This article is an excerpt from our report on stock tokenization. The full report can be found in “2026: The Year of Tokenized Stocks”

When the underlying technical primitives change, the range of businesses that can be built on top of them changes as well. Stablecoins were the first clear example of this shift. Major issuers such as Tether and Circle now have roughly $250B in stablecoins in circulation, and Tether has grown into a company that holds more U.S. Treasuries than most G20 countries.

The business scope of stablecoins has already moved beyond issuance. It now spans orchestration layers (i.e., BVNK, Stripe), onchain neobanks (i.e., Ether.Fi, UR), and stablecoin payment terminals (i.e., Ingenico-WalletConnect), with products that are already in active commercial use.

New technologies have consistently created new forms of economic activity, and new business opportunities have followed. The natural question, then, is what kinds of opportunities tokenized stocks unlock.

In this section, we map out the lifecycle of stock tokens, examine the current market landscape, and highlight the business opportunities that are beginning to emerge.

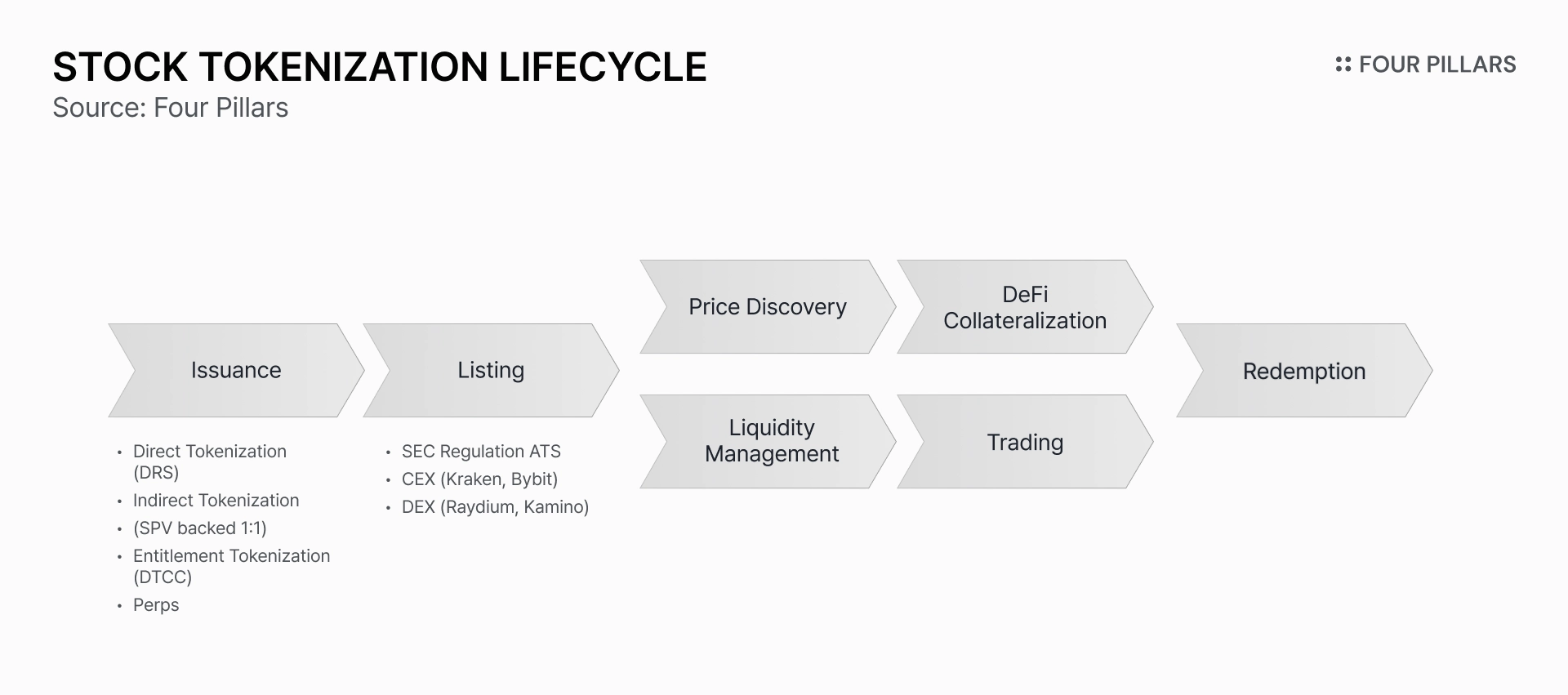

The tokenized stock market is still in its early stages, and most discussions today remain focused on tokenization models. Issuance, however, is only the starting point. In the sections below, we walk through the full lifecycle of stock tokens, from issuance to listing on trading venues, price discovery and liquidity formation, use as collateral, and eventual redemption.

To ground this analysis, we focus on three representative case studies: Securitize, Backed Finance, and Robinhood. We compare how each stage differs across these models and identify the key considerations at each step.

Securitize: Issues stock tokens directly through an SEC-registered transfer agent. Investors can participate only via approved wallets, and the tokens carry the same ownership rights, voting rights, and dividend rights as traditional shares.

Backed Finance: An SPV holds the underlying shares and issues bearer debt securities that reference the shares, packaged in token form.

Robinhood: When an investor purchases a stock token through the Robinhood app, Robinhood EU acquires the shares via a U.S. broker and issues the stock token as a derivative contract rather than as the underlying shares.

The first step in the lifecycle is the tokenization of the underlying shares. The key distinction lies in the legal ownership structure implied by each tokenization model. This structure determines where the token can trade and who is allowed to participate. We omit the detailed mechanisms here, as each model was covered in the previous section.

Securitize: Supports secondary trading of stock tokens on its own ATS. The ATS partners with OTC market makers that operate as SEC- and FINRA-registered broker-dealers, facilitating trades via both order book and RFQ mechanisms.

Backed Finance: xStocks trade freely on a 24/7 basis across CEXs such as Bybit and Kraken, as well as DEXs such as Jupiter and Raydium.

Robinhood: Robinhood stock tokens can be traded only within the Robinhood app and currently operate on a 24/5 schedule.

Trading venue access varies by tokenization model, and execution mechanics differ accordingly. On the Securitize ATS, order matching and settlement occur offchain under existing securities market rules. By contrast, xStocks face no venue restrictions. They trade via order books on CEXs and via non-custodial, onchain AMMs on DEXs. Robinhood acts as both counterparty and liquidity provider, internalizing user order flow within its platform.

Securitize: Under Reg NMS, Securitize’s ATS is required to provide fair execution prices. At the point of order matching, it references prices formed in traditional stock markets and verifies that executions fall within acceptable price ranges.

Backed Finance: xStocks integrate oracles that source reference prices for the underlying stocks onchain. Solana-based stock tokens primarily rely on Pyth Network, while EVM deployments combine multiple data sources, including Chainlink, to construct reference prices.

Robinhood: Stock token prices are determined within Robinhood’s internal ledger system and directly reference regular-session prices from U.S. stock markets such as Nasdaq and NYSE.

Price discovery provides a fair reference price that allows investors to trade efficiently. Compared to traditional stocks or crypto-native assets, price discovery for stock tokens involves more friction. While crypto assets default to 24/7 onchain trading, the underlying markets for stocks remain offchain.

The most challenging factor is regular trading hours. When markets are open, arbitrage keeps stock token prices closely aligned with their underlying shares. Premiums and discounts are quickly corrected using real-time price feeds, and token prices converge toward spot stock prices.

However, U.S. stock markets close for 16 hours on weekdays and remain shut over weekends. During these periods, no dominant reference price exists, and the price linkage of 24/7-traded stock tokens can weaken. Off-hours trading also introduces higher risks of price gaps, stale data, and execution instability.

As a result, stock tokens require safeguards to manage offchain and off-hours risk. These include market-status tracking, data freshness detection, circuit breakers, and event-awareness logic. In response, oracle providers have begun integrating contextual metadata into their data feeds alongside raw prices.

Traditional ATSs and market data vendors are also entering the stock token market by supplying after-hours price feeds to oracle networks. In addition, if NYSE’s planned 24/5 trading support is implemented, price gap risks may be reduced across most trading hours, excluding weekends.

