Prices in prediction markets are not mere trade outcomes but public probability signals that compress the information participants are willing to back with capital.

Because financial incentives force people to reveal their actual beliefs rather than their stated opinions, prediction markets often produce signals that outperform polls and expert commentary.

These markets operate most effectively when information updates continuously, participation is recurrent, and the event has real economic or social weight.

Unlike gambling, which generates outcomes detached from reality, prediction markets turn wagering into an information-producing mechanism whose output can be reused and analyzed.

They also separate probabilistic exposure from the complex derivative structures that traditionally embed it, offering a cleaner and more direct way to express uncertainty.

Volume, open interest, and user activity all indicate that prediction markets have achieved product–market fit, with Polymarket and Kalshi forming the core of the ecosystem’s liquidity and participation.

As large consumer platforms integrate prediction markets into their own workflows, the center of value capture is beginning to shift from venue infrastructure toward the distribution layer that controls user flow.

The path forward hinges on resolving oracle fragility, improving capital efficiency for long-dated markets, and introducing leverage primitives that expand how belief can be expressed.

When I began writing this piece, the first challenge was simply getting a clear picture of prediction markets. The information exists, but it is fractured across academic papers, builder docs, sports-betting analogies, forum threads, and half-formed explanations on CT. What’s missing is a single coherent view of what these markets actually are and what they enable.

After spending weeks inside the architecture, it becomes obvious that prediction markets are not a novelty or a clever betting interface. They are a financial primitive with a much wider natural scope than the form they currently take.

If prediction markets grow into something significant, it won’t be because they make speculation easier. It will be because they offer a way to turn belief into a measurable public signal. Robin Hanson captured this years ago in his piece Futarchy: Vote Values, But Bet Beliefs:

“Speculative markets pay anyone who sees a bias in current prices to come and correct it.”

That sentence anchors the entire report. Prediction markets convert information into action, and action into price. The mechanism is simple, but the implications are profound.

This piece is an attempt to map that mechanism — how prediction markets work today, how they can scale, and what a world built around priced belief might look like.

"You make money if you're right. You lose money if you're wrong. And as a result, it creates this information that's really useful for people. (Polymarket) is the most accurate thing we have as mankind right now, until someone else creates some sort of a super crystal ball."

- Shayne Coplan, Founder & CEO of Polymarket

Charlie Munger once joked that he spent his whole life understanding the power of incentives and still managed to underestimate it.

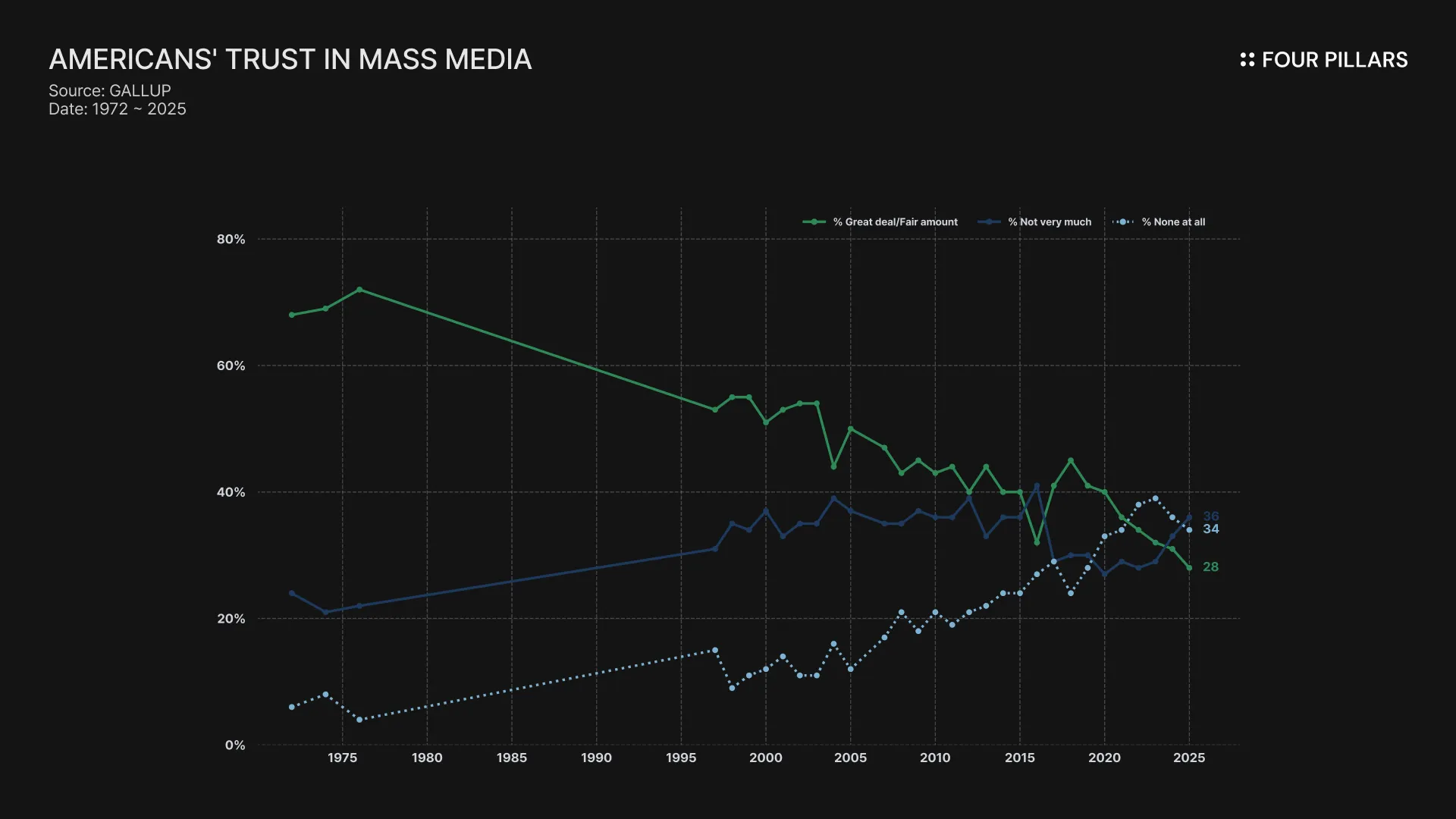

Saying and doing are different things. Social media and newspapers show what people say; prediction markets show what people actually believe. Once someone can wager on an outcome, their private expectation becomes public information. The price becomes a compressed record of those beliefs.

Money is one of the few places people don’t lie. When expressing a view requires staking capital, the noise falls away. What remains is a probability shaped by the information each participant is willing to back with risk.

Hayek’s 1945 essay The Use of Knowledge in Society formalized this idea. Most useful knowledge is dispersed — local, contextual, and unavailable to any central authority. A price aggregates these fragments because each movement reflects someone acting on information only they had. Markets coordinate this dispersed knowledge without needing to collect it.

Prediction markets apply this to forecasting. Every event becomes a tradable claim, and the resulting price becomes the implied probability. If a contract trades at 0.55, the market is treating the outcome as 55%. If you believe the probability is higher, you buy; if lower, you sell. Each trade adjusts the collective estimate.

This is why prediction markets often outperform polls, pundits, and models that ignore market data. Polls face structural issues. Response rates across many survey modes have fallen sharply, and pollsters themselves acknowledge the rising risk of nonresponse bias. At the same time, pundits are rewarded for confidence and not calibration. Meanwhile, prediction markets reward accuracy and penalize error.

The Harris–Trump race showed this clearly. Throughout late summer and early fall of 2024, major polling averages and media coverage described the race as effectively tied, with Harris holding a slight edge. Prediction markets disagreed. Platforms including Polymarket steadily priced Trump as the favorite, and by late October coverage was openly discussing the gap between polling and market pricing. Polymarket saw billions of dollars traded on the election and ultimately resolved to Trump after he won.

Source: Polymarket

What drives these outcomes? As traders update their views and take the other side of one another’s positions, the price converges toward the point where private information meets collective belief. That equilibrium is a weighted bet on the future, priced by people with skin in the game.

Gambling is not a useful category if you care about how information moves. Poker, sports betting, perps, and prediction markets all involve putting money behind a belief about uncertainty. The real distinction is that some systems are designed so that the byproduct of speculation is a public, reusable probability signal. Others are designed so that the byproduct is just house revenue.

At the pure gambling end are closed games like roulette or slots. The odds are fixed, the edge is baked in, and the randomness lives entirely inside the game. Players may have preferences or superstitions, but when the wheel stops spinning, nothing has been learned about the outside world. The information died at the table.

Sports betting already sits closer to prediction markets. A moneyline on an NFL game or a total in the NBA playoffs is a live estimate of how likely a particular outcome is, given all available information. Sharp books and exchanges do, in practice, function as information markets. Syndicates, quants, and fans push odds until they roughly reflect collective belief. That is why economists and forecasters often use sports odds as data.

Prediction markets generalize this structure and extend it:

The underlying is always an explicit real-world event. An election, a policy decision, a macro print, a protocol upgrade.

Both sides are tradeable. You can buy “YES” or effectively buy “NO,” and exit before resolution. You are not just a customer against a house; you are one side of an order book against other traders.

Fees are kept low enough that tiny mispricings are worth trading. This is what makes fine-grained information extraction possible.

Prices are treated as public forecasts.

Poker and casino games can be highly skill-based, but they remain closed loops: information goes in, money and ego come out, nothing is left behind for anyone else. Sports betting sits in the middle. In its sharpest venues, it effectively becomes a single-domain prediction market; in others, it is simply a high-rake entertainment product.

Prediction markets are built on purpose to sit on the “information market” end of that spectrum. They take the same basic human behavior (betting on uncertainty) and wire it into a mechanism where the side effect is a live, auditable probability surface the rest of the world can use.

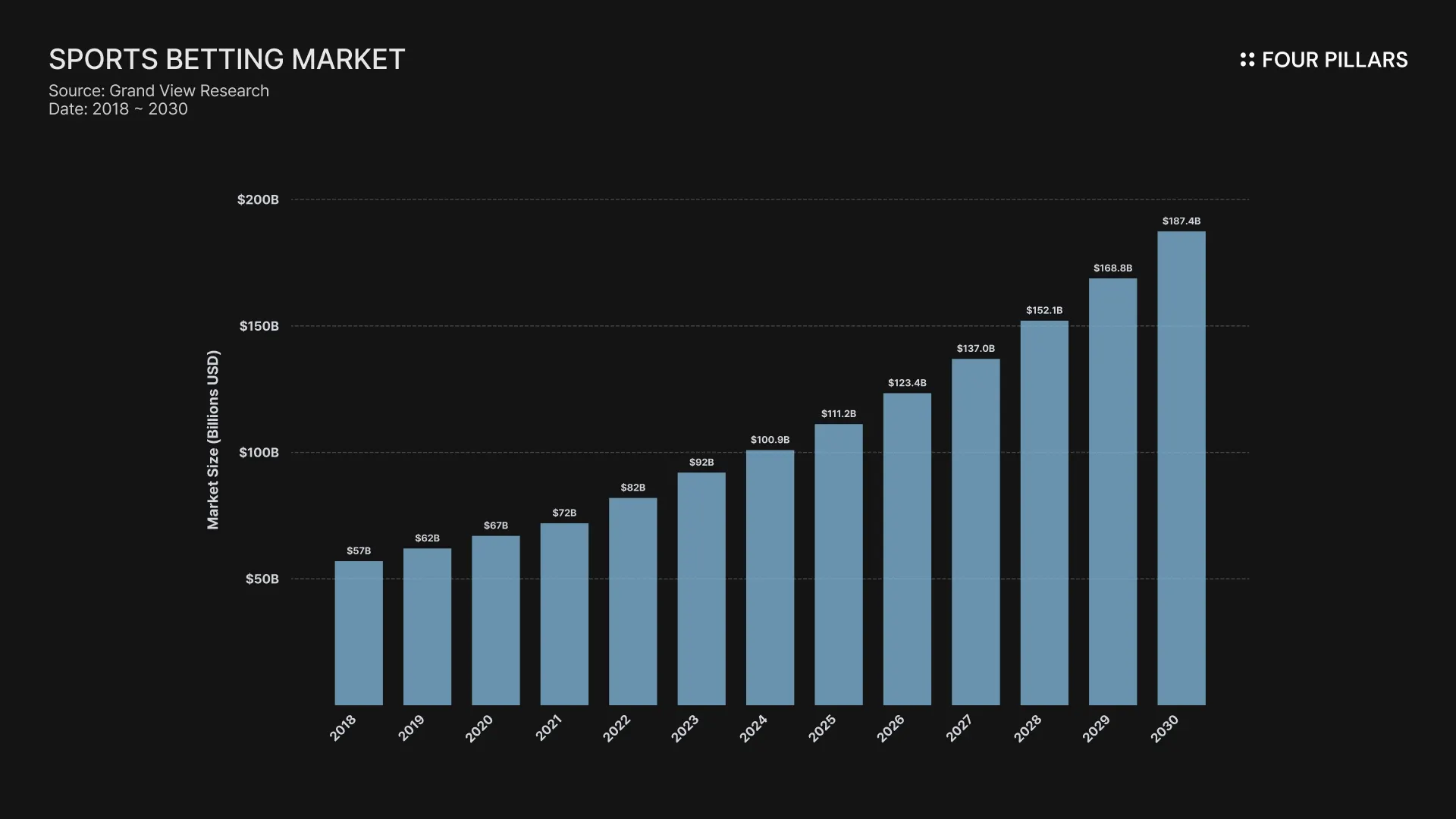

The global sports betting market alone is roughly $100 billion today and projected to approach $187 billion by 2030. The question is not whether people will bet; they already do. The question is whether we can harness that behavior to produce something socially useful.

None of this makes them safe or morally superior. People can and do overbet their beliefs. The point is narrower: if people are going to stake money on what they think will happen regardless, we can at least design the system so that the outcome is more than P&L and house rake. We can obtain a public measure of belief about the future.

Prediction markets have a reputation for being “wrong” whenever a high-probability event doesn’t happen. But that’s not how you evaluate a probability system. A contract trading at 0.70 isn’t claiming the outcome will happen. It’s claiming it will happen 70% of the time across many similar events.

The only proper test is calibration. When markets say 70%, does reality land around 70% over a large sample? Across election markets, corporate forecasting experiments, and academic studies, the answer has generally been yes.

Where prediction markets do run into trouble is market structure. A market is only as good as the information and incentives inside it. Thick markets, with lots of participants, meaningful capital, diverse information, tend to be well-calibrated. Thin markets are the opposite. They attract a few motivated traders but not enough depth to stabilize the price, so idiosyncratic opinions can move the line more than they should.

