Japan remains a market with a high share of cash usage, yet at the same time has built one of the most pioneering and systematic cryptocurrency regulatory frameworks in the world. This regulatory clarity removes uncertainty for businesses and provides an optimal environment to expand operations stably across exchanges, stablecoins, tokenization, and more.

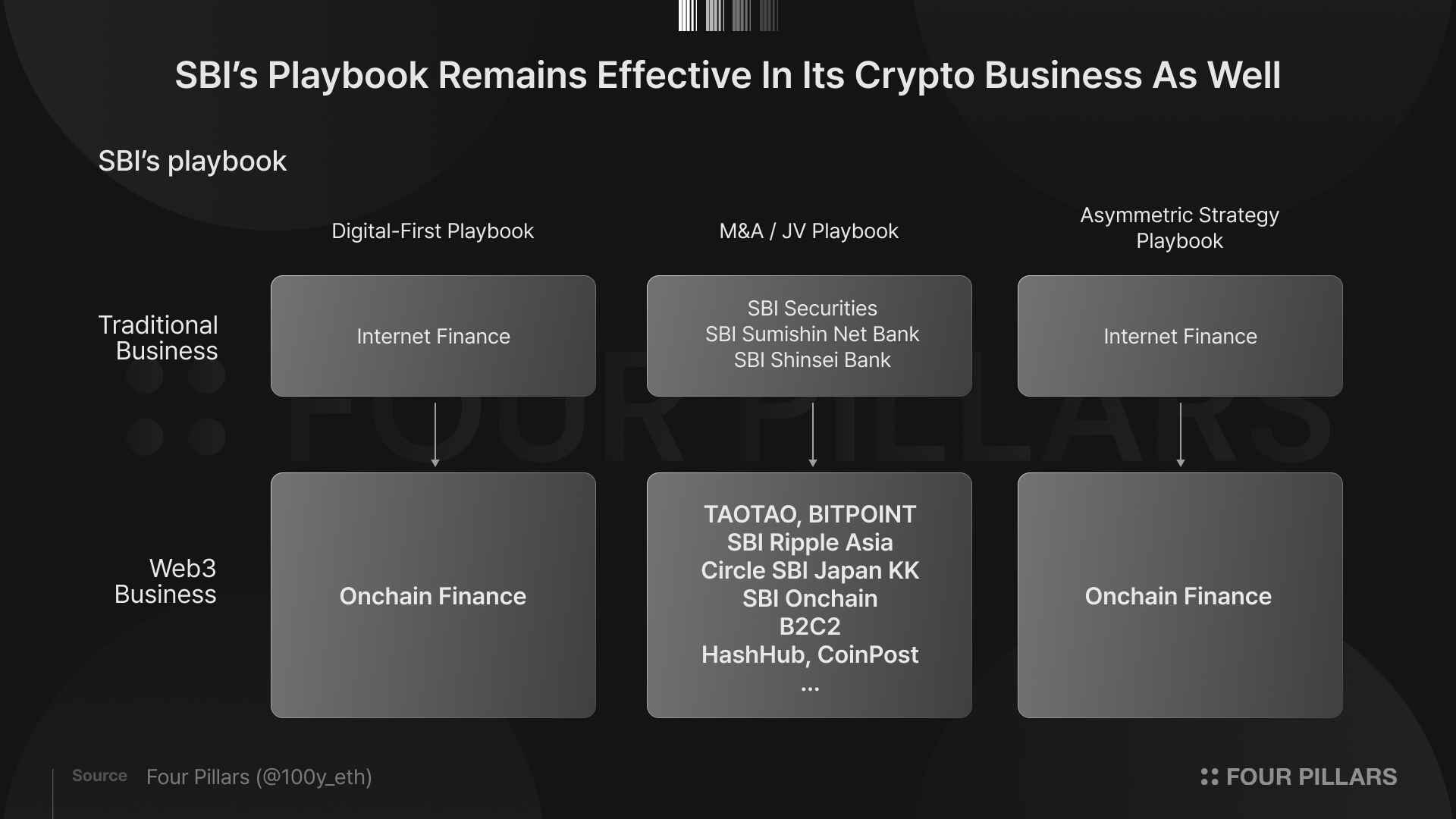

SBI has grown based on a digital-first DNA that originated from internet-based finance, a platform expansion strategy through M&A and joint ventures, and an asymmetric strategy that avoids head-on competition while preempting new markets. This playbook is directly applied to its cryptocurrency business as well, serving as the driving force behind rapid expansion across exchanges, market making, stablecoins, tokenization, and beyond.

