Institutional adoption of crypto is accelerating globally, and institutional ETH staking is emerging as one of the most prominent services among a wide range of crypto offerings for institutions. This is driven by factors such as regulatory clarity, simplicity, and stability.

However, unlike retail participants, institutions face multiple barriers when staking large amounts of ETH. These include lack of support for DPoS, slashing risk, technical complexity, accounting and reporting requirements, compliance, security concerns, and liquidity lockups.

Existing staking providers offer institutional ETH staking through methods such as custodial staking and white labeling. Recently, following Ethereum’s Pectra upgrade, non-custodial ETH staking has also become available to institutions. One solution to watch in particular is Lido’s stVault, which has been gaining significant attention. It provides a modular structure that allows institutions to designate their own operators and configure customized vaults, effectively addressing many of the key hurdles in institutional ETH staking.

What about the institutional ETH staking market in Korea? While Korea has developed a very large retail-driven crypto market, its corporate and institutional crypto sector remains relatively underdeveloped due to conservative and slow-moving regulations. Nevertheless, interest in crypto among corporations and institutions has recently been very strong. With expectations that corporate crypto investment as well as crypto ETFs, will be permitted this year, Korea represents a highly promising market for institutional ETH staking.

The crypto market, once dominated by retail investors, has now undeniably shifted toward an institution-led market. Asset managers such as BlackRock are launching crypto ETFs and tokenizing real-world assets. Platforms like Robinhood, DTCC, and Nasdaq are tokenizing equities, while payment companies such as Stripe and Visa are actively integrating crypto into their payment flows.

In other words, the market is maturing, and institutional investors are embracing crypto as a new asset class while actively entering related businesses and investments. But why are institutions choosing crypto among so many asset classes and technologies? There are two primary reasons.

1.1.1 From a Portfolio Perspective

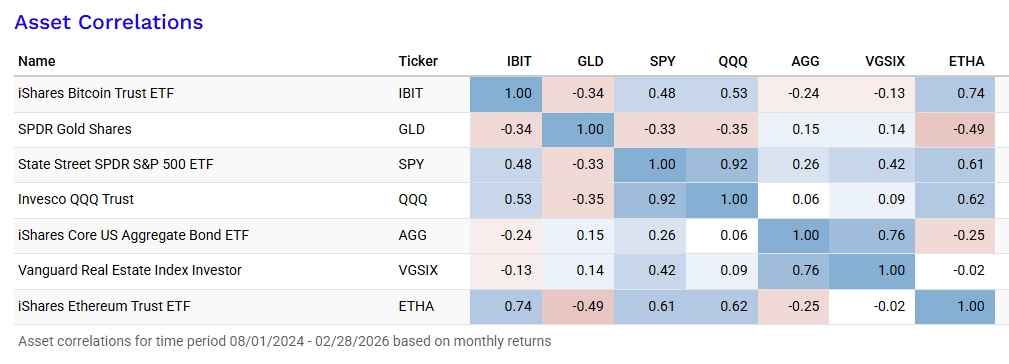

Source: Portfolio Visualizer

The first reason is the attractiveness of crypto as an asset from a portfolio standpoint. Regardless of the long-term outlook of the crypto industry, crypto has now grown into a sufficiently large asset class. Most importantly, crypto assets exhibit a fundamentally different risk-return profile compared to traditional assets.

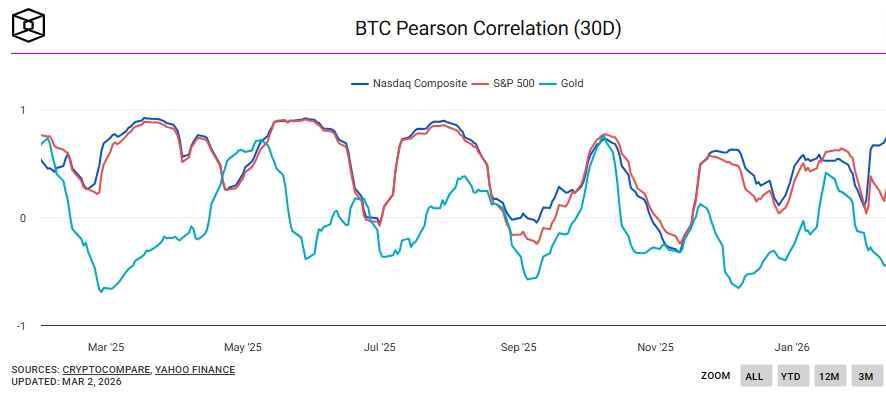

Source: The Block

For example, while Bitcoin is often referred to as digital gold, recent correlation data shows that Bitcoin has the strongest negative correlation with gold. At the same time, it does not consistently show high correlation with equities. Depending on the period, its correlation with the stock market can be high, negligible, or even negative.

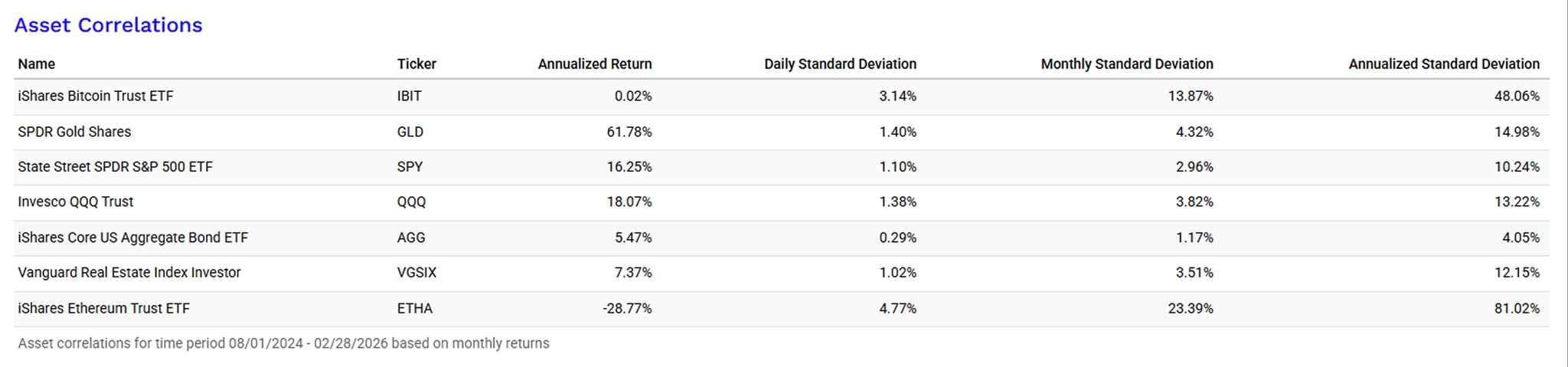

Source: Portfolio Visualizer

From a volatility perspective, crypto can also be attractive to institutional investors. While high volatility may be a disadvantage for simple buy-and-hold strategies, it can be a compelling feature for institutions such as hedge funds that actively seek volatility.

