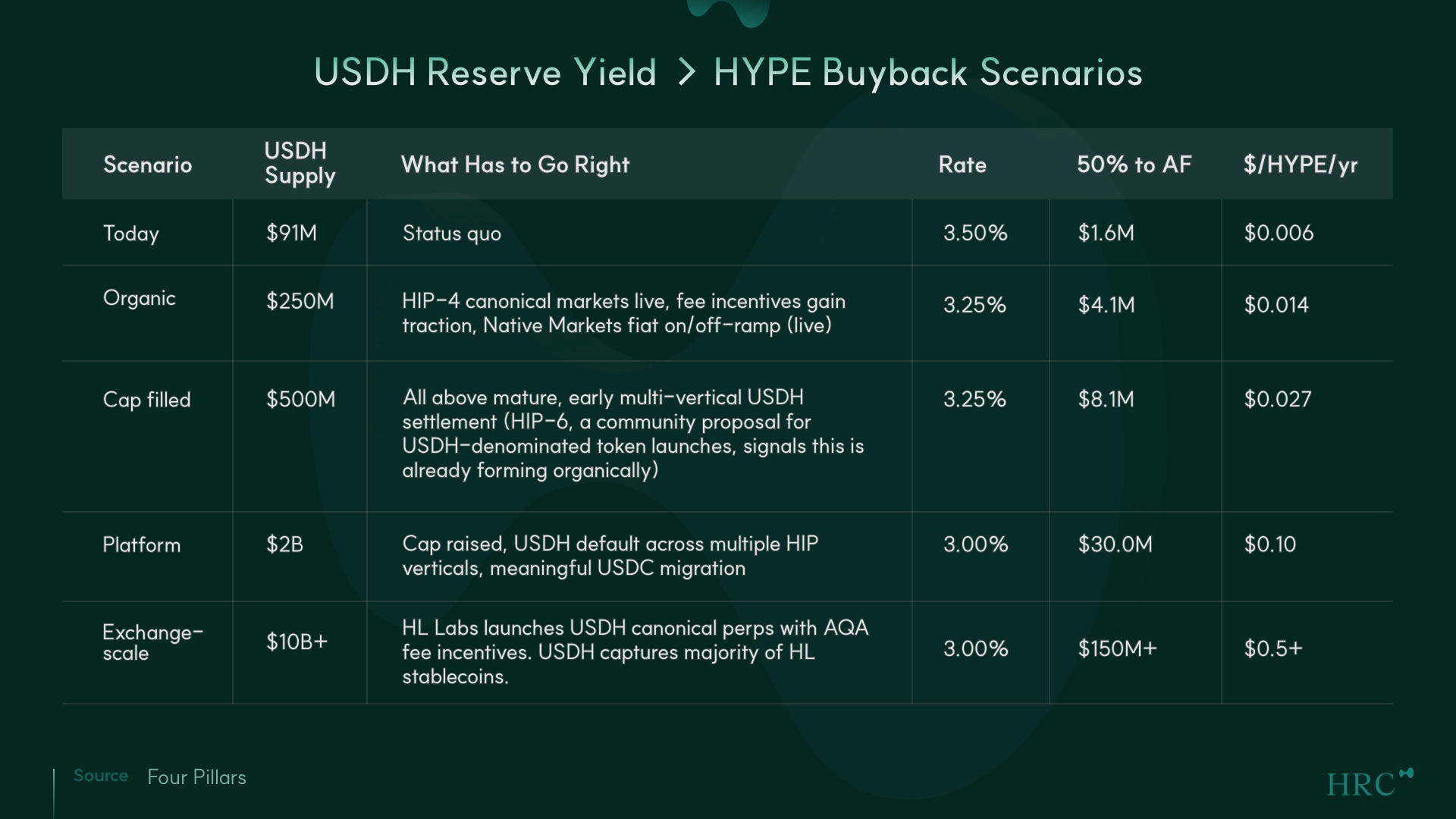

USDH generates ~$0.006/HYPE in annual buyback yield at $91M supply, a rounding error against $600M+ in trading fee buybacks. It stays immaterial until supply crosses $1.5B.

USDH is losing share of a growing market. USDC captured nearly all net stablecoin inflows on Hyperliquid since February while USDH is flat-to-declining from its March peak.