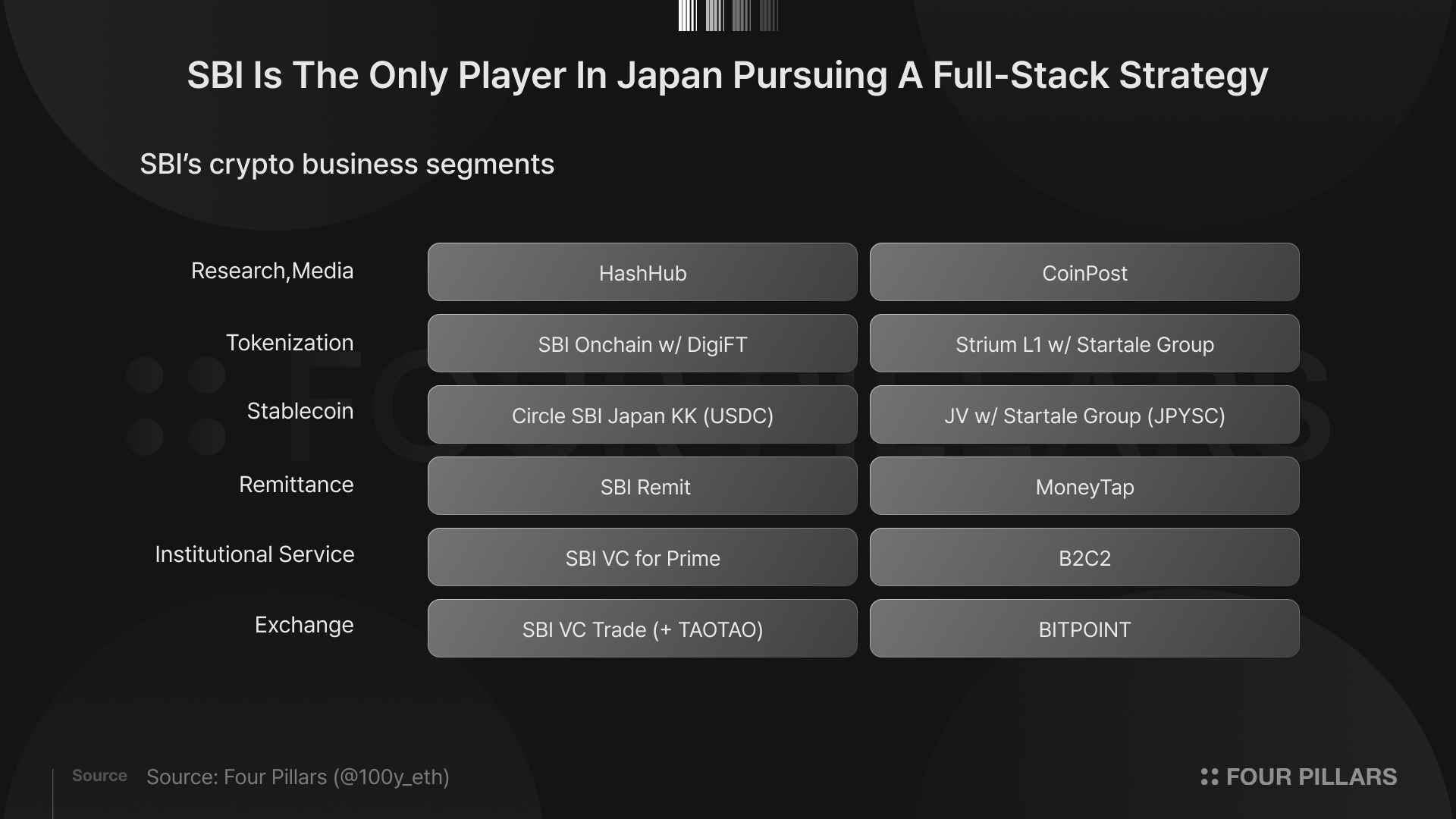

Unlike megabanks such as MUFG and SMBC, which focus on specific areas like infrastructure or payments, SBI is building a full-stack strategy centered on exchanges that connects liquidity, payments, investment, and tokenization. Through this, SBI is positioning itself not just as a participant in the cryptocurrency business in Japan, but as a key player designing a new financial infrastructure that integrates traditional finance and digital assets.

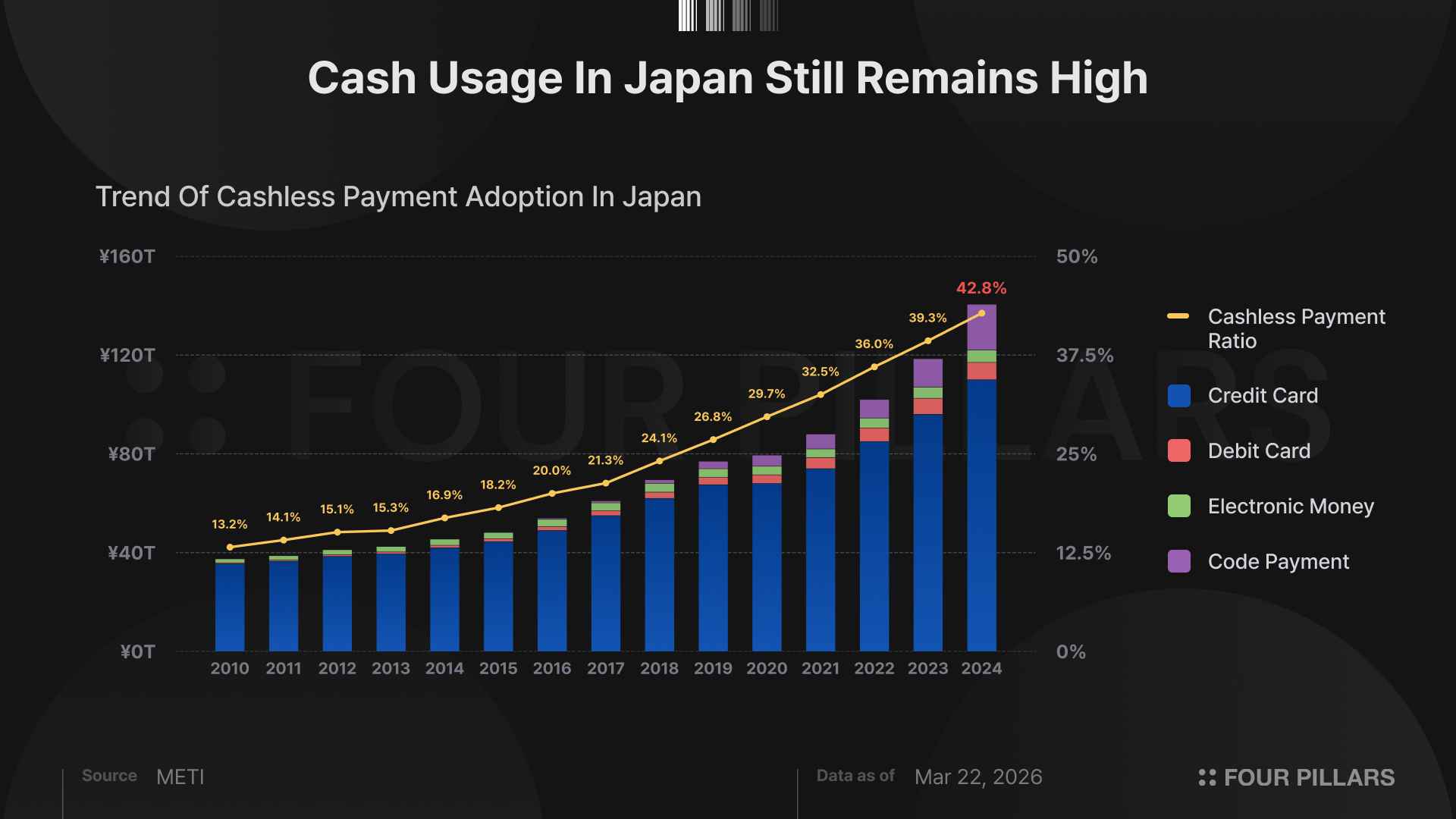

The dazzling night skyline of Tokyo and its towering buildings. Many people think of Japan as a country of cutting-edge technology and a highly advanced financial market. In reality, Japan’s financial market is indeed built on a massive economy, ranking third in the world after the United States and China. However, contrary to this image, there is an interesting characteristic in everyday life in Japan. That is the continued high reliance on cash usage.

