What Happened?

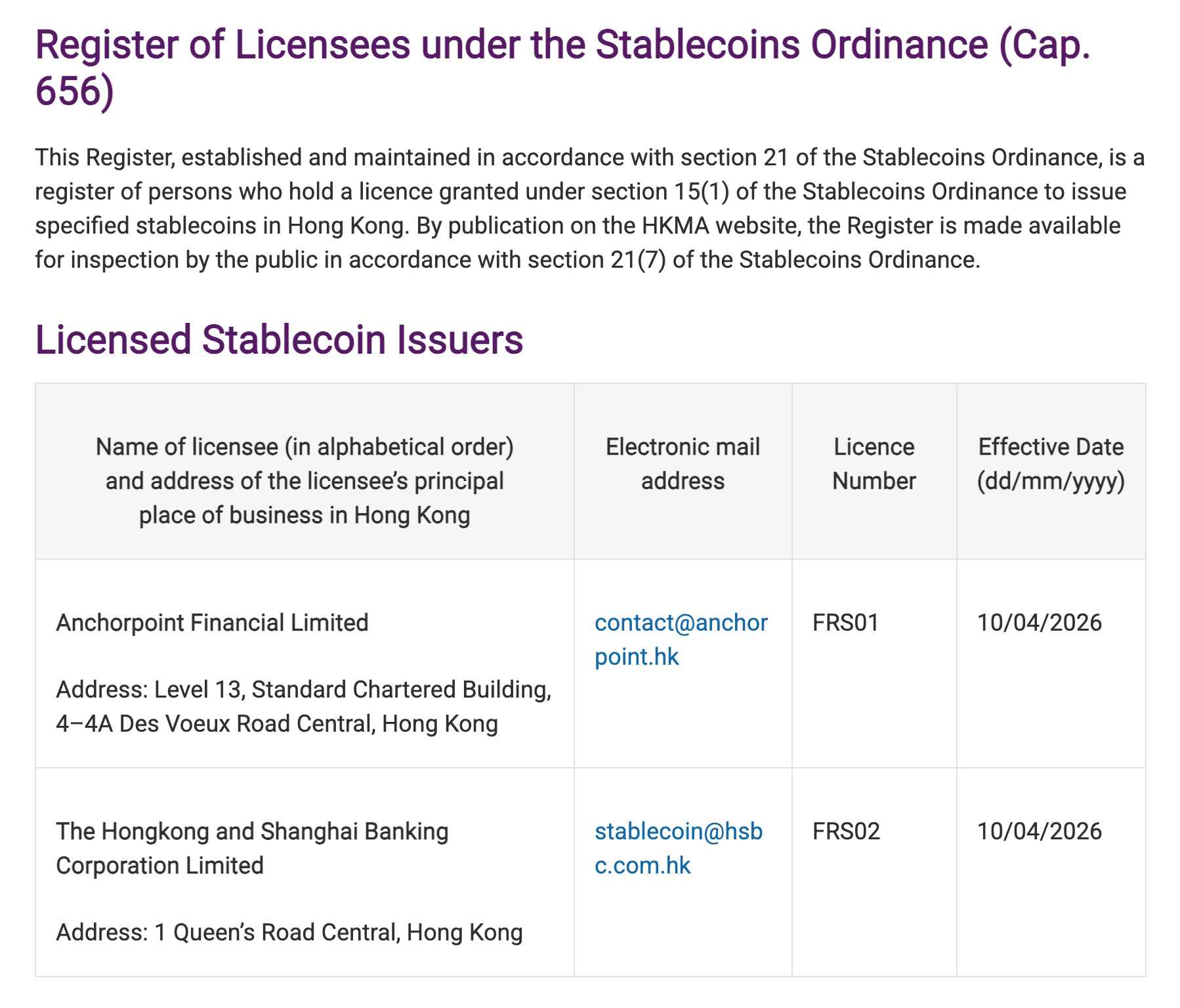

Source: Hong Kong Monetary Authority

On April 10, 2026, the Hong Kong Monetary Authority (HKMA) granted its first stablecoin issuer licenses under the Stablecoins Ordinance (Cap. 656). The two recipients are HSBC, one of Hong Kong's note-issuing banks, and Anchorpoint Financial, a three-way joint venture led by Standard Chartered. The approvals came eight months after the ordinance took effect on August 1, 2025.

