What Happened?

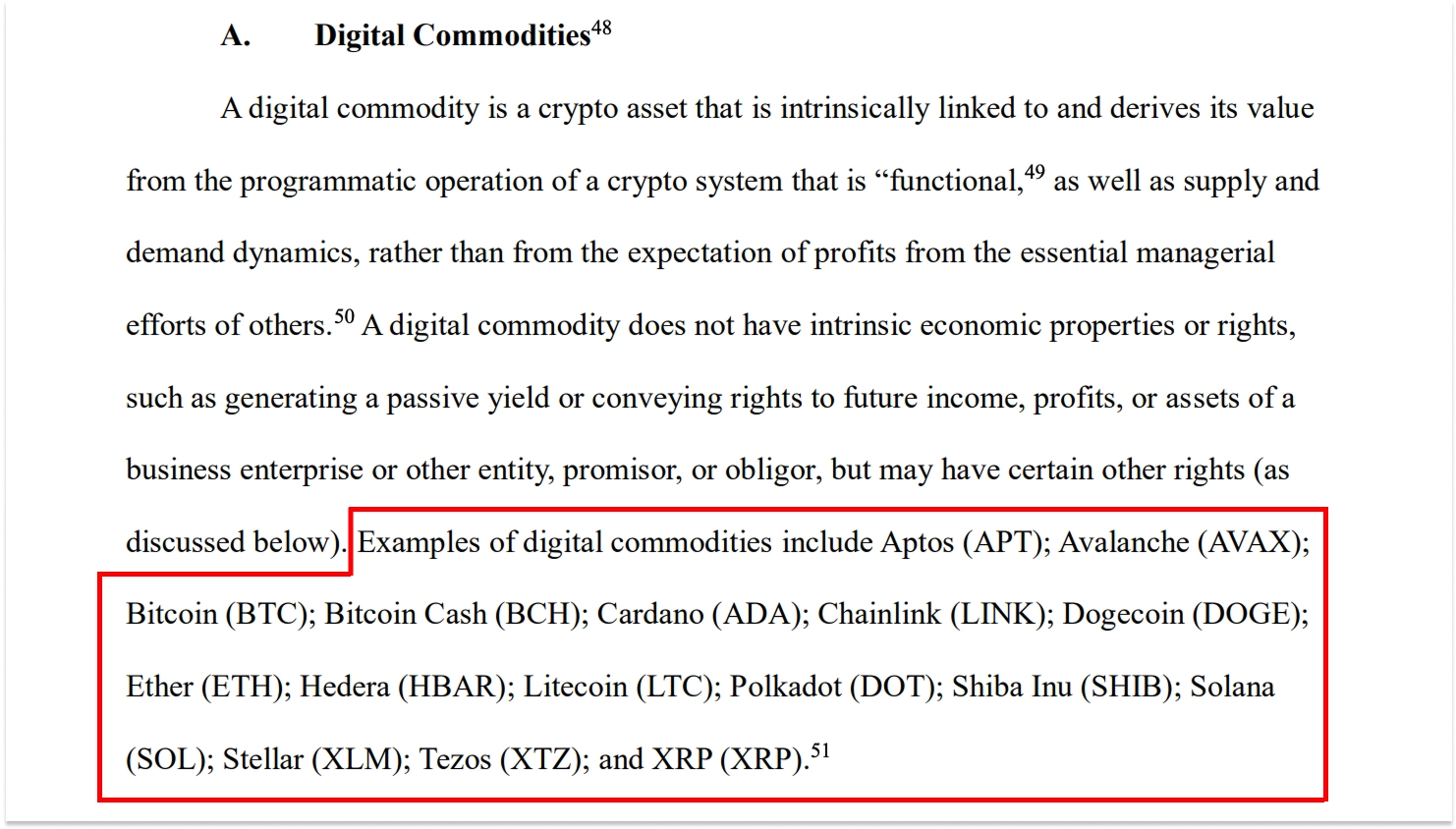

The SEC and the CFTC released a 68-page joint interpretive statement classifying 16 crypto assets as digital commodities. The list includes Bitcoin, Ethereum, Solana, XRP, Dogecoin, Cardano, Avalanche, Chainlink, Polkadot, Hedera, Litecoin, Bitcoin Cash, Shiba Inu, Stellar, Tezos, and Aptos. These assets are no longer subject to securities law and now fall under CFTC jurisdiction.

