What Happened?

Across Protocol, a cross-chain bridge protocol backed by Paradigm, is exploring a transition from its existing DAO structure to a corporate structure. The team recently posted a “temperature check” proposal on the governance forum to begin discussing with the community the possibility of transitioning the protocol’s operational structure from a DAO plus token model to a U.S. C-Corp structure.

If the proposal is implemented, a newly established entity called AcrossCo would become the operating body responsible for protocol development, partnerships, and commercialization. Existing ACX token holders would have two options. The first option would allow holders to exchange their ACX tokens for equity in AcrossCo at a 1:1 ratio. The second option would allow holders to redeem their tokens for USDC. The redemption price would be calculated based on the 30-day average market price, and the exchange window is expected to remain open for approximately six months.

Participation would also vary depending on the size of token holdings. Large token holders would be able to convert their tokens directly into equity. Smaller holders would likely participate through an SPV structure that allows them to hold equity indirectly. The proposal is still in the early discussion stage, and a formal governance vote could follow if the community response is favorable.

The motivation behind this structural transition comes from the team’s recognition that the DAO structure can limit institutional partnerships. Many corporate partners require a clearly defined legal counterparty and accountable entity for contractual agreements. As a result, it is often difficult to execute large-scale business agreements using a DAO structure alone.

Researcher’s Comment

What makes this proposal interesting is that it is not simply a governance change. It represents a direct experiment at the boundary between token economics and traditional equity structures. Most DeFi projects have historically relied on tokens to simultaneously grant governance rights and economic participation. However, when it comes to real-world business operations such as institutional partnerships, legal agreements, and intellectual property management, token-based DAO structures have increasingly revealed their limitations.

Across’ proposal can be seen as a practical compromise to address this issue. The protocol itself would remain a permissionless infrastructure, while business operations and commercialization would be handled through a corporate entity. In other words, the software would continue to operate as a decentralized network, while corporate activities would follow a traditional company structure. This can be viewed as a hybrid model combining a protocol and a company.

More importantly, the proposal introduces the possibility that token holders could transition from simple governance participants into actual shareholders. If this model is successfully implemented, it could signal a broader shift in how tokens are defined within DeFi projects. Instead of functioning purely as utilities or governance instruments, tokens could begin to resemble assets that carry economic rights closer to those of equity.

This development could also influence the structure of the token market itself. Many project tokens have historically struggled to establish clear value capture mechanisms beyond governance participation. If token-to-equity conversion becomes a viable model, tokens may begin to be perceived not only as network assets but also as capital assets similar to venture investments.

Ultimately, the Across experiment brings back a fundamental question within the Web3 industry. It forces the ecosystem to once again confront the question of whether a token can or should function as a form of equity.

What Happened?

In March 2026, Nasdaq announced plans to build a tokenized equity infrastructure in partnership with Payward, the parent company of the cryptocurrency exchange Kraken. The goal of this collaboration is to create an “equities transformation gateway” that connects traditional capital markets with blockchain networks. The framework aims to establish a structure that directly links regulated equity markets with decentralized finance ecosystems.

Under this framework, tokenized equities representing publicly listed shares on a 1:1 basis would be issued. These tokens would be designed to carry the same rights as traditional shares. Mechanisms are also being considered to automate corporate actions such as shareholder voting and dividend distribution using blockchain infrastructure.

Kraken would serve as the global distribution partner within this structure. Tokenized versions of Nasdaq-listed stocks would be made available to Kraken users, allowing investors to trade equity tokens within a blockchain-based environment. Nasdaq’s longer-term objective is to build an equity market that can operate on a 24-hour basis. The framework could potentially launch as early as 2027.

This collaboration is built on Kraken’s xStocks infrastructure. xStocks is a tokenized equity framework backed by real shares held as collateral. Since its launch, the platform has reportedly processed more than 25 billion dollars in cumulative trading volume and attracted over 80,000 users.

Researcher’s Comment

Early tokenized equity projects mostly relied on an indirect tokenization model. In this structure, a third party holds the underlying shares and issues tokens that track the value of those shares. However, token holders in these systems often do not have legal ownership of the underlying equity. Combined with regulatory risks and liquidity limitations, this structure has prevented the market from achieving meaningful scale.

The Nasdaq model differs in a critical way. The key point is that the issuer participates directly in the structure. Tokenized equities maintain the same rights structure as traditional shares and connect directly to official market infrastructure. In this setup, the token becomes not just a price-tracking instrument but a digital representation of an actual security.