The Stablecoins Ordinance, which came into force on August 1, 2025, is Asia's first standalone stablecoin legislation. It establishes a licensing regime for issuers of Fiat-Referenced Stablecoins (FRS). Issuers must incorporate in Hong Kong, hold minimum paid-up capital of HK$25 million (waived for licensed banks), maintain 100% high-quality liquid reserves in bankruptcy-remote segregated trust accounts, offer redemption at par within one business day, and undergo regular independent audits. Interest payments by issuers are legally prohibited. Unlike Singapore, which limits issuance to SGD and G10 currencies, Hong Kong's framework imposes no currency restriction. HKD, USD, EUR, and CNH are all permitted. Unlicensed foreign stablecoins such as USDT and USDC are accessible only to professional investors.

HSBC is one of Hong Kong's three note-issuing banks with direct authority to print Hong Kong dollar banknotes. Until now, HSBC has concentrated its digital asset capabilities on two pillars other than stablecoins. The first is its Tokenised Deposit Service (TDS) for corporate clients, launched in Hong Kong and Singapore in May 2025 and since expanded to the UK and Luxembourg, with live transactions currently running across four countries and five currencies. The second is its digital bond platform Orion, which has supported cumulative digital-native bond issuance of $3.5 billion, including the Hong Kong government's HK$10 billion digital green bond issued in November 2025, the largest of its kind globally.

Anchorpoint Financial took an entirely different route. Established in February 2025 as a three-way joint venture between Standard Chartered, Animoca Brands, and HKT (Hong Kong Telecommunications, the city's largest telecom operator), with Standard Chartered as the lead shareholder. The JV entered the HKMA sandbox in July 2024, testing use cases such as tokenized payroll processing and cross-border settlement, and was the first applicant to formally signal its license application on the ordinance's effective date of August 1, 2025. Its target product is an HKD-pegged stablecoin designed to bridge Animoca's Web3 gaming platforms for in-app payments, HKT's Tap & Go mobile wallet for retail payments, and Standard Chartered's banking network for cross-border settlement, all under a single token.

Researcher's Comment

This first issuance marks the moment Hong Kong's four-year regulatory buildout finally moved beyond the design phase. From HKMA's January 2022 discussion paper on stablecoins, the timeline spans 4 years and 3 months through the December 2023 joint consultation, July 2024 framework conclusions, May 2025 legislative passage, and August 2025 ordinance effective date, culminating in the first license. All the resources Hong Kong has invested thus far went into building the regime. From here, the burden shifts to proving the regime actually works in the market.

The distribution strategies of the two licensees stand in sharp contrast. HSBC follows a single-bank model, publicly committing to launch its HKD-pegged stablecoin in the second half of 2026 and positioned to prioritize B2B territory such as treasury, capital markets, and cross-border settlement, building on existing institutional client relationships. Anchorpoint, by contrast, follows a three-way JV model and has said it plans to begin operations within the coming months. Its consortium structure targets retail payments and Web3 use cases simultaneously. The former is a vertical integration model built on trust. The latter is a consortium model prioritizing channel breadth. Hong Kong's first batch of licenses effectively runs a live experiment pitting these two models against each other in the same market, and whichever one acquires actual users faster in the second half of 2026 will shape the structure of the FRS stablecoin market.

Both issuers face two common constraints as their distribution plans move from paper to market:

The first is a structural constraint already embedded at the design stage. HKMA's AML guidelines permit licensed stablecoin transfers only between KYC-verified wallets, with travel rule requirements applying to transfers above HK$8,000. In practice, this means HKD stablecoins will be implemented with on-chain whitelists embedded in their smart contracts. Regulated safety is secured, but at the cost of the frictionless circulation that USDT and USDC enjoy.

The second is that the available market space is already occupied. EnsembleTX, launched in November 2025, is a live tokenized deposit settlement platform with seven participating banks. HSBC's TDS is already running live corporate transactions across four countries and five currencies. The largest market, institutional payments and treasury management, is effectively claimed by tokenized deposits. On top of that, tokenized deposits can pay interest while FRS stablecoins are legally barred from doing so under the ordinance. There is no structural basis for FRS to compete with tokenized deposits for the same bank clients. What remains for FRS stablecoins is retail payments, cross-border remittance, and on-chain settlement.

Two variables are worth watching from here:

First, the degree of mainland China's policy intervention. The most conspicuous absence from the first batch is Bank of China (Hong Kong, BOCHK), the only one of Hong Kong's three note-issuing banks left out. It has not disclosed a formal reason, but mainland authorities instructed JD.com and Ant Group last year to pause their Hong Kong stablecoin pilots, and have since formally banned the issuance of unauthorized RMB-pegged stablecoins. A core differentiator of the Hong Kong framework from the outset has been the premise that Chinese entities could, under "One Country, Two Systems," operate digital money businesses under Hong Kong licenses in ways that bypass mainland regulation. If mainland policy closes off that route, Hong Kong's identity as "the hub connecting Chinese capital to the global digital money market" gradually fades.

