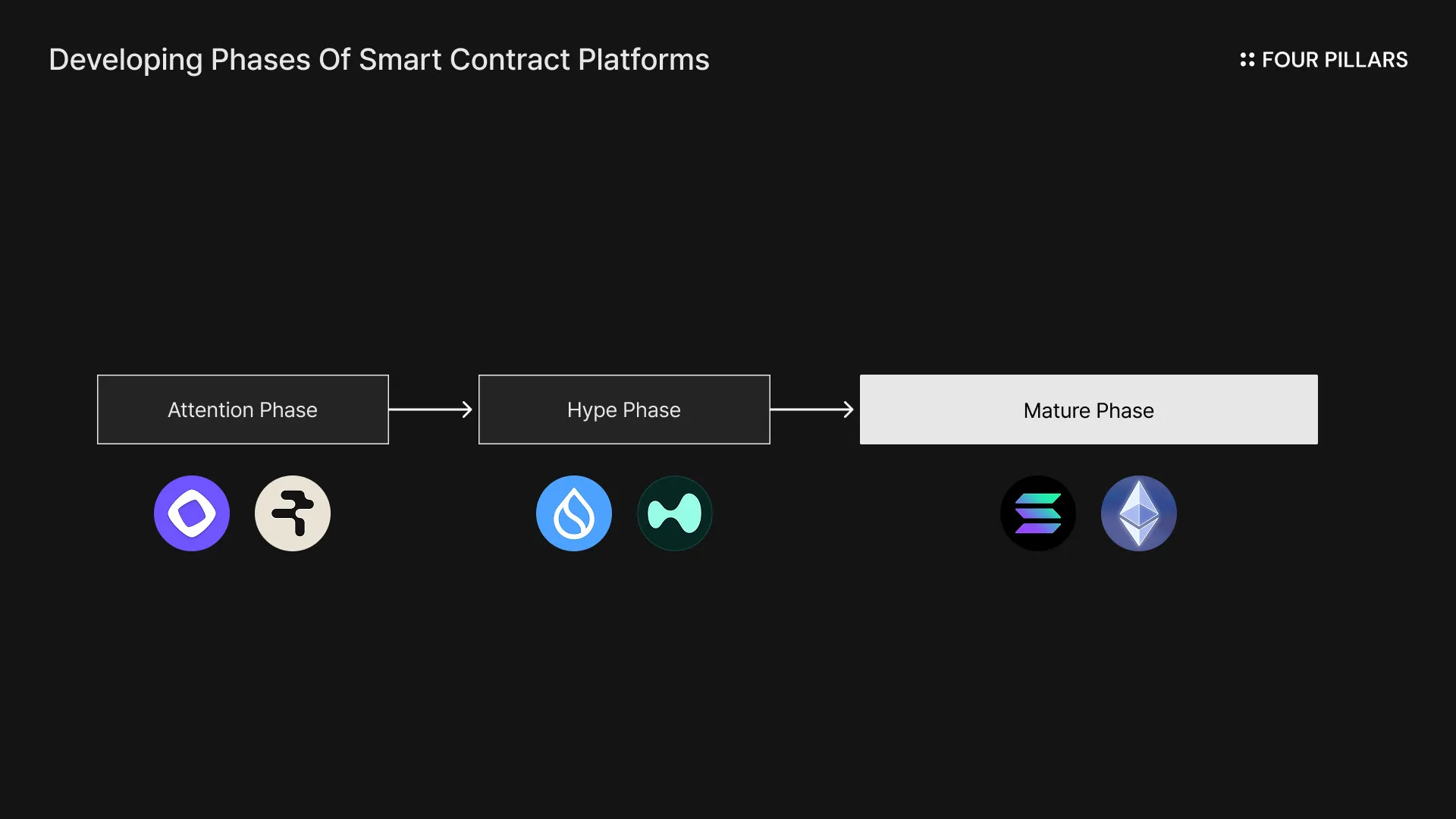

I believe the growth trajectory of smart contract platforms can be divided into three distinct phases. The first is the Attention Phase, where a platform begins to attract market interest. The second is the Hype Phase, where that attention translates into real expectations and investor conviction. The final stage is the Maturity Phase, where the platform not only meets market expectations but also establishes a sustainable ecosystem beyond short-term excitement. Based on these criteria, Ethereum and Solana can be seen as platforms that have entered the maturity phase, while Sui and Hyperliquid sit in the hype phase, and Monad and Rialo remain in the attention phase. What we should focus on going forward is whether Sui and Hyperliquid—and similarly, Monad and Rialo—can each progress to the next stage. For Sui and Hyperliquid, this will require deeper ecosystem expansion, while Monad and Rialo must solidify their differentiated value propositions.

