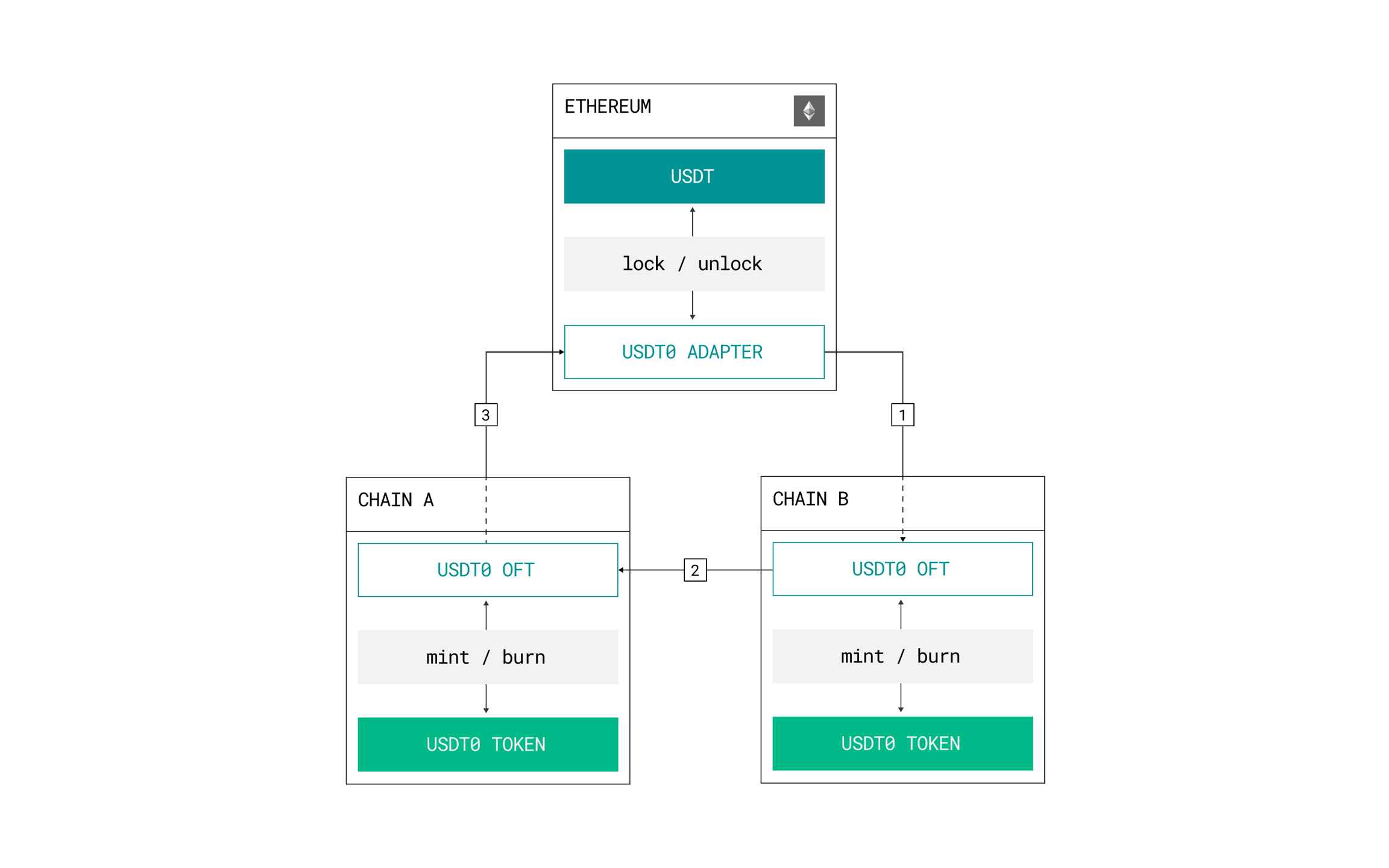

Source: USDT0 docs

USDT0 follows LayerZero’s OFT standard and works as follows:

USDT locking: When USDT is transferred from Ethereum to another chain, it is locked in a smart contract on Ethereum mainnet.

