What Happened?

On March 3, 2026, Marc Zeller, founder of the Aave Chan Initiative (ACI), posted on the Aave governance forum that ACI would not renew its contract with Aave DAO and would wind down operations over the next four months. Since its founding in early 2023, ACI operated with a team of eight members and led 61% of all governance activity over three years. The group designed revenue strategies responsible for 48% of protocol revenue and executed $101 million in incentives. Aave’s native stablecoin GHO also grew from $35 million to $527 million during ACI’s tenure. Despite these results, ACI received a total of only $4.625 million in compensation over the three year period.

The immediate background of this departure is a governance dispute between Aave Labs and independent service providers. The dispute began in December 2025 when a community member pointed out that fees generated from the CoW Swap integration were flowing to Aave Labs rather than the DAO treasury. BGD Labs later proposed transferring brand assets to the DAO, but Aave Labs submitted the proposal to a Snapshot vote during the holiday period. The vote ultimately failed due to abstentions and opposing votes.

In January 2026, Aave founder Stani Kulechov posted a proposal outlining the future roadmap, which proceeded to an official vote in February. The proposal requested approximately $51 million in stablecoins and 75,000 AAVE tokens and passed with 52.58% approval.

ACI questioned the legitimacy of the vote. Zeller claimed that approximately 233,000 AAVE tokens from three address clusters believed to be connected to Aave Labs ultimately flipped the vote outcome. He also stated that 111,000 tokens delegated by Kulechov were included in this group. Before the vote, ACI demanded four conditions including stronger onchain milestone tracking and limits on self voting. However, these requests were not addressed before the vote concluded.

Meanwhile, BGD Labs also announced on February 20 that it would not renew its contract with Aave DAO after April 1, citing concerns about governance direction and centralization risks. After news of the departures of ACI and BGD Labs spread, the price of the AAVE token fell by more than 10%.

ACI plans to complete the remaining work for the Skyward program over the next four months, open source its internal governance infrastructure, and transfer responsibilities such as the Aave Liquidity Committee and GHO Stewards to successor teams or the DAO. Zeller did not disclose detailed future plans but indicated that he would consider joining if BGD Labs builds a new protocol.

Researcher’s Comment

This incident once again highlights the fundamental limitations of the DAO governance model. Aave DAO promotes a structure where token holders determine the protocol’s direction through voting. However, because Aave Labs simultaneously holds the brand, communication channels, and significant voting power, a practical asymmetry of power has emerged. When independent contributors raised concerns, the issues were pushed through by voting power rather than resolved through consensus. As a result, two of the core teams that led the protocol’s growth over the past three years announced their departures within weeks of each other. If the voting mechanism of a DAO itself cannot guarantee decentralization, it raises the question of how it fundamentally differs from board decisions in traditional corporations.

At the same time, it is important to note that this dispute is not simply a power struggle but is also tied to a practical question of who can ship software quickly. The Aave Labs side viewed the DAO’s consensus process as an obstacle to building competitive products, while independent contributors argued that such efficiency is simply another name for centralization. The situation in which both BGD Labs, the core technical team, and ACI, the core governance team, are simultaneously absent during the transition from V3 to V4 shows that the cost of this conflict is far from trivial. How Aave fills this gap will become an important precedent for governance experiments across the broader ecosystem.

What Happened?

Although there has been significant progress since the launch of the Trump administration, crypto regulation in the United States previously lacked a clear framework and relied heavily on litigation driven enforcement. Tokens were not clearly distinguished between securities and commodities, and regulatory uncertainty often pushed US based crypto companies to move overseas. The Crypto Market Structure Bill aims to address these issues by defining the distinction between commodities and securities for tokens, clarifying the authority of the SEC and CFTC, and establishing various investor protection provisions to build a regulatory structure for the crypto market.

The predecessor of the Crypto Market Structure Bill had been under discussion since 2022. After the Trump administration took office, the process accelerated, with the CLARITY Act introduced in May and passing the House in July. However, the process is currently delayed before Senate committee review due to conflicts between the banking sector and the crypto industry. There are two main reasons behind this.

