SDEV’s $134M capital raise decomposes to $76M in external capital, 943.6M SKY from the Foundation, and roughly 30% of typical governance polling turnout.

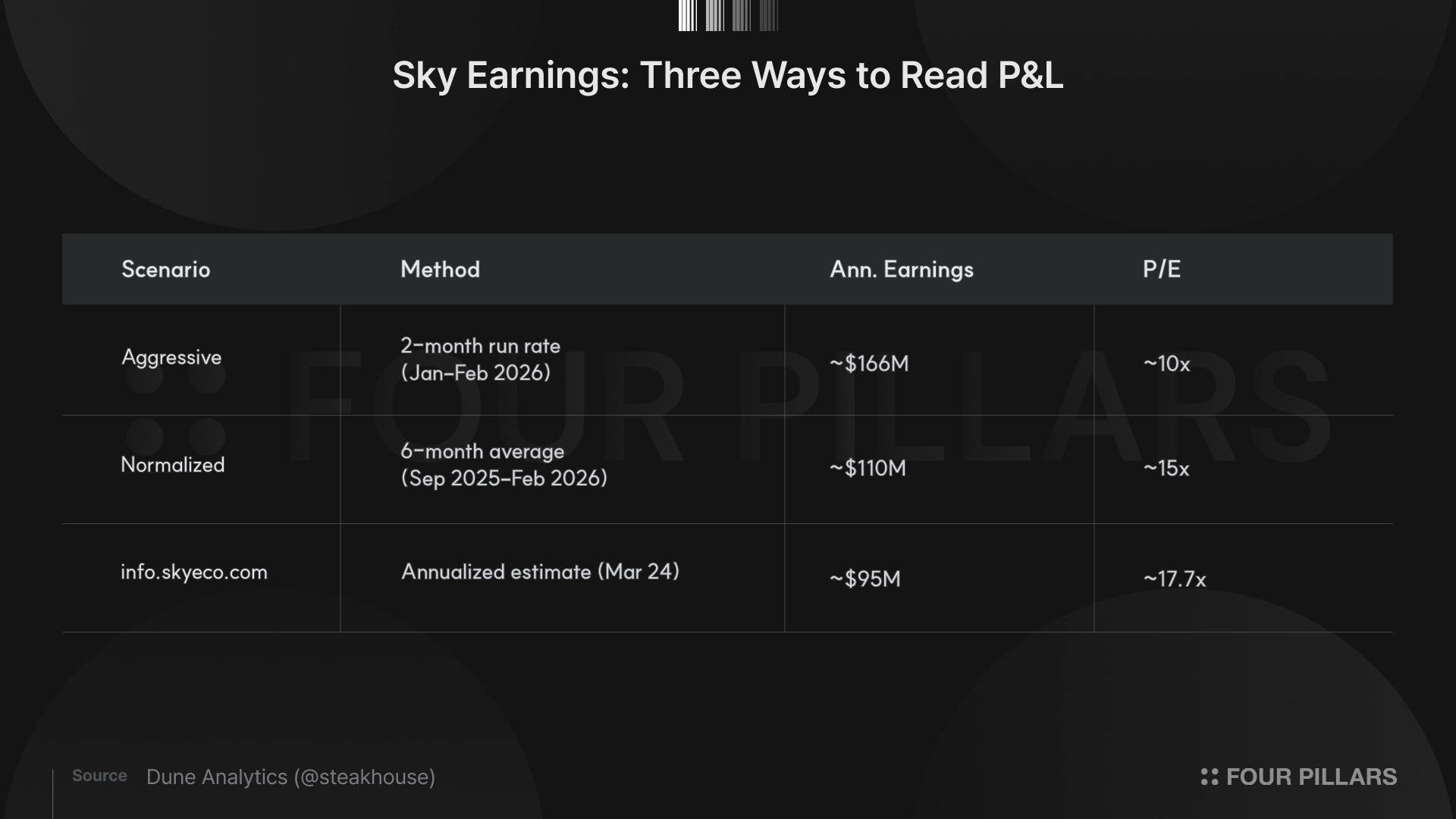

Sky runs a $12.57B lending business that flipped positive. Annualizing the two-month run rate gives ~$166M in earnings (~10x P/E), normalizing over six months gives ~$110M (~15x P/E).