If Hyperliquid launches canonical USDH perps with AQA fee advantages and becomes the multi-vertical settlement (e.g. HIP-4, HIP-6), supply could blow past $10B.

That said, the infrastructure case doesn’t need the yield to work. USDH is counterparty diversification, native settlement for new HIP verticals, and a fiat on/off-ramp that bypasses USDC.

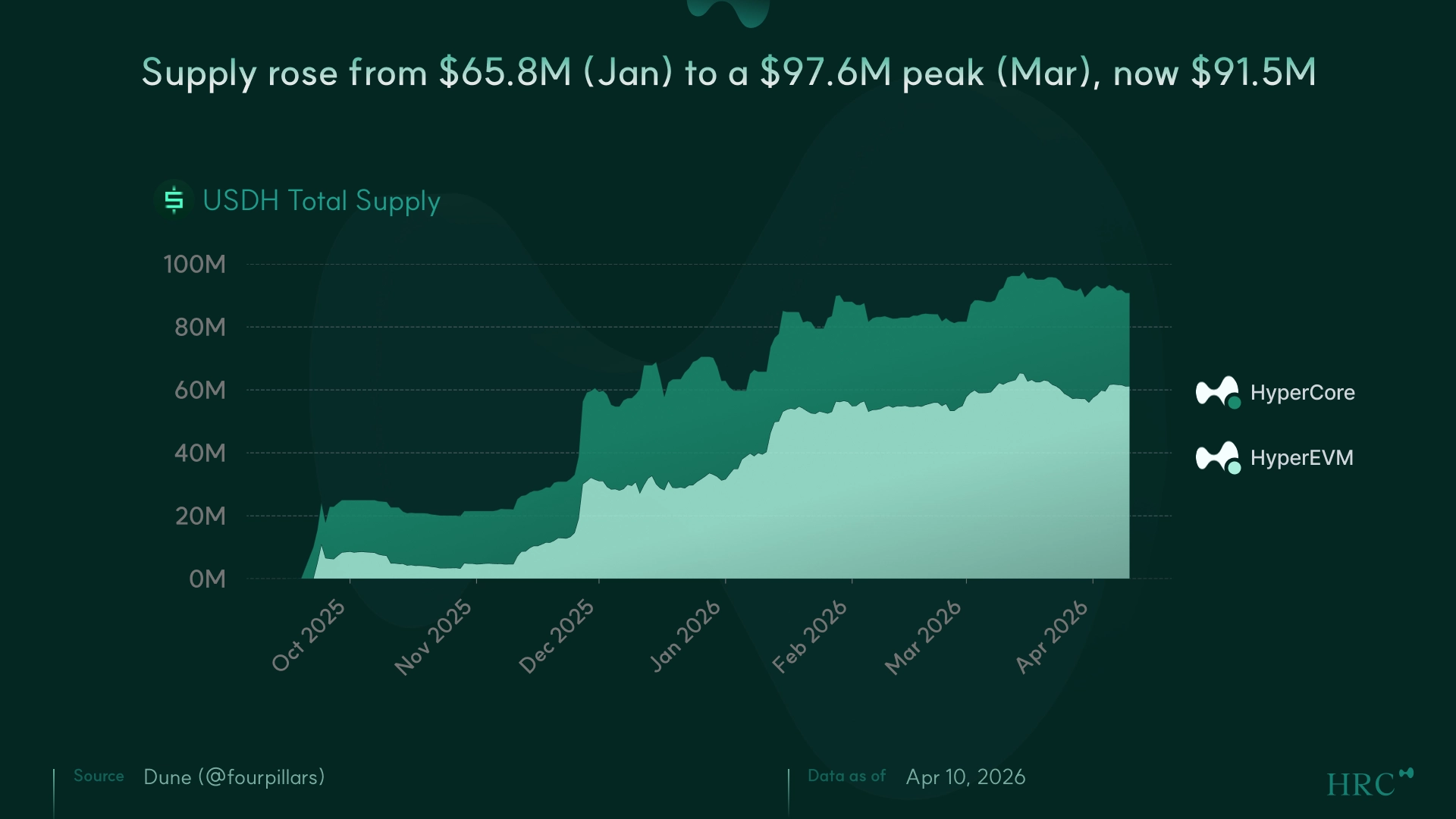

Total stablecoins on Hyperliquid’s L1 are $5.31B. USDC accounts for $4.97B (93.7%). USDH holds $91.5M (1.73%) and is shrinking, down 1.86% week-over-week. The supply went from $65.8M in January to a $97.6M peak in March, then pulled back to $91.5M.

