Lido is Ethereum's largest staking protocol with $18.7B in TVL and $37.4M in annual revenue, yet LDO sits at $0.32, down 95.6% from its ATH. The causes are declining revenue and market share, combined with a governance-only token design that returns none of the protocol's earnings to holders.

A one-time buyback of $20M, approximately 7.2% of LDO's market cap, along with a long-term automated buyback + LP mechanism through NEST, is set to launch in 2026. The structure aims to simultaneously deepen on-chain liquidity and reduce circulating supply, rather than simply burning tokens.

With both revenue and market share declining, whether to spend treasury funds solely on token price support or invest in protocol growth and service expansion is the hardest question the DAO faces. Deciding how to prioritize these competing demands is itself an act of governance, and the true value of the LDO token.

Lido is the largest staking pool and liquid staking platform on the Ethereum network, holding the highest share of staked ETH. Lido issues its own token, LDO, whose official name is "Lido DAO." What does it truly mean to be a DAO (Decentralized Autonomous Organization)? Is it simply the authority to decide a protocol's governance? How far does that governance extend? Isn't distributing a protocol's revenue also within the DAO's authority? Lido, the dominant force in Ethereum staking, is now confronting these questions head-on.

The protocol still manages tens of billions of dollars in TVL and generates tens of millions in annual revenue, yet LDO has fallen 95.6% from its all-time high and lingers near its all-time low. Recently, the Lido governance forum has seen a wave of proposals aimed at boosting token value, including LDO buybacks. Can LDO token actually make a comeback? This article examines Lido's current situation in terms of market share and revenue, and takes a closer look at the proposals nearing execution that are designed to enhance LDO's token value.