This shift has the potential to significantly reshape the boundary between traditional finance and the crypto market. If shares of major publicly listed companies can be issued as tokens and move freely within onchain environments, equities may evolve from assets traded only on exchanges into programmable financial assets that can be utilized within DeFi ecosystems.

Ultimately, this collaboration signals a broader shift in the direction of tokenized finance. The model appears to be moving away from tokenized assets created by crypto-native companies toward onchain securities issued directly by traditional financial institutions. This transition could become one of the most important structural changes within the emerging RWA market.

What Happened?

Hong Kong’s financial regulators are expected to announce the first recipients of stablecoin issuance licenses under the city’s new regulatory framework. According to reports, a consortium led by HSBC and Standard Chartered is being widely viewed as a leading candidate for the initial licenses.

The Hong Kong Monetary Authority introduced the Stablecoin Ordinance in August 2025, establishing a licensing framework for fiat-referenced stablecoins. Under this regime, any entity that intends to issue stablecoins in Hong Kong or issue Hong Kong dollar-linked stablecoins overseas must obtain a license from the HKMA.

So far, the HKMA has received 36 formal applications. During the initial stage, regulators plan to grant licenses to only a small number of issuers. Industry sources suggest that the first approvals could be announced as early as late March 2026.

HSBC and Standard Chartered have attracted particular attention as potential early issuers because both banks already hold banknote issuance rights in Hong Kong. Regulators are reportedly prioritizing large financial institutions in the early stage in order to ensure stability and credibility in the market.

Standard Chartered has also been preparing to issue a Hong Kong dollar-linked stablecoin through a joint venture with Animoca Brands and the Hong Kong telecommunications company HKT. The consortium previously participated in the HKMA’s stablecoin sandbox program.

The regulatory framework requires stablecoin issuers to maintain reserves backed by high-quality liquid assets, guarantee one-to-one redemption, segregate customer assets, and comply with strict anti-money laundering regulations.

Researcher’s Comment

One of the most notable aspects of Hong Kong’s stablecoin policy is that the initial issuance structure appears to be designed around banks. HSBC and Standard Chartered are currently being discussed as potential candidates for the first licenses, and regulators are expected to approve only a very small number of issuers in the early stage.

This direction is already reflected in the regulatory design itself. Hong Kong’s stablecoin regime requires issuers to maintain one hundred percent reserves, implement strict anti-money laundering controls, maintain comprehensive risk management systems, and guarantee redemption within one business day. These requirements are effectively comparable to bank-level regulatory standards. As a result, large banks or institutions working in consortium with banks naturally emerge as the most viable candidates for early licenses.

This approach prioritizes financial stability over the speed of innovation. Hong Kong does not appear to view stablecoins as independent crypto products. Instead, regulators are designing them as regulated financial assets that can function within the payment and settlement infrastructure of the traditional financial system. Authorities have also signaled that they intend to expand the market gradually by adopting a “stricter before looser” strategy during the early stages of implementation.

Crypto

Ethereum Foundation sells 5,000 ETH to Tom Lee's BitMine in $10 million OTC deal

Optimism's OP Labs cuts 20% of staff to 'do fewer things well'

Aave suffers oracle glitch, triggering $26 million in unfair wstETH liquidations

Institution

BlackRock's staked Ethereum ETF records over $15.5 million volume on first day

Wells Fargo files 'WFUSD' trademark covering crypto trading, payments and tokenization services

Grayscale debuts Avalanche staking ETF on Nasdaq under ticker GAVA

SEC and CFTC commit to work together on crypto policy and introduction of new products

Mastercard launches global crypto partner program with Binance, Ripple and more

Nasdaq partners with Kraken parent Payward to link tokenized equities with DeFi networks

Tech

Investment

Asia

Metaplanet launches VC and asset management subsidiaries, bets on Japanese stablecoin JPYC

TOKEN2049 Dubai moved to 2027 amid heightened security risks in UAE

South Korea crypto exchange Bithumb hit with suspension, CEO faces disciplinary action

