This article is excerpted from 'The Necessity of KRW Stablecoins and Proposal for a Legislative Framework', a report co-authored by Hashed Open Research and Four Pillars. The full report can be found at Four Pillars.

State of the Stablecoin Market

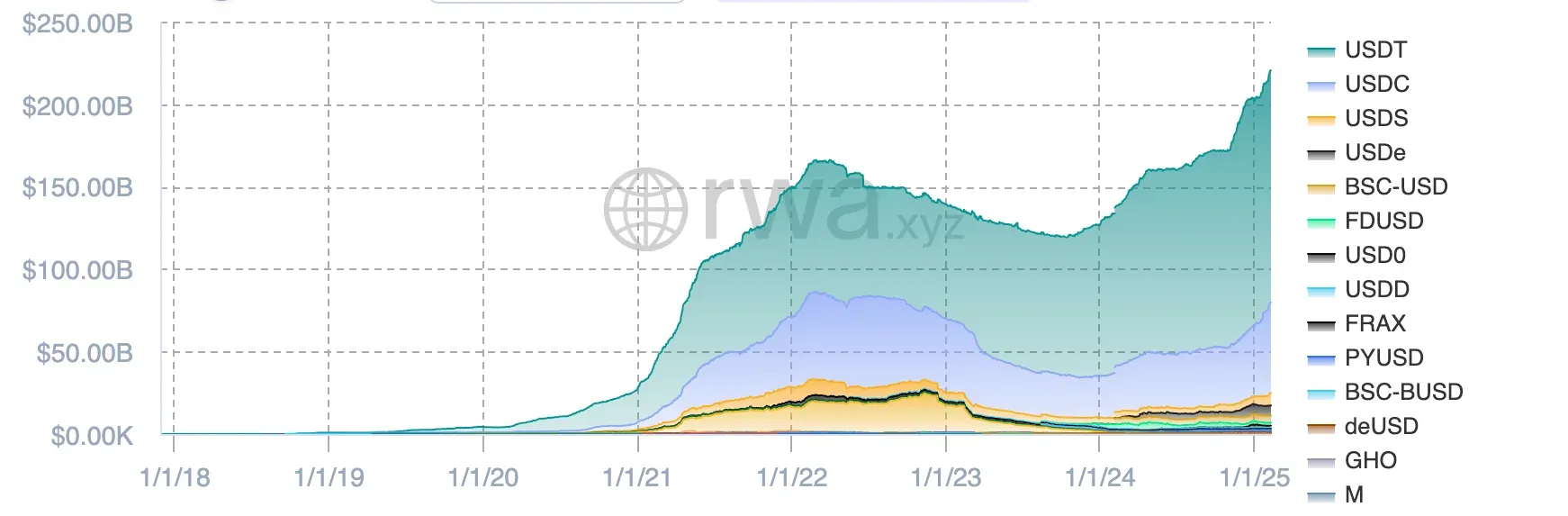

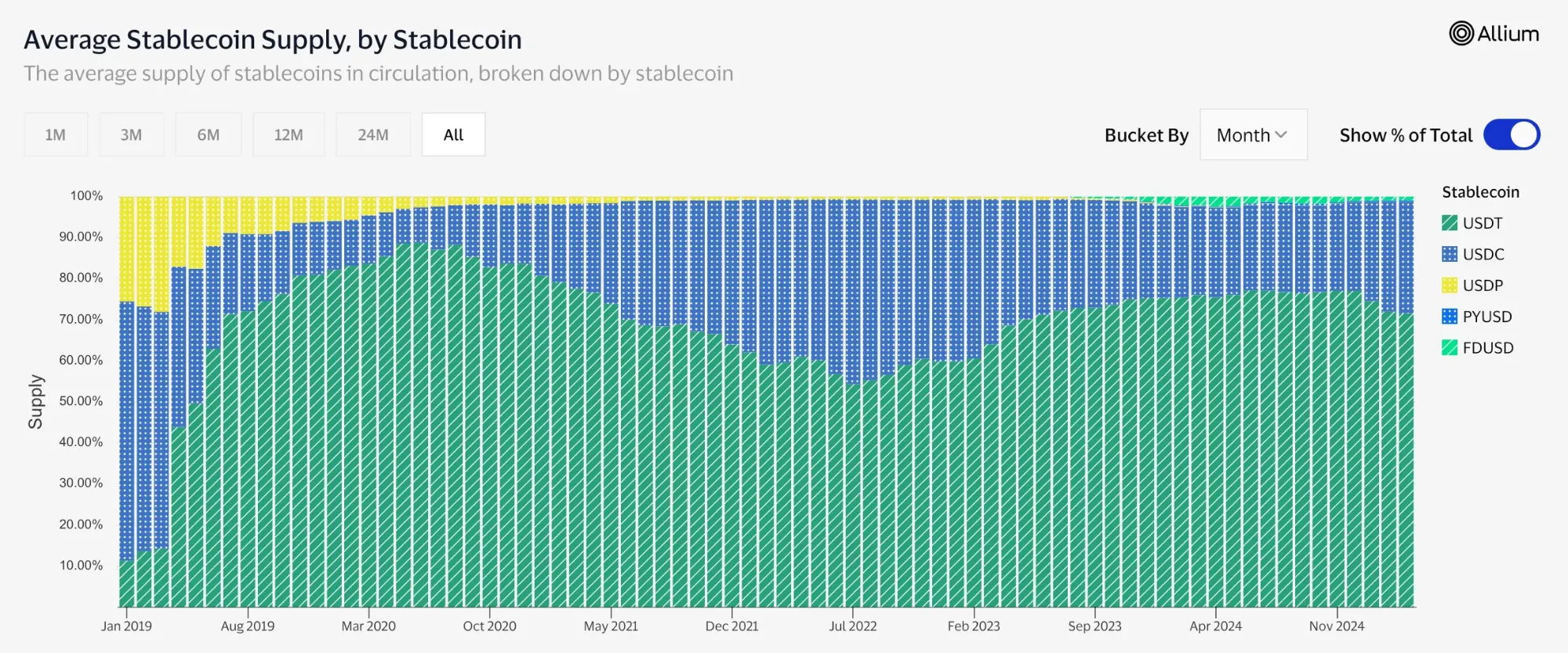

In 2024, stablecoin issuance increased by more than 64% compared to the previous year, exceeding $200 billion. However, USD-based stablecoins, primarily USDT and USDC, continue to dominate over 95% of the market.

Stablecoin issuers generate billions of dollars in annual revenue from their treasury holdings as collateral, and the United States is leveraging this opportunity to strengthen dollar hegemony in both global and digital economies.

Analysis of Stablecoin Use Cases

Stablecoins have the potential to replace existing payment and remittance systems due to their high accessibility, low fees, programmability, and non-custodial nature.

Stablecoin adoption is growing rapidly, particularly in countries with low currency stability and underdeveloped financial services, serving as an alternative payment system and dollar access method.

Stablecoins serve as the base currency for almost all trading pairs on exchanges, playing a crucial role in initial user acquisition and liquidity building. This creates network effects that establish high reliability and utility, providing a foundation for expansion into other use cases.

State of the Korean Stablecoin Market

Stablecoins now represent over 20% of daily trading volume on major Korean exchanges, yet regulatory frameworks remain under-developed.

USD stablecoins in Korea primarily facilitate access to foreign crypto markets rather than serving real economy needs, due to the local premium and limited crypto penetration.

The accelerating exodus of Korean capital to offshore platforms threatens domestic market competitiveness and the KRW's relevance in digital finance.

Opportunities of a KRW Stablecoin

A KRW stablecoin would help Korea secure regulatory sovereignty in the growing global competition for stablecoin market positioning.

Korea's exceptionally high trading volumes provide strategic advantages that could make a KRW stablecoin more viable than other non-USD alternatives.

Beyond resolving market inefficiencies like the kimchi premium, a KRW stablecoin could become foundational infrastructure for Korea's innovation and strengthen its position in global digital finance.

“Stablecoins, a novel form of interoperable and programmable money, have the potential to rewire the global financial system. In doing so, they could allow software to eat banking and financial services — sectors left relatively untouched by the internet.”

Christian Catalini, Founder of the MIT Cryptoeconomics Lab

Stablecoins are digital assets pegged to fiat currencies like the US dollar, combining blockchain's advantages while eliminating cryptocurrency's volatility. If we could redesign our financial system from scratch, we would likely incorporate most features that stablecoins already offer: 24/7 accessibility, instant low-fee transfers from anywhere in the world, programmability across a common tech stack, and selective transparency.

Source: RWA.xyz | Stablecoins

The stablecoin market has grown to a scale rivaling traditional financial sectors. In 2024, as market conditions improved alongside advances in blockchain scalability and user experience, stablecoin adoption has accelerated dramatically. Total stablecoin market capitalization grew by over 64% in the past year, surpassing $200 billion. Dollar-backed stablecoins now represent more than 1% of the total dollar supply (M2), marking their transition from experimental technology to a significant component of the financial ecosystem.

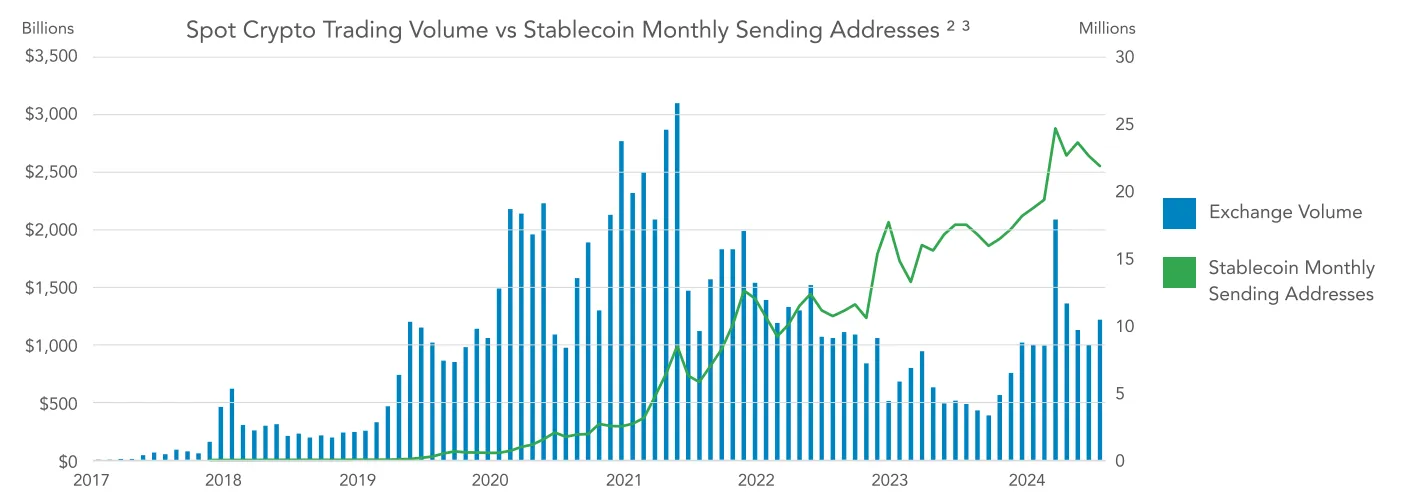

Source: Stablecoins: The Emerging Market Story - Castle Island VC

Stablecoins have emerged as blockchain's definitive killer app, showing the strongest product-market fit of any blockchain application to date. While their growth initially tracked crypto market cycles in 2017 and 2021, since 2022 they've shown decoupling from the broader crypto market, steadily increasing adoption regardless of external conditions. By late 2023, monthly stablecoin transaction volume exceeded $4 trillion—five times higher than the previous year. Even when excluding arbitrage and inter-exchange transfers, adjusted volume reached $700 billion.

The user base continues to expand, with stablecoins now held in over 100 million wallets and approaching 25 million monthly active users—exceeding the customer base of many emerging market financial institutions. This adoption shows impressive geographic and economic diversity: developed nations use stablecoins for efficient cross-border payments, emerging markets leverage them against inflation, and the unbanked access financial services previously beyond reach.

This trajectory indicates that stablecoins are evolving beyond the crypto ecosystem to become catalysts for global financial innovation. They offer promising solutions to persistent challenges that traditional systems have failed to address: cross-border payment inefficiencies, financial exclusion, and the limitations of non-real-time settlement systems.

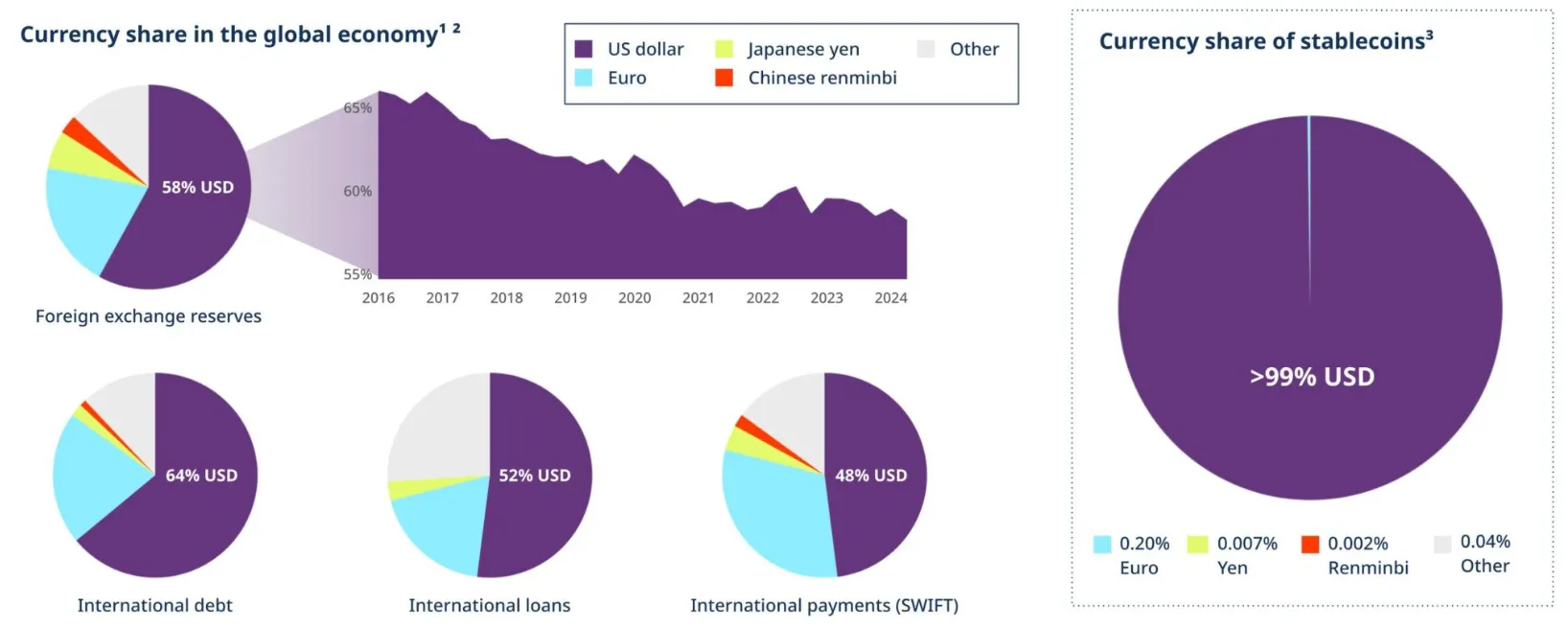

1.2.1 Dollar's Dominant Position in the Stablecoin Market

Source: State of Crypto Report 2024 - a16z Crypto

One of the most notable characteristic of the stablecoin market is the overwhelming dominance of the US dollar. Stablecoins pegged to the dollar account for nearly 99% of the entire market. Euro-based stablecoins follow a distant second with less than 0.5% market share, while stablecoins based on other fiat currencies remain insignificant with issuance volumes below $100 million each. While the dollar's status as the world's reserve currency is undisputed, its concentration in stablecoins is even more extreme than in traditional finance, where the dollar accounts for about 88% of international forex trading and 40-50% of global payments.

This dollar concentration stems from two key factors. First, most countries have neither erected regulatory barriers against dollar stablecoins nor offered viable alternatives, allowing users to naturally gravitate toward the most liquid and widely used assets. Second, the dollar's strength against major currencies in recent years has increased the preference for dollar-denominated assets.

