On June 5, 2025, Circle, the issuer of USDC, successfully debuted on the NYSE, injecting vitality into the entire stablecoin industry. Circle was able to attract intense interest through its vertically integrated product strategy, supported by the crypto-friendly political climate in the United States.

As Circle drew explosive attention, people naturally began searching for the next winner under the GENIUS Act. There is a stablecoin protocol that evokes a sense of déjà vu with Circle and is guiding the industry with a similar strategy: Frax Finance.

Frax Finance is a stablecoin protocol that issues frxUSD, a GENIUS Act–compliant stablecoin. It goes beyond simple issuance by presenting itself as a stablecoin operating system, providing FraxNet—a frontend that enables easy use of frxUSD—and Fraxtal, the high-performance blockchain that underpins it.

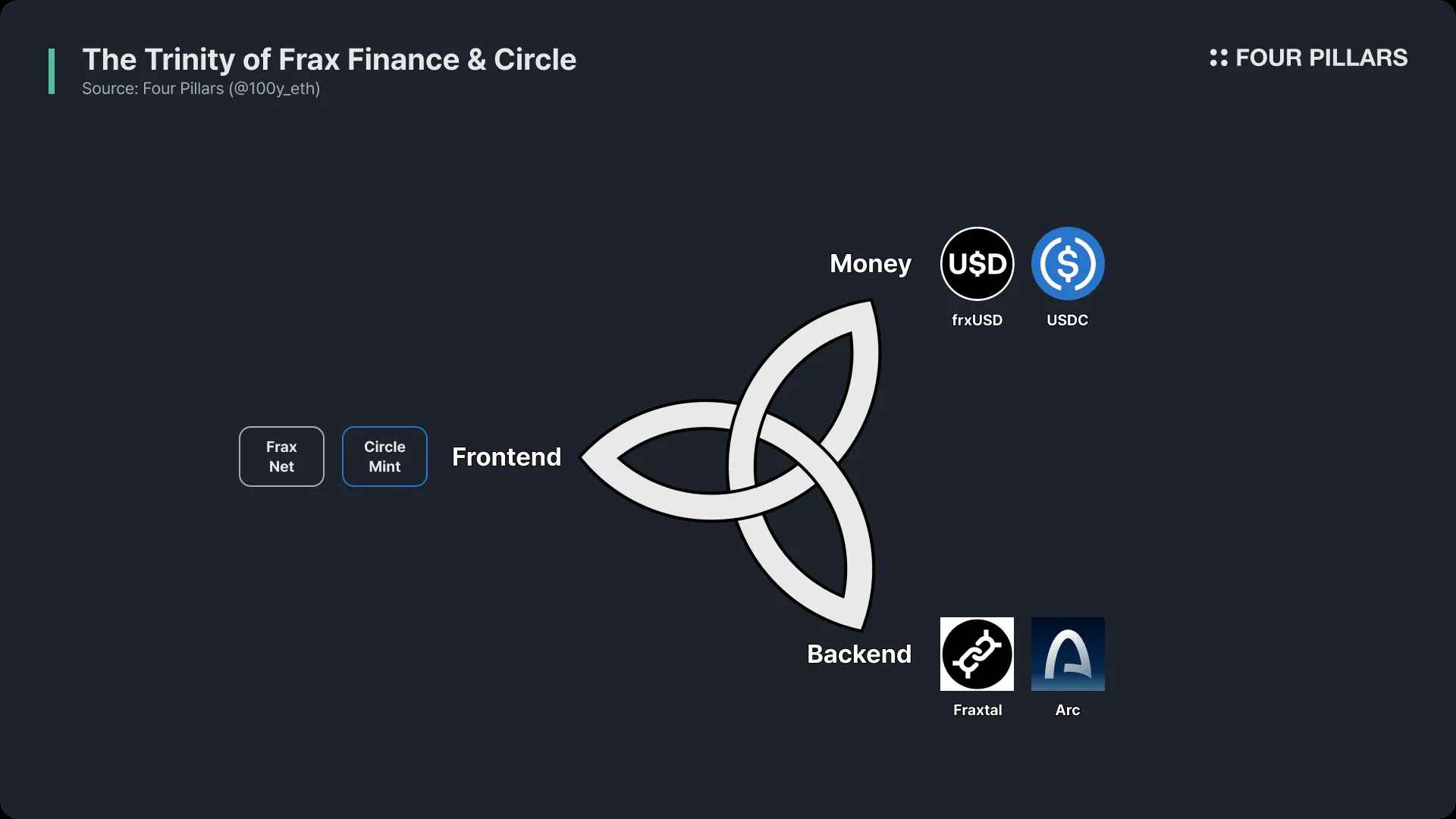

The three components of a financial system are money, the frontend, and the backend. From the perspective of financial industry development, today’s inefficient backend systems will gradually shift toward blockchain. In this trend, the three components of a stablecoin-based system are the stablecoin, the frontend, and the blockchain network. Frax Finance is one of the few projects building all three elements, presenting a vertically integrated direction.