Securitize: Secures liquidity through partnerships with OTC market makers on its ATS.

Backed Finance: xStocks connect to CEX order books supported by market makers while also sourcing onchain liquidity from external LPs via DEX pools.

Robinhood: Liquidity for Robinhood stock tokens is confined to the platform itself and depends on Robinhood’s internal order book and affiliated market makers.

Liquidity management ensures that stock tokens can absorb market trading activity smoothly. Beyond supporting large trades, sufficient liquidity depth is essential for stock tokens to function as collateral, preventing unnecessary liquidations driven by price impact and allowing borrowers to unwind positions when needed.

In practice, stock token trading typically occurs on thin liquidity. This leads to frequent price swings and excessive slippage for traders. For example, swapping $1M of TSLAx on Jupiter results in roughly 5% slippage, while NVDAx experiences slippage as high as 80%, rendering it effectively untradeable. Compared to traditional exchanges such as CME, where price impact is measured in single-digit basis points, these levels are difficult to accept.

Liquidity constraints largely stem from market-making challenges. In public markets, market makers supply liquidity by managing inventory under risk constraints and allocating capital efficiently. stock token markets present unfavorable conditions on several fronts.

High inventory costs: Market makers must pre-acquire stock tokens from issuers before supplying liquidity, incurring issuance and redemption fees as well as operational friction related to brokers and custodians.

Low inventory turnover: stock tokens cannot always be redeemed instantly beyond small sizes, and redemption limits are often set on daily or weekly schedules. This prevents rapid inventory reduction and forces market makers to unwind positions gradually, reducing capital efficiency and spread capture.

Limited hedging options: During off-hours, hedging instruments are unavailable. Market makers facilitating weekend trading bear direct price risk and respond by quoting wide spreads and small sizes. Investors who buy at a premium during weekends risk immediate losses when prices converge to spot stock levels at market open.

For these reasons, protocols, exchanges, and investors are forced to adopt conservative operating strategies in the stock token market. These include lower LTV ratios, wider safety margins, and avoiding off-hours trading altogether. Over the long term, stock token markets may seek to reduce dependence on traditional stock venues and evolve into base markets themselves. Achieving this, however, would require substantial changes across regulatory frameworks and financial infrastructure and remains a longer-term challenge.

Securitize: Through DS Protocol features such as KYC enforcement, transfer restrictions, and address whitelisting, Securitize is positioned to enable collateralization within a permissioned ecosystem composed of pre-approved participants and applications.

Backed Finance: xStocks are already used as collateral across permissionless DeFi protocols such as Kamino and Loopscale.

Robinhood: Robinhood stock tokens are restricted to trading within the platform and do not support collateralization services.

Tokenized bonds such as BUIDL and USTB have already established themselves as DeFi collateral assets that generate stable Treasury yields alongside additional lending income. stock tokens extend this model further by enabling 24/7 collateralized borrowing against stock exposure, allowing users to access stablecoins without selling their holdings.

At the same time, stock token collateralization differs materially from crypto-native assets. Regulatory compliance, price discovery, and off-hours risk interact in more complex ways. As with trading, collateralization splits along tokenization models into permissionless DeFi on one side and compliance-oriented DeFi, using tools such as ERC-3643, on the other. We examine specific cases in more detail in later sections.

Securitize: Allows tokens to be transferred to traditional brokerage accounts or redeemed through DTCC, where tokens are burned and equivalent shares are delivered to the investor’s existing stock account.

Backed Finance: xStocks can be redeemed through the Backed Finance platform into fiat currency or stablecoins, with settlement guaranteed within T+3 business days. Smaller redemptions can be processed immediately using working capital.

Robinhood: Robinhood stock tokens do not support redemption into underlying shares and can only be exited through secondary market sales.

The final stage of the lifecycle is redemption, where stock tokens are converted back into cash or underlying shares. The redemption mechanism distinguishes between tokens that represent derivative exposure and those directly linked to the underlying asset. It also determines whether token prices can converge toward underlying stock prices over the long term.

Breaking down the lifecycle of stock tokens makes it easier to see what kinds of new businesses can emerge. As stock tokens move through the market as a new asset class, new points of friction appear, and with them, new stakeholders that did not previously exist.

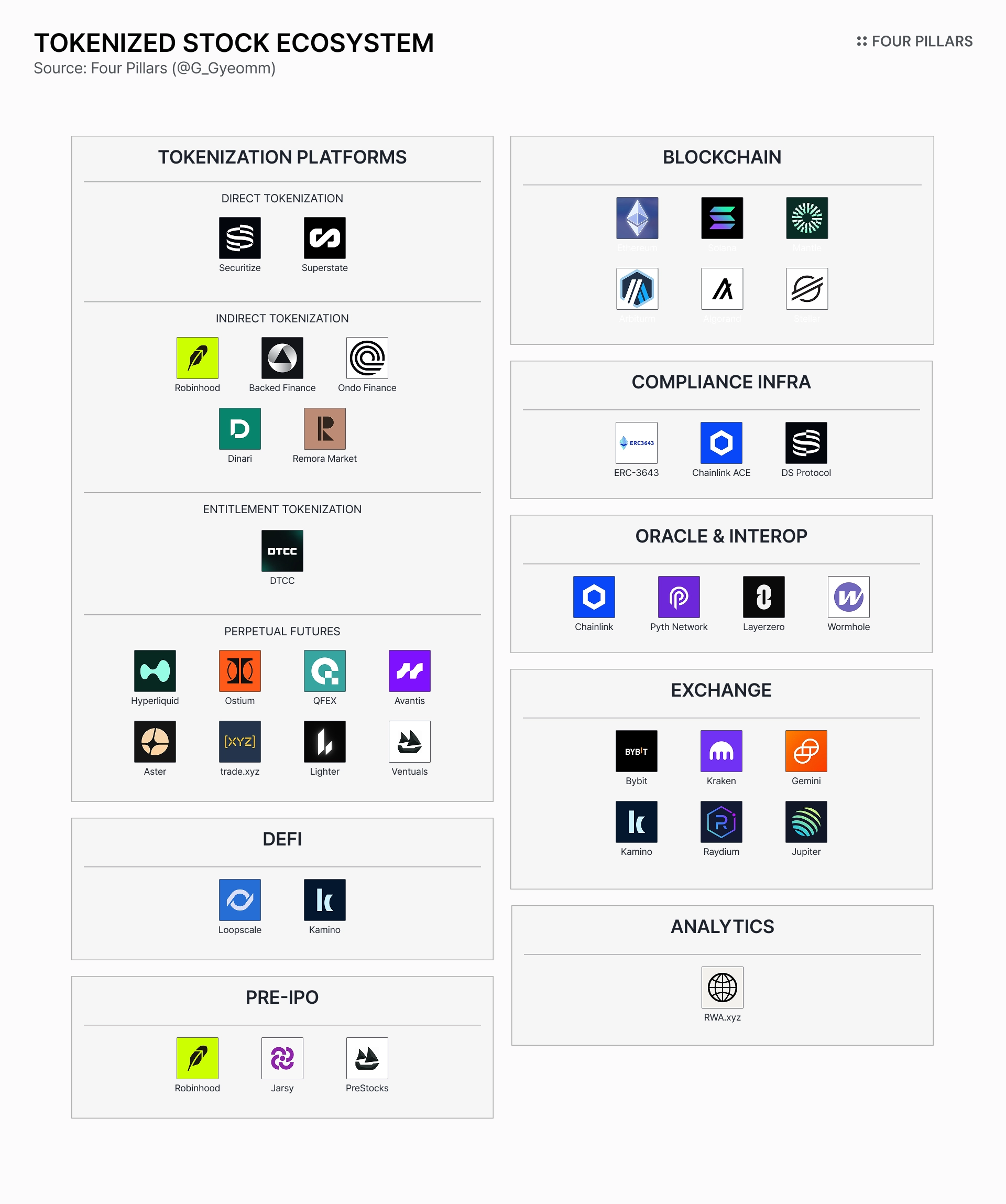

In the sections below, we examine the key sectors that make up the stock token market, focusing on blockchains, tokenization platforms, compliance infrastructure, oracles, and DeFi. For each, we outline the major players and the current state of the sector.