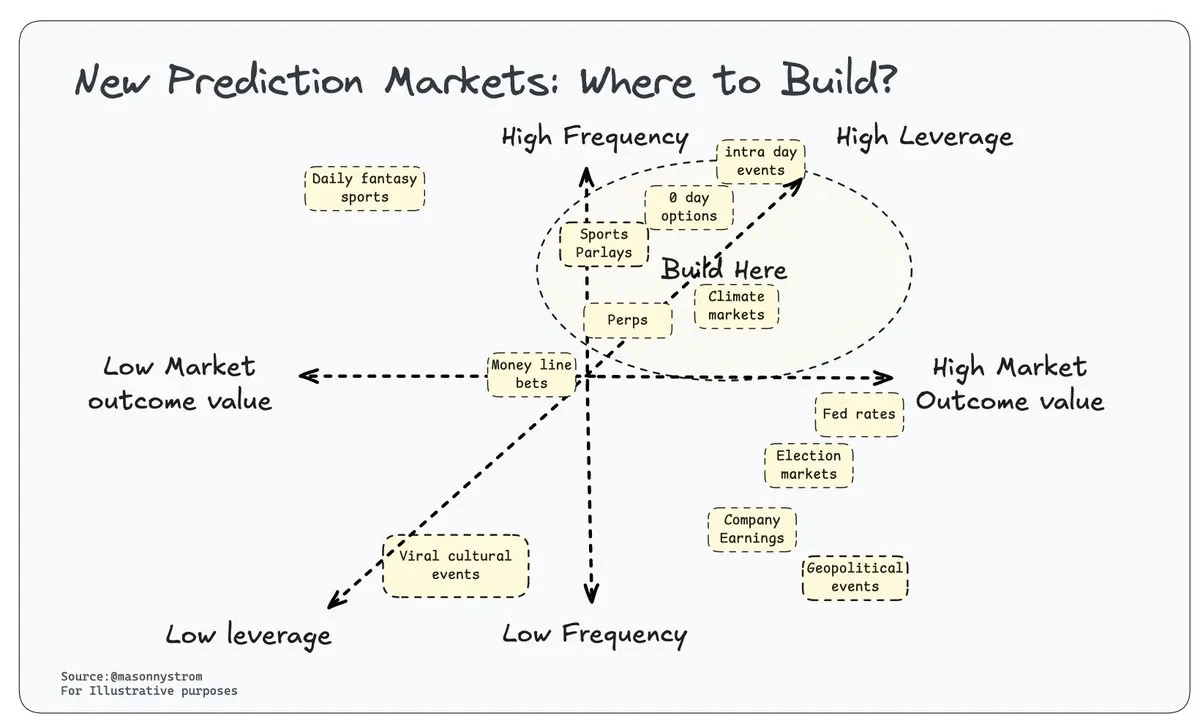

Mason Nystrom from Pantera Capital made this point clearly: different prediction markets perform differently depending on the type of event and the structure around it. High-leverage products (like parlays or intraday markets), highly frequent events (which bring users back repeatedly), and high-value outcomes (like elections or major macro prints) all create the conditions for thicker, more reliable markets. Essentially, these features shape how much information the market can actually extract.

Source: X (@masonnystrom)

This is why some contracts look erratic or off. Many events simply don’t have natural hedgers or institutional participants. Nobody needs to hedge the probability of a presidential debate happening or a streamer mentioning a specific word. Without organic demand, markets rely on speculators alone, which makes them structurally thinner and more volatile.

Prediction markets don’t eliminate uncertainty, and they don’t replace careful reasoning. Their job is narrower. Take the information traders bring, weight it by conviction and risk, and produce a number that reflects the current distribution of beliefs. When markets deviate, it’s usually a sign of thin liquidity or poor incentives, not a failure of the mechanism itself.

Most of finance looks complicated because it has accumulated decades of structure, regulation, and jargon. But underneath that surface, a surprising amount of it reduces to the same primitive—it creates places where people can express beliefs about the future and attach consequences to those beliefs. Prices move because expectations change. Instruments exist because different participants want different ways to formalize those expectations. Once you look through that perspective, the distance between traditional markets and prediction markets becomes much smaller.

Over time, each corner of finance developed its own specialized machinery for expressing these beliefs: valuation models, settlement conventions, margin systems, industry-specific contract designs. The structure varies, but the logic is the same. Someone thinks the world will look one way; someone else thinks it will look another; a market forms to let them meet.

Source: CMEGroup

All of these instruments take different legal forms and live inside different regulatory boxes, but they share the same underlying structure. Someone pays because they believe the probability of a future event is mispriced. Traditional markets wrap these questions in contracts, intermediaries, and settlement rules.

Prediction markets expose the underlying interaction directly. Once everything is expressed as a state-dependent claim, you can see that a huge share of financial activity is already about pricing probabilities. Prediction markets just make that explicit and frictionless. Instead of hiding a forecast inside a complex instrument, the forecast is the thing being traded.

This section naturally extends the idea from 3.1. One reason prediction markets spread quickly in crypto is that they match the mental model traders already use. Once you reduce most financial instruments to simple state-dependent questions, it becomes obvious why traders gravitate toward primitives that express those states directly.

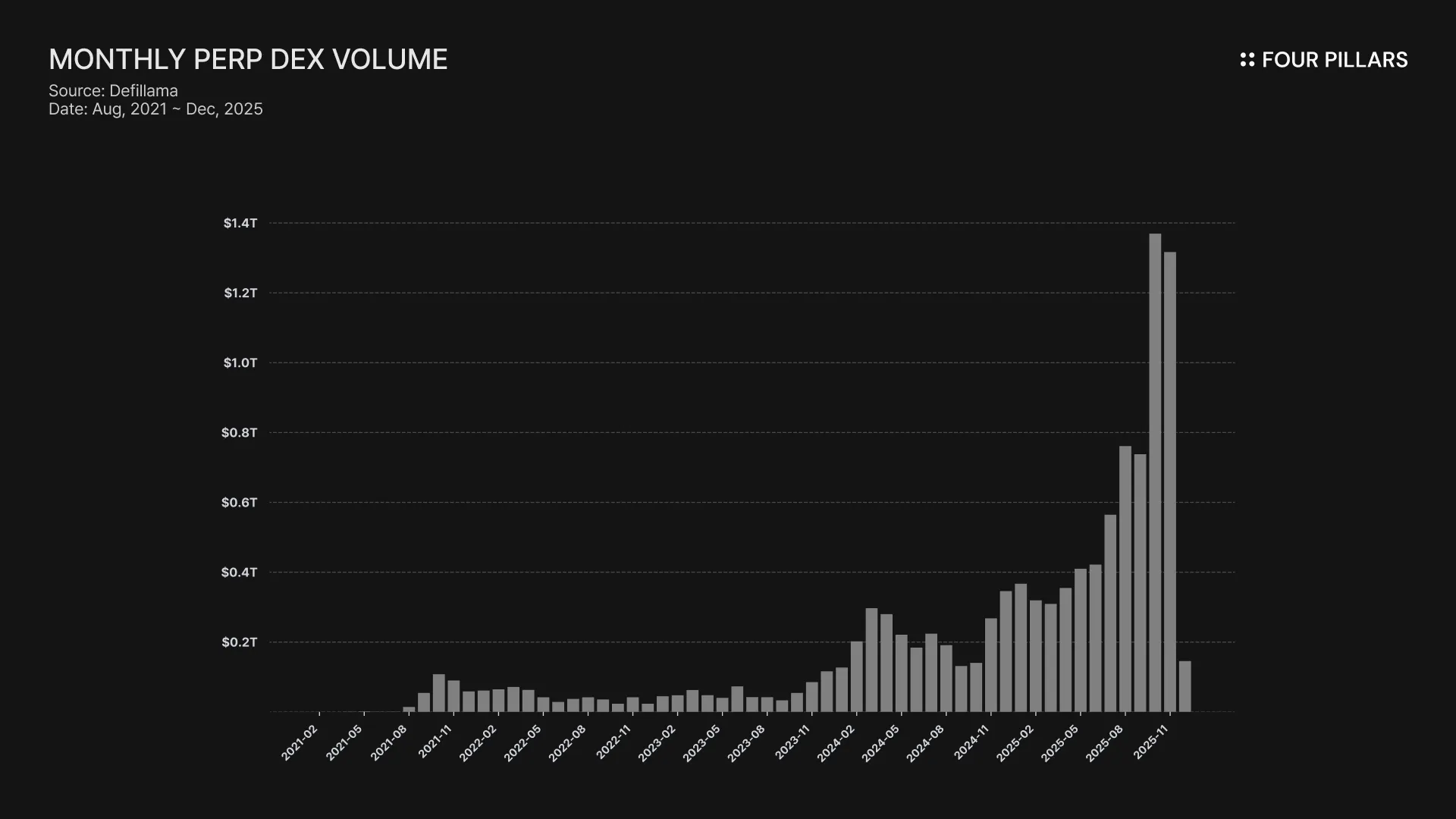

Perps became dominant because they stripped away the complexity of traditional options. No expiry, margin for capital efficiency, and 24/7 access. You express a view and you size it. Simple. It’s why perps grew from a niche product to more than $1.3 trillion in monthly volume last month.

Prediction markets work the same way. A YES/NO contract is the cleanest expression of a directional belief. If you think the event is more likely than the price implies, you buy. If you think it’s less likely, you sell. Essentially, the interface is a single line that maps directly to probability. That simplicity is why retail traders pick it up immediately.

It also lets you express or hedge views that would be awkward or expensive in traditional markets. Hedging a low probability geopolitical risk through options would require a combination of OTM puts, timing decisions, margin management, and implied-vol calculations. Meanwhile, a prediction market reduces that entire structure to one question: yes or no? It’s a hedge, a speculative bet, or a conviction trade, all in one primitive.

This doesn’t mean prediction markets replace options or futures. It just means that for many real-world questions (political events, macro prints, sports outcomes, protocol upgrades, etc.) the simplest possible structure often captures the intended exposure better than a stack of derivatives.

Traders don’t need to translate their view into an instrument. The instrument already matches the view.

Prediction markets let traders express more than single-directional views. They let you express how events relate to one another without requiring the layers of engineering that traditional derivatives demand (h/t to Tulip King, whose Prediction Market Supercycle framed this idea sharply and is worth reading if you want a deeper dive).

Source: X (@0xTulipKing)

Most financial instruments force you to compress a complex worldview into a single directional bet. You might believe a company will beat earnings but still sell off, or that an airdrop won’t happen but the token will drop for other reasons, or that a macro event will affect one asset but not another. Options can express parts of those ideas, but only through combinations of strikes, expiries, and spreads. It’s workable, but it's not natural.

Prediction markets, on the other hand, is free from this constraint. Because every event is a standalone contract, you can express views across multiple dimensions without engineering a payoff structure. A trader can buy “YES” on NVDA beats earnings and “YES” on NVDA trades lower the next day — a position that reflects a clear view about expectations versus reaction, but which would require a messy options structure in traditional markets.

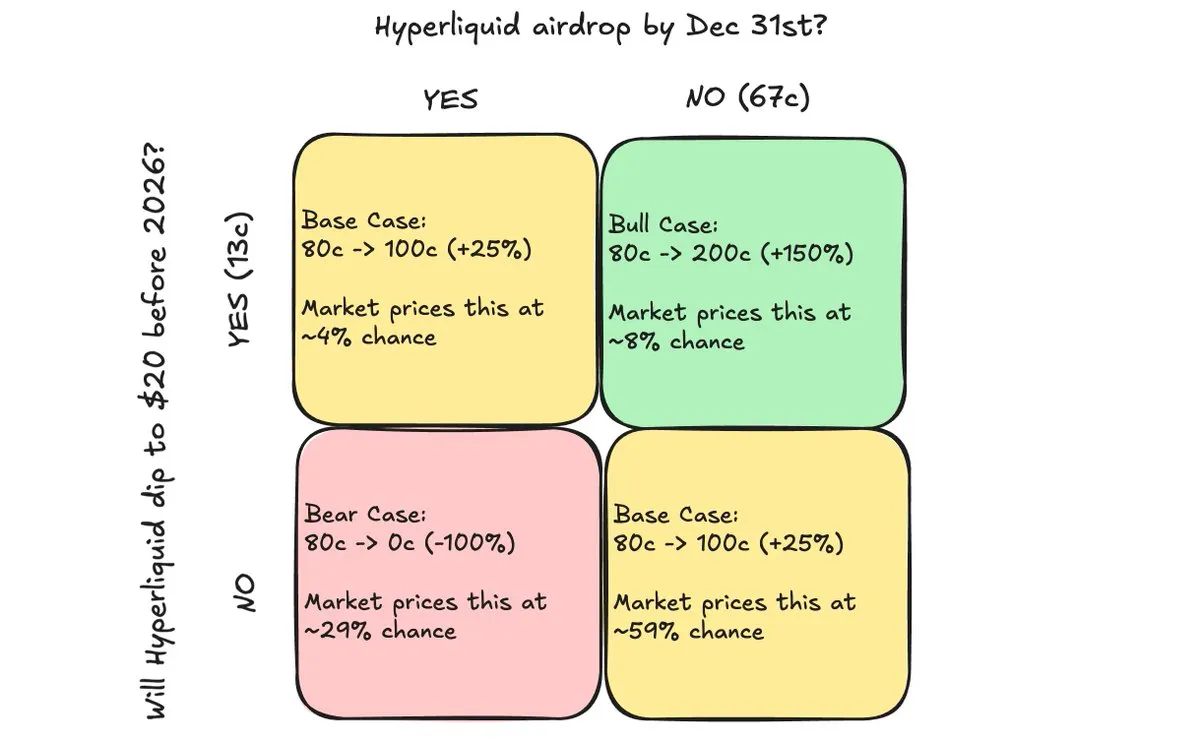

The same applies on-chain. A simple example is Hyperliquid: a trader could buy “NO” on Hyperliquid airdrop by Dec 31 while also buying “YES” on Hyperliquid dips below $20 before 2026. The payoff matrix captures a view about supply shocks, sentiment, and market structure. Instead of bundling this into spreads or calendar structures, a trader builds it directly from primitives.

This flexibility scales. You can pair political events with macro prints, protocol votes with token flows, or weather outcomes with commodity prices. The market becomes a canvas for expressing how different events interact. Correlation (something traders usually infer indirectly) becomes a first-class object you can trade explicitly.

None of this exists to make markets more complex. It’s the opposite. Prediction markets let traders express worldviews in a way that matches how they actually think. Rather than forcing everything through the lens of a single asset price, they let you trade the relationships between events themselves.

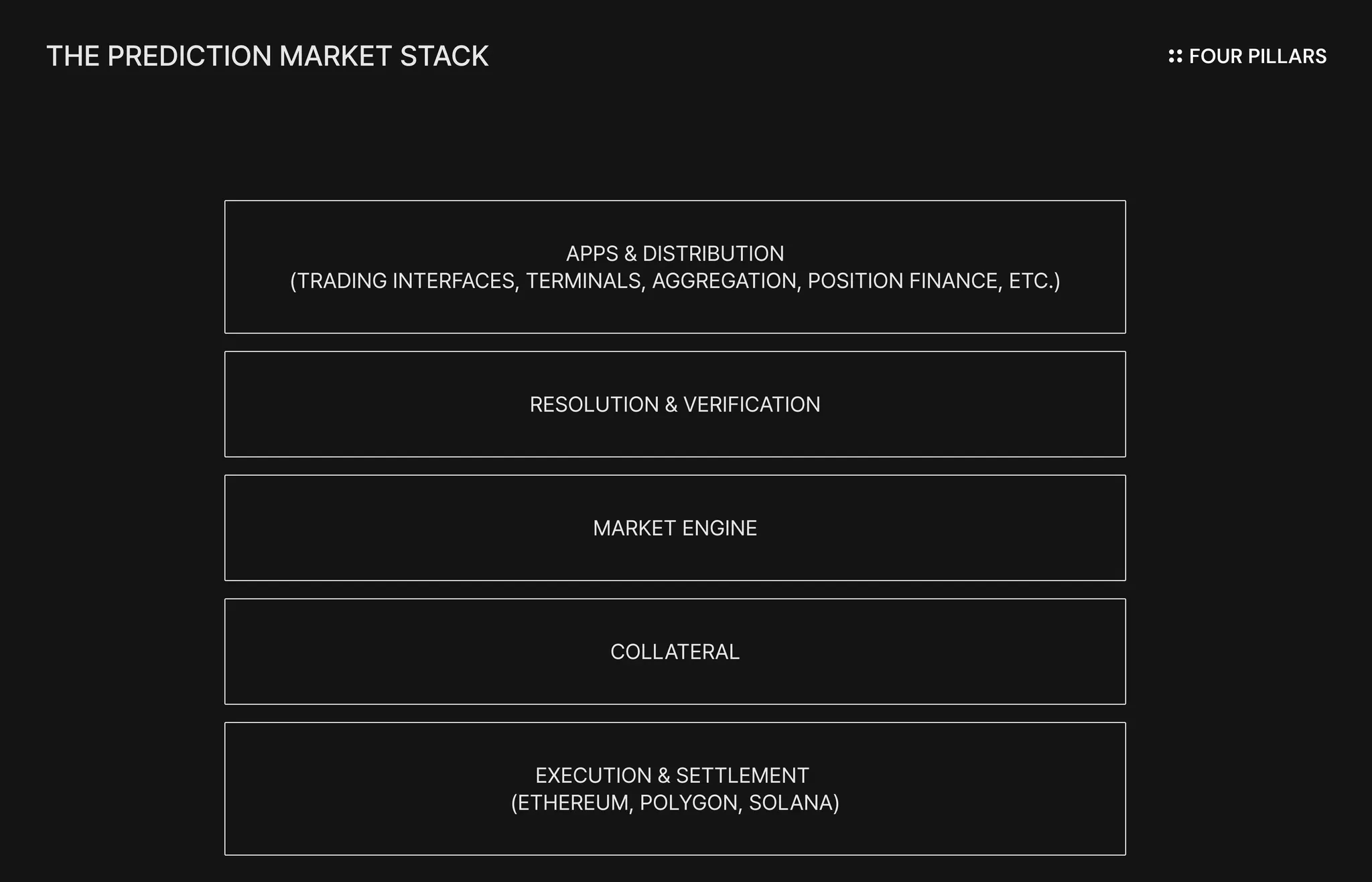

The stack described in this section is framed primarily through the architectures of Polymarket and Kalshi. In practice, they are the only prediction markets operating at meaningful scale today, and their design choices define the design space the rest of the ecosystem builds around.