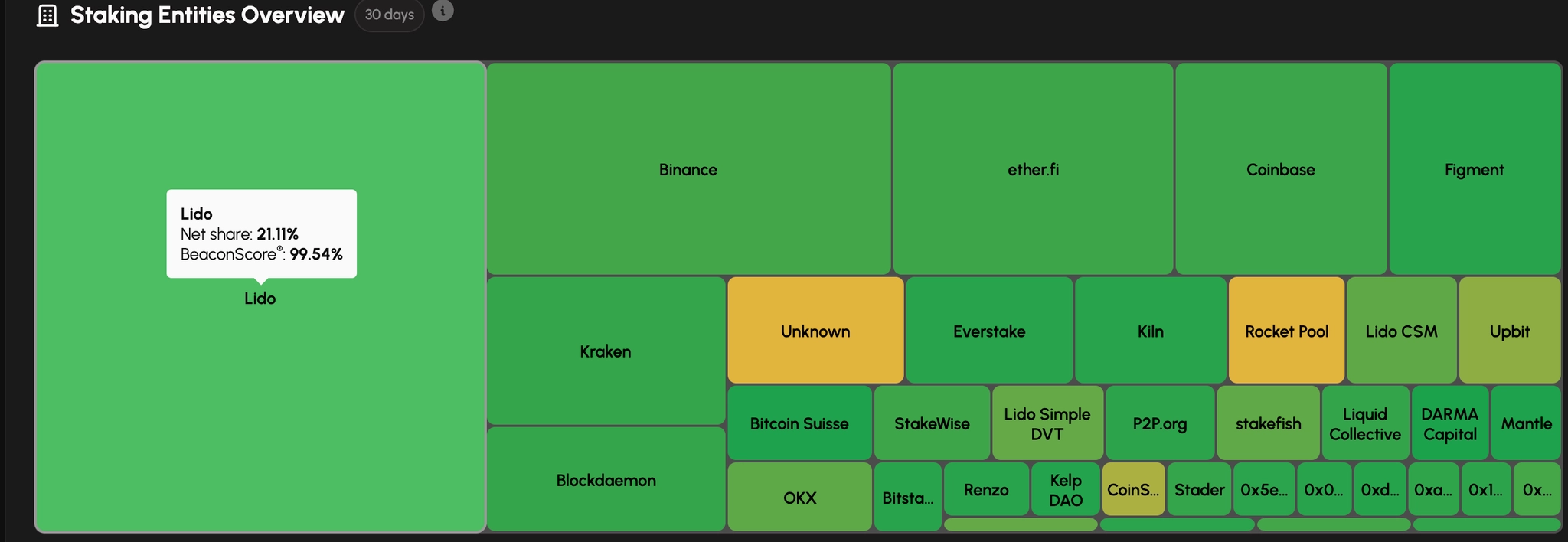

Lido is the leading protocol in the Ethereum liquid staking market. As of March 2026, it is also the largest staking pool, holding 21% of all staked ETH on Ethereum. Users deposit ETH into Lido and receive stETH, which can be freely used across DeFi while staking rewards accumulate automatically. stETH is integrated into over 100 DeFi protocols including Aave, Curve, and Uniswap, positioning it as a de facto reserve collateral asset that serves as the foundation of Ethereum's DeFi money legos.