According to Japan’s Ministry of Economy, Trade and Industry (METI), the cashless payment ratio in Japan in 2024 was 42.8%, which has been steadily increasing each year, but conversely, cash payments still account for 57.2%. Considering that neighboring countries such as China and South Korea have cashless payment ratios exceeding 80%, it becomes clear that despite having a large financial market, Japan still shows relatively low adoption of financial technology among consumers.

There are multiple social and cultural factors behind the high proportion of cash payments in Japan. The first factor is low inflation. Japan has experienced low prices and deflation for about 30 years following the collapse of the bubble economy. As a result, the perception has formed that holding cash does not significantly erode its value, which has contributed to the continued use of cash. The second factor is an aging society. Japan has a very high proportion of elderly population, and in general, older individuals tend to be relatively less receptive to adopting new payment methods or digital technologies. This demographic structure also plays a role in maintaining the high share of cash payments in Japan.

As discussed above, Japan is a country with a very high proportion of cash usage. However, paradoxically, Japan also has one of the clearest and most crypto-friendly regulatory frameworks in the world. Considering that cash is the most fundamental form of money while cryptocurrency represents its most innovative form, this contrast is striking. Despite the slow market adoption of financial technology, Japan exhibits an interesting structure where regulation moves far ahead.

When it comes to cryptocurrency, it is no exaggeration to say that Japan has been the most pioneering country in establishing regulations globally:

2016 Payment Services Act (PSA) Amendment: In 2016, Japan became the first country in the world to legally define cryptocurrency. This was driven by the 2014 Mt. Gox incident. After Mt. Gox, a Japan-based cryptocurrency exchange, was hacked for approximately 850,000 BTC, the Japanese government recognized the need for exchange regulation and amended the Payment Services Act. Key changes included 1) the legal definition of virtual currency, 2) mandatory registration of cryptocurrency exchanges with the Financial Services Agency (FSA), and 3) the introduction of user protection regulations for exchange customers.

2019 Amendments to the Payment Services Act and the Financial Instruments and Exchange Act (FIEA): Following the Mt. Gox incident, the 2018 hack of Coincheck, which resulted in a loss of approximately $500 million, led to further strengthening of investor protection and derivatives regulation. As a result, both the PSA and FIEA were amended simultaneously. For reference, FIEA is Japan’s securities law. These amendments strengthened exchange-related regulations such as stricter requirements for segregation of customer assets and enhanced security system standards, while also introducing regulatory frameworks for cryptocurrency derivatives and ICO/STO.

2022 Introduction of Stablecoin Regulation: In June 2022, Japan introduced one of the world’s first dedicated regulatory frameworks for stablecoins. This was implemented through amendments to the Payment Services Act, introducing a new concept called Electronic Payment Instruments (EPI). Only banks, trust companies, and fund transfer service providers are permitted to issue stablecoins, and they are required to maintain 100% reserves. Businesses seeking to distribute stablecoins must also register with the FSA.

2023 Implementation of the FATF Travel Rule: The Travel Rule is an international anti-money laundering standard that requires the transmission of sender and recipient information during cryptocurrency transfers, with the goal of ensuring AML/CFT compliance. Japan amended the Act on Prevention of Transfer of Criminal Proceeds, mandating that all virtual asset service providers (VASPs) in Japan comply with the Travel Rule.

In addition, in 2025, further amendments to the Payment Services Act introduced a new licensing regime for cryptocurrency brokerage businesses alongside stablecoins, and granted the government authority to order exchanges to hold assets domestically within Japan. More recently, there have been official efforts to shift cryptocurrency regulation from the PSA to the FIEA, signaling that the Japanese government increasingly views crypto not as a payment method but as an investment product subject to securities regulation.

Over the years, Japan has introduced cryptocurrency regulations in a phased manner through amendments to the PSA and FIEA. In other words, the Japanese cryptocurrency market has already moved past the stage of debating whether to allow crypto. The current focus is on how to expand the integration points between cryptocurrency and traditional finance within the institutional framework. This direction from the Japanese government and legislature provides regulatory clarity for the many companies operating crypto-related businesses in Japan.

According to the Japan Virtual and Crypto Assets Exchange Association (JVCEA), as of March 2026, there are a total of 32 cryptocurrency exchanges operating in Japan, including SBI VC Trade and Line BITMAX. In January 2026 alone, monthly spot trading volume reached approximately JPY 1.5444 trillion, indicating a highly active exchange ecosystem.

Moreover, Japan’s blockchain industry participation extends beyond exchanges, with many traditional conglomerates actively involved. Major corporations such as Sony, SBI Holdings, LINE, SMBC, MUFG, NTT Group, and Rakuten are all expanding various crypto-related businesses based on clear regulatory frameworks. This suggests that Japan’s crypto industry is transitioning from a retail-driven exchange market to a broader ecosystem encompassing institutional financial products and payment infrastructure.

In this major transition phase, the most notable player in Japan’s crypto market is undoubtedly the SBI Group. SBI began showing early interest in cryptocurrency as early as 2016, when it invested in the bitFlyer exchange. Since then, SBI has collaborated with Ripple, R3, and Circle, and has acquired numerous crypto-related companies including B2C2, BITPoint, TaoTao, CoinPost, and HashHub. As a result, SBI has been expanding its cryptocurrency business more consistently and aggressively than any other player in Japan.

