Three months in, 39 points separates two Nasdaq-listed vehicles holding the same asset. The gap comes down to three structural variables in order: warrant topology, accretion rate, mNAV.

PURR is passive treasury accumulation. HYPD is active DeFi participation with a validator business that earns commission on third-party capital. Both theses are internally coherent.

The most important data point for HYPD drops April 14, the 10-K.

Note: PURR financials reference their 4Q25 10-Q (period ended Dec 31, 2025). HYPD financials reference their 3Q25 10-Q (period ended Sept 30, 2025). Market data as of Mar 6, 2026.

PURR (Hyperliquid Strategies, formerly Sonnet BioTherapeutics) came out of a reverse recapitalization with Atlas Merchant Capital. CEO David Schamis is from Atlas, Bob Diamond chairs the board as former CEO of Barclays, and they closed with $300M cash plus 12.5M HYPE contributed at $580M fair value. The strategy is accumulate HYPE, buy back shares, grow the per-share ratio, repeat.

HYPD (Hyperion DeFi, formerly Eyenovia) is asking a different question. They pivoted from ophthalmic drug delivery in July 2025, raised $50M PIPE plus $30M ATM, and built out an active DeFi operation under CEO Hyunsu Jung, a co-branded validator with Kinetiq that earns commission on third-party delegations, a liquid staking token called HiHYPE, HAUS agreements with Credo and Felix, 300K HYPE allocated to Native Markets supporting the USDH stablecoin. The thesis isn't just own HYPE but participate in what HYPE is building and capture yield from infrastructure that scales independently of HYPE's price.