These distinctive characteristics, compared to other asset classes, make crypto an attractive addition to institutional portfolios.

1.1.2 From an Industry Perspective

The second reason is the mass adoption of the blockchain industry. The reason financial services are easy to use today is due to improvements in the frontend, while the backend still relies on outdated infrastructure built decades ago.

This outdated financial infrastructure creates trust costs such as asset fragmentation, slow settlement times, and high fees. Blockchain technology removes these trust costs through consensus protocols and incentive systems. It has the potential to be adopted across various financial infrastructures, including remittances, payments and settlement, and trading, improving not only the frontend but also fundamentally transforming the financial backend.

In practice, blockchain technology is already being actively adopted across multiple sectors, starting with finance. Examples include the GENIUS Act, BlackRock’s BUIDL, Robinhood’s stock tokens, the rapid adoption of stablecoins in Latin America, crypto ETFs, and DTCC’s move toward 24/7 trading. These developments illustrate how blockchain is improving outdated infrastructure and gaining real-world adoption.

Institutions are entering the crypto space. What are their needs? Institutions have diverse needs across each stage of interacting with crypto, from acquisition to holding to utilization. For example, they require services such as OTC and brokerage for purchasing, wallet solutions, custody, and treasury management for holding, and staking and lending for utilization. To meet these demands, many companies in today’s crypto market are offering a wide range of institutional crypto services.

Among the various institutional crypto services, this article focuses on institutional staking.

As more institutions adopt crypto, the importance of the staking industry will inevitably increase. Once institutions enter the crypto space, there will always be situations where large amounts of crypto are held, whether directly by the institutions themselves or on behalf of their clients and retail customers.

However, simply holding crypto through custody leads to high opportunity costs. In the case of BTC, native utilization is relatively limited, so the opportunity cost is not as significant. But for most PoS assets such as ETH and SOL, institutions can participate in a wide range of activities including staking, lending, and liquidity provision. As a result, institutions naturally have a strong incentive to generate yield rather than just passively holding crypto.

From this perspective, staking serves as the first step for institutions to generate yield from their crypto holdings.

Security: Staking is one of the safest ways to utilize crypto assets. For example, CeFi requires trusting a third-party institution, while DeFi introduces smart contract risk. In contrast, staking is a core function embedded within PoS blockchains themselves, making it one of the most secure ways for institutions to generate returns on their crypto assets.

Simplicity: Staking is straightforward. There is no need to design complex fund strategies, evaluate smart contract risks, or actively manage positions. Returns are relatively stable compared to other strategies, making them highly predictable. This predictability is especially important for institutions managing large amounts of capital.

Benchmark: Because staking is both the simplest and safest yield-generating activity, it is often treated as a benchmark among various investment strategies. In some cases, activities such as lending or liquidity provision may even offer lower yields than staking. When considering the risk-return profile, staking naturally serves as a baseline for comparison.

Regulatory Clarity: In the past, staking faced regulatory uncertainty regarding whether it could be considered a security. However, in 2025, the SEC’s Division of Corporation Finance clarified in an official statement that staking, including liquid staking, does not constitute the offer or sale of securities under federal securities laws. In March 2026, the SEC further reinforced this position by issuing new guidance explicitly stating that protocol staking is not a security. This regulatory clarity provides a strong foundation for institutions to engage more actively in staking.