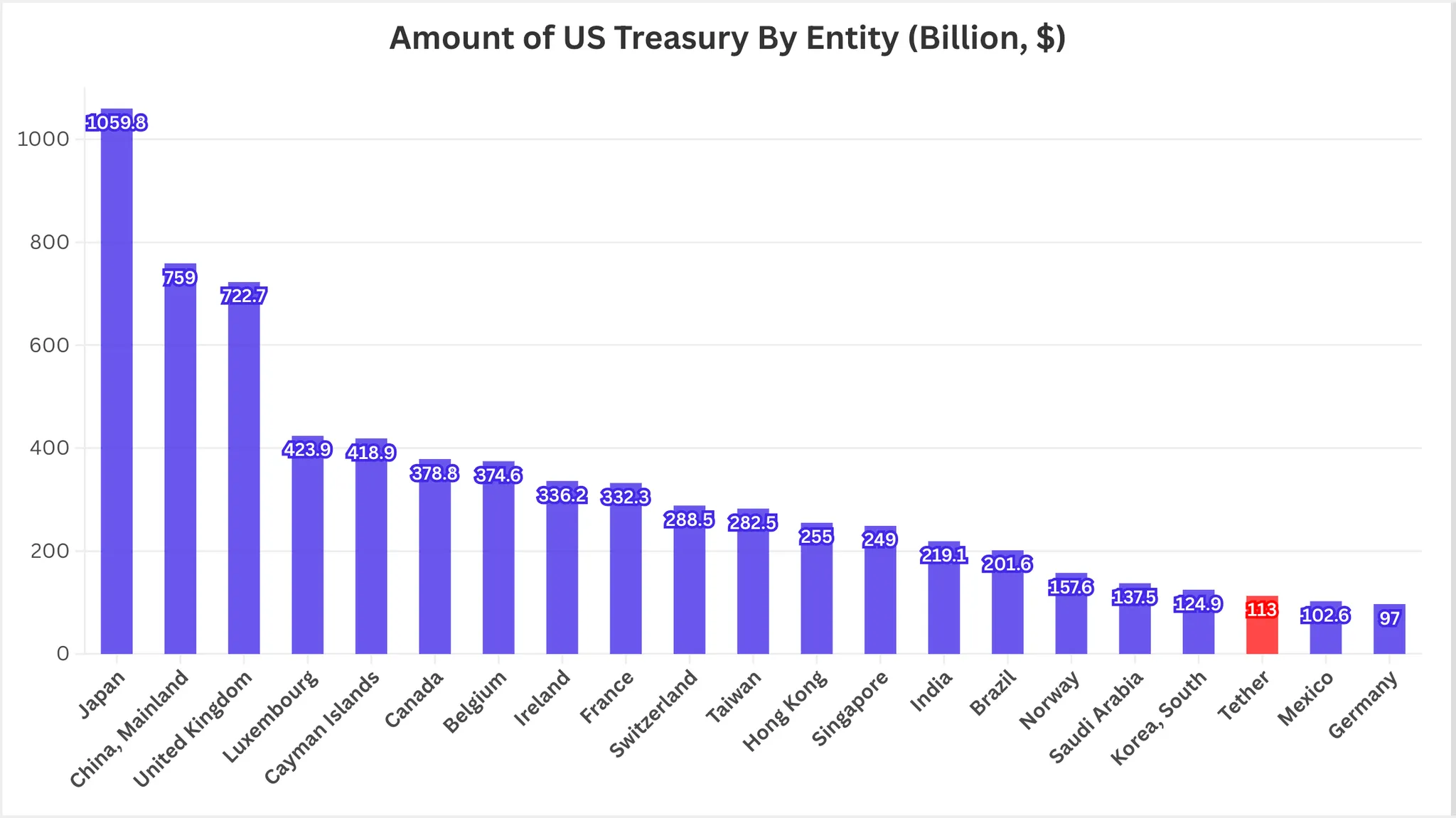

Source: Treasury International Capital (TIC) System

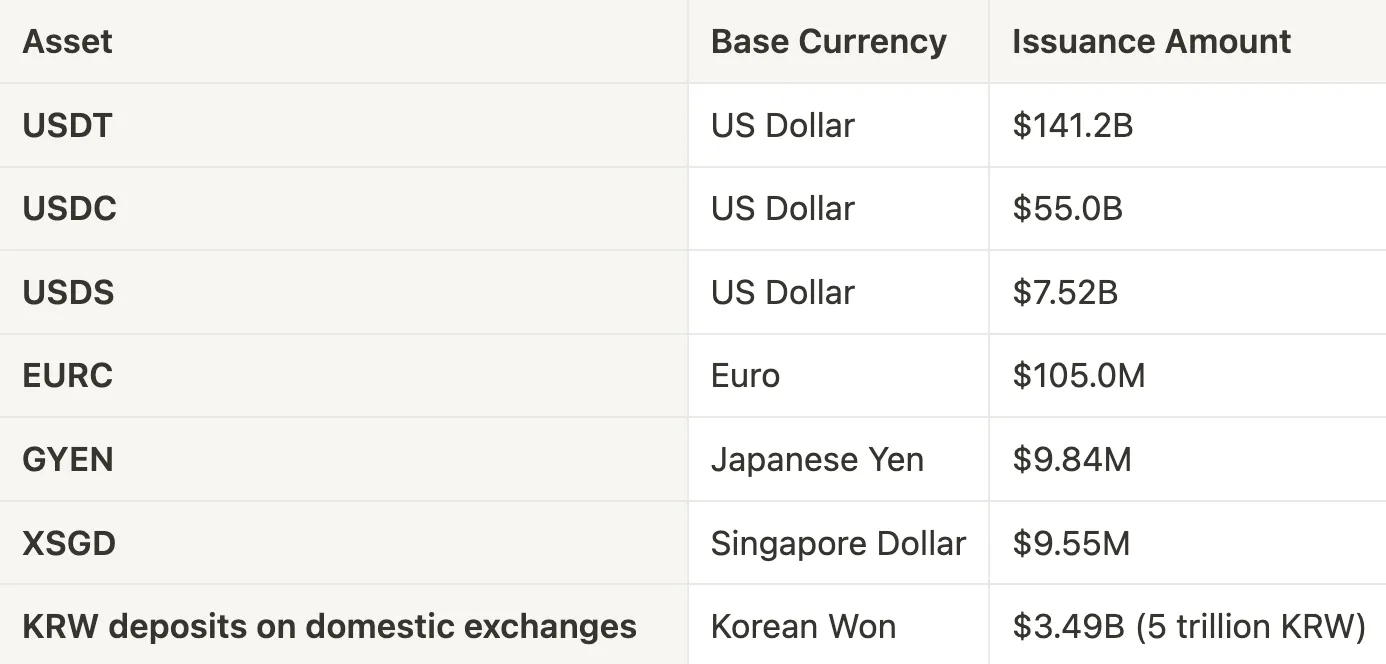

As a result of this dollar-centric ecosystem, issuers have accumulated massive reserves, primarily invested in US Treasuries. Tether, the leading stablecoin issuer with approximately $140 billion in circulation, holds substantial Treasury investments that rank 19th globally—higher than countries like Germany or Mexico—and at current growth rates could surpass South Korea's holdings by 2025.

Source: Tether Transparency

According to Tether's financial disclosures, the company recorded $4.5 billion in net profit for Q1 2024 alone—triple BlackRock's $1.5 billion for the same period. Tether's reserves are predominantly in cash equivalents, with 65.74% ($94.5 billion) invested in US Treasuries. Similarly, Circle, USDC's issuer, reported revenues of $779 million for the first half of 2023.

1.2.2 America's Strategy to Strengthen Dollar Dominance in Digital Assets

"Stablecoins have the potential to ensure American dollar dominance internationally to increase the usage of the US dollar digitally as the world’s reserve currency, and in the process create potentially trillions of dollars of demand for US Treasuries, which could lower long-term interest rates"

David Sacks, US AI and Crypto Czar

The United States clearly recognizes the growth of the stablecoin market and its potential to expand dollar influence globally, viewing it as a strategic opportunity to reinforce American economic power and dollar hegemony. David Sacks, whom Trump appointed as AI and Cryptocurrency Czar, recently noted at a conference that stablecoins could strategically strengthen the dollar's international dominance and generate demand for US Treasuries. This indicates that the US now views stablecoins not just as financial technology innovations but as instruments of economic and monetary strategy.

With this positive outlook on stablecoins, the Trump administration is actively advancing supportive policies. Shortly after taking office, Trump issued an executive order on stablecoins that explicitly aimed to "promote the development and growth of legitimate, proper dollar-based stablecoins to protect the dollar's international dominance." The administration has halted central bank digital currency (CBDC) development in favor of supporting a privately-led stablecoin ecosystem.

The Trump administration's digital asset policy is built around establishing regulatory clarity and reinforcing American economic primacy. While the Biden administration created uncertainty through "regulation by enforcement," the Trump administration favors building a clear regulatory framework through legislation. Unlike Biden's CBDC-focused approach, Trump has explicitly committed to supporting privately-issued stablecoins.

This policy direction is evident in key legislation like the FIT21 and GENIUS Acts, which establish clear federal regulatory frameworks for stablecoin issuers, applying Federal Reserve and OCC oversight to issuers with more than $10 billion in circulation. These initiatives explicitly prohibit algorithmic stablecoins and require issuers to maintain 1:1 cash or cash equivalent reserves to support token values, enhancing market stability.

America's approach can be viewed as a strategy to establish a new form of monetary dominance in digital finance, particularly as international de-dollarization efforts emerge. The substantial Treasury holdings that stablecoin issuers have accumulated play a significant role in financing US government debt, potentially aiding America's fiscal operations in the short term.

2.1.1 Can Stablecoins Replace Existing Payment Networks?

“Stablecoins are room-temperature superconductors for financial services. Thanks to stablecoins, businesses around the world will benefit from significant speed, coverage, and cost improvements in the coming years.“

Patrick Collison, Stripe CEO

Source: How stablecoins will eat payments, and what happens next?

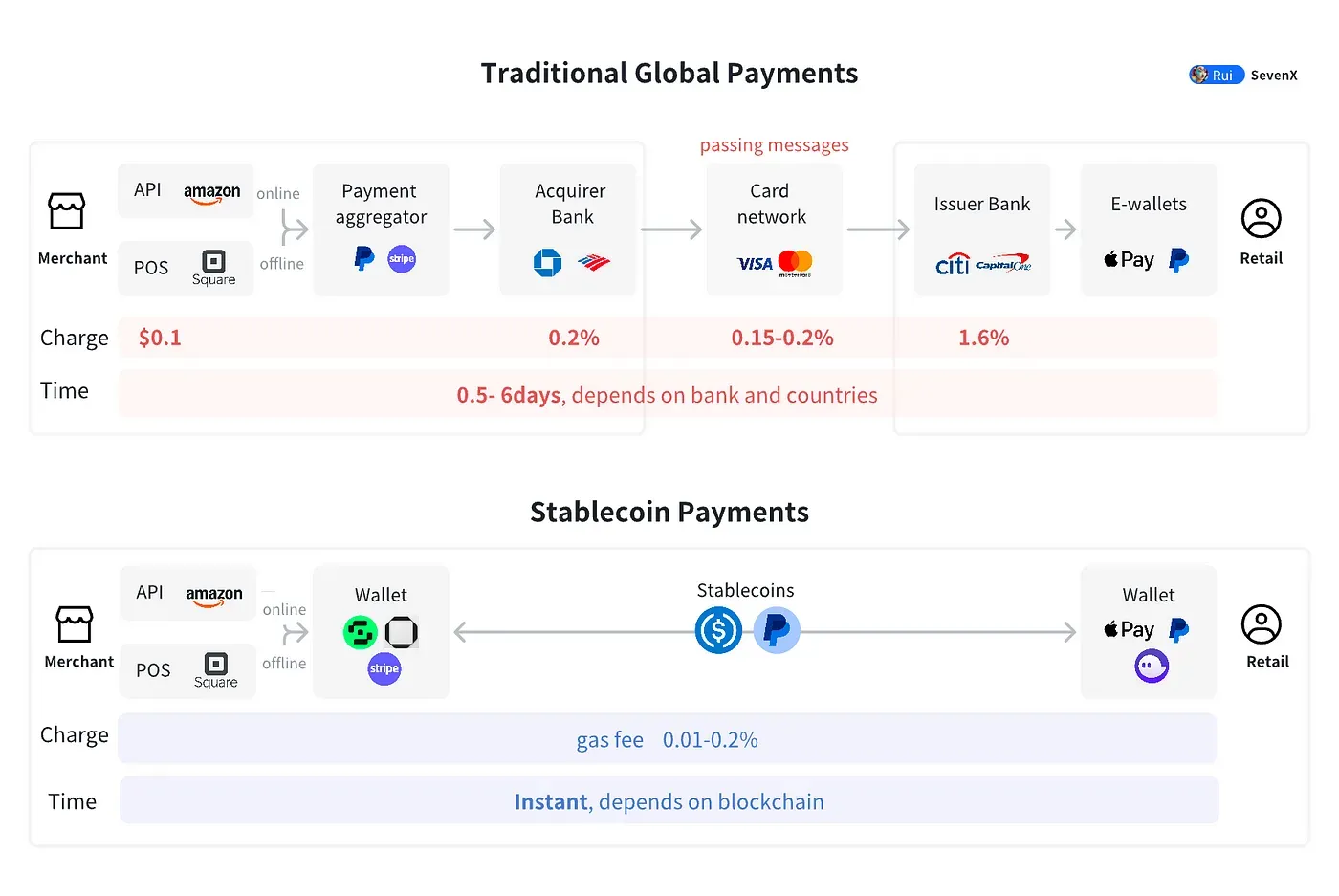

Stablecoin-based payment methods offer superior characteristics compared to traditional financial payment systems in several aspects. The four key requirements for a payment system are cost, timeliness, reliability, and convenience. Stablecoins have clear advantages over existing payment systems, particularly in terms of cost and timeliness. When transacting with stablecoins on major high-performance blockchains, transfers can be completed in seconds to minutes worldwide for just a few cents, regardless of the transfer amount.

Source: Stablecoin Playbook - Rui Shang

The cost efficiency of stablecoin-based payment methods is particularly beneficial for low-margin businesses (restaurants, retail stores, etc.) and companies engaging in international transactions. Since both payment processors and distributors share an interest in replacing high-cost payment solutions, major payment processors like Stripe, PayPal, and Shopify are adopting stablecoins to improve their margins. Stripe currently charges a 1.5% fee for stablecoin payments, which is 30% lower than card payment fees, and recently acquired Bridge.xyz for approximately $1 billion to strengthen its market position.

Source: How stablecoins will eat payments, and what happens next - a16z Crypto

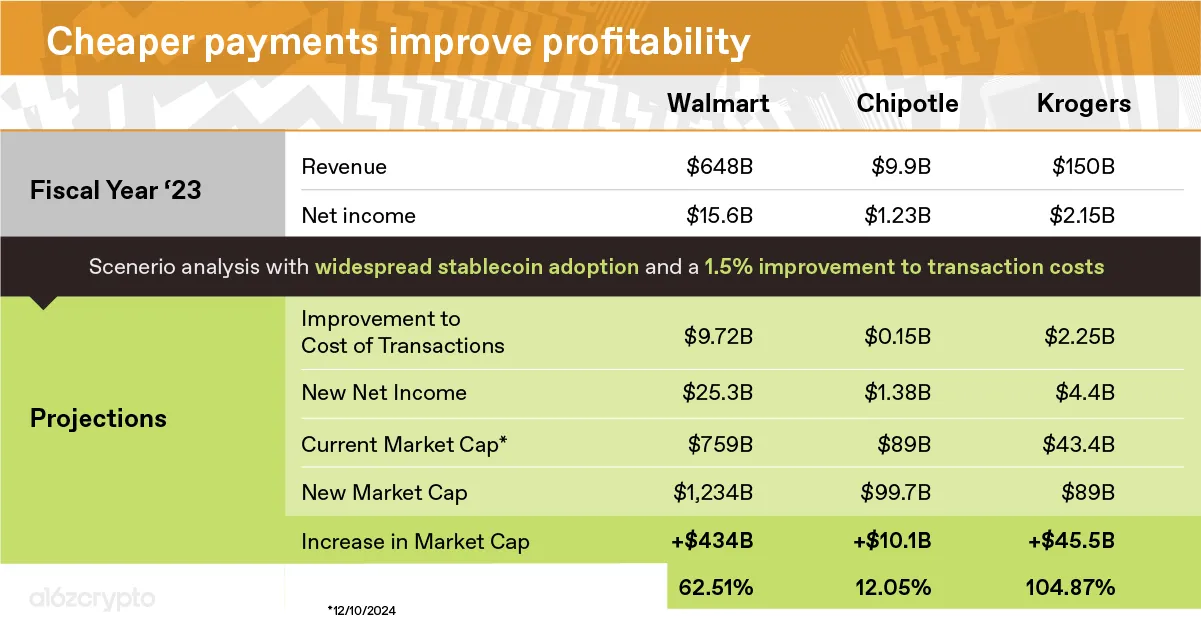

Stablecoin-based payment methods can significantly improve business profitability. For instance, Walmart has annual sales of $648B and pays about $10B in credit card fees, while its net profit is around $15.5B. If stablecoin adoption substantially reduces payment fees, profitability could improve by up to 60%.

Beyond cost advantages, stablecoins excel in transaction speed, permissionless access, and programmability. Traditional international remittance systems take 2-3 business days, while stablecoins complete transfers in seconds to minutes, depending on the blockchain network. Recent expansion and increased adoption of high-performance blockchains like Ethereum rollups, Solana, and Sui have significantly improved the processing efficiency of stablecoin-based payment solutions while reducing fees. Additionally, programmability through smart contracts enables complex financial transactions such as conditional payments, automated agreements, and escrow services to be implemented in code, greatly enhancing compatibility and transaction efficiency across financial services.

However, due to unclear regulations and imperfect user experiences with onchain services, stablecoins as payment solutions have not yet achieved sufficient market adoption. The adoption of stablecoin payments is expected to occur gradually, initially among innovative startups and edge cases of consumer needs, then spreading to everyday users and conservative businesses as the platforms mature. Sam Broner, a partner at A16Z, identified three factors that will accelerate stablecoin adoption in business and consumer sectors:

Increased back-office integration: Stablecoin orchestration (monitoring, delivery, integration) will be built into payment processors like Stripe, allowing businesses to adopt stablecoin payment methods without additional processes or engineering changes, processing payments at much lower costs than existing systems.

Improved onboarding and shared incentives: Stablecoin companies are sharing incentives and improving onboarding solutions to attract end users on-chain. Simultaneously, major consumer applications like Venmo, ApplePay, and PayPal are supporting cryptocurrencies, allowing users to benefit from the expanded stablecoin ecosystem without needing to adopt new apps or user behaviors.

Regulatory clarity: Businesses are more likely to adopt stablecoins when they have confidence in the regulatory environment. As regulatory frameworks like the European Union's Markets in Crypto-Assets (MiCA) are established, businesses can consider transitioning from legacy payment rails to stablecoin infrastructure.