The interpretive statement also established an official taxonomy that divides digital assets into five categories: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. Of these, only digital securities remain under the SEC's securities law jurisdiction. Immediately after the announcement, current SEC Chair Paul Atkins said, "We're not the securities and everything commission anymore," signaling a clear break from the Gensler-era approach of asserting broad jurisdiction over nearly all crypto activity.

Staking, mining, airdrops, and the wrapping of non-security tokens were also excluded from securities transactions. The statement further clarified that even tokens initially sold as investment contracts may lose their securities status once the network becomes sufficiently decentralized. This narrows the scope of the Howey test while establishing, for the first time, the principle that a token's regulatory status can change over its lifecycle.

That said, the interpretive statement is an executive branch guidance document, not law. For it to gain permanent legal force, Congress must pass the CLARITY Act. The bill passed the House in July 2025 and cleared the Senate Agriculture Committee in January 2026, but still awaits a vote in the Senate Banking Committee. Reports this week indicated that the committee is targeting an April vote, while an agreement on the stablecoin yield provision has already been reached, removing what had been the bill's biggest obstacle.

Researcher’s Comment

This is the first time the SEC and the CFTC have answered the decade-old question, "Is this token a security or a commodity?" through an established framework rather than through piecemeal litigation. In particular, the five-category classification system makes it possible to predict, from launch, which regulatory regime a new token is likely to fall under. Regulatory uncertainty has long been one of the largest valuation discounts across the crypto industry. This creates a path for that discount to shrink structurally.

The practical impact is likely to appear first in the ETF and derivatives markets. Now that 16 assets have been classified as digital commodities, trading them on CFTC-regulated futures markets has a clearer legal basis, which is a prerequisite for accelerating the ETF approval process. In fact, during the same week, Grayscale filed for a Hyperliquid (HYPE) ETF and Morgan Stanley submitted an amended S-1 for a Bitcoin ETF. Clearer classification is directly opening the product pipeline.

At the same time, the statement shows that the SEC's overall approach to crypto has changed. Under Gensler, the SEC filed more than 100 lawsuits against firms including Ripple, Coinbase, and Kraken, litigating the security status of individual tokens in court. Under Atkins, the SEC has been withdrawing those cases one by one while issuing an interpretive statement that organizes token classification in a comprehensive way. It has also signaled that a 400+ page "Reg Crypto" rule proposal could be released within one to two weeks.

Still, the market reaction has been less enthusiastic than many expected. The day after the announcement, the Fed's rate hold and hawkish signal coincided with the release, wiping more than $100B off the crypto market, while BTC fell from $76K to below $70K. Part of that was clearly macro pressure. But it also showed that, with most Layer 1 tokens already down 30% to 60% from last year, regulatory clarity alone is not enough to complete the case for buying tokens. The statement itself is also administrative guidance rather than law, meaning a future administration could reverse it. If Congress fails to pass the CLARITY Act before the August recess, the process could slip into 2027. The framework is now in place, but legal finality and a restoration of market confidence are separate issues.

What Happened?