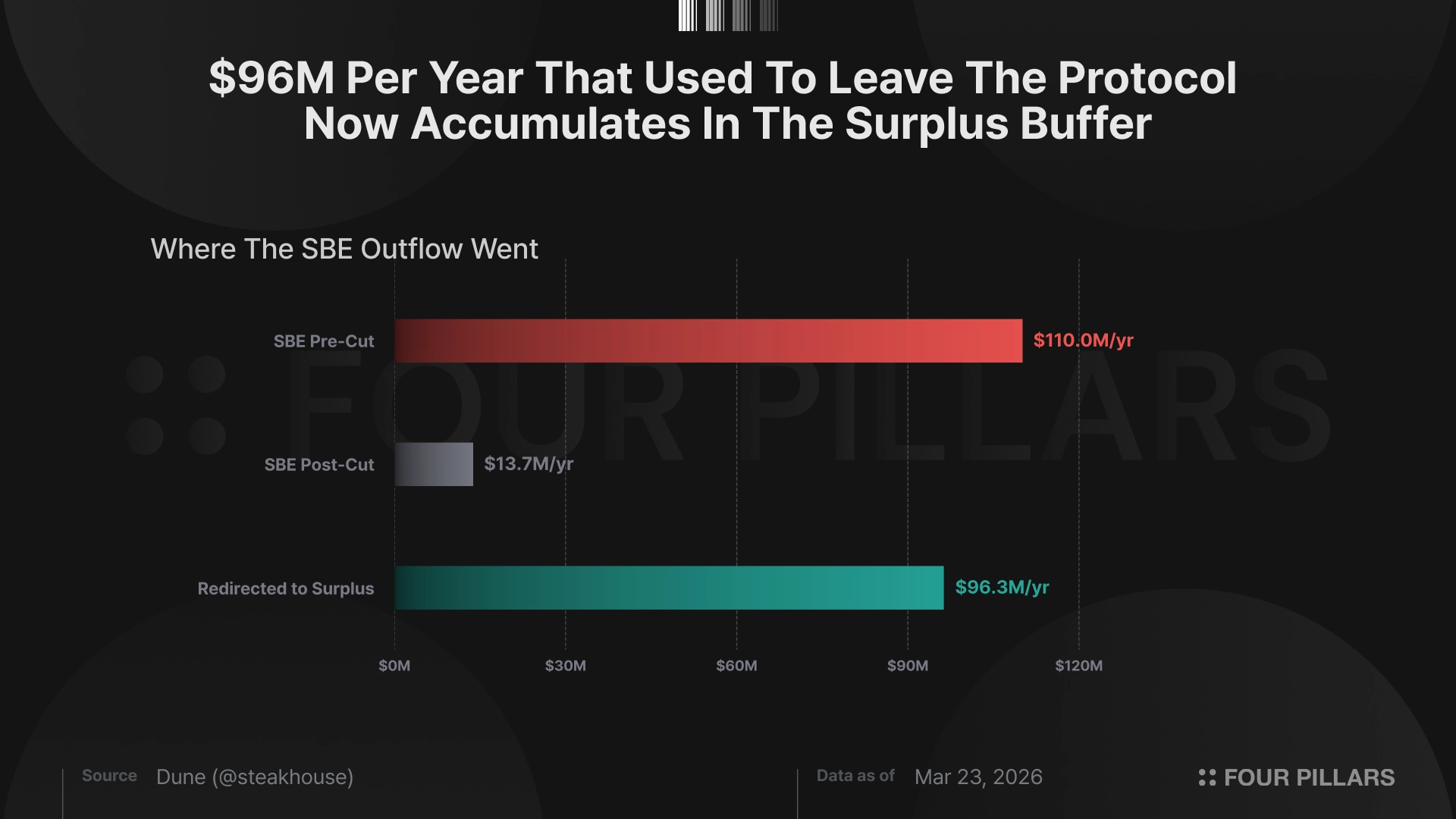

Governance cut the buyback by 87.5%, emissions by 16.2%, and SSR by 25bp in three weeks. The same actions that narrowed the pipe to tokenholders accelerated surplus accumulation by ~$96M per year.

The math for SKY stakers and non-stakers diverges.

SDEV lists on NYSE April 3, having started life as NovaBay Pharmaceuticals at a roughly $30M market cap. The rebrand to Stablecoin Development Corporation and the associated capital raise produced a $134M headline, but the decomposition is more specific.