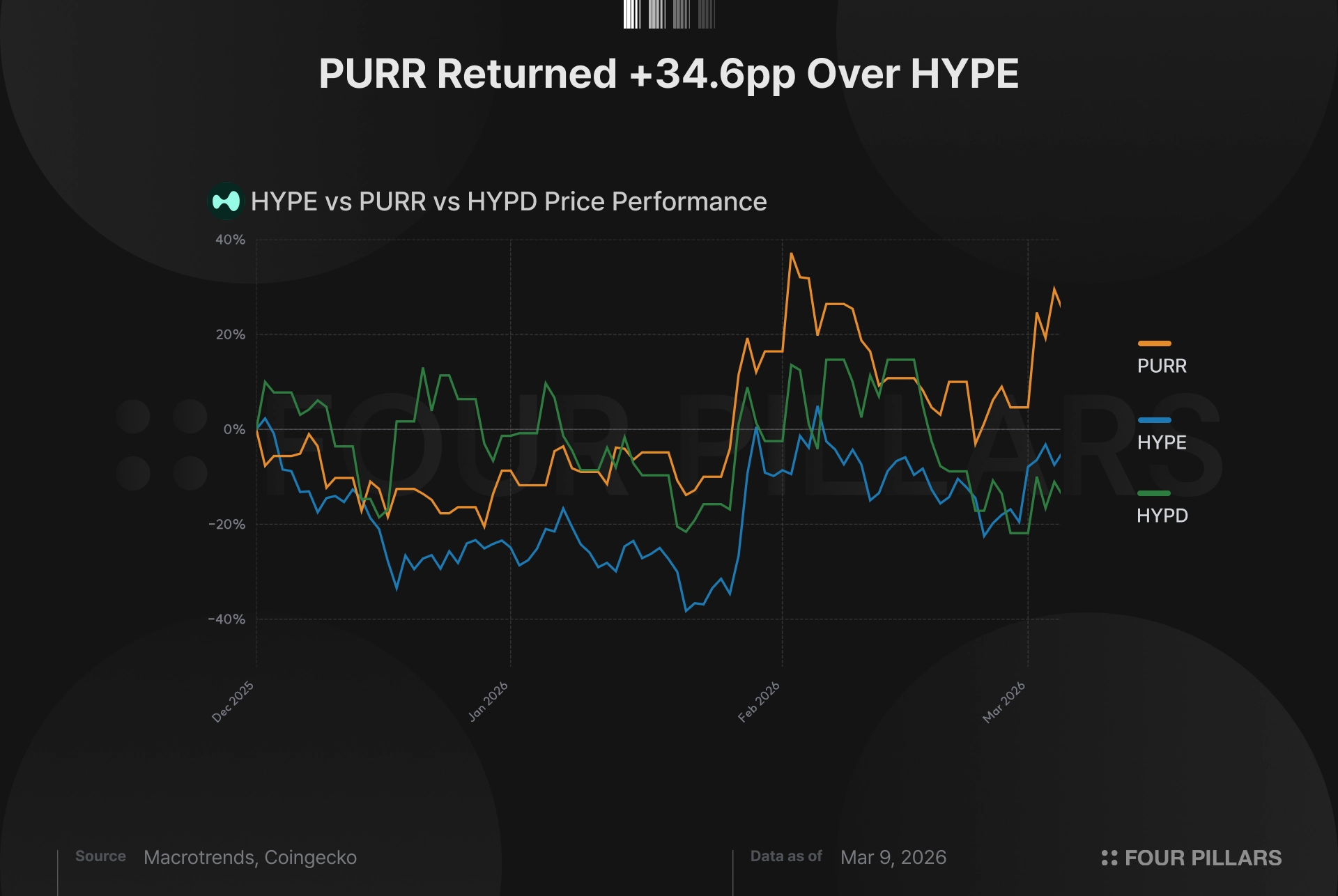

Same Nasdaq listing, same underlying asset. Over the three months we're looking at, HYPE returned -9.7%, PURR returned +24.9%, HYPD returned -14.1%.