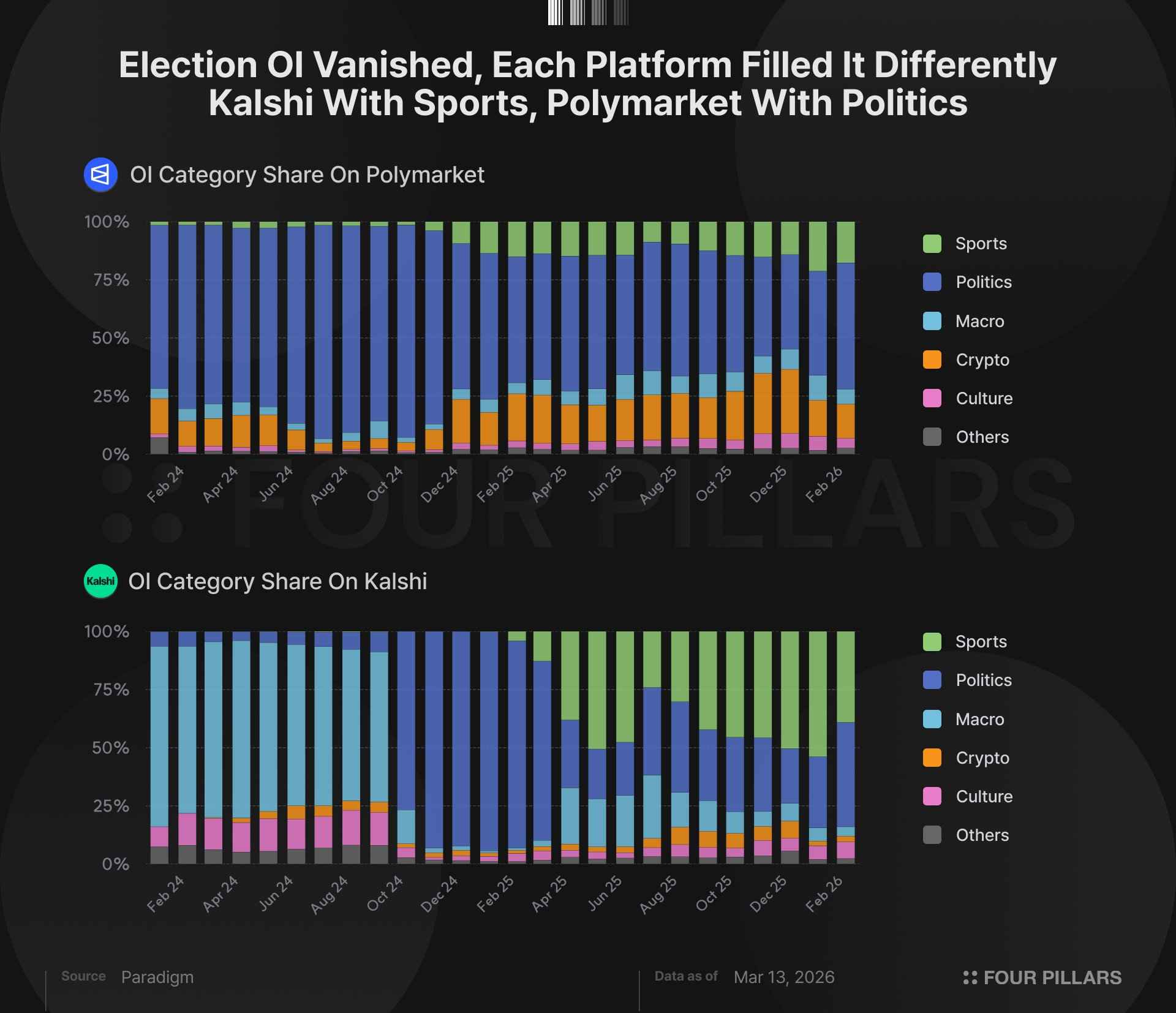

Kalshi's category evolution is dramatic. During the 2024 election, politics consumed over 90% of all OI. Now it's roughly split between politics (~41%) and sports (~46%), with culture (~6%) and macro (~4%) filling the rest. From a single-category platform to a much more balanced mix.

Polymarket also hit 95%+ politics during the 2024 election. But unlike Kalshi, it stayed politics-heavy at 54% today. Still, diversification is happening. Sports went from barely ~1% in early 2024 to ~21%, and crypto holds a steady ~13%. The category mix is broadening, especially after the December 2025 US re-entry.

The category split reveals two completely different user bases. Kalshi's crypto OI share is just ~2%, Polymarket's is ~15% (reflecting its crypto-native origins). Sports is the inverse: Kalshi ~46% vs Polymarket ~21%. Same industry, but completely different user profiles. Mainstream sports bettors are flocking to Kalshi, while crypto-native users with political interests are concentrating on Polymarket.