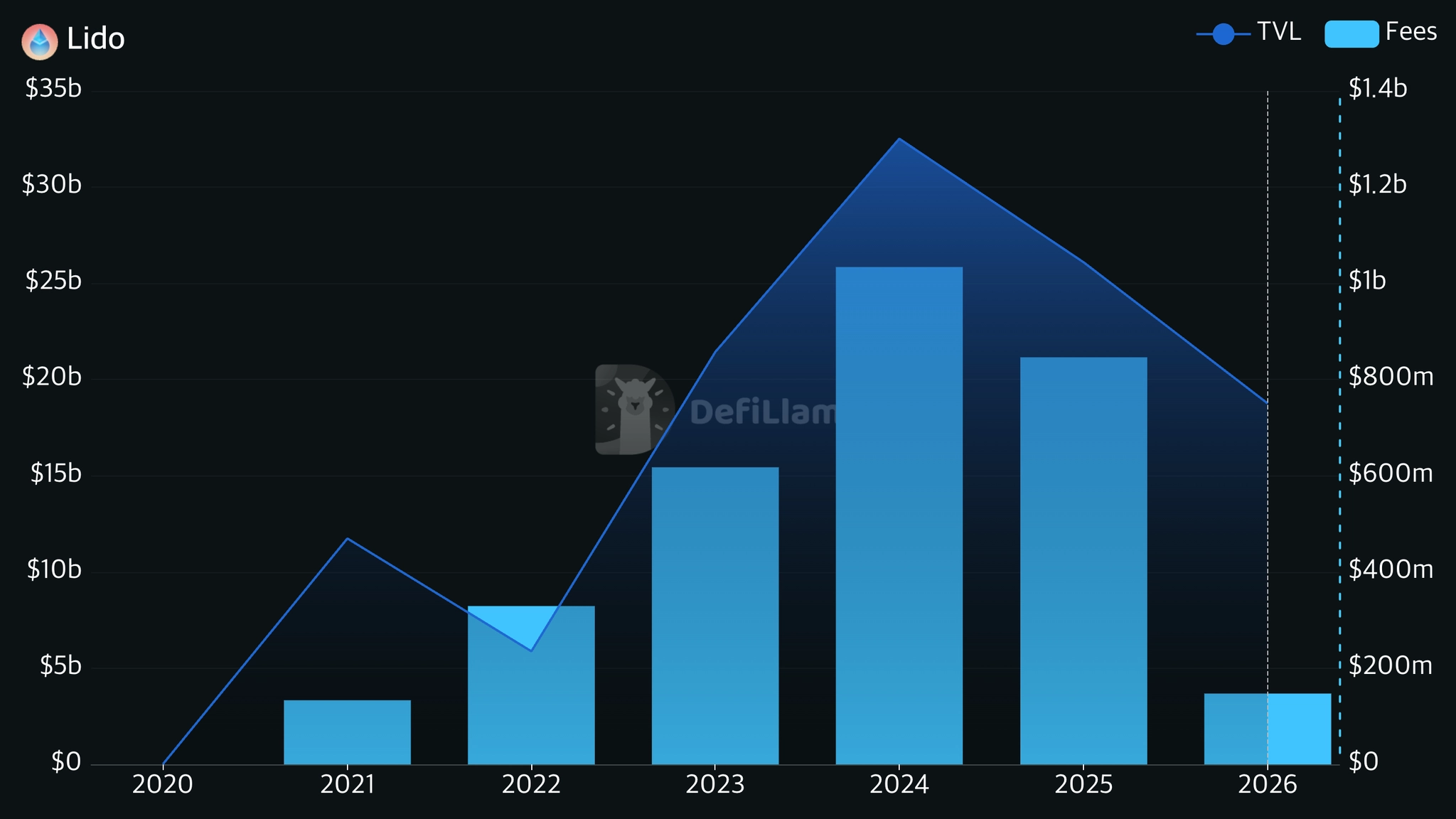

Source: DefiLlama

As of March 30, 2026, Lido's TVL stands at approximately $18.7B. While this remains second among all DeFi protocols, it has declined significantly compared to mid-2025 when it exceeded $38B. The decline in TVL is driven by both falling ETH prices and shrinking market share. The primary cause is the drop in ETH price from over $4,000 in the summer of 2025 to less than half that level by March 2026. However, even measured in ETH terms, TVL decreased from 9.63M ETH to 8.81M ETH, a decline of approximately 8.5%.

Source: beaconcha.in

Lido's share of the total Ethereum staking market has fallen from over 28% in 2024 to approximately 21% as of March 2026. The primary drivers are the entry of large institutional players such as BitMine and Grayscale, the launch of staking ETFs by firms like BlackRock, and the broader shift of Ethereum staking's key participants from retail to institutional. Capital migration to competing liquid staking platforms like ether.fi has also played a role. The fact that ether.fi's share grew from under 1% in early 2024 to 6% by 2026 demonstrates that the decline in demand for liquid staking itself is not the root cause.

On the revenue side, Lido takes a 10% fee on staking rewards, split evenly between node operators (5%) and the Lido DAO treasury (5%). In 2025, Lido's protocol fee revenue was $37.4M, down 23% from $48.5M in 2024. Total gross staking rewards generated across the protocol also fell 18%, from $1.03B to $846.7M.

This is the result of total staked ETH on the Ethereum network increasing while Lido's share of that pool has shrunk. As total staked ETH grows, the probability of block proposals decreases, reducing execution layer (EL) rewards, while consensus layer (CL) rewards also naturally decline along the issuance curve. Revenue per staked ETH is falling as total staking grows, and Lido's share is declining rapidly on top of that.

That said, Lido has shown some results in cost optimization. Operating expenses were reduced 10% year-over-year in 2025, saving 41% against budget. By adjusting the fee structure for Curated Module operators, who account for the majority of the Lido pool, the DAO's effective take rate was raised from 4.96% to 6.11%, a 23% increase. Revenue may have declined, but margins improved.

The utility of the LDO token is, in practice, limited to a single function: governance voting. LDO holders can vote through Snapshot (off-chain) and on-chain voting to determine key protocol parameters such as fee rates, node operator selection, treasury spending, and upgrade direction. Routine decisions are handled efficiently through EasyTrack, a streamlined governance mechanism, while significant matters are put to a full vote. Given that Lido's governance decisions can affect the entire Ethereum ecosystem, the Dual Governance system introduced in 2025 opened a governance participation path for stETH holders as well, establishing a check on unilateral decision-making by LDO holders.

However, LDO offers no economic incentives whatsoever: no direct revenue distribution, no fee sharing, no staking rewards. Even as Lido generates tens of millions of dollars in annual revenue, that income accumulates in the DAO treasury and never flows back to LDO holders. While this design was intentional to mitigate regulatory risk given LDO's nature as a governance token, the result has been a prolonged absence of any value accrual mechanism.

Voting participation is also low. Actual governance participation stands at just 5-6% of the circulating supply. If the value of a governance token derives from voting participation, it is difficult to justify the token's value when participation is this low. This criticism has been consistently raised within the community itself.

According to a governance health analysis by ChainSights posted on the Lido governance forum in February 2026, only about 170 out of more than 32,500 Lido Snapshot followers actually vote, and the top 5 wallets hold approximately 65% of all voting power. Lido's position is that many of these are treasury and CEX wallets and should not be viewed as simple power concentration, but the structural limitation of decision-making being concentrated among a small number of delegates is clear. Much of the governance discussion takes place in private group chats and meetings, and regular holders must rely on limited public information when participating in votes.