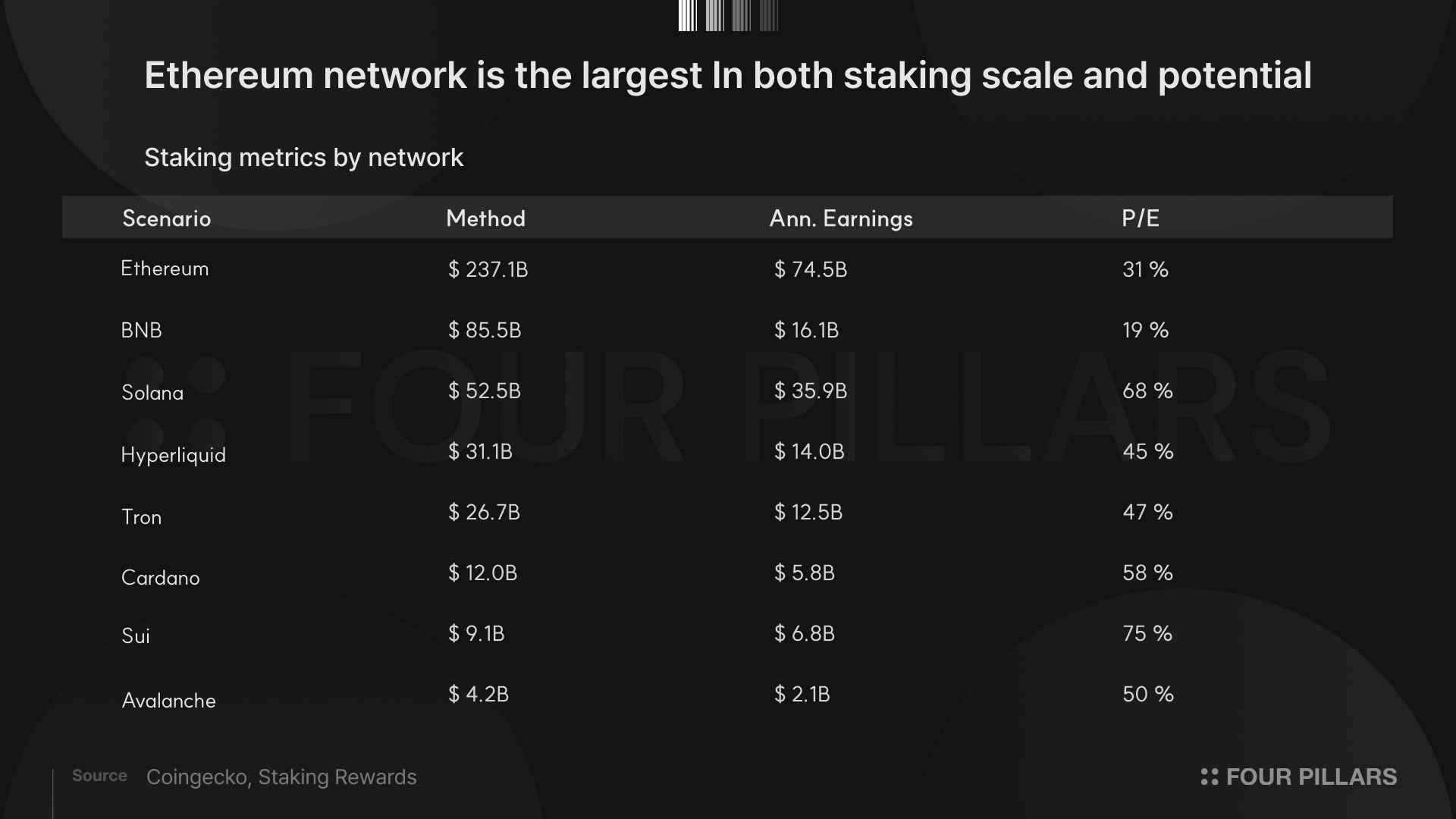

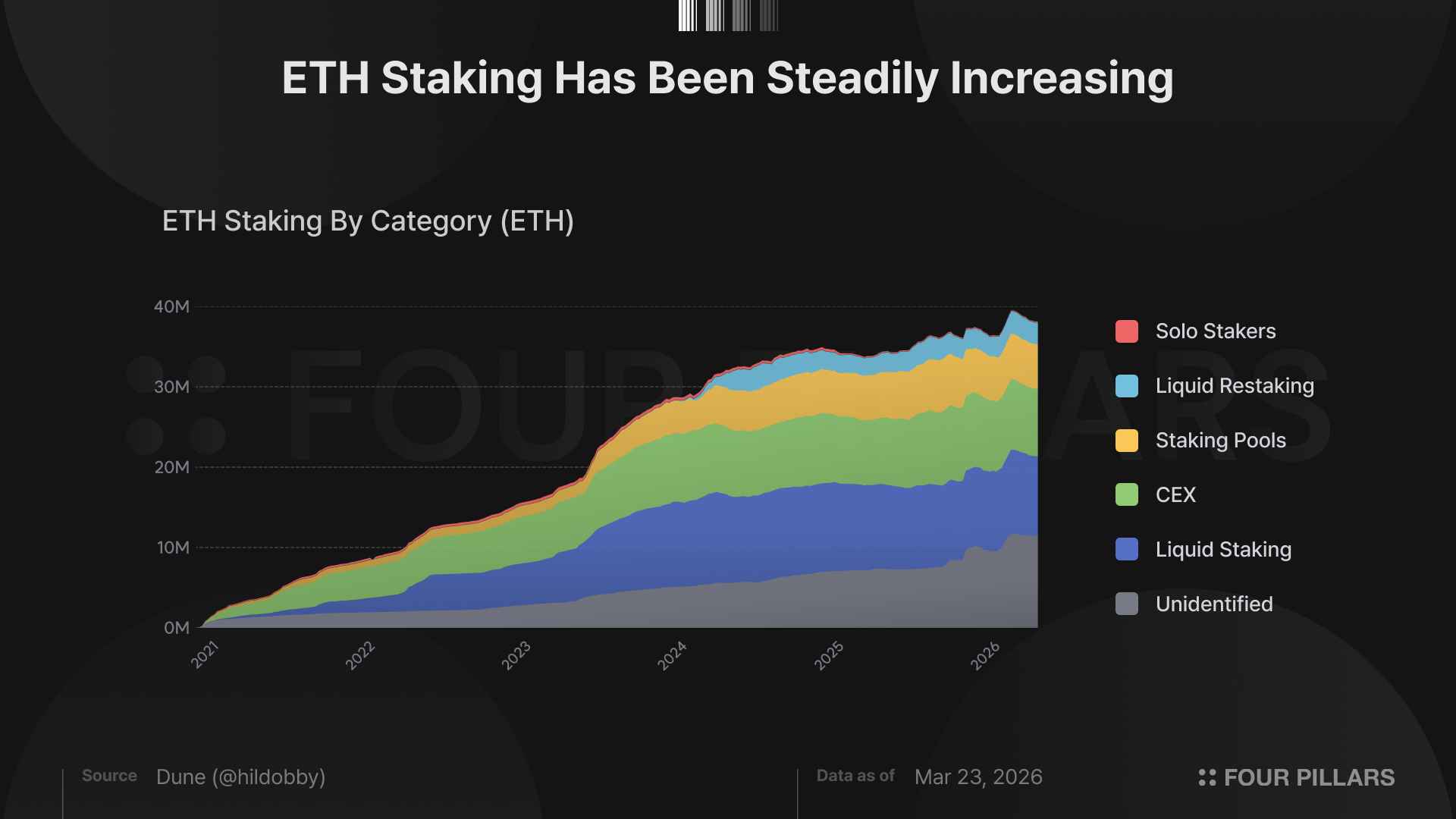

Among all assets in the institutional staking sector, Ethereum (ETH) stands out as the most notable. Ethereum has the largest market capitalization among PoS blockchains and a vast on-chain ecosystem. Although only about 31% of total ETH supply is currently staked, the total staked value is approximately $75B, making it the largest staking market. This is roughly twice the size of Solana, which ranks second.

Despite ETH’s price volatility, the total amount of staked ETH continues to trend upward over time. Considering that ETH is the second most institutionally adopted crypto asset after BTC, the ETH staking market is expected to grow explosively with increasing institutional participation.

So how large is the institutional ETH staking market? Institutions can stake ETH in multiple ways, including running solo validators, using liquid staking protocols, or delegating to staking providers. Because these activities cannot be clearly distinguished on-chain, it is impossible to precisely measure the size of the institutional ETH staking market.