USDT0 minting on destination chain: An equivalent amount of USDT0 is minted on the destination chain, reflecting the locked USDT on Ethereum mainnet.

Cross-chain bridging: USDT0 can freely bridge to other networks. During this process, USDT0 is burned on the source chain and minted on the destination chain.

Redemption: USDT0 can be redeemed by unlocking the original USDT on Ethereum mainnet.

Without a system like USDT0, on networks where USDT is not natively supported, multiple versions of USDT bridged by third parties would exist, resulting in severe liquidity fragmentation.

For example, if USDT is natively supported on chain A but not on chain B, and bridge providers X, Y, and Z exist in the market, then on chain B, USDT liquidity could be fragmented into X-wrapped USDT, Y-wrapped USDT, and Z-wrapped USDT. This results in a terrible user experience and highlights the need for solutions like USDT0 based on LayerZero OFT.

Bridge validation is performed by the LayerZero DVN network, and USDT0 and LayerZero act as validators for USDT0.

2.2.2 Circle USDC

Native issuance supported on: Ethereum, Base, Solana, Arbitrum, Aptos, Algorand, Avalanche, Celo, Cosmos (Noble), Hedera, Linea, Near, Polkadot, Optimism, Polygon PoS, Sonic, Stellar, Sui, Unichain, World Chain, XRPL, zkSync

Bridge solution: Circle’s own CCTP

USDC, the second largest stablecoin by size, supports native issuance on 23 networks. Circle supports seamless bridging of USDC using its own bridge solution, CCTP. The mechanism of CCTP works as follows (assuming a transfer from chain A to B):

Burn: The USDC held by the user is burned on chain A.

Verification (attestation): Circle’s attestation service observes the burn event and sends a signed verification to chain B.

Mint: Upon receiving the signed attestation from Circle, chain B mints USDC of the same value for the user.

Like OFT, CCTP follows a burn-and-mint model, which helps prevent liquidity fragmentation across chains. The burn verification is conducted by Circle itself.

2.2.3 PayPal PYUSD

Native issuance supported on: Ethereum, Solana

Bridge solution: LayerZero OFT

PYUSD is issued by PayPal in partnership with Paxos and is integrated into the PayPal app, which is a major advantage in terms of distribution. PYUSD is supported only on Ethereum and Solana, and bridging between the two is done via LayerZero OFT. The bridge is validated by Paxos, Google Cloud, and LayerZero as DVN validators.

2.2.4 Others

FDUSD: Issued by FD121 in Hong Kong, currently supports native issuance on Ethereum, Sui, Solana, BNB, and Arbitrum. No cross-chain solution is provided, but centralized exchanges like Binance appear to partially serve the role of bridging through deposit and withdrawal.

RLUSD: Issued by a subsidiary of Ripple Labs, supports native issuance on Ethereum and XRPL. No cross-chain solution is supported.

USDG: Issued by a Singapore-based subsidiary of Paxos, currently supports native issuance on Ethereum and Solana. No cross-chain solution is supported.

EURC: Circle’s euro-denominated stablecoin, supports native issuance on Ethereum, Base, Avalanche, Solana, and Stellar. Uses Circle’s CCTP for cross-chain bridging.

EURCV: A euro stablecoin issued by SG-Forge, a subsidiary of Societe Generale in France, was initially launched on Ethereum and is planning to support Solana and XRPL in the future.

USD1: Issued by World Liberty Financial, which is affiliated with members of the Trump family. Initially supported Ethereum and BNB networks and plans to support Tron. Uses Chainlink CCIP as its cross-chain solution.