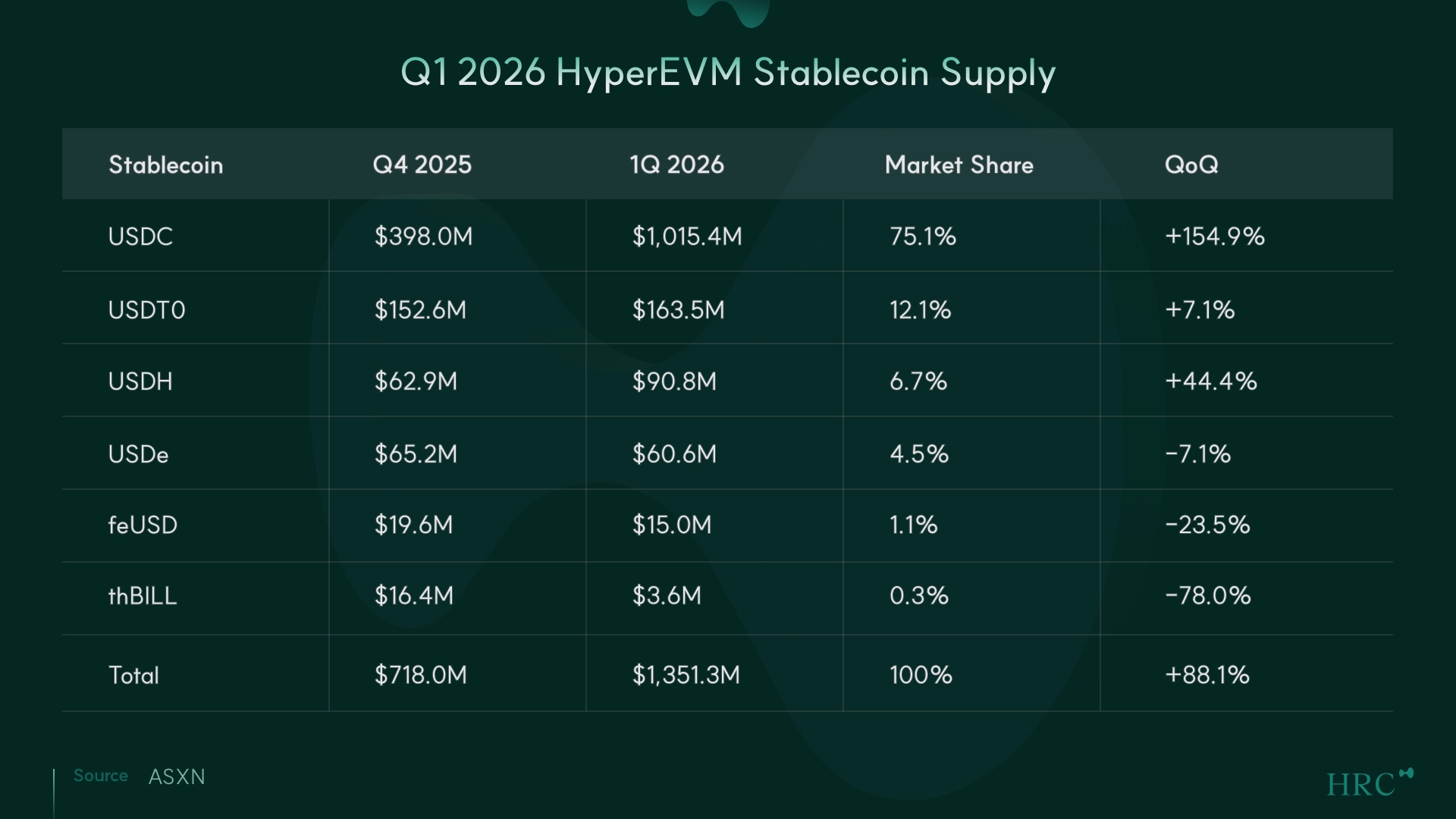

Meanwhile, total HL stablecoins grew from a February trough of $4.37B to $5.31B, with USDC on HyperEVM alone up 182% month-over-month. USDC’s surge traces largely to Circle’s native USDC and CCTP v2 integration on HyperEVM. USDH still grew 44.4% QoQ on its own terms ($62.9M to $90.8M).