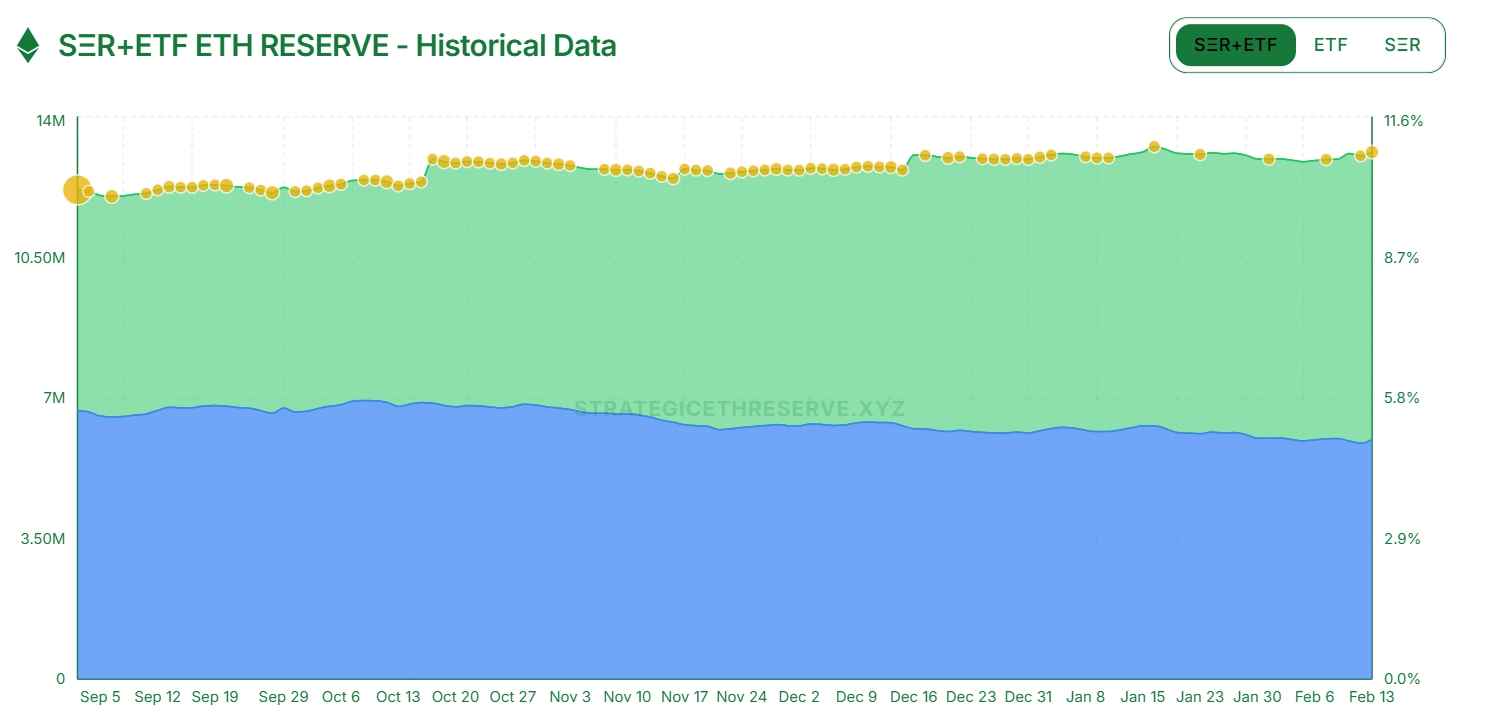

However, we can get a rough sense of its potential size by looking at the amount of ETH held by DAT companies and ETF products.

Source: Strategic ETH Reserve

The total ETH held by ETH-focused DAT companies and ETH ETFs is approximately $13B, representing about 11% of the total ETH supply.

BitMine, the largest ETH-holding DAT company, holds about 3.7% of the total ETH supply and actively stakes a significant portion of it. According to its disclosures, BitMine stakes approximately 67% of its ETH holdings and has even built its own staking infrastructure called MAVAN (The Made in America Validator Network).

In addition to BitMine, SharpLink Gaming, the second-largest ETH DAT company, stakes nearly 100% of its ETH holdings. The third-largest, The Ether Machine, is also preparing to stake its ETH and participate in DeFi.

For ETH DAT companies that acquire and hold large amounts of ETH, simply holding the asset creates significant opportunity costs. As a result, most of these companies are either actively participating in staking or planning to do so. The presence of such players makes institutional staking an essential service.

Soruce: The Block

The large size of the ETH ETF market is also expected to act as a powerful catalyst for the growth of institutional ETH staking. While most ETH ETFs do not yet allow staking, many of them manage substantial amounts of ETH, including ETHA with $6.9B and ETHE with $1.8B in assets.

Recently, BlackRock launched an ETH staking ETF, the iShares Staked Ethereum Trust (ETHB). Despite being live for only about a week, the fund has already surpassed $250M in assets. Notably, VanEck has applied for an ETF that stakes ETH using Lido, the leading liquid staking protocol, and is currently awaiting approval.

In Europe, staking-enabled ETH ETPs such as 21Shares Ethereum Staking ETP, WisdomTree Physical Lido Staked Ether ETP, and Bitwise Ethereum Staking ETP are already available. In Hong Kong, products such as the MicroBit Ethereum Spot ETF and Bosera Ethereum Spot ETF are also on the market.

With the SEC recently clarifying that staking is not a security and with the launch of BlackRock’s ETH staking ETF, more ETH is expected to flow into staking-enabled ETFs. As a result, the institutional ETH staking market is projected to experience rapid and substantial growth.

Despite growing interest in ETH staking, staking large amounts of ETH at an institutional level remains highly complex.

2.4.1 Ethereum PoS Characteristics and Custody Issues

Ethereum is a pure Proof of Stake blockchain rather than a Delegated Proof of Stake system. Unlike DPoS, where ownership remains with the user while staking power is delegated at the protocol level, Ethereum assumes that the staker directly operates validator nodes.

As a result, institutions typically either run validators themselves for the ETH they hold or delegate to staking providers with custody licenses, such as exchanges. While it is possible for non-custodial providers without custody licenses to offer staking services, the process is inherently more complex compared to DPoS networks.