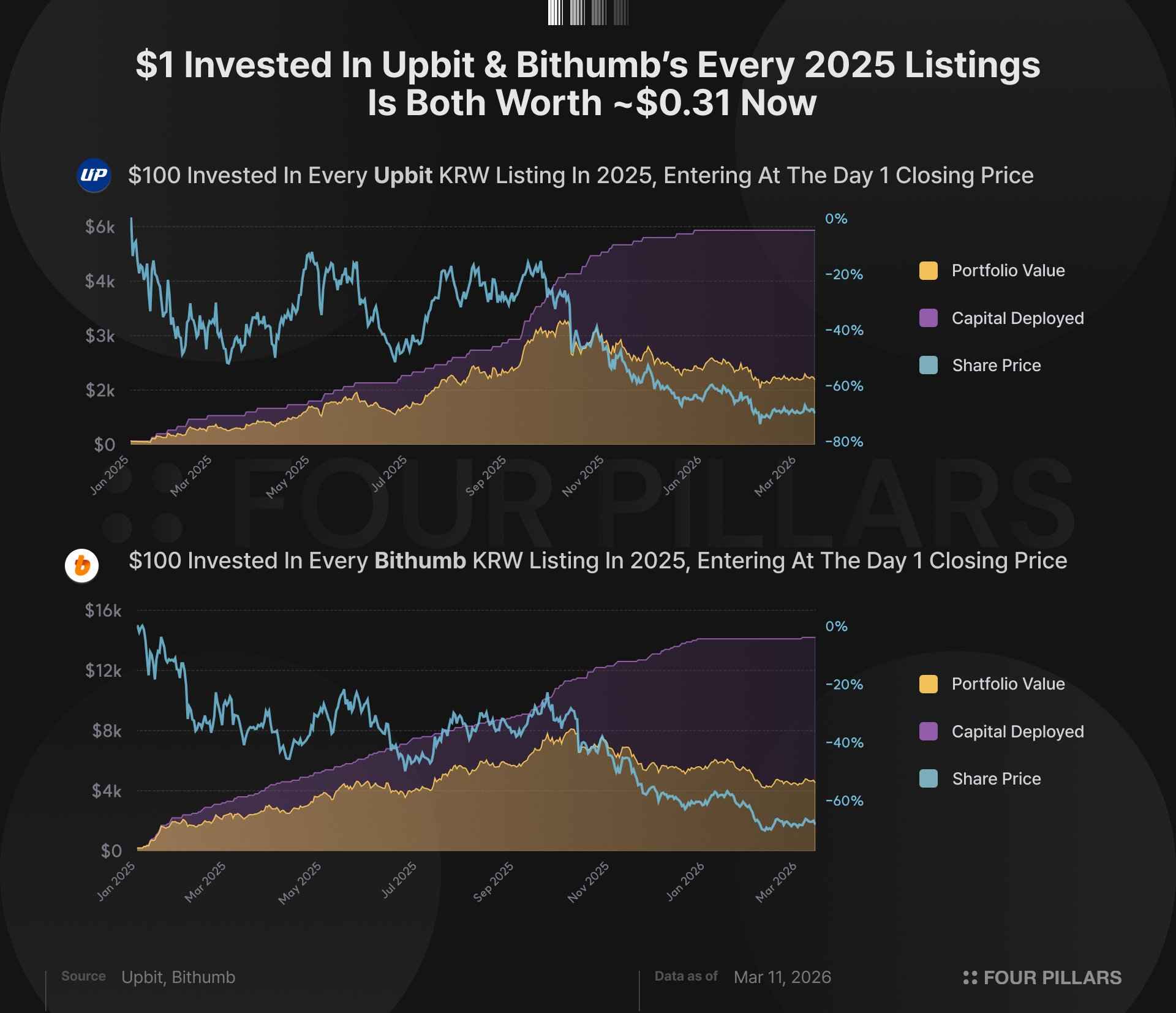

Buying every new listing on Upbit and Bithumb in 2025 at day-1 close left you with roughly $0.31–$0.32 per dollar invested. Both exchanges delivered about a 70% loss.