2.1.2 Stablecoin Thrives in Emerging Economies

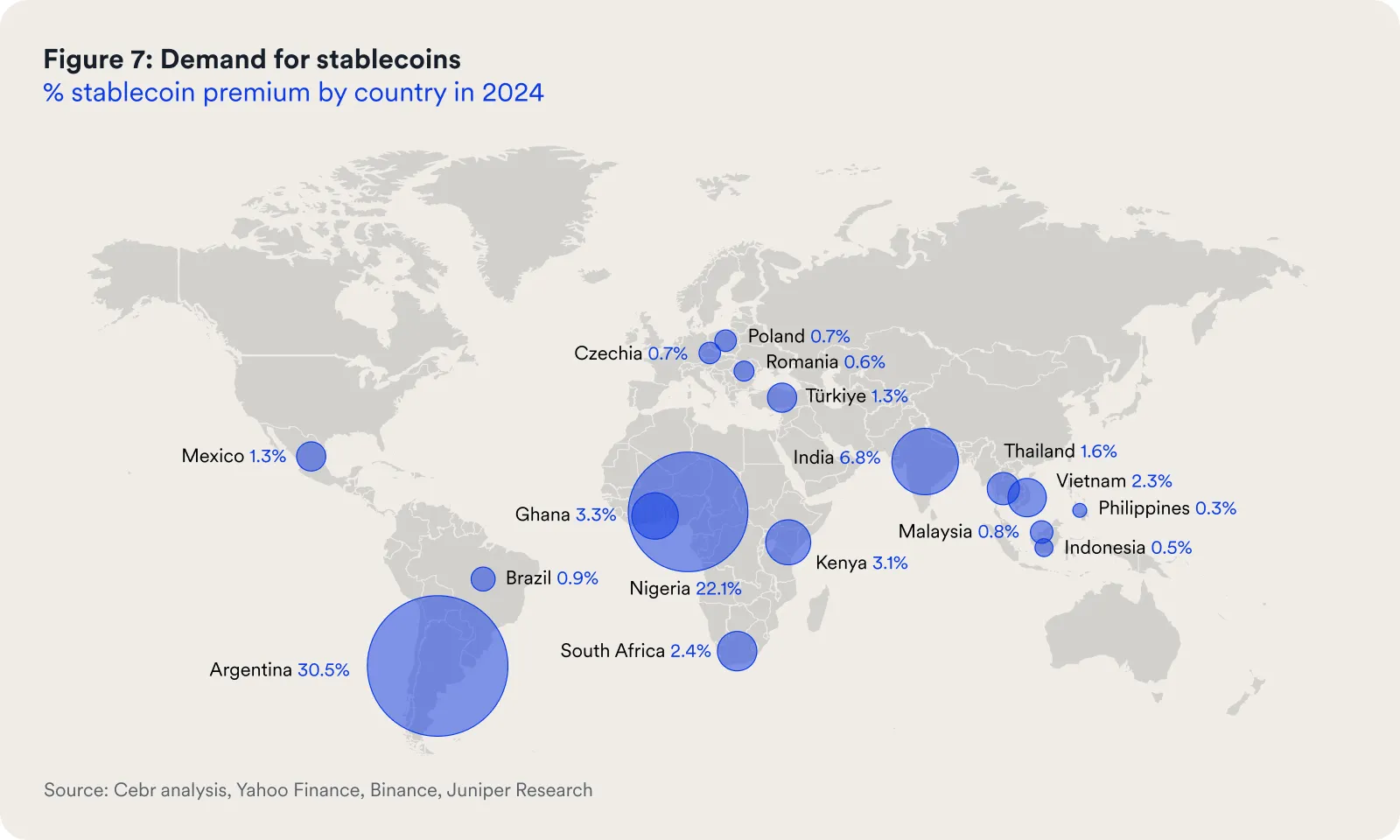

The superiority of stablecoins as a payment system is particularly pronounced in countries with low currency stability and underdeveloped financial services. In these regions, stablecoins serve not only as a simple payment method but also as a stable store of value. In fact, stablecoin usage is notably higher in countries experiencing unstable local currency values or high inflation, such as Argentina, Nigeria, Turkey, and Venezuela.

In these countries, stablecoins provide greater accessibility to the US dollar compared to traditional systems. For example, in Mexico, banks cannot provide USD accounts to people who don't live within 20km of the US border. In Colombia and Brazil, individuals cannot open dollar bank accounts, while in Argentina, although USD bank accounts exist, they have transaction limits and operate on an "official" exchange rate that differs from the market rate. In these circumstances, stablecoins have become an effective alternative for accessing actual dollars.

Source: State of Crypto Report 2024 - a16z Crypto

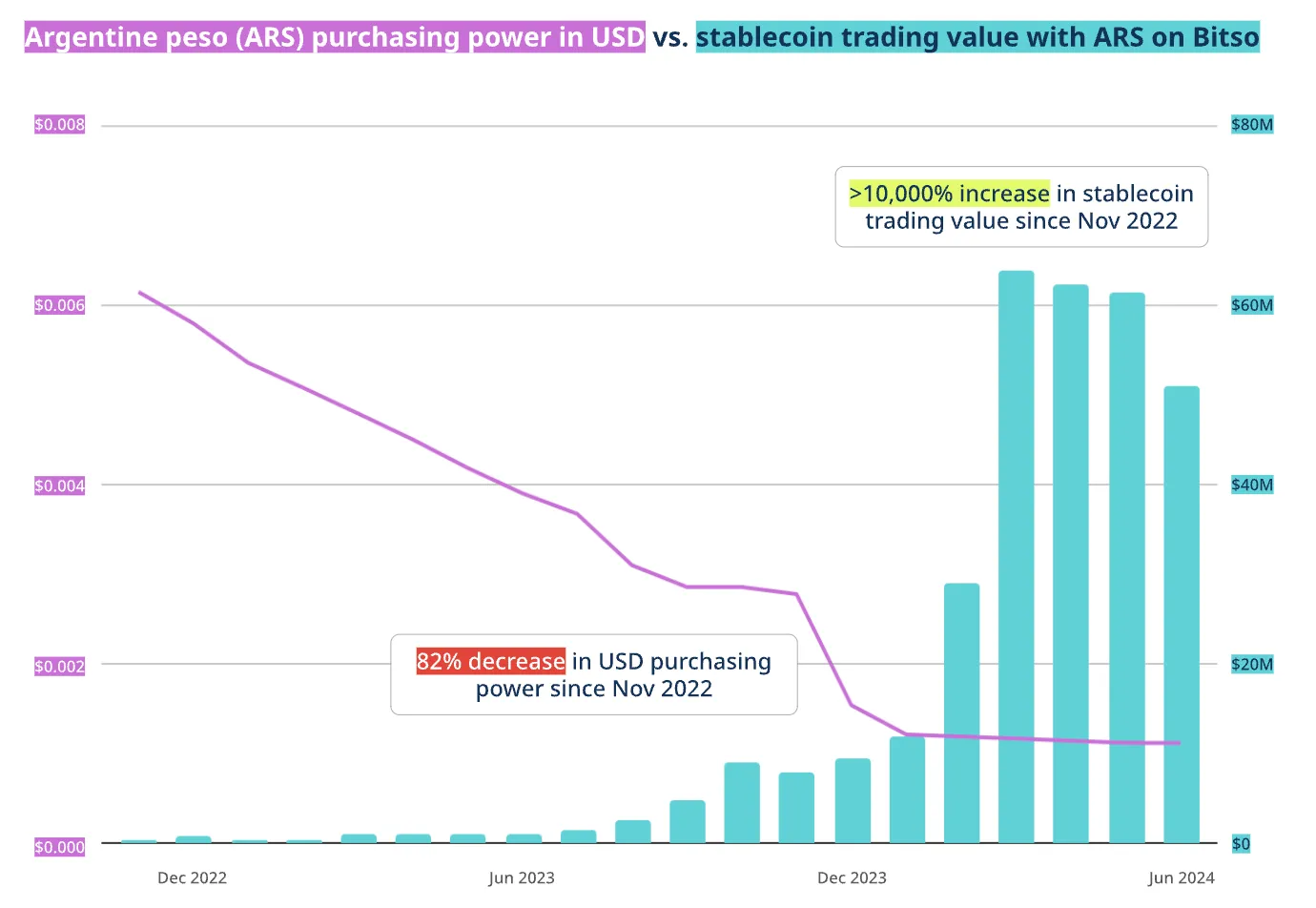

In Argentina, demand for stablecoins has surged as the value of the peso continues to decline. During 2022, the peso's value fell by more than 45% against the US dollar, and inflation rose to 211% in 2023. Under these conditions, Argentinians are using stablecoins as an alternative to preserve asset value. Stablecoins sometimes trade at premiums of up to 30% above general market prices on local exchanges, demonstrating that stablecoins are perceived as an alternative to dollars in a situation where access to dollars is restricted.

Source: Stablecoins 101 - Chainanlysis

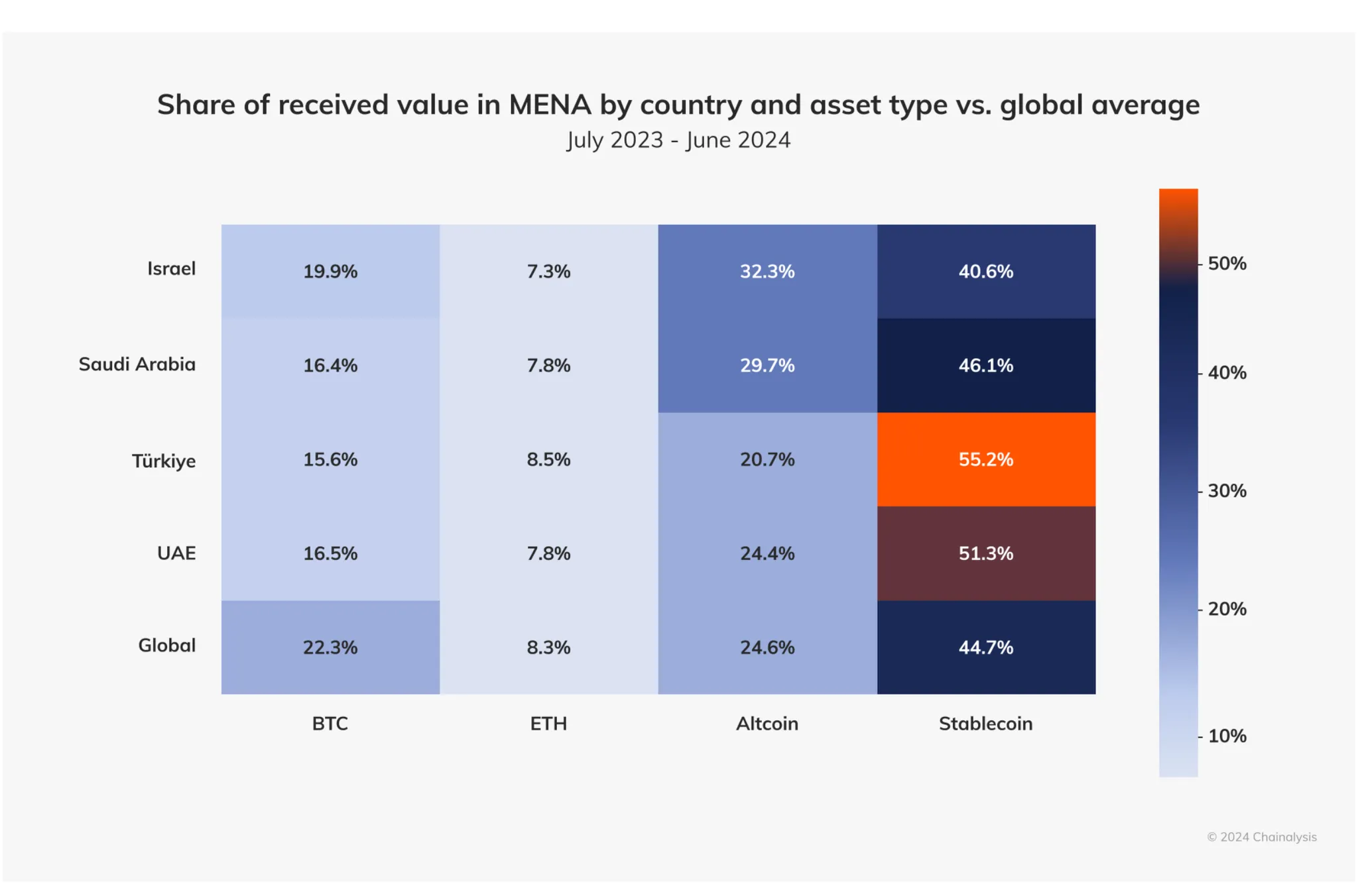

Similar patterns are observed in the Middle East. In Turkey, the declining value of the lira and persistent inflation have led to a surge in stablecoin usage. According to a Chainalysis report, Turkey has one of the world's highest stablecoin transaction volumes relative to GDP at 3.7%, reflecting strong demand for a stable store of value and medium of exchange instead of the local currency. In Turkey, stablecoins have established themselves not just as speculative instruments but as practical financial alternatives.

In African countries facing severe foreign exchange shortages, stablecoins have become an important tool for enabling international payments. The CEO of Yellow Card, an African fintech company providing trade, remittance, and corporate payment APIs using stablecoins, remarked, "In Africa, it's not about comparing stablecoins with other financial tools, but comparing having stablecoins versus having nothing at all," emphasizing that stablecoins are becoming the only alternative for international payments amid severe foreign exchange liquidity shortages across the continent.

Source: The decade of digital dollars - BVNK

These high adoption rates stem from several common characteristics of these countries. First, they experience unstable local currency values or high inflation, making it difficult to preserve asset value. Second, access to stable foreign currencies like the US dollar is restricted due to government regulations or foreign exchange reserve shortages. Third, banking systems and fintech infrastructure are either insufficiently developed or have failed to gain trust.

An analysis of BVNK shows that, on average, a 4.7% premium is being paid in 17 emerging markets, with Argentina's premium reaching up to 30%. As of 2024, these 17 countries are estimated to pay a total premium of $4.7 billion to secure access to stablecoins, a figure projected to increase to $25.4 billion by 2027.

In conclusion, in regions with low currency stability and underdeveloped financial services, stablecoins have established themselves as tools for financial inclusion beyond simple cryptocurrency investment vehicles. By simultaneously addressing three key issues—local currency value instability, restricted dollar access, and insufficient financial infrastructure—stablecoins play a crucial role in enabling stable value storage, efficient international remittances, and access to basic financial services in these regions.

Additionally, considering that countries with high stablecoin adoption rates are not included in the traditional dollar economic zone, this stablecoin usage can be seen as a new form of dollarization. Unlike physical dollars, digital dollar-based stablecoins are spreading across borders, bypassing national monetary sovereignty. This trend is expected to continue, with dollarization through stablecoins likely to accelerate, especially in regions where improvements in local financial infrastructure are slow.

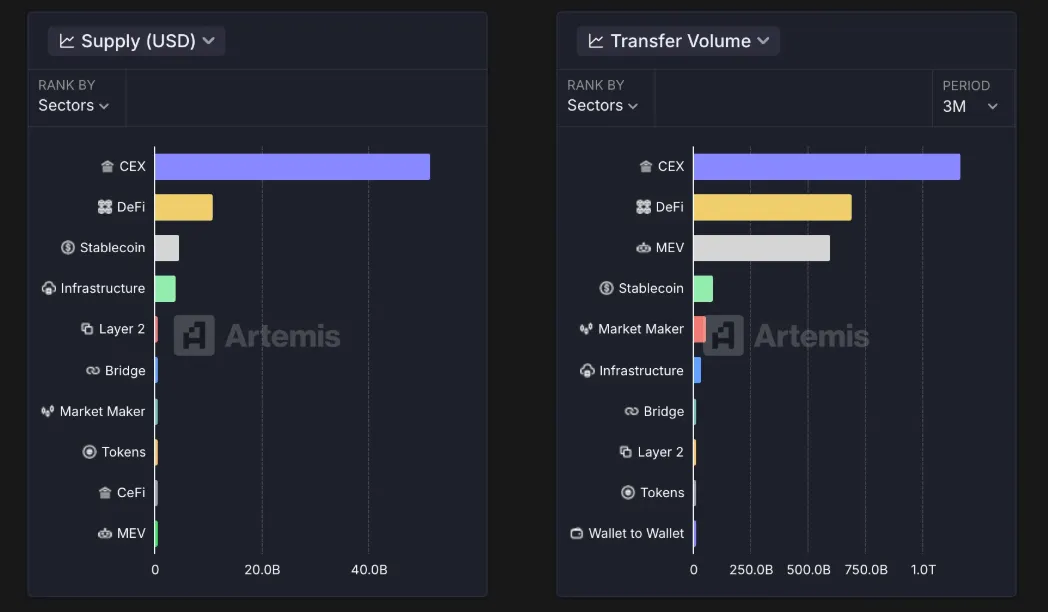

2.2.1 The Surge in Stablecoin Usage Within Exchanges

Source: Artemis Stablecoin Dashboard

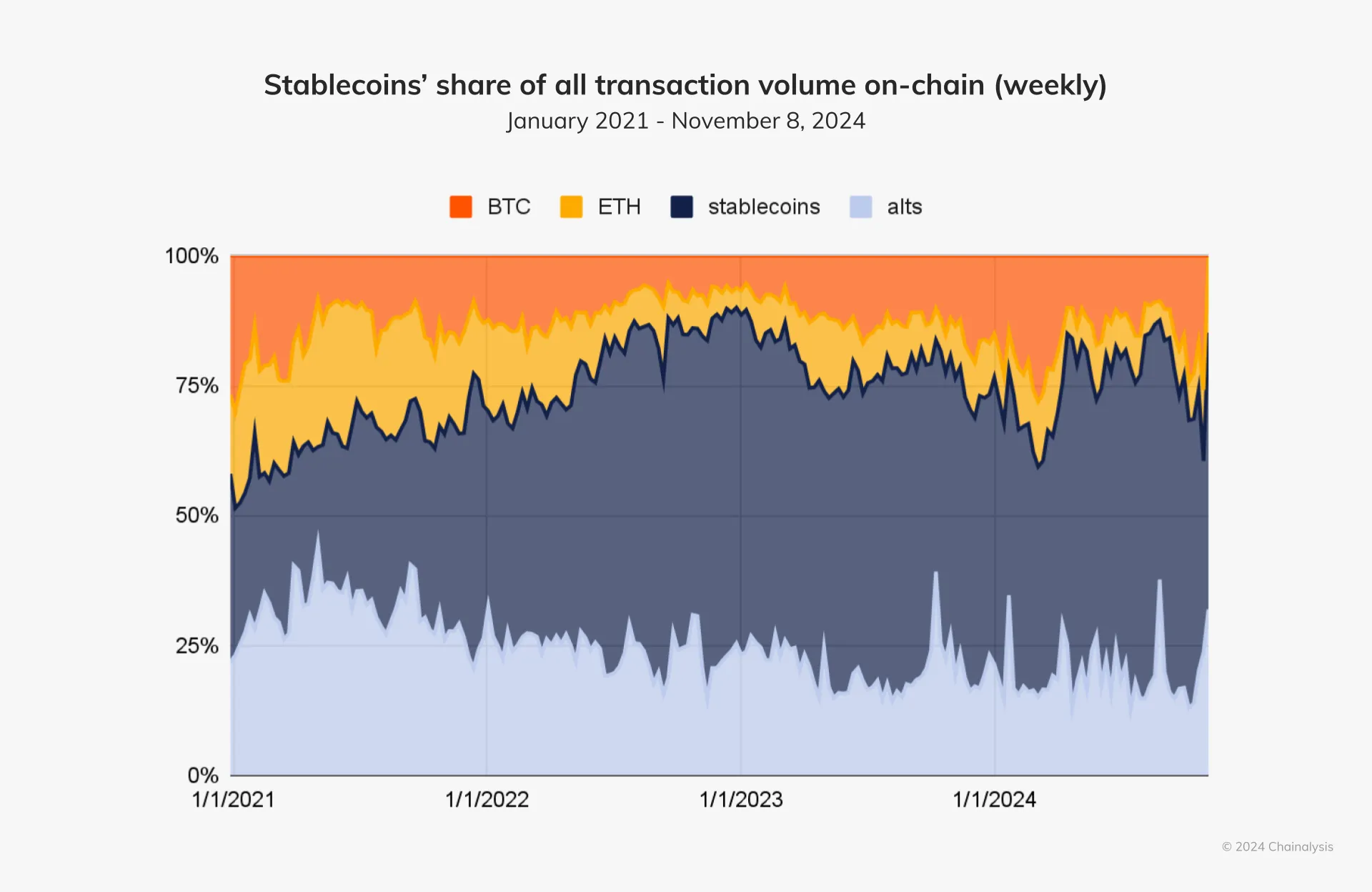

While stablecoins show great potential as payment and remittance systems, their most common use today is within cryptocurrency exchanges. Looking at the evolution of stablecoins, during the bull market of 2017 and 2021, the need for dollar-denominated assets grew as exchanges expanded, and stablecoins emerged as the ideal solution, leading to their rapid growth.