Disclaimer: As mentioned in the introduction, the blockchains most frequently discussed in Korea in relation to KRW stablecoins are Kaia and Avalanche. Therefore, the following characteristics will include comparisons to those networks. To reiterate, this article is not arguing that KRW stablecoins should not be issued or distributed on networks like Kaia or Avalanche. Rather, it argues that companies issuing KRW stablecoins must begin with Ethereum as their primary issuance network, and that further issuance or distribution on networks like Kaia or Avalanche is acceptable.

We can see that all major stablecoins generally begin with issuance on Ethereum. Is this a coincidence? I firmly believe it is not, and I argue that if KRW stablecoins are to be issued, their initial issuance must start with Ethereum as the central network. The reasons why Ethereum is the optimal network for launching a stablecoin are as follows.

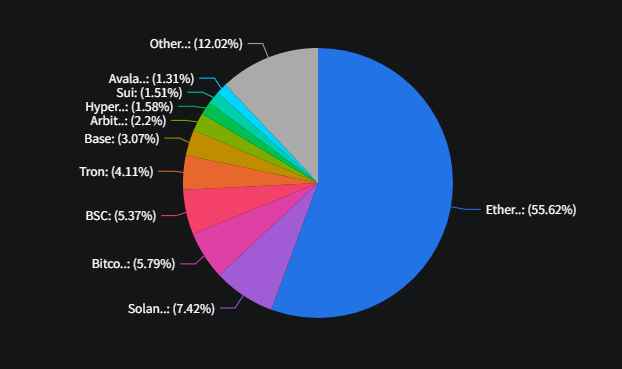

Source: DefiLlama

Across all blockchain networks, Ethereum holds overwhelmingly dominant liquidity. The total value locked (TVL) in Ethereum’s DeFi protocols is around $61 billion, and over $126 billion worth of stablecoins exist on the network. Compared to Solana, the second-largest ecosystem, Ethereum’s DeFi TVL is about 8 times larger and its stablecoin TVL is about 13 times greater.

For reference, Kaia’s DeFi TVL is around $35 million and stablecoin TVL is around $106 million, meaning Ethereum is approximately 1,740 times and 1,180 times larger respectively. Avalanche has a DeFi TVL of around $1.45 billion and stablecoin TVL of around $1.5 billion, making Ethereum roughly 42 times and 84 times larger in comparison.

Issuing a stablecoin is not the end goal; utilization is the key. With its overwhelming liquidity, Ethereum supports an unmatched ecosystem of infrastructure and applications, making it one of the strongest reasons for beginning stablecoin issuance on Ethereum.

The Ethereum network has never experienced a complete chain outage since its launch. While there have been issues such as Geth clients being disrupted by DoS attacks or bugs in the Nethermind client, the network has never entirely halted due to Ethereum validators using a diverse range of clients.

In contrast, Kaia experienced prolonged block production outages in 2020 and 2021, and Avalanche has suffered from multi-hour outages in 2023, 2024, and 2025. Other networks such as Solana, Aptos, Polygon PoS, Sui, and Tron have also experienced full chain halts in the past. Since stablecoins inherently deal with money, the stability of the underlying network is a critical factor.

Ethereum not only offers rich liquidity in crypto assets, but also hosts all major stablecoins. In addition, institutions such as BlackRock, VanEck, and Franklin Templeton have onboarded tokenized funds to Ethereum. These massive network effects will continue to incentivize stablecoin issuers and institutions worldwide to issue stablecoins and real-world asset tokens on Ethereum, establishing a virtuous cycle of growth.