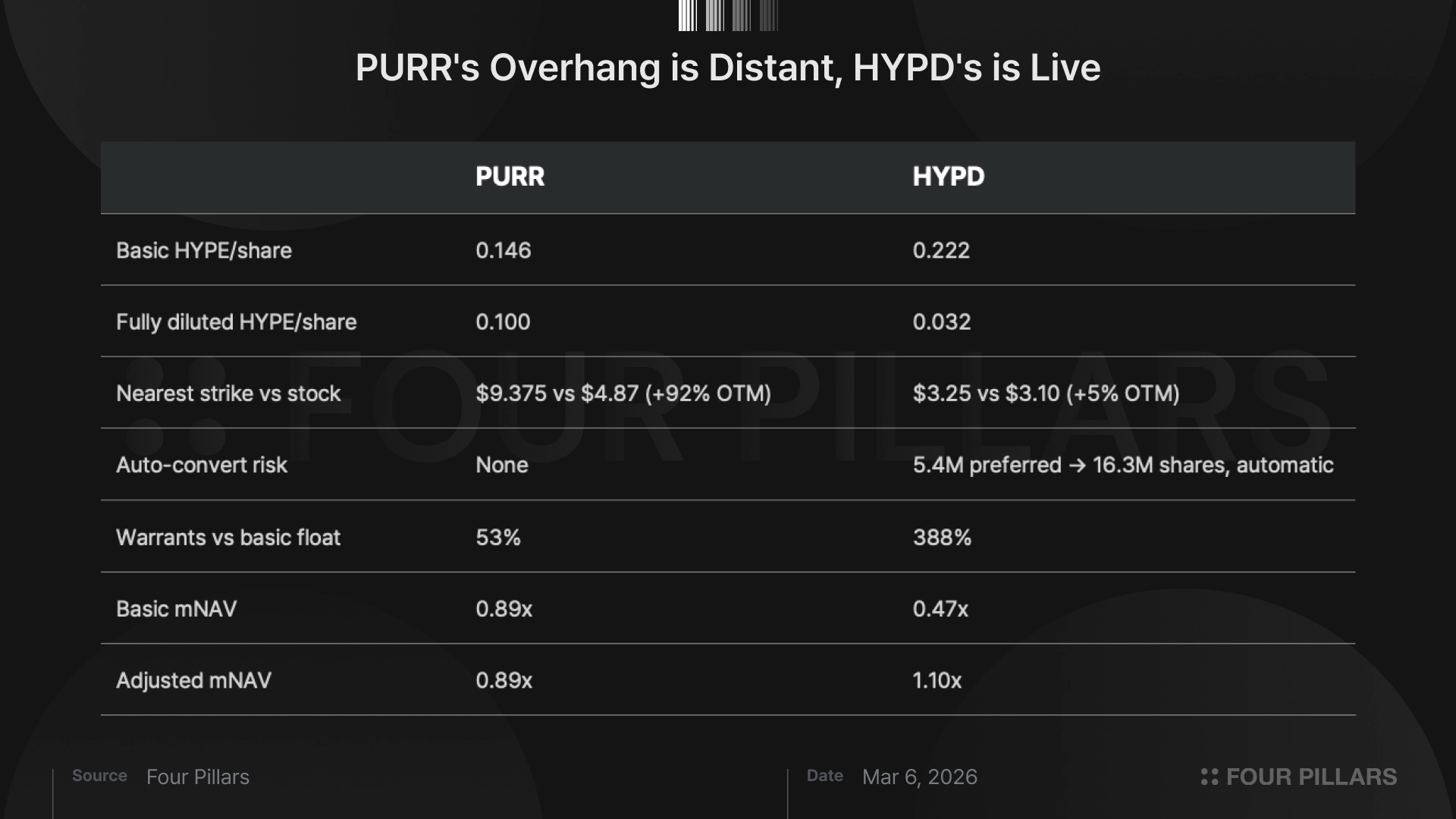

On basic shares HYPD looks better (0.222 HYPE per share against PURR's 0.146), and you'd wonder why HYPD isn't trading at a premium. Fully diluted it reverses, PURR at 0.100 versus HYPD at 0.032, but the number that matters is which dilution is live at current prices.

PURR's dilutive stack is 26.6M preferred conversion shares at $6.25 and 29.8M warrants at $9.375, $12.50, and $18.75 against a $4.87 stock, so 90 to 280% out of the money. The basic-to-FD gap of 31% is real on paper and irrelevant in practice because none of that paper is getting exercised anytime soon.

HYPD's dilutive layer reflects how you capitalize an active strategy. The 5.4M Series A preferred shares convert automatically at 3:1 into 16.3M common with no exercise price — no optionality, just a near-doubling of the share count the moment it triggers. And then 32.6M warrants sit at a $3.25 strike against a $3.10 stock, which is $0.15 out of the money and represents 3.9x the current basic float. HYPD's intraday high on March 5 was exactly $3.25. That's the warrant strike functioning as a ceiling because anyone who knows the structure knows what happens if it breaks through. That said, If those warrants do exercise, $106M in proceeds flows into NAV, meaning real capital for ecosystem deployment and not just dilution.

This is why mNAV tells two different stories depending on which version you use. Basic mNAV is PURR at 0.89x ($603.7M market cap against $674.8M NAV) and HYPD at 0.47x ($26.0M against $54.9M gross NAV). Adjusted mNAV folds in warrant exercise proceeds and the resulting share expansion, keeps PURR at 0.89x because its warrants are irrelevant and flips HYPD to 1.10x.

Basic asks what the equity is worth if nothing converts, and adjusted asks what it's worth if everything does. For a passive treasury those answers converge. For an active one capitalized with near-money warrants they're 63 points apart, and the $3.25 ceiling makes the gap self-reinforcing.