Source: CoinMarketCap

LDO's price trajectory has been brutal. Based on CoinMarketCap data, after recording an ATH of $7.24 in 2021, it entered a prolonged downtrend and fell to $0.27 on March 8, 2026, setting a new all-time low. As of March 30, 2026 when this article was written, LDO sits at approximately $0.32, down about 95.6% from its ATH. Market cap is approximately $272M, with a fully diluted valuation (FDV) of roughly $320M.

What is even more concerning is the collapse in relative value against ETH. The LDO:ETH ratio currently stands at approximately 0.00016, a 63% discount to the 2-year median of 0.00043. Over the same period, Lido's protocol revenue declined by approximately 20%, while the LDO:ETH ratio dropped by roughly 50%. In other words, the token price has collapsed far beyond what the deterioration in profitability would justify.

Of the total supply of 1 billion tokens, approximately 849 million (84.9%) are already in circulation. While the limited potential for additional selling pressure from future unlocks is a positive, it also means this is the price even with the vast majority of tokens already unlocked and available for sale.

A protocol managing $18.7B in TVL having a token market cap of just $272M translates to a TVL-to-market-cap ratio of only 0.012. This extreme gap between protocol scale and token value indicates that the token is failing to reflect the protocol's value. The community sentiment toward the token has deteriorated to the point where proposals to retire LDO entirely have appeared on the forum, and this is the direct backdrop against which the buyback proposals discussed below have emerged.

Source: Lido Research Forum

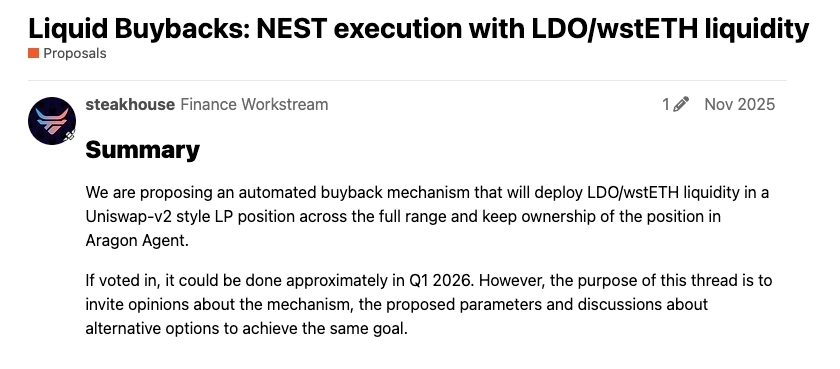

In November 2025, the Steakhouse team submitted a proposal to the Lido governance forum to build an automated mechanism for buying back LDO using surplus revenue from the DAO treasury. The core idea is not simply buying and burning or locking away LDO, but rather pairing bought-back LDO with wstETH in a Uniswap V2-style LP position that grows progressively over time. The design was inspired by MakerDAO's Smart Burn Engine.

The rationale is as follows. LDO's on-chain liquidity is extremely shallow, at roughly $90K within ±2% price impact. Straightforward buybacks would face significant slippage, and the size of each purchase would be limited. However, by deploying bought-back LDO into an LP, on-chain liquidity depth improves gradually, creating a positive feedback loop where future buybacks become more efficient. Since the LP tokens are owned by Aragon Agent, the DAO's treasury contract, the LDO locked in the LP is effectively removed from circulation.

The proposed initial parameters for activation conditions are as follows (parameters are subject to change):

ETH price above $3,000

Annualized protocol revenue (USD basis) above $40M

Distribution: 50% of treasury inflows exceeding $40M

Price impact: within 2% per purchase

Cap: $10M maximum on a rolling 12-month basis

This design is intentionally anti-cyclical. Buybacks activate only when ETH prices are high and revenue is sufficient, eliminating the risk of depleting the treasury during bear markets. Conversely, buybacks scale up more aggressively during bull markets. Lido's revenue is denominated in ETH. When ETH prices are low, the protocol accumulates ETH, and when prices rise, LDO buybacks proceed under more favorable conditions.

The execution process works as follows. First, funds are transferred to the NEST contract through EasyTrack governance. Then, a portion of wstETH is swapped for LDO via Stonks v2, and the purchased LDO is paired with the remaining wstETH into an LP position. Finally, the LP tokens are returned to Aragon Agent. NEST conducts small daily auctions targeting roughly half of daily treasury inflows (approximately 5-6 stETH), with a safety mechanism that automatically cancels the auction if the price deviates more than 2% from the oracle reference price.