Crypto as an asset class is also reaching an important inflection point where fundamentals are finally being established. As the SEC’s stance on tokens becomes increasingly clear, even app tokens that were previously dismissed as “meme coins” have begun to link application revenue with token value through revenue-driven token buyback strategies. This creates a more concrete framework for evaluating token value. Moreover, smart contract platforms are now experimenting with mechanisms that connect ecosystem growth directly to token value—going beyond simple governance and transaction fee models. As a result, the key question becomes which platforms can build the strongest and most sustainable fundamentals over time.

Lastly, the stablecoin market is poised for significant disruption. Until now, the space has effectively been a duopoly dominated by Tether and Circle. But going forward, major networks are likely to push for their own native stablecoins, investing heavily in their growth. Revenue generated from stablecoin business models may increasingly be reinvested back into the ecosystem. In particular, Bridge’s Stablecoin-as-a-Service model removes many of the long-standing obstacles that have prevented ecosystems from launching their own stablecoins, suggesting that we may soon see a proliferation of chain-specific stablecoins competing for market share. We are entering an era where stablecoin issuers create chains, and chains create stablecoins. Where does this competition ultimately lead?

The growth trajectory of smart contract platforms can broadly be divided into three stages. The first is the “attention stage”, where a platform begins to capture the market’s interest. The second is the “hype stage”, where that attention transforms into real expectations and speculative capital.

The final phase is the “maturity stage”, where a platform actually delivers on those expectations and builds a sustainable ecosystem that outlives any short-term mania.

To be blunt, in today’s market, the only smart contract platforms that can reasonably be described as having entered the “maturity stage” are Ethereum and Solana. Every other platform either:

initially succeeded in drawing attention but has yet to prove its sustainability, remaining stuck in the “hype stage”, or

still lingers in the “attention stage” with vague expectations but no clear results or substance.

Going one step further, many infrastructure projects preparing for mainnet launch today have not even managed to reach these stages. They exist in a reality where they are completely ignored by the market. In this piece, I will not bother mentioning such projects. In my view, these are already effectively past the end of their life cycle, even if they haven’t realized it yet.

Instead, this article will focus on the major smart contract platforms that currently remain in the “hype” or “attention” stages, examine their defining characteristics, and explore how they might realistically transition into the “maturity stage.”

If we were to pick the two infrastructure projects that have generated the most hype in this cycle, they would undoubtedly be Sui and Hyperliquid. The two could not be more different in most dimensions—design philosophy, strategy, and long-term vision—yet each has managed to engineer its own version of a successful hype cycle.

Let’s go through each platform in turn to understand how they entered the hype stage.

1.1.1 Sui – A “Planned Economy” Style of Growth and a New Playbook

I often compare blockchains to nation-states. A blockchain ecosystem is, in essence, a massive economic system and a space where people come together to make governance decisions—very much like a country. If that analogy holds, then the way a blockchain grows can also resemble how a country develops.

From this lens, I see Sui’s growth strategy as closely mirroring the developmental model of certain nation-states—particularly those like Korea or Singapore, where the government initially leads the build-out of economic infrastructure, and later hands over growth to the private sector.

Sui introduced a brand-new programming language, Move, and designed nearly all of its core technology from scratch, securing a genuinely innovative technical foundation. But this very originality became an obstacle to ecosystem expansion. To build anything meaningful on Sui, developers must first deeply understand Sui’s unique technology stack—an investment of both time and talent.

So the question becomes: with a limited pool of builders in the early phase, how do you bootstrap an ecosystem? The answer was fairly straightforward:

If there aren’t enough builders yet, the entity that understands Sui best—the core team, Mysten Labs

In practice, Mysten Labs behaved like the government of a developing country, directly planning and deploying critical infrastructure—roads and power plants in the real world, core protocols and primitives in Sui’s case.

Concrete examples include:

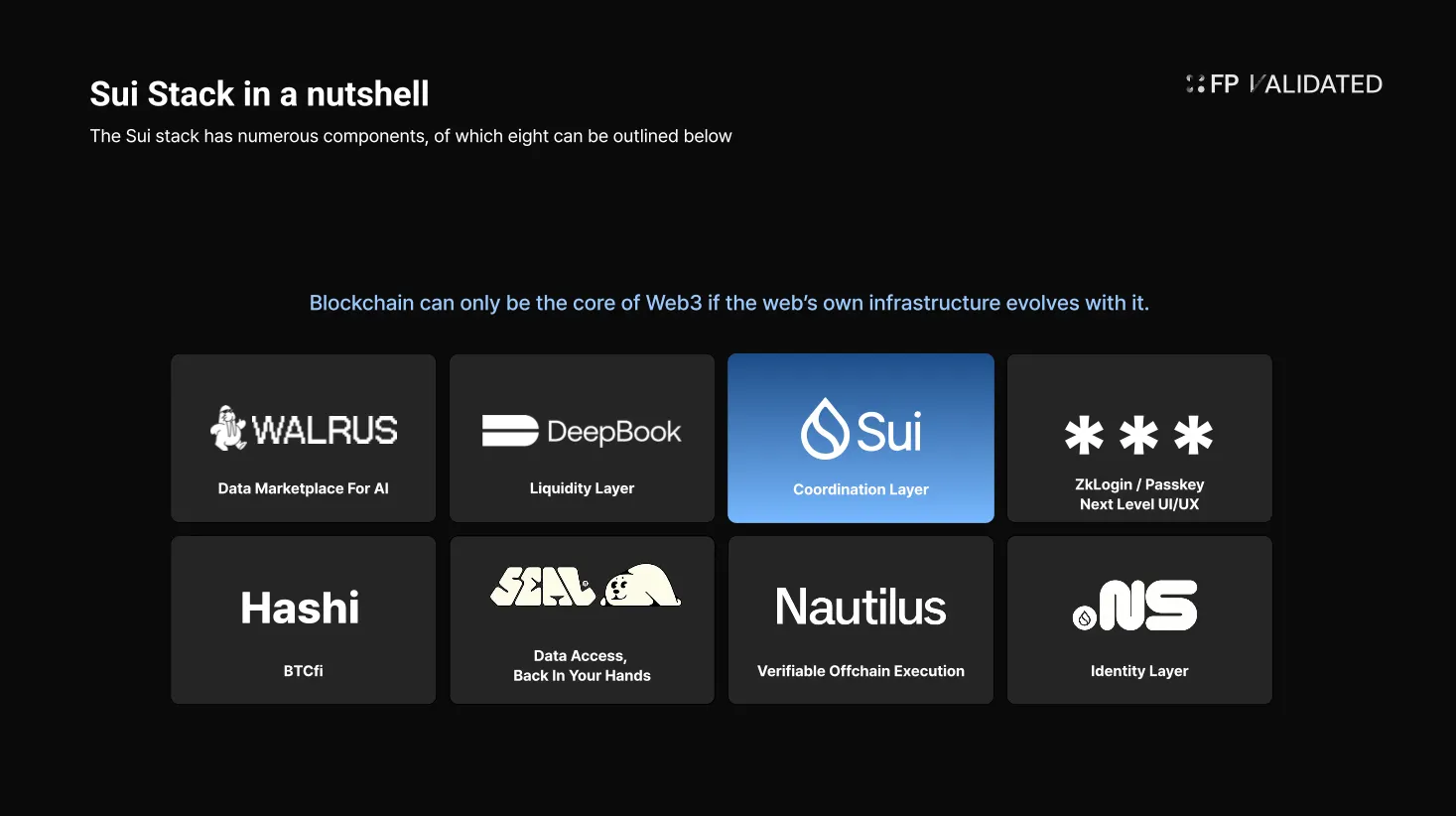

DeepBook – the liquidity layer (central limit order book)

Walrus – the data marketplace / data availability layer

SuiNS – the identity layer (naming service)

Mysten didn’t stop at simply building infrastructure. They also distributed large-scale token airdrops for their products to the community, providing tangible incentives for ecosystem participation. This strategy spread quickly across the industry: projects like Aptos and Story began adopting similar approaches, proving that Sui’s strategy had become a new playbook for other L1s.

The result was a large influx of new users into the Sui ecosystem. The combination of an increasingly engaged community and strong technical expectations pushed Sui firmly into the “hype stage.”

1.1.2 Hyperliquid – One Killer App Is Enough

Hyperliquid, by contrast, followed almost the exact opposite strategy of Sui. Instead of trying to grow an entire ecosystem, Hyperliquid focused relentlessly on one single app: the exchange.

In my view, there are only three categories in this industry where product-market fit (PMF) has been unequivocally demonstrated:

Stablecoins

Exchanges

Token businesses

Hyperliquid combined the exchange and the token business to drive its hype.

Under the banner of a “decentralized Binance”, Hyperliquid built a platform where users can trade a wide range of assets and, critically, distributed a significant portion of the token supply to highly engaged early users, without involving venture allocations. This model helped cultivate a community that borders on religious in its loyalty.

On top of this, Hyperliquid implemented a revenue model in which protocol revenue is used to buy back the token. That allowed them not only to stabilize token performance after a large airdrop, but also to drive a >10x increase from TGE, further strengthening community cohesion.

The net result is that Hyperliquid has become a venue where users trade assets without needing ongoing airdrops or point incentives. At the time of writing, Hyperliquid is consistently ranked among the top 1–2 protocols by revenue, making it one of the most successful products in the entire blockchain industry. Its “revenue + buyback” model has kicked off a broader trend, and much like Sui, Hyperliquid has carved its own path into the hype stage.

1.1.3 Ecosystem, Ecosystem, Ecosystem – The Common Challenge Facing Both

Despite their differences in character and growth strategy, Sui and Hyperliquid share several key traits:

They are both newly emerged blue-chip blockchain infrastructure in this cycle.

They have both successfully reached the hype stage.

And crucially: they both struggle to build sustainable ecosystems, and thus cannot yet be said to have reached “maturity.”

Let’s start with Sui.