Second, whether the currency-neutral framework actually works in practice. The ordinance permits HKD, USD, EUR, and CNH, and this currency-neutral design was originally built to attract CNH (offshore RMB). But with Yinfa No. 42's ban on RMB-pegged stablecoins and HKMA's draft supervisory guidelines requiring reserves to be held in the same currency as the stablecoin, the CNH option now exists only on paper. Adding the fact that HKD has been pegged to the US dollar within the 7.75 to 7.85 band since 1983, the Hong Kong framework effectively narrows to HKD and USD, and HKD stablecoins resemble indirect dollar stablecoins. Whether currency neutrality, the framework's original point of differentiation, survives in the market will determine the framework's character.

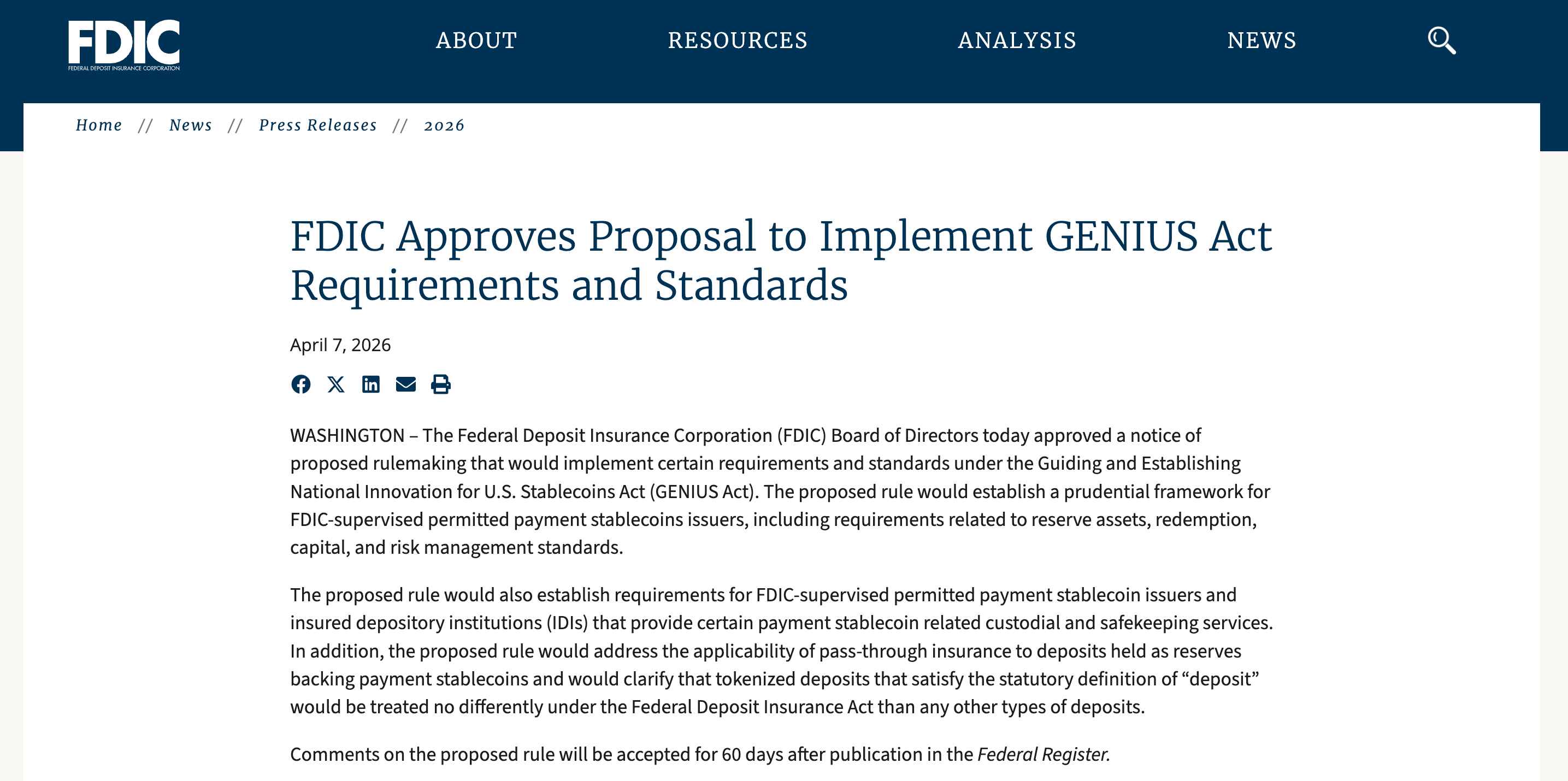

Source: FDIC

What Happened?