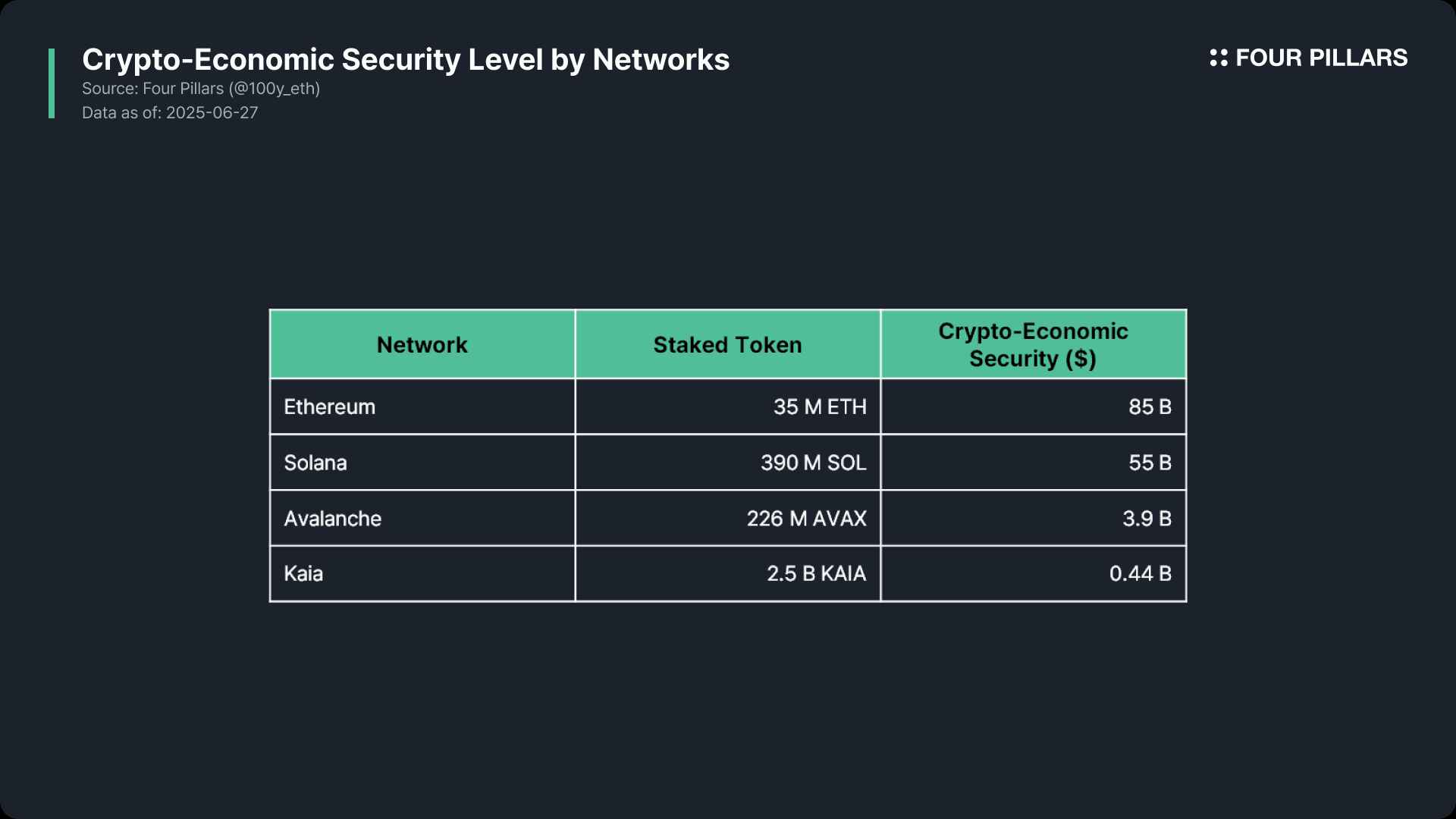

Ethereum is the most economically secure smart contract network in the world. As of June 27, 2025, its crypto-economic security scale is estimated at around $85 billion, while Solana, Avalanche, and Kaia are at approximately $55 billion, $3.9 billion, and $440 million respectively. With the largest crypto-economic security scale, Ethereum is the best-suited network to securely support large-scale stablecoin liquidity.