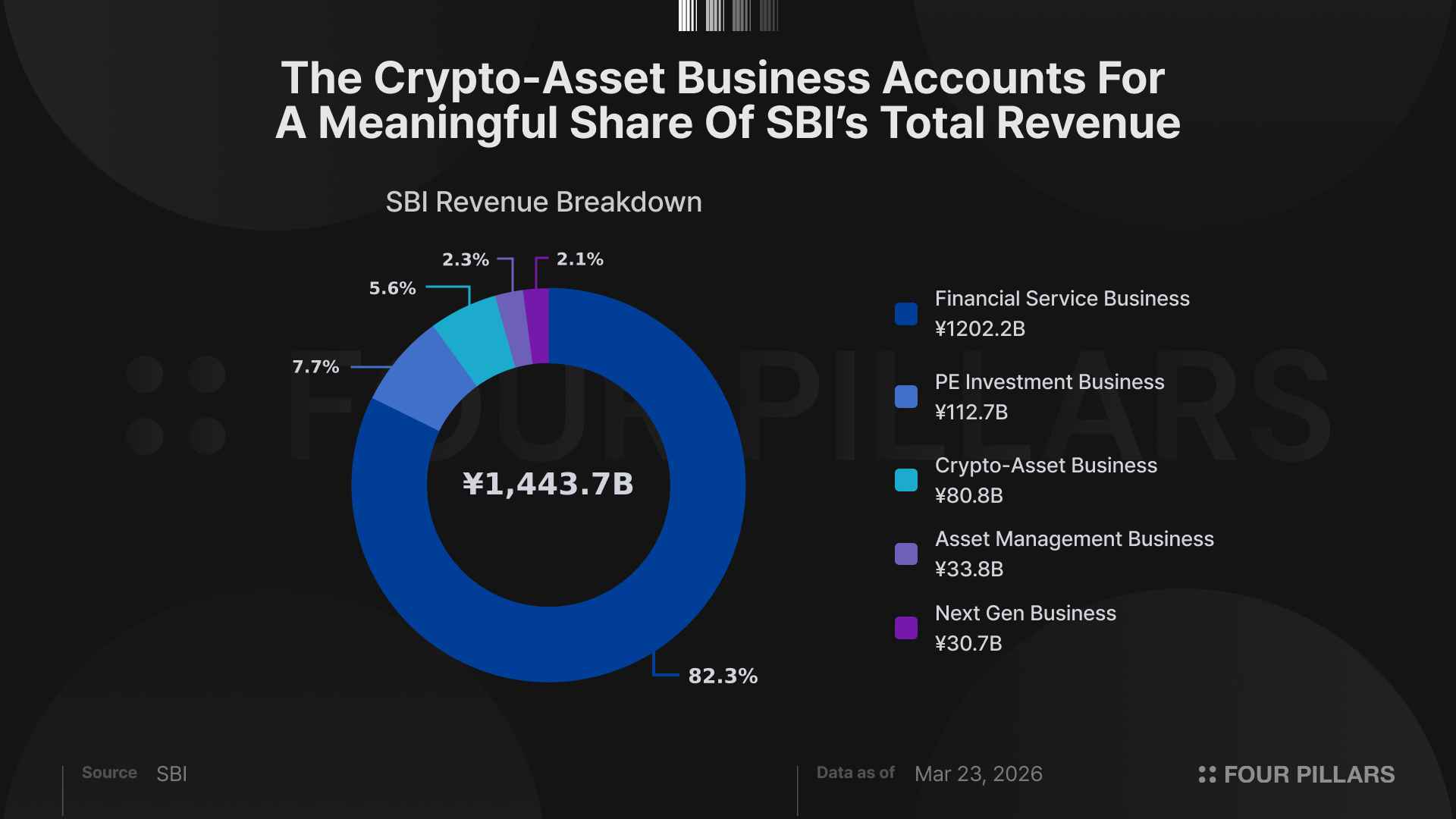

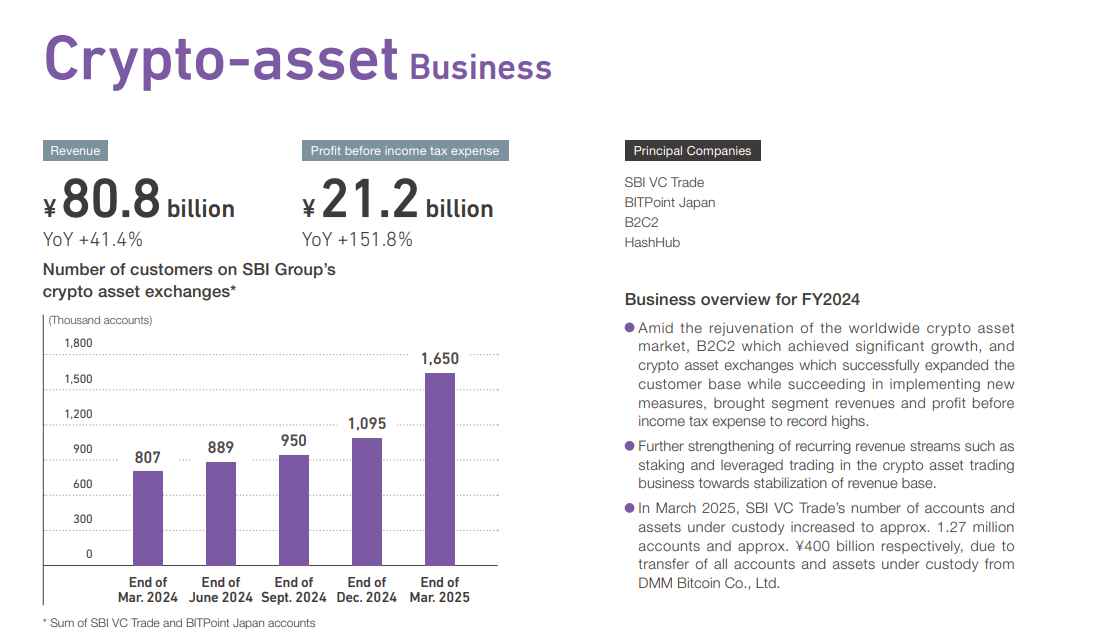

In 2025, SBI Group’s crypto business recorded approximately JPY 80.8 billion in revenue and JPY 21.2 billion in pre-tax profit, representing a year-over-year revenue growth rate of +41.4%. Considering that SBI Group’s total revenue in 2025 was around JPY 1.4 trillion, the crypto business accounted for approximately 5.6% of total revenue. This is a significant share, making it the third-largest business segment within SBI after financial services and private equity investments.