On April 7, 2026, the U.S. Federal Deposit Insurance Corporation (FDIC) approved a notice of proposed rulemaking implementing the GENIUS Act through a board vote. The 191-page rule proposes a prudential framework for FDIC-supervised Permitted Payment Stablecoin Issuers (PPSIs), covering standards for reserves, redemption, capital, liquidity, risk management, interest payments, and cybersecurity.

The proposed rule is subject to a 60-day comment period, with the final rule expected by the GENIUS Act's statutory deadline of July 18, 2026. Some provisions may be revised based on industry feedback. This is the FDIC's second GENIUS Act rulemaking following its December 2025 application procedures proposal, and the second prudential framework from a banking regulator after the OCC's February 2026 proposal.

The rule sets out five core requirements: (1) 1:1 full backing with eligible reserve assets and daily monitoring; (2) redemption within two business days, with FDIC notification required for large redemptions exceeding 10% of outstanding supply within 24 hours; (3) a minimum of $5 million in capital for the first three years, composed solely of CET1 and AT1 instruments (Tier 2 not recognized); (4) a separate "operational backstop" liquidity pool equivalent to 12 months of operating expenses; and (5) deconsolidation of the PPSI subsidiary from the parent bank's regulatory capital calculation.

The FDIC used this rule to settle two ambiguities in the GENIUS Act. First, the scope of deposit insurance. Deposits held by a stablecoin issuer as reserves at a bank are treated as corporate deposits of the issuer and protected only up to the standard $250,000 limit. Pass-through insurance to individual stablecoin holders does not apply. Tokenized deposits, by contrast, receive the same $250,000 per-holder protection as ordinary bank deposits as long as they meet the statutory definition of "deposit" under the Federal Deposit Insurance Act, regardless of whether they exist in blockchain token form.

Second, the scope of the interest payment prohibition. The GENIUS Act already banned direct interest payments by issuers, but interpretive ambiguity remained for workaround paths where exchanges or other third parties pay rewards to stablecoin holders, effectively producing the same outcome. The proposed rule specifies that third-party arrangements are also captured when an issuer represents that its token "pays interest or yield simply for holding or using a payment stablecoin." That said, the industry is growing comfortable with the interpretation that "properly designed" programs such as activity-based rewards may still fall outside the rule's scope, and the final contours of this boundary will be shaped through the 60-day comment period and the ongoing Clarity Act discussions.

Researcher's Comment

Tensions among U.S. regulators over stablecoin regulation are running higher than at any point to date. The FDIC rule is only one visible surface of that tension. Taken together with the Treasury, White House, and SEC moves that emerged the same week and the Senate's Clarity Act negotiations, it becomes clear that the executive branch, legislature, and regulators are each staking out positions on how to draw the actual contours of U.S. stablecoin regulation. This week made that transitional moment visible all at once.

The core of the FDIC rule is that the regulator's position on the scope of the interest payment prohibition has been documented for the first time. The GENIUS Act originally banned only direct interest payments by issuers, leaving interpretive room for third-party workaround paths where exchanges pay rewards to stablecoin holders, effectively yielding the same outcome. This interpretive gap was the legal basis that enabled Coinbase to pay passive rewards to USDC holders, and Circle's revenue structure and USDC demand itself have depended substantially on this channel.

The line the FDIC actually drew is closer to distinguishing "yield from simply holding or using" from "rewards tied to separate economic activity," not a blanket ban on all third-party rewards. The rule's language ("simply for holding or using") prohibits yield that accrues merely from passive holding while leaving room for rewards tied to actual use such as payments or trading to fall outside the rule's scope. This is why the concerns the industry held at the time of the February OCC proposal have largely subsided by the time of this FDIC rule.

Beyond the FDIC rule, the broader picture of U.S. stablecoin regulation surfaced simultaneously through moves from other institutions and industry figures:

On April 3, the Treasury released a proposed rule laying out principles for determining whether state-level regulatory regimes are "substantially similar" to the federal framework, closing off the scenario where smaller states could brand themselves as stablecoin hubs with lower standards.

On April 8, the White House added a different angle. An internal White House study released that day assessed the risk of stablecoin interest payments driving bank deposit outflows as limited. The signal reads as the executive branch building up a theoretical case for allowing yield even as the FDIC moves to codify the prohibition.

On April 10, Coinbase CEO Brian Armstrong publicly pushed for swift passage of the Clarity Act. Around the same time, Senate negotiations over the scope of permissible stablecoin interest and rewards were reported to be approaching agreement after months of deadlock.

