What Happened?

On April 1, 2026, Australia passed new legislation requiring crypto platforms to obtain financial services licenses. The legislation, titled the Corporations Amendment (Digital Assets Framework) Bill 2025, cleared both houses of parliament. It was introduced by the Treasury in November 2025.

The law introduces two new regulated categories under the Corporations Act. Digital asset platforms cover exchanges and similar services that hold crypto on behalf of users. Tokenized custody platforms apply to firms that hold real-world assets and issue digital tokens representing those holdings. Both categories must obtain an Australian Financial Services Licence (AFSL) from ASIC, the country's securities regulator.

Instead of regulating crypto itself, the law targets the companies in the middle that control customer funds, aiming to reduce risks like commingling, insolvency, and misuse of assets that have caused losses in past crypto failures. Licensed platforms are required to safeguard client assets, provide standardized disclosures, maintain dispute resolution systems, and meet governance and risk management standards equivalent to those imposed on brokers and fund managers.

Smaller platforms receive limited exemptions. Firms holding less than A$5,000 per customer and processing under A$10 million in annual transactions are not subject to full licensing requirements. The bill is now awaiting royal assent. Once enacted, it will take effect after a 12-month period, giving crypto firms time to comply with the new licensing regime.

Researcher's Comment

The most immediate question this bill raises is which players will stay and which will leave. Crypto.com already holds two Australian Financial Services Licences, obtained years ago through an acquisition of a local payments firm. Swyftx has publicly engaged with regulators but warned the Senate Committee that the AFSL framework "relies heavily on historical AFSL concepts that do not map cleanly to digital assets."

Beyond these two, most exchanges operating in Australia have not made public statements about their AFSL readiness. The transition period will test whether smaller or less capitalized platforms can absorb the compliance costs or whether they will exit the market entirely.

Local exchanges like CoinSpot, Independent Reserve, CoinJar, and BTC Markets have invested in compliance infrastructure over recent years, anticipating stricter regulation. These firms are better positioned than offshore platforms that treated AUSTRAC registration as sufficient. But AFSL licensing involves capital adequacy standards, governance frameworks, and dispute resolution systems that can cost hundreds of thousands of dollars to maintain. The result will likely be a more consolidated market with fewer but better-capitalized operators.

One notable limitation of this legislation is its narrow scope. The bill focuses almost entirely on custody and exchange intermediaries. It does not address stablecoin issuance, token classification, or disclosure requirements for token offerings in any meaningful way.

Compare this to the EU, where MiCA covers stablecoin regulation, token issuance rules, and service provider licensing under a single framework. Japan has similarly established distinct regulatory categories for stablecoins and token offerings alongside exchange licensing. The U.S., despite its ongoing legislative battles, is simultaneously advancing the CLARITY Act for token classification and the GENIUS Act for stablecoins. Australia's bill addresses only one piece of that puzzle, with stablecoin and token issuance provisions either absent or scattered across other proposals and ASIC guidance documents.

Still, the bill provides a foundation that did not exist before. The Binance and Kraken enforcement actions showed that ASIC was willing to regulate crypto under existing law, but doing so through litigation alone created unpredictability for compliant operators. A formal licensing regime, even one limited to custody, removes that ambiguity for the largest category of market participants.

Australia's move also carries implications beyond its own borders. Hong Kong, Singapore, and Japan have each moved forward with crypto licensing frameworks in different ways. Australia's entry into this group adds pressure on jurisdictions that have not yet established clear rules, particularly in Southeast Asia.

Regulatory clarity in one country tends to accelerate conversations in neighboring markets, as both firms and regulators benchmark against what peers are doing. If the AFSL-based model proves workable, it could serve as a reference point for other common law jurisdictions considering similar intermediary-focused approaches. The bill is incomplete, but its passage signals that Australia intends to participate in the regulatory competition now underway across the region.

What Happened?

Hong Kong has missed its self-imposed March deadline to issue licenses for Hong Kong dollar stablecoin issuers, with the Hong Kong Monetary Authority yet to approve any applications. As of April 1, 2026, the HKMA's public register of licensed stablecoin issuers remains empty.