Many crypto exchanges struggled to establish or maintain relationships with traditional banks. After 2017, as regulatory uncertainty around crypto market increased, banks became increasingly hesitant to work with crypto-related businesses. In this environment, stablecoins offered exchanges a way to provide dollar-based transactions without requiring direct connections to traditional financial systems.

For instance, when exchanges had their banking services suspended in certain countries due to regulatory uncertainties, stablecoins allowed them to maintain operations by giving users a way to deposit and withdraw dollar-valued assets. This became crucial for exchanges operating in regions with strict or unclear regulations.

Stablecoins also became an efficient solution for transferring funds between different exchanges. Unlike traditional bank transfers with high fees and lengthy processing times, stablecoin transfers are fast, inexpensive, and available 24/7. This enabled traders to more effectively execute arbitrage strategies across multiple exchanges.

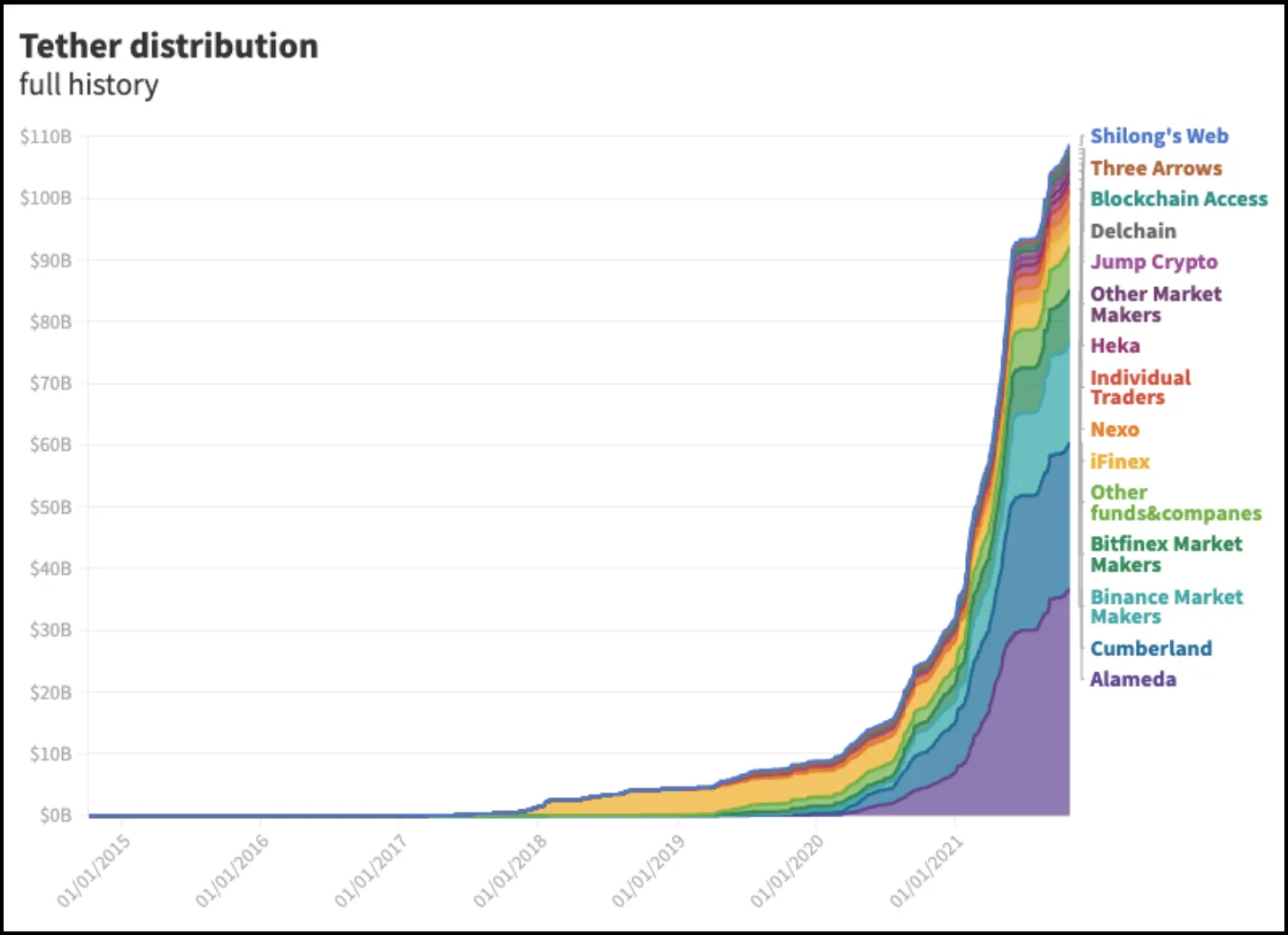

Source: Tether Papers - Protos

During Tether's (USDT) market cap surge in 2021, most of the issuance was concentrated among market makers and hedge funds. At that time, the largest holder of Tether wasn't the issuer iFinex, but Alameda Research, the sister company of FTX.

As stablecoin adoption accelerated on exchanges between 2017 and 2021, they became the standard base currency for trading pairs. With BTC/USDT pairs replacing BTC/USD, exchanges could operate using only stablecoins without needing to maintain separate dollar markets for each cryptocurrency. This simplified exchange operations while offering users more trading options.

In summary, stablecoins were instrumental in cryptocurrency exchange growth, while exchanges provided the essential platforms for stablecoins to build liquidity and a user base. This mutually beneficial relationship has strengthened as the crypto ecosystem expanded, explaining why a significant portion of stablecoin activity today occurs within or between exchanges.

2.2.2 How Exchanges Strengthen Tether’s Dominance

"People don't understand how powerful the moat is - they won the game of being money on exchanges. For Binance to try and change the status quo of having USDT as the quote currency would be an enormous risk to their business, so they never want to touch it”

Guy Young, CEO of Ethena Labs

The liquidity, deposit/withdrawal routes, and user base built around exchanges for stablecoins have created powerful network effects, providing stablecoin issuers with first-mover advantages that have led to sustained market dominance. The case that best illustrates this phenomenon in the stablecoin market is Tether and the TRON blockchain.

Source: Visa Onchain Analytics

Since its initial launch in 2014, Tether has maintained nearly 70% market share despite continuous challenges from competitors and extremely volatile market conditions. Circle, the issuer of USDC, can be considered a major competitor in the stablecoin market. Despite being more regulation-friendly and actively engaged with traditional companies compared to Tether, Circle still struggles to threaten Tether's position.

Three major factors can be identified in Tether's ability to build and maintain dominance:

First-mover advantage: Tether was the first to enter the stablecoin market and built a strong network of connections between exchanges and users. This early advantage created a barrier that has been difficult for latecomers to overcome.

Liquidity: Tether is the stablecoin with the highest liquidity on most exchanges, meaning large transactions can be executed without significantly impacting the market. High liquidity has created a virtuous cycle, attracting more users and traders.

Exchange integration: Tether has secured routes for easy deposits and withdrawals through deep integration with major cryptocurrency exchanges. This integration has enhanced the usability of Tether and led more users to choose it.

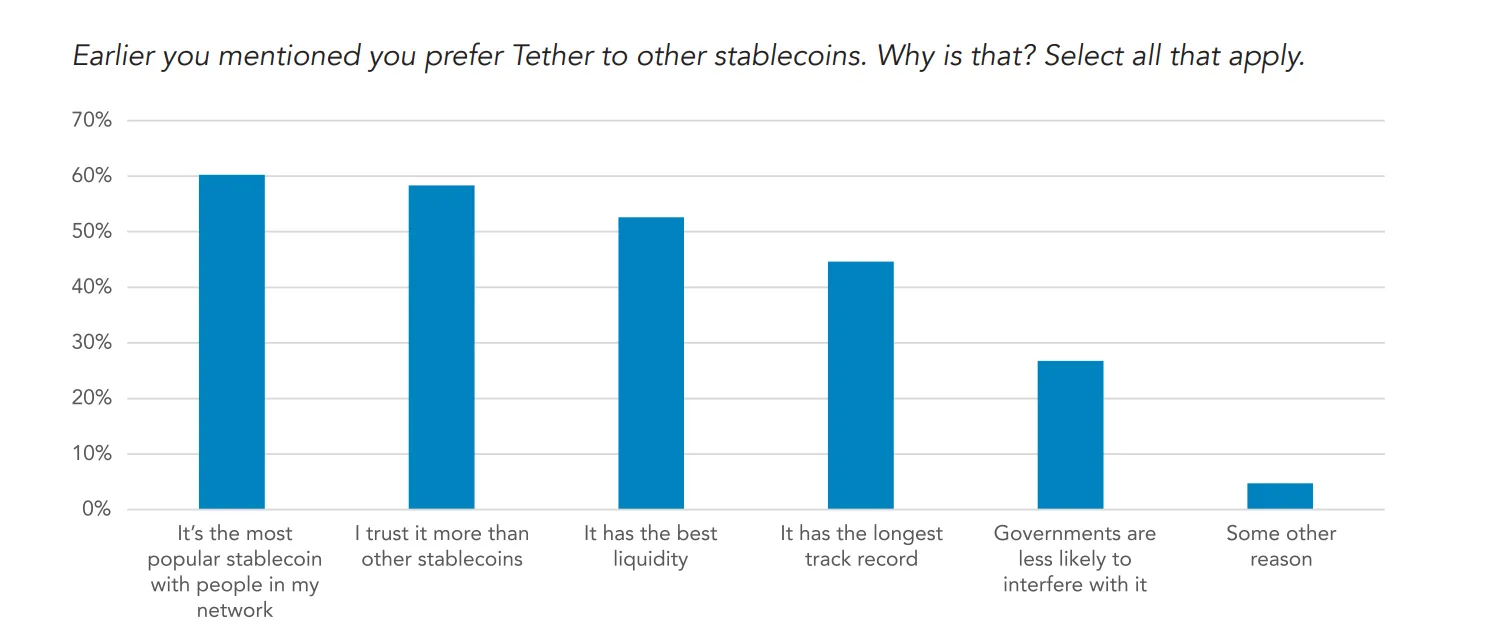

Source: Stablecoins: The Emerging Market Story - Castle Island Ventures

According to a stablecoin market analysis published by Castle Island Ventures, users prefer Tether because "it's widely used around them" (60%) and "it has high credibility" (58%). This indicates that the initially established user base and trust continue to translate into market dominance.

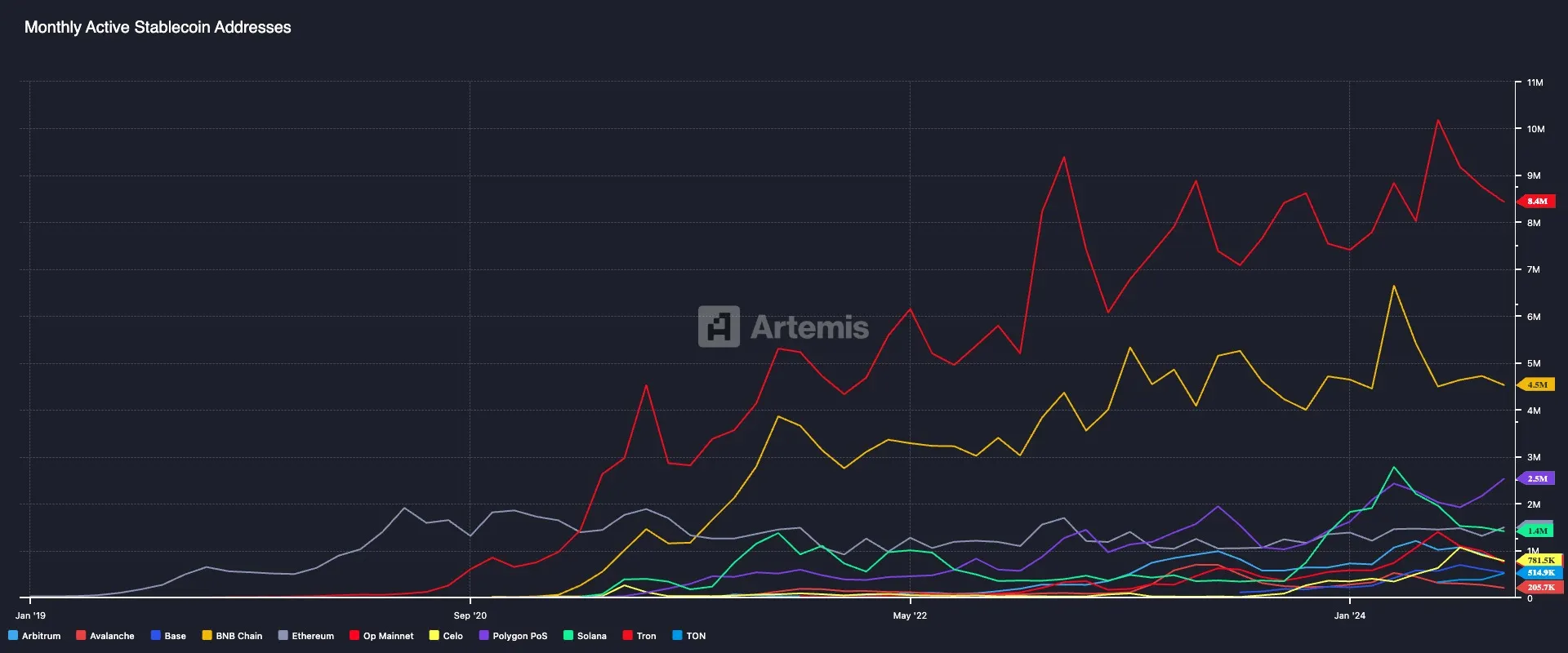

Source: Artemis Stablecoin Dashboard

The TRON blockchain presents another case of influence in the stablecoin market centered around exchanges. Compared to other major blockchains like Ethereum, Base, and Solana, TRON ranks lower in terms of monthly transaction volume, fees, and active addresses, showing relatively low network activity. However, it consistently leads in stablecoin issuance volume and active stablecoin trading addresses.

The following factors have played important roles in TRON's unusually high market share in the stablecoin sector:

Low transaction fees and fast settlement times: During boom periods when Ethereum gas fees soared, TRON offered significantly lower transaction fees, making it a suitable alternative for small transactions. Its fast block confirmation time also provided advantages to market makers and traders sensitive to timing in fund movements between exchanges.

Strategic partnership with Binance: From the early launch of the TRON network, Binance supported TRON as the default blockchain for Tether deposits and withdrawals. Considering that Binance has over 150 million users in more than 150 countries, with particularly strong positions in emerging markets such as Latin America, Africa, and Asia, this made TRON-based Tether the default choice for retail users.

After initial market penetration through Binance, the TRON network began to be adopted as the default option for Tether deposits and withdrawals on other major global exchanges, naturally creating a virtuous cycle where users choose the TRON network when moving funds between exchanges. As a result, TRON has established itself as the de facto standard for on-chain stablecoin transfers, particularly becoming the most common on/off-ramp route for individual users in emerging markets.

In conclusion, the cases of Tether and TRON well illustrate how first-mover effects and network effects centered around exchanges can powerfully operate in the stablecoin ecosystem. Platforms that secure an early user base and liquidity can maintain their advantage based on these benefits, making it difficult for new competitors to enter the market. These network effects also serve as an important foundation for stablecoins to expand into broader use cases beyond simple trading mechanisms and become payment infrastructure.

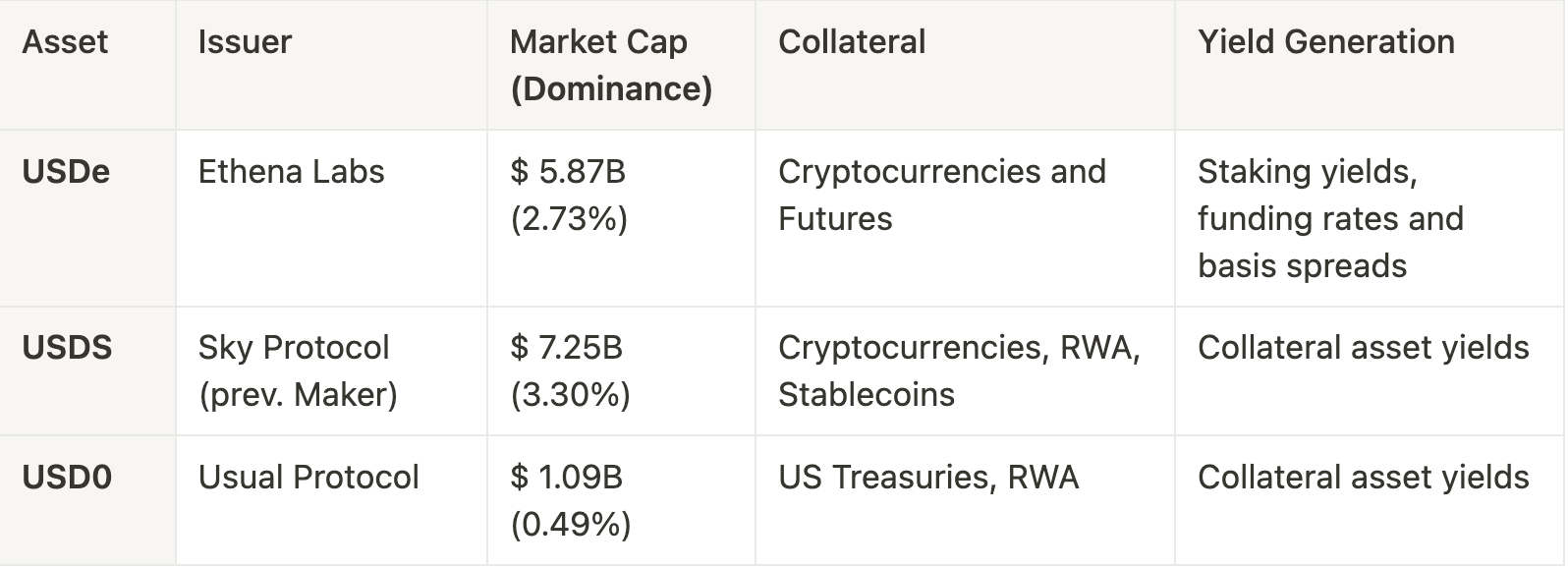

Yield-bearing stablecoins have carved out a significant position in the stablecoin market, representing approximately 6-7% of total market issuance. Unlike USDT or USDC, which primarily function as mediums of exchange, these stablecoins primarily serve as stores of value.