The remaining variable is the Clarity Act's interest provision. The 30% probability of 2026 passage put forward by Wintermute's Head of Policy Ron Hammond reflects the uncertainty around this variable. If the interest prohibition is confined to yield from passive holding, activity-based rewards will be permitted and stablecoins will secure some room to compete with tokenized deposits at the consumer product layer. If the final rule is applied more broadly, stablecoins will be pushed into retail payments and public-chain on-chain settlement, while tokenized deposits absorb the institutional market.

The structural basis for this market split is already largely visible in the current rule. Stablecoins receive neither interest nor deposit insurance, while tokenized deposits receive both. The conditions under which the latter holds a structural advantage among two ways of representing the same dollar on-chain are spelled out in the rule itself, and this is why bank-issued tokenized deposit initiatives such as JPMorgan's JPMD, Project Ensemble, and HSBC's TDS have been expanding rapidly.

Either way, the U.S. stablecoin market will split into two lanes starting in the second half of 2026. One is the PPSI lane, where Circle, PayPal, and large issuers entering as bank subsidiaries compete under FDIC/OCC supervision. The other is the tokenized deposit lane, where JPMorgan, Bank of America, and major regional banks issue against their own balance sheets on chains like Base and Ethereum. Where the Clarity Act's interest provision draws the boundary between these two lanes will be the final answer to the question this week's FDIC rule has raised.

Crypto

Institution

White House clears review of rule that could open path for crypto in $10 trillion 401(k) market

Bipartisan lawmakers introduce PREDICT Act to bar federal officials from prediction markets

NYSE parent ICE invests another $600 million in Polymarket, expanding bet on prediction markets

Tech

Investment

Digital asset manager ParaFi raises $125 million for new venture fund: Bloomberg

Circle Ventures leads Tazapay Series B extension, bringing the round to $36 million

Stablecoin startup Payy, focused on private transactions, raises $6 million in seed funding

Asia

Ripple joins Singapore central bank initiative to test RLUSD trade settlements

Startale Group closes $63 million Series A with investments from SBI Group and Sony Innovation Fund