Two-thirds of USDH supply sits on HyperCore as trading collateral rather than on HyperEVM, meaning it’s being used for its intended purpose, just not at scale yet.

Fee incentives exist (20% lower taker fees, 50% better maker rebates, 20% more volume credit on USDH-quoted pairs), but there are no canonical USDH-quoted perp markets. The only USDH pairs are HIP-3 builder markets deployed by Ventuals, Markets.xyz, and Felix — markets with thin liquidity and a fraction of total platform volume. The incentives are real, but they apply to too small a surface to move the needle on USDH adoption. The supply cap was raised to $500M in March 2026 and sits at 18.2% utilization. The constraint isn't the cap or the incentive structure. It's that USDH hasn't reached the markets where the volume concentrates.

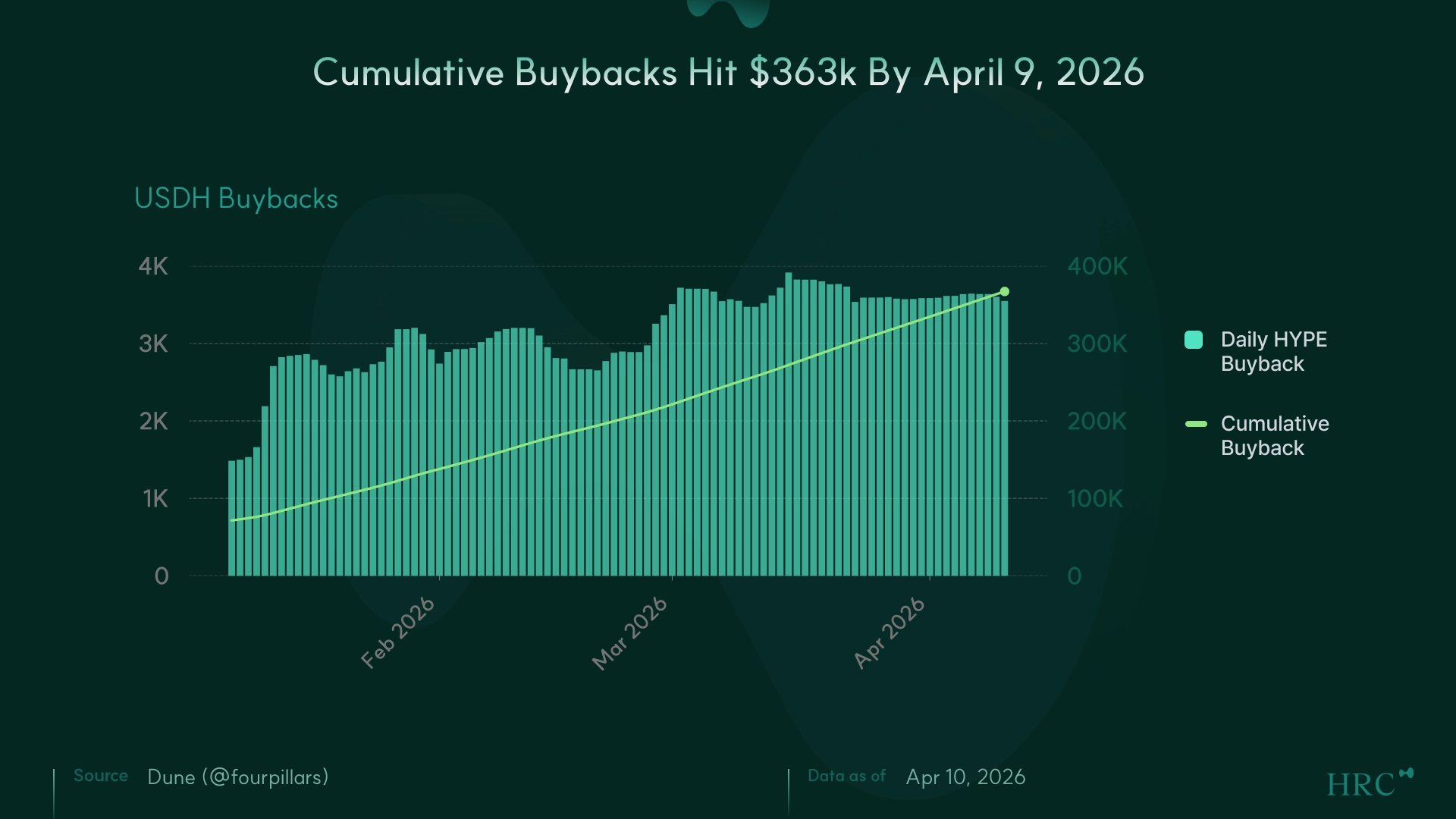

USDH backing sits in T-bill equivalents (BlackRock BUIDL, Superstate, JPMorgan). Reserve yield splits 50/50 between HYPE buybacks via the Assistance Fund and ecosystem growth.