Different yield-bearing stablecoins employ various collateral structures and revenue generation methods. Ethena Labs' USDe uses cryptocurrencies and futures as collateral, while Sky Protocol's USDS (previously Maker Protocol) is backed by a combination of cryptocurrencies, RWAs, and other stablecoins. Usual Protocol's USD0 generates returns primarily from US Treasuries and other RWAs.

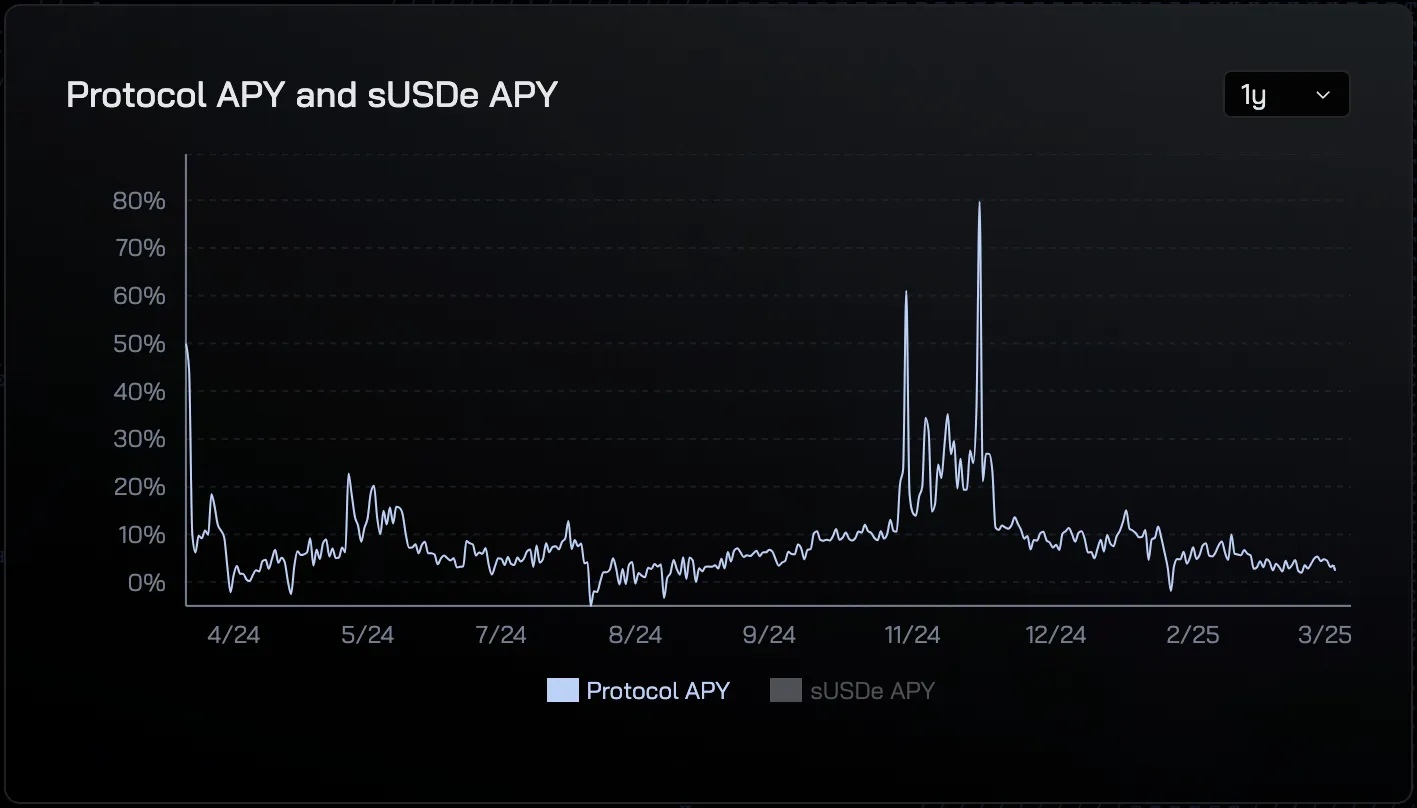

Source: Ethena Protocol Transparency

What unites these stablecoins is their ability to leverage blockchain's unique mechanisms to deliver interest rates that would be difficult to achieve in traditional finance. They offer impressive yields—ranging from 5% to double-digit percentages—without exposing holders to the volatility typically associated with crypto assets.

These products fill an important market gap. Standard stablecoins like USDT and USDC don't protect against inflation, whereas yield-bearing alternatives provide actual asset growth beyond simply holding cash. For progressive investors, they represent an attractive middle ground—offering better yields than traditional low-risk investments while maintaining significantly more price stability than volatile crypto assets.

3.1.1 Regulatory Uncertainty and Sovereignty Concerns Following Stablecoin Expansion

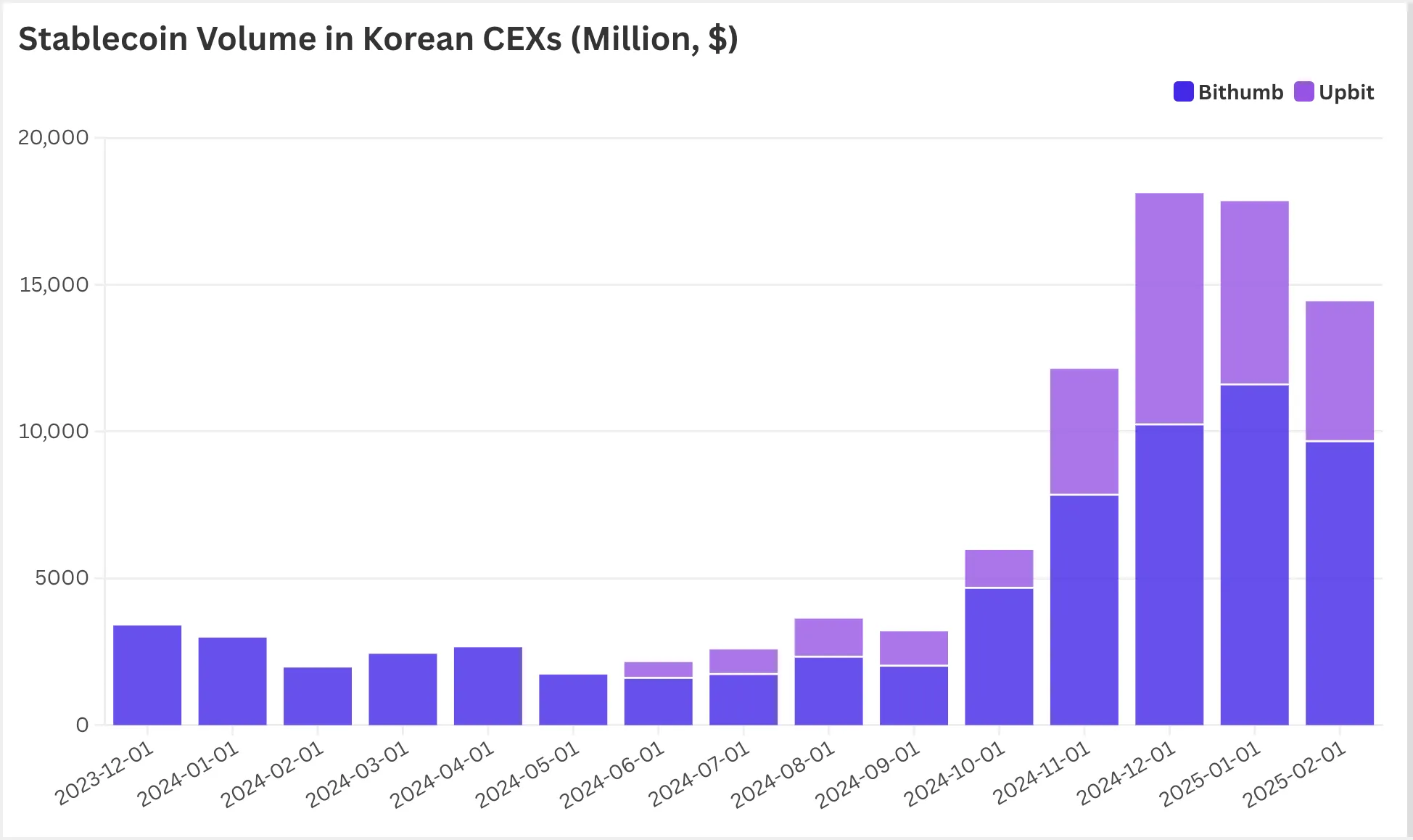

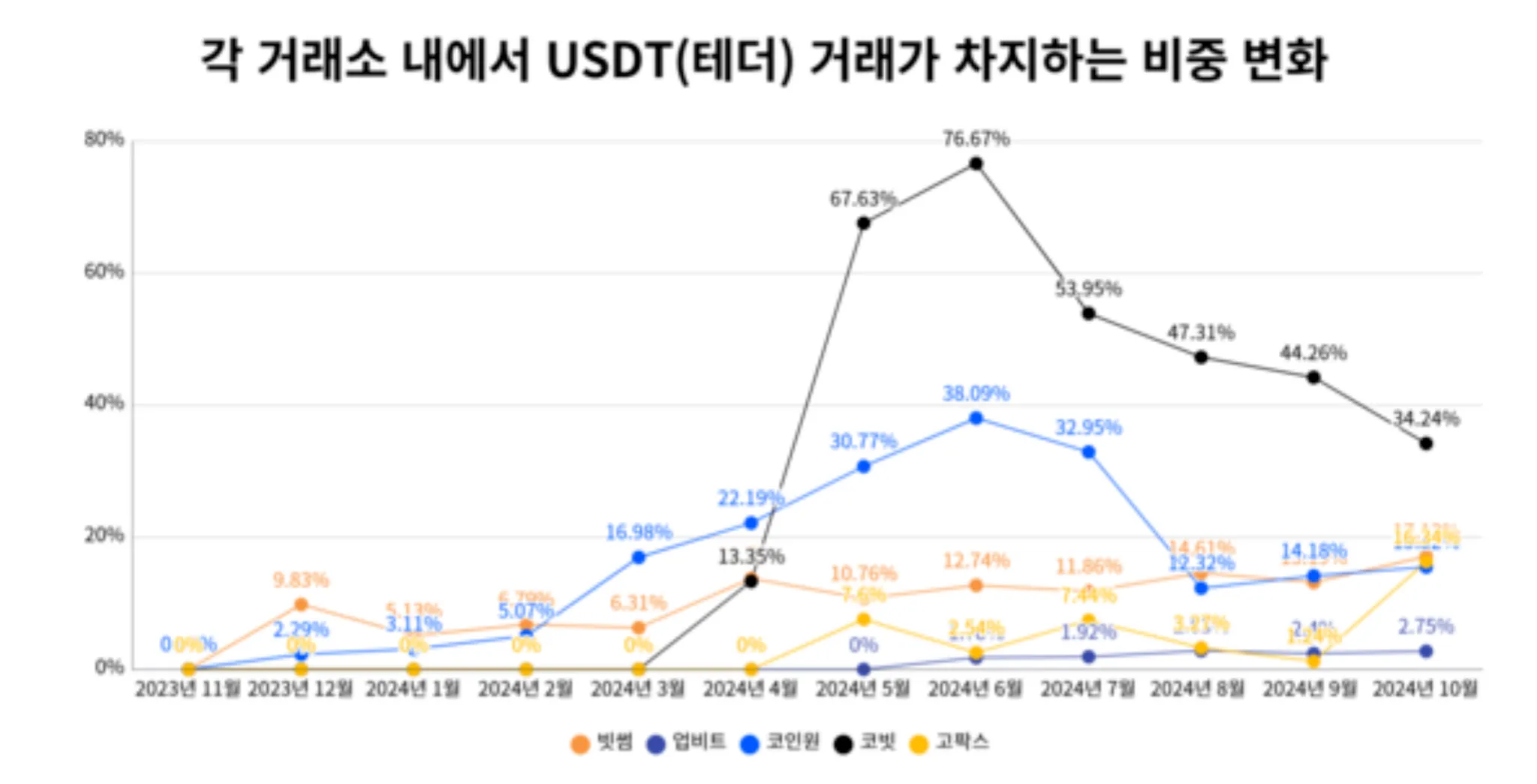

Dollar-based stablecoins first entered the Korean cryptocurrency market when USDT was listed on Bithumb in late 2023. Following this, other major exchanges including Upbit, Coinone, and Korbit also began listing USDT and other dollar-based stablecoins. Since their introduction, stablecoin trading volume has grown remarkably fast, now accounting for over 20% of the total daily trading volume across major exchanges. The combined weekly USDT trading volume on Upbit and Bithumb already exceeds $1 billion, making it the second highest traded cryptocurrency after Bitcoin.

This rapid growth of dollar-based stablecoins has raised significant concerns from a financial policy and regulatory perspective. It's challenging to clearly define whether these dollar-pegged coins are payment instruments or capital, and as stablecoins' influence expands and their adoption in the real economy increases, this distinction will become even more difficult to maintain and control. This could potentially threaten the stability of Korea's financial system and the utility of the Korean won.

Source: “9조 거래” USDT(테더), 韓 시장서 빠르게 확산 - 디지털 에셋

Chang-Yong Lee, a Governor of the Bank of Korea, has explicitly expressed concern that widespread adoption of stablecoins could diminish the role of central bank money and reduce the effectiveness of monetary policy. This is being recognized not just as a change within the cryptocurrency market, but as a fundamental challenge to the national monetary system and economic sovereignty. Furthermore, if stablecoins issued by global companies like PayPal's PYUSD and associated payment solutions become more widespread, it could make it increasingly difficult to manage domestic capital flows and maintain monetary policy independence.

Under the current regulatory framework, the legal status of dollar-pegged stablecoins remains ambiguous. There's no clear definition of whether they should be considered "payment instruments" under foreign exchange law or as part of capital transactions. This legal uncertainty makes effective supervision and regulation difficult. While stablecoins traded on exchanges with KYC and Travel Rule compliance can be somewhat controlled, as the scope of stablecoin utilization expands and real economic activity conducted through stablecoins increases, these measures alone may not be sufficient to prevent the erosion of the won-based economic zone.

Additionally, most stablecoin issuers are foreign companies that aren't directly subject to domestic regulatory oversight. This creates potential blind spots in Korea's financial regulatory framework, particularly limiting the authorities' ability to intervene during crisis situations. The current situation, where dollar-based stablecoins account for more than 95% of the global stablecoin market, presents a direct challenge to Korea's won-centered financial ecosystem.

3.1.2 Evaluating the Possibility of Stablecoin Adoption in Korea's Economy

In light of the rapidly growing stablecoin trading volume on Korean exchanges and the strategic moves being made in the United States, concerns have emerged about whether stablecoins are already being widely adopted in Korea's real economy. Some media reports have claimed that local vendors are conducting transactions with stablecoins, or that approximately 10% of foreign trade is settled using stablecoins. However, actual investigation revealed these claims to be largely exaggerated. Dongdaemun merchants still prefer cash transactions, and digital payment system adoption remains low. In official foreign trade settlements, traditional banking channels continue to dominate, with stablecoin usage accounting for at most 3% of transactions.

Despite these concerns, the possibility of widespread adoption of dollar-based stablecoins in Korea's real economy remains limited at present. This is due to structural factors specific to the Korean market.

First, Korea has one of the world's most advanced financial and fintech service environments, which reduces the demand for switching to stablecoins. With high adoption rates of major domestic fintech services like Toss, KakaoPay, and NaverPay, the additional utility that stablecoins could provide is relatively limited. In particular, leading fintech services like Toss already abstract away most inefficiencies in the existing financial system, offering 24-hour real-time transfers, low fees, and high accessibility—most of the advantages that stablecoins claim to offer. This isn't unique to Korea; stablecoins have rarely replaced existing fintech services in major developed countries.

Additionally, the persistent "kimchi premium" in the Korean market acts as an economic barrier to accessing dollars through stablecoins. Throughout 2024, dollar-based stablecoins traded on domestic exchanges have maintained an average premium of 3-7% compared to global markets, forcing investors to accept unfavorable exchange rates when purchasing dollars with Korean won. While we mentioned earlier that stablecoins have become established as a means of dollar access in emerging markets despite premiums, these countries generally lack viable alternatives for accessing dollars—a fundamentally different condition from Korea, which already has relatively high dollar accessibility through other means.