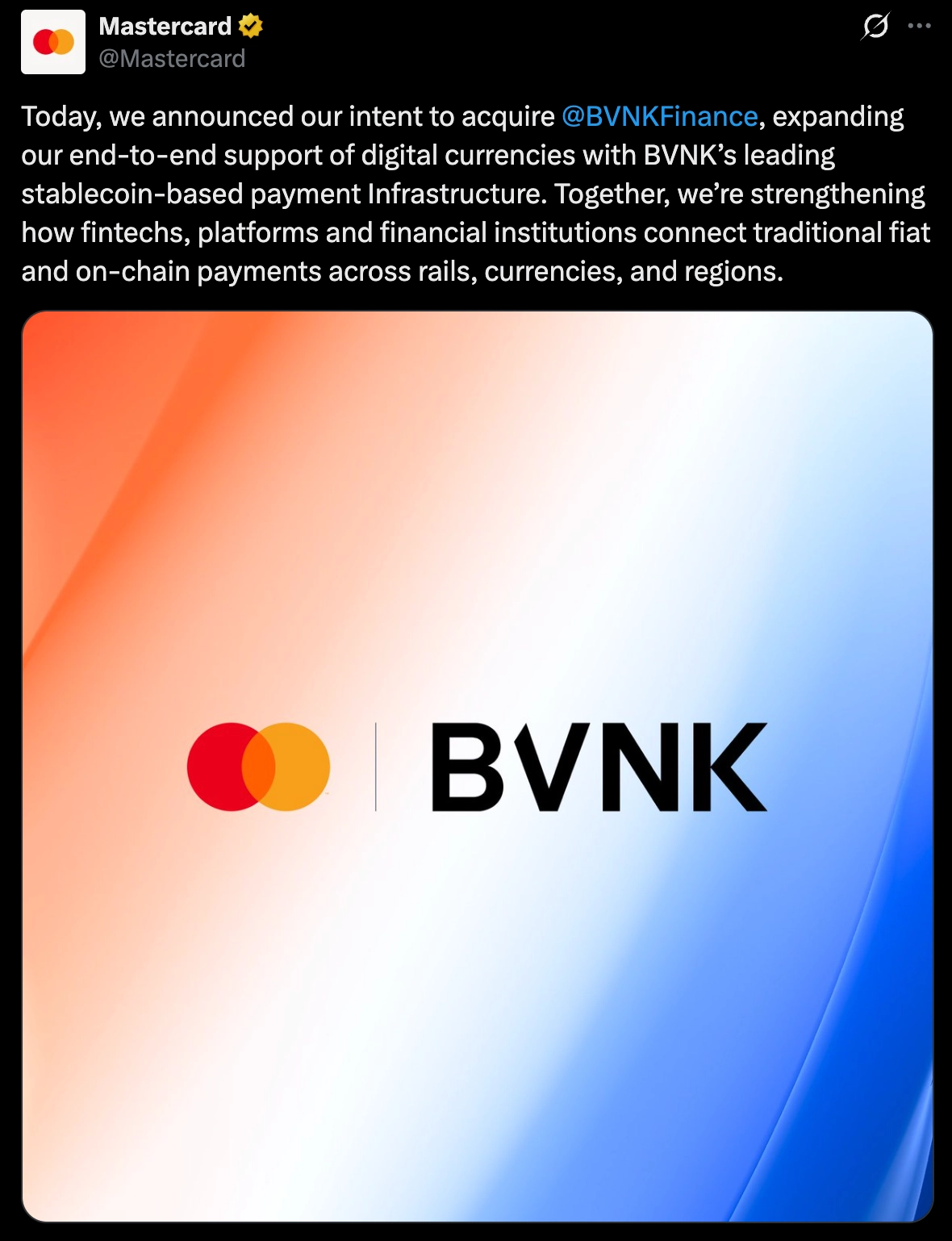

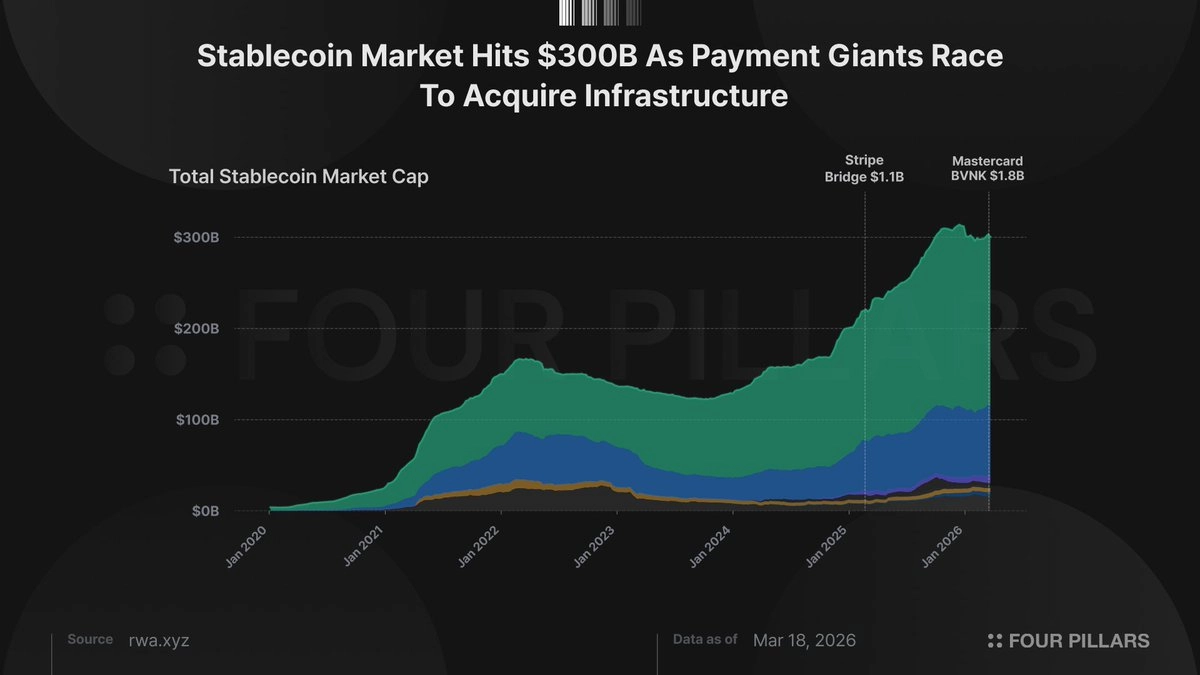

On March 17, Mastercard agreed to acquire London-based stablecoin infrastructure startup BVNK for up to $1.8B. Of that amount, $300M is tied to performance-based earnout conditions, and the acquisition is expected to close within the year pending regulatory approval. The deal surpasses Stripe's $1.1B acquisition of Bridge, making it the largest M&A transaction in stablecoin history.

Since its founding in 2021, BVNK has built infrastructure for stablecoin payments across major blockchains including Ethereum, Tron, and Solana in more than 130 countries. Its platform combines fiat-stablecoin conversion, cross-border payouts, and enterprise wallets into a single stack, and it has already secured major payment clients such as Worldpay, Deel, Flywire, and dLocal. As of 2025, it was processing $30B in annual volume, up 2.3x year over year, while revenue stood at roughly $40M at the end of 2024.

The acquisition followed a competitive process. BVNK held acquisition talks with Coinbase in the second half of 2025 at a valuation of around $2B, but those discussions broke down in November over profitability concerns. Mastercard also explored acquiring Zerohash, a BVNK competitor, at a valuation of roughly $1.5B to $2.0B, but that effort also failed. BVNK's existing investors included Visa Ventures, meaning Mastercard ultimately acquired infrastructure that Visa had not only backed financially but also partnered with.

Mastercard CPO Jorn Lambert said that "most financial institutions and fintechs will eventually offer digital currency services," describing the BVNK acquisition as a move designed "to bring the benefits of tokenized money into the real world." Mastercard already operates the Multi-Token Network (MTN), its own permissioned blockchain infrastructure for tokenized deposit settlement between banks and institutions. In that sense, MTN handles institutional wholesale settlement, while BVNK covers commercial payments on public blockchains.