There are now hundreds of apps on Sui, yet when users think “Sui ecosystem,” there are only a handful of services that truly come to mind. The closest candidates would be:

Cetus

Suilend

Bluefin

Prime Machine

(This is not meant to disparage other builders’ efforts.)

The key point is this: the business models of these projects are not inherently “Sui-native.” While Suilend, for example, does leverage Sui’s technical characteristics to improve UX, it’s hard to argue that the lending model itself could only exist on Sui.

In other words, Sui achieved an early surge in value—boosting ecosystem TVL and revenue—largely thanks to Mysten Labs’ top-down strategy and infrastructure rollout. But since then, we’ve seen very few examples of “purely ecosystem-driven builders” delivering outsized growth.

So far, there have been almost no breakout projects that:

aren’t built directly by Mysten Labs, and

fully leverage Sui’s unique infrastructure to create business models that are truly only possible on Sui.

That absence is one of the structural limitations facing Sui today.

Of course, infra projects like IKA are being built on Sui and introducing interesting technologies. But even so, it’s hard to say that any of these have yet become the defining flagship projects of the Sui ecosystem. At the time of writing, aside from the infrastructure built by Mysten Labs, it is difficult to find any Sui ecosystem project that has reached even $500M in fully diluted valuation, let alone $1B.

There are many reasons why Sui’s ecosystem growth has been underwhelming, but from my vantage point, one critical issue is this:

Mysten Labs continues to build products—and in some cases, those products compete directly with ecosystem players.

Sui’s early success owed a lot to Mysten’s ability to ship high-quality products. But how long can the ecosystem grow under a model where Mysten remains the primary driver? Just as high-growth developing countries eventually transition from state-led to private-sector-led growth, Sui too must eventually move towards an ecosystem where independent builders lead expansion.

From that perspective, Sui needs to seriously reflect on when and how it will make that transition.

As IKA founder David has argued, in an environment where no one knows what products Mysten might decide to launch next, it’s understandable that some developers may find Sui less attractive. If Mysten can at any time release a direct competitor to your product, the playing field feels inherently skewed. Bearing that kind of uncertainty and asymmetry is a significant risk from a builder’s standpoint.

Source: Messari

Hyperliquid is no exception to these ecosystem challenges.

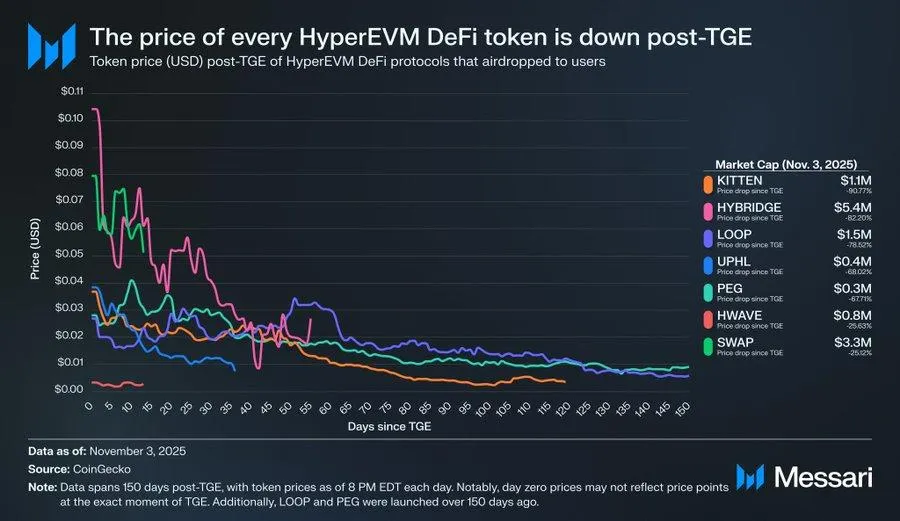

While Hyperliquid has successfully turned $HYPE into a powerful deflationary asset, it has failed thus far to build a sustainable HyperEVM ecosystem.

When you look at the price performance of major tokens in the HyperEVM ecosystem, the pattern is clear: most of them have trended downwards since launch. This alone is enough to make the community skeptical about HyperEVM’s long-term vision.

At the root of this issue is a fundamental disconnect between Hyperliquid Core (the exchange) and the HyperEVM ecosystem.

Hyperliquid Core is already a successful product with a highly loyal user base of traders. But those traders have little reason to move capital onto HyperEVM. The user personas are different. Perp traders—who rely on leverage and active trading—are naturally less inclined to lock their assets up in DeFi or buy NFTs.

When HyperEVM first launched, many expected Hyperliquid Core users to naturally spill over into the ecosystem. The reality has been the opposite. As time has passed, hype around HyperEVM has steadily faded.

We saw the peak of this downward sentiment recently, when news broke that the Hyperliquid team was testing a feature on the core testnet suspected to be BLP (BorrowLendingProtocol). If this functionality is indeed rolled out to Core, then lending protocols on HyperEVM will be forced to directly compete with the core product.