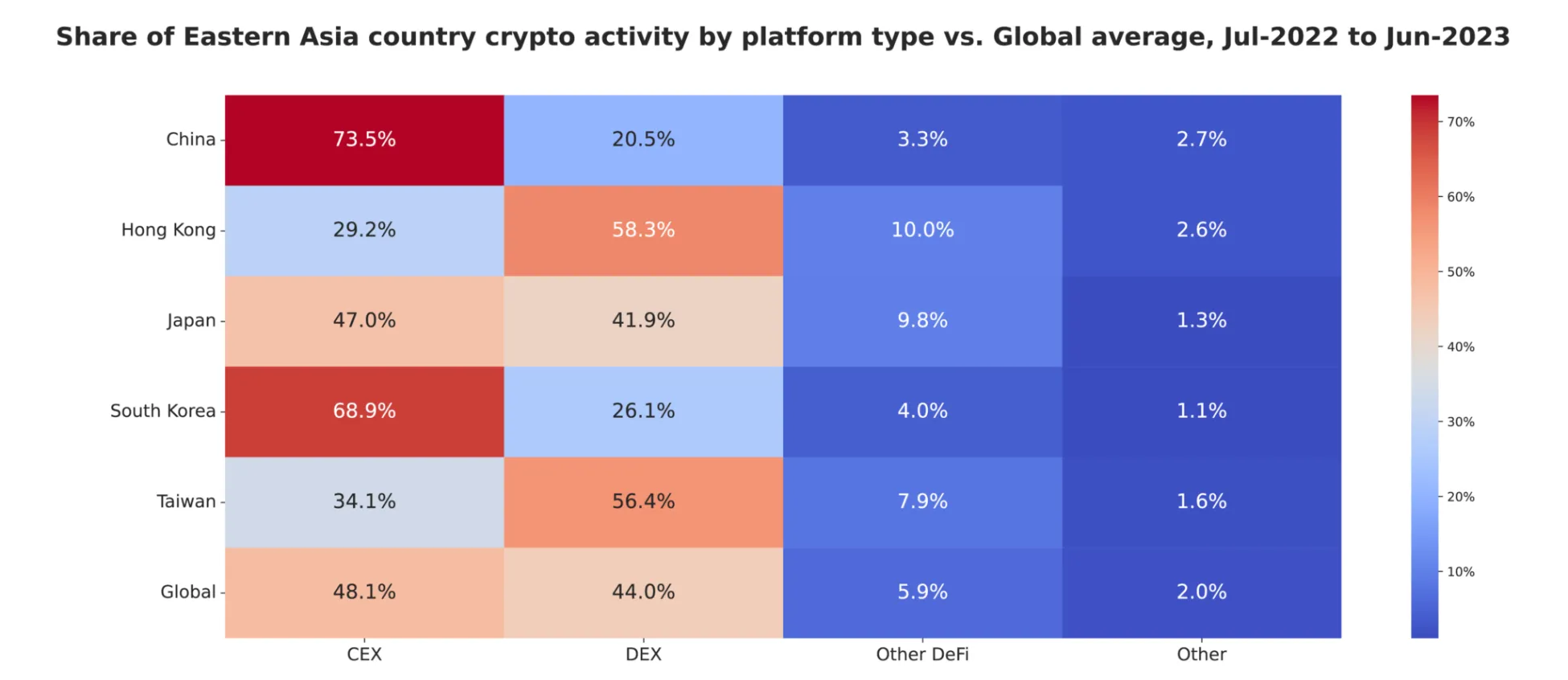

Source: Eastern Asia Cryptocurrency Adoption 2023 - Chainanalysis

Lastly, considering that Korea's adoption and utilization of onchain tools remains lower than global levels, stablecoin adoption in the real economy appears premature. Compared to other countries, Korea faces higher language and cultural barriers, meaning that cryptocurrency wallets and transfer services haven't yet gained sufficient traction. Moreover, due to strict regulations, most services for purchasing cryptocurrencies outside of exchanges are not permitted, making it difficult to establish a sufficient user base for utilizing stablecoins in the real economy.

3.2.1 Gateway to Overseas Exchanges and DeFi

Source: Eastern Asia: Institutions Drive Adoption in South Korea and Hong Kong - Chainanlysis

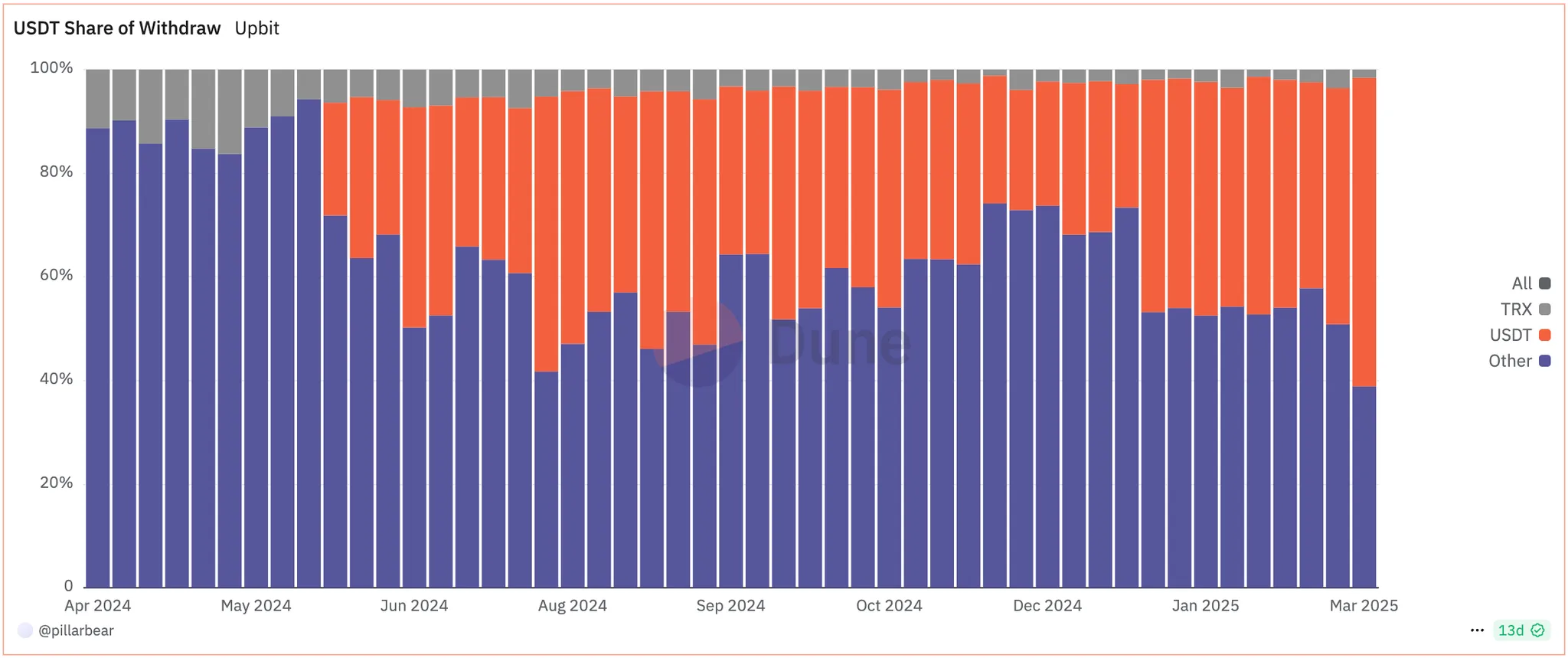

According to data provided by Chainalysis, the main purpose of stablecoin transactions appears to be transferring funds from domestic exchanges to foreign exchanges or personal wallets. The proportion of stablecoins in outflows from Korean exchanges began to increase dramatically from the moment USDT was first listed on Bithumb in late 2023. Notably, the amount of stablecoins flowing to overseas exchanges during this period showed figures very similar to Bithumb's USDT trading volume, suggesting a strong correlation between these two phenomena.

A similar pattern appears to be occurring at Upbit, Korea's largest cryptocurrency exchange. Since USDT was listed in June 2024, the proportion of stablecoins in total transferred funds has continuously increased. According to the most recent data, approximately 60% of total outflows are now occurring through USDT. This indicates that stablecoins have quickly become the primary channel for Korean investors to transfer funds to overseas exchanges.

The main reasons for preferring stablecoins when transferring funds are clear. Stablecoins minimize exposure to price volatility during the transfer process, allowing users to avoid unwanted market risk. Additionally, since most global exchanges support deposits and withdrawals of major stablecoins like USDT or USDC, users can immediately utilize them for trading without additional conversion steps, increasing transaction efficiency.

3.2.2 Inefficiencies in Korea's Cryptocurrency Market

At the root of capital outflow through stablecoins lies the structural inefficiency of Korea's cryptocurrency market. These inefficiencies stem from interconnected factors: the market's closed structure, limited product diversity, and disconnection from global markets.

A defining characteristic of Korea's cryptocurrency market is its strict regulatory environment and resulting isolation from global markets. Under the current regulatory framework, users must be domestic residents with verified personal mobile phones and local bank accounts—an intensive identity verification process. While intended to prevent money laundering and protect investors, this creates a powerful entry barrier that restricts market participation to Korean citizens only, limiting market liquidity and connectivity.

Source: Eastern Asia Cryptocurrency Adoption 2023 - Chainanalysis

The prohibition on corporate cryptocurrency exchange accounts is particularly significant as it fundamentally excludes institutional investors from the Korean market, weakening market stabilization and price discovery. Although discussions about allowing corporate participation since 2024, the initial phase is expected to be highly restrictive with limited practical benefits.

Korea's strict regulatory environment also directly constrains investment opportunities. While overseas exchanges and DeFi services offer comprehensive financial services—from spot trading to futures, margin trading, options, liquidity staking, and interest-bearing products—domestic exchanges are essentially limited to simple spot trading. This lack of product diversity goes beyond merely reducing investment options; it eliminates chances of risk management and portfolio optimization for investors. Without hedging mechanisms during market downturns or leverage opportunities during uptrends, efficient capital allocation and investment strategy development become impossible.

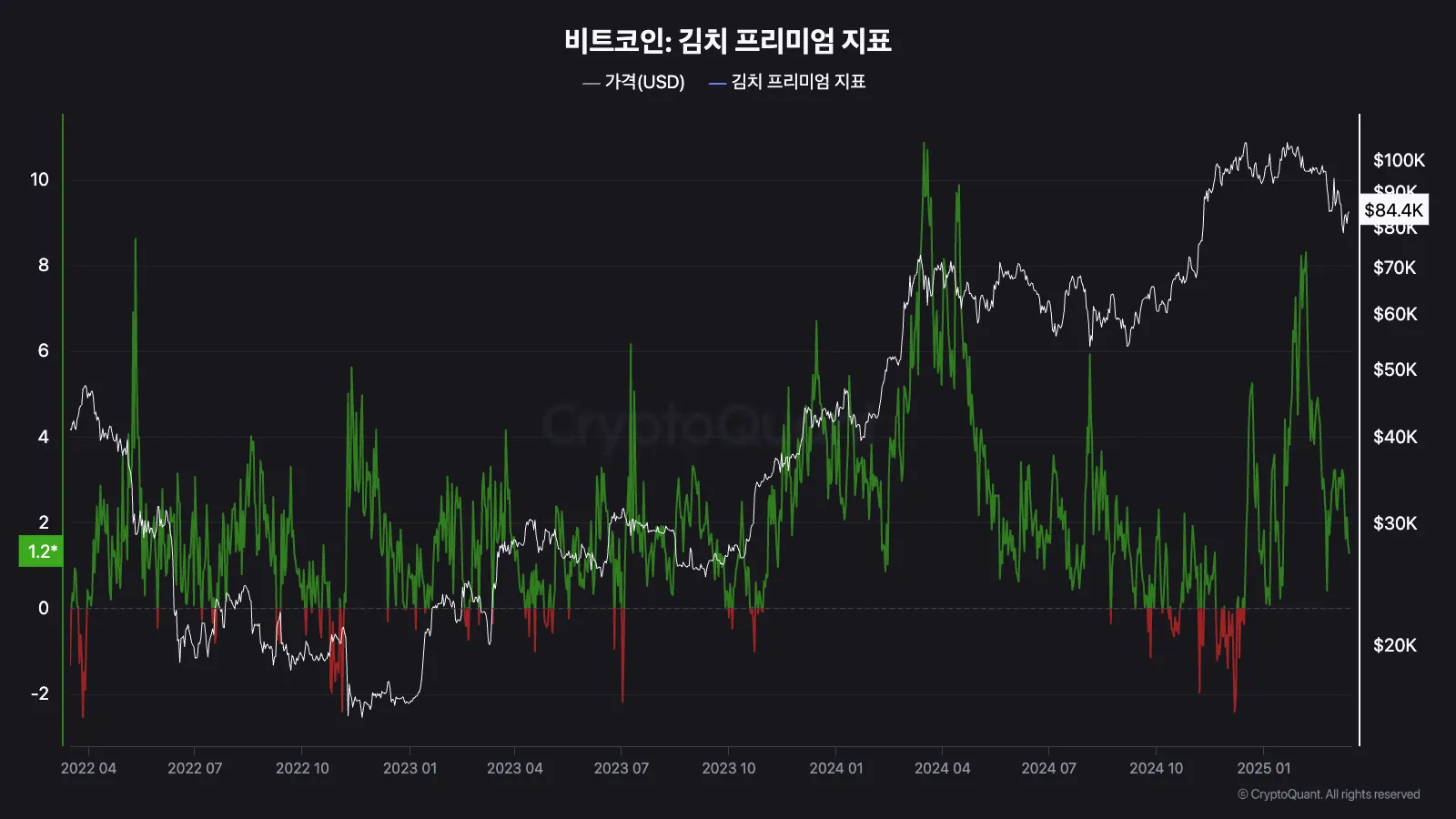

Source: Bitcoin Kimchi Premium - CryptoQuant

The Korean cryptocurrency market's closed nature increases the cost of accessing won-based markets, creating persistent price disparities with global markets. The "kimchi premium"—the price premium in domestic exchanges compared to global exchanges—typically ranges from 3-7% even in normal market conditions, reaching nearly 10% during investment frenzies, causing continuous harm to Korean investors. The fundamental reason for the kimchi premium is that restricted capital movement between domestic and international markets prevents arbitrage from normalizing prices.

Source: Kimchi Premium: Key Traits and Causes in Korea's Crypto Market

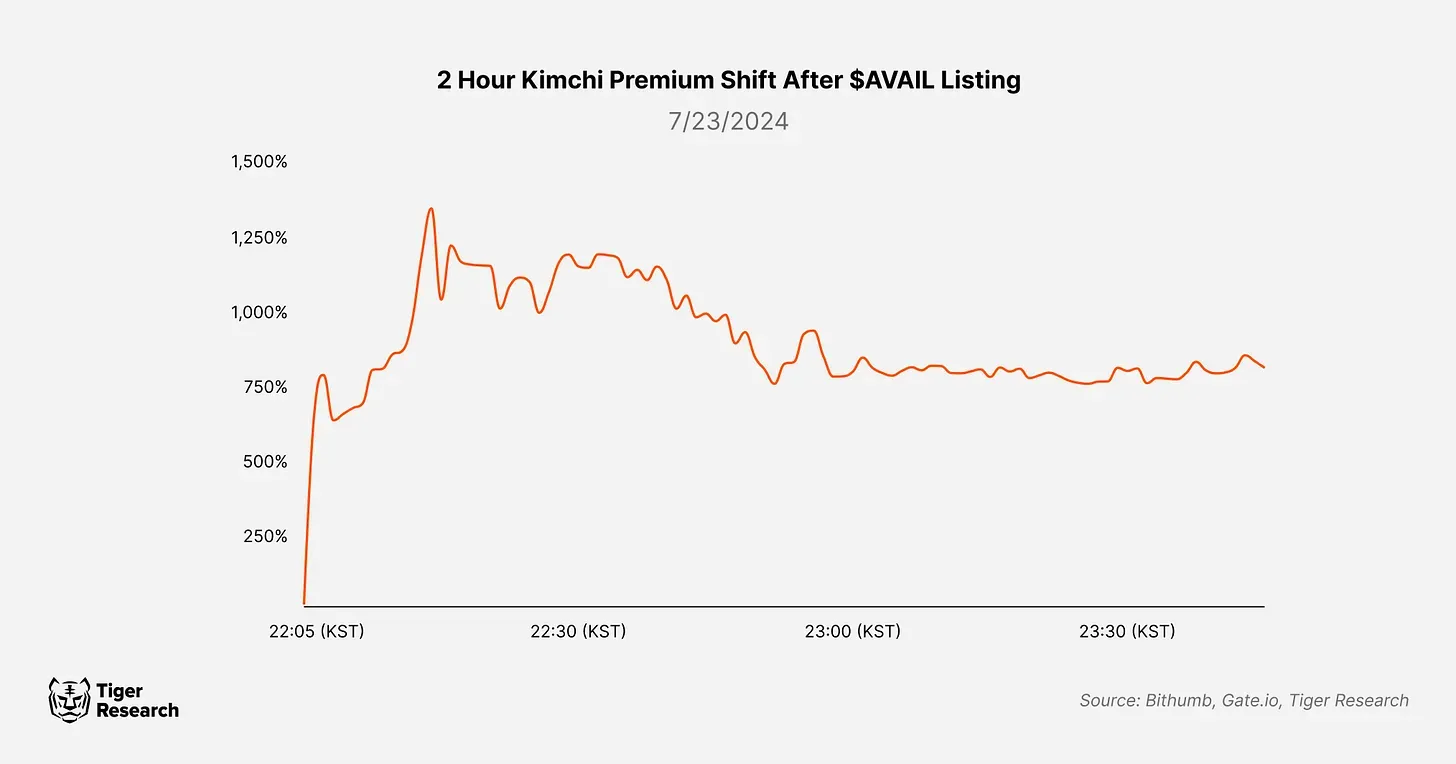

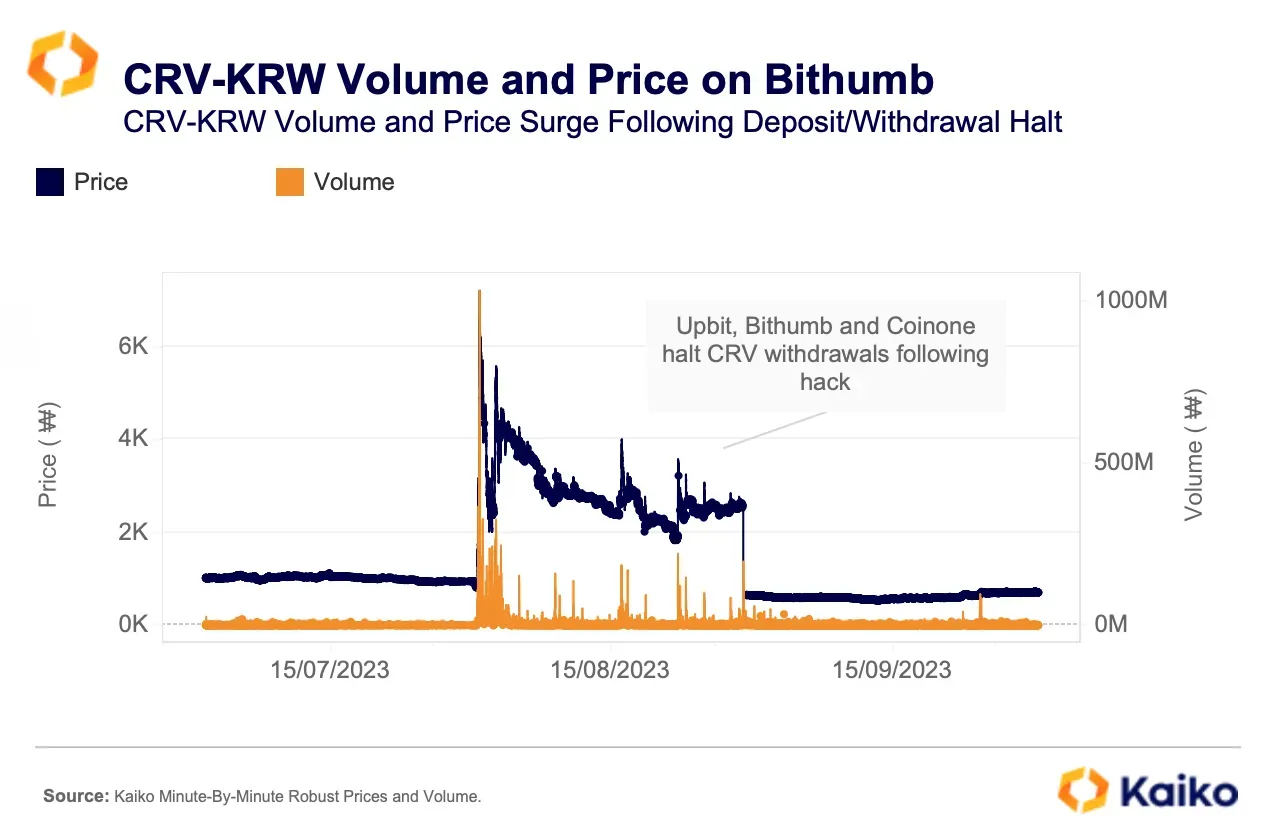

Sometimes, the price disparity caused by market isolation manifests in extreme forms like "listing beam" or "captive pumping." Listing beam refers to newly listed assets experiencing abnormal price surges on domestic exchanges compared to global markets. A prominent example was the $AVAIL listed on Bithumb in July 2024, which recorded an astronomical 1,255% premium over global markets. This isn't a temporary phenomenon but a recurring one stemming from structural market inefficiencies, interfering with rational investment decisions and creating unnecessary loss risks.