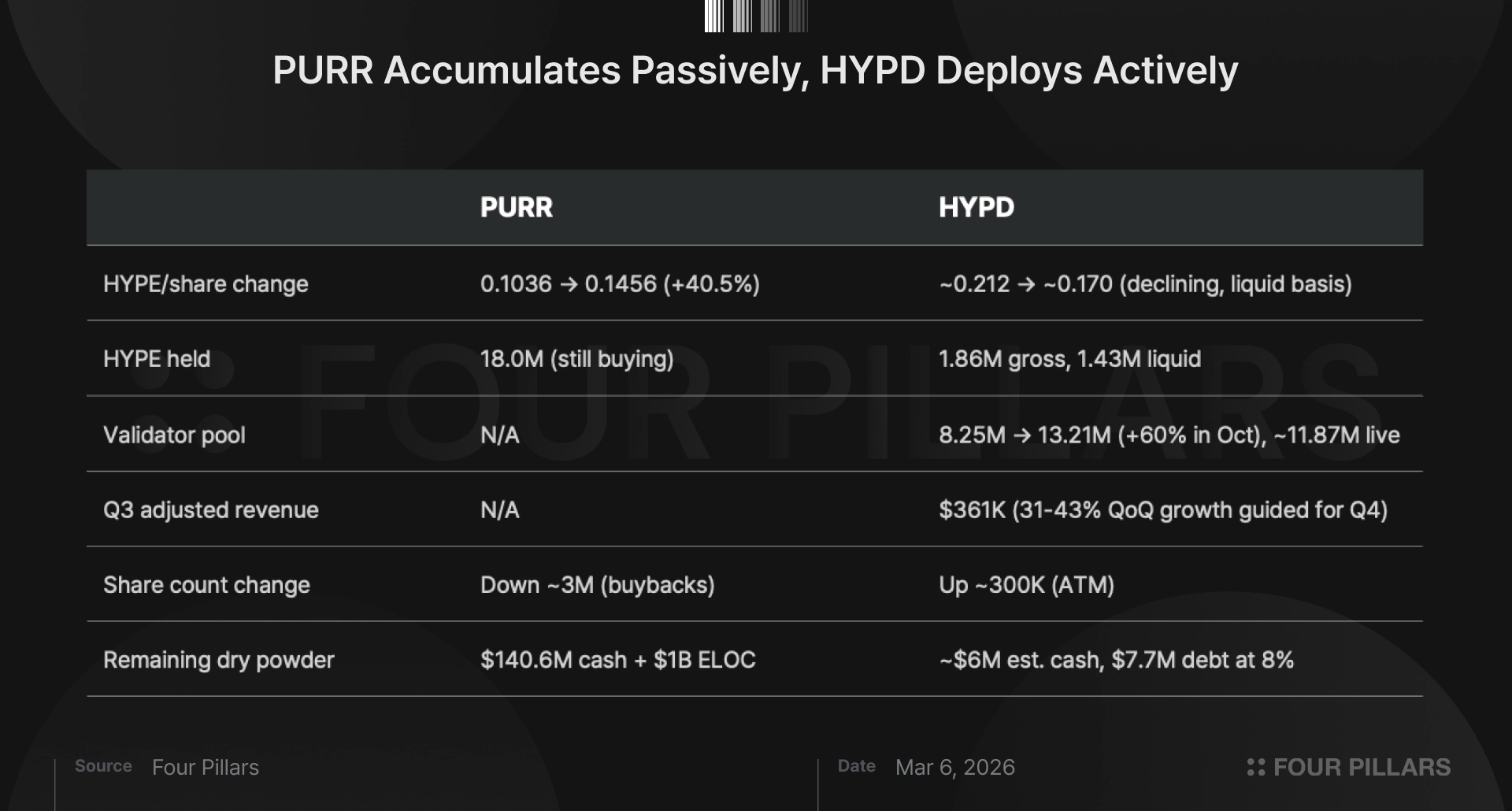

PURR grew from 0.1036 HYPE per share at close on December 2nd to 0.1456 by early March, 40.5% in three months, and their live dashboard now shows 18.0M HYPE held. They deployed $129.5M buying roughly 5M additional HYPE and used $10.5M to buy back around 3M shares with zero new issuance the whole time. $140.6M in cash and a $1B equity line with Chardan sit untouched because drawing it makes sense above 1.0x mNAV and they're at 0.89x. Cross that threshold and the standard DAT playbook opens (issue equity at premium, buy HYPE, grow per-share exposure, stock re-rates, repeat).