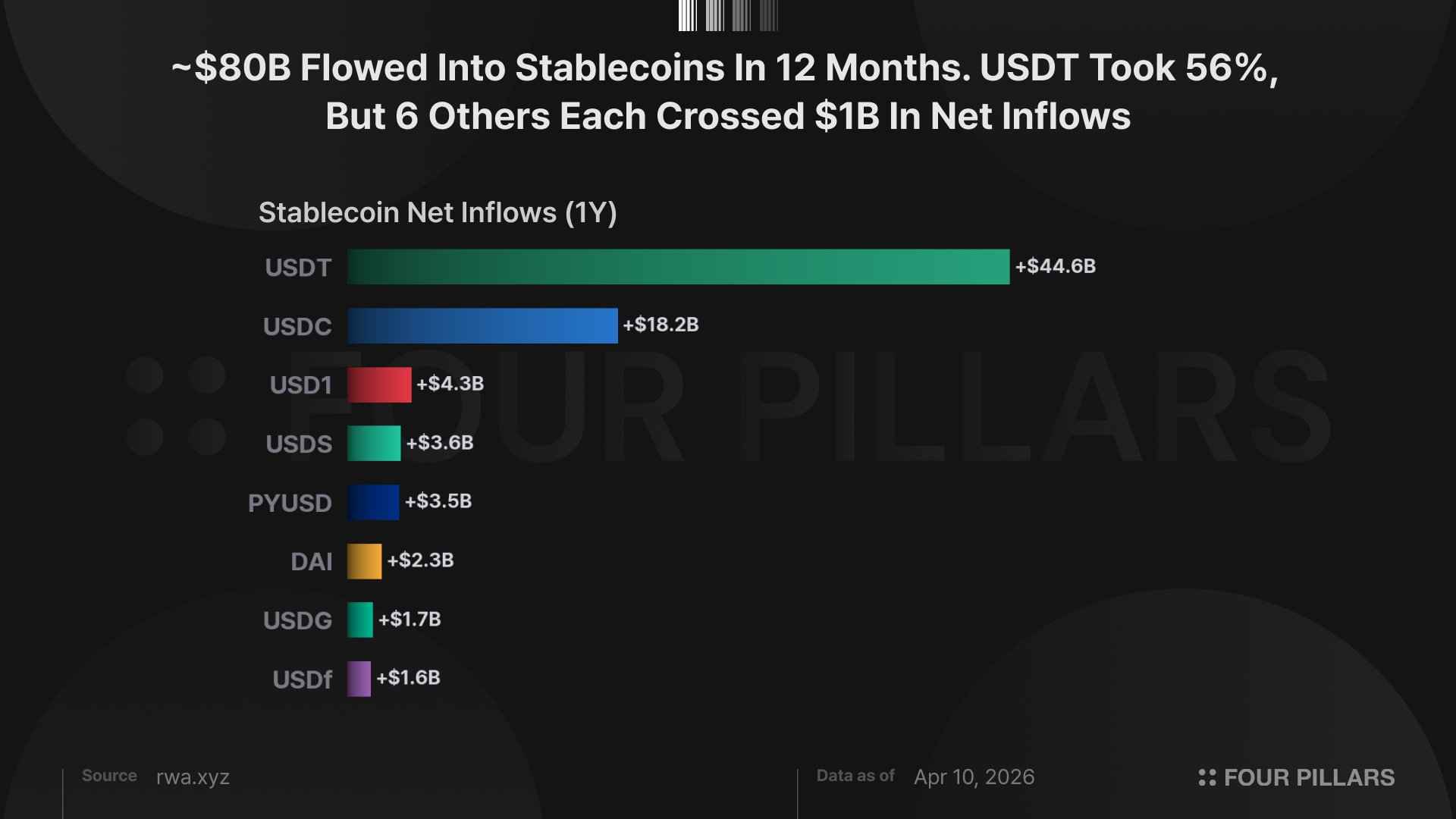

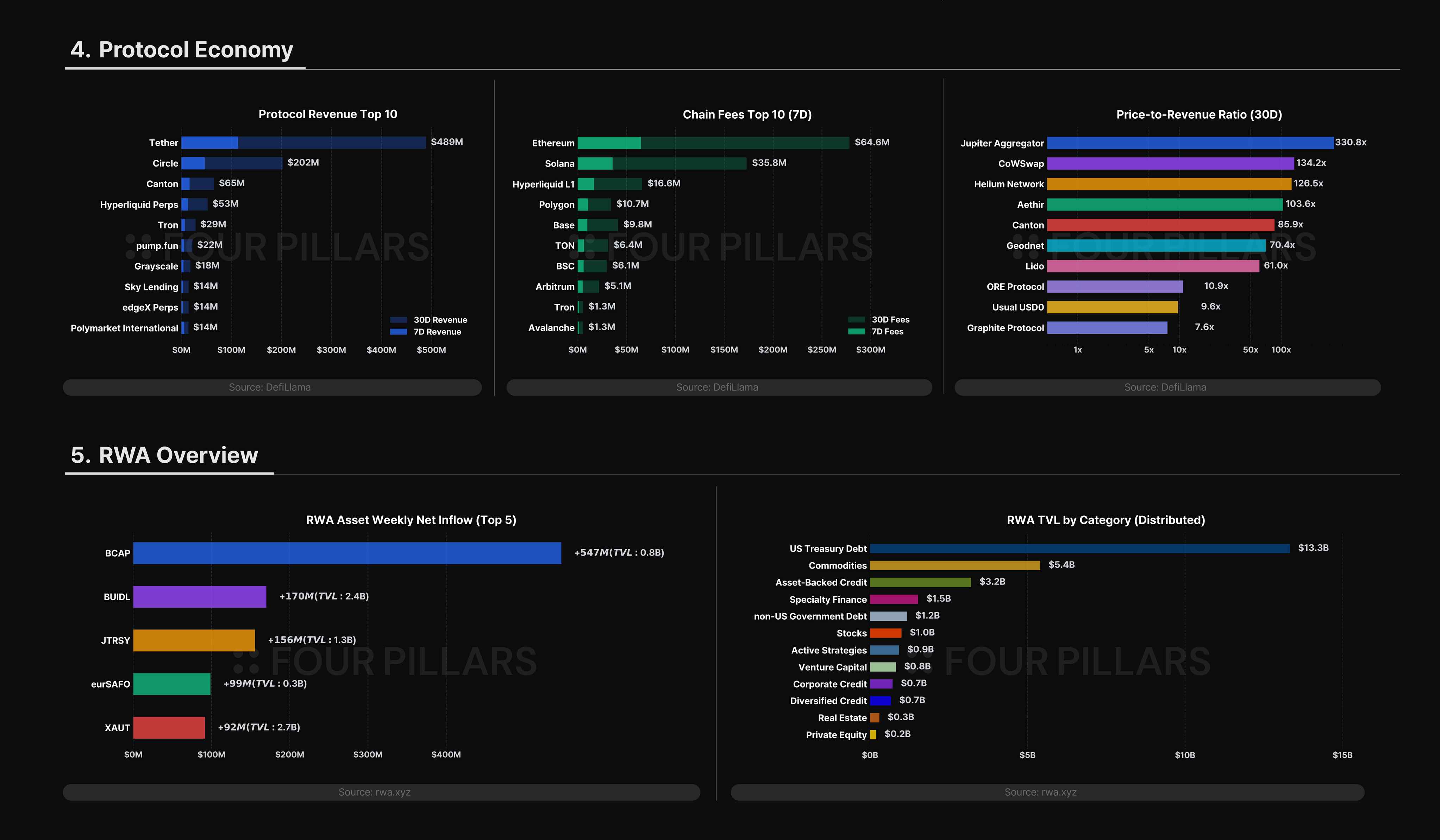

Top 2 grew 29% ($203B→$261B), but all other stablecoins combined grew 82% ($22B→$40B). A group that held 10% of the market a year ago captured 24% of new capital inflows.

1Y net flows tell the story. USDT +$44.6B, USDC +$18.2B, then USD1 +$4.3B (from zero), USDS +$3.6B, PYUSD +$3.5B, DAI +$2.3B, USDG +$1.7B, USDf +$1.6B. 6 stablecoins outside the top 2 each attracted over $1B in 12 months, each through a different distribution channel, from political networks to exchange revenue-sharing to fintech onramps.