In the short term, such a move might be positive for $HYPE token value, as it further consolidates value at the core level. But from the perspective of the HyperEVM ecosystem, it risks being clearly negative: ecosystem projects would now find themselves competing against the core team itself.

That leaves us with a set of unresolved questions:

How will Sui and Hyperliquid break through their ecosystem limitations?

When will Mysten Labs shift from centralized leadership to king-making—elevating capable builders and fostering true ecosystem independence?

Why is Hyperliquid building lending functionality at the core level, and how can that decision coexist with HyperEVM’s stated goals?

Time will answer these questions. But if they fail to solve these problems, the outcomes could be:

Sui becomes “just another smart contract platform,” and

Hyperliquid remains “just a highly profitable decentralized exchange.”

Of course, it’s also true that 90% of other projects in the market aren’t even at a level where they can wrestle with problems like these, which is its own kind of irony. Still, it would be far better for the industry if both Sui and Hyperliquid successfully navigate these challenges and set positive precedents for others.

And it’s too early to be pessimistic. When Solana—now regarded as “mature”—was still in its hype phase, it nearly died in the aftermath of the FTX collapse. Ethereum went through its own formative crises as well. Growing pains are an inevitable part of any ecosystem’s journey.

Sui and Hyperliquid have already completed their TGE and reached a point where it’s meaningful to debate whether they’ll transition into the maturity stage.

On the other side, there are projects that are still pre-TGE but have already captured meaningful attention and show potential to grow into something akin to Sui or Hyperliquid in the future.

In my view, Monad and Rialo are prime examples of this category.

Let’s look at them one by one.

1.2.1 Criticism Is Also Attention – Monad Has Locked in Early Mindshare

Few projects in recent crypto memory have attracted as intense a spotlight as Monad. Some are extremely bullish, others argue the expectations are wildly overblown. But for a pre-TGE project like Monad, this level of attention is, in itself, a major asset.

In this industry, attention is value.

At this point, almost everyone in the space has at least heard of Monad, and most are watching for its mainnet launch. That doesn’t mean all expectations are positive, but the fact that Monad has captured this level of focus means it starts from a far more advantageous position than most other pre-TGE projects.

To become a truly “hyped” project in the way Sui or Hyperliquid have, Monad needs to go beyond just ecosystem talk and clearly demonstrate what makes it unique. Sui created its own playbook; Hyperliquid created its own; Monad will need a distinct, non-copy-paste playbook of its own.

Monad talks a lot about “technology,” but even Sui—which was arguably the most tech-forward L1 of its generation—found that technology alone was not enough to generate sustainable hype. Monad will need concrete strategies that ensure airdrop recipients don’t just sell and leave, but instead have reasons to keep capital parked in the ecosystem and find further opportunities to generate value there.

That said, Monad does have some relative advantages when compared to Sui and Hyperliquid:

Versus Sui, Monad can tap into the massive existing EVM developer ecosystem, a huge advantage in terms of potential builder base.

Versus Hyperliquid, Monad benefits from more naturally aligned incentives—Hyperliquid still struggles with the gap between Core users and HyperEVM users, whereas Monad can design more unified alignment from day one.

If Monad can capitalize on these strengths while learning from the precedents set by Sui and Hyperliquid—and ultimately craft its own playbook—it has a realistic chance to grow into an infrastructure project that truly enters the hype stage.

1.2.2 Rialo – The Raw Disruptive Power of Real Innovation

If Monad has a natural talent for attracting attention, Rialo competes on the strength of its technology itself.

And when I say “technology,” I’m not talking about the usual clichés of TPS (transactions per second) or latency. Rialo questions something more fundamental: the basic architectural assumptions that underlie most blockchains.

Historically, when a new blockchain launched, the “must-have” infra stack always included things like oracles and bridges. But Rialo starts by questioning why these infra components are even necessary in the first place.

In the early days of blockchains, blockspace was extremely limited. That naturally forced the system to offload various responsibilities to third parties. Today, however, blockspace is more abundant, and chains are more than capable of directly interfacing with external data.

If:

oracles are just a mechanism to bring off-chain data on-chain, and

bridges are just a way to bring data from other chains into your chain,

then Rialo’s design philosophy is essentially:

“Why rely on third parties, when the chain itself can perform these roles directly?”

This is a radical departure from how blockchains have traditionally been designed. It moves us from static blockchains to dynamic blockchains, and that alone makes Rialo a project worth paying attention to.

If Rialo works as described in theory, the range of possible applications that can be built on it becomes enormous.

One example is a CEX–DEX unified aggregator. Because Rialo allows smart contracts to directly call HTTPS/REST APIs, a user could, in theory, initiate a trade on a CEX via an API call without ever visiting the CEX frontend. At the same time, the contract could also query and interact with DEXs on other chains via APIs, dynamically finding and executing the best price across all venues.

