Original Content: https://x.com/sonyasunkim/status/2030668622901756294

RWA looping has become one of the most talked-about strategies in DeFi.

Source: X (@kylesamani)

The setup is compelling: a structural wave of real-world assets tokenizing on-chain, borrowing rates at cycle lows, and a spread between RWA yields and funding costs that looks attractive.

The trade is:

Deposit a yield-bearing RWA yielding x%

Buy more of the asset

Repeat until reaching z leverage

In theory, this transforms a x% real-world yield into a x+(z-1)*(x–y)% leveraged yield strategy.

The problem is that in practice, it's nearly impossible to execute. The core problem is structural, and it stems from a single incompatibility: DeFi moves at block speed, but RWAs do not.

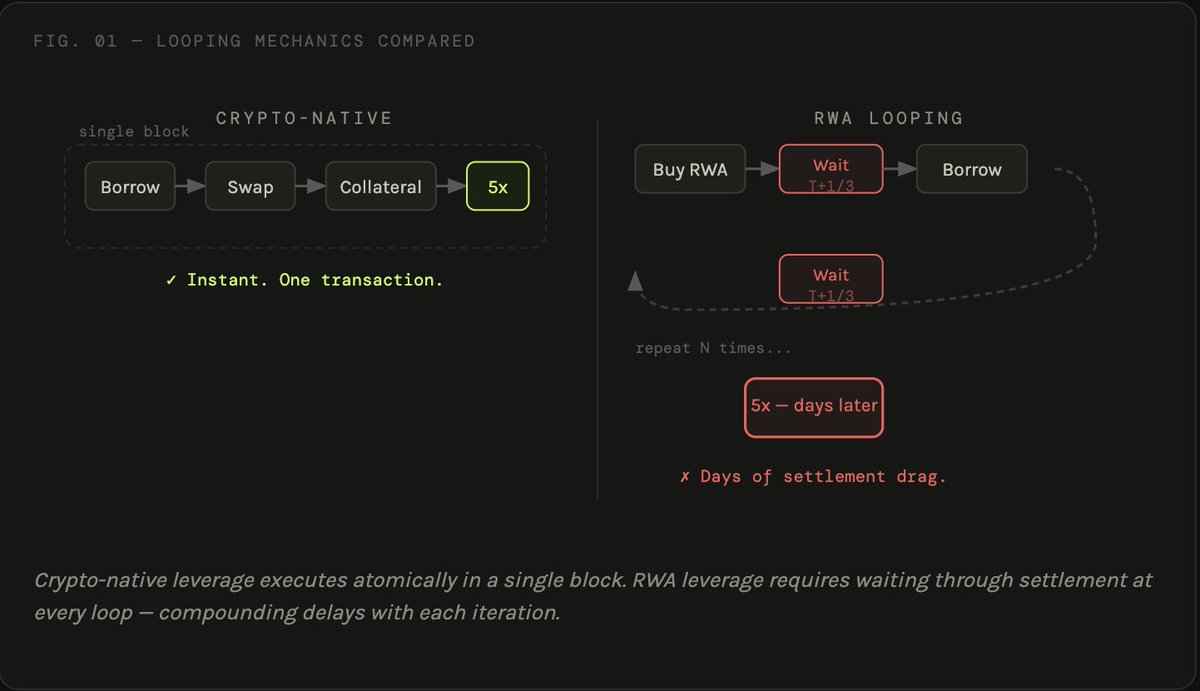

Crypto-native leverage is elegant precisely because it's atomic. A flash loan lets you borrow, swap, post collateral, and loop within a single block. If anything fails, the transaction reverts. No settlement risk, no capital sitting idle, no operational complexity.

RWAs break this entirely. Most tokenized funds - T-bills, credit instruments, money market products - settle on T+1, T+3, or longer. Each leverage loop becomes a discrete, asynchronous event: buy, wait for settlement, post collateral, borrow, wait again, repeat.