In stock tokenization, blockchains serve as the most fundamental infrastructure required to finalize ownership transfers. Historically, discussions around blockchain selection have focused on technical considerations such as transaction throughput, block finality, and developer tooling.

For stock tokens, however, regulatory compliance becomes the primary consideration. As a result, attention has shifted toward how blockchains can programmatically enforce regulatory requirements.

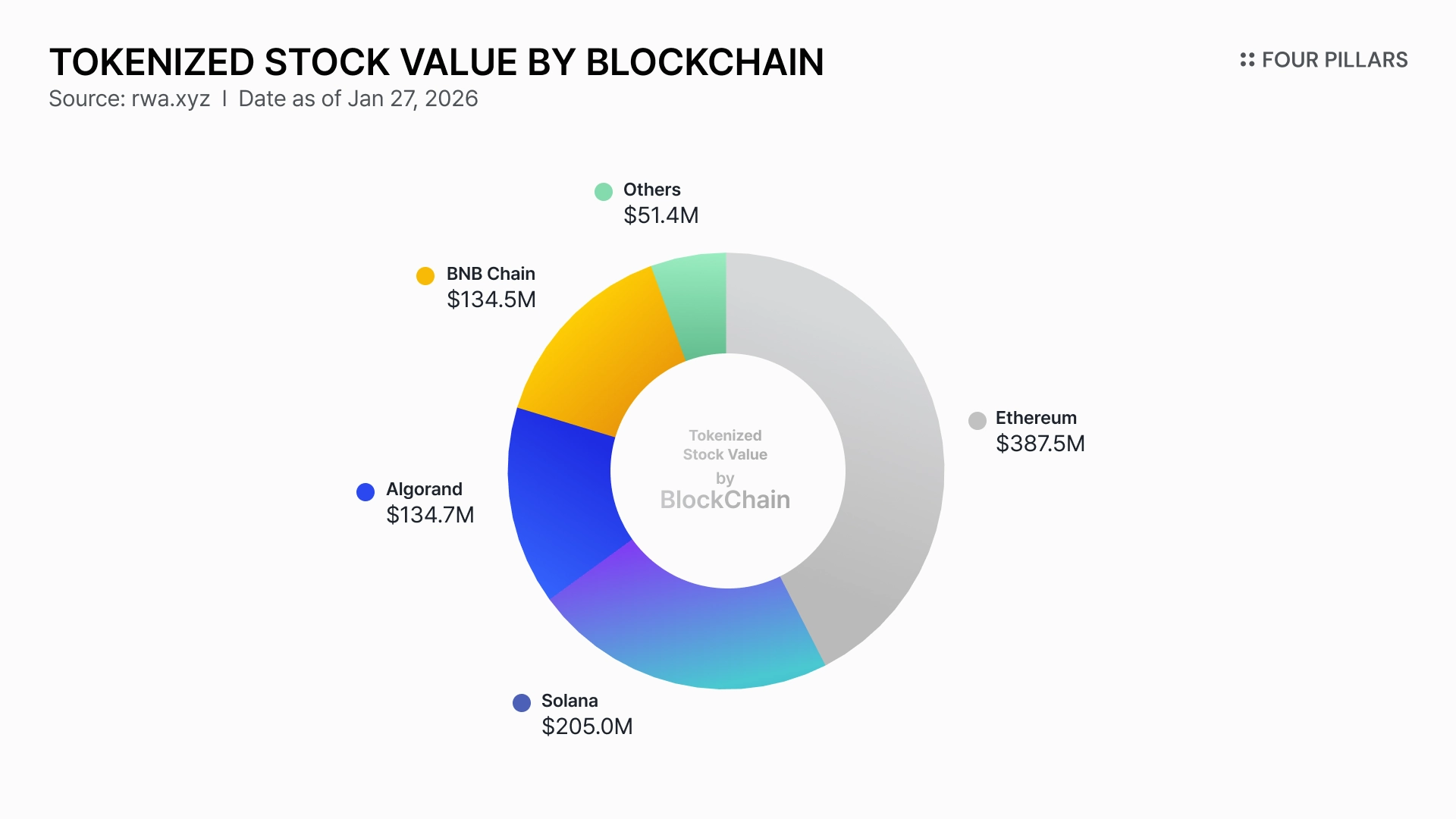

When market share is measured by the issuance volume of stock tokens, Ethereum remains dominant, followed by Solana, Algorand, and Stellar.

Ethereum is widely viewed as the blockchain with the lowest downtime risk and has built a strong institutional track record through multiple RWA issuances, including BlackRock’s BUIDL.

Solana, by contrast, has developed an stock token ecosystem centered on more flexible, trade-oriented products. Chains with strong retail trading activity have attracted stock tokens such as those issued by Backed Finance and Ondo, where liquidity and trading flexibility are prioritized.

Algorand and Stellar, which have seen relatively lower usage in other segments, stand out in stock tokenization for their regulatory compliance capabilities. Both chains natively support features such as transfer restrictions, permissioning, and asset recovery at the protocol level, without requiring additional middleware.

In practice, WisdomTree has issued five mutual funds totaling $20M, including stock portfolios, on Algorand. Securitize also selected Algorand as the issuance chain for approximately $150M of EXOD stock tokens.

Stellar

Stellar allows issuer, distributor, and holder roles to be separated at the chain level. After an asset is issued on Stellar, users must establish a trustline with the issuer in order to hold the asset, and the issuer can approve or deny that trustline. By combining this structure with features such as transfer restrictions, authorization requirements, revocability, and clawback, Stellar can implement the control surface required for stock tokens.

Algorand

Algorand embeds compliance features directly into the token itself. Its token standard, ASA (Algorand Standard Asset), allows issuers to programmatically define manager, freeze, clawback, and reserve addresses at asset creation. This enables issuers to approve or freeze transfers for specific accounts and reclaim assets in response to regulatory or legal requirements.

At the contract level, Algorand’s stateful smart contracts apply rules such as conditional transfers, holder eligibility checks, and jurisdiction-based policies. Together, these mechanisms enable enforcement of KYC status, accredited investor access, and transaction restrictions required for stock tokens.