The community raised several points of discussion. First, there were concerns that the $40M revenue threshold and $10M cap are overly conservative. Revenue above $40M already represents surplus after operating expenses, so limiting allocation to 50% of that surplus with a $10M cap on top was seen as unnecessarily restrictive.

Others suggested adding valuation-based triggers that reflect LDO's relative undervaluation. The ETH > $3,000 condition alone cannot capture situations where the LDO:ETH ratio is at extreme lows.

Quantitative analysis of impermanent loss (IL) from the LP approach was also conducted by the community. Monte Carlo simulations estimated average annual IL for the LDO/wstETH LP at approximately 10%. However, Steakhouse argued that since the DAO would never withdraw from this LP, the IL would never be realized, and should be viewed as an operational cost of the strategic goal of improving liquidity. The fact that a declining LDO price increases LDO's share in the pool, making buybacks more efficient, is also an intended feature.

According to Lido Labs, the manual module based on NEST has been developed and is expected to go live after Q2 2026 technical validation. Automated LDO buybacks are expected to begin within 2026.

Source: Lido Research Forum

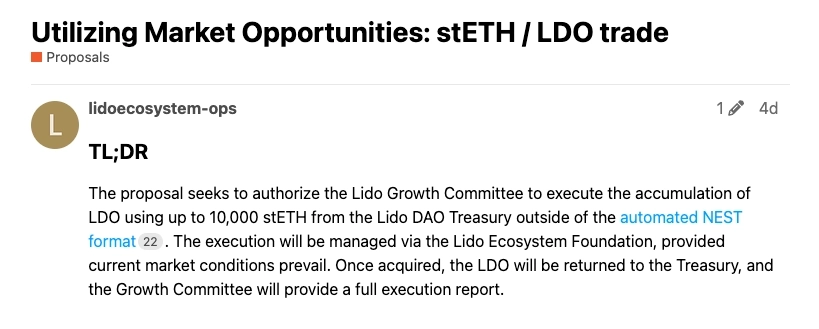

On March 27, 2026, the Lido Ecosystem Operations team posted a proposal separate from the NEST automated buyback, designed as a one-time opportunistic buy to capitalize on the current extreme price dislocation.

This proposal is straightforward since it is a one-time buyback. Up to 10,000 stETH (approximately $20M at current prices) would be withdrawn from the DAO treasury, used to purchase LDO on the open market, and the acquired LDO returned to the treasury. While NEST is a long-term automated buyback mechanism, this proposal is based on the judgment that "LDO is abnormally cheap right now, so let's buy."

The rationale behind this proposal is clear. As discussed earlier, the LDO:ETH ratio of 0.00016 represents a 63% discount to the 2-year median and a 70% discount to the typical level of ~0.0005 over the past two years. Yet during the same period, protocol revenue declined only 20%, operating expenses were cut 13%, and the fee take rate was raised 23%. The argument is that the token price is excessively discounted relative to fundamentals.

The execution structure for this one-time buyback is as follows:

Budget: up to 10,000 stETH (executed in 1,000 stETH batches)

Tolerable slippage: within 3% of the reference price

Executor: Growth Committee (through the Lido Ecosystem Foundation)

Execution channels: on-chain (CoW Swap, 1inch, Uniswap) + off-chain (Binance, OKX, and other CEXs)

Governance structure: execution report posted to the forum after each 1,000 stETH batch, followed by a new EasyTrack motion with a 3-day objection period

Before each batch is executed, the trigger price and execution window are publicly disclosed on the forum. Token holders can object through EasyTrack at any time to halt the next batch, or terminate the entire buyback program via a Snapshot vote. The proposal also explicitly states that purchased LDO will not be used for governance voting.

This type of buyback is typically executed on-chain, but this proposal is distinctive in that it explicitly permits the use of CEXs. On-chain LDO liquidity is only about $90K within ±2%, whereas Binance and OKX each offer over $100K in depth within ±2%. The design also allows OTC execution through existing market maker relationships. Of course, sending funds to CEXs carries freezing and blocking risks, so mitigation measures are included such as distributing execution across multiple exchanges and limiting batch sizes.