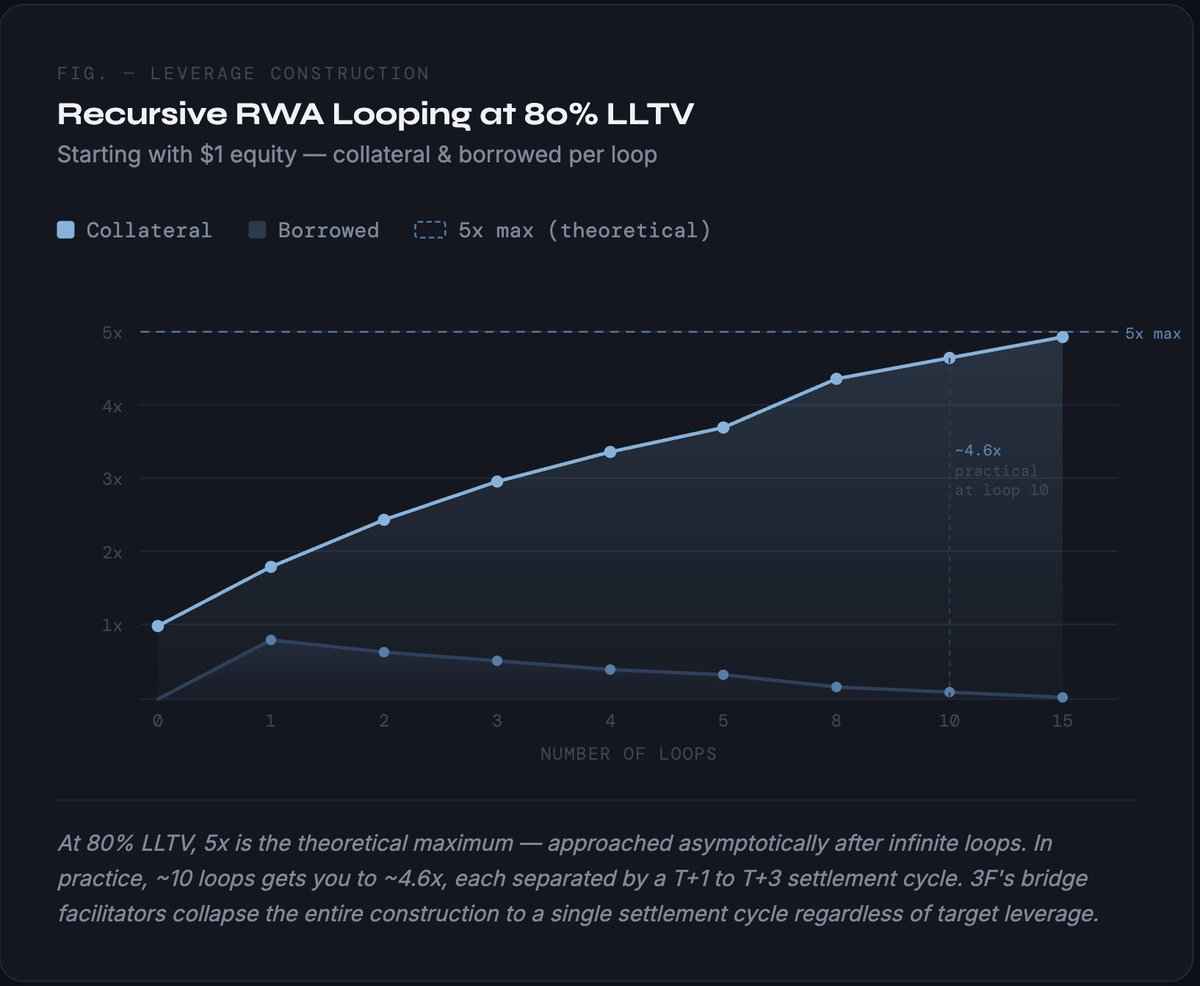

Suppose the RWA is collateral on a lending market at 80% LLTV (theoretical max leverage of 1/(1-80%) = 5x). Reaching a meaningful approximation to 5x requires roughly 10-15 loops. For a T+1 instrument, that's a minimum of 10-15 days of sequential execution. For a T+3 asset, that stretches to 30-45 days - nearly a full month just to build the position. Unwinding the trade would take just as long. The compounding cost of time is not a minor inconvenience; for a strategy whose entire thesis is yield generation, 30 days of drag before the position is even fully constructed is a structural problem.