Unlike USDe or sUSDS, USDH holders earn nothing directly. This means USDH demand is entirely exchange-driven, not yield-driven, and scales with Hyperliquid’s product usage rather than competing for yield-seeking capital.

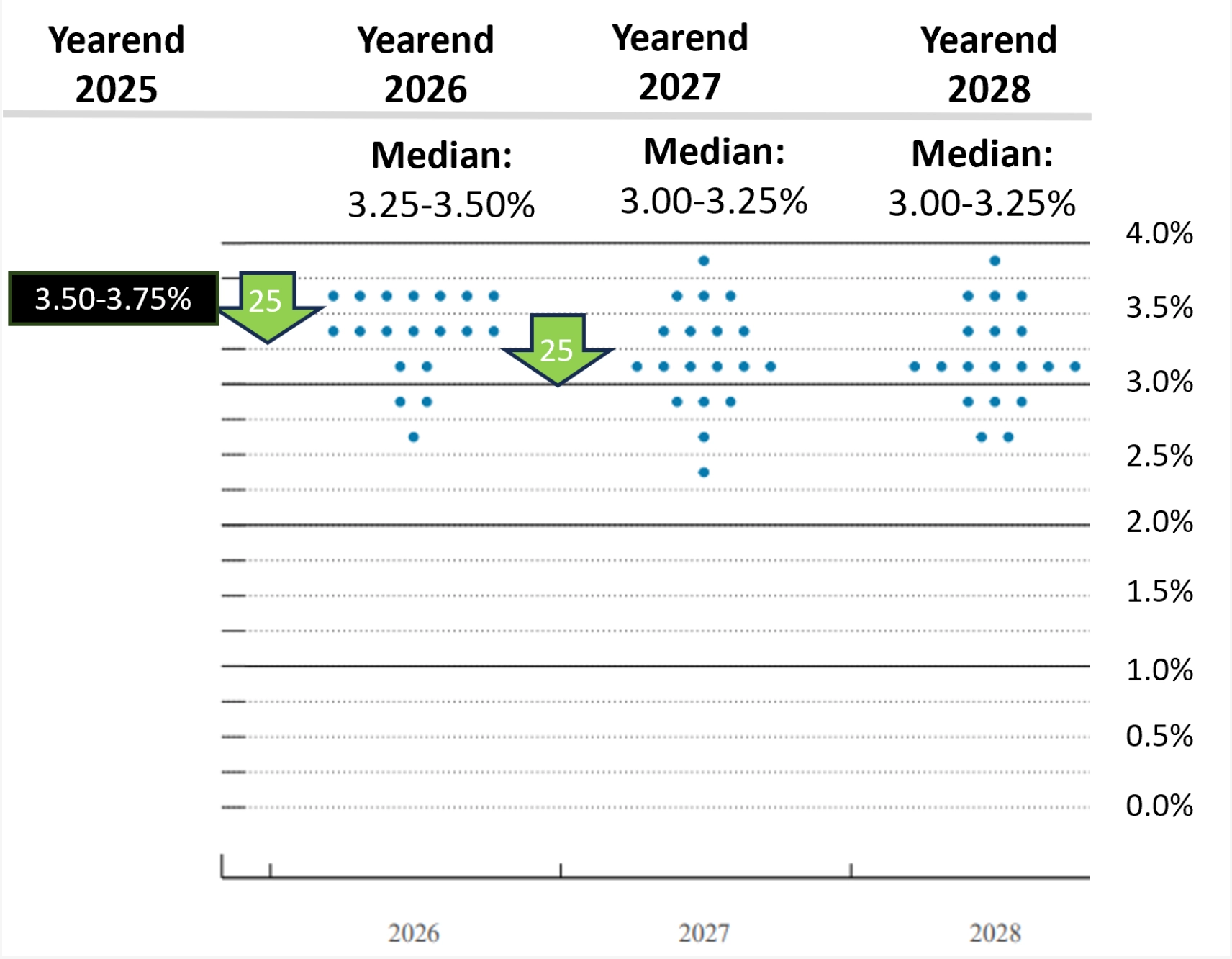

The buyback share is additive to the existing fee-driven flow of ~$600M-700M annualized. With ~299M HYPE circulating, the per-token math across five supply scenarios looks like this, with rate assumptions from the March 2026 Fed dot plot (14/19 FOMC members project zero or one cut in 2026):