The first is the conflict between Democrats and Republicans. Trump had emphasized the importance of the crypto industry even before taking office. Both before and after his inauguration, members of Trump’s family have also been involved in various crypto ventures including World Liberty Financial. Democrats view this as a serious conflict of interest. They believe that if the bill passes, Trump’s family businesses could benefit directly. As a result, there is a push to add conflict of interest provisions to the bill such as banning the president and family members from issuing crypto assets and prohibiting public officials from endorsing crypto.

The second and most important issue is stablecoin interest payments. A stablecoin related law, the GENIUS Act, already passed in 2025. While the law prohibited issuers from directly paying interest to holders, it did not clearly prohibit distribution channels such as exchanges or platforms from providing rewards. In practice, Coinbase provides rewards to USDC holders and PayPal distributes interest like rewards to PYUSD holders using this structure. The banking sector views these products as similar to bank deposits and argues that they create risks of deposit outflows and unfair competition within the financial industry. As a result, banks have attempted to slow the bill’s progress.

While the Crypto Market Structure Bill remained stalled in the Senate, Trump publicly voiced support for the bill this week and criticized banks for delaying the legislation. Notably, it was also revealed that Trump held a private meeting with Coinbase CEO Brian Armstrong shortly before making the statement. Coinbase has been one of the largest contributors to crypto industry lobbying, providing nearly $100 million in funding to the crypto focused PAC Fairshake.

Researcher’s Comment

Even though the issue of stablecoin interest payments was already addressed and passed in the GENIUS Act, the reason it is being discussed again in the Crypto Market Structure Bill is clear. Interest payments on stablecoins are an extremely important issue for both the banking sector and the crypto industry.

Because I personally work in the crypto industry, I understand how important stablecoin reward programs are for building an ecosystem and I believe they are essential. At the same time, it is also understandable that the banking sector raises concerns about deposit outflows and shadow banking risks.

However, the criticism from the crypto industry toward the banking sector is also justified. Most US bank savings accounts currently offer interest rates below 1%, while banks charge interest rates of more than 5 to 6% when lending those funds. In other words, banks raise capital very cheaply and lend it out at significantly higher rates, capturing the large net interest margin almost entirely for themselves.

Stablecoins represent an inevitable technological evolution in financial infrastructure. In this context, the issue of stablecoin interest payments becomes a key catalyst for democratizing the revenue that banks have historically monopolized and distributing it to platforms and users, thereby accelerating industry adoption.

The emergence of stablecoins may feel to banks today much like the arrival of money market funds once did in the past. Because of this, resistance from the banking sector toward the stablecoin industry will likely remain intense. However, stablecoins represent an unstoppable trend, and from the perspective of long term financial development, interest payments on stablecoins will likely become unavoidable.

What Happened?

The regulatory framework for crypto exchanges in South Korea is rapidly taking shape. On March 4, the Financial Services Commission discussed the key elements of the government’s review draft of the Digital Asset Basic Act. While the existing Virtual Asset User Protection Act, the first phase of legislation, focused primarily on user protection and unfair trading regulations, the second phase legislation, the Digital Asset Basic Act, will cover exchange licensing requirements, issuance and disclosure regulations, stablecoin oversight, and exchange governance structures. Final coordination between the ruling party and the Financial Services Commission is currently underway, and legislation is expected as early as the second half of 2026.

The new bill is also expected to include provisions that legalize market making activities. Under the current legal framework, there is no exception clause for market makers, meaning that all forms of liquidity provision could theoretically be treated as market manipulation. To address this, the Financial Services Commission is considering a structure where exchanges such as Upbit and Bithumb delegate market making activities to professional institutional firms.

Meanwhile, the Financial Services Commission is expected to include a provision in the Digital Asset Basic Act limiting the ownership stake of major shareholders in crypto exchanges to 20%. On March 3, the Financial Services Commission and the Democratic Party’s Digital Asset Task Force agreed on this 20% cap. The grace period will be three years after the law takes effect. Exchanges whose market share falls below a certain threshold, estimated at around 20%, will be granted an additional three years, allowing a maximum grace period of six years. Upbit and Bithumb, which together hold around 90% of market share, will likely need to restructure their ownership within three years, while Coinone, Korbit, and Gopax are expected to receive the full six year adjustment period.