The delay comes after repeated assurances from senior officials. At Consensus Hong Kong in February, Financial Secretary Paul Chan Mo-po said licenses would begin to be issued in March. In the 2026/27 Fiscal Budget, Chan went further, stating that a "small number" of compliant issuers would receive their licenses that month.

The HKMA has not provided a specific reason for the delay. A spokesperson told CoinDesk that "the HKMA is actively taking forward the licensing matter and will announce further details in due course." No updated timeline has been given.

Hong Kong's stablecoin regulatory framework has been under development since late 2023. The Stablecoins Ordinance took effect on August 1, 2025, making fiat-referenced stablecoin issuance a regulated activity. The regulator confirmed receiving 36 formal applications, with only a small number expected to be approved in the initial round.

Three groups participated in the HKMA's stablecoin issuer sandbox, which launched in March 2024: JINGDONG Coinlink Technology Hong Kong Limited, a subsidiary of JD.com; RD InnoTech Limited; and a consortium of Standard Chartered Bank (Hong Kong), Animoca Brands, and Hong Kong Telecommunications (HKT). RD InnoTech was founded by former HKMA chief executive Norman Chan Tak-lam.

These sandbox participants are widely viewed as frontrunners for the first licenses. Standard Chartered's consortium formally established Anchorpoint Financial Limited in August 2025 and indicated its interest with the HKMA to apply for a stablecoin issuer license on the same day the Ordinance took effect. HSBC has also been reported as a leading candidate, given its status as one of Hong Kong's note-issuing banks.

Researcher's Comment

Among the 36 applicants, the most likely first-round recipients are already clear. According to Bloomberg, the HKMA is approving HSBC and Standard Chartered as the first licensed stablecoin issuers, with crypto exchange OSL also expected to receive a license. In total, only three to four licenses are expected in the initial batch. This is not a coincidence. HSBC and Standard Chartered are two of Hong Kong's three note-issuing banks, which means they already operate within the currency board system that backs physical HKD banknotes with U.S. dollar reserves. The HKMA is treating stablecoin issuance as a digital extension of that same monetary infrastructure.

What makes HKD stablecoins structurally interesting beyond Hong Kong's domestic market is the Linked Exchange Rate System. Since 1983, the HKD has been pegged to the USD within a narrow band of 7.75 to 7.85 per dollar. This means an HKD stablecoin is, in effect, indirectly pegged to the U.S. dollar. The Stablecoins Ordinance even includes an explicit exception: reserve assets for HKD stablecoins can be held in USD rather than HKD, reflecting this peg.

This has a practical implication for cross-border adoption. As the Richmond Fed noted, because HKD is pegged to USD, stablecoins issued in Hong Kong are indirectly pegged to the U.S. dollar. For users and institutions in Asia, an HKD stablecoin functions similarly to a USD stablecoin in terms of value stability, but it operates under a non-U.S. regulatory regime. This matters because the U.S. GENIUS Act imposes strict requirements on foreign issuers offering USD-pegged stablecoins to American markets. An HKD stablecoin, by contrast, sits outside U.S. securities and banking jurisdiction while still tracking the dollar through the currency peg. For cross-border payment flows in Asia, particularly trade settlement and remittances, this creates a regulated dollar-equivalent instrument that is not directly subject to U.S. regulatory reach.

There is also a broader geopolitical dimension. Hong Kong-based stablecoins could pursue a dual-track approach, with HKD-pegged tokens for international markets and potential interoperability with the digital yuan for use within the Greater Bay Area. For Beijing, the rise of USD stablecoins has become a geopolitical concern, and having a regulated HKD stablecoin ecosystem in Hong Kong gives China a controlled environment to experiment with digital currency competition without directly opening the mainland to crypto.

That said, the delay raises a timing question. The global stablecoin market reached roughly $309 billion in market capitalization as of January 2026, with transfer volume hitting approximately $33 trillion in 2025. Of fiat-backed stablecoins, 97% are denominated in U.S. dollars. Every month without licensed HKD issuers is a month in which USDT and USDC continue to consolidate their dominance in Asian cross-border flows. The HKMA's cautious approach has its logic, but the window for establishing HKD stablecoins as a credible alternative to USD stablecoins in regional trade settlement is not unlimited.