Source: SBI

Why is SBI so deeply committed to cryptocurrency, and how did it become the most influential player in Japan’s crypto market? This article analyzes the path SBI has taken in the crypto business so far, as well as its future trajectory.

2.1.1 The Birth of SBI

SBI was founded in July 1999 in Tokyo, Japan under the name SoftBank Investment Corporation. The company originated as the financial and investment arm of the SoftBank Group, which was rapidly growing at the time through aggressive investments in the internet industry.

SoftBank, founded in 1981 by Masayoshi Son, initially started as a software distribution business. However, in the 1990s, it grew into a core player in Japan’s internet industry through aggressive investments in internet companies and the establishment of Yahoo Japan.

In this context, SoftBank established a separate investment company to expand financial and investment businesses suited for the internet era, which became SoftBank Investment Corporation. The initial purpose of this company was venture capital investment in internet and IT-based companies. In other words, SBI began as the financial services and venture investment arm within the SoftBank Group focused on investing in the growth of the internet industry.

SBI’s founder, Yoshitaka Kitao, was the CFO of SoftBank at the time and a key executive responsible for the group’s investment strategy alongside SoftBank founder Masayoshi Son. He was tasked with expanding the financial and investment businesses within SoftBank, and as a result, established SoftBank Investment and took on the role of CEO.

2.1.2 Entry into Financial Services: SBI Securities

SBI Securities is one of Japan’s leading online brokerage firms and a core financial services company under SBI Holdings today. Its origins trace back to the emergence of internet-based securities services in Japan in the late 1990s.

In the early 1990s, following the collapse of Japan’s bubble economy, the government announced financial system reforms in 1996 to address the crisis. The goal was to build a free and fair global financial market. As part of this reform, financial regulations were significantly relaxed. One of the key changes was the liberalization of brokerage commissions. Previously, stock trading fees in Japan were fixed by the government, but they were partially liberalized in 1994 and fully liberalized in 1999. This triggered price competition among brokerage firms and created the foundation for the emergence of online securities firms.

Amid this shift, SoftBank focused on financial businesses leveraging internet technology and partnered with the U.S. online brokerage firm ETRADE to launch an online securities business in Japan. As a result, in 1998, SoftBank and ETRADE established a joint venture structure called ETRADE Japan and launched an internet-based securities business using an existing Japanese brokerage firm as a base. The company was later reorganized as ETRADE Securities and began offering online stock trading services in October 1999, becoming one of the early players in Japan’s online brokerage market.

In the early 2000s, as SoftBank Group restructured its financial business, the online securities business was gradually integrated under the SBI Group. In particular, in 2003, ETRADE Securities merged with ETRADE Japan, solidifying its position as a core financial services company within the SBI Group.

The company later operated under the name SBI ETRADE Securities, and in 2008, after ending the use of the ETRADE brand in the U.S., it was renamed SBI Securities. This marked its full establishment as SBI Group’s brokerage arm, after which it rapidly grew in Japan’s retail investor-focused online brokerage market. Today, SBI Securities is one of the largest online brokerage firms in Japan, providing a wide range of financial services including stock trading for retail investors, investment trusts, bonds, overseas equities, and IPO underwriting. It serves as a core pillar of the securities business within the internet-based financial ecosystem built by the SBI Group and plays a significant role in Japan’s online brokerage market.

2.1.3 Independence from SoftBank

In the early 2000s, SoftBank Group’s business strategy began to shift. SoftBank reorganized its strategy to focus more on telecommunications and global technology investments, and accordingly, financial businesses increasingly came to be operated under SBI.

As part of this transition, SBI initiated organizational restructuring to evolve into an independent financial group.

In 2005, SoftBank Investment changed its name to “SBI Holdings” and transitioned into a holding company structure. This marked a structural shift from being a simple investment subsidiary within the SoftBank Group to becoming an independent financial group.

The decisive turning point came in 2006. In August of that year, SoftBank sold all of its shares in SBI Holdings, completely ending the capital relationship between the two companies. Through this transaction, SBI became fully independent from the SoftBank Group and established itself as an independent financial services group.

Although the capital relationship with SoftBank ended, the two companies continued some business collaborations. However, in terms of management and governance, SBI began operating as a fully independent entity and, from that point forward, actively pursued its strategy of building an internet-based financial ecosystem.

2.1.4 Launch of an Internet Bank: SBI Sumishin Net Bank

In the mid-2000s, Japan’s financial market saw growing demand for a new type of banking model that could complement traditional branch-based banks alongside the expansion of online financial services. In response, SBI Holdings sought to expand its internet financial platform, while Sumitomo Mitsui Trust Bank aimed to explore new digital financial businesses leveraging its stable financial infrastructure and trust banking capabilities.

The two companies decided to combine their strengths to establish an internet-based bank, and as a result, in September 2007, SBI Holdings and Sumitomo Mitsui Trust Bank jointly founded SBI Sumishin Net Bank.

Unlike traditional banks, SBI Sumishin Net Bank adopted an internet-only banking model that minimized physical branches and provided most financial services online. Through this model, it aimed to lower operating costs and offer competitive interest rates and services while providing a wide range of financial services such as deposits, transfers, loans, and mortgage lending via internet and mobile platforms.

The establishment of this bank marked a key milestone in SBI Group’s strategy to build an internet-based financial ecosystem. SBI had already been expanding retail financial services through its online brokerage business (SBI Securities), and by adding an internet bank, it sought to create a comprehensive digital financial platform connecting securities, banking, and asset management services.

Since then, SBI Sumishin Net Bank has grown rapidly in Japan’s internet banking market and established itself as a leading digital bank. Today, it is considered one of the major players in Japan’s internet banking sector alongside Rakuten Bank, maintaining a top-tier position in terms of deposit size and customer base. Its annual revenue is estimated to be around JPY 120–140 billion, and it serves as a key pillar of SBI Group’s financial services business.

2.1.5 Securing a Traditional Bank: SBI Shinsei Bank

SBI Shinsei Bank represents a significant strategic investment by the SBI Group to secure a traditional commercial bank. The origins of this bank trace back to a financial institution that underwent restructuring during Japan’s financial crisis, and it later pursued a new growth strategy after being incorporated into the SBI Group.