Before breaking down the stack, it’s worth clarifying why blockchains show up at all in modern prediction markets:

Open access: Blockchains allow anyone, anywhere, to participate without relying on domestic banking systems. More participants mean thicker markets and better price discovery.

Verifiable settlement: Onchain settlement makes market state observable, auditable, and hard to tamper with. This avoids operational disputes and reduces trust in intermediaries.

Enforced commitments: Smart contracts lock collateral, execute trades, and settle payouts without discretionary intervention. That solves the commitment risk in prediction markets.

Composability: Onchain positions become programmable assets. Apps can borrow against them, stake them, bundle them, or route them into automated strategies.

Machine-native participation: AI agents can trade directly onchain without accounts or permission. This expands who can provide information to the market.

Neutral rails: Public chains operate outside any single jurisdiction’s infrastructure. For global prediction markets, neutral settlement avoids relying on one country’s legal system.

Decentralization also plays a role. It reduces single points of failure around resolution and provides a neutral environment during periods when events or payouts may be sensitive.

Blockchains don’t replace the entire stack. But they provide the foundational properties (open access, verifiable settlement, enforced commitments) that make global, programmable prediction markets possible. With that in mind, we can walk through the stack itself.

Execution architecture determines where balances live, how trades settle, what collateral is usable (today: USD and USDC), how fast markets can update, how composable positions are, and what trust assumptions users inherit.

Currently, prediction markets span both onchain and offchain execution environments. Onchain systems trade flexibility for performance; offchain systems trade composability for regulatory clarity. These design choices ripple upward into the collateral layer, market engine, resolution mechanisms, and the applications built on top.

4.2.1 Onchain Execution (e.g. Ethereum, Polygon, Solana)

Platforms like Polymarket settle trades directly on public blockchains like Polygon using USDC as collateral. Balances, positions, and market states live on-chain, usually as ERC-1155 tokens. Deposits from other chains or assets are ultimately bridged or swapped into USDC on the settlement chain.

This model favors transparency and composability. Any downstream application can inspect positions or treat them as collateral. The tradeoff is that performance, latency, and fees are tied to the underlying chain, which shapes how fast markets can update and how much volume they can handle.

4.2.2 Offchain Execution (e.g. Kalshi Clearinghouse)

Kalshi operates under a regulated derivatives-exchange architecture. Its clearinghouse records USD and USDC balances internally and processes matches, fills, and settlement within its own ledger. Onchain tokenization on Solana provides an external representation of positions, but the clearinghouse remains the authoritative source of truth. This model enables high throughput and regulatory certainty, but centralizes trust and limits the programmability and permissionless extension that onchain markets enable.

Collateral constrains how markets can grow. It determines friction (bridging, conversion), regulatory pathways, margin mechanics, and the ability to create long-duration markets without introducing yield or mark-to-market complexity. Stable collateral also simplifies the market engine: a YES share and a NO share must sum to one unit of value, and the collateral must reliably hold that peg.

In the future, we may see tokenized T-bills, yield-bearing stablecoins, or natively interest-accruing collateral integrated into this layer. But today, this layer is extremely narrow by design:

Kalshi’s clearinghouse maintains balances in USD and USDC, with USD as the canonical settlement asset. Deposits from a wide range of rails (ACH, card, PayPal, crypto) are converted into cash or custodied USDC inside the clearinghouse ledger. The choice is deliberate: USD enables regulatory compliance, simplifies accounting, and avoids the volatility and risk profiles that would complicate CFTC oversight.

Polymarket uses USDC / USDC.e as its base collateral on Polygon, Base, and other chains. Regardless of how users deposit (ETH, SOL, BTC, stablecoins on other chains) the system bridges or swaps everything into USDC before positions can be taken. This creates a single, stable unit of account across the entire onchain market.

The market engine is the part of the stack traders actually experience. Every match, fill, and price update originates here. It defines liquidity characteristics, expressiveness, fairness, and operational risk. And because prediction markets ultimately encode probabilities, the engine’s structure has an immediate impact on how meaningful those probabilities are.

4.4.1 Orderbook Engines

Most large prediction markets rely on central limit order books (CLOBs). Users place bids and asks, the engine matches them, and the best available price becomes the market’s quote. The design choices underneath (tick sizes, fee structure, matching logic, cancellation rules) shape liquidity and trading behavior.

Polymarket uses a hybrid CLOB, where sequences and matches occur off-chain while settlement is enforced on-chain through signed messages. This reduces latency and cost without sacrificing non-custodial settlement. Orders are market/limit orders, with makers providing liquidity and takers filling them; matching follows first-in-first-out priority within price levels. Prices are calculated as the implied probability from the matched bid and ask (e.g., a YES order at $0.60 matches a NO at $0.40, setting the market price at 60% probability for YES).

Kalshi runs a fully off-chain CLOB governed by its clearinghouse, enabling high throughput, low latency, and strict compliance with CFTC rules. It supports limit and market orders, with matching based on price-time priority. Prices range from 1¢ to 99¢, directly reflecting probability.

A practical difference emerges in their API design. Polymarket exposes lightweight REST/WebSocket endpoints suitable for automated trading and bots, while Kalshi’s API is more structured and compliance-gated, mirroring traditional derivatives venues. This affects who can participate programmatically and how liquidity forms around each engine.

While CLOBs dominate because they support precision and tight spreads, new entrants experiment with alternative mechanisms that prioritize accessibility or virality.

Melee uses a bonding-curve model similar to AMMs. Prices move automatically along a curve as users buy or sell outcome tokens, echoing the dynamics of meme-token launches on platforms like Pump.fun. This makes market creation permissionless and social, though spreads are wider and execution is less precise.

Similarly, Myriad runs AMM-based markets across Abstract, BNB Chain, and Linea. Liquidity pools rebalance prices algorithmically for binary and multi-outcome markets across sports, crypto, and macro. AMMs guarantee continuous liquidity but introduce slippage when pools are thin.

Historically, platforms like Polymarket and Limitless initially relied on AMMs but transitioned to CLOBs in recent years (Polymarket in late 2022 and Limitless in 2025) to achieve better execution and depth amid explosive user growth; older protocols such as Augur and Gnosis used AMM variants like the Logarithmic Market Scoring Rule (LMSR) but have seen reduced activity in the current landscape.

On the innovation front, Paradigm proposed pm-AMM in late 2024, a specialized AMM tailored for prediction markets to enhance uniformity and efficiency over traditional designs, though it remains in early adoption stages and signals ongoing experimentation in the space.

4.4.2 Event Structure

The engine also determines the types of events that can be traded. Binary outcomes (YES/NO) are the core primitive, but platforms extend this to categorical markets (multiple discrete choices), date-based expiries, and scalar markets tied to numerical ranges.

Polymarket embraces a wide range, including intraday markets that expire within hours (great for fast-moving events like sports games) and rolling markets that reset daily or weekly for ongoing trends. Kalshi sticks to verifiable structures like binaries tied to official data, avoiding more complex or leveraged setups. This variety lets you express detailed views but it also demands strong, well designed backend systems to manage the added rules and resolutions without confusion.

4.4.3 Risk and Margin

The market engine enforces collateral requirements, handles partial fills, and computes maximum exposure. In Kalshi, every contract is fully collateralized at $1 with no leverage. Buyers post the purchase price, sellers the complement, ensuring no margin calls or liquidation risk. Polymarket mirrors this logic with USDC-backed YES/NO tokens, requiring full collateral for positions; partial fills are supported in the orderbook, but exposure is capped at the staked amount.

Simpler collateralization rules reduce systemic risk but limit product innovation. Introducing leverage or partial collateralization requires more complex risk engines, which is why most prediction markets avoid them today.

4.4.4 Market Creation

Engines differ in who can list markets. Kalshi uses a permissioned model with strict rules for contract definitions and verifiable outcomes—markets must specify resolution sources (e.g., official data feeds) and undergo internal review for CFTC compliance before listing.

Polymarket is more flexible, allowing rapid listing of trending events as long as the oracle and contract specifications meet platform criteria. Users propose markets via the interface, with approval based on UMA oracle feasibility and event verifiability.

In contrast, platforms like Melee and Opinion enable fully permissionless creation, where anyone can launch opinion-based or sentiment-driven questions without prior review, fostering viral growth but relying on community moderation to filter low-quality listings.

Market creation models determine how fast the market universe grows and how quickly prediction markets can respond to real-world events.

Prediction markets only work if someone can say, with authority, what actually happened. The resolution layer provides that trust. It determines how outcomes are validated, how disputes are handled, and when funds can be released. A legally supervised resolver offers clarity and enforceability; a decentralized resolver enables permissionless market creation and global access but depends on honest participation and proper incentive alignment.

4.5.1 Off-chain Resolution

Kalshi’s resolver is defined entirely by its CFTC-approved rulebook. It is not algorithmic, oracle-based, or token-governed. It is a legal system with three core components:

A. Predefined Outcome Sources

Every Kalshi market includes a “Rules Summary” specifying:

what counts as the outcome

which data source determines it (e.g., BLS, NHC, BEA, Federal Reserve, official election certification)

how edge cases are treated

B. Resolution by Clearinghouse

Kalshi Klear (the clearinghouse) executes final settlement once the official data is released, but it follows the contract’s prescribed outcome source. It does not “interpret” results — it applies them.

No voting, no staking, no challenge windows

The clearinghouse updates all positions according to the rules

Payout is immediate and final under CFTC oversight

C. Exception Handling

The rulebook outlines limited scenarios where Kalshi can adjust or cancel trades—e.g., corrupted data feeds, erroneous publications, or “extraordinary circumstances.” These must follow formal procedures and are subject to regulatory audit.

Any adjustment or cancellation must comply with the procedures in the rulebook and is subject to CFTC oversight.

Kalshi’s clearing-house rulebook enforces full collateralization, segregation of funds, and legally binding settlement, but it does not define which event types are allowed or disallowed. Instead, whether a market can list (e.g. sports, elections, politics, economics) depends on CFTC rulings or state-level gaming regulations. As a result, the permissible universe of event contracts is shaped externally, not by Kalshi’s internal governance.

4.5.2 On-chain Resolution

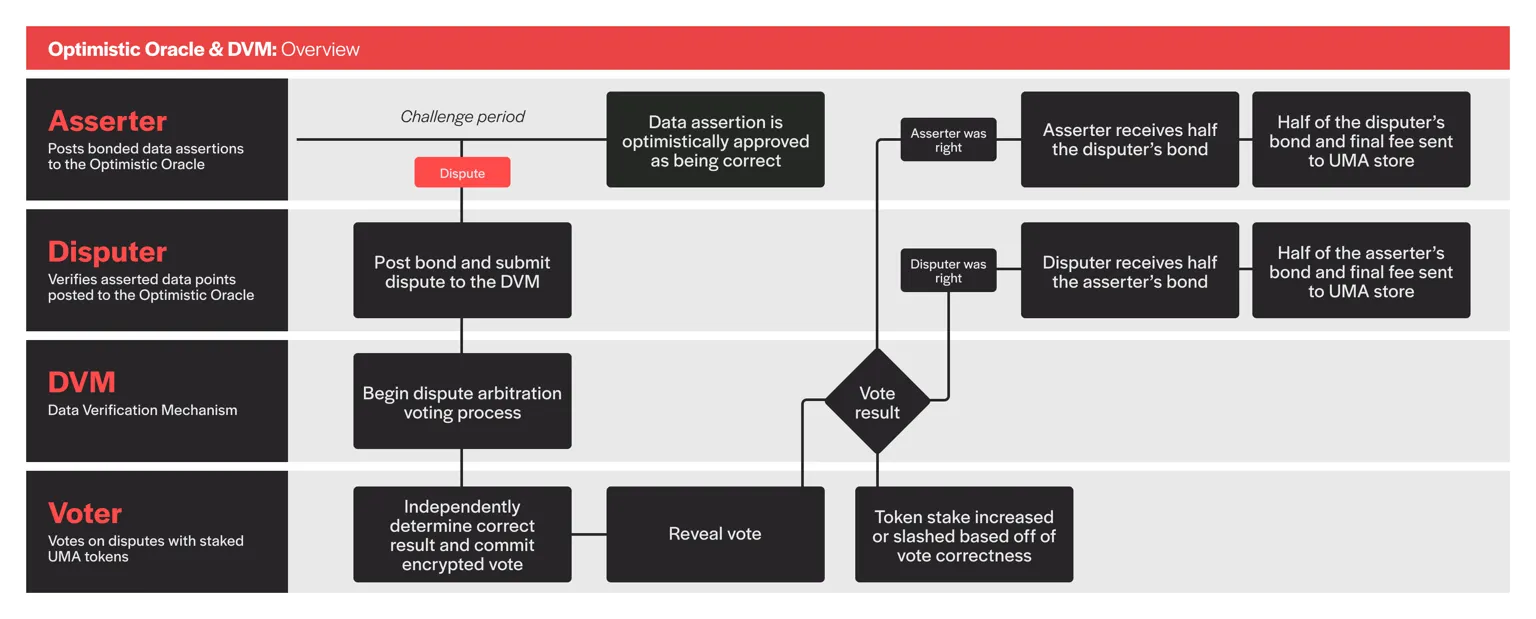

Polymarket relies on UMA’s Optimistic Oracle. UMA resolves markets through an optimistic, economic security model rather than a legal one. Its mechanism has three stages:

Source: UMA docs

A. Propose

After a market’s end condition is met, anyone can publish a proposed answer (e.g., “YES” or “NO”). This is a signed assertion accompanied by a bond.

B. Challenge Window

A dispute window opens (usually hours to days).

If no one disputes the proposal → it becomes final

If challenged → escalation to UMA’s DVM (Data Verification Mechanism)

C. DVM Vote

UMA tokenholders vote on the correct outcome.

Voters are rewarded if they vote with the majority

Challengers lose their bonds if wrong

Proposers lose theirs if the proposal was incorrect

The logic is economic: bad answers are unprofitable, and good answers are rewarded. The system relies on the assumption that honest voting is more profitable than manipulation, allowing permissionless market creation, flexible event definitions, and global accessibility.