Crypto

Major Solana-based trading platform Drift exploited for at least $200 million

Paradigm is Building Its Own Prediction Markets Trading Terminal

Institution

SoFi launches 'Big Business Banking' combining fiat and crypto on a single regulated platform

Coinbase receives conditional approval for national trust charter from OCC

Charles Schwab opens waitlist for direct bitcoin and ether trading, targeting Q2 limited launch

Tech

Tech, crypto giants to help steward Coinbase's neutral x402 payments protocol under Linux Foundation

Investment

Franklin Templeton agrees to buy CoinFund spinoff to expand crypto investment offering

Stablecoin card issuing infrastructure platform Kulipa raises $6.2 million seed round

The Better Money Company raised $10 million led by a16zcrypto

Tether Makes Final Push for Fundraising at $500 Billion Valuation

Asia

Upbit operator Dunamu sees 10% revenue drop to $1 billion in 2025 as crypto trading cools

South Korea's KB Card taps Avalanche for 'hybrid' stablecoin credit card

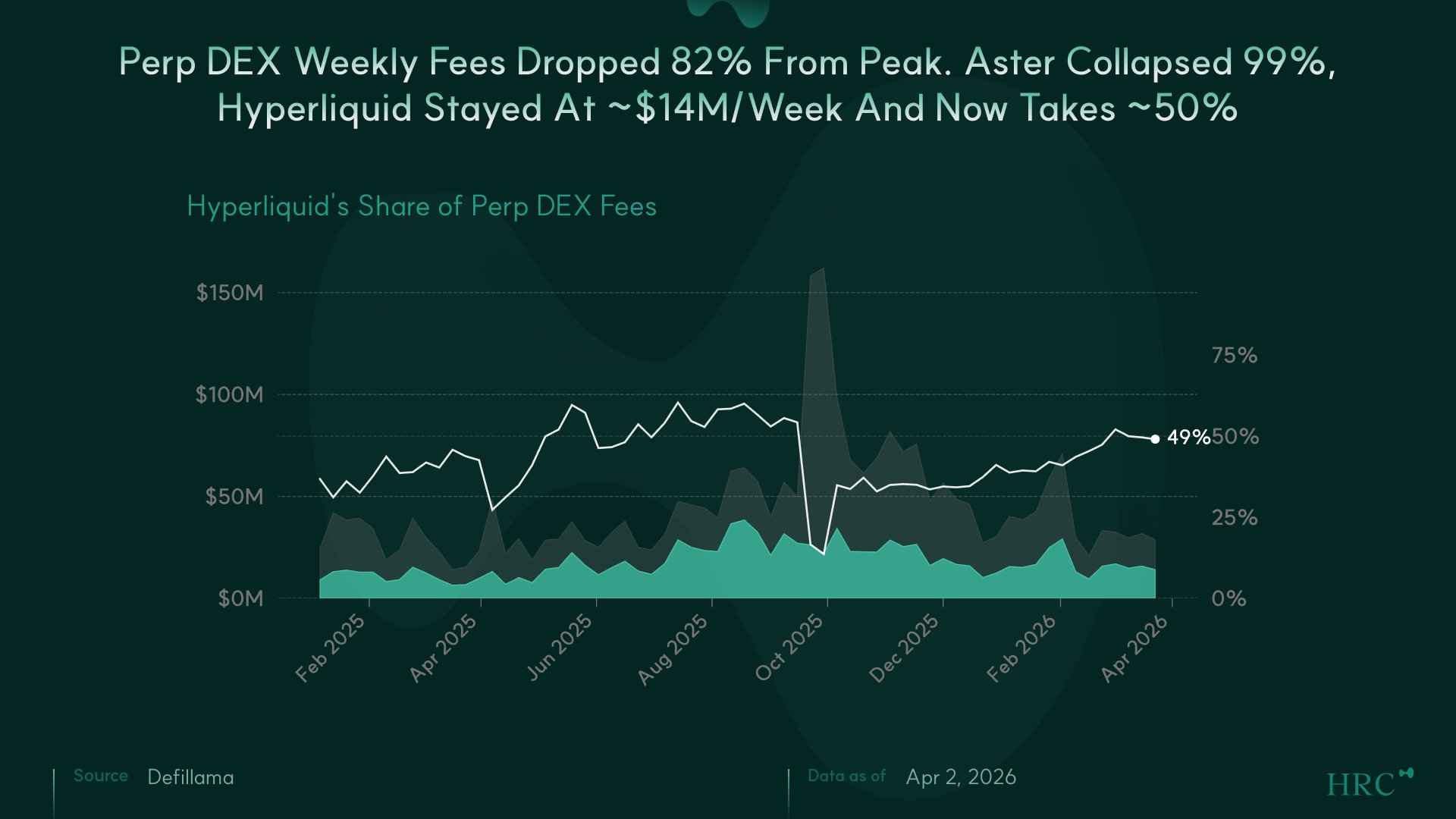

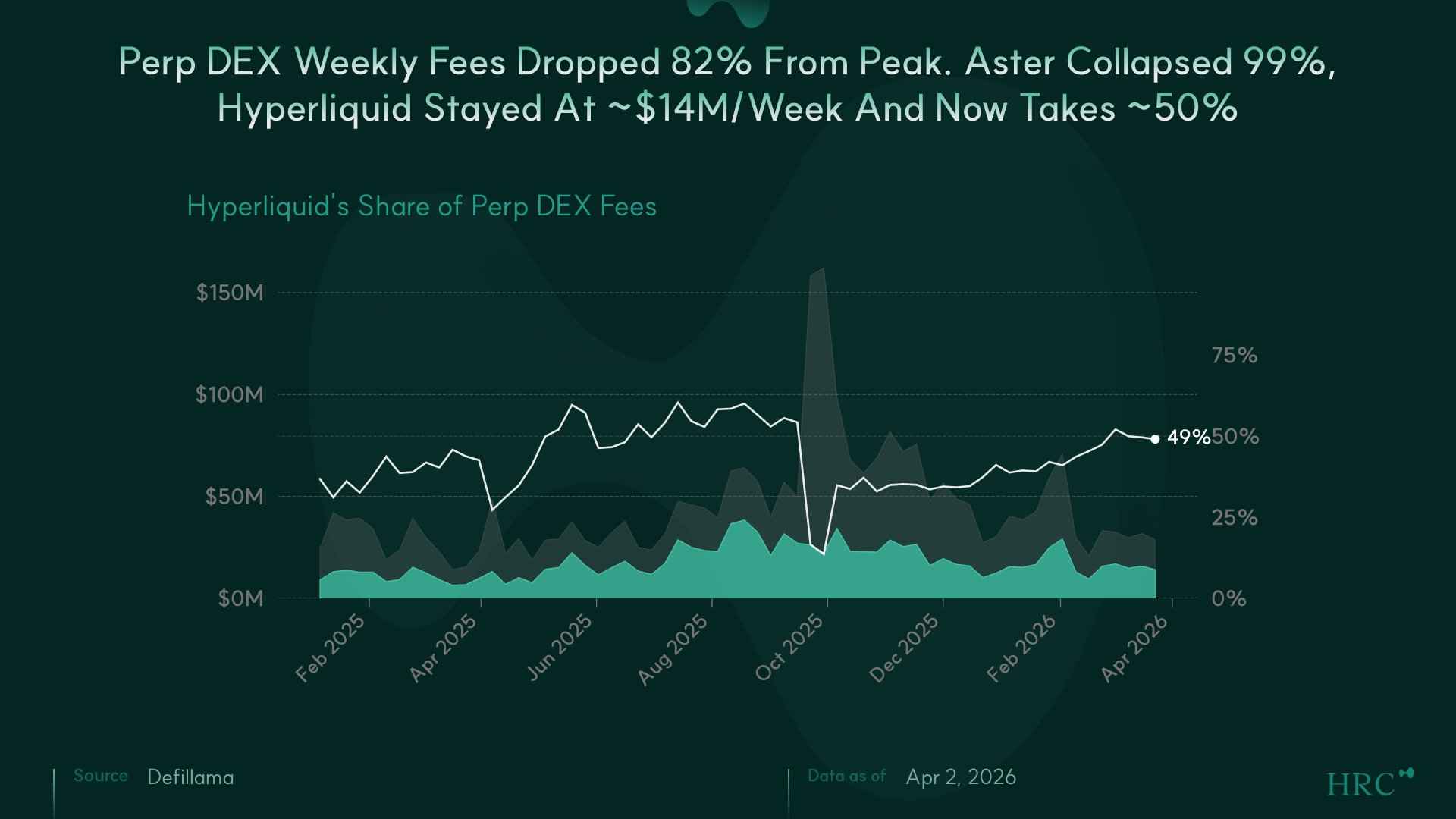

70% of that peak was Aster alone ($111.7M/week). Excluding Aster, the organic market declined from $48.9M to $26.7M.