Source: Fidelity

Of that $134M, external capital accounts for $76M (56.7%). Tether Investments contributed $25M in cash; Framework Ventures, R01 Fund, and others contributed $51M in stablecoins. The remaining 43.3% came from the Sky Frontier Foundation, which contributed 943.6M SKY tokens valued at roughly $58M. For every dollar of external capital that went in, about $1.76 in SKY exposure sits in the vehicle, with nearly half seeded by the Foundation.

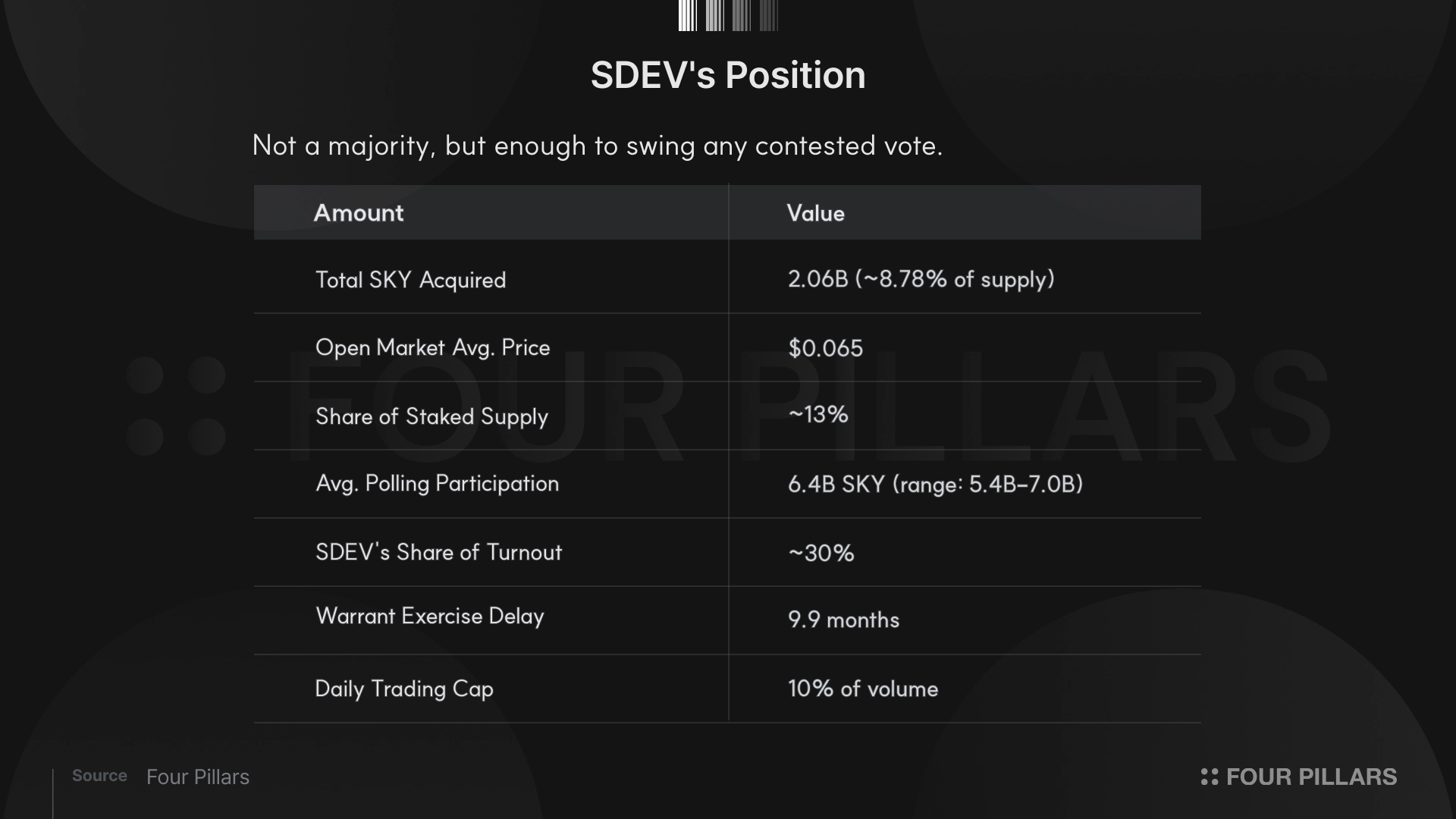

SDEV acquired 2.06B SKY in total, roughly 8.78% of total supply and about 13% of staked supply, with open market purchases averaging $0.065 per token. All acquired SKY is staked. The warrant structure tells you how investors priced liquidity. Exercise delayed 9.9 months, daily trading capped at 10% of volume. At current SKY secondary liquidity of roughly $12M per day, building or exiting a meaningful position takes weeks, and the discount to market partly compensates for that lockup.