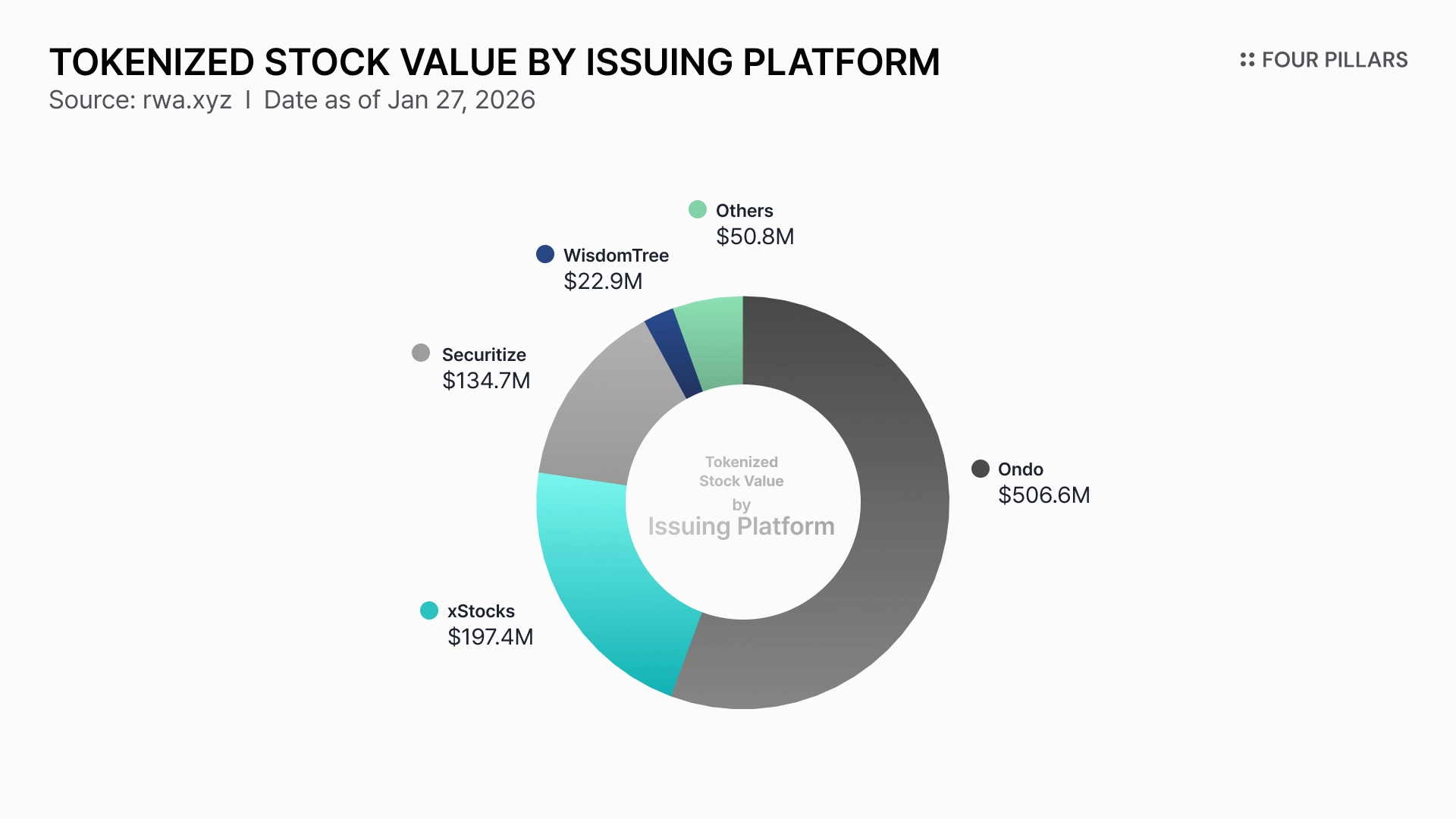

While the total issuance of tokenized Treasuries stands at roughly $9.3B, the cumulative issuance of stock tokens remains around $900M, a gap of more than tenfold.

The relationship reverses when viewed through the lens of traditional market size. The U.S. stock market is estimated at about $68T in market capitalization, while the outstanding stock of U.S. Treasuries is closer to $30T. On a global basis, stock markets are roughly twice the size of government bond markets. From this perspective, the addressable market for stock tokenization is significantly larger than that of tokenized Treasuries.

Against this backdrop, tokenization platforms emerge as the most important players to watch. Market share can be approximated using cumulative issuance, but the market remains too early for definitive comparisons. Securitize has issued only a single stock token to date, Exodus Movement Inc. (EXOD), and both Backed Finance and Ondo have been integrated with exchanges and DeFi for less than six months.

Looking ahead, market share is unlikely to be determined by issuance volume alone. Each platform adopts a different tokenization model with distinct legal ownership structures and compliance requirements. As a result, target investor bases and addressable markets vary widely.

Backed Finance

Backed Finance’s xStocks face no restrictions on trading venues. Rather than directly tokenizing shares in coordination with issuers, Backed purchases shares in public markets and issues stock tokens that reference those shares as underlying assets.

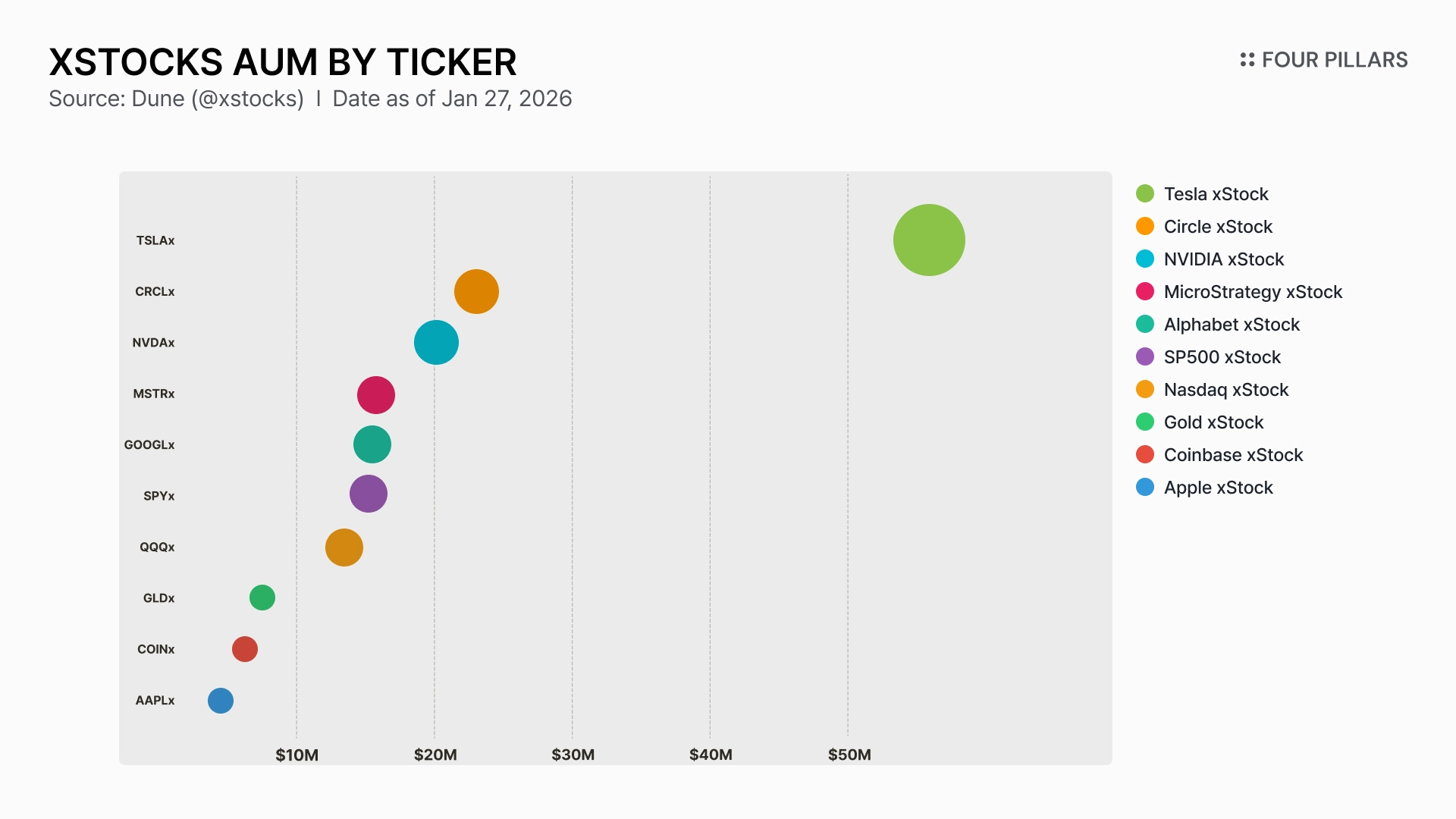

This structure allows Backed Finance to supply high-demand stocks to secondary markets with greater flexibility. In practice, xStocks issuance is concentrated in popular names such as TSLAx, CRCLx, and NVDAx.

In addition, an analysis of trading data from Backed Finance and Ondo between July and October 2025 shows that 78% of all trades were under $100. This suggests that indirect tokenization models have been effective at capturing retail demand for micro-sized stock trades.

Securitize

Direct tokenization models such as Securitize’s provide an end-to-end framework for issuance, trading, and redemption under U.S. securities law. This preserves legal ownership in full but comes at the cost of flexibility relative to indirect models, where any publicly traded stock can be tokenized and traded freely once shares are acquired.

Even so, regulatory alignment is likely to become increasingly decisive. Recent debate around the Clarity Act reflects growing efforts to clearly classify digital assets as securities, commodities, or other categories, and to define the applicable regulatory regime.