Researcher’s Comment

The competition among global payment companies to acquire stablecoin infrastructure is now taking on a recognizable pattern. After acquiring Bridge for $1.1B in February 2025, Stripe launched its own blockchain, Tempo, signaling an effort to build proprietary rails that can bypass card networks. Visa, meanwhile, has been settling transactions onchain with USDC since 2023 and now holds more than 90% share in crypto card volume. Mastercard's acquisition of BVNK belongs to the same trend. Once regulation became clearer and the market became more legible, the conclusion appears to have been that the two-to-three-year gap required to build this internally would be more expensive than paying an acquisition premium.

What matters in the BVNK deal is not just the technology. It is also the licensing bundle. Operating stablecoin infrastructure commercially requires jurisdiction-by-jurisdiction licenses, and the time required to secure those approvals is itself a barrier to entry. In the U.S., a firm needs state-by-state money transmitter licenses across 49 states. In Europe, it needs MiCA compliance. In Hong Kong, it needs HKMA approval. Once partner banking relationships and a validated customer base are added on top of that, internal buildout can take years. What Mastercard paid $1.8B for was not just BVNK's codebase, but the entire regulatory portfolio and customer network accumulated over five years.

This acquisition should not be read solely as a defensive move to protect Mastercard's legacy card business. For card networks, stablecoins are a two-sided phenomenon. As Coinbase Payments' integration with Shopify shows, direct USDC payments can bypass card rails entirely and therefore represent a threat. At the same time, stablecoins also open markets that card networks could never fully reach in the first place, especially cross-border B2B payments where correspondent banking can cost $20 per transaction and take three to five days to settle. Mastercard's bet reads less like a defense of existing card volume and more like a bid to capture that new TAM.

That said, the self-cannibalization risk remains. If the same transaction shifts from cards to stablecoins, Mastercard may still remain somewhere in the flow, but its revenue per transaction will decline. In card payments, merchants typically pay 2% to 3% in total transaction costs, of which Mastercard captures only a few basis points as network fees. By contrast, a USDC payment on Base costs roughly one cent per transaction. The margin Mastercard can earn on stablecoin rails is structurally thinner. The key question for the BVNK deal is whether volume from new TAM can offset that compression, and how quickly stablecoins expand their share of real-world payment activity.

What Happened?

Tempo, a payments-focused Layer 1 blockchain incubated by Stripe and Paradigm, officially launched its mainnet. At the same time, it open-sourced the Machine Payments Protocol (MPP), a standard co-developed with Stripe. MPP is a protocol that standardizes how AI agents and software services request, approve, and settle payments programmatically.

Since emerging publicly in September 2025, Tempo raised $500M in its October Series A round at a $5B valuation, with Thrive Capital, Greenoaks, and Sequoia among the participants. After launching a public testnet in December, it has now gone live on mainnet this week. Design partners include Visa, Mastercard, Deutsche Bank, Standard Chartered, Revolut, Nubank, Shopify, OpenAI, Anthropic, Ramp, and DoorDash.

MPP is a protocol for session-based payments between AI agents. When an agent opens a session with a service, it prefunds the session, processes multiple API calls offchain, and then settles the entire session with a single onchain transaction once the session ends. As of launch day, more than 100 services, including Alchemy and Dune Analytics, had already been listed in the MPP-compatible payments directory.

Although MPP runs on Tempo, it is designed to remain rail-agnostic. Through a single token standard called SPT (Shared Payment Tokens), it abstracts stablecoins, cards, wallets, and BNPL into one protocol layer. That means an agent can move between a data API call paid with stablecoins and an airline booking paid with a credit card within a single task, while rail selection is handled at the protocol level. Visa has extended MPP into its own card network, while Stripe integrated it with its own payment methods, including cards and wallets.

Researcher’s Comment

The feature that drew the most attention alongside Tempo's mainnet launch was MPP. MPP was built as a separate protocol rather than as an extension of Coinbase's x402. While the two are interoperable because both use the same HTTP 402 primitive, Stripe's official documentation clearly distinguishes them as separate protocols.