Ethereum is the most decentralized smart contract network in terms of token distribution, foundation management, number and distribution of validators, governance, and stakeholder dynamics. This provides not only ideological justification for issuing stablecoins on Ethereum, but also practical benefits by avoiding the centralization risks associated with other networks. Decentralization delivers meaningful utility in this context.

Looking at global stablecoin examples, issuance networks can be categorized into four types:

Single Network: The stablecoin is issued on only one network. This is easy to manage but has the drawback of limited ecosystem expansion. EURCV is an example.

Multichain without Native Bridge: The stablecoin is natively issued on multiple networks, making it easier to expand than model 1, but still lacks bridge support. This raises concerns about liquidity fragmentation caused by third-party bridges. Examples include FDUSD, RLUSD, and USDG.

Multichain with Native Bridge: The stablecoin is natively issued on several networks and is supported by native bridges like CCTP, CCIP, or OFT. It enables ecosystem expansion and supports all natively issued stablecoins, but if the issuer does not support certain networks, liquidity fragmentation may still occur via third-party bridges. Examples include USDC, PYUSD, EURC, and USD1.

Multichain with Canonical Bridge: The stablecoin is issued natively on multiple networks, and additionally uses a canonical burn-and-mint bridge mechanism to enable seamless use across other networks without liquidity fragmentation. This model is the most effective for ecosystem expansion but may cause user confusion since two versions of the stablecoin exist: native and bridged. However, in practice, only one version is typically used per network, so this rarely poses a problem. USDT is an example.

Based on the above, I would like to propose an approach for issuing KRW stablecoins.

4.2.1 Ethereum Must Be Included

Ethereum is the only network that possesses all the characteristics needed for stablecoin issuance, including liquidity, stability, security, decentralization, and an active ecosystem. From the perspective of a stablecoin issuer, there is no reason to bypass Ethereum and choose another network. Regardless of how many networks are natively supported in the initial issuance, Ethereum must be included.

4.2.2 Choose Native Issuance Networks Strategically

Most stablecoins, even if they support multiple networks, tend to concentrate on a few. For example, of the $156.8 billion in USDT circulation, $80 billion is on Tron and $73 billion is on Ethereum. Of the $59 billion in USDC, $41 billion is on Ethereum and $6.8 billion is on Solana. This suggests that simply supporting many networks does not guarantee success.

Given the nature of the KRW, it is highly likely that KRW stablecoins will be used less actively in the global on-chain ecosystem than USD stablecoins. Therefore, issuing on too many networks beyond Ethereum could lead to liquidity fragmentation. Issuers must carefully select a small number of networks that align strategically with their KRW stablecoin business.

In this context, Kaia may offer strategic advantages for KRW stablecoin issuance and distribution. While Kaia no longer has direct ties to Kakao, Naver, or LINE, it maintains historical and indirect connections, has a high percentage of Korean employees, and a relatively large Korean user base. However, its low liquidity and crypto-economic security level may limit the scalability of KRW stablecoins. If affiliates such as Kakao Pay or Kakao Bank were to issue a KRW stablecoin, Kaia could become a viable option.

Avalanche presents a slightly different situation, which can be split into two cases:

Avalanche C-Chain: As a public network, it has relatively strong liquidity and security. However, if a KRW stablecoin issuer were to support an additional network beyond Ethereum, networks like Solana and Base would likely take priority over Avalanche C-Chain, as they offer higher liquidity, stronger security, more users, and more vibrant ecosystems.

Avalanche Subnet: If the KRW stablecoin is introduced on Avalanche Subnet, which is designed for institutional use, the issuer may designate validators and implement default KYC/KYB functions, creating a semi-public, semi-private blockchain. In this case, it would be difficult to coexist with public networks such as Ethereum, Solana, Base, or Kaia. Issuance may be limited to just this network, which may be ideal for regulatory compliance but unfavorable for ecosystem expansion.

If the issuer seeks inflows of foreign capital, networks like Solana and Base, which have large overseas user bases and well-developed ecosystems, may serve as strong second choices after Ethereum.