Frax Finance stands at a major turning point for the next chapter. From the founder’s political leadership in shaping the original GENIUS Act draft, to its vertically integrated product vision through the stablecoin operating system, and even to the sweeping transformation of the protocol through the Polaris upgrade, Frax Finance is more thoroughly preparing for the future envisioned by the GENIUS Act than anyone else.

Source: CNBC

On June 5, 2025, Circle was listed on the New York Stock Exchange (NYSE) under the ticker symbol CRCL. The IPO price was set at $31 per share, higher than the initially expected $27 to $28 range, raising approximately $1.1B. On the first trading day, the opening and closing prices were $69 and $83 respectively, and as of August 25, 2025, the stock price was around $135. This positioned Circle as one of the most successful IPO cases.

Circle’s NYSE listing carries implications beyond being a simple milestone for the company. Coupled with the passage of the GENIUS Act, the easing of SEC regulations, and the crypto-friendly stance of the Trump administration, it served as a signal that crypto companies could enter the traditional financial markets. Moreover, the hot reception of Circle in the public market instilled confidence that stablecoin infrastructure could also thrive in traditional finance.

In other words, Circle’s listing was not just its own success but a victory for the entire stablecoin industry.

Source: Circle

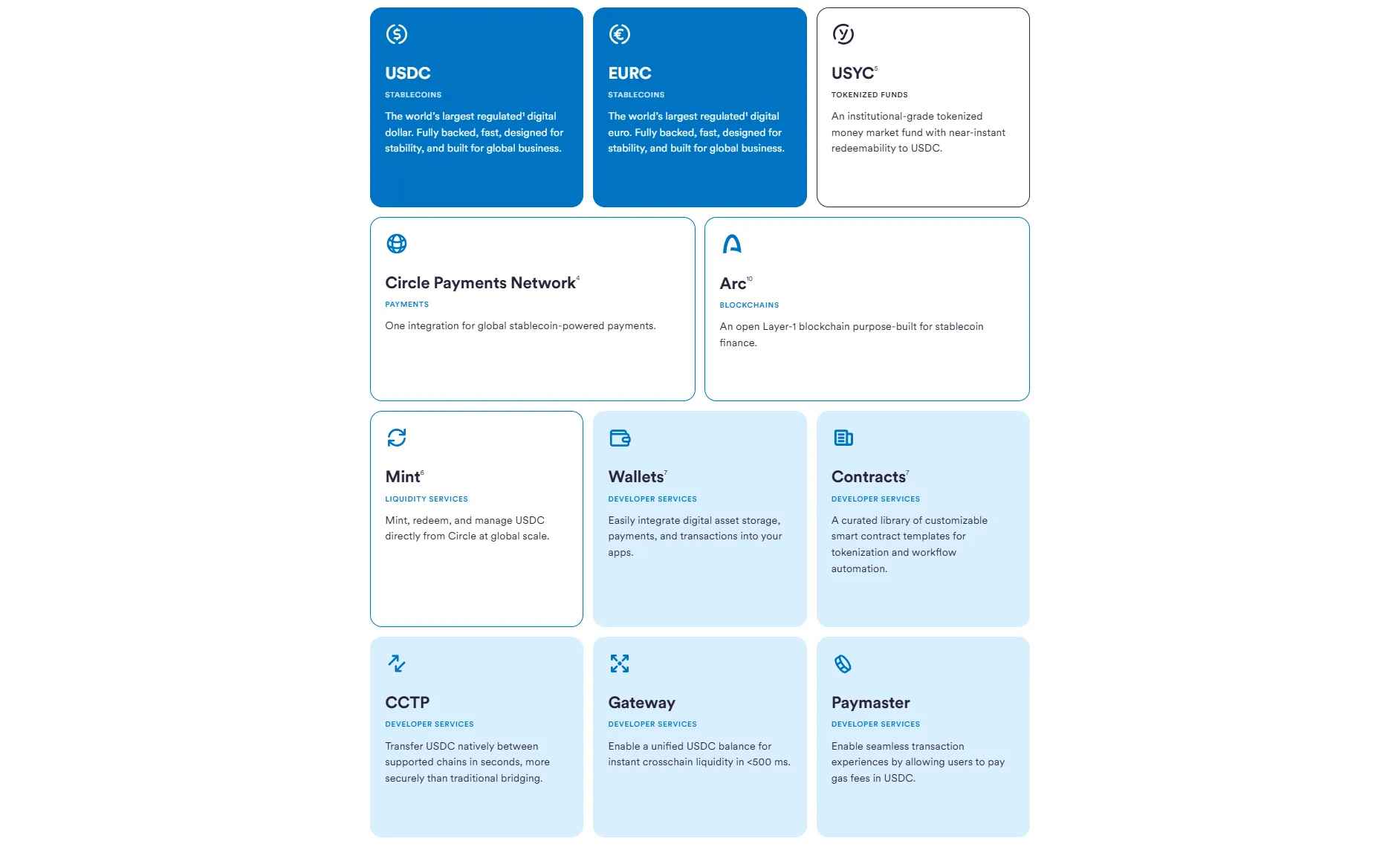

Circle is one of the world’s largest stablecoin issuers, providing the dollar-pegged USDC and the euro-pegged EURC. In addition, under its mission of building a new internet-based financial system, Circle offers a wide range of products such as:

Circle Payments Network (CPN): Circle’s standard for global fund transfers, aiming to serve as a blockchain-based alternative to SWIFT. Financial institutions and corporations using CPN can efficiently process cross-border remittances and settlements through Circle’s infrastructure and various public blockchains. For more information, see “CPN: Towards Digital Native SWIFT.”

Circle Mint: Integrated with traditional banking networks such as wire and SEPA, Circle Mint allows corporate and institutional users to instantly mint USDC and EURC, and redeem them at a 1:1 ratio with fiat currency. Notably, Circle Mint is the only official channel for directly issuing USDC.

Circle Wallets: A wallet SDK service that enables Web2 companies to easily integrate blockchain-based wallets into their services. Beyond simple wallets, it also provides account abstraction, MPC-based security, RPC nodes for transaction broadcasting, compliance options, multi-chain support, and more.