Out of all listings combined, only a handful posted positive returns. KITE was the standout on both exchanges (+233% on Upbit, +210% on Bithumb). The rest of the winners were gold-linked tokens like XAUT and PAXG, or late-year listings that simply haven't had time to bleed yet.

Bithumb listed 2.4x more tokens than Upbit but ended up in the same place. More listings didn't mean more opportunities. It just meant more ways to lose money at the same rate.

Interestingly, Binance wasn't much different either. According to c4lvin's analysis, Binance's 2025 listings returned -71.7%, worse than both Korean exchanges. The listing event itself structurally works against day-1 buyers, regardless of the exchange.

Lido's Curated Module (CM) is the core module responsible for roughly 92% of all stETH staking volume. However, the limitations of its original design are becoming increasingly apparent: a rigid fee structure, inflexible stake allocation, and an accountability framework that relies solely on reputation.

The 0x02 validator type (EIP-7251) introduced in Ethereum's Pectra upgrade raised the maximum effective balance per validator from 32 ETH to 2,048 ETH. This shift demands an architecture-level redesign for large-scale staking protocols like Lido.

CMv2 aims to transform the Curated Module from a "managed registry" into a "Validator Marketplace" through the introduction of bond-based economic accountability, a seven-category node operator classification system, streamlined governance, and native 0x02 support.

The full migration is expected to take approximately 4.5 to 6 months and will incur an estimated protocol-level reward loss of around 738.5 ETH. This will be the largest infrastructure transition in Lido's history.

Three months in, 39 points separates two Nasdaq-listed vehicles holding the same asset. The gap comes down to three structural variables in order: warrant topology, accretion rate, mNAV.

PURR is passive treasury accumulation. HYPD is active DeFi participation with a validator business that earns commission on third-party capital. Both theses are internally coherent.

The most important data point for HYPD drops April 14, the 10-K.

If you had invested $100 in each of the 59 tokens newly listed on Upbit in 2025, your portfolio would be worth roughly $0.31 per dollar as of March 11, 2026. Bithumb (144 tokens) shows the same figure at $0.31, and Binance (92 tokens) comes in at $0.29. All three exchanges delivered approximately 70% losses.

Of Upbit's 59 tokens, only two ended in profit: KITE (+232.8%) and BARD (+9.3%). Bithumb fared only marginally better, with just 8 out of 144 tokens in the green. The median ROI was -80.9% for Upbit and -82.1% for Bithumb.

The average ROI of the 50 tokens listed on both major Korean exchanges (-69.4%) was virtually identical to that of the 94 tokens listed exclusively on Bithumb (-68.9%). This suggests that being listed on multiple major exchanges offers no guarantee of subsequent price performance.

DVT is key infrastructure for removing single points of failure in validator operations. SSV Network has implemented it as a permissionless protocol accessible to anyone, and it has grown into an infrastructure layer used by about 17% of all ETH staked on Ethereum. Within the DVT market, it has effectively become the standard.

The essence of the SSV tokenomics essence is a redefinition of the token's role. The previous utility, as a fee payment gate, is removed through the shift to ETH. In its place, cSSV is given two functions: the right to receive a share of network fees in ETH and the right to participate in oracle selection.

The practical effect of the transition will depend on execution. The main points to watch are whether the Effective Balance Oracle can move to a decentralized model, whether cSSV can secure DeFi liquidity, and whether the bApps ecosystem can show visible progress.

Across Protocol has posted a proposal to dissolve its DAO and token structure, transitioning to a U.S. C-Corporation called AcrossCo. ACX token holders are offered two options: a 1:1 token-to-equity conversion, or a USDC buyout at $0.04375, a 25% premium over the 30-day average price. Following the announcement, ACX surged approximately 85%, with the market reacting strongly to the "token-to-equity conversion" narrative itself.

Recent developments, including Backpack's token-to-equity staking and the sidelining of TNSR holders during Coinbase's acquisition of Vector, illustrate how rapidly the boundary between tokens and equity is being redrawn.

At the same time, Uniswap's fee switch, Sky's buyback program, and Aave's revenue-sharing proposal demonstrate that it is possible to imbue tokens with economic value within a DAO structure, suggesting that token-equity convergence is not the only path forward.

Across's experiment is not an isolated event. It represents a broader industry-wide reckoning with the legal structures of crypto projects and the fundamental value proposition of tokens. The solutions, however, are not one-size-fits-all; the optimal path depends on each protocol's revenue structure and business model.

Dive into 'Narratives' that will be important in the next year