Source: Kimchi Premium: Key Traits and Causes in Korea's Crypto Market

The "captive pumping" phenomenon similarly occurs when deposits and withdrawals for specific cryptocurrencies are temporarily suspended, allowing extreme price volatility due to limited liquidity. In August 2023, Curve DAO Token ($CRV) formed a nearly 700% price premium on domestic exchanges despite suspended deposits and withdrawals due to security vulnerabilities. These abnormal price formations represent pathological phenomena resulting from information asymmetry, Korean retail investors' high speculative tendencies, and isolated market environments, fundamentally undermining a healthy investment environment.

Ultimately, the structural inefficiencies of Korea's cryptocurrency market can be understood as a chain reaction caused by the closed market structure and regulatory constraints. Liquidity shortages due to restricted market participation, investment strategy limitations due to product diversity deficiencies, and price distortions due to isolation from global markets interact to form a self-reinforcing inefficiency structure. As long as these structural problems remain unsolved, the exodus of rational investors to overseas markets will remain inevitable.

3.2.3 Accelerating Exodus and Emerging Risks to Monetary Sovereinity

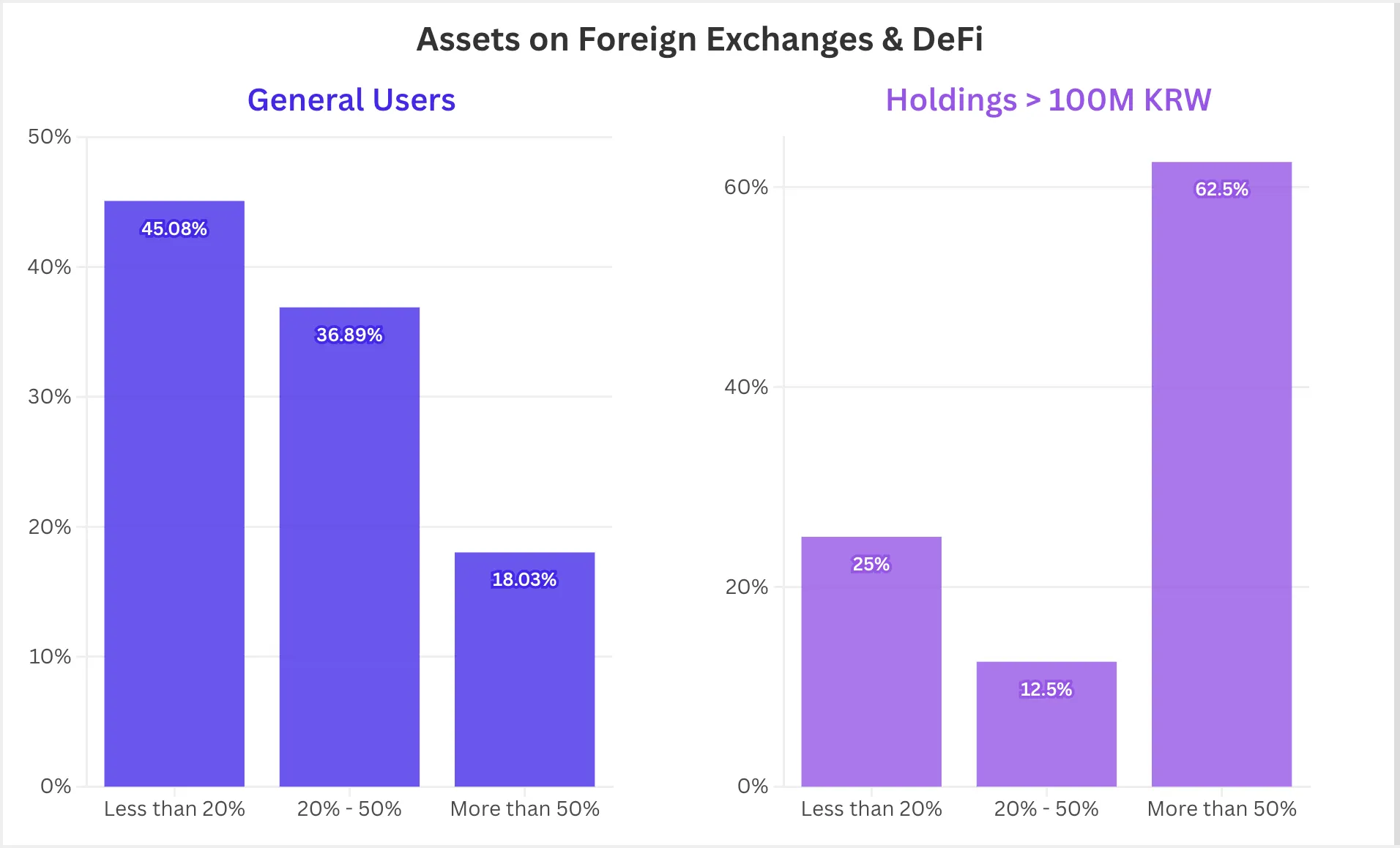

Source: 한국 가상자산 투자자, 그들은 누구인가 - 해시드 오픈 리서치

The structural inefficiencies in Korea's cryptocurrency market are driving an exodus among domestic investors. According to a survey by Hashed Open Research, while average investors primarily keep their assets on domestic exchanges, those holding more than 100 million won (approximately $75,000) clearly tend to store most of their assets on foreign exchanges or in custodial wallets. This suggests that investors with greater capital and information access are more inclined to leave the domestic market.

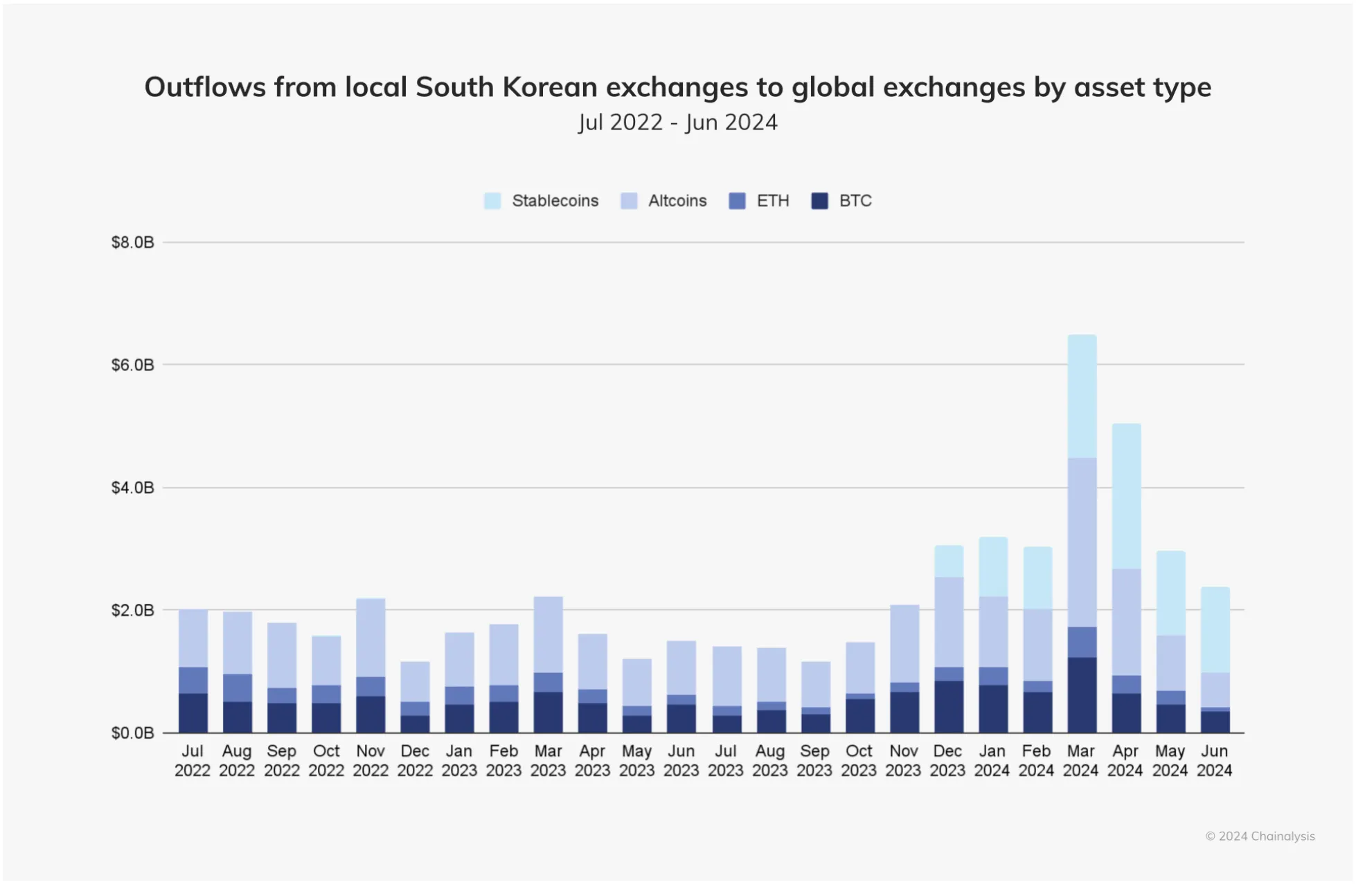

According to the Financial Services Commission's survey of virtual asset business operators, the amount of funds transferred from domestic exchanges overseas has more than tripled from 21.6 trillion won in the second half of 2022 to 74.8 trillion won in the first half of 2024—a period of less than two years. Moreover, capital flight from domestic exchanges is showing an accelerating trend. The period-to-period growth rate jumped from 28.3% in the second half of 2023 to 96.3% in the first half of 2024.

The capital outflow isn't simply about seeking better investment opportunities abroad. In an environment where structural problems in the domestic cryptocurrency market undermine investor confidence and make rational investment decisions difficult, moving to overseas platforms has become almost inevitable.

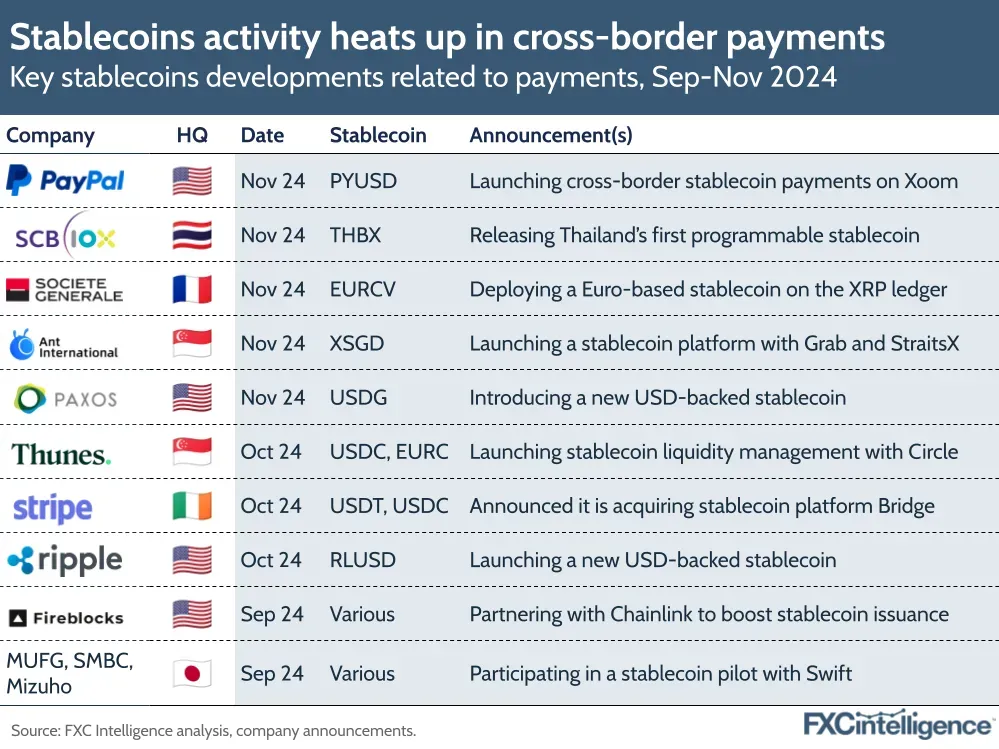

Source: Stablecoin payments heat up in 2024

The impact will increase as the line between cryptocurrencies and the real economy continues to thin. Integration of stablecoins with traditional financial systems is already advancing quickly in global markets. In the US and Europe, people can now get Visa or Mastercard cards linked to their crypto wallets, or use stablecoins directly through payment platforms like PayPal, Stripe, and Shopify.

If these services become widely available to average consumers in Korea, dollar-based stablecoins could extend their influence into the real economy, which would likely weaken the role and control of the Korean won. Such developments would be difficult to address through basic regulations or company-level initiatives alone.

In summary, the growing stablecoin trading volume in Korea reflects more than just speculative interest—it indicates capital leaving the domestic market due to fundamental inefficiencies in Korea's cryptocurrency ecosystem. This presents a meaningful challenge to the long-term strength of the won-based economy and Korea's financial system, requiring forward-thinking solutions. The next chapter will explore the potential introduction of a Korean won stablecoin as a possible response to these structural issues and its expected benefits.

4.1.1 The Intensifying Global Competition in the Stablecoin Market

While there are various perspectives on the stablecoin market, it's unlikely that this massive and influential market will remain permanently monopolized by the US dollar or controlled exclusively by Tether and Circle. Instead, we expect countries to develop stablecoins based on their national currencies and integrate them into their existing economic systems.

Many countries are now competing to establish their position in the stablecoin market and protect their currency's usability by implementing regulatory frameworks and collaborating with businesses. In response to the growing influence of USD-based stablecoins that threaten the usability of domestic currencies, numerous nations are implementing their own regulatory requirements and partnering with companies.