Importantly, prediction markets do not need to use UMA. The resolution layer is modular: systems could rely on Chainlink, centralized reporting, specialized committees, or entirely new mechanisms. UMA is simply the design Polymarket currently uses at scale. Its tradeoffs are real, but they sit outside the scope of this stack overview. We return to UMA’s limitations in Section 7.

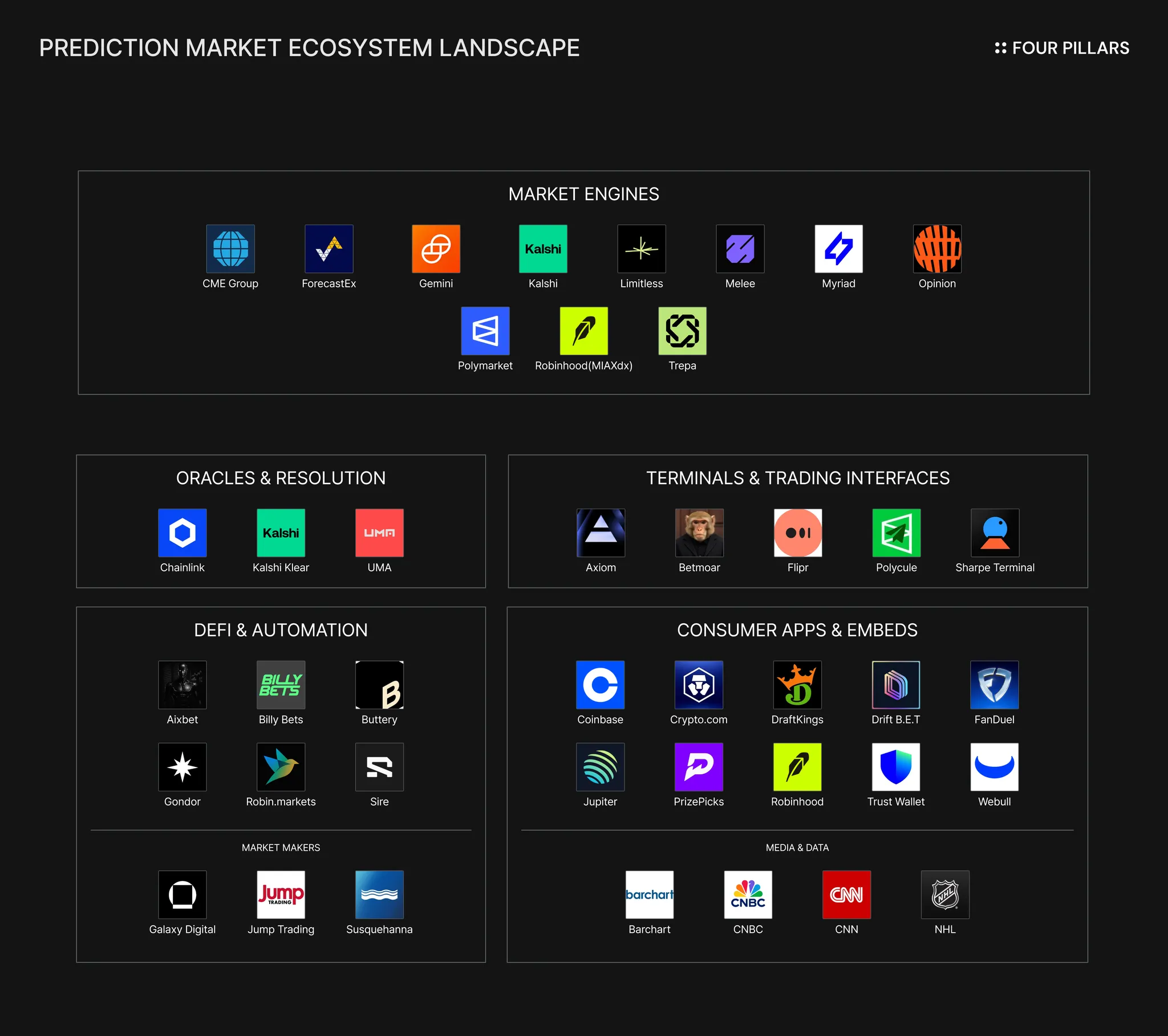

The apps layer sits at the top of the stack and connects users to the underlying market engines. It includes interfaces, terminals, and position-finance tools built on top of Polymarket and Kalshi. Unlike the lower layers, which are tightly concentrated, the app layer is already fragmenting as builders package the engines into specialized workflows.

4.6.1. Trading Interfaces and Terminals

These are frontend applications that route orders into Polymarket’s or Kalshi’s engines:

Trading terminals

Mobile and desktop UIs

Analytics dashboards

Social-embedded interfaces

Vertical-specific sites (e.g., weather, sports, macro)

4.6.2 DeFi

This category includes applications that build on top of prediction-market positions rather than executing trades themselves. These products treat positions as financial primitives that can be lent against, staked for yield, bundled into structured exposures, or used as collateral within broader onchain or offchain systems.

On the regulated side, Kalshi directly offers 3.5% APY on idle balances and certain open positions, showing that yield-bearing PM exposure is not exclusively an on-chain concept. This layer will likely expand as positions become more composable, tokenized, or used as primitives in structured products.

4.6.3 Aggregation and Automation

As APIs mature, bots, arbitrage systems, and AI agents increasingly operate in this layer:

Market-making bots and arbitrage systems

Automated routing engines

Prediction Market Agents (PMAs): AI-driven agents that trade based on user preferences or market analytics (e.g., Aixbet, Sire Agent, BillyBets) (h/t Cookies’ Rise of Prediction Market Agents)

Importantly, Galaxy Digital has already said it is exploring becoming a liquidity provider for both Polymarket and Kalshi. This is an early signal that professional firms will enter PM liquidity formation the same way HFTs and quant desks professionalized CEX and derivatives liquidity. Jump Trading and Susquehanna International Group (SIG) is already acting as a market maker on Kalshi, reinforcing that institutional liquidity provision is starting to take hold.

The space is still early, and many more types of apps and actors will appear as prediction markets mature.

Prediction markets entered 2025 as a marginal category and are leaving it as a regulated financial product with real traction. The biggest shift is that the CFTC now actively supervises the category, and the platforms that matter (Kalshi and Polymarket) operate under this structure in very different ways.

5.1.1 Federal Landscape

Under the Commodity Exchange Act (CEA), event contracts are treated as binary options or swaps, which puts them squarely inside the CFTC’s jurisdiction.

The regulator designates compliant platforms as DCMs (Designated Contract Markets) and, in Kalshi’s case, operates a paired DCO (Derivatives Clearing Organization) through Kalshi Klear. This is the framework that governs everything from margining and settlement to market-integrity rules.

This year saw the most aggressive expansion of the sector in its history:

In January, Kalshi launched sports contracts after a 2024 court win clarifying the legality of event contracts.

In May, the CFTC dropped its appeal against Kalshi’s election-contract approval, effectively ending the multi-year fight and validating Kalshi’s approach.

In July, Polymarket acquired QCX LLC, a CFTC-registered DCM, for $112M, paving the way for its U.S. relaunch. It received full CFTC approval to operate domestically on September 3, including brokered intermediation.

New venues were also approved: Railbird (DCM) and ForecastEX (self-certified sports markets).

The Trump administration’s regulatory posture has been explicitly permissive, framing prediction markets as financial infrastructure rather than gambling products.

5.1.2 Federal–State Conflict

2025 also made clear that federal CFTC supervision does not preempt state gambling laws, especially for sports.

Several states issued cease-and-desist letters (Nevada, New Jersey, Arizona, Arkansas), with mixed court outcomes:

Kalshi won early injunctions

Lost in Maryland and later Nevada (Nov 25), where a judge ruled state gaming laws still apply

The NFL publicly warned league personnel against participating

New York introduced the ORACLE Act, aiming to define when event contracts constitute illegal gambling.

Litigation from gaming associations and tribal entities continues, with no unified precedent on whether CEA preemption applies.

5.1.3 Regulatory Coordination & Uncertainty

In September, the SEC and CFTC held a joint roundtable on harmonizing crypto, derivatives, and prediction market regulation—a sign that the U.S. is moving toward a coherent national framework rather than fragmented enforcement.

Remaining uncertainty includes:

Whether certain PM categories will face federal excise taxes

How to classify event-driven markets for AML/KYC

How to surveil PM-specific risks (wash trading, MNPI misuse, manipulation incentives)

How far CEA authority extends into categories that resemble state-regulated gambling

Despite this, the direction of travel is clear: prediction markets are being absorbed into the derivatives regulatory perimeter, not pushed out of it.

5.1.4 International Landscape

Outside the U.S., regulation is fragmented:

EU & UK generally treat prediction markets as gambling, requiring national gaming licenses; Polymarket has been geo-blocked in France.

Asia is more restrictive. Singapore, South Korea, Philippines, Thailand, Taiwan classify PMs as illegal gambling; Australia cracks down on offshore markets via ACMA.

Offshore hubs like Curaçao continue to host unregulated PM operators.

5.1.5 Where This Leaves the Polymarket–Kalshi Axis

Kalshi operates as a fully regulated financial exchange, expanding aggressively into sports, macro, political events, and foreign elections.

Polymarket operates globally on-chain, now with a compliant U.S. foothold through QCX, and has become the center of crypto-native prediction market infrastructure.

Both paths are viable. But the U.S. market is now large enough that regulation has become the competitive moat, and the axis between Polymarket and Kalshi is defined by regulatory shape as much as by technical design.

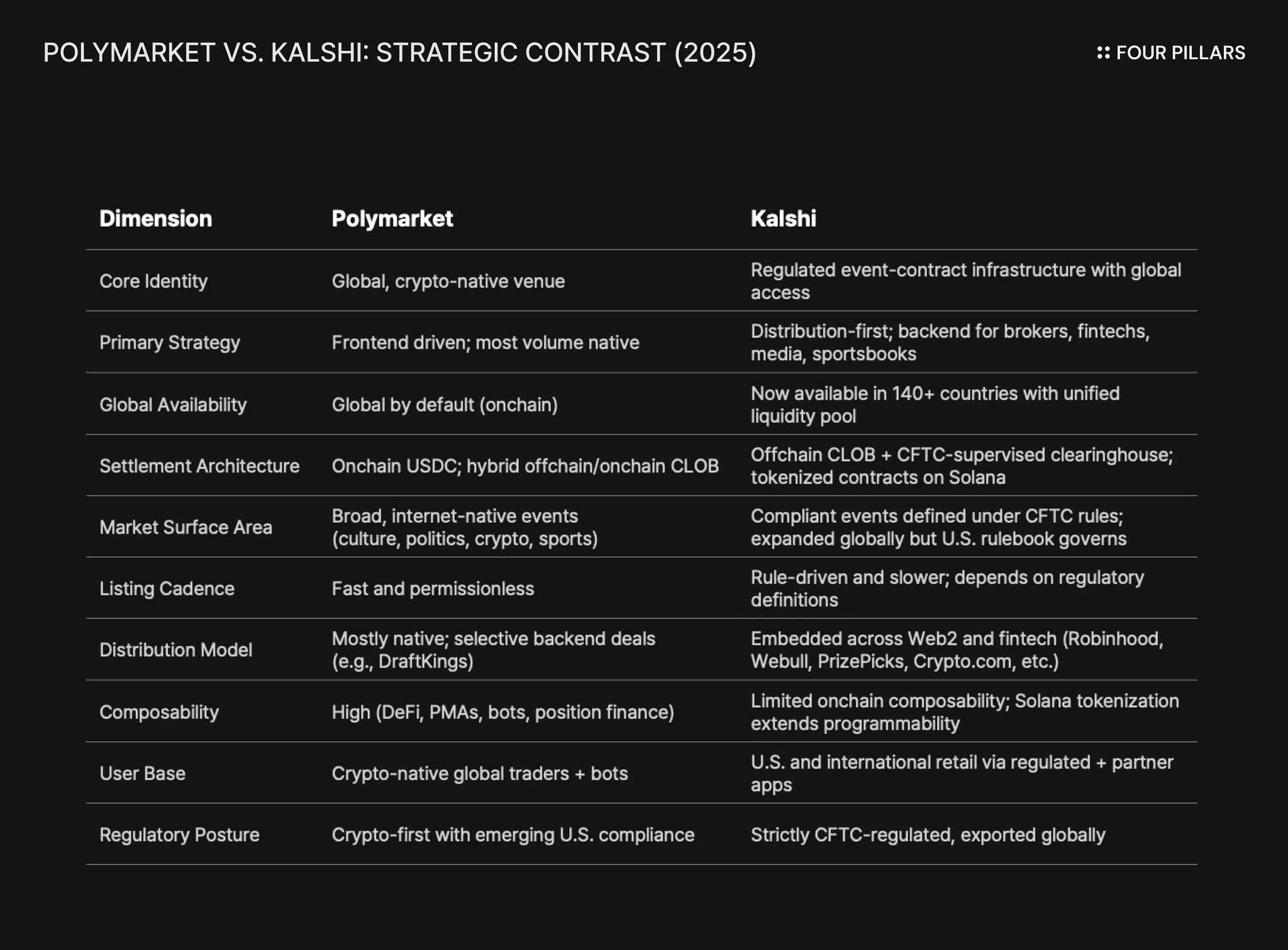

Prediction markets have converged on two dominant strategic models, represented by Polymarket and Kalshi. Both aspire to power external applications, but the degree to which they rely on (or even want) third-party distribution differs sharply. Their product strategies shape who uses the markets, what gets listed, and how each platform positions itself in the broader financial ecosystem.

5.2.1 Polymarket: Global, Crypto-Native, Frontend led, “Internet Events”

Polymarket’s strategy remains anchored in operating as a global, crypto-native venue. The platform’s trading activity is still dominated by its own interface, its own API endpoints, and its own liquidity network. While Polymarket can power external products (as seen in its backend role for DraftKings’ prediction app) the platform has been more cautious about pursuing a full infrastructure-as-a-service model. Its growth continues to come from being the primary destination for retail event trading, not from distributing markets through third-party channels.

Polymarket differentiates itself through a technical and operational posture that favors speed and breadth. Markets settle onchain in USDC, positions are tokenized as ERC-1155 assets, and the hybrid offchain/onchain CLOB enables rapid listing and real-time updates. This architecture supports the full spectrum of “internet events” (politics, culture, sports, macro, crypto sentiment, etc.) and enables downstream programmability.

Developers can build on Polymarket without permission, which has already led to tools such as gondor (lending against PM positions), Robin.markets (position staking), and various automated agents and bots that trade directly through Polymarket’s APIs.

Despite the infrastructure being open and composable, Polymarket’s product identity is still fundamentally frontend led. The platform invests heavily in its own UI, social distribution, category breadth, and retail onboarding.

Backend partnerships exist but are selective; the dominant usage pattern is users trading directly through Polymarket itself. Even with U.S. access returning through QCX, Polymarket’s positioning remains a fast-moving, global-first, permissionless venue.

Where Kalshi is optimizing for embedded distribution, Polymarket is optimizing for surface area, speed, and global retail liquidity. It is the primary destination platform for crypto-native prediction markets, and its backend ambitions, while technically feasible, are not the center of its strategy today.

5.2.2 Kalshi: Regulated, Distribution-First Infrastructure

Meanwhile, Kalshi’s strategy is to become the regulated infrastructure layer for event contracts, and that strategy has recently expanded beyond the United States. Although Kalshi initially operated exclusively as a U.S. CFTC-regulated DCM and clearinghouse, the platform opened international access in October 2025, extending availability to over 140 countries. This rollout introduced a unified global liquidity pool—international users and U.S. users now trade the same markets, improving depth and pricing while keeping settlement anchored in Kalshi’s clearinghouse, provided they satisfy Kalshi’s KYC requirements and comply with local restrictions where applicable. Access is currently blocked or restricted in 38–45 jurisdictions due to local gambling or financial regulations.