The materiality threshold sits around $1.5B at 3.25% rates, where USDH yield crosses ~5% of annual trading fee buybacks. That’s 3x the current cap and 17x current supply. Each prerequisite (cap raise, multi-vertical settlement, organic USDC migration) is individually plausible and collectively ambitious. The last row requires a governance decision to launch canonical USDH pairs (practically an HL Labs call at this stage of validator decentralization), and one nobody outside the ecosystem can predict.

March 2026 Fed Dot Plot Showing Projected Target Range of Fed Funds Rate

Source: Bondsavvy

The table also overstates slightly. Zero-fee USDC-to-USDH conversion means traders can JIT-mint for the fee discount and redeem immediately, so headline supply may overstate sticky reserves earning yield. And HIP-4 forces USDH settlement in canonical prediction markets, but that vertical has unproven volume on Hyperliquid, so the chicken-and-egg is only partially broken.

Only two exchange stablecoins have ever crossed $1B in supply, and both were Binance’s. BUSD reached $23.5B at peak, and FDUSD hit $4B in under a year. Every exchange stablecoin that tried organic growth without canonical market pairs, e.g. Huobi’s HUSD ($393M peak), OKX’s USDK ($43M), Gemini’s GUSD ($599M), died below $600M.

Binance used two levers: aggressive incentives (zero-fee major pairs that made BUSD the cheapest way to trade BTC) and outright mandates (forced conversion of rival stablecoin balances). The incentive lever worked. BTC/BUSD volume exceeded BTC/USDT by 65% purely on cost. The mandate lever was unique to Binance's market power and doesn't fit HL's ethos.

USDH is currently on the USDK path — fee incentives exist but only on HIP-3 builder markets with thin liquidity and a fraction of total platform volume. The canonical perp markets where volume concentrates have no USDH pairs at all. The documented strategy appears to be new verticals first (HIP-4 → future HIPs), add canonical markets later.

To be clear, canonical BTC-USDH or ETH-USDH perps don't exist today and haven't been proposed through governance. Everything is speculative. But Binance proved the dual-pair model works. BTC/BUSD ran alongside BTC/USDT and volume migrated to the cheaper pair rather than fragmenting. Hyperliquid could do the same with AQA fee advantages pulling volume naturally. That's the incentive path without the mandate path. Untested at this scale, but the mechanism that drove BUSD's growth before Binance layered on forced conversion. At $10B+ supply, $150M+/year in incremental buyback flow is no longer a rounding error.

~$5B in USDC sitting on Hyperliquid is ~$5B of dependency on Circle's custody and compliance decisions, and roughly $192M/year in reserve yield flowing to Circle and Coinbase instead of to Hyperliquid. For a protocol running $37B FDV with ambitions to become the house of all finance, that's both a single point of failure and a massive revenue leak worth building around.

USDH demand becomes endogenous to Hyperliquid's product roadmap. HIP-4 canonical markets settle exclusively in USDH. If the next HIP vertical does the same, and the one after that, supply growth stacks with each product launch rather than depending on per-market fee incentives. HIP-6, a community proposal for USDH-denominated token launches, is early evidence that this pattern is forming organically, though nothing has materialized yet. Native Markets extends this further with a direct fiat-to-USDH on/off-ramp that bypasses USDC entirely.

Schwab and Robinhood earn billions from client cash sitting in sweep accounts, and nobody opened a brokerage account for the sweep yield. USDH is the same structural play applied to on chain exchange infrastructure, except the yield accrues to tokenholders through buybacks rather than to equity holders through earnings.

The yield math matters at $1.5B supply. The infrastructure argument is valid at $91M. The path to $10B runs through canonical markets and multi-vertical settlement.

Dive into 'Narratives' that will be important in the next year