If enacted, stock tokens would almost certainly be classified as securities based on the nature of their underlying assets. This would subject stock token issuance to more rigorous scrutiny under existing securities laws.

In this context, regulatory compliance is unlikely to remain optional. For licensed issuers and for investors who prefer stable dividends and long-term holdings, tokenization platforms that meet regulatory requirements are likely to become the default choice.

In stock tokens, investor eligibility checks typically operate only at issuance or redemption, or within proprietary ATS environments. Once stock tokens trade onchain or are used as collateral, they enter an environment built around wallet-based, bearer-style transfers.

As a result, controlling whether participants are eligible investors and whether activity occurs within permitted jurisdictions becomes a central challenge. A range of compliance infrastructures has emerged to address this need.

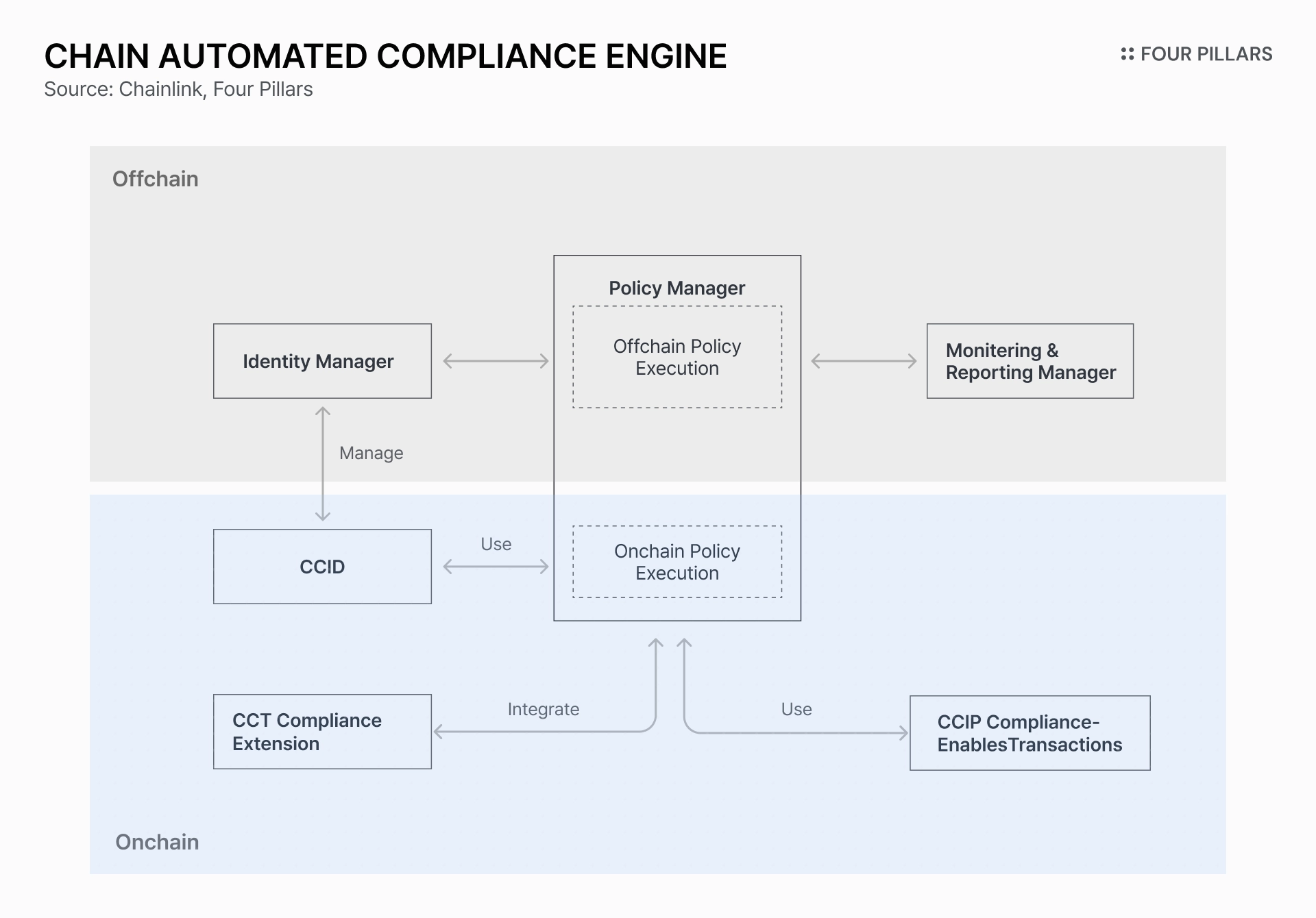

Chainlink Automated Compliance Engine (ACE)

Chainlink’s ACE is designed to enable tokenized assets to circulate onchain while meeting regulatory requirements. Its goal is to standardize verification of investor eligibility, jurisdictional constraints, and AML/KYC requirements, and to make those verifications interoperable across chains and applications.

One of ACE’s core components, CCID (Cross-Chain Identity), is a cross-chain identity framework that represents investor credentials. Offchain-verified information such as KYC, AML, and accreditation status is stored onchain as encrypted proofs rather than exposed data. Users can reuse credentials across multiple chains and DeFi applications, while service providers satisfy compliance requirements without accessing personal information.

Another component, the Cross-Chain Token Compliance Extension (CCT), is a modular layer that attaches compliance logic to token standards such as ERC-20 and ERC-3643. It connects tokens to CCID, policy managers, and CCIP, allowing issuers to embed compliance logic without redesigning token structures.