Sky polling votes average roughly 6.4B SKY in participation, ranging from 5.4B to 7.0B across 33 completed polls since July 2025. SDEV's 2.06B represents about 30% of typical polling turnout. Not a majority, but enough to swing any contested vote.

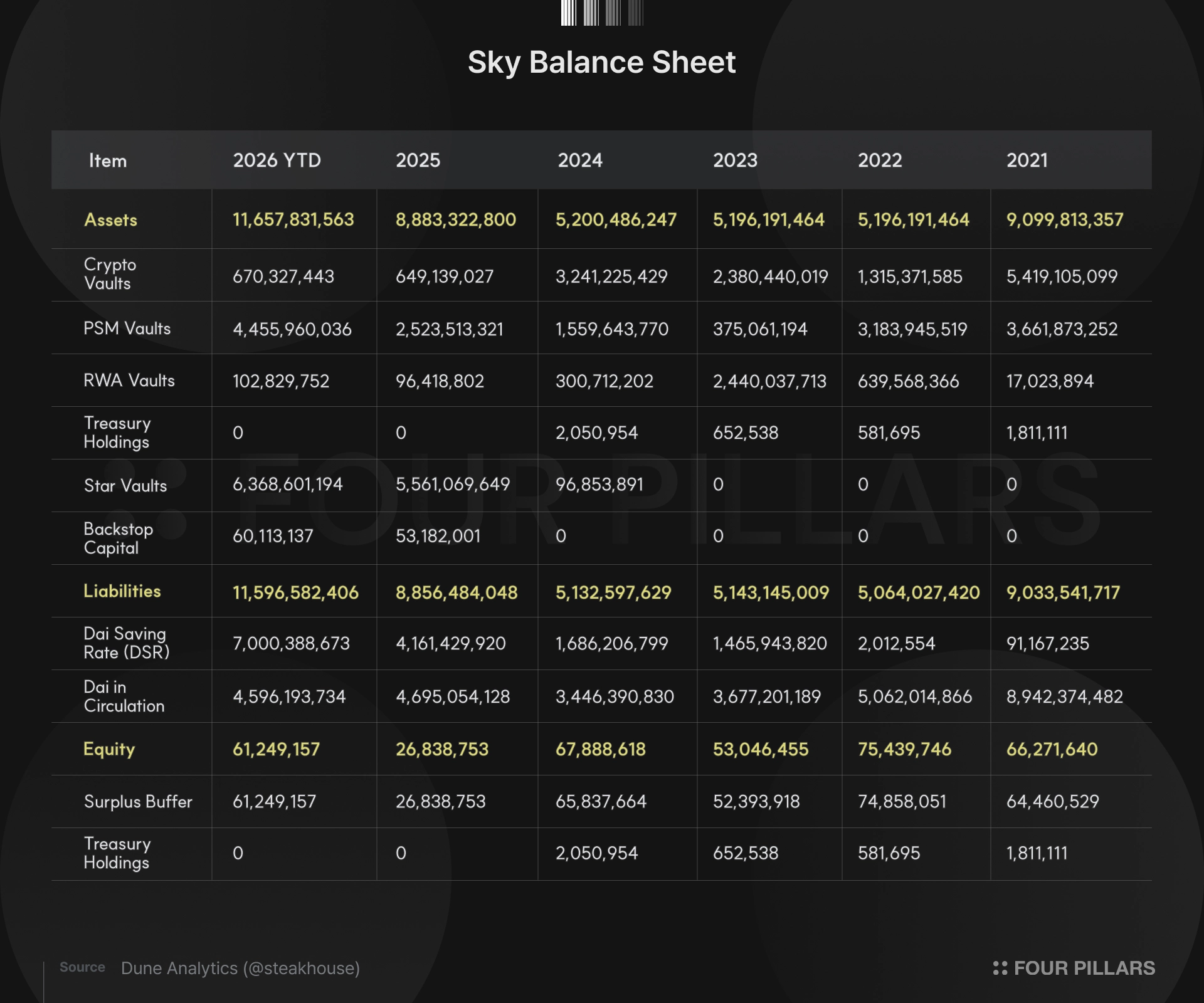

Sky's total assets sit at $12.57B against $62M in equity (surplus buffer). That gives you a leverage ratio around 200:1, but the number means something different here than it would at a bank. The risk profile that makes 200:1 terrifying in TradFi (illiquid assets, opaque credit quality, maturity mismatch) doesn't map onto a programmatically liquidatable, overcollateralized collateral book.