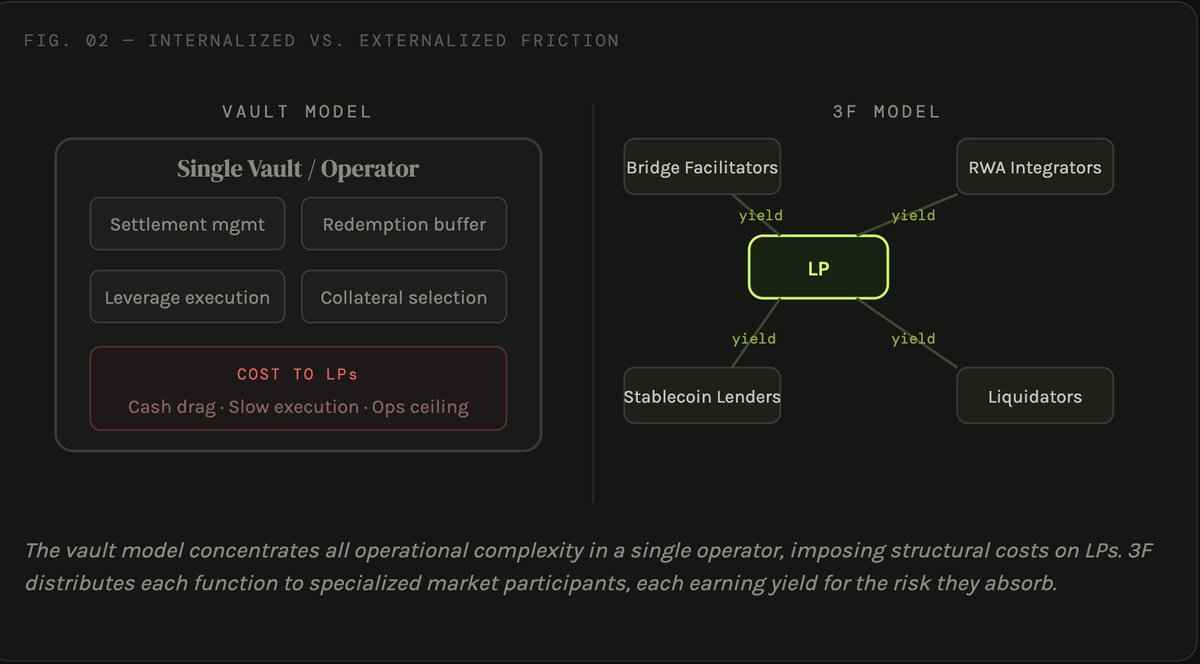

Most RWA looping strategies live today handle these frictions by internalizing them inside a single, centrally-managed vehicle. Leveraged RWA vaults deploy curator-managed strategies where the risk curator oversees the entire lifecycle of the leveraged position. Yield-bearing stablecoins also take a similar approach, running recursive RWA strategies internally as a yield source for their stable asset.

In both designs, one operator must absorb every friction point simultaneously:

Settlement delays compound across each loop, slowing position construction/unwind and forcing constant recalibration of duration risk as each layer settles at a different point in time. In fast-moving markets, this lag can prevent the strategy from ever reaching its optimal leverage target - by the time the position is fully constructed, the rate environment may have already shifted.

Redemption liquidity must be actively managed - vaults are forced to hold idle stablecoin buffers so users can exit without waiting through settlement cycles, creating a structural drag on yield that never fully goes away.

Collateral selection demands ongoing underwriting - ensuring the spread between RWA yield and borrowing cost remains wide enough to justify the position after fees and operational costs.

The system works, but at a cost to the LPs.

DeFi has repeatedly shown that open markets outperform centralized intermediaries when it comes to pricing and absorbing risk. Lending protocol liquidations are the canonical example - rather than a single entity managing unwind events, a competitive market of liquidators ensures positions are closed quickly and at fair prices. The protocol sets the rules; the market does the work. The result is a system that gets more efficient as participation grows, not less.

The same logic applies to RWA leverage. The frictions - settlement delays, redemption liquidity, collateral underwriting - are not problems to be hidden. They are discrete risks, and risks have a price. The question is whether they should be absorbed by a single vault operator, or whether they can be decomposed into open markets where specialists compete to provide each service more efficiently.

The answer suggests a different kind of architecture entirely: rather than a vertically integrated vault, a coordination network where each friction becomes a function, and each function becomes a market.

@3f_xyz is a one-click leverage protocol for asynchronous assets like RWAs - built around the premise that the most efficient way to handle operational complexity is not to absorb it, but to distribute it. Rather than one operator managing everything, 3F decomposes the RWA leverage stack into discrete functions and creates open markets for each. Specialists compete to fill each role, earn yield for doing so, and make the overall system more efficient over time.

Bridge Facilitators - Earn Yield by Collapsing Settlement Delays

The most structurally novel component of 3F is the bridge facilitator network, which eliminates the looping mechanic entirely.