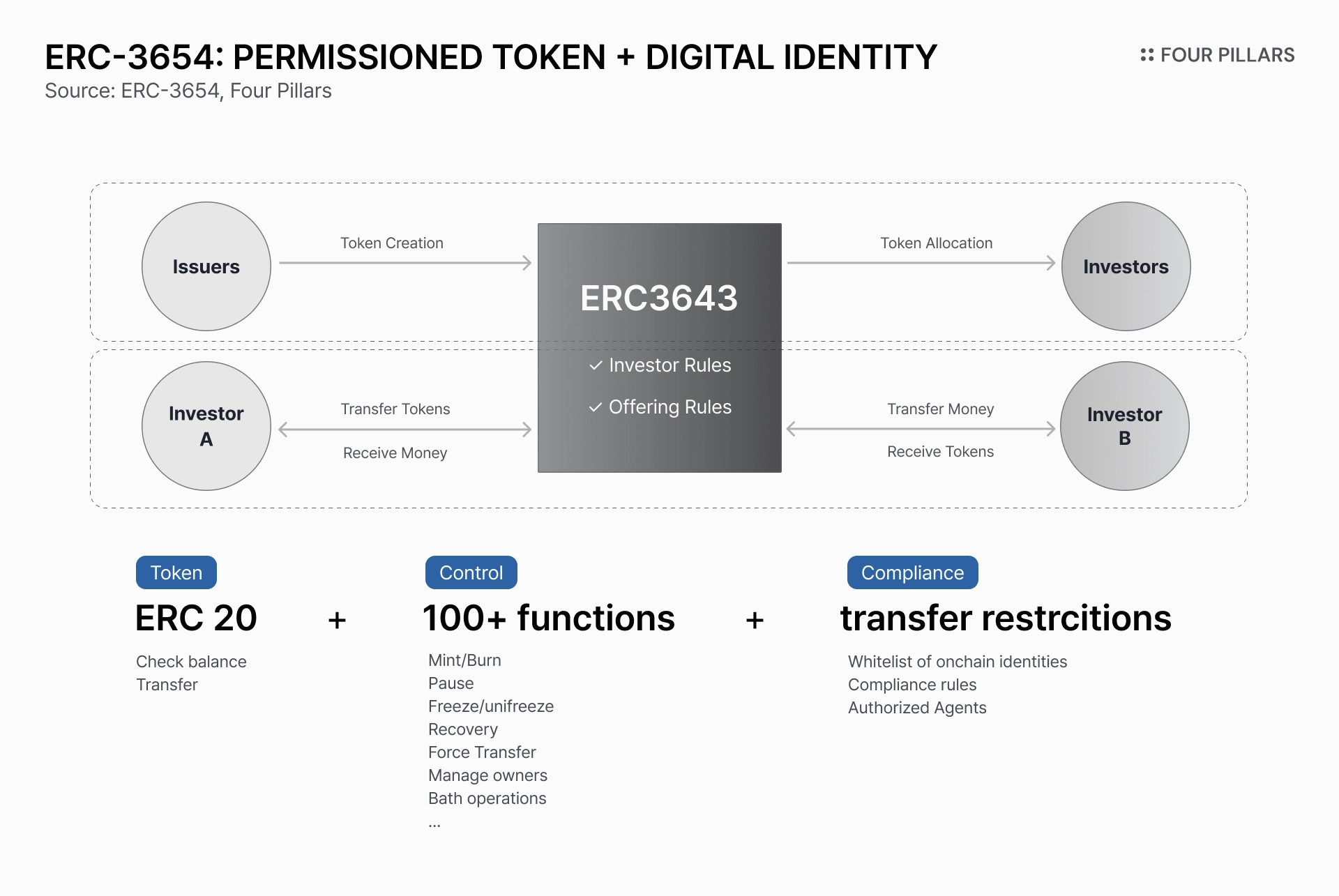

ERC-3643: T-REX Protocol (Permissioned Token Standard)

ERC-3643 is an Ethereum-based standard designed for RWA tokenization. It extends ERC-20 with permissioning features that control identity verification, KYC/AML status, investor eligibility, and jurisdictional access.

ERC-3643 tokens integrate with an onchain identity registry called ONCHAINED at issuance. The registry maps verified attributes such as KYC status and jurisdiction to wallet addresses without storing personal data. Only addresses that have passed offchain verification and are registered can receive or transfer ERC-3643 tokens.

All token actions, including issuance, transfer, and collateralization, query the ONCHAINED registry in real time. Issuers can flexibly define policies such as holding limits, transfer restrictions, country blocks, and lock-up periods.

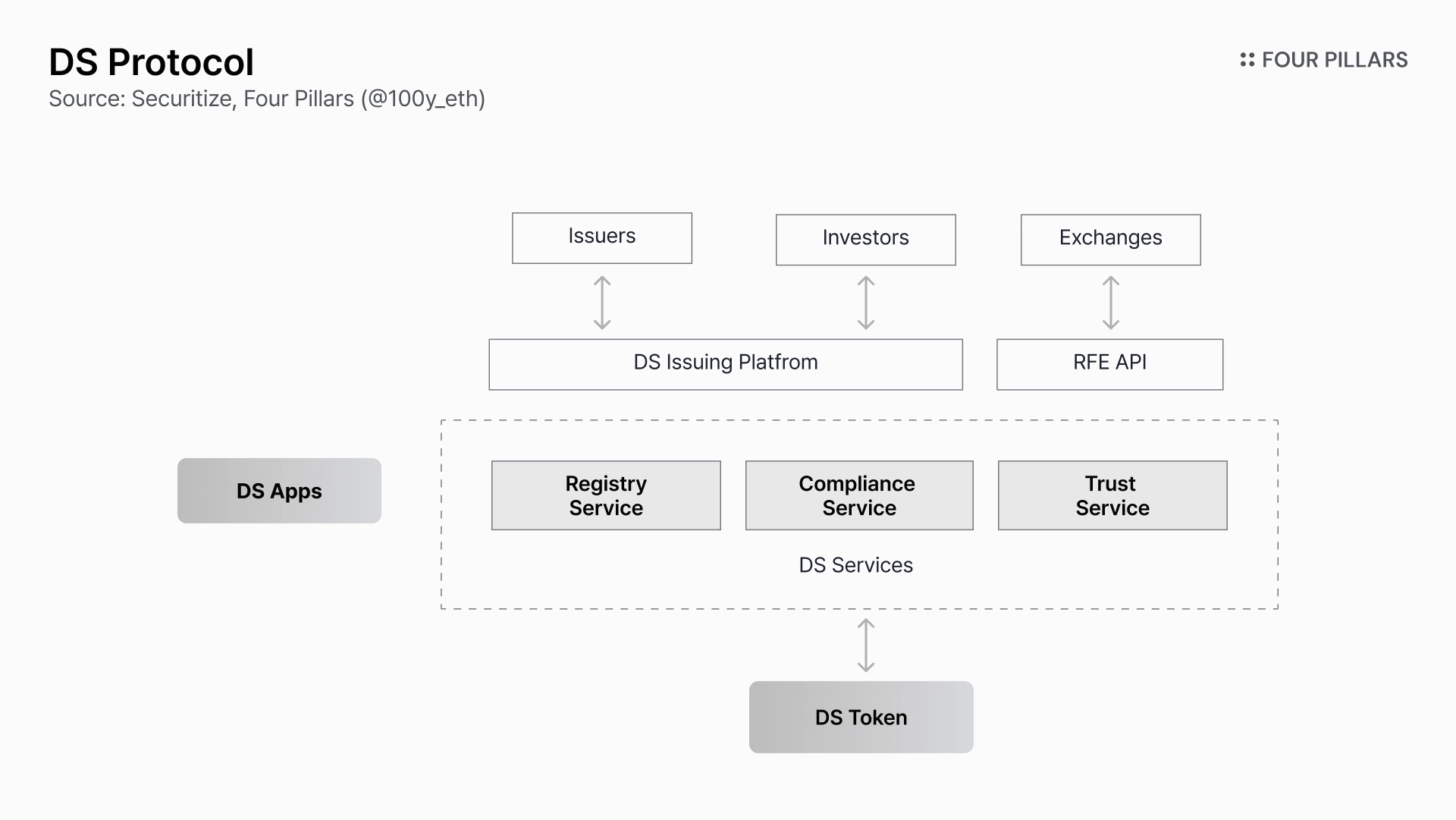

Securitize DS Protocol

Securitize’s DS Protocol is a proprietary compliance infrastructure already used to support the circulation of BlackRock’s BUIDL. Like Chainlink ACE and ERC-3643, it enables ERC-20 tokens to enforce compliance checks at the token level, but it is limited to Securitize-issued securities.

The DS Protocol verifies investor eligibility, transfer limits, and regulatory compliance before allowing any token transfer. It also supports vesting conditions and forced recovery, features required for securities.

Its registry manages the list of investors eligible to hold DS tokens and stores limited regulatory attributes such as nationality and accreditation status, without recording personally identifiable information. This approach preserves privacy while enabling compliance.

Nasdaq generated over $600M in U.S. market data revenue in 2023, while ICE, the owner of NYSE, generated $1.4B from market data and connectivity services in the same year. Market data has long been a core business in traditional stock markets.

In crypto, oracle providers initially focused on relaying offchain exchange prices onchain. With the rise of RWAs, they have expanded to deliver real-time NAV updates for Treasury funds and spot prices for precious metals.