The balance sheet scaled fast. Star Vaults went from zero to $6.4B since October 2024, channeling institutional credit demand through Spark into the protocol's lending book. The model is to borrow via SSR (currently $6.56B at 3.75%), lend through vaults at higher rates, pocket the spread. Net interest margin hit 0.39% in February 2026, but the trajectory wasn't linear. NIM was 0.09% in February 2025, went negative in November (-0.012%), and was still 0.09% in January 2026 before the February jump. Gross revenue that month was $57.28M, the best in protocol history. The P&L, which bled $90.81M across 2025, flipped to +$27.61M in the first two months of 2026.

Annualizing the two-month run rate gives roughly $166M, or about 10x P/E against a $1.68B market cap. But February alone accounts for the bulk, with January's net interest revenue at $9.3M and February's at $41.5M. Normalizing over six months and annualizing gives roughly $110M after operating costs, closer to 15x P/E. SKY trades at roughly 25x P/TBV ($1.6B FDV against $62M in equity).

Either way, this is a spread business on an overcollateralized book. There is no operating leverage moment where margins go from 30% to 70%. Deposits cost 3.75%, lending earns slightly more, and growing the book from $12.6B to $25B doubles revenue but also doubles deposit costs. The surplus accumulates linearly, not exponentially.

The old vow.flap() pathway is dead (vow.bump = 0, vow.hump set to the maximum uint256). The active buyback route runs through Kicker.flap(), which triggers Splitter.kick(), which routes to FlapperUniV2SwapOnly.exec(). That last contract swaps USDS for SKY on UniV2 and sends it to a receiver address. No LP creation, no impermanent loss. The FlapperUniV2 contract that did create LP was replaced in February 2025, and all existing LP was unwound in March 2026.

Now look at what governance did in one month.

February 26: emissions cut roughly 16.2% (1B to 838.18M SKY per 180 days).

March 8-9: SSR cut from 4.0% to 3.75%.

March 13: SBE(Smart Burn Engine) kbump cut 87.5% (approximately 48K to 6K USDS per lot).

Three parameter changes in three weeks. USDS depositors took a 25bp rate cut, so all stakeholders shared some pain. But an 87.5% cut to the buyback versus 25 basis points off the deposit rate tells you where the adjustment falls when margins need managing. The deposit rate can't move much without losing depositors, so tokenholder returns become the adjustment variable. The kbump parameter is flat-rate, denominated in USDS per lot, not a percentage of revenue or a function of balance sheet size. Protocol assets grew from roughly $5B to $12.57B in fifteen months and the pipe to tokenholders never widened. Then governance cut it by seven-eighths.

Which read you take determines whether SDEV's governance position matters. The short-term read is that governance cut tokenholder returns on every available margin. Revenue doubled, the buyback ran on fixed-rate plumbing that never scaled, and then governance made it smaller.

The long-term read is that every dollar that doesn't leave through the SBE stays in the surplus buffer. The SBE was running roughly $300K per day, about $110M annualized. After the cut, that dropped to roughly $37.6K per day, about $13.7M annualized. The difference, nearly $96M per year, now accumulates in the surplus buffer instead. Governance didn't destroy value. It redirected it from current distribution to surplus accumulation.

On the emissions side, DssVestMintable mints SKY at roughly 10.73% APY on staked supply, translating to about 7% annual inflation on total supply after the February cut. At $1.68B FDV, that's roughly $118M per year in dilution, which means at the $110M normalized earnings figure, the protocol generates just enough to offset what emissions take away.

I don't hold SKY. I think this token only works under one specific configuration. Staked, with a governance catalyst you can't time. If you're not staking, you're losing ground to annual dilution with no income to show for it. If you are staking, you're flat against dilution while waiting for a pipe that governance to eventually reopen. And even then, what you're waiting for is mainly a spread business where the surplus accumulates linearly.

But if you're institutional capital that can stake, sit on a multi-year horizon, and build governance weight like SDEV, the picture inverts. You neutralize the dilution, you're buying into a $12.57B lending business at 15x normalized earnings with a real floor under it, and the surplus stays on the balance sheet, available for growth or eventual redistribution. From here, you need time and NIM.

Dive into 'Narratives' that will be important in the next year