Rather than competing for end users directly, Kalshi is leaning into being the backend: a CFTC-regulated DCM with its own clearinghouse, high-integrity settlement, and the regulatory posture required for mainstream fintechs, brokerages, sportsbooks, and media platforms to embed prediction markets safely.

This approach is already visible in the integrations. Robinhood, PrizePicks, Webull, Crypto.com, ProphetX, Coinbase, Trust Wallet, and multiple sportsbooks have either launched or announced products that rely on Kalshi’s rails.

Data and media groups like CNBC, CNN, the NHL, Barchart, and StockX now surface Kalshi’s markets or license event data, while infrastructure partners such as SIG and Coinbase Custody sit behind the system.

The Solana expansion through DFlow and Jupiter extends this model even further. Kalshi becomes a programmable backend for any app that wants prediction markets, while all resolution and settlement remain anchored in Kalshi’s CFTC-supervised clearinghouse. A number of teams (e.g. Axiom, Sharpe Terminal, Meridian, Matchr, Stand.trade) have already expressed interest under this model.

Kalshi has also integrated crypto rails: global users can fund accounts with debit cards or USDC. In recent months, Kalshi has recruited talent from the crypto sector to support these efforts, indicating plans to deepen ties with digital asset communities and integrate into major crypto apps and exchanges within the next 12 months.

Kalshi’s approach is to let the distribution layer fragment, let partners own the UX, and win by being the compliant, low-cost infrastructure beneath them, much like how CME or ICE sit beneath a fragmented ecosystem of brokers, apps, and terminals.

Polymarket may eventually expand into more backend partnerships, but Kalshi is already building its entire product identity around that role.

5.2.3 Business Models

Polymarket generates revenue through minimal trading fees, charging 0.01% on taker orders for U.S. trades post-relaunch while maintaining zero fees globally to prioritize volume growth. It also monetizes data licensing, providing probability feeds to hedge funds and media for event insights.

Additionally, its rewards program incentivizes liquidity by distributing daily USDC pools (e.g., $2,500 for Politics, $1,000 for Sports, $500 for Pop Culture) proportionally to users placing qualifying limit orders within specified spreads (±3–4¢) and minimum sizes (20–50 shares) across categories. This model supports its frontend-led identity, focusing on user acquisition and ecosystem composability over immediate monetization.

Kalshi earns from transaction fees of $0.01–$0.02 per contract (plus 0.25% maker fees on major events), offset by rebates (up to 25~50%) to high-volume partners like Webull or PrizePicks to drive routed flow. This backend-focused model emphasizes low-cost infrastructure, with revenue tied to partner integrations and regulatory compliance to capture a share of the broader event-contract economy.

Fee structures can always change as platforms evolve to adapt to competition or regulation.

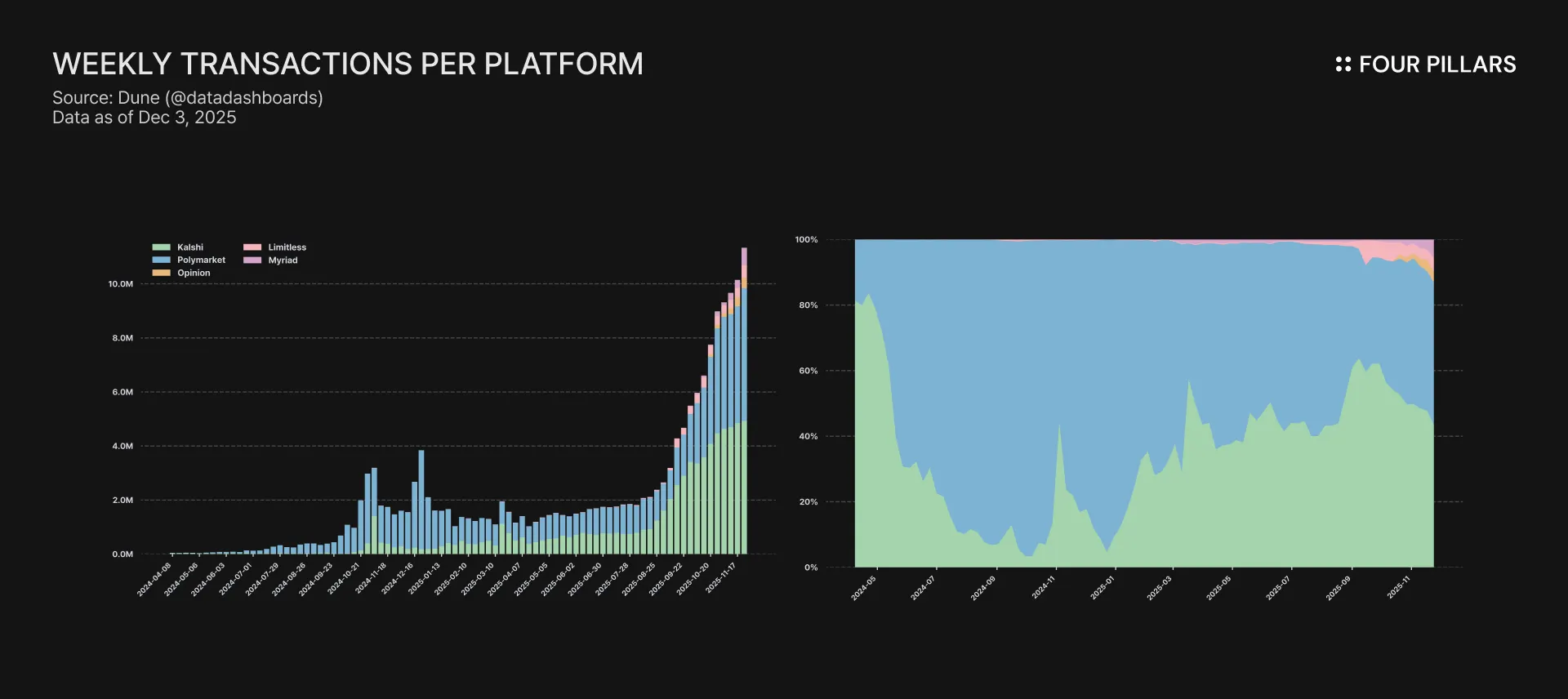

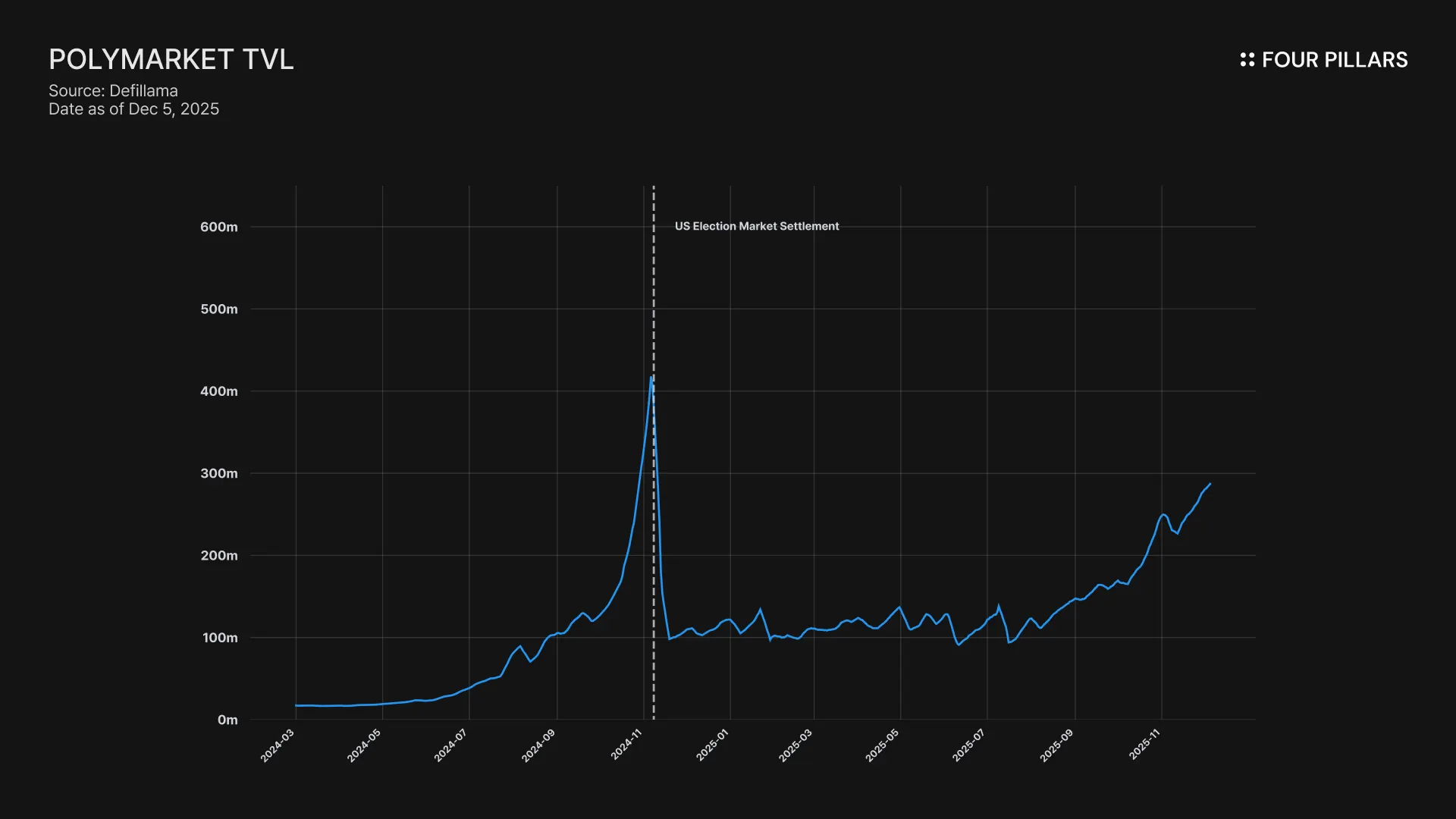

Over the past two years, prediction markets have shifted from episodic bursts of activity (U.S. elections, isolated macro prints, the occasional viral moment) to something closer to a continuously active system. Reported volume, trade counts, open interest, and daily returning users are all materially higher, and activity is now distributed across sports, politics, macro, crypto, and culture rather than clustering around single marquee events. Polymarket and Kalshi anchor most of the liquidity and define the shape of the category today.

5.3.1 Market Size and Growth

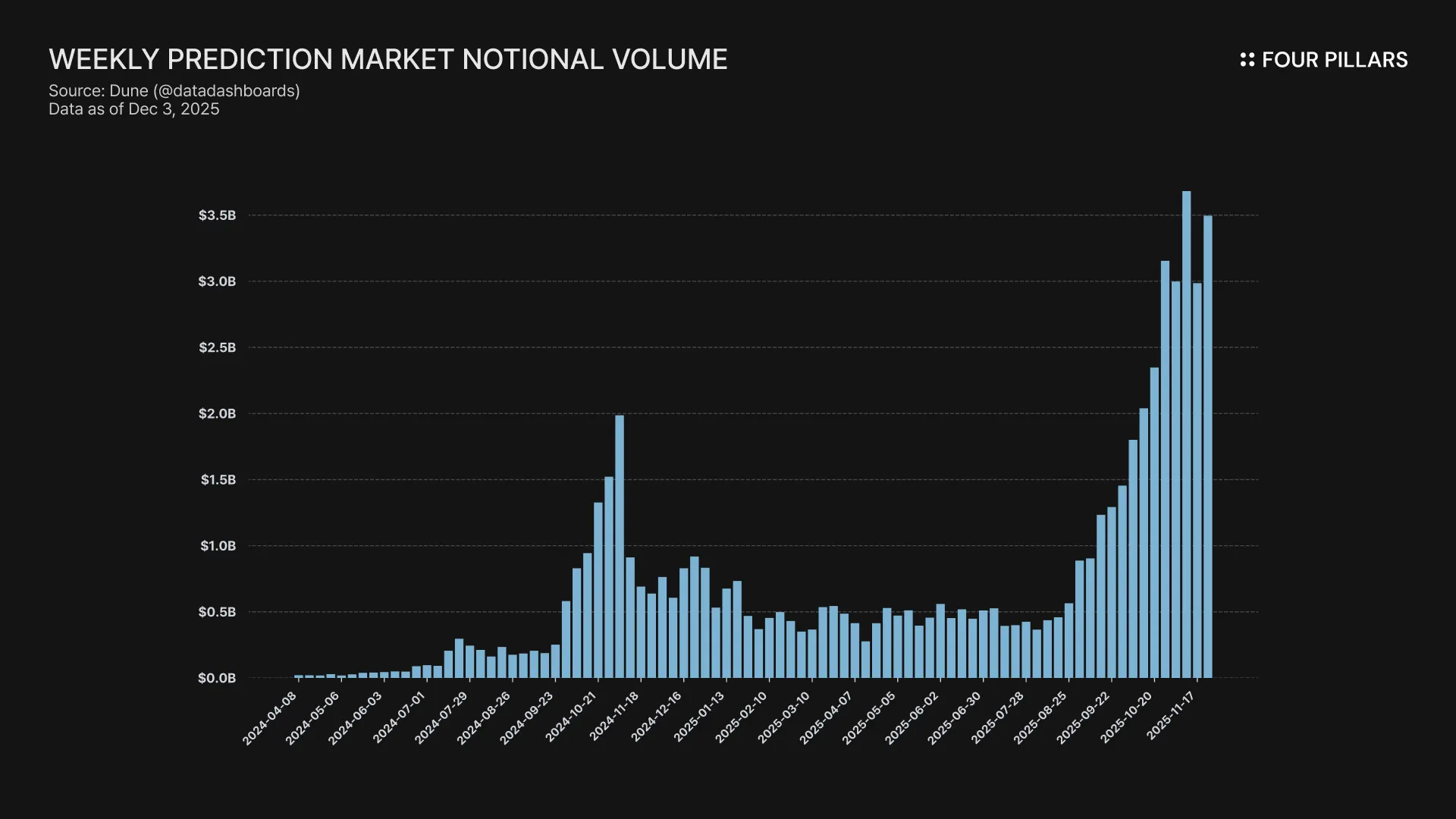

On the aggregated data, total notional traded across major venues (Polymarket, Kalshi, Opinion, Limitless, Myriad) grew from ~$16.4bn in 2024 to ~$44.2bn in 2025 YTD, an increase of roughly +170% YoY on the available period.

That growth is heavily skewed to 2025 H2. In 2025:

H1 2025: ~$12.4bn traded

H2 2025 (through late November): ~$31.8bn

H2 is already running at 2.5–3.0x H1 volumes, with Q4 showing a clear breakout. On a monthly basis, the system was transacting $1.6–2.5bn/month through June, then inflected to $5.8bn in September, $9.3bn in October, and $13.2bn in November. Total trades grew from ~32.4m in 2024 to ~142.9m in 2025 YTD, a 4.4x increase.

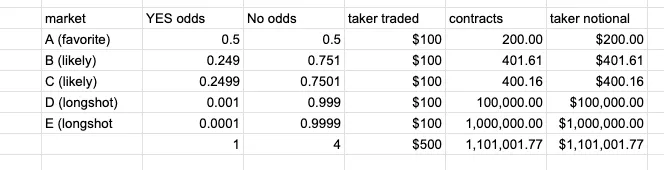

That said, the “$44.2 billion” needs decoding. Prediction markets report binary notional: every YES or NO share counts as a $1 contract regardless of the price a trader pays. A 1¢ YES is one contract, just like a 60¢ YES. This convention makes sense if you care about exposure (each share is a $1 payoff if correct) but it also means reported notional routinely exceeds actual cash turnover.