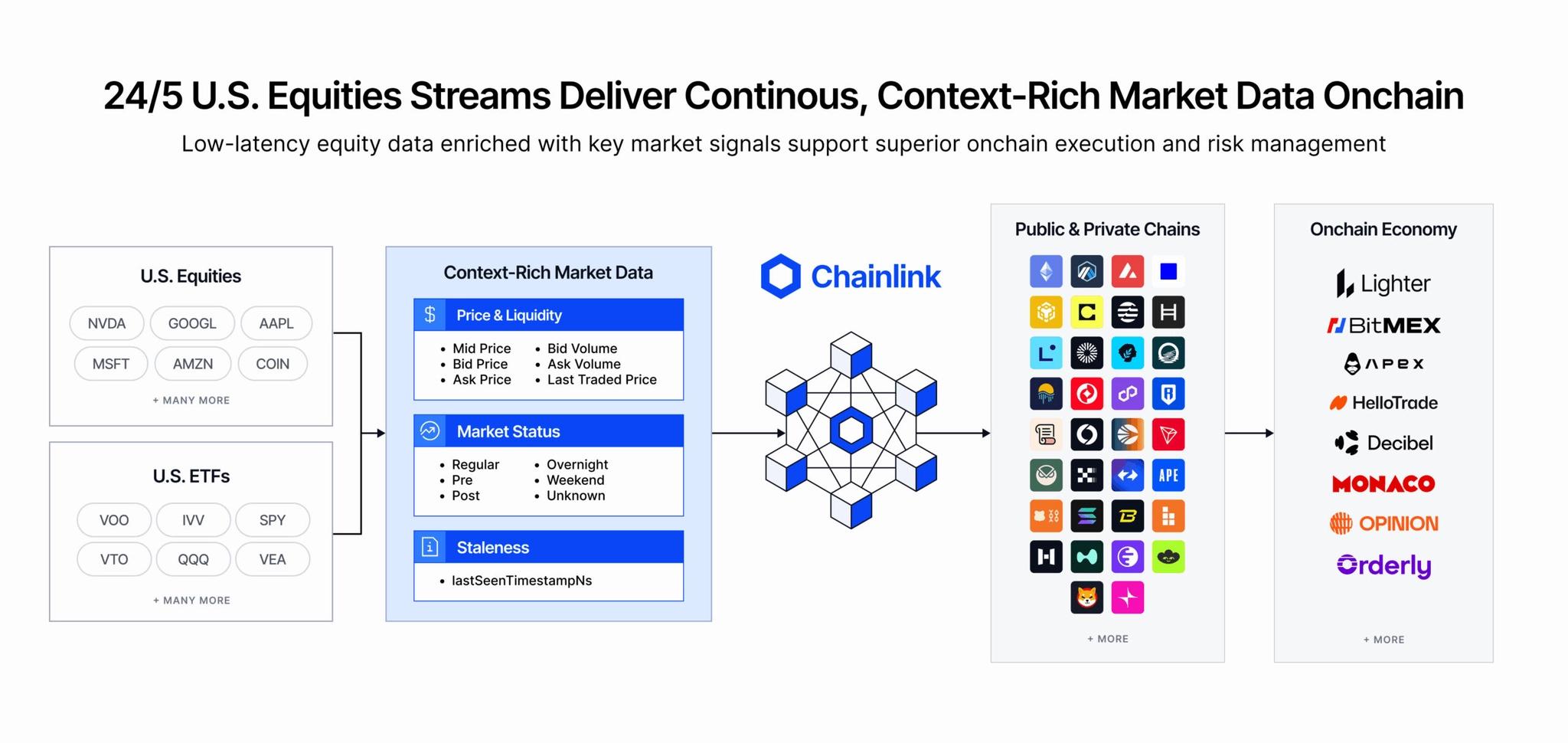

As stock tokenization scales, oracles are evolving further into data vendors that supply not only prices but also trading context such as market hours, liquidity conditions, and off-hours status.

Chainlink

Source: Chainlink

Chainlink’s Data Streams aggregate prices from at least three traditional financial data vendors. Offchain prices from consolidated tapes and vendors such as Bloomberg are validated and securely delivered onchain.

Beyond prices, Chainlink also provides contextual metadata required for stock token trading, including logic that allows smart contracts to detect whether markets are open, closed, or in low-confidence states.

Pyth Network

Pyth Network sources first-party market data directly from financial institutions and exchanges, minimizing latency by avoiding intermediaries. Banks, exchanges, and financial institutions including Revolut, AMINA Bank, Cboe Global Markets, and LMAX provide high-fidelity data directly to Pyth.

Pyth also integrates overnight U.S. stock trading data through its partnership with Blue Ocean ATS, an SEC-registered overnight exchange. This enables more reliable reference pricing for stock tokens outside regular trading hours.

Exchanges serve as the primary venues where stock tokens are traded. If tokenization platforms structure and issue stocks as a primary market, exchanges such as Bybit and Kraken function as the secondary markets, analogous to NYSE or Nasdaq.

Outside of regulated ATS environments, most stock token trading currently takes place on CEXs. For exchanges, stock tokens represent both a response to latent demand from crypto-native investors and a potential growth vector. For tokenization platforms, exchanges offer distribution to KYC-verified users and access to deep, market-maker-supported order books.

In this context, exchanges such as Bybit, Kraken, and Gemini have begun supporting stock token trading. In December 2025, Kraken acquired Backed Finance.

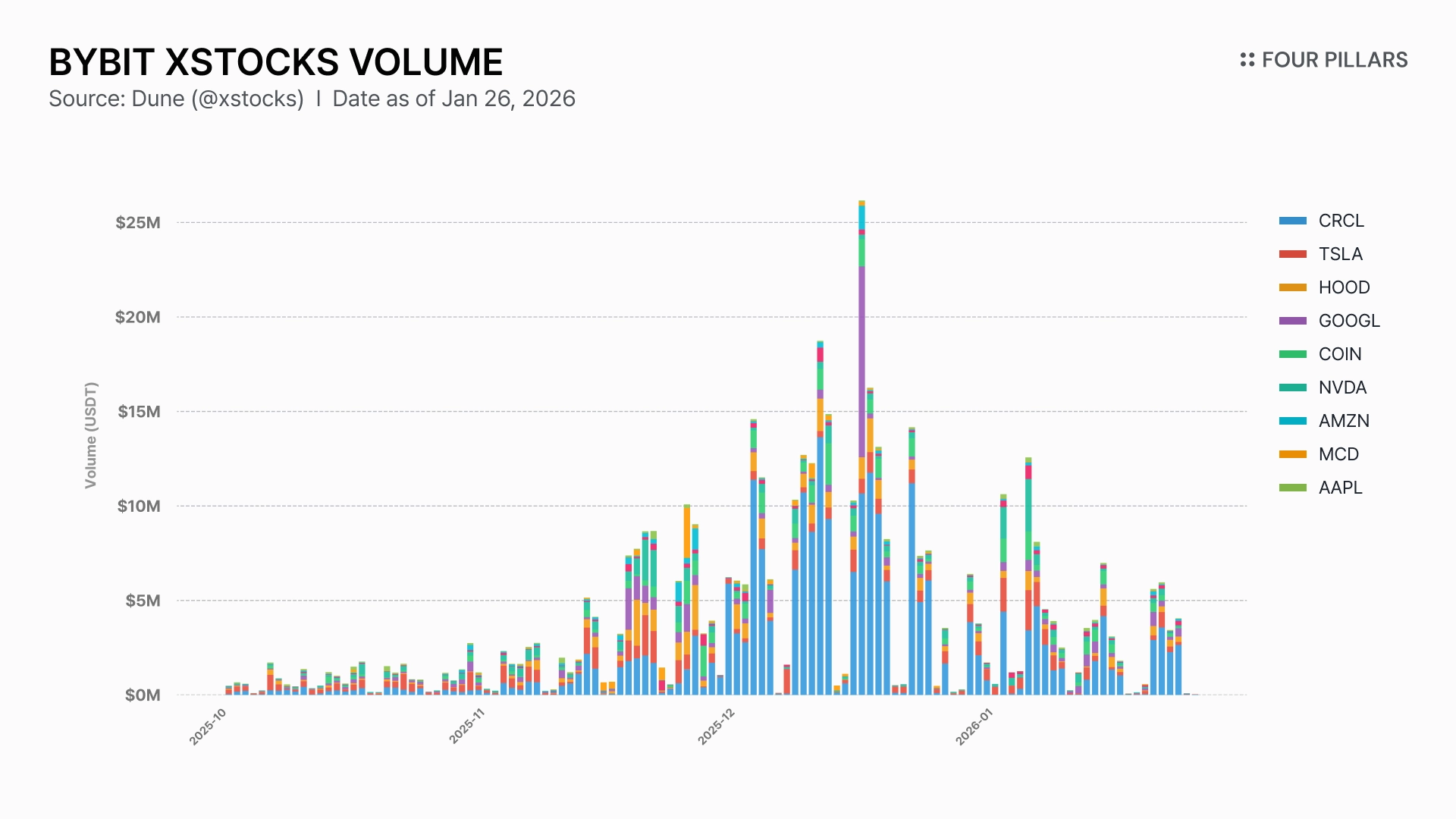

Bybit xStocks

Bybit supports 24/7 spot trading for ten xStocks assets, including COINx, NVDAx, and AAPLx. Only secondary trading is available on the platform, while redemptions are handled through Backed Finance for users who complete KYC/AML, based on NAV.