Researcher’s Comment

The measures proposed in the Digital Asset Basic Act, including the transition to a licensing system, the institutionalization of market making, limits on major shareholder ownership, and mandatory disclosure requirements, collectively move in the direction of increasing regulatory control over exchanges. The Financial Services Commission has consistently argued that crypto exchanges should be redefined from private companies into public market infrastructure and regulated accordingly.

Among the new policies, the introduction of a market maker framework is actually long overdue. Korean exchanges have historically lacked formal market making mechanisms, resulting in structurally thin liquidity and a market structure in which new listings rely on organic buy side absorption. This has also been one of the reasons behind the abnormal expansion of the so called kimchi premium.

After market making becomes permitted, the kimchi premium is likely to shrink. As a result, projects that previously expected abnormal premiums in the Korean market during new listings may need to rethink their listing strategies. Arbitrage traders who relied on the premium for profit will also likely need to adjust their playbooks. However, considering that this was originally an exceptional market phenomenon unique to Korean exchanges, this change can be viewed as a normalization process.

On the other hand, the ownership cap on major shareholders raises questions. The Financial Services Commission argues that crypto exchanges should be treated as market infrastructure similar to the Korea Exchange and that excessive control by a small number of shareholders should be dispersed. However, major exchanges such as Nasdaq and NYSE in the United States do not impose artificial ownership caps of this kind. In the European Union and Singapore, regulators typically supervise exchange ownership through suitability reviews rather than strict ownership limits. In this sense, criticism that the rule represents a form of regulatory isolationism appears reasonable.

Concerns are also emerging about the long term expansion potential of exchanges. Korean financial regulators have already built significant regulatory barriers around the establishment and operation of crypto exchanges over several years. Requirements such as real name bank account partnerships, ISMS certification, VASP registration, and unfair trading monitoring obligations already function as a regulatory regime close to a licensing system. Adding a policy that forcibly disperses founder ownership afterward may effectively strip founders of control regardless of market integrity considerations. This could weaken incentives for exchanges to expand their businesses independently or grow through market competition.

Coinbase provides a useful precedent in negotiations between exchanges and regulators. The Coinbase board has participated in the legislative process of major bills such as the GENIUS Act and the CLARITY Act. Even while clashing with the banking industry over the issue of stablecoin interest payments, Coinbase has maintained communication channels with both parties in Congress and built a framework for dialogue between industry and regulators. Because of this regulatory engagement, Coinbase has been able to expand its leadership across the entire industry, from Base to institutional custody, acquisitions such as Deribit and Echo, and venture investments. It remains an open question whether Korean exchanges, operating under a structure that forces ownership dispersion, will be able to make decisions with similar flexibility in the future.

Crypto

Institution

Kraken Achieving Fed Master Access Has Several Implications For Crypto

Apollo Crypto to manage tokenized mEVUSD targeting returns on stablecoins

U.S. banking agencies say capital should be same for standard or tokenized securities