MPP's session-based structure is designed around how agents actually consume services. Humans tend to make occasional large payments. Agents are the opposite. Their default pattern is to make hundreds of API calls while repeatedly paying micro-amounts, often just a few cents or less per request. If every call triggered an onchain transaction, blockchain throughput and fees would become the ceiling on an agent's speed and cost efficiency. MPP solves this by prefunding a session, handling requests through offchain vouchers, and then settling the session with a single onchain transaction at the end. In other words, it fixes the number of onchain actions to the number of sessions rather than the number of requests. If Coinbase's x402 is request-level payments, MPP pushes the abstraction one level deeper into session-level payments.

Rail neutrality is another key design difference. Through SPT (Shared Payment Tokens), MPP abstracts stablecoins and card/wallet rails into a single protocol. Even if an agent moves between a data API call paid with stablecoins and an airline booking paid with a credit card within one task, the rail transition is handled at the protocol level. That said, any agent payment routed through Stripe rails is still subject to Stripe's standard fees. Stripe is open-sourcing MPP as an open standard, but at the same time it is clearly trying to capture the payment traffic created by that abstraction inside its own ecosystem.

This week saw Mastercard's acquisition of BVNK, Visa's release of agent-focused CLI tooling, and Tempo's MPP mainnet launch all happen at once. Payment infrastructure companies are internalizing stablecoins and agent payments in different ways. Mastercard is doing it through acquisition. Visa is doing it by extending its existing card network. Stripe is doing it through its own blockchain and protocol stack. The methods differ, but the direction is the same. The blockchain transition of payments infrastructure is no longer a set of isolated experiments. It is accelerating into an industry-wide structural shift.

Crypto

Resolv’s USR stablecoin depegs after attacker mints 80M unbacked tokens, ~$25M exploited

Tally, governance solution used by Uniswap and Arbitrum, to shut down

Coinbase launches perpetual futures on M7 stocks including Apple, Tesla, and Nvidia

Institution

CFTC grants no-action relief on broker registration for Phantom wallet’s derivatives trading feature

Lawmakers reach agreement on stablecoin yield provisions, clearing major hurdle for the CLARITY Act

S&P Dow Jones licenses S&P 500 perpetual futures brand to Hyperliquid

Tech

Sui begins testing new VM with full execution layer rewrite, mainnet rollout expected in early April

Alchemy expands x402-based onchain payment APIs for AI agents

Visa Crypto Labs launches CLI tool for autonomous AI agent payments

Investment

Asia

South Korean lawmakers push to abolish planned 22% crypto tax

Vietnam moves to restrict overseas exchanges; five bank-backed firms pass initial licensing review

Metaplanet raises $531M targeting global institutions, sets goal of 210,000 BTC by 2027

Stablecoins have already become one of the largest payment rails in the world. With roughly $300B in market cap, $8.93T in monthly transfer volume, ~237M holders, and ~48M monthly active addresses, the scale is comparable to traditional networks. For context, Mastercard processed $10.6T in total volume for all of 2025, while stablecoins are handling nearly that much every single month.

The market is continuing to grow rapidly. Market cap is up ~50% year over year, and the number of holders increased by +4.95% in the last 30 days alone. USDC saw $4.9B in net inflows over the same period.

The market structure remains dominated by two major players but is gradually fragmenting. Tether holds $185B (61%), while Circle accounts for $77B (26%). The remainder is increasingly distributed across newer entrants such as Sky Ecosystem ($7.7B) and Ethena ($5.9B).

Against this backdrop, Mastercard’s $1.8B acquisition of stablecoin payments infrastructure firm BVNK is a natural progression. BVNK processes approximately $30B in annualized volume and provides an orchestration layer that unifies fragmented chains, assets, and settlement flows. The deal reflects Mastercard’s strategy to internalize abstraction over the fragmented stablecoin payment stack rather than relying on external providers.