To date, xStocks on Bybit have recorded approximately $550M in cumulative trading volume, with steady activity outside weekend off-hours.

Onchain RWA-backed lending markets are growing rapidly. One driver has been the declining competitiveness of crypto-native yields. As returns on crypto assets fell, borrowing demand and LP yields declined in parallel.

With crypto money market APYs around 5% and U.S. Treasury yields near 4%, the incentive to participate in crypto-collateralized lending instead of government-backed returns has weakened. Against this backdrop, RWA-focused lending markets have gained traction. Aave Horizon, launched in August 2025, reached $600M in deposits and $200M in loans within six months.

stock tokens are emerging as the next RWA collateral class after Treasuries. Aside from off-hours liquidation risk, stock tokens combine relatively stable volatility with meaningful upside, making them attractive collateral assets.

Kamino: Isolated Pool Lending

Kamino is a Solana-based lending protocol that operates pool-based markets. In July 2025, Kamino launched dedicated xStocks lending pools, allowing users to borrow stablecoins against stock tokens such as SPYx, AAPLx, and TSLAx.

Each asset operates in an isolated pool with its own risk parameters and liquidity. Losses in one pool do not propagate to others. LTVs for xStocks are capped below 50%, compared with 70–80% LTVs commonly allowed for ETH collateral.

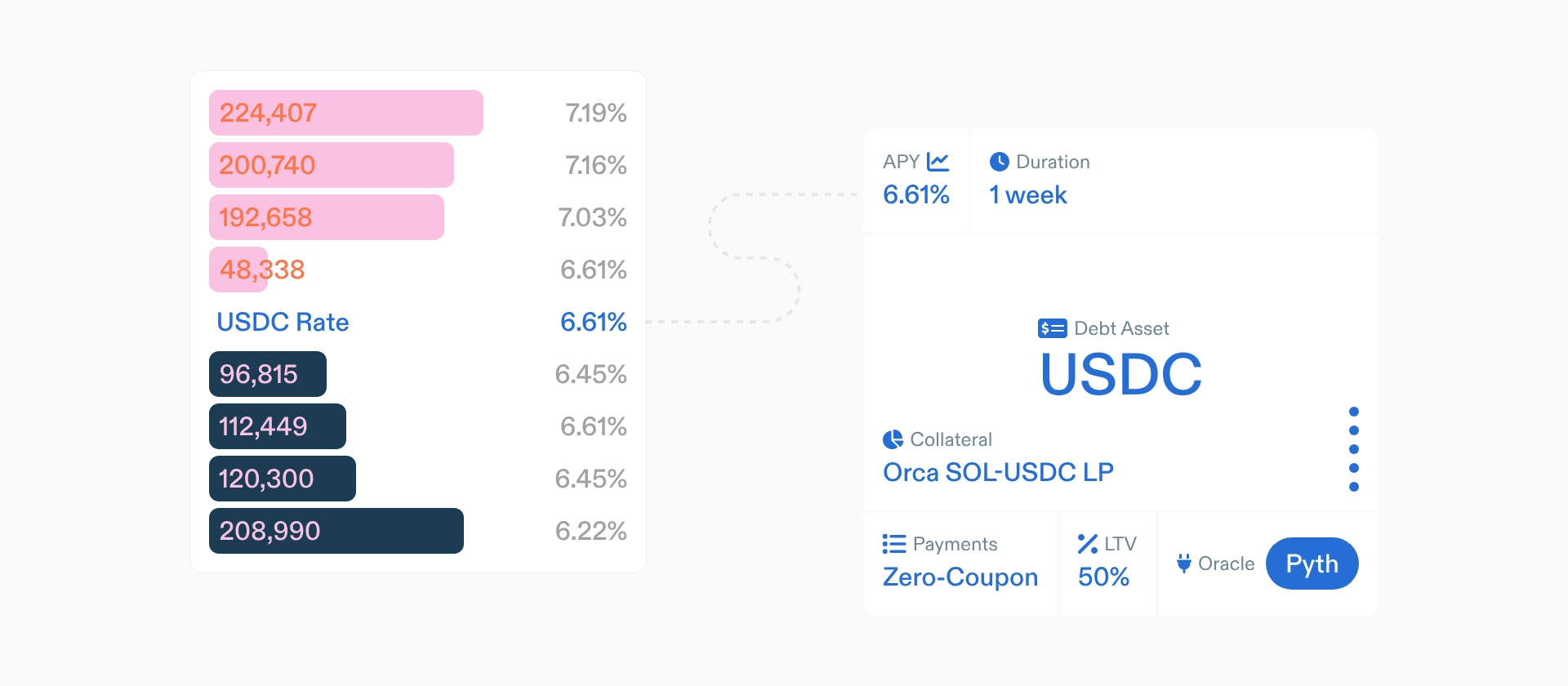

Loopscale: Order Book–Based Lending

Source: Loopscale

Loopscale is a Solana-based lending protocol that offers fixed-rate, fixed-maturity loans through an order book model.

Loan execution: Borrowers submit loan orders specifying size, maturity, rate, and collateral, or match existing orders. Upon execution, funds are borrowed at a fixed rate, and xStocks collateral is locked in escrow.

Maturity repayment: At maturity, borrowers repay principal and interest and withdraw their collateral. Terms are fixed at execution, making repayment amounts predictable.

Liquidation: Real-time price oracles monitor collateral value. If LTV exceeds liquidation thresholds, third parties can liquidate positions in exchange for collateral and liquidation incentives.

Order book lending offers advantages for stock tokens. Risk can be priced directly through negotiated LTVs and interest rates. Fixed terms reduce uncertainty during off-hours. Markets can form with minimal initial liquidity, as a single lender and borrower are sufficient to match.

stock token lending remains early. On Loopscale, looped positions backed by xStocks can currently be unwound only during U.S. market hours, a design choice intended to mitigate off-hours oracle and price-gap risk.

Pre-IPO Tokenization

Pre-IPO tokenization refers to issuing tokens that reference shares of private companies. Robinhood has gone beyond public stocks to launch tokens tied to private firms such as OpenAI and SpaceX, opening 24/7 access for global investors to assets previously limited to private markets.

These tokens do not grant legal ownership of the underlying shares and are not redeemable. In practice, most pre-IPO stock tokens rely on indirect tokenization, where an SPV holds the shares and issues corresponding tokens.

OpenAI has explicitly stated that it “was not involved in or approved any stock transfer” related to Robinhood’s tokenized offering, highlighting the unresolved ownership and consent issues that remain in this model.

Onchain IPO: Superstate DIP (Direct Issuance Program)

Superstate’s DIP is a compliant platform that allows SEC-registered public companies to issue new shares directly onchain.

Companies set issuance terms based on real-time market prices, and investors purchase shares directly from the issuer. Secondary trading is limited to whitelisted wallets.

Superstate’s onchain transfer agent system, Opening Bell, updates shareholder registries at issuance. Issued tokens are treated as official shares with CUSIP identifiers and carry the same economic and voting rights as common stock.

Unlike traditional stock offerings or ATM programs, onchain IPOs reduce issuance costs by removing underwriters and intermediaries. They also provide global investors with 24/7 access, positioning them as a potential new capital formation channel.

Although they fall under the same broad category of tokenization, fiat, bonds, and stocks differ fundamentally. Fiat and bonds are usage-driven assets centered on payments, collateral, and yield. stocks, by contrast, are primarily held and traded. As a result, stablecoins and bond tokens support broader value chains and business opportunities, while stock tokenization offers a narrower set of new activities.

Even so, the potential impact of stock tokenization should not be understated. Traditional stock markets are structurally inefficient, and tokenization offers a powerful tool to address those inefficiencies. It also has the potential to unlock stock-based financial activity that has historically been inaccessible to retail investors.

This transition will not be trivial. Liquidity management, price discovery, and regulatory alignment remain open challenges. But if these issues can be navigated, stock tokenization could move beyond experimentation and into a sustained phase of adoption.

Dive into 'Narratives' that will be important in the next year