2.4.2 Penalty Risks

Ethereum validators are probabilistically assigned roles in each slot based on their staked assets. Successfully performing these roles yields rewards, while failure results in penalties that reduce the staked assets. In cases of violations considered harmful to the network, such as attacks, staked ETH can be slashed significantly.

If a node experiences downtime, the validator fails to perform its assigned duties during that period. This leads not only to missed rewards but also to penalties on the staked assets. Notably, most other blockchains outside Ethereum impose minimal or no penalties for downtime, which makes high availability especially critical in Ethereum infrastructure.

Double signing and surround voting are common causes of slashing. The issue is that double signing can occur due to simple operator mistakes. For institutions, slashing is an unacceptable event. Preventing it requires careful architectural design as well as economic safeguards such as insurance.

2.4.3 Infrastructure Complexity

Unlike many other blockchains that are relatively standardized around a single client, Ethereum’s infrastructure is modular. This results in significant variation in how different operators run their systems. Factors such as whether Distributed Validator Technology is used, which execution and consensus client combinations are deployed, and what mechanisms are in place to prevent slashing all need to be evaluated.

Ethereum node operators must manage combinations of execution clients, consensus clients, and validator clients. To achieve high availability, they may adopt external DVT protocols such as SSV or Obol, or implement architectures like DVT-Lite. This requires the capability to maintain client diversity across modules while ensuring stable operations.

Key management is also more complex. Unlike DPoS blockchains where a single validator can accept unlimited delegation, Ethereum requires 32 to 2,048 ETH per validator key. With frequent deposits and withdrawals and dynamically changing validator balances, institutions must carefully manage validator keys and ensure secure signing processes, often using external signers. For institutions operating thousands or tens of thousands of validators, key management complexity increases exponentially.

From an operational standpoint, continuous 24/7 monitoring is essential, along with the ability to detect and respond to incidents in real time. Structured incident response processes must be in place. Additionally, to avoid single points of failure, infrastructure must be geographically distributed and diversified across providers.

2.4.4 Security and Compliance

When using custodial staking services, institutions must assess the security and risks associated with the service provider.

In contrast, when running their own nodes or using non-custodial staking providers, managing the withdrawal credential key becomes the most critical factor. Ethereum separates the validator key used for node operations from the withdrawal key that represents ownership of the staked assets.

Typically, the operator holds the validator key, while the client retains the withdrawal key. As long as the withdrawal key is securely managed, even if the operator’s infrastructure is compromised and validator keys are stolen, the staked assets cannot be withdrawn. However, an attacker could still use stolen validator keys to maliciously trigger slashing events and reduce the staked balance.

Therefore, even non-custodial staking providers must maintain robust security standards, including certifications such as SOC 2 and ISO 27001, and operate structured security management processes. The availability and coverage of insurance to protect against slashing losses are also key considerations for institutions.

From a compliance perspective, KYC and anti-money laundering procedures for counterparties are essential. Institutions must also maintain systems capable of supporting regular reporting and audits. Since staking regulations vary across jurisdictions and evolve rapidly, continuous monitoring and adaptability are required.

2.4.5 Accounting and Reporting

Accounting and tax treatment of staking rewards are also critical challenges for institutions. Recognition timing, accounting standards, and taxation differ by jurisdiction, and clear guidelines are often lacking.

In Ethereum, rewards come from multiple sources such as base rewards, block proposal rewards, and MEV, each with different timing and characteristics. Accurately categorizing and accounting for these under standards such as GAAP or IFRS is inherently complex.

Reporting is equally essential. Institutions must transparently report staking performance and returns to various stakeholders, including internal decision-makers, auditors, and regulators. This requires infrastructure capable of systematically tracking validator-level performance, reward details, slashing history, and overall portfolio returns.

To meet these needs, institutional staking providers are increasingly strengthening reporting and portfolio management capabilities as core services. For example, Kiln integrates validator operations, vault infrastructure, and portfolio reporting into a single dashboard, and supports audit-ready reporting aligned with GAAP and IFRS through its partnership with Cryptio. Figment also provides institutional-grade reporting features, including real-time portfolio tracking and flexible reward statements.

As staking becomes integrated into broader institutional treasury and financial operations, reporting capabilities have become a key criterion when selecting staking providers.