Community reaction has been largely positive, as the perception of LDO's relative undervaluation is widely shared. This proposal is being pursued separately from the NEST automated buyback discussed above, and also serves as a transitional measure until the NEST buyback goes live in Q2.

Lido was, for a long time, the most profitable protocol in blockchain before perp DEX platforms like Hyperliquid emerged. Yet LDO's price has fallen even more steeply than the protocol's revenue decline. Investors have come to understand that the current LDO token structure cannot reflect the value of the Lido protocol.

Lido still has formidable protocol fundamentals: $18.7B in TVL, $37.4M in annual revenue, and 21% of Ethereum staking. But LDO remains near all-time lows. While the governance-only token design may have been effective at avoiding regulatory risk, the absence of any value accrual mechanism has led long-term holders to a fundamental question: "Why should I hold this token?"

The LDO buyback proposals and their implementation represent the Lido DAO's first substantive response to this problem. One is a long-term, sustainable buyback mechanism powered by protocol revenue, and the other is a discretionary opportunistic purchase leveraging an extreme price dislocation. Both proposals aim not simply to buy and burn LDO, but to pursue the dual objectives of reducing circulating supply and improving liquidity by deploying LDO into LPs or returning it to the treasury.

However, buybacks alone will not solve the token value problem. The causes of LDO's price decline extend beyond tokenomics. The fundamental issue of Lido's continuously declining staking market share and the resulting revenue decline must be addressed. To solve this, the treasury must not be spent solely on token price defense but also actively deployed to expand the protocol's service scope and restore competitiveness. Without revenue, there are no buybacks.

In fact, in March 2026, a proposal to allocate $5M from the DAO treasury to Lido Earn's ETH/USD vaults passed a Snapshot vote. This treasury allocation serves as first-loss protection for depositors' funds. In the event of a severe loss, the DAO's vault shares would be burned to absorb depositors' losses.

I believe this structure represents the most promising direction for the Lido protocol. The biggest reason both individuals and institutions hesitate to deposit into DeFi vaults is the risk of principal loss from hacking, slashing, and similar events. If Lido's staking revenue is consistently allocated as a loss protection budget for its vaults, the vaults Lido launches would undoubtedly become a highly attractive option.

Furthermore, fixating on short-term token price increases and buybacks could actually be counterproductive. The key lies in how well the treasury generated from revenue is managed in a balanced way. Buyback mechanisms that connect token value to protocol performance, service expansion to defend against market share decline, and capital deployment to earn institutional trust: all of these draw from a single resource, the DAO treasury. Deciding where, how much, and in what order of priority to allocate these limited resources is the essence of DAO governance, and the true value of the LDO token. LDO must become important in its own right.

In blockchain projects, metrics like protocol TVL and revenue alone can no longer directly reflect a token's value. Investors have grown smarter and have begun to demand more than simply holding a token and capturing price appreciation. I do not fully agree that this shift is 100% positive.

Ethereum has the most active off-chain social governance of any blockchain, yet ETH plays no role in that governance. This is because a protocol's long-term health and growth very often conflict with short-term token price movements. If the most important thing in a protocol's governance becomes token price appreciation, the protocol is likely to fail in the long run. Perhaps it would be better to split LDO into two separate tokens: one for governance and another that shares in protocol revenue.

That said, Lido's buyback proposals carry significant meaning. The upcoming one-time buyback of $20M represents approximately 7.2% of LDO's market cap, a substantial scale. An automated, long-term sustainable buyback mechanism through NEST is also being introduced.

Lido is still a profitable protocol, but it is in a critical situation with declining revenue and market share. At this juncture, the DAO plans to allocate a significant portion of its treasury funds toward buybacks for LDO token value enhancement. Whether it is more urgent to spend funds on recovering the protocol's market share and growth, or to first establish mechanisms for long-term token value enhancement, is an extremely difficult question.

How the launch of a buyback mechanism for Lido's governance token LDO will move the token's price, and what long-term impact this will have on the future of Lido as Ethereum's largest staking protocol, is well worth watching.

Dive into 'Narratives' that will be important in the next year