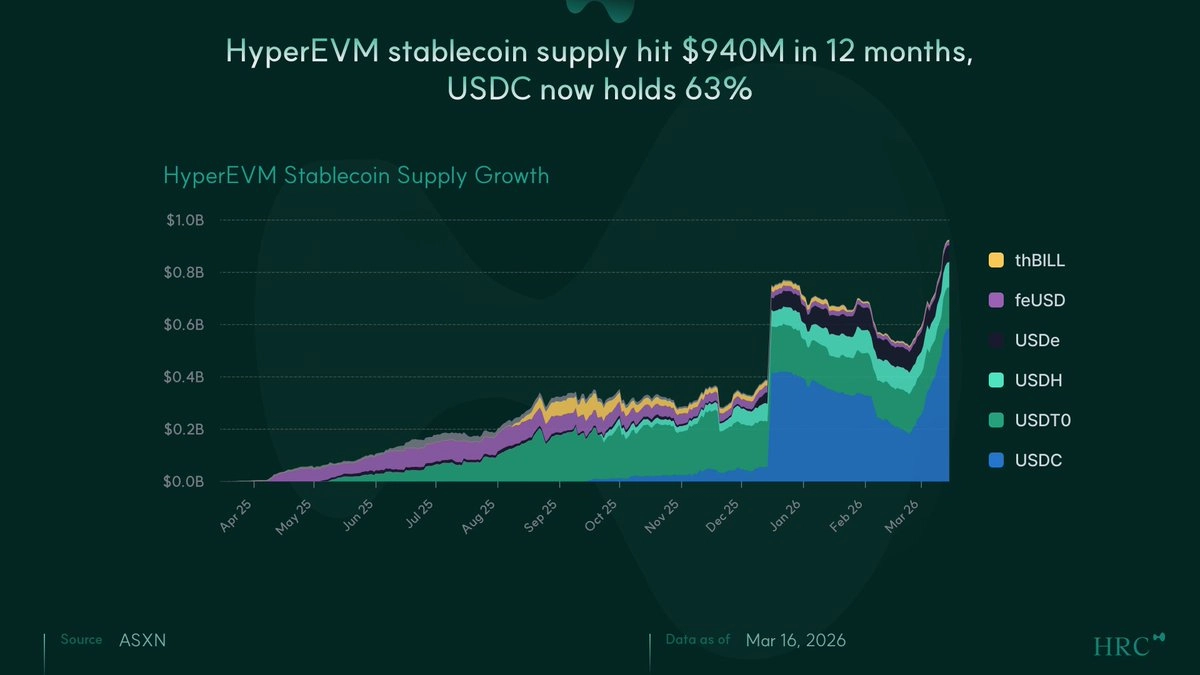

HyperEVM stablecoin supply surpassed $1.1B, up from $713M at year-end 2025. USDC dominates at $803M (73%), USDT0 holds $158M (14%), USDH $96M (9%).

Circle deployed native USDC on HyperEVM via CCTP V2 on Dec 8, 2025, enabling direct deposits from 12+ chains. On Dec 15–16, USDC saw +$360M inflow in two days, the largest single event in HyperEVM history. USDC has since overtaken USDT0 as the dominant stablecoin on HyperEVM, now holding ~73% share at $803M versus USDT0's $158M.

USDH holds 3rd place at $96M with steady, gradual growth. USDe declined to $63M as Ethena funding rates turned negative in Q1 2026.

MPP inherits x402's 402 flow, but it is a separate protocol that redesigns sessions and settlement. If x402 is on-chain payment by request, MPP is session-based payment built on deposit, streaming, and batch settlement.

MPP breaks down the "card versus crypto" frame through rail agnostic. Within a single task, an agent can move across stablecoins and cards, and MPP abstracts that shift at the protocol level.

MPP and x402 differ in the depth of abstraction. MPP ties x402's components into a single layer. At the same time, it is part of Stripe's platform strategy to capture the value of agent payments within its own ecosystem.

x402 and MPP have a complementary relationship. One is bottom-up and the other is top-down. The future of 402-based agent payments will depend on whether a flywheel emerges in which one side absorbs the other's innovations.

