Nasdaq recently announced plans to build infrastructure for tokenized equities. Along with the announcement, it outlined four core goals.

Maintain control: Even after tokenization, shareholder rights and regulatory frameworks remain unchanged.

Operational automation: Voting, dividends, investor communication, and corporate actions will be handled through smart contracts.

24/7 global trading: The goal is to create a market where global investors can trade around the clock.

Permissionless market connectivity: Build a bridge that connects traditional financial markets with onchain markets.

Nasdaq’s tokenized equities will be legally identical to existing shares, and the system will connect to the DTCC settlement infrastructure.

One detail worth paying close attention to is Nasdaq’s plan to partner with Kraken to enable permissionless market connectivity.

Kraken plans to build something called the Equities Transformation Gateway, an infrastructure layer that allows equities from traditional financial markets to be used on permissionless onchain markets. Kraken’s parent company Payward will function as the settlement layer within this system.

Kraken is already active in Europe. It operates with a MiCA license and also holds a MiFID II license, meaning it is capable of offering tokenized equities to European investors.

This direction is not new for Kraken. The company has been investing in tokenized equity infrastructure for years. One notable example is its 2025 acquisition of Backed Finance, the company behind the xStocks service.

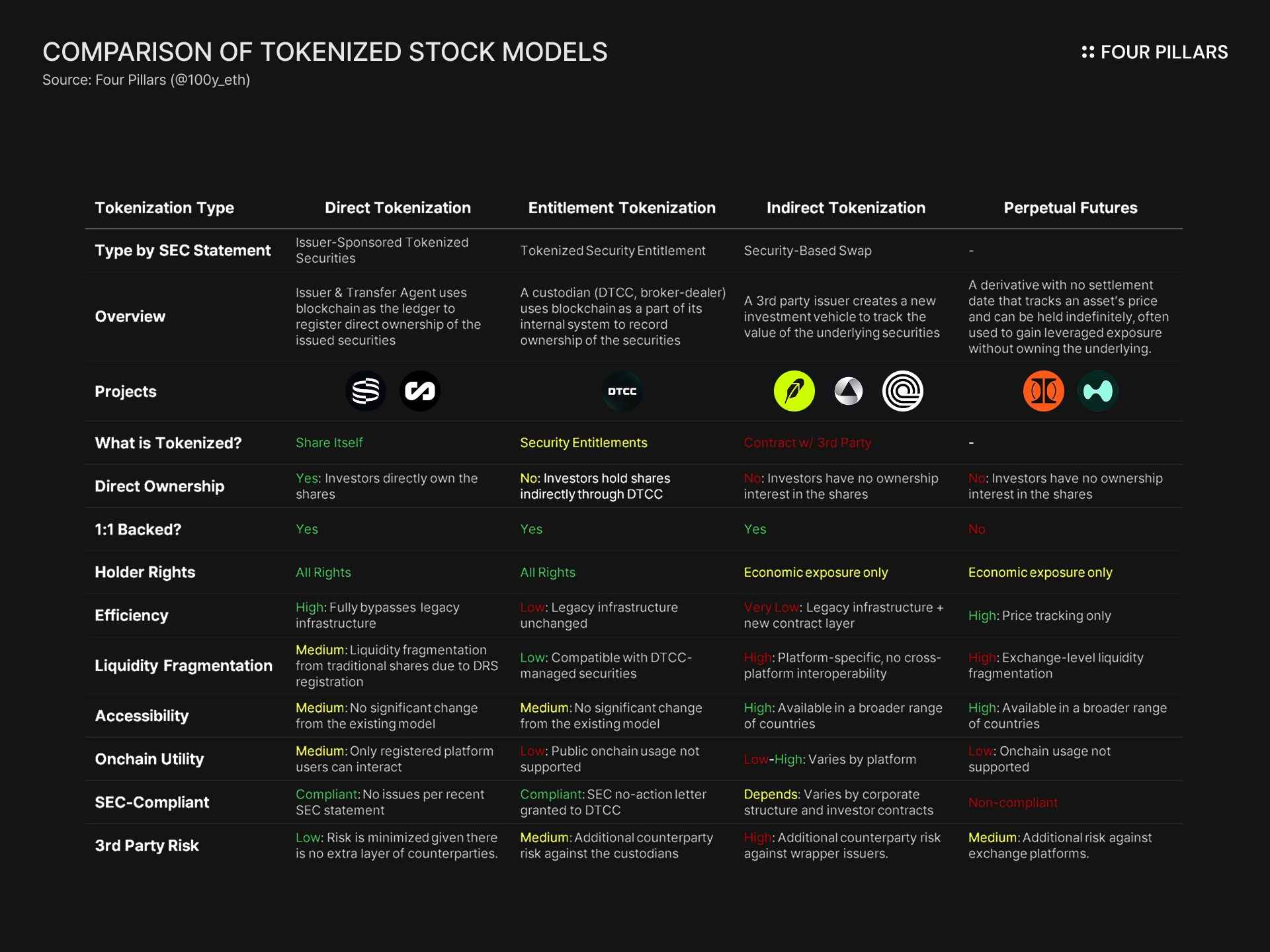

However, the tokenization model used by xStocks today is what’s known as “indirect tokenization.”

Under this model, Backed Assets Ltd., a Jersey-based SPV, purchases shares on behalf of users. Those shares are then held by a licensed custodian, and what gets tokenized onchain is a derivative contract referencing those shares.

In other words, xStocks currently provides price exposure to equities rather than the actual shareholder rights. This structure is best understood as a transitional tokenization model.

But if you look closely at the newly announced partnership with Nasdaq, it strongly suggests that xStocks may evolve beyond this transitional structure. The future model would likely grant the full set of shareholder rights while complying with regulatory requirements.

xStocks is not the only project moving in this direction. A number of platforms that previously relied on indirect tokenization models are now preparing to transition toward fully regulated tokenization frameworks.

Take Ondo Global Markets as an example. Today it offers indirectly tokenized equities using a BVI-based SPV structure. Recently, however, Ondo submitted a filing to the SEC, hinting at plans to shift toward a regulatory-compliant tokenization model.

Ondo is also well positioned for such a transition. The firm previously acquired Oasis Pro, giving it access to infrastructure that includes licenses for transfer agent, broker-dealer, and ATS operations. That foundation could support a move toward compliant equity tokenization.

Robinhood is moving along a similar path. In early 2025, the company submitted a policy proposal to the SEC asking for a regulatory framework that would allow real-world assets to be tokenized on blockchain networks.

Robinhood currently relies on an indirect tokenization structure as well. But once the regulatory environment for RWA tokenization in the United States becomes clearer, the company could pivot toward a compliant model and expand services to U.S. users.

The direction of equity tokenization is becoming increasingly clear.

The industry is moving toward direct tokenization or entitlement tokenization, where token holders gain actual rights tied to the underlying asset.

Indirect tokenization appears to be only a temporary bridge.

The more interesting question going forward is what happens once U.S. regulations become clearer. When that moment arrives, it will be worth watching how direct tokenization and entitlement tokenization models coexist within the same ecosystem.