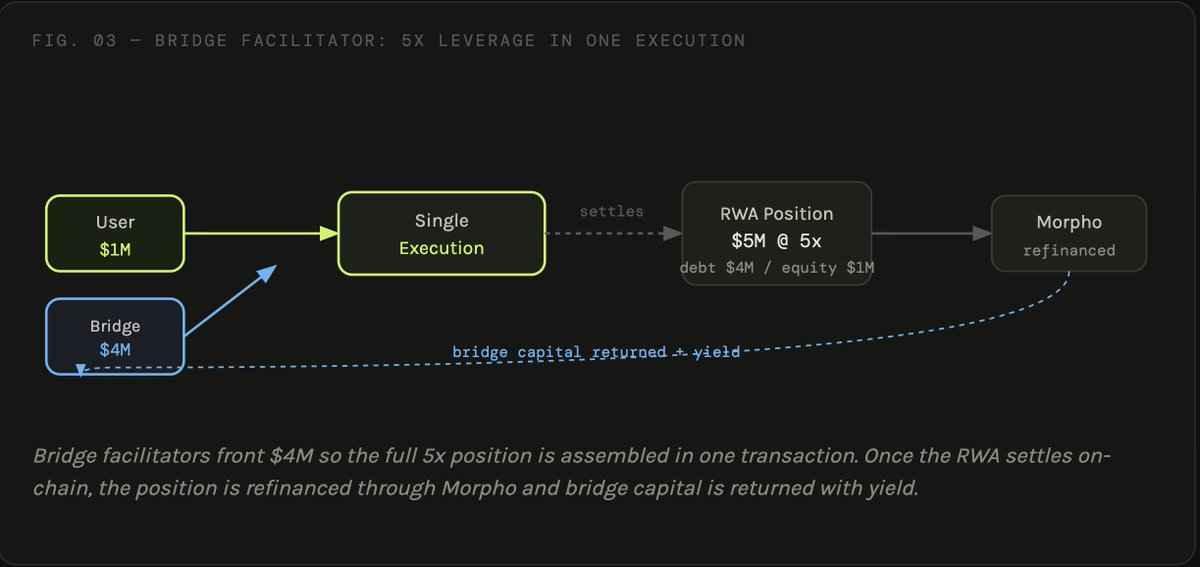

Rather than building leverage through sequential loops, bridge facilitators provide the full up-front capital needed to assemble a position in a single execution. A user targeting 5x leverage on $1M deposits their equity; bridge facilitators supply the remaining $4M; the full $5M RWA position is purchased at once and refinanced through @Morpho as collateral settles on-chain. Total construction time drops from N × T to just T, regardless of target leverage.

The same logic applies in reverse. To unwind, bridge facilitators front the $4M needed to repay the Morpho loan, releasing the full collateral in a single redemption. The RWA redeems once, the proceeds repay the bridge, and the LP receives their equity back. Total unwind time drops from N × T to T as well.

Build or unwind, the settlement delay that was previously a structural drag on vault LPs becomes a short-duration yield opportunity for bridge facilitators - capital deployed for one settlement window, then recycled into the next position.

RWA Liquidity Integrators - Earn Fees Coordinating Instant Redemption Flows

Bridge facilitators collapse leverage construction and unwind to a single settlement cycle; but for longer-duration RWAs where that cycle might be quarterly, even one settlement cycle can be too long. A user who wants out today shouldn't have to wait three months.

Rather than internalizing this as idle liquidity buffer, 3F externalizes it. Specialized integrators could coordinate instant redemption flows as a dedicated function, and users choose: wait one settlement cycle to unwind at par, or exit immediately at a market-priced cost.

The integrator type naturally matches the asset. Shorter-duration RWAs suit players who offer atomic swaps between RWAs and stablecoins around the clock (e.g. @multiliquid_xyz). Longer-duration assets suit operators who can price the discount to par based on asset risk and time to primary market redemption - managing the timing complexity that a generic vault simply isn't built for (e.g. @FissionXYZ). Either way, integrators earn fees for absorbing an operational layer that would otherwise sit as dead weight on LP yield.