Ethereum's P2P network performance is determined not by peer count, but by the quality of mesh composition, and nodes in regions with low node density face structural disadvantages. GossipSub forms a mesh of just 6 to 12 peers per topic, and peer scoring causes high-latency nodes to fall into a vicious cycle of mesh exclusion. In node-dense regions like Europe and North America, nearby peers boost each other's scores in a virtuous cycle, while nodes in Asia, South America, and Africa can be pushed out of the mesh and remain periphery peers even with the same number of connections.

Upcoming Ethereum roadmap changes including FOCIL, PeerDAS, and slot time reduction will further strengthen the need for geographic diversity. FOCIL's censorship resistance relies on the geographic diversity of its 17-member committee, the evolution from PeerDAS to Full DAS depends even more heavily on the geographic distribution of data columns, and shorter slot times amplify the impact of regional latency gaps.

Running validators in non-Western regions requires more effort, but operators can contribute to the global balance of GossipSub meshes through forming regional node clusters, leveraging DVT, and engaging in governance. At the same time, major staking pools like Lido should prioritize geographic diversity in operator onboarding, and the Ethereum protocol itself must evolve to lower barriers to entry for non-Western regions. Meaningful geographic diversity requires the combined efforts of individual node operators, major staking pools and institutional stakers, and protocol designers.

$328M in buybacks at 99.5% daily precision for 8 months, corroborated by two independent aggregators that weren’t consulted and agree on the number. Manipulating numbers requires fabricating revenue that simultaneously fools DeFiLlama, matches Adam_tech’s Dune Solana-only indexing at a stable 68-69% ratio, and is backed by 105.17B PUMP sitting in verifiable wallets.

The August 2026 “dilution cliff” is a substitution, not a stack, and the buyback absorbs 2x new supply at current revenue. Community emissions stop when team/investor vesting starts. Monthly emissions go from 10B to 9.2B.

What’s actually suppressing the multiple is categorical (sin stock), trust-based (pseudonymous team, discretionary buyback), and flow-driven (alleged insider selling into the buyback).

As of Mar 12, MORPHO trades at $1.96B FDV on zero tokenholder revenue, all-time. The fee switch that would change this has never been proposed in 128 Snapshot votes.

Governance is essentially a four-player game. Stake Capital, Gauntlet, NEMO Ventures, and leuts.eth hold the majority. They have little incentive to turn on the fee switch. Even if they did, the bull case (25% fee, 25x multiple) implies $756M: 30% below where the token trades today.

123.9M tokens unlock over the next 12 months, a 22.6% increase in circulating supply (per Coingecko). Apollo covers 18 cents on every dollar of that at maximum pace, and almost certainly via OTC, not open market.

Morpho can be the dominant lending protocol and MORPHO can be a bad token at the same time, because protocol moats and token value accrual are different questions entirely.

MoneyX is a conference representing the Asian finance and fintech industry, hosted by JPYC, Progmat, TV Tokyo, SBI Group, and CoinPost. It serves as a platform to discuss key issues shaping the next generation financial ecosystem, including digital assets, stablecoins, payment infrastructure, and regulatory environments.

Four Pillars participated in MoneyX as the exclusive research partner, and this article aims to share summaries of the sessions as well as various insights related to the Japanese market gained on site.

Contrary to common perceptions in the global market, Japan appears to be one of the most open markets toward the transition to onchain finance. Its approach, which emphasizes compliance first and internalization strategies, as well as a coexistence model for CBDCs, deposit tokens, and stablecoins, provides valuable examples that other countries may reference.

Lido faces two competing challenges: decentralization and operator reliability. IDVTC is a strategic attempt to address both simultaneously by combining identity verification (ICS) with DVT.

Lido has spent two years validating DVT adoption through SimpleDVT, and the voluntary DVT adoption observed within CSM serves as the foundation for proposing IDVTC.

IDVTC converts DVT's risk reduction into economic incentives. Distributed validator operation lowers the risk of penalties and slashing, and that reduced risk translates into lower bond requirements and greater capital efficiency. For Lido, which pursues both structural safety and decentralization, IDVTC is a significant milestone.

Dive into 'Narratives' that will be important in the next year