Aster collapsed 99% ($111.7M → $1.54M/week). Hyperliquid declined 33% ($20.5M → $13.7M), while the ex-Aster market fell 45%. Incentive-driven volume disappeared, while product-driven volume contracted less.

Hyperliquid accounts for ~50% of perp DEX fees with no close second. edgeX (18%) is the only other protocol above 10%. HIP-3 commodities and equities now drive ~40% of Hyperliquid volume, creating a revenue stream unavailable to competitors. 97% of fees are allocated to HYPE buybacks (~$2M/day).

Perp DEX fees are contracting, but Hyperliquid’s market share continues to rise (~40% in January → ~50% in March). If the broader market recovers, Hyperliquid is well positioned to capture upside from a structurally dominant position.

Monthly volume crossed $100M in Sep 2024, then $600M in Mar 2026, a 6x increase in 18 months.

The card landscape diversified in 2025. In Jan 2025, RedotPay handled 88% of all volume. By Mar 2026, new entrants (EtherFi, KAST, Karta, Tria) captured 26% combined. EtherFi currently holds #2 with $62.6M, narrowly ahead of KAST at $60.1M.

All of this runs on traditional rails. Mastercard dominated early crypto card volume, but Visa moved aggressively into the space and now handles $581.8M of the $600M total, capturing 97% market share.

Solana is not simply trying to build a faster blockchain, but to become on-chain infrastructure capable of replacing real-world capital markets. In doing so, it places relatively higher priority on execution speed, latency, and reliability over ideological goals like decentralization. Infrastructure upgrades such as Firedancer, Alpenglow, and DoubleZero are all designed around this direction.

While Solana has already achieved high throughput and low latency, the primary bottleneck is no longer performance. Instead, it lies in the MEV-driven structure that determines transaction ordering and inclusion. In particular, the Jito-centric block production model optimizes MEV extraction while introducing latency, execution uncertainty, and infrastructure dependency. This is not merely a performance issue, but a problem of market microstructure.

Solana’s long-term roadmap goes beyond performance improvements and focuses on redefining transaction ordering and execution itself. Architectures such as BAM, ACE, MCL, and APE aim to redesign how transactions are ordered and executed across different layers. Rather than eliminating MEV, these approaches seek to distribute its influence and make the market structure more fair and predictable. Ultimately, the key challenge for Solana is aligning infrastructure direction with economic incentives.

The RWA market has surged from roughly $1 billion in 2023 to over $27 billion as of March 2026. Yet current blockchain infrastructure still faces structural limitations in performance, compliance, and interoperability when it comes to handling institutional-grade financial assets. Pharos is a finance-focused Layer 1 blockchain designed to close this infrastructure gap.

Pharos defines its own framework called the "Degree of Parallelism" (DP), which maps the evolution of blockchain performance across stages from DP0 to DP5. While most high-performance blockchains today sit between DP2 and DP3, Pharos targets DP4 and beyond. To get there, it implements asynchronous BFT consensus where all validators propose blocks simultaneously, a dual VM supporting both EVM and WASM, a six-stage block processing pipeline for concurrent execution, and Pharos Store, which achieves up to 80% reduction in storage costs compared to conventional blockchain storage.

Pharos's SPNs (Special Processing Networks) are modular extension layers that share the security of the mainnet while independently handling workloads such as high-frequency trading, privacy computation, and AI inference. They can be read as a blockchain-native reimagining of the institutional specialization structure found in traditional finance.

Pharos has formed the RealFi Alliance with partners including Chainlink, LayerZero, and Centrifuge, building an ecosystem that spans from asset tokenization to distribution and settlement. It is also advancing real-world asset integration through a partnership with Hong Kong-listed GCL New Energy, covering energy revenue right tokenization, decentralized energy trading, and more.