2.4.6 Liquidity Lockups and Low Yields

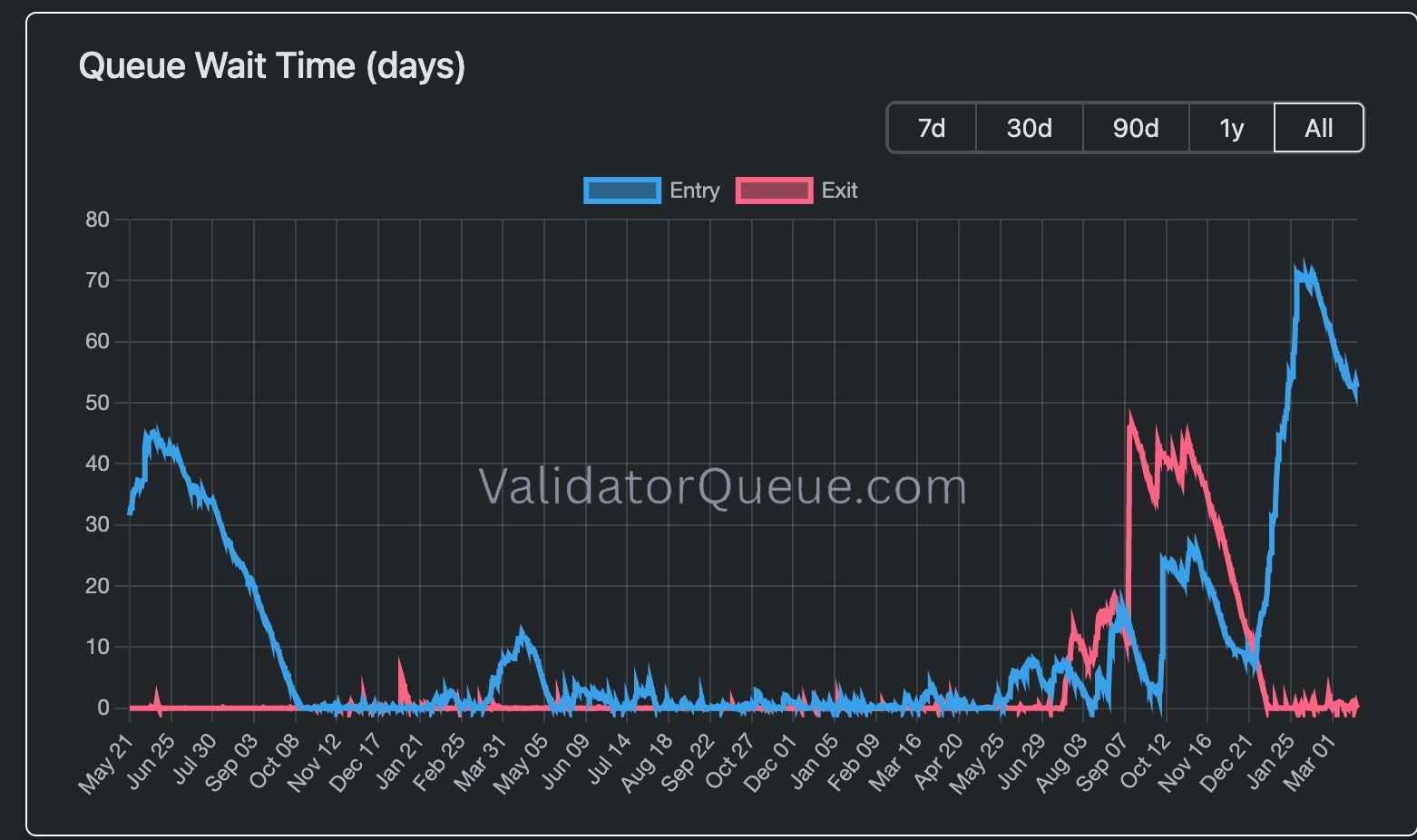

Ethereum staking involves waiting periods for both deposits and withdrawals. To protect network security from rapid validator set changes, Ethereum imposes a churn limit on how many validators can enter or exit per epoch. As of March 23, 2026, deposits require approximately 51 days of waiting, while withdrawals involve around 4 hours of initial delay plus an additional 8.2 days for processing. This introduces significant liquidity uncertainty for institutions.

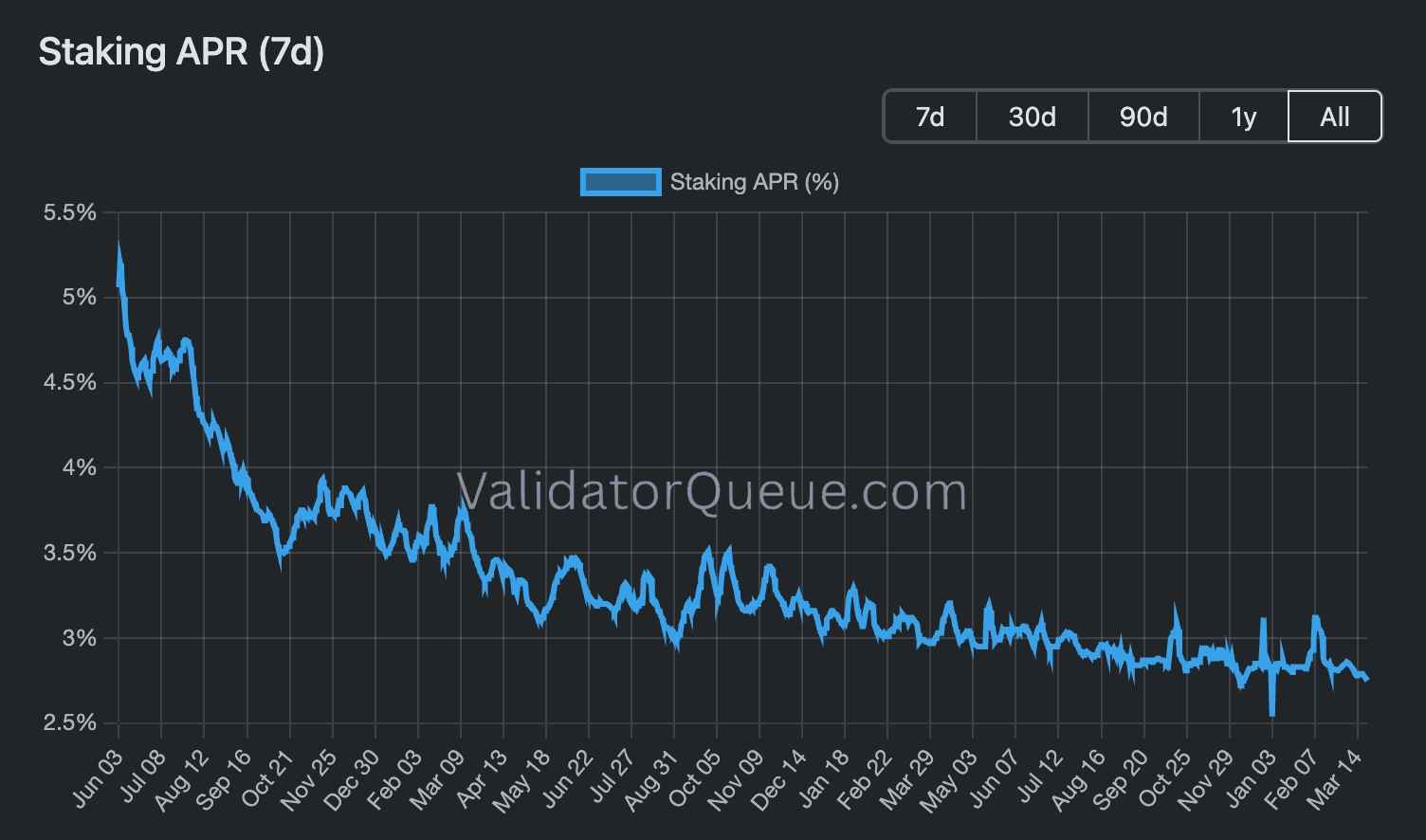

Additionally, the average Ethereum staking APR is currently around 2.86%, which is not particularly high after accounting for node operation costs or staking service fees. The rapid growth in staking participation, driven by DAT companies and staking-enabled ETFs, further impacts returns.