Rialo already has the infrastructure to enable applications that are “only possible on Rialo.” Whether it transitions from the attention stage to the hype stage will depend on how well theory translates into practice.

If Rialo launches successfully and behaves as designed, I expect many future blockchains to adopt Rialo’s design philosophy as a template.

Some argue that crypto “has no fundamentals,” and dismiss the space altogether. But what do we actually mean by fundamentals?

In simple terms, fundamentals refer to the underlying value, cash flows, and demand drivers that support an asset.

In equities, that means:

revenue,

operating income,

net income,

cash flow, and

capital structure.

With this definition in mind, we can revisit the question:

Does crypto still have no fundamentals?

I would argue the answer is no. While it’s true that most assets are still priced heavily on narratives and expectations, I believe the market is gradually shifting from pure narrative to fundamental-oriented evaluation.

One of the biggest reasons for this shift is the changing stance of the SEC.

Under the Biden administration, the SEC took the view that tokens are effectively securities. This meant that, even if DeFi protocols or other applications issued tokens and sold them into the market, there was no safe way to link protocol revenues to token value without incurring securities-law risk.

That regulatory overhang is now weakening.

The SEC has clearly stated that Ethereum is not a security, and

In the Ripple case, the court ruled that XRP is not a security in all contexts.

In other words, the blanket risk that “any token = security” has receded.

At the same time, more and more protocols—Hyperliquid among them—are using protocol revenues to buy back tokens, and these models are working well enough that others are beginning to follow. Many projects are now exploring ways to use their revenue to turn their tokens into deflationary assets through buybacks.

On top of that, we’re seeing a growing trend where major ecosystems issue their own native stablecoins and reinvest the resulting profits back into their ecosystems. This is a strategic move to leverage a proven product (stablecoins) to build self-reinforcing capital cycles and strengthen fundamentals.

From this vantage point, there are several protocols and initiatives that I think are especially worth watching.

Not long ago, Uniswap proposed a governance proposal to use protocol revenue to burn its governance token, $UNI. The key detail here is that the proposal doesn’t only cover future revenue, but also includes treasury funds accumulated from past protocol fees, which would be used to burn roughly 100 million $UNI in one shot.

This is more than just a Uniswap-specific event. It’s a major milestone for all protocols that have steadily generated revenue.

Starting with Uniswap, we can expect that any protocol that has found PMF and generates stable revenue will explore ways to align protocol profits with tokenholder incentives.

Even protocols without current revenue but with strong revenue potential will become the center of new narratives. Historically, crypto narratives have been dominated by speculative themes. Going forward, I think we’ll see more narratives like:

“How strong is this protocol’s earnings potential?”

Instead of:

“This tech is cool,” or “The community is strong.”

In that world, market potential and revenue scalability become the narrative themselves. The era of mid-curve thinking—weighing both fundamentals and upside carefully—will replace pure reflexive speculation as the most effective way to navigate the market.

From that perspective, the first things to watch are protocols operating in sectors where PMF is already proven and where they play foundational roles.

In my view, there are four categories in today’s crypto market with clearly demonstrated PMF:

Token trading

Token creation

Stablecoins

Leverage

Examples:

Uniswap sits squarely in the “token trading” category,

Hyperliquid, which uses token buybacks funded by revenue, belongs in a similar bucket,

Pump.fun is a hybrid of “token trading” + “token creation”,

SKY (e.g., Maker’s Sky ecosystem) straddles both “stablecoins” and “leverage.”

For lending protocols, we should focus on those with sustainable models without heavy artificial incentives—platforms like Aave and Morpho in the Ethereum EVM ecosystem.

If institutional participation increases, platforms that onboard real-world assets (RWA) on-chain will be worth watching as well. And if DATs (Digital Asset Treasury managers) start staking their assets at scale, staking infrastructure protocols will also benefit.

In short, we’re entering a period where the market will increasingly prioritize real numbers and sustainable revenue over pure memes. (That doesn’t mean the meme market disappears, just that it will no longer be the only game in town.)

Of course, we should be careful with the term “buyback” itself.

Some projects label what are essentially artificial token purchases—not backed by real revenue—as “buybacks.” Even when buybacks are revenue-based, using something like 95% of revenue for buybacks is an obvious red flag for sustainability. Using every dollar of revenue on buybacks is not automatically “good.”

Just like in traditional markets, businesses often need to reinvest revenue into growth. Most successful companies did not reach scale by funneling all revenue back to shareholders from day one.

As buybacks have become a narrative in themselves, we’re seeing some protocols become unhealthily obsessed with buybacks. We should be cautious of:

buybacks with no underlying business substance, and

extreme, unsustainable buyback policies.

If you want to see which protocols are actually generating real, consistent revenue, tools like DeFiLlama are a good place to start.

Another type of “fundamental,” in my view, lies in protocols that change the structural nature of crypto assets in a more sound and substantive direction.

So far, when we’ve talked about “token-based economies,” what we mostly meant was loosely aligned incentive structures.