The predecessor of SBI Shinsei Bank was the Long-Term Credit Bank of Japan (LTCB), established in 1952. This bank played a major role in providing long-term financing during Japan’s economic growth period. However, following the collapse of Japan’s asset bubble in the 1990s, it faced severe management difficulties due to a rapid increase in non-performing loans. In 1998, the Japanese government nationalized the bank to stabilize the financial system, and after restructuring, it was relaunched as a new entity.

In 2000, a group of investors led by U.S. investment firm Ripplewood Holdings acquired the bank, and it was rebranded as “Shinsei Bank.” The new management team consisted largely of professionals from foreign financial institutions, and the bank re-entered the Japanese financial market by expanding its retail banking and investment banking functions. In 2004, it was listed on the Tokyo Stock Exchange, establishing itself as a private financial institution.

However, due to the global financial crisis and intensifying competition in Japan’s financial market, Shinsei Bank faced the need to redefine its long-term growth strategy. In this context, SBI Holdings pursued the acquisition of Shinsei Bank to secure a traditional bank that could generate synergies with its existing securities, internet banking, and asset management businesses.

As a result, in 2021, SBI Holdings acquired a stake in Shinsei Bank through a tender offer and became its largest shareholder, incorporating the bank into the SBI Group. Following the group integration strategy, the bank was renamed “SBI Shinsei Bank” in 2023, establishing itself as a core banking subsidiary within the SBI Group.

Today, SBI Shinsei Bank is considered a mid-sized commercial bank in Japan, providing retail banking, corporate banking, and consumer finance services. With total assets of approximately JPY 10 trillion, it is smaller than Japan’s major megabanks such as MUFG, SMFG, and Mizuho. However, it is being utilized as a key bank within SBI Group’s strategy to build a new financial ecosystem in combination with its digital financial platform.

In this way, the incorporation of SBI Shinsei Bank marked an important step for SBI to expand beyond its existing securities (SBI Securities) and internet banking (SBI Sumishin Net Bank) businesses into a comprehensive financial group that also includes a traditional commercial bank.

Looking at SBI’s growth trajectory, we can derive consistent insights into the playbook it has used throughout its business expansion.

The first is a digital-first strategy. SBI has launched almost all of its businesses as internet-based financial services. SBI Securities, SBI Sumishin Net Bank, and SBI Insurance correspond to online brokerage, internet banking, and online insurance respectively, and SBI’s core strategy is to evolve into an internet-based financial platform. Given that SBI was originally founded to invest in internet technology companies, it has consistently maintained this DNA.

The second is a platform expansion strategy through M&A and joint ventures (JV). When entering new businesses, SBI often relies more on acquisitions and partnerships rather than building from scratch internally. The predecessor of SBI Securities was a joint venture with the U.S.-based E*TRADE, SBI Sumishin Net Bank was established as a joint venture with Sumitomo Mitsui Trust Bank, and SBI Shinsei Bank was the result of a stake acquisition. Through strategic acquisitions and joint ventures, SBI reduces initial investment costs while leveraging existing customer bases.

The third is an indirect strategy instead of head-on competition. While SBI is a major player in Japan’s financial market, it is still smaller in scale compared to megabanks such as MUFG, SMBC, and Mizuho. Therefore, rather than competing directly with these institutions, SBI has expanded its business by preemptively capturing new markets, such as building online financial platforms during periods of rapid internet development.

SBI’s recent business expansion moves are notable. In particular, blockchain and cryptocurrency represent a sector where all three of the aforementioned playbooks are being applied simultaneously.

SBI’s active investment and expansion into cryptocurrency and blockchain are driven by both an interest in technological innovation and its strategic positioning within Japan’s financial market. In other words, this is not merely about adopting new financial technologies, but rather a strategy aimed at reshaping the competitive landscape of the existing financial system.

Playbook 1: From its early days, SBI has pursued a strategy of building a financial ecosystem centered on internet-based financial services. It has grown into a digital financial company by connecting various services such as securities (SBI Securities), internet banking (SBI Sumishin Net Bank), asset management, and insurance through online platforms. Within this structure, blockchain technology has been recognized as a key tool for making financial transactions more efficient. SBI has identified blockchain as a technology capable of digitizing core financial infrastructure such as cross-border remittances, payments, and asset transactions, and began expanding related investments and businesses relatively early.

Playbook 2: A key milestone in SBI’s full-scale entry into the blockchain sector was its partnership with the U.S. fintech company Ripple. In 2016, SBI invested in Ripple Labs and became a major shareholder with approximately a 9% stake. In the same year, it established SBI Ripple Asia as a joint venture with Ripple to build a blockchain-based remittance network across Japan and Asia. This initiative aims to create a faster and lower-cost payment infrastructure compared to traditional international remittance systems, and it has been implemented in real financial services through a network of partner banks in Japan.

In addition, SBI has aggressively expanded its blockchain business by investing in, acquiring, and forming joint ventures with a wide range of companies, including blockchain exchanges, Web3 media companies, blockchain research firms, and stablecoin-related businesses.

Playbook 3: SBI’s proactive stance in digital assets is driven not only by technological potential but also by the competitive structure of Japan’s financial market. The Japanese financial industry is dominated by megabanks such as Mitsubishi UFJ, Sumitomo Mitsui, and Mizuho, which control the market through their asset scale and corporate banking networks. In contrast, while SBI operates across securities, internet banking, and asset management, it does not possess the same level of traditional large-scale banking infrastructure. To overcome this structural limitation, SBI chose a strategy of preempting the digital finance and blockchain-based financial markets rather than competing directly within the existing system.

As part of this strategy, SBI is actively pursuing a wide range of initiatives, including operating cryptocurrency exchanges, investing in digital assets, developing stablecoin businesses, and issuing blockchain-based bonds. More recently, it has also been expanding investments in digital asset platform companies and scaling its global cryptocurrency operations. These activities go beyond simple investment, aiming instead to build a new financial infrastructure that connects digital assets with the traditional financial system.