The punchline is in the chart. PURR beat HYPE by 35 points during a drawdown. That's what happens when you're deploying cash into a falling asset while simultaneously shrinking the share count. Spot HYPE recovered from -30% back to -10%. PURR recovered the same distance but on significantly more HYPE per share, and the market re-rated the equity toward NAV on top of that. The structure, not the asset, produced the return.

HYPD's Q3 headline is $6.6M net income and $7.95M adjusted EBITDA on a $26M market cap, and the more interesting line underneath is the validator. The 8.25M and 13.21M staked HYPE figures in the supplement represent the total validator pool (HYPD's own staked HYPE plus third-party delegations) on which HYPD earns 4% commission. With HYPD's gross HYPE at 1.86M, the bulk of that pool is external capital choosing their infrastructure.

That pool grew 60% in a single month from 8.25M in September to 13.21M in October and currently sits at roughly 11.87M per live staking data. Let's say it stabilizes around 12M HYPE at a $30 price and 2.2% APR with a 4% commission cut. That's roughly $320K annualized from capital that largely isn't even HYPD's to deploy.

Meanwhile, the KNTQ airdrop, 1.92M tokens from the Kinetiq TGE, adds balance sheet exposure to Kinetiq's growth that no passive treasury can replicate structurally.

CFO David Knox guided 31-43% QoQ adjusted revenue growth for Q4, which the April 10-K will confirm or not.

On the treasury side, gross HYPE is 1.86M with liquid at 1.43M as roughly 435K HYPE sits deployed across Felix, Native Markets, and Kinetiq. Shares grew ~300K via ATM and HYPD carries $7.7M in Avenue Capital debt at 8% interest on a $26M market cap. The ATM shelf can't run accretively at $3.10 against $6.54 basic NAV per share (every ATM share sold is equity at roughly half book). Management bought 189K shares in December at $3.14 to $3.59, the CFO personally put in $100K worth, and the basic NAV discount they're buying into is pretty wide.

For any DAT, the evaluation sequence is warrant topology first because that determines which mNAV version is meaningful and whether the accretive equity loop is accessible, accretion rate second because HYPE per share is the real scorecard regardless of where the stock trades on any given day, and mNAV last with which version to use falling out of step one automatically.

By that sequence, PURR's trigger is mNAV crossing 1.0x, at which point the equity line activates and the flywheel starts. HYPD's immediate variable is the stock holding above $3.25, which brings $106M in fresh capital but also drops 32.6M shares onto an 8.4M basic float — dilutive, but it also funds the next phase of ecosystem deployment. And then the validator pool trajectory each quarter, because that's the revenue line that scales without requiring HYPD to sell more equity at half book.

April 14 is the date that matters most for HYPD. HYPD's 10-K drops with full yield figures, treasury reconciliation, updated cash balance, and whether the warrant structure has changed. The Q4 revenue guidance is aggressive, 31-43% growth off a $361K base gets you to somewhere between $474K and $516K, and whether the validator commission and HAUS fees are moving that number is what the 10-K will show.

Data gaps: HYPD's current cash balance is estimated at ~$6M (last confirmed $8.2M at Sept 30, 2025). Reconciliation between 1.43M liquid HYPE and 1.86M gross requires the 10-K. PURR's cash may be lower than $140.6M if additional purchases occurred since Feb 11. Validator pool commission economics are estimated based on publicly available APR and stake data — actual Q4 revenue figures will be confirmed in the 10-K. I have no disclosed position in either PURR or HYPD.

Dive into 'Narratives' that will be important in the next year