Ethereum’s consensus layer rewards are designed to scale with the square root of total staked ETH. As staking participation increases, the total reward pool grows modestly, but the number of validators sharing it grows faster. As a result, APR per validator declines. The probability of being selected as a block proposer also decreases, and expected execution layer rewards diminish.

Source: ValidatorQueue

The Ethereum roadmap aims to reduce infrastructure complexity and operational costs by increasing the maximum stake per validator and lowering node requirements. Nevertheless, staking alone remains a relatively low-yield activity.

In this context, institutional ETH staking is not simply about depositing ETH. It is a complex undertaking that requires addressing multiple layers of requirements, including infrastructure operations, security, compliance, accounting, and liquidity management. Determining the appropriate operational approach to staking is therefore a critical and challenging decision for institutions.

Given the complexity of directly staking ETH, specialized staking providers offer services that operate validators on behalf of institutions. There are four primary ways institutions can participate in ETH staking.

2.5.1 Custodial Staking

This is the most straightforward approach, where institutions entrust both custody and staking to a licensed provider. Exchange-based staking services are a common example. While this approach minimizes operational burden, it requires relinquishing control over assets to a third party and typically involves higher intermediary fees.

2.5.2 Non-Custodial Staking

Ethereum does not provide native delegation at the protocol level. However, because validator keys used for consensus are separate from withdrawal keys that represent asset ownership, non-custodial staking can be implemented indirectly.

Until early 2025, fully non-custodial staking was effectively impossible on Ethereum because withdrawal rights were tied solely to validator keys. If a staking provider refused to process withdrawals, users could not retrieve their funds.

This issue was resolved with EIP-7002, introduced in the May 2025 Pectra upgrade, which enabled withdrawals to be triggered using the withdrawal key. As a result, Ethereum now supports fully non-custodial staking. However, challenges remain, including the possibility that providers could trigger withdrawals using validator keys without user consent, as well as user experience difficulties associated with managing withdrawal keys.

2.5.3 White Labeling

In this model, institutions outsource only the infrastructure operations to specialized operators. The institution provides staking services under its own brand, while validator operations are handled by external providers. Both custodial and non-custodial configurations are possible.

2.5.4 Lido v3 stVault

Can institutions go beyond simple staking and participate in liquid staking?

One of the biggest limitations of existing liquid staking services like Lido has been the inability for institutions to select their own operators. In Lido’s traditional structure, the protocol manages operators at the module level and distributes staked ETH automatically, preventing institutions from customizing configurations or choosing specific operators.

This creates issues where institutional ETH is pooled together with assets from unknown participants, making it difficult to meet institutional requirements for compliance, accounting, and reporting.

Lido v3 addresses this with the introduction of stVault. stVault provides a modular structure that allows institutions to designate their own operators and configure customized vaults. Institutions can select trusted operators and tailor parameters such as fees, while still benefiting from Lido’s infrastructure and user experience.

In addition, the liquid staking token stETH issued through Lido enables institutions to mitigate liquidity constraints and deploy their assets in on-chain financial activities for additional yield.

This structure effectively addresses most of the challenges outlined earlier for institutional ETH staking, and despite being recently launched, stVault has quickly become one of the most closely watched solutions in the space.

As a research firm based in Korea, Four Pillars often receives questions from overseas protocols we collaborate with, such as whether Korean institutions can participate in institutional services like staking. This section aims to help global readers easily understand Korea’s institutional staking market.

Korea’s retail staking market is primarily exchange-driven. Major Korean exchanges such as Upbit, Bithumb, Coinone, and Korbit all offer staking services for various PoS assets, including ETH.

Upbit provides staking for six assets, including Ethereum, Cosmos, Solana, Cardano, Polygon, and Cronos, charging a 10% fee on staking rewards. Bithumb supports staking for 16 assets, the largest number among domestic exchanges, with an average fee of around 6.6%, lower than Upbit. Coinone and Korbit also operate staking services.

All of these exchanges provide custodial staking services based on assets deposited by users. When users deposit assets into the exchange, the exchange stakes them either internally or through trusted staking providers and distributes the rewards.

Some users also participate in staking directly through personal wallets. They may use liquid staking protocols such as Lido or operate validators themselves. There is even a Korean Ethereum solo validator community. However, this segment is relatively small compared to exchange-based staking. Korea’s digital asset trading and financial activities remain structurally centered around exchanges.

To understand Korea’s institutional staking market, it is necessary to first examine the country’s regulatory environment for digital assets. In short, institutional ETH staking in Korea is still highly restricted, but the landscape is rapidly evolving.

3.2.1 Regulatory Status of Digital Assets for Institutions

Before discussing institutional staking, it is important to determine whether corporations are even allowed to hold digital assets. There is no law explicitly prohibiting corporate ownership of digital assets. However, in practice, corporations have been effectively blocked from opening real-name accounts on domestic exchanges.

This was not due to explicit legal prohibition, but rather because financial authorities had advised partner banks not to issue real-name accounts to corporations. As a result, corporate purchases of digital assets were effectively restricted, which in turn limited their ability to hold them. Some companies have bypassed this by acquiring digital assets through overseas subsidiaries or OTC markets.

This situation began to change gradually starting in 2025. In November 2024, the Virtual Asset Committee was established, initiating discussions around corporate real-name accounts. In February 2025, the Financial Services Commission announced a roadmap for corporate participation in the digital asset market. As part of the first phase, in June 2025, non-profit organizations and exchanges were allowed to open corporate accounts for the purpose of selling digital assets.

In the first half of 2026, the second phase aims to allow listed companies and registered professional investors to trade digital assets. Under this phase, corporate investments are expected to be limited to within 5% of equity capital and restricted to the top 20 assets by market capitalization on major domestic exchanges. Major KRW-based exchanges such as Upbit, Bithumb, and Korbit have already established systems to serve corporate clients. Upbit has registered 233 corporate clients, while Bithumb has around 200.

This means that Korean corporations will be able to invest in and hold digital assets relatively freely within regulatory limits. Given the conservative nature of domestic institutions, they are likely to allocate primarily to BTC and ETH, which can be interpreted as a positive signal for the expansion of institutional ETH staking.