4.2.3 Adopt a Cross-Chain Solution

A successful KRW stablecoin issuer would likely support native issuance on Ethereum and a few public networks. Without a cross-chain bridge between them, users and platforms that adopt the stablecoin could face difficulties managing liquidity. For example, moving KRW stablecoins from chain A to chain B might require redemption and reissuance by the issuer or reliance on third-party bridges, which increases risks and causes liquidity fragmentation.

To support smooth liquidity management, issuers should adopt cross-chain bridge solutions based on the burn-and-mint model, as seen in models 3 and 4 above. While Circle can operate its own CCTP due to its scale, for KRW stablecoin issuers it may be inefficient to build their own. Instead, they can easily manage liquidity by adopting solutions like LayerZero’s OFT or Chainlink’s CCIP.

Up to this point, we have examined why a successful KRW stablecoin must be issued on the Ethereum network. For planners, developers, and investors who have been long exposed to the stablecoin ecosystem, it may seem obvious to say, “Of course stablecoins should be issued on Ethereum.” However, since discussions around stablecoins in the Korean market have only recently begun in earnest, I believed it was necessary to write this article.

There is, however, another reason why it is difficult for Korea to easily choose a public network like Ethereum as the foundational network for KRW stablecoins. It lies in the unique characteristics of Korea as a country and the Korean won as a currency. Korea is a nation heavily dependent on exports. This naturally demands strict monitoring of foreign currency flows and exchange rates. Due to past experiences such as the depletion of foreign reserves during the IMF crisis, Korea maintains highly stringent foreign exchange laws.

Due to the nature of these laws, activities such as large-scale remittances or receipts by individuals or corporations, foreign currency borrowing, and foreign currency exchanges must be reported or notified in detail. If a KRW stablecoin is introduced and starts freely moving across borders, it could become a major headache for institutions like the Bank of Korea, National Tax Service, Korea Customs Service, and the Financial Supervisory Service.

Some may argue that KRW stablecoins should not be issued on public networks like Ethereum or Solana but rather on fully private networks or regulation-friendly platforms like Avalanche subnets. This is a valid argument when considering Korea’s unique circumstances.

However, we must revisit the question of why stablecoins are being introduced in the first place. Korea is a financially advanced country. With existing banking systems, payment networks, and various fintech services, citizens already participate in economic activities without difficulty. Blockchain and stablecoins are not only expected to enhance global accessibility and reduce intermediary fees, but also hold the potential to radically transform the traditional securities market, payment systems, and remittance infrastructure.

From this perspective, if KRW stablecoins are issued primarily on private networks, they would bring little benefit over the existing financial system. Furthermore, in terms of global alignment, such an approach could result in Korea being left out of the rapidly evolving global stablecoin landscape.

There are also several policy-related barriers to entry due to the unique nature of KRW stablecoins, which will be discussed in a future article.

Source: Shinsegae Group

According to recent cryptocurrency-related legislative proposals in Korea, it appears that stablecoins will be issued by banks, non-bank institutions, or companies. This means that the decision of which network to support for KRW stablecoin issuance is entirely up to the issuer. In other words, one issuer may choose only Kaia, another only Avalanche, and another may choose Ethereum along with a few other networks.

However, one point should be emphasized: choosing which network to support for stablecoin issuance is like choosing which supermarket to distribute your product in. Would you not naturally consider distributing in the Ethereum supermarket—a place that is the safest, holds overwhelming capital and customers, and has been chosen by all other stablecoin issuers?

Source: Coinmarketcap

The market has its priorities reversed right now. Of course, traders need to analyze and speculate on which stocks or tokens could benefit most from the issuance of a KRW stablecoin. That is their job. But builders and industry professionals should think differently. We need to discuss why there has suddenly been a surge of interest in KRW stablecoins, what real-world use cases they can generate, and what strategies are necessary for them to be meaningfully used. Strategies around stablecoins must follow from this analysis. KRW stablecoins are a product with too much potential to be consumed as just a narrative.