Transfer volume ($10.2T/month, +9.7%) and active addresses (55.17M, +15.2%) are growing while 30-day supply is flat (-0.08%). The same $300B is circulating faster. Stablecoins are shifting from idle reserves to active payment and settlement infrastructure.

242M holders globally, 105 stablecoins tracked. The market is fragmenting as each new entrant targets a different use case.

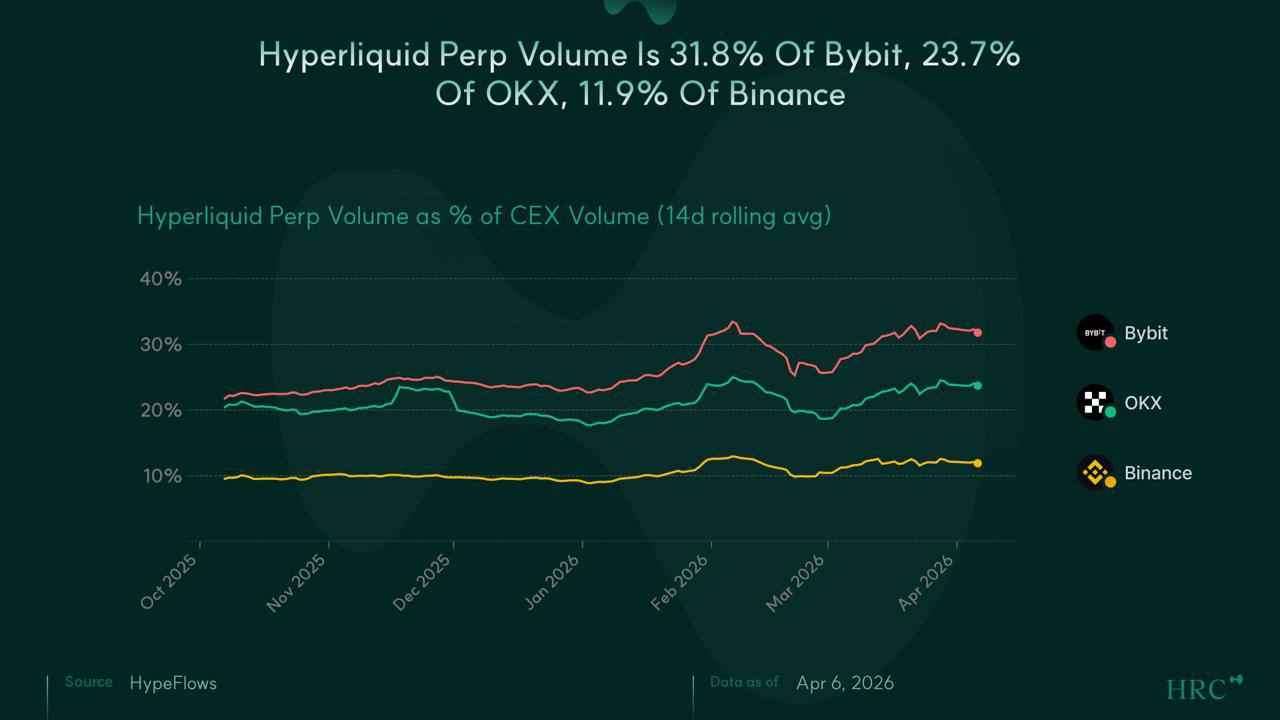

HL has crossed $4T in cumulative volume and $1B in cumulative fees, expanding beyond crypto perps into RWA perpetuals and institutional settlement.