Japan remains a market with a high share of cash usage, yet at the same time has built one of the most pioneering and systematic cryptocurrency regulatory frameworks in the world. This regulatory clarity removes uncertainty for businesses and provides an optimal environment to expand operations stably across exchanges, stablecoins, tokenization, and more.

SBI has grown based on a digital-first DNA that originated from internet-based finance, a platform expansion strategy through M&A and joint ventures, and an asymmetric strategy that avoids head-on competition while preempting new markets. This playbook is directly applied to its cryptocurrency business as well, serving as the driving force behind rapid expansion across exchanges, market making, stablecoins, tokenization, and beyond.

Unlike megabanks such as MUFG and SMBC, which focus on specific areas like infrastructure or payments, SBI is building a full-stack strategy centered on exchanges that connects liquidity, payments, investment, and tokenization. Through this, SBI is positioning itself not just as a participant in the cryptocurrency business in Japan, but as a key player designing a new financial infrastructure that integrates traditional finance and digital assets.

Institutional adoption of crypto is accelerating globally, and institutional ETH staking is emerging as one of the most prominent services among a wide range of crypto offerings for institutions. This is driven by factors such as regulatory clarity, simplicity, and stability.

However, unlike retail participants, institutions face multiple barriers when staking large amounts of ETH. These include lack of support for DPoS, slashing risk, technical complexity, accounting and reporting requirements, compliance, security concerns, and liquidity lockups.

Existing staking providers offer institutional ETH staking through methods such as custodial staking and white labeling. Recently, following Ethereum’s Pectra upgrade, non-custodial ETH staking has also become available to institutions. One solution to watch in particular is Lido’s stVault, which has been gaining significant attention. It provides a modular structure that allows institutions to designate their own operators and configure customized vaults, effectively addressing many of the key hurdles in institutional ETH staking.

What about the institutional ETH staking market in Korea? While Korea has developed a very large retail-driven crypto market, its corporate and institutional crypto sector remains relatively underdeveloped due to conservative and slow-moving regulations. Nevertheless, interest in crypto among corporations and institutions has recently been very strong. With expectations that corporate crypto investment as well as crypto ETFs, will be permitted this year, Korea represents a highly promising market for institutional ETH staking.

Lido is Ethereum's largest staking protocol with $18.7B in TVL and $37.4M in annual revenue, yet LDO sits at $0.32, down 95.6% from its ATH. The causes are declining revenue and market share, combined with a governance-only token design that returns none of the protocol's earnings to holders.

A one-time buyback of $20M, approximately 7.2% of LDO's market cap, along with a long-term automated buyback + LP mechanism through NEST, is set to launch in 2026. The structure aims to simultaneously deepen on-chain liquidity and reduce circulating supply, rather than simply burning tokens.

With both revenue and market share declining, whether to spend treasury funds solely on token price support or invest in protocol growth and service expansion is the hardest question the DAO faces. Deciding how to prioritize these competing demands is itself an act of governance, and the true value of the LDO token.

On April 1, 2026 at 16:05 UTC, an exploit worth approximately $285M struck Drift Protocol, a leading perpetual DEX on Solana. The attack was a sophisticated collateral manipulation scheme: the attacker used compromised admin keys to list a worthless token on a new spot market, disabled withdrawal safeguards, and then drained real assets using the fabricated collateral value.

The attack combined durable nonce-based pre-signing with sophisticated social engineering. Starting March 23, the attacker created durable nonce accounts for two multisig signers and two attacker-controlled accounts. Even after a legitimate multisig migration on March 27, the attacker re-established access to signers of the new multisig. The attacker obtained pre-signatures from legitimate signers through transaction misrepresentation, stored them via durable nonces, and batch-executed them on April 1 to seize admin authority. No seed phrase leaks or smart contract bugs were involved.

This incident marks yet another major operational security failure, coming just 10 days after the Resolv exploit. Resolv collapsed because it had no multisig at all; Drift collapsed despite having one, due to a low threshold and the absence of additional security mechanisms. Together, these two incidents demonstrate that a fundamental redesign of privilege structures is overdue.