Take a typical L1 and its native token.

We usually say the token has three main roles:

providing economic security for the chain (staking, validation),

enabling governance participation, and

serving as the fee token for using the chain.

On paper, this looks like robust token utility. But this alone is still not enough to claim a strong fundamental value proposition.

Consider a scenario where a “killer app” launches on a chain and generates tens of millions in daily revenue. Users might buy the L1 token to pay fees, but the vast majority of the value created by that app does not accrue directly to the chain token.

On fast, low-fee chains like Solana or Sui, transaction fees are tiny. So even if transaction volume grows dramatically, fee revenue alone will only marginally improve the L1 token’s fundamentals. The biggest beneficiaries will still be the apps themselves.

Now that dApps can use their own revenue to buy back their own tokens, from an investor’s perspective, owning the app token may often be more rational than owning the L1 token where the app resides.

This is a bit like imagining Instagram as a separately listed company beneath Meta:

If Instagram delivers a huge earnings beat, Instagram’s stock would surge,

But Meta’s stock might barely move.

Value is fragmented, not consolidated.

In Korea, a similar pattern can be observed with Kakao—subsidiaries can generate huge revenue, but the parent company’s stock doesn’t fully capture all that value. (Of course, blockchains are permissionless systems rather than corporate groups with direct control—but the analogy helps illustrate the point.)

Ultimately, solving this requires a tighter economic link between the fee token and applications.

We see a useful analogy in Alphabet (Google’s parent company). Alphabet owns massive businesses like Google, Waymo, DeepMind, and Google Cloud. Each of these units is large enough to be a standalone public company, but they remain under the Alphabet umbrella.

As a result:

Alphabet itself has enormous scale, and

When subsidiaries perform well, their value accrues back to Alphabet.

In some ways, it’s time for the crypto industry to explore similar value-accrual structures.

