Jeff built a prediction market in 2018. Deaux (decentralized event contracts, off-chain matching, on-chain settlement) incubated by Binance Labs in their first cohort. It failed because the infrastructure didn't exist, crypto had maybe a few million users, and nobody could tell if what they were building was legal. Now he runs the largest perps DEX in crypto, a custom L1, and a token that crossed into the top 10 at $10B market cap. HIP-4 is him going back to finish what he started.

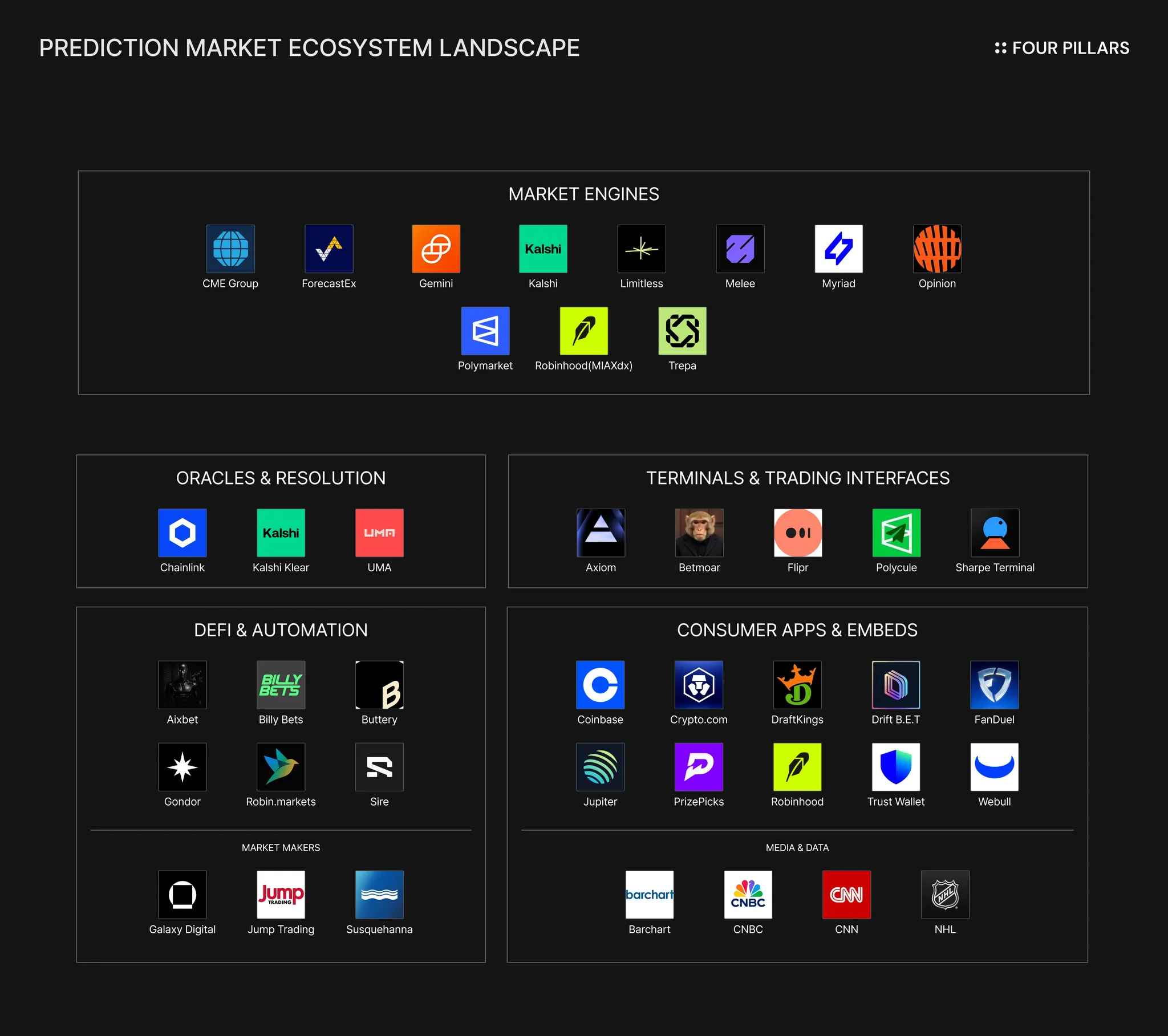

Kalshi just raised $1B at $11B. Polymarket is $9B from its ICE round, secondaries north of $12B. Both decacorns built on prediction markets alone. Kalshi did $263.5M in fee revenue last year ($63.5M in December alone) on a variable fee formula that blended out to roughly 1.15% across $23B in notional volume. Robinhood (~$80B mc) liked it so much they're building their own exchange after calling PMs their fastest-growing business ever. Coinbase (~$50B) embedded Kalshi contracts as part of its "Everything Exchange" expansion. When two of the largest consumer finance apps treat your product vertical as must-have infrastructure, the TAM argument is settled.

HIP-4 likely adds prediction market revenue to the same buyback-and-burn as perps — unconfirmed, but given it runs on HyperCore, it's a reasonable assumption. The fee mechanism isn't announced yet, but for reference perps run 4.5 bps taker / 1.5 bps maker, and 99% of all perp fee flows to the AF, which already holds 40M+ HYPE.

And then there's USDH. Canonical outcome markets will be USDH-denominated, so prediction market growth drives USDH reserves higher, and 50% of that reserve yield flows to the AF on top of trading fees.

Standalone PMs don't have what Hyperliquid already has. An active trader base, on-chain order book, portfolio margin, HyperEVM, all composable. As I wrote in my prediction markets deep dive, every prediction market today is fully collateralized with zero leverage, which caps what you can actually build on top of them. HIP-4 composing with portfolio margin is a form of capital efficiency that Polymarket and Kalshi structurally cannot offer.