Tracking HL perp volume as a percentage of each major CEX (Binance, Bybit, OKX) reveals the same pattern across all three: HL's volume share rises during volatility, corrects partially, then re-establishes at a higher floor. Bybit's ratio peaked at ~33% in February, pulled back to ~26%, then re-accelerated to 31.8%.

What makes this notable is that HL's CEX ratio kept climbing even as other DeFi perp protocols saw their volumes decline over the same period. This isn't a rising tide lifting all boats. HL's position in the DeFi perp landscape is becoming increasingly entrenched.

As AI agents move beyond text generation into high-value domains such as asset management, payments, and contract execution, the need for verifiability and accountability over agent behavior has surged. EigenCloud targets this gap head-on, positioning itself under the narrative of "a verifiable cloud for the agentic era."

EigenCloud recombines three infrastructure primitives built in 2025 (EigenLayer, EigenDA, EigenCompute) from the perspective of agents. By providing a single stack that covers what an agent executed (EigenCompute), what data it consumed (EigenDA), and what economic consequences follow upon violation (EigenLayer), EigenCloud assembles an end-to-end verification framework for agents.

But EigenCloud's ambition extends beyond verification as a service. It is positioning itself as the infrastructure layer for multi-agent organizations that autonomously generate revenue. Agentic companies could represent an entirely new asset class. If these systems become economically relevant online, they will likely require trusted compute, verifiable data integrity, and machine-native coordination rails, which is where EigenCloud becomes a natural infrastructure layer and opens a path to meaningful long-term revenue.

EigenCloud raises five questions spanning agent trust models, economic agency, enterprise operations, tokenization, and autonomous organizations, progressively defining the infrastructural conditions required for agents to function as economic actors. EigenCloud has declared a strategic pivot: moving beyond selling infrastructure to developers, it will now build applications and agents directly.

The areas where a verifiable cloud delivers its sharpest value can be organized along five axes: financial agents, multi-agent economies, data sovereignty, AI adjudication, and sovereign agents. Among these, use cases such as regulation-ready autonomous funds, agent credit systems, AI content provenance marketplaces, and automated SLA enforcement between agents stand out as scenarios where verifiability translates directly into commercial value.

Much like in January and February, March’s proposals reflect a growing set of complex challenges emerging alongside the protocol’s maturation, and, as a result, Core EIP discussions are not only expanding in scope but also unfolding in increasingly granular and specialized directions.

Looking ahead to the second half of the year, following the Hegota Upgrade, the introduction of FOCIL is expected to expose the structural limitations of the current builder–relay-centric paradigm; in turn, this will likely catalyze more active discussions around follow-up proposals, including enshrined PBS, encrypted mempools, and fee market design.

Meanwhile, in March, Ethereum Foundation revisited Ethereum’s identity and role through two blog posts. Anchored in unforkable persona grounded in the CROPS principles, and reinforced by years of accumulated trust and ecosystem maturity, Ethereum is poised to further evolve into a more robust form of public infrastructure.

Lido's existing emergency pause mechanism, GateSeal, required annual redeployment due to its single-use design, and as the number of protected contracts grew beyond ten, the operational burden compounded.

CircuitBreaker eliminates the redeployment burden while preserving GateSeal's security properties through three design choices: a permanent address, independent per-contract permission management, and heartbeat-based proof of committee liveness.

CircuitBreaker serves as a governance design case study in how a decentralized protocol can structurally reduce the operational cost of an inherently centralized tool like emergency pausing.

USDH generates ~$0.006/HYPE in annual buyback yield at $91M supply, a rounding error against $600M+ in trading fee buybacks. It stays immaterial until supply crosses $1.5B.

USDH is losing share of a growing market. USDC captured nearly all net stablecoin inflows on Hyperliquid since February while USDH is flat-to-declining from its March peak.

If Hyperliquid launches canonical USDH perps with AQA fee advantages and becomes the multi-vertical settlement (e.g. HIP-4, HIP-6), supply could blow past $10B.

That said, the infrastructure case doesn’t need the yield to work. USDH is counterparty diversification, native settlement for new HIP verticals, and a fiat on/off-ramp that bypasses USDC.

Worldpay/GP on LayerZero : Payment DVN

Some of the charts below are powered by CryptoQuant. For those interested in exploring the underlying data in greater detail, CryptoQuant provides access to a comprehensive suite of onchain and market analytics used by institutional participants.

Dive into 'Narratives' that will be important in the next year