Ultimately, SBI’s strong commitment to cryptocurrency and blockchain can be understood as the result of two strategic objectives combined. First, it seeks to enhance the efficiency of financial services by leveraging blockchain as next-generation financial infrastructure. Second, it aims to secure new growth drivers in digital finance and digital asset markets in order to reshape its relatively disadvantaged competitive position within the traditional financial system. Through this strategy, SBI is positioning itself as a next-generation financial platform company that bridges traditional finance and digital assets.

Among its cryptocurrency businesses, SBI operates across a wide range of areas including exchanges, mining, RWA tokenization, market making, and media. To understand this, it is important to examine how SBI has expanded its operations in the crypto sector. The key milestones in SBI’s cryptocurrency business are as follows:

(2016.01) Strategic investment in Ripple Labs

(2016.04) Investment in Japanese cryptocurrency exchange bitFlyer

(2016.04) Joined the R3 blockchain research consortium

(2016.05) Established SBI Ripple Asia as a joint venture with Ripple Labs

(2016.10) Established SBI Virtual Currencies, a wholly owned subsidiary operating a cryptocurrency exchange

(2017.05) Investment in R3

(2017.08) Began cryptocurrency mining at overseas data centers through subsidiary SBI Crypto

(2017.09) Completed registration as a virtual asset exchange operator with Japan’s FSA

(2017.10) Established SBI Digital Asset Holdings (SBI DAH) to oversee global digital asset operations

(2018.01) Launched SBI AI & Blockchain Fund

(2018.06) Official launch of cryptocurrency exchange service SBI VC Trade

(2018.08) Additional investment in R3, becoming its largest external shareholder

(2018.10) Launched MoneyTap, a Ripple-based P2P remittance app

(2019.01) Established SBI R3 Japan as a joint venture with R3

(2019.03) Announced the establishment of SBI Mining Chip Co., Ltd. to manufacture mining chips

(2019.09) Participated in the establishment of Boostry, a security token issuance platform with Nomura

(2019.11) Investment in global tokenization platform Securitize

(2020.04) Established Singapore-based institutional digital asset firm SBI Digital Markets

(2020.07) Investment in UK-based crypto market maker B2C2

(2020.10) Acquired 100% stake in Japanese crypto exchange TAOTAO

(2020.12) Initiated the establishment of AsiaNext, a Singapore-based crypto exchange, with SIX Group

(2020.12) Acquired approximately 90% stake in B2C2 and made it a subsidiary

(2021.03) Launched SBI Crypto Mining Pool service

(2021.07) Launched XRP-based Japan–Philippines remittance system with Coins.ph

(2021.09) Officially established AsiaNext JV (SBI Digital Asset Holdings + SIX)

(2021.12) Investment in Singapore-based crypto exchange Coinhako

(2021.12) Integration of SBI VC Trade and TAOTAO exchanges

(2022.05) Acquired 51% stake in Japanese crypto exchange BITPOINT

(2022.08) Withdrew from Bitcoin mining operations in Siberia, Russia

(2023.02) Acquired 100% stake in Japanese blockchain research firm HashHub

(2023.02) Fully acquired the remaining 49% stake in BITPOINT

(2023.09) AsiaNext received approval from MAS

(2023.11) Signed MOU with Circle, the largest stablecoin issuer in the United States

(2024) SBI VC Trade launched institutional crypto prime brokerage service “SBIVC for Prime”

(2024.01) AsiaNext launched its first live product, crypto derivatives trading

(2024.04) Signed MOU with Franklin Templeton to establish a crypto ETF management JV in Japan

(2024.09) Signed MOU with Japanese BTC treasury firm Metaplanet and provided operational infrastructure

(2024.11) Following the hack of Japanese crypto exchange DMM Bitcoin, SBI VC Trade acquired customer accounts and assets

(2025.03) Signed agreement to establish a JV with Circle

(2025.03) Bitcoin futures listing on Dojima Exchange

(2025.03) SBI VC Trade obtained Japan’s first license to handle USDC and began distribution

(2025.06) Invested a total of $50 million in Circle

(2025.08) Signed MOU for the distribution of Ripple-issued RLUSD stablecoin in Japan

(2025.08) Acquired a majority stake in Web3 media company CoinPost

(2025.08) Investment in Singapore-based RWA trading platform DigiFT

(2025.08) Announced Japan’s first crypto ETF plan

(2026.08) Announced JV with Startale Group

(2025.09) Announced partnership with Japanese BTC treasury firm Remixpoint

(2025.10) Invested $200 million in XRP treasury firm Evernorth

(2025.11) Established JV “SBI Onchain” with DigiFT

(2026.02) Announced plan to acquire a majority stake in Singapore-based crypto exchange Coinhako

(2026.02) Launched JPYSC yen stablecoin with Startale Group

(2026.02) Launched Strium L1, a blockchain for tokenized trading, with Startale Group

(2026.03) Issued SBI START Bond, a blockchain-based corporate bond

(2026.03) SBI VC Trade launched USDC lending service

One of the most core cryptocurrency businesses within the SBI Group is its exchange operations in Japan. SBI VC Trade originated from SBI Virtual Currencies, established in 2016, and launched its cryptocurrency trading service VC Trade in 2018. In 2020, SBI acquired a competing exchange, TAOTAO, to expand its exchange business, and in 2021, it integrated SBI VC Trade and TAOTAO. In 2023, it further acquired another Japanese exchange, BITPOINT, and currently operates two exchanges: SBI VC Trade and BITPOINT.

Although the largest cryptocurrency exchanges in Japan are often cited as bitFlyer, CoinCheck, and bitbank, SBI VC Trade is also among the top-tier exchanges, generating approximately JPY 17.5 billion in revenue in 2025. In 2026, SBI VC Trade is expected to merge with BITPOINT, another exchange operated by SBI, which is likely to further increase its scale.

Alongside exchange operations, market making is another core business within SBI’s crypto segment. In 2020, SBI acquired approximately 90% of the global market-making firm B2C2, making it a subsidiary. B2C2 is a UK-based company founded in 2015 that provides crypto trading liquidity to financial institutions worldwide.

B2C2’s main businesses are as follows:

Over-the-counter (OTC): Supports institutional spot and derivatives trading, as well as lending and borrowing, in off-exchange markets.

Market making: Provides institutional-grade liquidity to exchanges.