3.2.2 Classification of Staking Regulations

Even if corporations are allowed to hold digital assets, whether they can use them for staking is a separate issue. The legal status of staking services in Korea is not yet fully defined.

Currently, the Act on the Protection of Virtual Asset Users requires service providers to maintain “effective control” over user assets. In the case of staking, it remains unclear whether depositing user assets into blockchain networks violates this requirement.

From a regulatory perspective, staking providers that hold private keys and provide custodial services must register as Virtual Asset Service Providers. On the other hand, non-custodial staking models where users delegate directly from their own wallets, or models where providers validate using their own nodes while holding equivalent assets, may not require such registration.

However, if staking is deemed to go beyond simple deposit and constitute asset management, it could become subject to additional regulations under the forthcoming Digital Asset Basic Act.

It is also worth noting that major jurisdictions such as the United States, Japan, Europe, and Hong Kong already allow staking while strengthening internal controls and disclosure requirements. The United States has recently clarified that staking is not a security. While Korea’s regulatory stance has been relatively conservative, it is likely to gradually align with global trends.

3.2.3 ETFs

What about ETFs, which could become the largest channel for institutional ETH staking in Korea?

Currently, Korea does not allow spot ETFs for digital assets. This stands in contrast to the United States, where Bitcoin and Ethereum spot ETFs are actively traded and BlackRock has even launched an ETH staking ETF.

However, the Korean government has signaled plans to introduce spot digital asset ETFs in its 2026 economic policy direction, with implementation tied to the Digital Asset Basic Act. Once spot ETFs are introduced, the path toward ETH staking ETFs could naturally follow.

In practice, major asset managers are already preparing. Korea Investment Management has formally requested approval for a BTC ETF, while Mirae Asset has experience launching and managing global crypto ETFs through its subsidiary Global X in the United States and Europe. If domestic regulations are relaxed, the launch of crypto ETFs by Korean asset managers is likely to follow.

3.2.4 Separation of Finance and Industry Principle

Korea has a unique regulatory principle known as the separation of finance and industry. This principle restricts financial institutions such as banks, securities firms, and insurers from directly entering or investing in the digital asset industry.

The potential relaxation of this principle has been identified as one of the key digital asset issues for 2026. If relaxed, it could significantly accelerate ETH investment and staking participation by Korean financial institutions.

Despite regulatory constraints, Korea’s digital asset and staking markets have substantial potential.

3.3.1 A Massive Retail Market

Korea ranks among the top countries globally in terms of retail digital asset trading volume. Millions of retail investors are already active in the market, and staking through exchanges is familiar to many. This large retail base provides a strong foundation for rapid growth in institutional staking once corporate participation is fully enabled.

3.3.2 Imminent Opening of the Corporate Market

In the first half of 2026, listed companies and professional investors are expected to be allowed to trade digital assets. Once corporate investment begins in earnest, tens of trillions of KRW in new capital could flow into the market. As these entities accumulate ETH, demand for yield generation through staking, similar to ETH-focused DAT companies in the United States, will naturally emerge.

3.3.3 ETF Roadmap

With the Korean government signaling the introduction of spot digital asset ETFs in 2026, a pathway could open for ETH spot ETFs and eventually ETH staking ETFs over the mid to long term. Given that Korean investors are already investing in overseas crypto ETFs, domestic ETF launches are likely to see strong demand.

3.3.4 Direction of Phase 2 Legislation

The upcoming Digital Asset Basic Act is expected to include comprehensive provisions covering classification of service providers, scope of business, disclosure obligations, and stablecoin regulations. Once implemented, it will clarify the legal status of staking services and significantly reduce uncertainty for institutional participation.

Given that jurisdictions such as the United States, Europe, Japan, and Hong Kong have already established regulatory frameworks that permit staking, Korea is also expected to move in a similar direction to maintain global alignment.

Ultimately, within the broader trend of institutional crypto adoption, ETH staking is no longer just a supplementary yield strategy but is becoming a foundational layer of institutional asset management. Its appeal from a portfolio diversification perspective, combined with the structural necessity of blockchain infrastructure innovation and increasing regulatory clarity, has made institutional inflows into crypto a structural trend, with ETH at its core. Once ETH is held, staking becomes not optional but essential.

Institutional ETH staking has already been validated as a market, particularly in the United States. Applying this global trend to Korea, while institutional participation is currently limited due to regulatory constraints, the direction is clear. Corporate ownership and trading of digital assets are being gradually permitted, ETFs are on the horizon, and regulatory frameworks for staking are taking shape.

Given the conservative nature of domestic institutions and their likely focus on BTC and ETH, demand for institutional ETH staking in Korea is likely to expand structurally over time. In other words, while Korea may be a late entrant compared to global markets, it has the potential to experience a more compressed and accelerated growth curve.

At this inflection point, the key question is how effectively complex institutional requirements can be abstracted and delivered in executable forms. This is where solutions like Lido’s stVault become particularly important. stVault enables operator selection, vault-level segregation, and customizable fee and policy configurations, while also providing liquidity and DeFi composability through stETH. This design addresses many of the traditional trade-offs in staking, including custody, compliance, and liquidity.

Key factors to watch in Korea’s institutional ETH staking market include:

Regulatory clarity and detail: How staking, custody, and asset management activities will be defined under the Digital Asset Basic Act and related regulations

Legal classification of staking: Whether staking is treated as simple deposit activity or as investment/asset management, and how this affects regulatory requirements

Timeline of regulatory changes: The sequencing and timing of corporate trading permissions, ETF introduction, and potential relaxation of financial regulations

Scale of institutional capital inflows: The extent to which listed companies and professional investors allocate ETH into their portfolios

Permitted staking models: Whether custodial or non-custodial staking structures will be allowed or prioritized

Adoption of institutional infrastructure: The pace at which global staking providers and infrastructure solutions enter the Korean market

Role of ETFs and indirect exposure: How ETH spot ETFs and staking ETFs will influence institutional staking demand

Participation of financial institutions: Whether banks and securities firms will be allowed to engage in staking and related services, including potential changes to the separation principle

Adoption of liquid staking: Whether institutions will move beyond simple staking to use structures like liquid staking tokens such as stETH, and how regulators respond

Development of risk and accounting standards: How accounting and tax standards for staking rewards, slashing risks, and valuation will be established

Dive into 'Narratives' that will be important in the next year