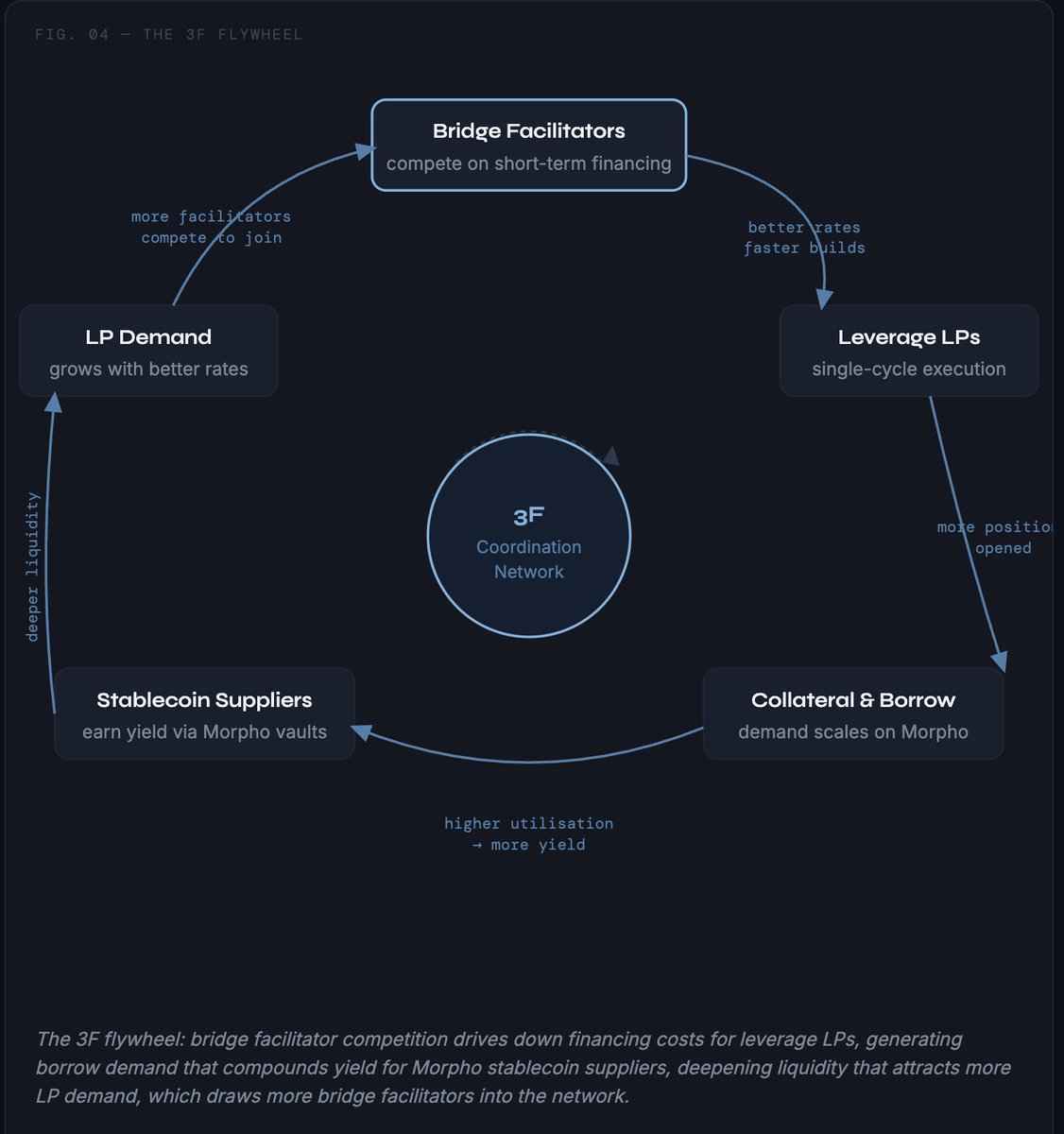

3F is building the foundational leverage network for RWAs - a coordination layer where synthetic dollar protocols, hedge funds, vault curators, and DeFi users can access deep, efficiently priced RWA leverage without absorbing the operational complexity that comes with it. Rather than each player internalizing the same frictions in isolation, they plug into a shared network where those frictions are externalized, priced, and competed away by every participant acting in their own interest.

The flywheel is self-reinforcing: as more bridge facilitators compete to offer the most efficient short-term financing, leverage LPs gain access to better rates and single-cycle execution. This drives greater collateral and borrow demand, which powers yield to Morpho stablecoin suppliers, which deepens the liquidity available for LPs to deploy further, which in turn attracts even more bridge facilitators into the network.

For every participant who helps make it work, there is yield on the table.