Yet in many of the recent discussions about KRW stablecoins, I feel that quite a few people fail to recognize what should be obvious. That is Ethereum. Regardless of which chain we personally prefer, we cannot talk about stablecoin issuance without including Ethereum. The reality is that most stablecoins have either been issued on Ethereum first or eventually expanded to Ethereum for a number of reasons. So why has Ethereum consistently been chosen by stablecoins? While others have covered technical points like security and decentralization, I would like to focus on the strategic side.

First, Ethereum currently has the most liquidity of any chain. Whether measured by DeFi TVL or total stablecoin supply, Ethereum undeniably has the largest market among all blockchains. If you want to talk about using stablecoins onchain, it makes no sense to leave out Ethereum, which hosts Uniswap, Aave, Morpho, Spark (by MakerDAO), Curve, Compound, and more. When building a product, skipping over the largest consumer market and targeting another is rarely the right choice unless there is a very specific reason.

Second, Ethereum is the Layer 1 chain most interconnected with other chains. This means that stablecoins can strategically expand to multichain ecosystems without excessive effort. Especially when considering Base and Arbitrum—ranked sixth and seventh in chain TVL—these are Ethereum Layer 2 chains. Moving assets to and from them is much easier and safer than moving across entirely different Layer 1s.

Third, Ethereum is the most value-neutral chain after Bitcoin. Chains currently being discussed as candidates for KRW stablecoin issuance all have much more visible stakeholders than Ethereum. If a KRW stablecoin is launched on a non-Ethereum chain, the group that benefits the most from this “fact” is likely the foundation or VC backing that chain. This is not inherently bad, but if we want to avoid unnecessary controversy, it is wiser to choose the most value-neutral chain for the initial issuance. While this argument may not be welcomed by certain chain foundations, launching a KRW stablecoin on a chain with clear stakeholder alignment invites the perception that the stablecoin is being used for narrative-driven gain, rather than for genuine product success. I see no reason to create such complications from the start. If we want to stay focused on the product without distraction, then Ethereum is the most strategic first choice.

Anyone who has followed my writing knows that I have consistently maintained a critical stance toward Ethereum. I believe it is healthier for the market to be made up of diverse Layer 1s with different values, rather than one platform dominating everything. Even so, stablecoins are a different story. Even if multichain deployment is planned, Ethereum must be the first chain considered. This is not about allegiance but because Ethereum is the most rational choice from a strategic perspective.

Finally, more important than the chain is who issues the stablecoin.

What matters more than which chain the KRW stablecoin is issued on is who issues it. Personally, I do not welcome the fact that commercial banks and large corporations are rushing to file trademarks related to stablecoins. Many of them have not taken the time to understand the market and are only doing this because their upper management told them to “look into stablecoins.”

The same goes for large tech companies. They are too busy using the stablecoin narrative to boost their stock prices, with no concrete blueprint for how to create actual demand. This reminds me of the “metaverse” craze in 2021. We all know how many Korean companies jumped into blockchain through metaverse and gaming in 2022 and 2023, only to abandon the effort after a few years. These companies lacked understanding of the industry from the start. To them, blockchain and stablecoins are just “one of many sectors.” As time passes, they will lose interest in stablecoins just as they did with metaverse and gaming, downsize or shut down their teams, and further diminish their presence in the Korean market.

If anyone intends to issue a KRW stablecoin, I believe they must first announce a concrete strategy and have it validated by the market before saying “we are going to issue it.” Otherwise, the opportunity of a KRW stablecoin will end up as just another bubble remembered in history.

The Web3 ecosystem has become a major target of North Korean cyberattacks, and the blockchain networks used to issue stablecoins are not exempt from these threats. Their attack vectors span not only smart contract vulnerabilities but also infrastructure components like node clients and malicious validators. Given Korea’s geopolitical context, the issuance network for KRW stablecoins must have the highest level of security among existing blockchains. In my view, Ethereum is the only blockchain that meets this security standard.