As Jez pointed out, a $100 purchase of 1¢ long-shot YES shares becomes 10,000 contracts, which appears as $10,000 of notional volume. This is standard derivatives accounting rather than misreporting, but it makes prediction-market volume non-comparable to sportsbook handle or spot/perp turnover unless you adjust for the underlying price.

Source: X (@izebel_eth)

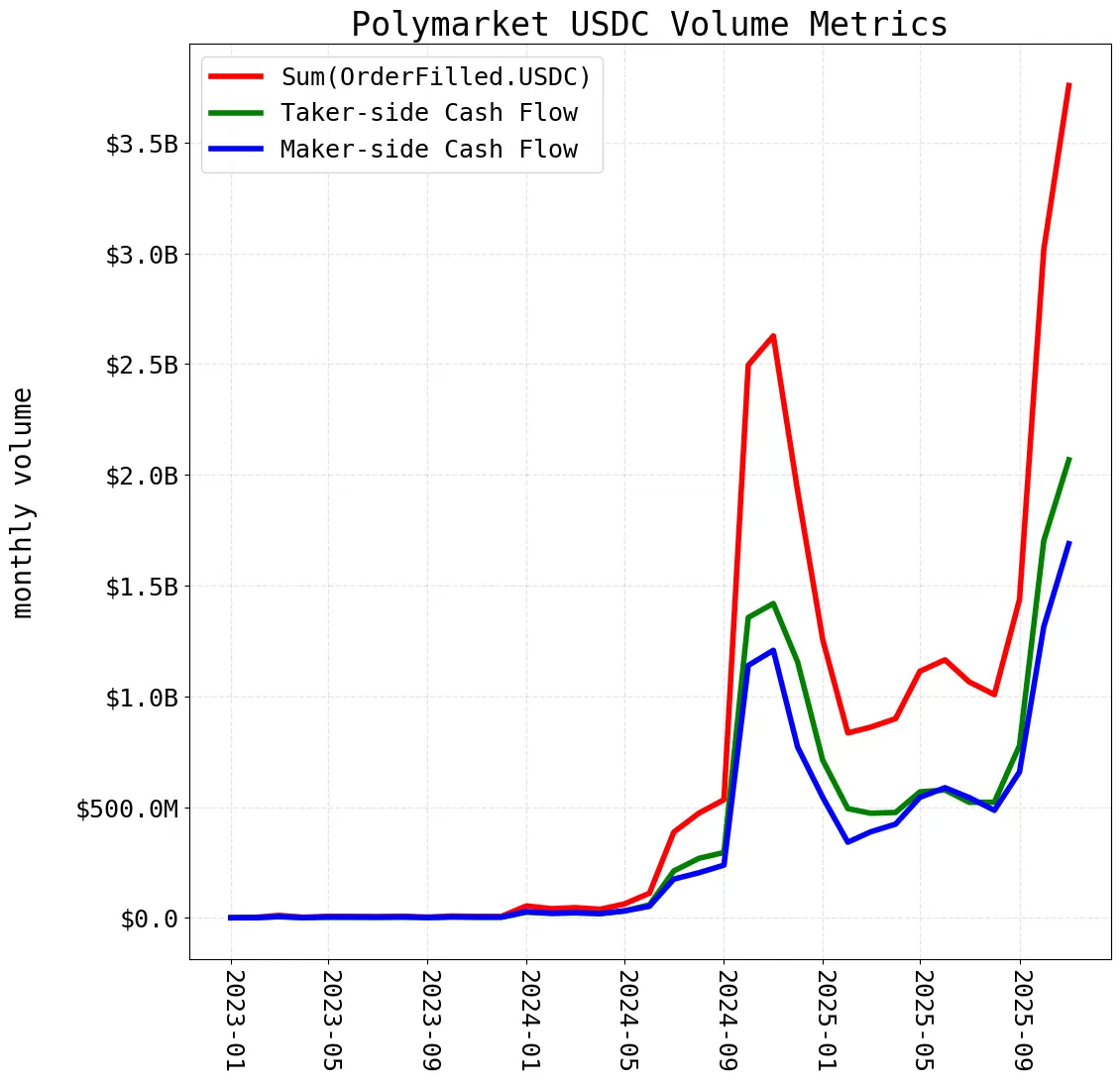

On top of that structural effect, Paradigm’s Storm highlighted that several analytics dashboards were double-counting Polymarket trades by summing both sides of each OrderFilled event. Because Polymarket emits one event for the maker and one for the taker, dashboards that aggregate all fills recorded a single trade twice.

Paradigm’s analysis shows real examples where a $4 fill appeared as $8 of volume. The underlying engine is correct; the error lives entirely in third-party consumption of the event stream. But it does mean that some historical “Polymarket did $X billion” claims were inflated by roughly 2× on top of the usual binary-notional inflation.

However, even after adjusting for both factors (dashboard double-counting and structural notional inflation) the directional story remains the same. More contracts are trading hands, more users are returning, and more capital is staying in the system between events. The category is growing; the only caveat is that notional exaggerates its scale if taken at face value.

5.3.2 Venue-Level Dynamics

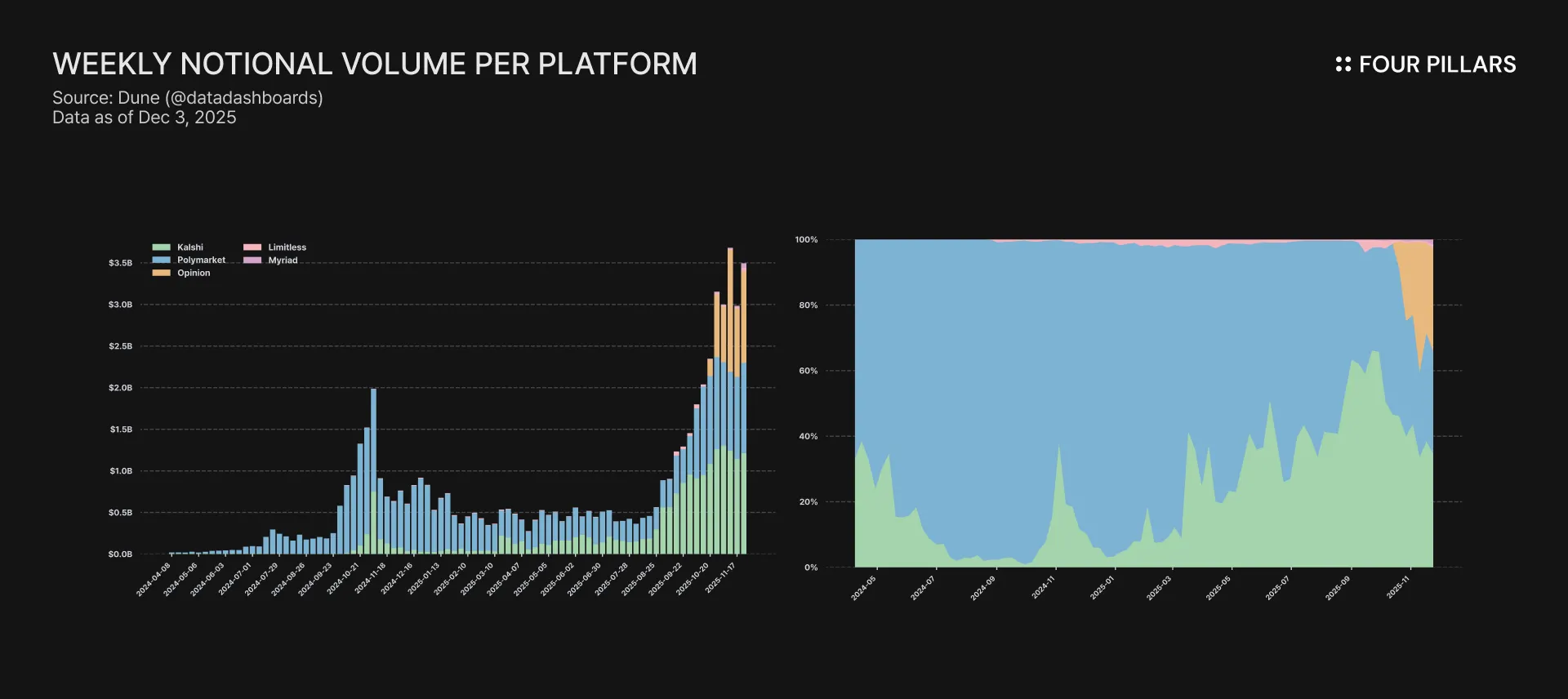

In 2024, Polymarket was effectively the market, with ~$14.4bn of $16.4bn in total notional (≈88% share), while Kalshi accounted for just ~$1.9bn (≈12% share). The picture in 2025 looks very different:

Polymarket: ~$21.5bn (≈49% of 2025 notional)

Kalshi: ~$17.1bn (≈39%)

Opinion: ~$5.0bn (≈11%)

Limitless + Myriad: ~1.5% combined

Three points matter here:

Polymarket is still the single largest venue by notional, and it grew ~50% YoY (from $14.4bn to $21.5bn).

Kalshi is the real share-gainer: from $1.9bn in 2024 to $17.1bn in 2025, roughly a 9x increase, closing much of the gap with Polymarket.

Opinion’s ~$5 billion, however, requires an analytical haircut. Its OI is thin, its user base small, and its volume is heavily incentive-driven ahead of a token. Therefore it should be treated analytically more like a token airdrop campaign than the arrival of a third foundational venue, until proven otherwise.

From a structural standpoint, the market has moved from a Polymarket-centric world in 2024 to a two-venue top line (Polymarket–Kalshi) in 2025. Meanwhile, the same interpretive caveats apply as at the aggregate level. Both Polymarket and Kalshi report binary notional, which inflates volume relative to cash especially in long-shot markets.

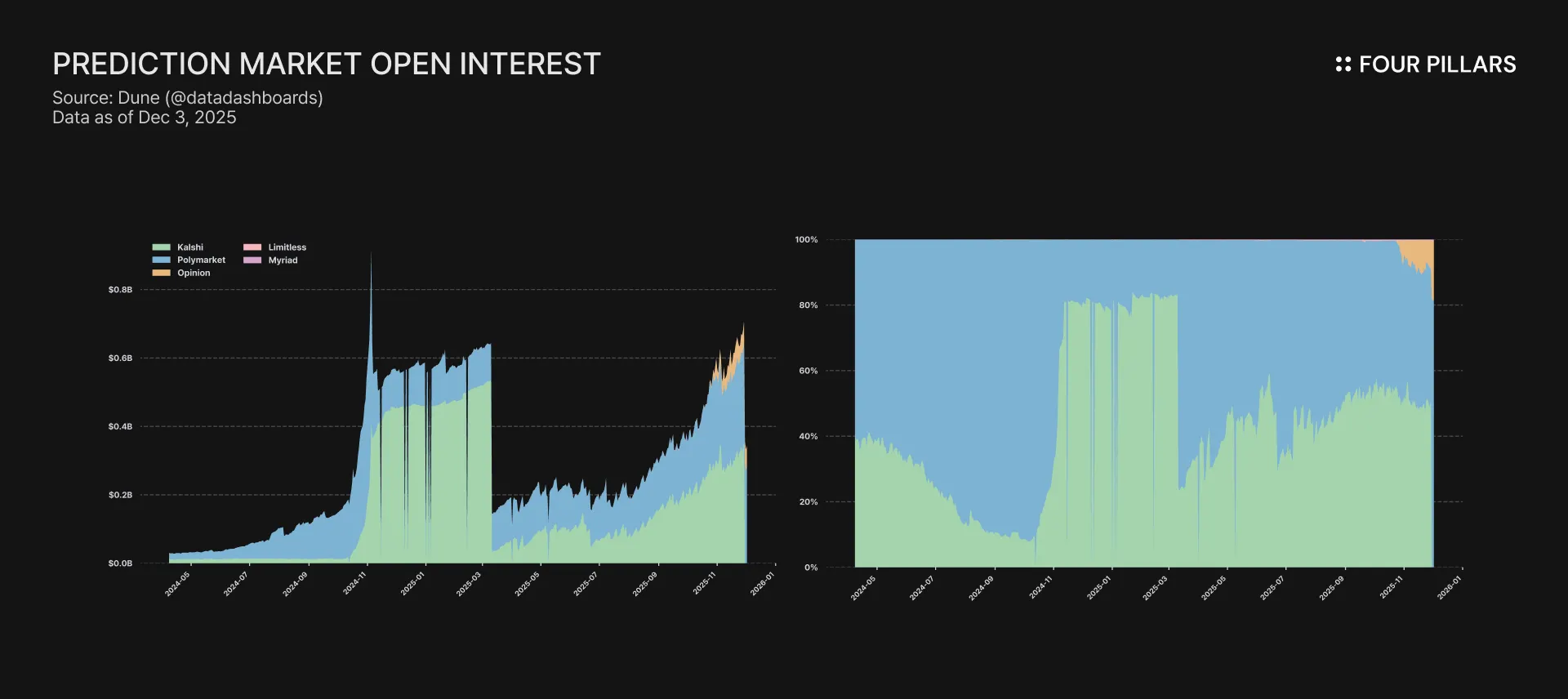

5.3.3 Open Interest

Open interest has grown alongside volume and is now meaningfully large. As of late November / early December 2025:

Kalshi: ~$355m open

Polymarket: ~$280m

Opinion: ~$62m

Limitless + Myriad: sub-$2m combined

Total outstanding risk sits just under $700m. More important than the absolute number is the pattern: OI has transitioned from spiky, event-driven peaks in late 2024 to a sustained band in 2025, with consistent capital staying in the system. This suggests that prediction markets are increasingly being used for persistent exposure (sports, macro, policy, crypto, culture), not just one-off electoral bets.

Kalshi and Polymarket together carry over 90% of OI, reinforcing the point that those two venues still anchor the risk in the system.