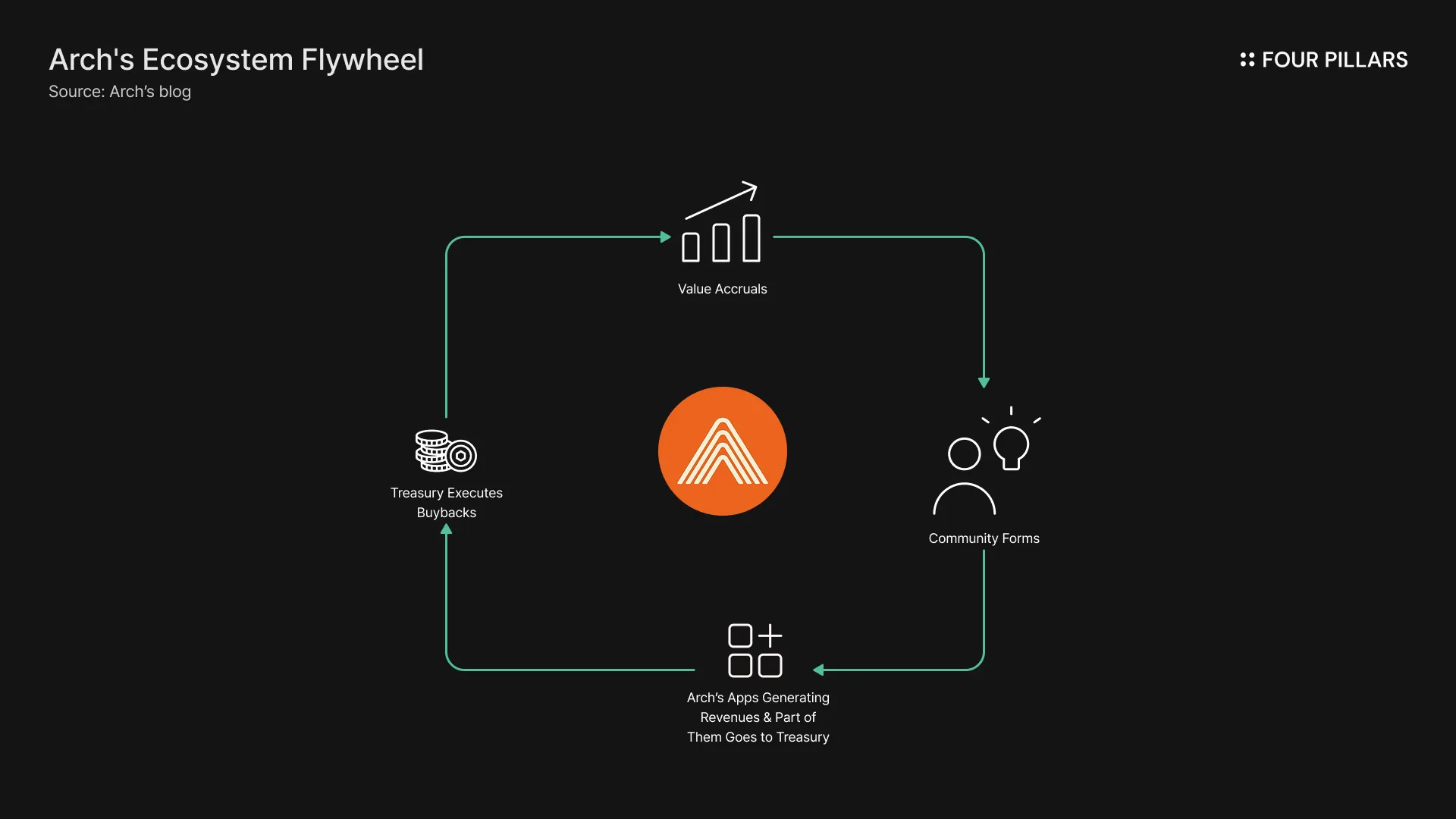

From this standpoint, Arch presents a particularly interesting playbook.

Arch’s model allows apps built on Arch to use a portion of their revenue to buy back the Arch network token. This is more than simple revenue sharing; it’s a conscious attempt to directly link network incentives with application performance.

To be clear, not every app on Arch is required to share revenue with the core team. But for projects that receive early support and “king-making” from the Arch Foundation, it’s likely that their success is structurally tied to value accrual for the Arch token.

In other words:

Arch is experimenting with a framework that ties the growth of the

network token

key ecosystem apps

a single economic flow

If this experiment succeeds, Arch token holders will no longer have to rely on vague expectations like “fees might grow a lot someday.” Instead, they’ll be able to evaluate Arch based on concrete metrics such as:

Which apps generate how much revenue?

What portion of that revenue is regularly used to buy Arch tokens each month?

This is a massive step toward more measurable, fundamental valuation.

Of course, this approach is highly experimental and carries real risk. Even if it works well in the early stages, conflicts of interest could emerge as apps scale and incentives diverge from those of the network.

Still, I see Arch’s value-accrual framework as one of the most important attempts to reposition crypto assets as mature financial instruments. If the core goal of token-based economies is to tightly align incentives among participants, then in my view: Arch’s proposed incentive structure is one of the most rational and fundamentally grounded.

Source: Stripe

When we talk about the fundamentals of a token or chain today, we tend to focus on chain-level revenue. We also look at metrics like TVL or stablecoin circulation, but those are at best indirect indicators, not direct reflections of token value.

In the future, I believe we’ll increasingly evaluate platforms based on:

“How many smart contract platforms have issued their own native stablecoins, and how much is theircirculating supply growing over time?”

As mentioned earlier, stablecoins have already achieved clear PMF and will continue to enjoy steady demand. The challenge is that, until recently, most blockchain foundations—even ones fully aware of this—have struggled to issue their own stablecoins.

Why?

First, regulation.

Second, even if regulatory issues were resolved, building the necessary infrastructure stack is non-trivial.

And even if both issues were solved, if each chain issues its own stablecoin in isolation, we face another challenge: fragmentation. Cross-chain users would be forced to juggle many different stablecoins, degrading UX and interoperability. This is why Tether and Circle have effectively dominated the market as a duopoly.

But what if:

stablecoin regulation became clearer,

foundations could easily issue their own stablecoins via shared infrastructure, and

those stablecoins were interoperable across chains?

Then we could see a new paradigm where new smart contract platforms no longer need to rely solely on Tether and Circle.

On the regulatory front, the U.S. has been moving toward clarity through legislation like the Genius bill for stablecoins. On the infrastructure side, a key development has been Bridge, acquired by Stripe, which now offers stablecoin issuance infrastructure.

Thanks to this, foundations can now act primarily as issuers, while Bridge handles:

legal and compliance,

custody,

and payment infrastructure.

This is effectively a “Stablecoin-as-a-Service” model. Using this setup, foundations can now issue their own stablecoins much more easily.

Even more importantly, stablecoins issued through Bridge’s infrastructure can be designed to be mutually interoperable across chains. This neatly addresses the fragmentation concern mentioned earlier.

If this model takes hold, Tether and Circle may one day find themselves competing directly against a broad array of Bridge-based stablecoin issuers.

The next question is: what happens to the profits from issuing these stablecoins?

Projects like Sui, which are planning to use Bridge to launch their own stablecoins, have indicated that all profits from stablecoin issuance will be recycled back into their ecosystems. This represents a clear intent to reclaim the value that previously accrued to Tether and Circle and redirect it toward their own communities.

If so, then the scale and usage of a platform’s native stablecoin will become a crucial metric for evaluating that platform’s intrinsic value.

Currently, chains that have either launched or announced plans to launch native stablecoins include:

Hyperliquid (USDH)

Sui (USDsui)

MegaETH (USDM)

I expect this list to grow significantly over the next year. Over a longer horizon, I believe the aggregate scale of Bridge-powered stablecoins could realistically grow to a level that challenges Tether and Circle.

Dive into 'Narratives' that will be important in the next year