Strategic liquidity partner: Goes beyond simple liquidity provision by working with projects to design the entire pipeline, from initial liquidity bootstrapping to stable trading environments, increased trading volume, and investor onboarding.

Stablecoin swaps: B2C2 has developed Penny, an institutional stablecoin swap infrastructure, where it acts as a liquidity provider to enable instant swaps between various stablecoins across multiple networks.

B2C2 collaborates with roughly half of Japan’s 32 JVCEA Type 1 exchanges to provide market-making services, and recently partnered with Standard Chartered to offer crypto trading infrastructure to institutional clients. While B2C2’s revenue is not publicly disclosed, considering the scale of its operations, it is likely to account for a significant portion of SBI Group’s crypto business revenue.

Beyond its core businesses such as exchanges, market making, and OTC, SBI Group is also engaged in a wide range of Web3-related activities:

Stablecoins: SBI collaborates with Circle to serve as a distribution channel for USDC. For example, SBI VC Trade was the first in Japan to offer USDC trading, launched USDC lending services, is working on real-world USDC payment and remittance infrastructure, and is also exploring integration between USDC and bank accounts in collaboration with SBI Shinsei Bank.

Prime brokerage: The SBI VC for Prime service is a specialized offering for institutions and high-volume traders, providing an institutional-grade trading environment along with asset management services such as lending and staking, as well as business support including consulting.

Remittance: Operates remittance services such as SBI Remit and MoneyTap based on XRPL.

Validator: Although not a core business, SBI operates validator nodes on networks such as Canton and XRPL.

Research/Consulting: SBI acquired blockchain research and consulting firm HashHub, providing research and advisory services to enterprises and investors.

Media: SBI acquired a majority stake in CoinPost, one of Japan’s most well-known blockchain media companies, and operates a media business.

Investment: SBI has long invested in numerous Web3 companies, including Securitize, Ripple Labs, R3, Zodia Custody, B2C2, and DigiFT.

In addition to SBI, Japan’s cryptocurrency market also includes the three major megabanks, MUFG, SMBC, and Mizuho, all of which are pursuing crypto-related initiatives.

MUFG focuses on infrastructure for issuing and managing cryptocurrencies. A key component of this strategy is Progmat, developed by its subsidiary Mitsubishi UFJ Trust. Progmat is a platform that integrates issuance, management, and settlement of various digital assets. It aims to connect blockchains such as Ethereum, Avalanche, and Polygon with traditional financial networks to tokenize a wide range of assets including cash, securities, real estate, and services. Currently, Progmat supports 39 security token projects and 4 utility token projects, with approximately 330 participating companies.

SMBC is taking a bank-centric approach. It has announced plans to develop its own banking payment infrastructure coin in collaboration with Ava Labs, Fireblocks, and TIS. It has also participated in experiments involving the exchange of digital bonds and DCJPY alongside NRI, Nomura, Boostry, and DeCurret, focusing on tokenized asset settlement and banking infrastructure.

Mizuho is relatively more conservative among the megabanks. It has limited standalone crypto initiatives and primarily participates in crypto-related projects in consortium form alongside MUFG and SMBC.

5.2.1 Full-Stack Strategy

Compared to the approaches of megabanks, SBI’s cryptocurrency business strategy clearly stands out. While MUFG focuses on infrastructure and SMBC takes a bank-centric approach, SBI is pursuing a full-stack strategy centered around exchanges.

5.2.2 Core Business: Exchanges

Cryptocurrency exchanges are at the center of SBI’s crypto business. Starting with its investment in bitFlyer, SBI operates its own exchange, SBI VC Trade, and has demonstrated strong commitment to the exchange business through acquisitions such as TAOTAO and BITPOINT. In particular, initiatives such as the market-making and OTC firm B2C2, the institutional service SBI VC for Prime, and the recently launched SBI VC Trade USDC lending service clearly show that SBI is expanding its business around the exchange as the core hub.

5.2.3 Aggressive Expansion through Acquisitions and Joint Ventures

SBI’s cryptocurrency business goes beyond exchanges and exchange-related services. Through the acquisition and joint venture strategies discussed earlier, SBI is rapidly expanding into areas such as remittance, stablecoins, research, and media. This approach enables SBI to quickly build a full-stack cryptocurrency business within the group.

5.2.4 Tokenization as a Future Business

Recently, SBI has shown strong interest in tokenization. It invested in DigiFT, a Singapore-based RWA trading platform, and established a joint venture called SBI Onchain. Additionally, through a joint venture with Startale Group, SBI is developing Strium L1, a blockchain specialized for tokenized financial transactions. As the global RWA market is growing rapidly and Japan already has a clear regulatory framework for tokenization, this segment has strong potential to become SBI’s next major cryptocurrency business following exchanges.

This research examined how SBI, a major Japanese financial group, has grown, why its expansion into cryptocurrency is a natural progression, what its key crypto business areas are, and how it has established itself as a dominant player in Japan’s crypto sector through a full-stack strategy.

The key point is that SBI has not merely “participated” in the cryptocurrency business. Rather, it is attempting to reconstruct the entire financial infrastructure, spanning exchanges, liquidity, payments, investment, and tokenization. Unlike traditional financial institutions that focus on specific areas, SBI’s approach is closer to integrating the entire digital asset market into a single platform.

Looking ahead, there are several key points to watch:

First, how quickly tokenization will be adopted in real financial markets. Given Japan’s established regulatory foundation, experimentation and commercialization may progress faster than in global markets, and SBI could play a leading role in this space.

Second, the integration of stablecoins with the banking system. The connection between SBI Shinsei Bank and stablecoins could evolve beyond a simple crypto business into the development of digital cash infrastructure.

Third, global expansion. Blockchain is inherently a global technology. SBI is already expanding its digital asset business in Singapore, Europe, and Southeast Asia, and it will be important to watch how far it can extend beyond Japan into global markets.

Taken together, SBI is no longer simply an internet-based financial company in Japan. Rather, it is more accurately described as evolving into a “hybrid financial platform” that bridges traditional finance and digital assets. If digital assets become a core component of the future financial system, SBI is likely to be one of the key players designing that infrastructure in Japan.

Dive into 'Narratives' that will be important in the next year