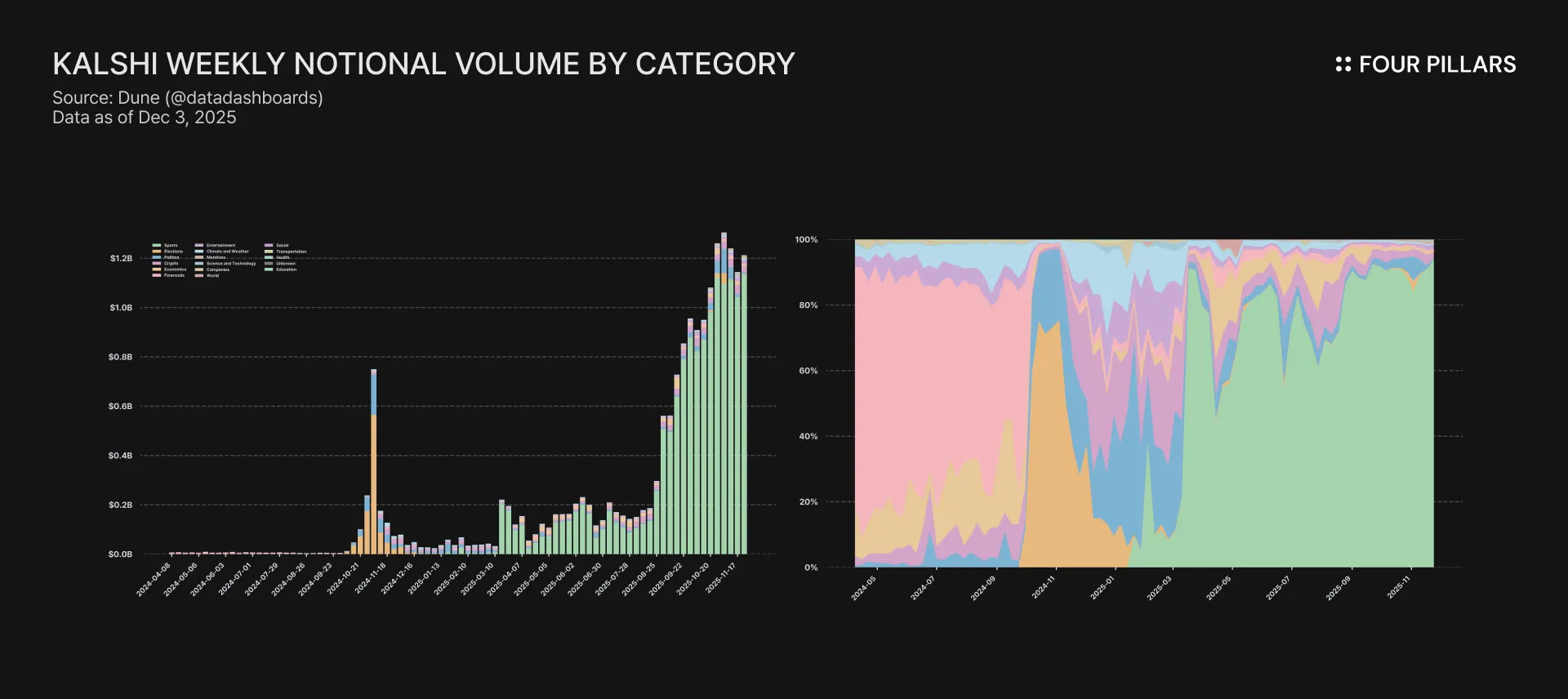

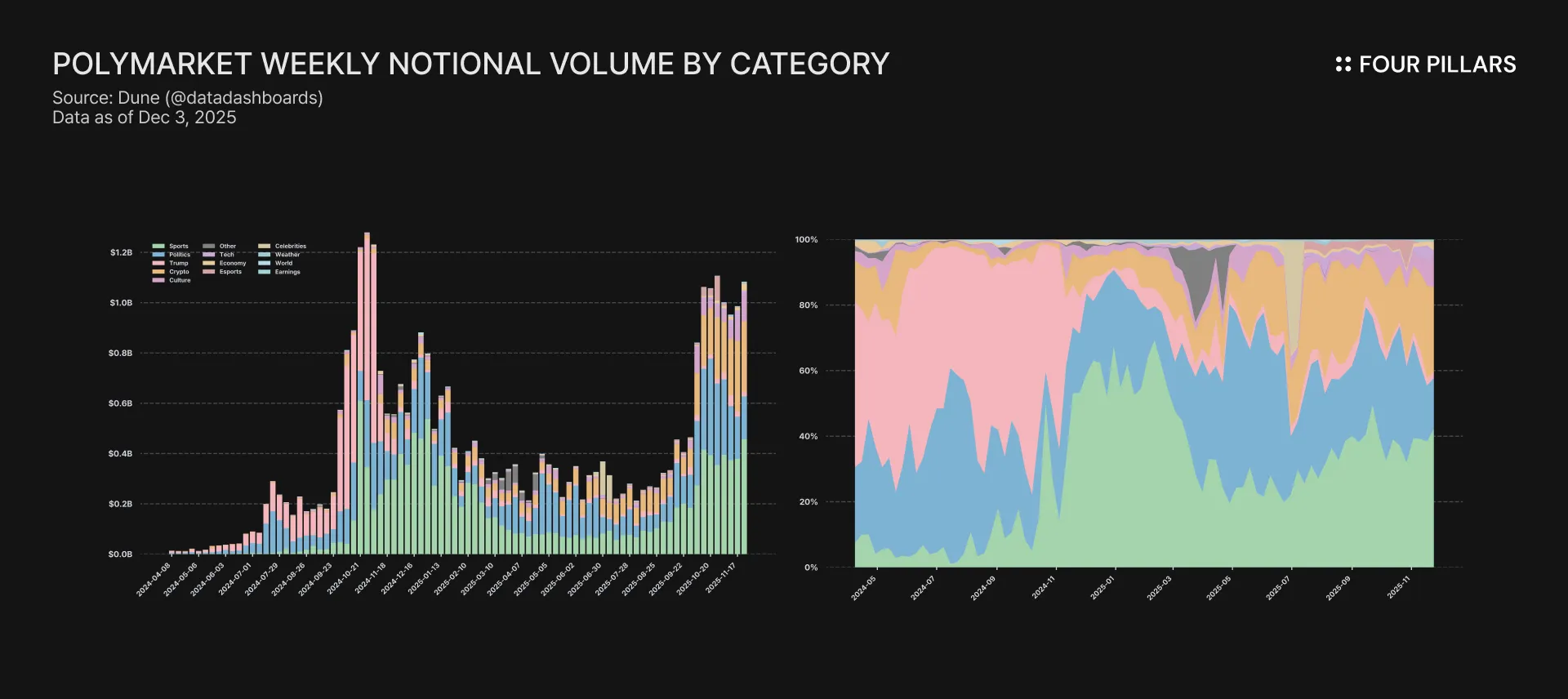

5.3.4 Category Mix and Platform Identity

The category-level breakdown makes the strategic divergence between Polymarket and Kalshi very clear.

On Polymarket, 2025 notional (~$21.5bn) breaks down roughly as:

Sports: ~$8.27bn (~38%)

Politics: ~$6.23bn (~29%)

Crypto: ~$3.81bn (~18%)

Culture: ~$0.94bn (~4%)

“Trump” tag: ~$0.84bn (~4%)

Long-tail categories (economy, tech, weather, esports, celebrities, world, earnings) fill the remainder.

A broad, narrative-driven mix where volume follows whatever the internet is focused on — sports cycles, elections, Fed path, crypto sentiment, cultural flashpoints.

On Kalshi, 2025 notional (~$17.1bn) is structurally different:

Sports: ~$14.5bn (~85%)

Crypto: ~4%

Politics: ~4%

Economics: ~2.5%

Entertainment: ~1–1.5%

All other categories (climate, financials, elections, tech, companies, social, health, etc.) together account for only single-digit percentages.

Kalshi has, in practice, become a sports-first venue with a regulated tail in macro, policy, and other verifiable categories. That profile is directly explained by its partner mix (PrizePicks, Webull, Crypto.com, ProphetX, DraftKings/Railbird, etc.) and the U.S. retail preference for sports-based prediction products.

5.3.5 Interpreting the Growth

Looking at 2025 in aggregate:

Total notional: $44.2bn vs. $16.4bn in 2024 (+170% YoY)

Total trades: ~143m vs. ~32m (+4.4x YoY)

Open interest: ~$700m vs. tens of millions a year prior

The category is expanding in breadth, depth, and persistence. More venues exist, more categories are active, open interest is no longer episodic, and prediction markets are now embedded in exchanges, wallets, sportsbooks, and brokerages.

But this should not be confused with a fully mature or uniform product–market fit. A meaningful portion of the growth is structural (binary notional), another is measurement noise (double-counting volume), and a third is promotional (Opinion and other incentive-heavy venues). After you haircut those factors, what remains is still significant: Polymarket and Kalshi anchor a mid-nine-figure risk system with sustained liquidity and tens of billions in genuine exposure trading across politics, sports, macro, crypto, and culture.

The correct way to interpret the data is not to dismiss volume as “inflated” but to understand what it measures. Treat notional as an exposure unit, not cash traded. Focus on retention, distribution, and integration rather than on screenshotable top-line numbers. The growth is real; the accounting is idiosyncratic. Any serious analysis has to hold both truths at once.

Although Polymarket and Kalshi anchor the market today, the competitive environment around them is expanding. A second wave of brokers, sportsbooks, exchanges, and consumer apps is beginning to experiment with prediction markets—some building internal infrastructure, others integrating existing rails. This does not diminish the centrality of Polymarket and Kalshi; rather, it shows that the category has become large enough that major consumer platforms no longer want to sit on the sidelines.

Over the past year, several large players have started embedding event markets directly into their ecosystems. Some rely on existing venues, others operate independently.

DraftKings’ decision to use Polymarket as the backend for its new predictions app is the clearest validation of Polymarket’s onchain infrastructure, particularly its ability to support high-frequency consumer use cases.

Conversely, FanDuel partnered with CME Group to launch event-style contracts entirely outside the Kalshi architecture, demonstrating that multiple regulated pathways now exist in parallel.

ForecastEx, which self-certified sports markets under CFTC procedures, has begun attracting institutional traders who want regulated exposure without depending exclusively on Kalshi.

Brokerages such as Interactive Brokers have also explored internal event-contract products, treating PMs as another flow type they may eventually support.

Gemini publicly announced that it is working on an internal event-contracts platform, positioning prediction markets as a new product category alongside brokerage and exchange services.

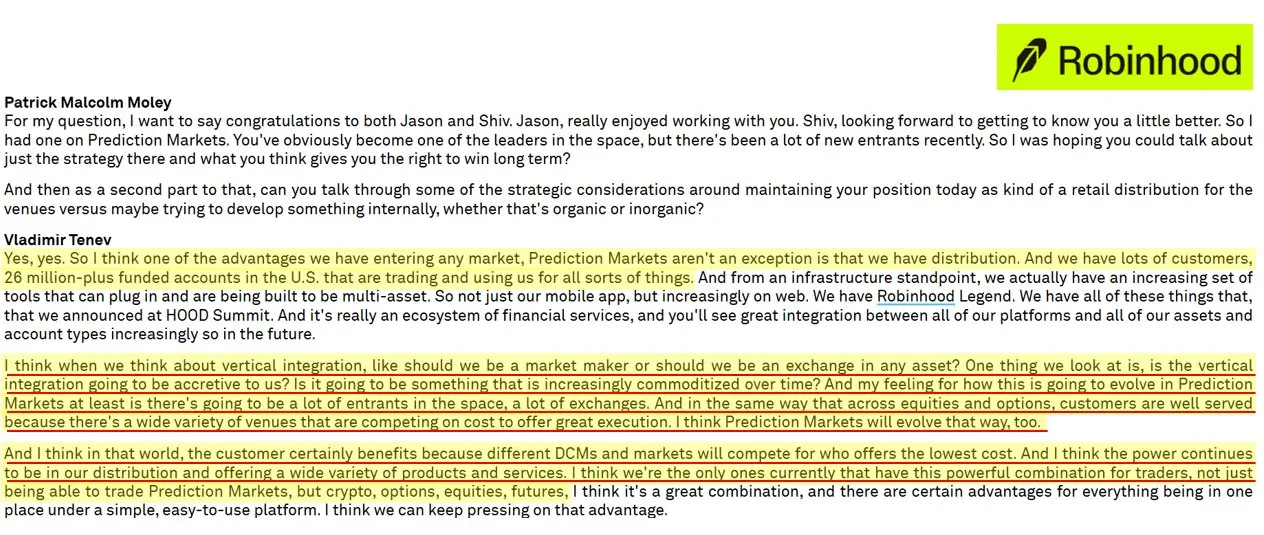

Robinhood is also a clear example of this trend. After initially integrating Kalshi rails, the company announced a joint venture with SIG to acquire MIAXdx and build its own CFTC-licensed exchange and clearinghouse. The intent is not to replace Kalshi overnight, but to reduce long-term reliance on any single upstream venue and create optionality around routing. In public commentary, Robinhood’s leadership has suggested that prediction markets will eventually resemble other exchange-traded products, with competition driven by execution cost rather than exclusivity.

Source: X (@TheOneandOmsy)

This shift is now reflected in early pricing dynamics. Kalshi fees range from roughly $0.01 to $0.02 per contract, with maker fees around 0.25% for larger events. To support volume routed through high-traffic partners like Webull or PrizePicks, Kalshi offers rebates, compressing effective venue revenue.

In October, Webull alone routed roughly 30 million Kalshi contracts, a level of volume that highlights both Kalshi’s traction and the economic reality of distribution-driven fee sharing. Polymarket’s U.S. relaunch undercut the market with 0.01% fees, reinforcing that cost competition is emerging as more venues and intermediaries enter the space.

That said, as more fintechs, brokers, sportsbooks, and crypto platforms experiment with prediction markets, the role of the upstream venue inevitably shifts. Execution may become one part of a larger routing landscape rather than the exclusive entry point for users.

In that environment, the real leverage sits with platforms that control distribution. They can direct flow across multiple rails, negotiate fees, and arbitrage between DCMs and onchain venues to secure the best pricing, lowest execution cost, and highest reliability. Venues, in turn, compete to remain in that routing set.

With the competitive landscape in view, we can be more direct about where value is likely to concentrate as prediction markets mature.

At the base, venues/engines (Polymarket, Kalshi, ForecastEx, CME, MIAXdx, Gemini) will remain the system’s trust anchors. Resolution credibility, regulatory licensing, and liquidity networks are not assets that can be easily forked. But trust is not the same as margin capture. Because switching costs are relatively modest, distribution platforms may eventually multi-home across engines. In that scenario, venues could remain indispensable while still facing significant fee pressure, as large apps route flow wherever execution and economics are most favorable.

At the top, distribution platforms (DraftKings, FanDuel, Robinhood, Webull, Coinbase, Trust Wallet) increasingly shape demand. Whoever owns the user relationship can route flow across venues, negotiate economics, and arbitrage execution quality. This resembles familiar patterns in Web2: Amazon with merchants, Google with publishers, Robinhood with exchanges. In prediction markets, a similar dynamic may emerge. Scale, UX, and mindshare may potentially become more defensible than ownership of a single venue.

A less obvious but potentially far more durable locus of value is reference data and canonical pricing. If certain venues become canonical for specific categories (Kalshi for sports, Polymarket for global internet-native events), their probability surfaces may start to function like benchmark indices. Once embedded into terminals, risk models, quant systems, and AI agents, switching costs harden. This is similar to how Bloomberg or ICE quietly anchor large parts of financial data infrastructure.

Finally, as explored in Sections 6 and 7, the emerging capital-efficiency and structuring layer—lending, yield wrappers, cross-margin systems, and structured exposures (event-futures, parlays, baskets)—may capture some value if it proves it can solve the constraints in today’s markets.

This section maps the key players across layers, focusing on their roles, funding, and contributions. The space is extremely nascent, so many new types and categories will emerge, and players will come and also disappear; treat this map as a starting point.

Market engines provide the core infrastructure for creating, executing, and settling prediction contracts, serving as the foundational layer where markets are matched and probabilities are encoded.

CME Group: CME Group operates as a derivatives marketplace offering event contracts on benchmarks like S&P 500, oil, gold, and crypto. As a public company, it has a market capitalization of approximately $100 billion as of Dec 2, 2025. CME Group is planning to launch swap-based event contracts with 24/7 trading in December 2025, including sports via FanDuel JV. Contracts are fully funded, with prices from $1 to $99 reflecting probabilities.

ForecastEx: ForecastEx is a CFTC-regulated platform for economic and climate event contracts, allowing yes/no trades on outcomes like elections and weather. It self-certified sports markets in October 2025 and launched election contracts. It recorded $12.68 million in volume on Election Day 2025.

Gemini: Gemini received a CFTC DCM license in December 2025, authorizing it to operate a regulated prediction market exchange for U.S. customers.

Kalshi: Kalshi functions as a CFTC-regulated prediction market exchange for trading event contracts on topics like elections, economics, sports, and crypto. It raised $1 billion in a Series E round in December 2025 at an $11 billion valuation, led by Paradigm, following a $300 million raise at $5 billion earlier in the year. Recent launches include tokenized markets on Solana and integrations with Google Finance.

Limitless: Limitless is a Web3 prediction market platform on Base, specializing in crypto and stock price forecasts with nonstop hourly and daily markets. It raised $10 million in a seed round in October 2025 led by 1confirmation, following a $4 million round in June 2025. The platform has surpassed $600 million in trading volume.

Melee: Melee is a Web3 prediction market platform allowing fact-based and opinion-based contracts. It raised $3.5 million in a seed round in September 2025 led by Variant and DBA, with no disclosed valuation. It launched its mainnet in September 2025 for social-media-style betting.