The passage of the GENIUS Act has accelerated the entry of traditional financial institutions, fintechs, and big tech companies into stablecoin issuance. However, as the number of issuers increases, stablecoin fragmentation is emerging as a structural issue that replicates the inefficiencies of traditional finance, and a stablecoin clearing layer is becoming essential infrastructure.

Two startups, Ubyx and The Better Money Company, have each raised $10M in seed funding and entered the competition to build stablecoin clearing infrastructure. While both share a similar goal of solving the many-to-many model problem, their clearing mechanisms differ slightly.

Historically, companies that solved many-to-many model problems have built massive scale and strong moats. In that context, stablecoin clearing could become a significant business opportunity. However, there is a key variable. As stablecoins increasingly gain recognition as money, there may be a view that clearing should be handled not by private companies but by governments or regulatory bodies. This is especially likely in more conservative financial markets such as Asia. It remains to be seen whether startups like in the United States or governments will ultimately take on this role.

What FTX got wrong was not the direction but the execution. In its second year, the exchange posted $1B in revenue, proposed a non-intermediated clearing model to the CFTC, and listed tokenized stocks. The vision FTX laid out mirrors where the entire crypto industry is heading today. What collapsed was not the vision but customer fund misappropriation, Alameda favoritism, and the absence of transparency. QFEX takes that vision and rebuilds it from scratch.

QFEX's edge lies in its trader DNA. The entire team comes from HFT trading houses, and the exchange's microstructure reflects inefficiencies they encountered firsthand: (1) a 100ms speed bump neutralizes latency arbitrage, (2) careful tick size calibration strikes a balance between top-of-book liquidity, tight spreads, and genuine price discovery, and (3) price bands block cascading liquidations before they start.

The TAM for perpetual futures is not crypto. Perps now compete directly with infrastructure serving roughly 6.8M CFD retail traders, $9.6T in daily global FX volume, and over $600T in OTC derivatives notional outstanding. No-expiry leverage, zero rollover burden, and 24/7 access are things legacy instruments never offered.

Perpetual futures are rapidly being institutionalized, yet almost no exchange has been purpose-built for traditional assets from the ground up. Adding traditional assets to a crypto exchange is a different problem from building an exchange for traditional assets. QFEX is the latter. Adding exchange-listed products to a B-Book broker is a different problem from designing on a public order book from day one. QFEX is the latter there, too.

EIP-8141, known as "Frame Transaction," is currently under consideration for inclusion in the Hegota hard fork. It separates the authentication, payment, and execution of Ethereum transactions, making each independently programmable. This allows Ethereum transactions to freely choose their signature algorithm (passkeys, quantum-resistant signatures, etc.), and enables features like gas fee sponsorship and batched execution of multiple calls within a single transaction at the protocol level.

Frame Transaction is more than a UX improvement. It is the foundation for Ethereum's broader direction, including quantum resistance, censorship resistance, and privacy, while also addressing the demands of an era defined by AI agent delegation. Vitalik described Frame Transaction as "an omnibus that wraps up and solves every remaining problem that AA was facing, and the culmination of nearly a decade of research."

Frame Transaction creates the conditions for Ethereum to evolve on its own without hard forks. Just as the EVM made the execution layer programmable through smart contracts, allowing diverse programs to be added to Ethereum without hard forks, Frame Transaction makes the verification layer programmable, enabling authentication innovations, both present and future, to happen without protocol modifications. This maps directly to the Ethereum Foundation's "walkaway test" vision: a protocol that remains sustainable even without the Foundation.

Display V2 is a major redesign of Sui's protocol-level rendering system, ensuring that NFTs and on-chain objects look the same across wallets, explorers, and marketplaces. By enforcing exactly one display per type, it eliminates the old problem of having to figure out which display is the "real" one.

This change is part of a broader shift in which Sui is migrating its entire data infrastructure from JSON-RPC to gRPC/GraphQL. Since the old approach simply wouldn't work under the new infrastructure, adopting V2 wasn't optional. Both Display V1 and JSON-RPC reach end-of-life in July 2026.

V2 allows templates to directly express information that previously required off-chain services: collection data, child objects, default values, and more. As builders start taking advantage of these capabilities, the richness of NFT information visible in wallet interfaces could look very different from what we see today.

Dive into 'Narratives' that will be important in the next year