CFTC chief Selig to clear path for U.S. perpetual futures in coming weeks

Tech

Investment

Asia

S.Korea set to legalize crypto market makers to align with global standards

Binance Exchange Plans Five More Asia Licenses as APAC Crypto Adoption Surges

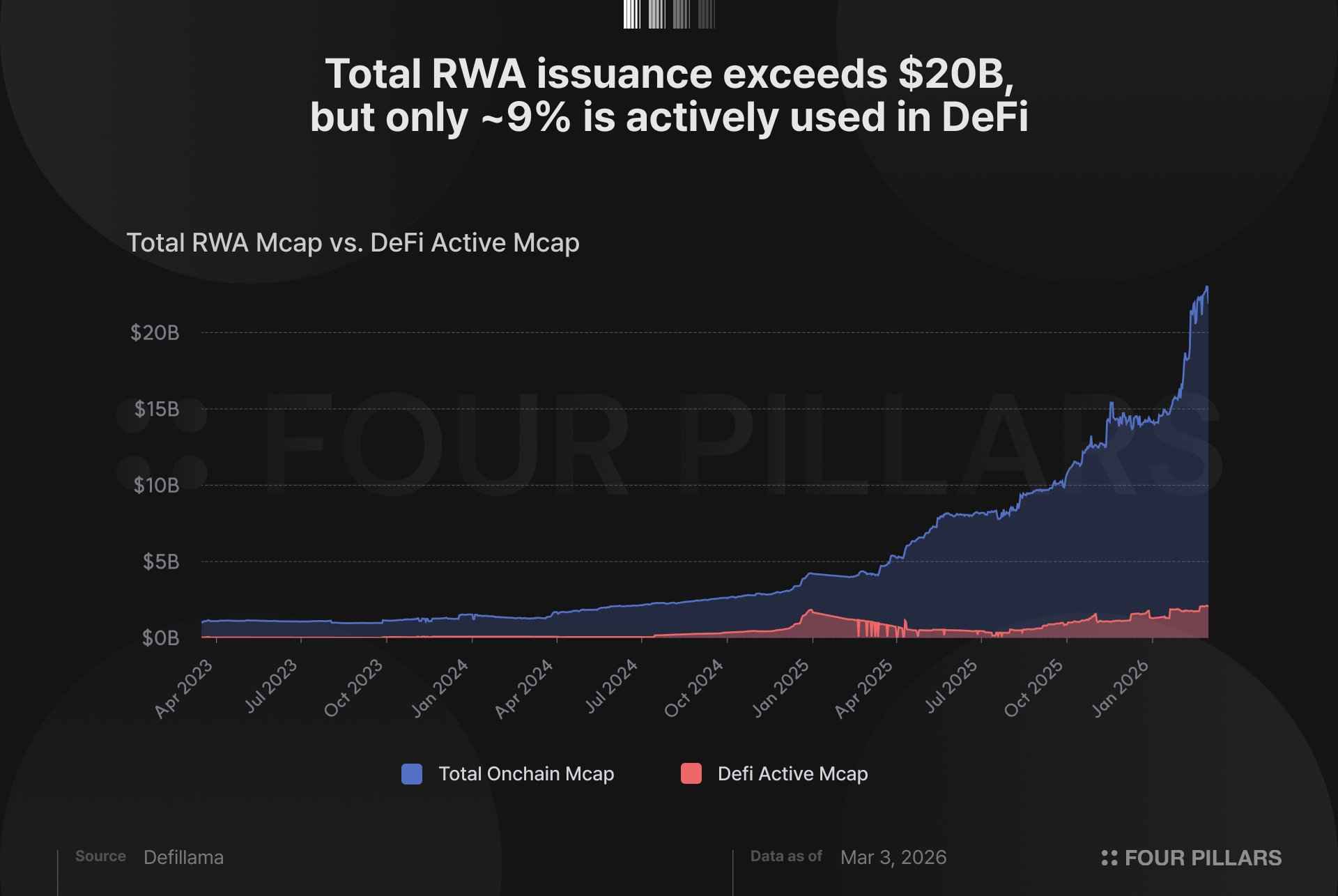

RWA onchain market cap hit ~$22B, but only ~$2.1B sits in DeFi. That's a 9.4% utilization rate.

Tokenized T-Bills and gold make up the bulk of RWA issuance, but most tokens just sit idle without DeFi composability.

The ~$20B gap between issued and DeFi-active RWAs is the biggest untapped opportunity in crypto.