Myriad: Myriad is a Web3 prediction market protocol on Abstract, BNB Chain, and Linea, supporting binary and multi-outcome markets for events like sports, crypto, and economics. It achieved a $100 million trading volume milestone in November 2025, growing 10x in three months. Recent launches include the first native prediction market inside Trust Wallet.

Opinion: Opinion serves as a prediction market platform on BNB Chain, focusing on sentiment-based markets within social networks. It raised over $5 million in 2025 at an undisclosed valuation. The platform launched with no-code market creation, achieving over $5 billion in trading volume in five weeks.

Polymarket: Polymarket operates as a decentralized prediction market platform enabling users to trade on event outcomes such as politics, sports, and crypto. It has raised $205 million across undisclosed rounds, including $55 million in 2024 led by Blockchain Capital at a $350 million valuation and $150 million in 2025 led by Founders Fund at a $1.2 billion valuation. In October 2025, it secured a $2 billion investment from Intercontinental Exchange (ICE), valuing the company at $8-9 billion. It is seeking additional funding at a $12-15 billion valuation.

Robinhood/MIAXdx: Robinhood Exchange/MIAXdx is a CFTC-licensed derivatives exchange acquired by Robinhood in a JV with Susquehanna in November 2025. The acquisition involved a 90% stake, with no disclosed valuation for MIAXdx. It plans to launch futures and derivatives for prediction markets in 2026.

Consumer apps and embeds refer to established platforms that incorporate prediction markets as a secondary feature within their core product, such as a brokerage or sportsbook app. These differ from terminals and trading interfaces (5.3), which are purpose-built tools focused exclusively on prediction market workflows like advanced order routing or analytics.

Barchart: Barchart integrates Kalshi data feeds for prediction market information in its platform. The partnership launched in November 2025.

CNBC: CNN licenses Kalshi data for real-time prediction market odds in its reporting.

CNN: CNN licenses Kalshi data for real-time prediction market odds in its reporting.

Coinbase: Coinbase plans to integrate Kalshi-powered prediction markets for events like elections and sports in its retail app. As a public company, it has a market capitalization of over $70 billion as of Dec 2, 2025.

Crypto.com: Crypto.com partners with Kalshi to provide sports prediction markets within its exchange app.

DraftKings: DraftKings is a sportsbook that acquired Railbird for up to $250 million in October 2025 to enter prediction markets. As a public company, it has a market capitalization of approximately $16.7 billion as of Dec 2, 2025. It launched sports contracts via Railbird in November 2025, with Polymarket as backend. It plans to spend $50 million on prediction market launches in 2025.

Drift BET: Drift BET is a Solana-based prediction market for events like politics and finance, built on Drift Protocol. Drift Protocol raised $28.8 million over two rounds.

FanDuel: FanDuel partners with CME Group to offer event contracts on sports, economics, and financial benchmarks. Fanduel is owned by Flutter Entertainment. Its prediction market is set to go live in December 2025 via a JV with CME.

Jupiter: Jupiter enables Kalshi tokenized prediction markets on Solana. It launched in December 2025, but no markets are live yet.

NHL: NHL licenses its data and marks to Kalshi for prediction markets on hockey events. The multiyear agreement was announced in October 2025.

PrizePicks: PrizePicks integrates Kalshi-powered sports prediction markets into its daily fantasy sports app. It was valued at $2.5 billion in a 2025 sale to Allwyn. It reported adjusted EBITDA of $339 million for the year ending June 2025.

Robinhood: Robinhood operates as a brokerage app with embedded Kalshi-powered prediction markets for events like elections and sports. It raised $323 million in a Series E round in 2020 at a $7.6 billion valuation, led by DST Global. As a public company, it has a market capitalization of approximately $120 billion as of Dec 2, 2025. In Q3 2025, it traded 2.3 billion event contracts, with October 2025 at 2.5 billion.

Trust Wallet: Trust Wallet integrates Myriad and plans Polymarket/Kalshi for native prediction markets in its wallet app.

Webull: Webull embeds Kalshi event contracts for economic and sports predictions in its brokerage app. It routed 30 million Kalshi contracts in October 2025. It offers hourly predictions on S&P 500, NASDAQ, Bitcoin, and Ethereum.

Terminals and trading interfaces are standalone tools dedicated to prediction market activities, such as order placement, analytics, and monitoring. These differ from consumer apps and embeds (5.2), which add prediction markets as one feature among many in broader platforms. The division isolates ecosystem-specific tools for dedicated users from integrations aimed at casual access through existing apps.

Axiom: Axiom is a YC-backed terminal for Kalshi tokenized markets on Solana. It is scheduled for launch in 2026 as the next Kalshi integration.

Betmoar: Betmoar is an analytics terminal for Polymarket with Discord bot integration. It ranked #1 in volume in Polymarket's Builders Program.

Flipr: Flipr is a terminal offering up to 10x leverage on Polymarket and Kalshi markets. It launched in July 2025 with a trading bot on X.

Polycule: Polycule is a Telegram bot for Polymarket trading and analytics. It raised $560,000 in June 2025.

Sharpe Terminal: Sharpe Terminal provides institutional-grade analytics and hedging tools for prediction markets. It features 30+ tools for tracking funding rates and market movements.

DeFi and automation layers develop financial primitives and automated systems using prediction market positions, such as lending protocols or AI agents for trading.

Aixbet: Aixbet is an AI agent for sports prediction markets, using machine learning for bets.

Billy Bets: Billy Bets is an AI platform for sports prediction markets, targeting the $250 billion gaming industry. It raised $1 million in a pre-seed round in September 2025 from Coinbase Ventures, Virtuals Ventures, Contango Digital, and CMS Holdings. It launched a terminal in June 2025, routing over $1 million in wagers.

Buttery: Buttery is a futarchy platform enabling permissionless leverage in prediction markets for governance bets.

Galaxy Digital: Galaxy Digital is in talks to act as a liquidity provider for Polymarket and Kalshi. As a public company, it has a market capitalization of approximately $9.8 billion as of Dec 2 2025.

Gondor: Gondor is a DeFi protocol enabling borrowing against Polymarket positions. It raised $2.5 million in a pre-seed round in September 2025 at a $25 million valuation, led by Maven11 Capital with participation from angels linked to Polymesh, Rhino.fi, Futuur, and Salt.

Jump Trading: Jump Trading serves as a market maker on Kalshi, providing liquidity for large trades. It joined Kalshi in November 2025.

Robin.markets: Robin.markets provides staking and yield generation on prediction market positions. It focuses on composable tools for PM holdings.

Sire: Sire Agent is an AI-driven tool for sports prediction market vaults and automation.

Susquehanna International Group (SIG): Susquehanna serves as a market maker on Kalshi, providing liquidity for large trades. It joined Kalshi in April 2024 and handles 30x more liquidity for institutional flows.

Oracles and resolution mechanisms verify event outcomes and settle contracts, ensuring trust in prediction markets.

UMA: UMA is an optimistic oracle system for on-chain data verification in Polymarket. It supports dispute resolution through economic incentives.

Kalshi Klear: Kalshi Klear is the clearinghouse for Kalshi, handling settlement based on predefined data sources under CFTC rules. It enforces full collateralization and processes payouts immediately.

Chainlink: Chainlink is a decentralized oracle network supplying external data for prediction market resolutions. It supports asset pricing in DeFi-integrated PMs like Drift and Azuro.

7.1.1 The Mechanics of Oracle Capture

The integrity of any prediction market depends on accurate, credible resolution. Today, that problem is handled in two radically different ways:

deterministic, rulebook-driven resolution

decentralized, optimistic or token-based oracles

Neither model is perfect.

Deterministic systems solve ambiguity, but only in domains where official data sources exist. They cannot scale to the full “internet events” universe, and they occasionally produce edge cases even in regulated markets.

Decentralized or optimistic models like UMA can scale across arbitrary event spaces but introduce new attack surfaces: plutocratic voting, collusion, griefing, vote-buying, and outright manipulation, especially when event payoffs exceed the cost of influencing resolution. This creates a misalignment where voters may prioritize personal gains over accurate verification, especially in high-stakes disputes.

Why does this happen? Oracles verify outcomes in prediction markets, but UMA relies on token-weighted voting, creating risks of capture where large holders influence resolutions for profit. In fact, IntotheBlock shows that 95% of UMA tokens are held by large holders.

With low participation (often around 18~20 million tokens voting) whales can dominate, turning the process into a plutocracy rather than a neutral mechanism. UMA's low market cap, around $70 million in Dec 3 2025, exacerbates this, as attackers can acquire stakes to dispute and resolve markets favorably, especially when payoffs exceed token penalties.

This tension became visible in 2024–2025 across multiple markets. Disputes involving Zelenskyy, NASCAR, the Venezuelan election, TikTok’s temporary outage, and geopolitics all illustrated the same structural weakness: whales could acquire enough voting power to override evidence, especially during low-participation windows. Even when the protocol “worked as designed,” user trust deteriorated. The Polymarket override in the Barron Trump / DJT token case is a clear sign of how fragile confidence becomes when oracle legitimacy is questioned.

UMA is the best-known example because of its prominence on Polymarket, but the problem is not UMA-specific—it is the fundamental oracle problem for any prediction market protocol that relies on token-weighted voting, subjective interpretation, or challenge-based settlement. As prediction markets grow into the billions, the incentives to manipulate resolution will only increase.

7.1.2 What a more robust resolution layer could look like

Solving this requires systems that raise the cost of manipulation and reduce unilateral control. Several emerging approaches could be combined into a multi-layer resolution architecture:

Multi-Oracle or Multi-Source Consensus: Instead of relying on a single oracle, markets can require agreement across several resolution sources or a weighted combination of data feeds and human arbitration. This functions like a multisig: no single oracle can be corrupted without corrupting the others. It costs more and is slower, but appropriate for high-value markets.

Expert Panels for Subjective or Complex Events: Some disputes might require domain expertise. A formal panel (lawyers, geopolitical analysts, sports officials, technical researchers) can be summoned for cases tagged as requiring expert review.

Reputation-Staked Jurors: Systems like Kleros demonstrate the value of juror accountability: participants stake reputation and lose it when they rule inconsistently or maliciously. A prediction market native “resolution juror” pool could emerge, where track records matter and bad actors are penalized economically and reputationally.

7.2.1 The Capital Cost Problem

Long-dated prediction markets face a structural issue that short-dated markets do not: the cost of capital overwhelms the informational signal. A contract that resolves in several months requires full collateralization at entry, and the collateral cannot be reused, re-staked, or re-allocated until resolution. This means the market maker or trader is effectively warehousing a dead asset for the entire duration of the market, leading to thin markets with low participation, erratic pricing, and vulnerability to manipulation.

Participants may be directionally correct, but the return profile is poor compared to alternatives. A 60¢ YES position on a 12-month horizon returns 66.7% if correct, but the annualized return is often inferior to what the same capital could earn in spot or perp trading, DeFi lending, structured yield products, or even short-dated prediction markets with higher turnover. Once you factor in opportunity cost, the expected value of participation becomes negative for most traders unless conviction or informational edge is unusually strong.

For market makers, the economics are equally bad. A long-dated binary contract offers none of the attributes that usually make liquidity provision profitable: no realized volatility to monetize, no gamma to scalp, no funding payments, no carry.

The scale of idle capital is already meaningful. Polymarket alone has +$300m locked in unresolved positions; imagine that earning even 4~5% APY for the duration of each bet. It would transform the economics for both users and platforms.

7.2.2 Pathways to Capital Efficiency

Fixing this is about designing prediction markets so that outcome positions behave like productive financial assets from day one. At a system level, that implies a few guiding principles:

Decomposability: Outcome tokens must be easy to split, merge, and restructure. The conditional token framework already enables this—collateral can be turned into outcome sets and recombined, and “negative-risk” conversions recycle unused exposure. A capital-efficient design would extend this so traders can break long-dated bets into shorter conditional segments instead of locking into a single payoff path.

Composability: Outcome tokens should integrate with the broader financial stack. In principle they are standard tokens, but risk constraints keep them siloed. A next generation of infrastructure would let them serve as collateral, LP assets, or structured-product components without turning downstream protocols into accidental prediction markets. This alone would prevent long-dated positions from becoming dead weight.

Capital productivity and liquidity recycling: Idle collateral must earn something. Using yield-bearing stablecoins (e.g. USDe, USDS) as collateral solve part of this, as does collateral reuse across non-overlapping or mutually exclusive events. A single dollar should be able to support multiple timelines or conditional branches, mirroring combinatorial logic and ensuring capital is not tied to only one risk surface at a time.

Risk isolation and lifecycle awareness: Because outcome tokens jump to either full value or zero at resolution, any composability must isolate this binary risk. Dedicated pools, conditional “verses,” or conservative margin rules prevent an event’s failure from contaminating other systems. Capital efficiency cannot come at the cost of system-wide solvency.

7.2.3 Early Implementations

The first wave of infrastructure already reflects these ideas. Gondor allows users to borrow against long-dated YES/NO positions. Robin.markets builds staking and yield pathways for dormant event exposure. Both treat outcome tokens as balance-sheet items rather than static commitments, and both depend on the fact that Polymarket’s positions are natively composable on crypto rails.

These are prototypes of a broader category that will likely emerge: yield-wrapped binary claims, collateral-recycling frameworks, structured PM exposures, and vaults that treat outcome tokens as productive assets. Long-dated prediction markets will not scale without this layer. Capital-efficient PMs will form the liquidity foundation of the entire sector, and this is poised to become one of the most important frontiers in prediction-market design.

Prediction markets today are structurally unlevered. A trader must fully collateralize the binary payoff from the moment the position is opened until the moment the event resolves. This prevents liquidation cascades and keeps risk simple, but it also makes prediction markets fundamentally different from the rest of crypto’s financial infrastructure. They have no delta, no continuous valuation surface, and no way to express edge without posting the full $1 payoff.

Work from Rajiv (Framework), John (Kalshi), Marc (Felix), Krane (Asula), and Kratik specifically the beautiful proposals in HIP-4: Event Futures and Parlays on HIP-4) offers a conceptual frame for how leverage could be introduced without compromising binary settlement.

7.3.1 Synthetic Delta Through Event-Futures

Event-futures, as described in HIP-4, introduce a linear payoff on the change in market-implied probability rather than on the final binary outcome. A trader earns or loses based on how the probability evolves over time, not just on the event’s conclusion. This effectively creates a delta, which prediction markets have historically lacked.

This works because:

probability is continuous and can be marked to market

collateral can be sized to typical probability swings rather than to the full $1 payoff

positions can be liquidated before resolution if collateral is insufficient

This transforms prediction markets from static binaries into tradable probability curves, allowing leverage to emerge naturally. Traders can scale exposure using margin instead of capital, and market makers can run hedged books instead of warehousing fully paid binaries.

This is not a change to the final payoff; event futures still resolve to 0 or 1. Rather, it is a change to the path that makes leverage safe.

Source: Bedlam Research

7.3.2 Baskets and Parlays as Composable Risk Units

Parlays, as developed in the Bedlam follow-up piece, offer a different levered structure. Instead of amplifying a single probability, they combine several 1× event-futures into a joint probability payoff. A parlay resolves to 1 only if all underlying singles resolve to 1.

This creates convexity without borrowing risk:

upside compounds when multiple edges align

downside is capped at the parlay premium

intermediate volatility does not cause liquidation (path-independent)

capital is reused across legs, improving capital efficiency

Mechanically, parlays behave like multi-event derivative baskets. Importantly, they avoid the failure mode of under-collateralized leverage: there is no liquidation jump risk at resolution, because parlays are fully collateralized for their worst-case loss. They create leverage structurally through AND-composition, not through debt.

Source: Bedlam Research