There are two major indicators for evaluating the security of a blockchain.

The first is economic security. This metric tends to be somewhat undervalued because, in massive blockchains like Ethereum and Solana, the scale of the assets securing the chain is so large that the likelihood of an economically motivated attack is extremely low. However, if we assume the worst-case scenario—an attack by a nation-state like North Korea—smaller networks may very well fall within their scope. This possibility must not be ignored.

The second is software maturity. Many blockchains have been built by forking Ethereum’s execution layer with modifications and adding their own consensus layer. This includes both Kaia and Avalanche. This architectural choice naturally makes them less stable than Ethereum. Once a network diverges from Ethereum’s legacy clients, any future updates to Ethereum’s execution clients could conflict with these custom changes, introducing bugs. Since these blockchains usually maintain only a single execution client instead of Ethereum’s diversified client ecosystem, any bug in that one client could impact the entire node network. Moreover, the consensus mechanisms are often developed independently, without perfect compatibility with the execution layer, making these networks vulnerable to downtime. Chains like Solana and Sui, which are not even based on the Ethereum Virtual Machine (EVM), have also experienced outages, as previously discussed. This shows that their software is still not mature. This is also why Solana, despite its reputation for performance, still labels its network as “mainnet beta.”

While other chains may show superior performance in specific areas, Ethereum remains the "capital" for secure stablecoin issuance. The issuing network inherently holds the strongest control over a token, and that control must be both safely managed and properly decentralized. Can any other chain truly surpass Ethereum’s decade-long operational stability, its $86 billion in economic security, and its decentralization with over 1.1 million validators?

In the previous post ‘Will Kakao Pay Issue a KRW Stablecoin on Kaia?’, I addressed only the possibility that Kakao Pay may choose Kaia as the issuance network for a KRW stablecoin, intentionally avoiding the question of whether it should. In this comment, I want to briefly share my thoughts on that necessity.

From the regulators’ point of view, Kaia’s—and arguably its only—strength is its regulatory responsiveness, or “compliance agility.” As a domestic Layer 1, Kaia’s internal development teams can promptly implement actions requested by authorities such as adjusting network parameters, setting wallet limits, pausing transactions, or disclosing on-chain reserves. This level of control aligns well with the Financial Services Commission and the Bank of Korea’s supervisory preferences and fits neatly into the narrative of financial sovereignty by avoiding reliance on foreign public chains.

However, concluding that Kaia should be prioritized for issuance simply because of its speed in regulatory compliance or its status as a domestic chain would be premature. The argument that “global chains are hard to control” and thus we should insist on Kaia is not unlike suggesting we should run a local network instead of using the internet. If a country were to actually adopt such a stance, it would effectively sever ties with global financial and trade networks, fall behind in security and technical advancements, and face talent and capital outflows. Similarly, excluding Ethereum from KRW stablecoin issuance would create structural limitations and external costs in terms of accessing global liquidity, using proven security systems, and maintaining compatibility with dominant token standards like ERC-20 and the broader global DeFi infrastructure.

More importantly, most risks on public chains stem not from the chain itself but from governance or security failures by the issuer or operator. Ethereum is the most trusted public blockchain among global financial institutions, with TVL roughly 1,740 times greater than Kaia (as referenced earlier). It is already being used by large banks and asset managers. It also has well-established incident response protocols built on years of audits and operational data. Its ecosystem maturity goes without saying. In other words, if you choose Ethereum, it is highly unlikely that the chain itself will be the source of any issue. On the other hand, issuing a KRW stablecoin natively on Kaia adds the technical stability risks of the chain itself on top of the usual operational risks, increasing the overall burden of risk management.

Therefore, if your top priority is security and minimizing risk vectors, it is far more reasonable to use Ethereum as the main issuance network and Kaia as a domestic payment layer.

Dive into 'Narratives' that will be important in the next year