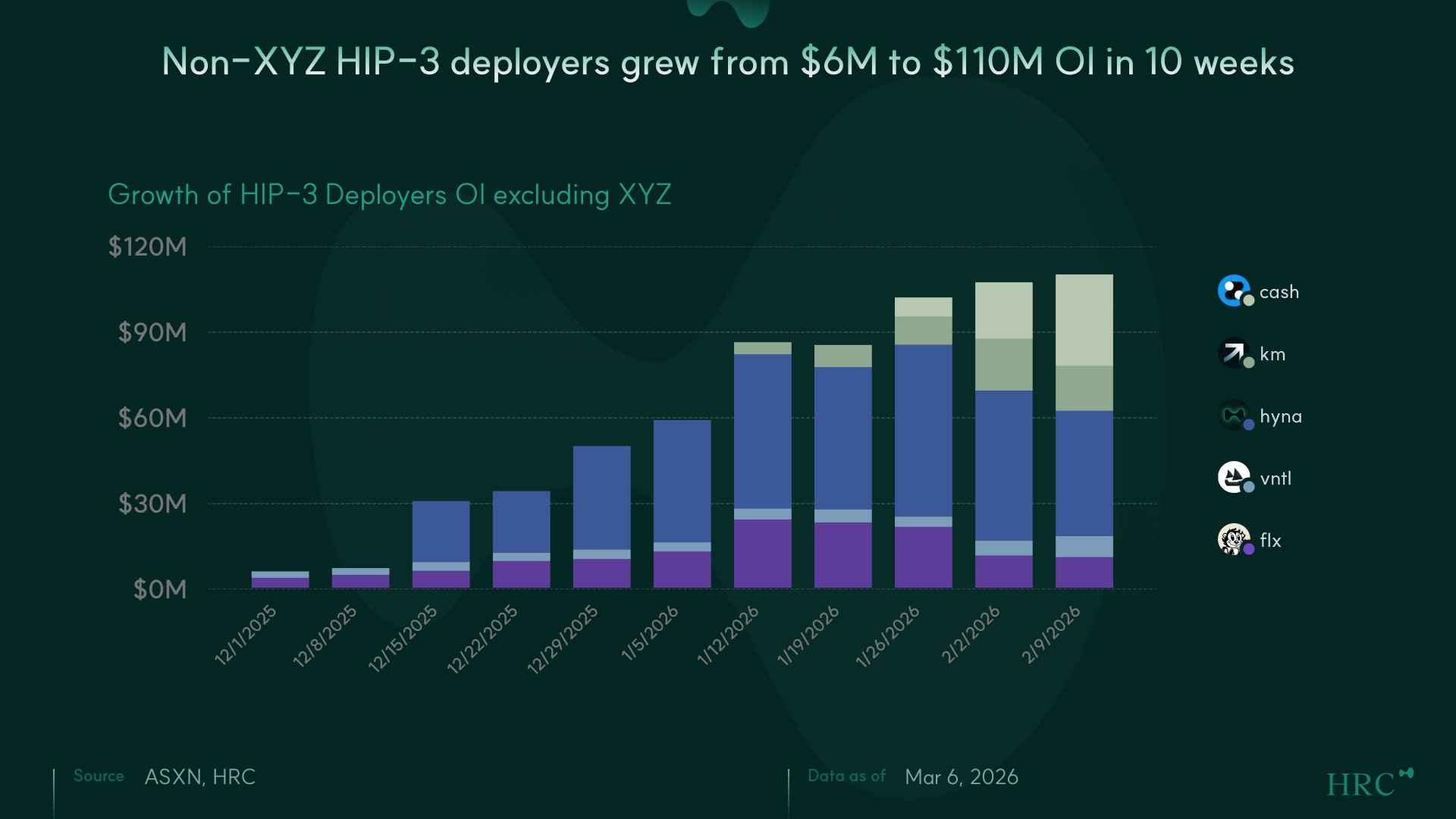

trade.xyz dominates the majority of HIP-3 volume, but non-XYZ deployers collectively grew from $6M to $110M OI in 10 weeks, with peak weekly volume reaching $2.2B.

Dreamcash is the breakout among new deployers. Launched 3 weeks ago, it already generates ~$1.1B in peak weekly volume. Volume growth outpacing OI growth signals active trading demand, not just passive positioning.

Hyperliquid's 24/7 structure gives HIP-3 a structural edge over COMEX. While COMEX closes on weekends, HIP-3 processed meaningful volume on SILVER and GOLD perps continuously, proving demand for around the clock risk transfer in commodity markets.

Tokens aren’t equity. Use EV/Holder Revenue, not EV/Protocol Revenue.

The accrual ratio (that % of protocol revenue actually reaches holders) is a revealing diagnostic. It ranges from 100% to 25% across our comp.

Not all “dilution” is the same. Team comp is an expense (in the multiple). Investor selling is a market event (out of the multiple).

Treasury Claim Discount: the question isn’t “what’s in the treasury” but “can holders get it out?”

This is a prototype framework. The excel file is attached, so feel free to improve it.

Dive into 'Narratives' that will be important in the next year