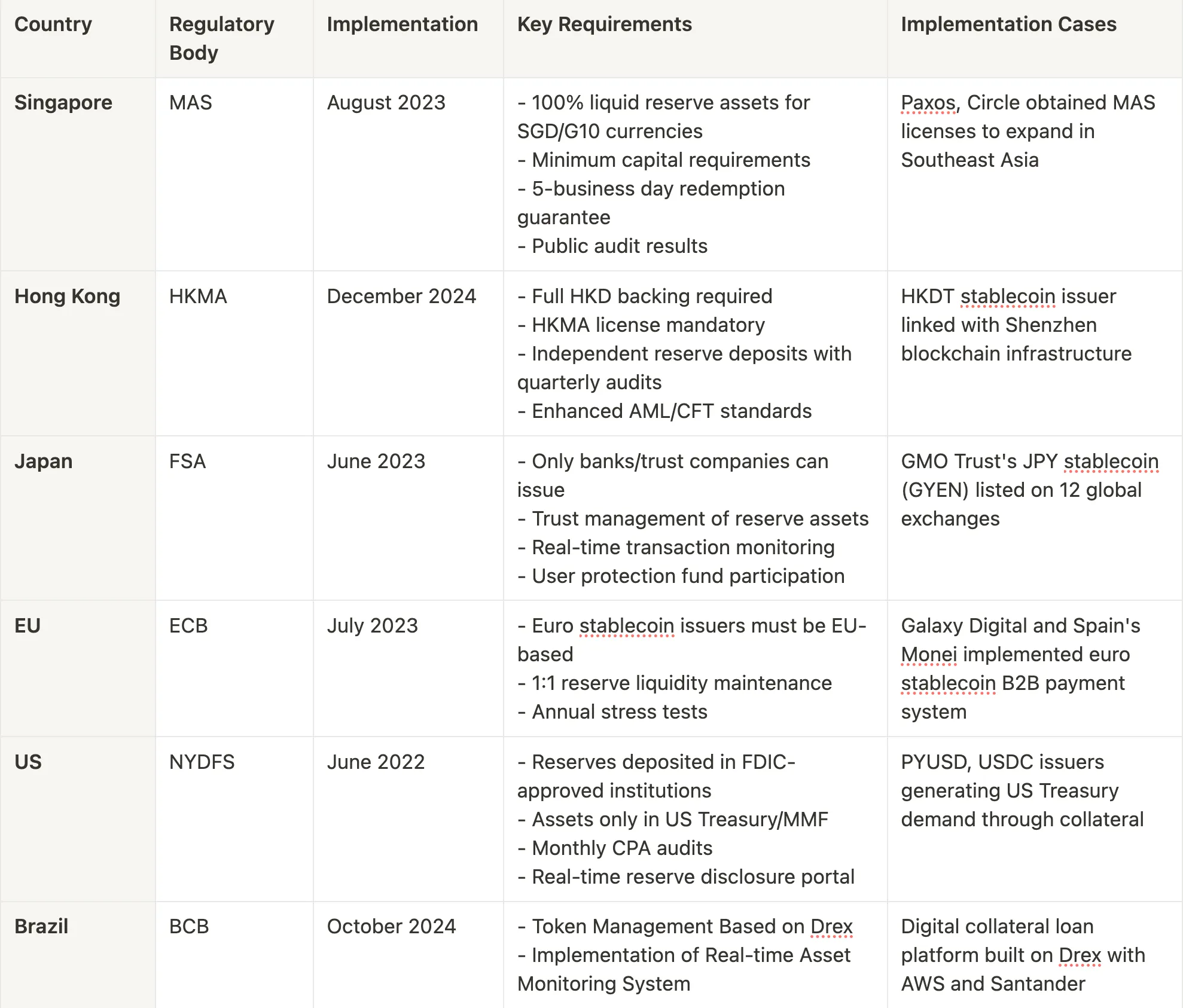

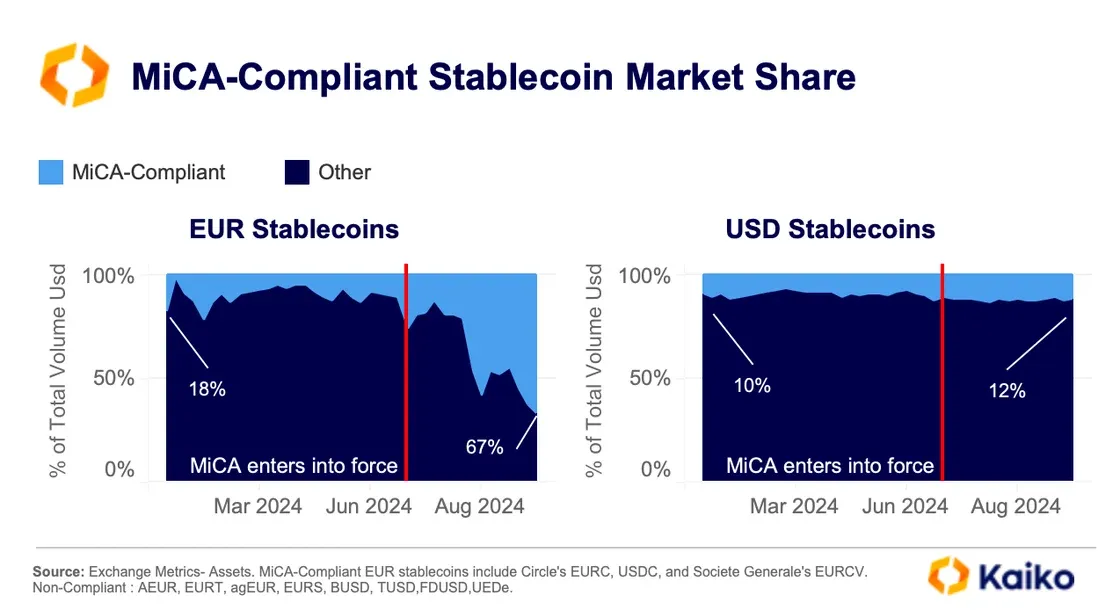

The EU has already established a comprehensive and harmonized regulatory framework for stablecoins through MiCA (Markets in Crypto Assets Regulation). This regulation provides a consistent legal environment for stablecoin issuance and operation across all EU member states, offering legal clarity to market participants, reducing regulatory fragmentation, and promoting new business and innovation.

In August 2023, the Monetary Authority of Singapore (MAS) announced a regulatory framework for Single-Currency Stablecoins (SCS). This framework targets stablecoins pegged to the Singapore dollar or G10 currencies, requiring issuers to maintain reserve assets to ensure value stability, maintain minimum base capital, and guarantee redemption within five business days.

Japan amended its Payment Services Act in 2023 to stipulate that only banks, fund transfer service providers, and trust companies can issue digital payment-type stablecoins. Stablecoins issued by banks are considered deposits and are protected by deposit insurance.

These stablecoin regulations adopted by major countries share common objectives:

Clarifying qualifications and requirements for stablecoin issuers to enhance market credibility

Setting strict standards for reserve management to ensure value stability

Emphasizing consumer protection and market transparency to build user trust

Aiming to secure the usability of national currencies in the digital economy through the issuance of domestic currency-based stablecoins

Source: MiCA is Reshaping EUR Stablecoin Markets

As stablecoin regulatory frameworks become clearer globally, we expect increased adoption of various stablecoin types. This may also promote the growth of non-USD stablecoins and expand the acceptance of digital assets across various jurisdictions and industries.

The introduction of clear regulatory frameworks like the EU's MiCA can have a positive impact on domestic currency stablecoin markets. After MiCA's implementation, stablecoin issuers complying with these regulations have shown significant market share increases compared to non-compliant issuers. This demonstrates how clear regulations can provide certainty to market participants and ultimately lead to greater adoption.

4.1.2 The Need for Stablecoin Regulation and KRW Stablecoin in Korea

Korea now needs to take proactive measures regarding stablecoin regulation. Currently, Korea lacks clear regulations specifically addressing stablecoins. However, as stablecoins grow in influence and scale, and considering international regulatory trends including the US's efforts to strengthen dollar dominance and other countries' responsive measures, there are increasing calls to establish a regulatory framework for stablecoins as soon as possible.

A Korean won (KRW) stablecoin could serve as more than just a new financial product—it could be an important tool for protecting and strengthening Korea's monetary sovereignty in the evolving global digital financial ecosystem. Particularly as dollar-based stablecoins exert greater influence on the financial system, a KRW stablecoin could play a crucial role in preserving the won's usability within the digital economy.

Currently, the trading volume of dollar-based stablecoins like USDT is surging in domestic and international cryptocurrency markets, and payment solution companies recognizing stablecoins' potential are rapidly adopting them. However, even if such services are introduced in Korea, without Korean won-based assets specifically for Korean users, they would have to rely on dollar-based transactions.

If this trend continues, the competitiveness of Korea's digital asset market and the usability of the Korean won will inevitably weaken in the long term. In this context, introducing a KRW stablecoin could serve as a catalyst for preserving the won's usability in the digital asset market and enhancing the competitiveness of related industries.

In these circumstances, establishing stablecoin regulatory requirements in Korea and further introducing a KRW stablecoin could be expected to have the following effects:

Securing Financial Regulatory Initiative: By establishing a clear regulatory framework, Korea can strengthen its influence in both domestic and international stablecoin markets and actively participate in setting international standards.

Strengthening KRW Usability in the Digital Economy: Introducing a KRW stablecoin would increase the utilization of the won in the global digital economy and mitigate the risk of weakened monetary sovereignty due to the spread of dollar-based stablecoins.

Improving the Health of Korea's Cryptocurrency Ecosystem: Stablecoin regulation could enhance the competitiveness of the domestic cryptocurrency market by strengthening connectivity with global markets.

In conclusion, introducing a KRW stablecoin and establishing a clear regulatory framework would be a proactive response to the expansion of dollar-based stablecoins, contributing to securing regulatory initiative at the national level and strengthening the usability of the Korean won. This would be an important strategic choice for maintaining Korea's economic sovereignty and competitiveness in the digital financial era.

4.2.1 Korea's Cryptocurrency Trading Volume Comparable to Global Markets

As explained earlier, countries are issuing stablecoins and strengthening partnerships with businesses to preserve their currency's usability, but few have achieved significant issuance volume and usage beyond the euro. Previous stablecoin initiatives by countries often failed because they couldn't secure sufficient liquidity and usability to compete with existing dollar-based stablecoins. Limited use cases and restricted access make it difficult to keep pace with rapidly evolving financial systems.

Source: State of the Korean Crypto Market

However, Korea has distinct strategic advantages that differentiate it from these countries. Korea's cryptocurrency trading volume stands out even compared to global markets, which could provide a significant strategic advantage for introducing a KRW stablecoin. Excluding Binance and Bybit, the world's largest exchanges, Upbit's trading volume is comparable to Coinbase, the largest US exchange. As of the first half of 2024, Upbit's average daily trading volume was approximately $2 billion, similar to Coinbase, and the combined volume of Korea's four major exchanges (Upbit, Bithumb, Coinone, and Korbit) exceeds that of Coinbase.

Exchanges play a pivotal role in the initial adoption and growth of stablecoins. As seen in the cases of Tether and Tron, the early user base and liquidity built around exchanges create ongoing network effects that are crucial for stablecoins to establish themselves as financial infrastructure. This is why Korea's cryptocurrency trading volume represents a key strategic advantage for KRW stablecoin adoption that other countries lack.

Korea's high trading volume signifies more than just investment enthusiasm. In the stablecoin market, securing initial liquidity and a user base forms the foundation for sustained growth, making Korea's active trading environment a decisive platform for KRW stablecoins to gain meaningful influence in the global market.

Source: Kimchi Premium: Key Traits and Causes in Korea's Crypto Market

In the first quarter of 2024, the KRW trading volume surpassed the USD trading volume in global cryptocurrency market. While this comparison excludes dollar-based stablecoins like USDT and USDC and only considers fiat currencies, it's still remarkable given the economic size difference between Korea and the US (approximately 12 times based on GDP). While major international currencies like the euro and yen show minimal market share in the stablecoin market, the Korean won's significant activity in cryptocurrency trading suggests a differentiated potential for success in the stablecoin market.

4.2.2 Potential Scale and Expandability of KRW Stablecoins

According to the Financial Services Commission's 2024 virtual asset business operator survey, total KRW deposits on domestic exchanges amount to approximately 5 trillion won ($3.5 billion). These exchange deposits alone significantly exceed the issuance volume of any non-dollar based stablecoin currently in the market. This indicates that if a KRW stablecoin were issued and adopted by major domestic exchanges, it could immediately secure the highest market share among non-dollar based stablecoins in the global stablecoin market.

Moreover, this figure only accounts for current deposits on exchanges, not considering assets held by Korean investors on foreign exchanges and personal wallets, or funds utilized in the on-chain ecosystem. When these are factored in, the potential market size for KRW stablecoins would be considerably larger.

The growth potential of KRW stablecoins extends beyond the current cryptocurrency market size and could expand further due to the following factors:

Korea's Unique Digital Economy Capabilities: Korea boasts world-class digital infrastructure and high technology adoption rates, which could accelerate the integration of digital assets into the real economy.

Potential Increase in Personal Wallet Users: The proportion of personal wallet usage among domestic cryptocurrency investors is currently low, but as user experience improves, this percentage could increase, leading to higher on-chain activity and stablecoin demand.

Potential Participation of Domestic Financial Institutions: With regulatory clarity, traditional financial institutions like banks, securities firms, and asset management companies could enter the digital asset market, providing additional growth momentum for KRW stablecoins.

In conclusion, KRW stablecoins have the potential to quickly enter the upper ranks of the global stablecoin market, representing Korea's clearest strategic advantage in the stablecoin market compared to other non-dollar countries.

4.2.3 Strategies for Ensuring Competitiveness of KRW Stablecoin

Based on Korea's active cryptocurrency market and potential market size discussed earlier, we can explore specific strategies for KRW stablecoins to secure global competitiveness.

Strategic Partnerships with Exchanges

Strategic partnerships with domestic exchanges are essential for the successful introduction of KRW stablecoins. Major Korean exchanges like Upbit and Bithumb already have millions of users and significant liquidity, making their cooperation crucial for achieving high initial adoption rates.

A relevant collaboration example is Bybit's partnership with the Brazilian real-based stablecoin (BRZ). After implementing BRZ, Bybit saw a 200% increase in trading volume in the local market and steady quarterly user growth. BRZ served as a gateway for Brazilian users to deposit and withdraw directly in their national currency without complicated exchange processes. Through on/off-ramp partnerships with the issuer, they integrated local financial systems into a single API, simplifying complex local regulations and procedures.

Integration with Payment Solutions and Web3 Ecosystem

For KRW stablecoins to achieve global competitiveness, they need to integrate seamlessly with DeFi and the Web3 ecosystem. By ensuring compatibility with internationally popular DeFi protocols, NFT marketplaces, and cross-chain bridges, KRW stablecoins can achieve high utility within the global digital asset ecosystem.

XSGD, the Singapore dollar-based stablecoin, significantly increased its real-world utility through integration with major fintech platforms like Grab, securing considerable influence in the Southeast Asian region. As of Q2 2024, Singapore's stablecoin payments surged to approximately $1 billion quarterly, with about 25% consisting of small transactions under $10,000, demonstrating high adoption in retail payments.

Cross-Border Payments and Specialized Transaction Sectors

As mentioned in the stablecoin adoption expansion scenario at the beginning of Chapter 2, KRW stablecoins could target specific niche markets in cross-border payments to build practical use cases. For example, considering the global demand for Korean Wave content and products, using KRW stablecoins for international payments related to K-pop, content, beauty products, and other Korean cultural goods could reduce transaction costs and serve as a natural connection point for market adoption.

4.3.1 Building a Fintech Ecosystem on top of Stableocoin

Source: Stablecoin Marketmap - Artemis

KRW stablecoins can serve as catalysts for strengthening the competitiveness of Korea's entire digital asset market, beyond merely functioning as a cryptocurrency trading medium. Stablecoins possess potential as new financial infrastructure due to blockchain's permissionless nature and programmability, enabling the derivation of core financial services such as payments, remittances, and cross-border transfers.

In the current absence of KRW stablecoins, Korea's financial ecosystem could face long-term competitive disadvantages. If Korea fails to respond appropriately during the restructuring of the global digital financial market, the domestic financial industry risks falling behind in global competition. Currently, companies entering digital financial areas like fintech, payments, and asset management, along with domestic users, have no choice but to rely on dollar-based infrastructure. Korean users seeking digital asset-related services inevitably have to transact through dollar stablecoins, which could naturally lead to a contraction of the won-based economy. If this trend continues and dollar stablecoins issued by foreign companies like Circle or Tether dominate Korea's digital asset ecosystem, there's a risk of weakening autonomy and independence in the domestic financial system.

Through KRW stablecoins, domestic developers and companies can build innovative financial services based on the Korean won, potentially strengthening the global competitiveness of Korea's fintech industry. Korea already has globally competitive fintech companies like Toss and Naver, whose global expansion could accelerate through integration with KRW stablecoins. Currently, fintech companies face significant barriers to overseas expansion due to regulatory compliance requirements and integration with local financial systems in each country, but if KRW stablecoins were integrated into global digital asset infrastructure, these barriers could be substantially lowered.

4.3.2 Addressing Domestic Market Inefficiencies

KRW stablecoins can contribute to resolving structural inefficiencies in Korea's cryptocurrency market. As analyzed in Chapter 3, the Korean cryptocurrency market exhibits various price distortion phenomena such as the Kimchi premium, listing price surges, and isolated price pumps, which cause unnecessary losses for domestic investors.

KRW stablecoins can be utilized to address these structural inefficiencies facing the domestic cryptocurrency market. By strengthening connectivity between domestic and international markets and improving accessibility for market participants, they can reduce price disparities and create a fairer, more efficient market environment, thereby enhancing investor protection.

Source: Stablecoin 101 - Chainanlysis

KRW stablecoins could particularly serve as a bridge to resolve the disconnect between global and domestic markets. If KRW stablecoins were listed on global cryptocurrency exchanges or on-chain markets, global investors could gain direct access to won-based assets. This would enable bidirectional capital flows, naturally helping to reduce price disparities between markets. Global investors would attempt arbitrage using KRW stablecoins to exploit price differences between domestic and global markets, which would naturally exert pressure to reduce the Kimchi premium.

There might be concerns that introducing KRW stablecoins could accelerate capital outflows from Korea, but in the long term, they could actually provide incentives for investors to remain in the domestic market by enhancing market competitiveness and transparency. One of the main causes of the current "departure from Korea" phenomenon is the structural inefficiency of the domestic market and limited investment opportunities. If these issues were resolved, it could help prevent unnecessary outflows of domestic capital.

4.3.3 Considerations for Implementing KRW Stablecoins

Several important considerations must be addressed as prerequisites for the successful introduction and sustainable development of KRW stablecoins.

Stability of the Korean Won's Value

When examining stablecoin adoption patterns globally, a clear trend emerges: in countries with instable currency, citizens overwhelmingly prefer USD-based stablecoins over those based on local currencies. Chapter 2 highlighted examples like Turkey, Argentina, and Nigeria, where persistent currency devaluation has driven users to pay significant premiums for dollar stablecoins.

For KRW stablecoins to succeed, the Korean won must maintain its value and stability. Any prolonged depreciation against the dollar would likely push Korean users toward USD stablecoins instead of won-based alternatives, potentially undermining adoption and utility of KRW stablecoins in the market.

Need for Broader Monitoring Systems

Stablecoins, by nature, derive value from blockchain and cryptocurrency's permissionless characteristic, which aims to lower barriers to entry in finance and currency. This inherently means they function as internet-based money that can move across borders and are difficult to control.

As users' economic activities expand with the introduction of KRW stablecoins, broader monitoring systems become necessary. The current Travel Rule may be effective in tracking fund movements between exchanges but has limitations in completely monitoring transfers to personal wallets or DeFi services.

Balancing Regulation with Innovation

For KRW stablecoins to serve as tools of innovation, regulatory clarity must be balanced with sufficient room for innovation. Overly strict regulations may inhibit innovation, while excessively loose regulations could threaten consumer protection and financial stability.

Building a successful stablecoin ecosystem requires close cooperation among various stakeholders, including government, financial institutions, fintech companies, cryptocurrency exchanges, and developer communities. Particularly in the initial implementation phase, a gradual approach to developing the regulatory framework through pilot projects or regulatory sandboxes could be effective.

Dive into 'Narratives' that will be important in the next year