CCTP: Since USDC is natively issued on more than 20 networks, liquidity fragmentation can occur. Circle’s cross-chain messaging protocol CCTP enables secure transfers of USDC across different blockchains through a burn-and-mint mechanism.

Circle Paymaster: Circle’s ERC-4337–based account abstraction feature. Instead of users paying blockchain fees in ETH, Circle Paymaster allows them to pay fees in USDC or have fees sponsored, enabling gasless transactions for customers.

USYC: At the end of 2024, Circle acquired Hashnote, the issuer of USYC, and incorporated it into its product lineup. USYC is a tokenized money market fund composed of U.S. treasuries and reverse repos. Institutional clients holding USYC gain access to stable on-chain yields, and the token can also be used as margin collateral on exchanges such as Deribit and Binance.

Arc: Announced in August, Arc is Circle’s USDC-focused L1 network designed with a high-performance consensus algorithm to make USDC usage seamless and efficient. For more details, see “Circle Unveils Arc: A Similar Yet Different Playbook from Tether.”

In this way, Circle is not only issuing stablecoins but also building infrastructure that allows both institutions and retail users to easily utilize stablecoins. Covering issuance, wallet infrastructure, cross-chain bridges, an L1 network, account abstraction features, and institutional solutions, this serves as a prime example of vertical integration in product strategy.

From a user experience perspective, Circle’s product lineup demonstrates its strength. Imagine a company leveraging Circle’s products: it could mint and redeem USDC instantly 1:1 through Circle Mint, provide its customers with easy access to stablecoin functions via Circle Wallets, Paymaster, and CCTP even if they are unfamiliar with Web3, adopt the Arc blockchain for the most seamless and efficient USDC usage, and rely on CPN for transactions and settlements with other financial institutions and corporations.

The core of stablecoins is not issuance but utility. While issuing stablecoins safely with collateral design and regulatory frameworks is important, issuance without real-world use cases is meaningless. Circle’s vertically integrated product roadmap lays the foundation for stablecoins to be widely adopted across both the real world and the on-chain ecosystem.

So how was Circle able to receive such heated attention not only from the blockchain industry but also from the traditional financial markets? Beyond product aspects, several factors such as the current political climate and Circle’s business model play a role:

Passage of the GENIUS Act: The GENIUS Act, the first federal law in the United States to clearly regulate dollar-based stablecoins, was the factor that most directly impacted not only Circle but the entire stablecoin industry. It established the legal status of stablecoins, the obligations of issuers, and consumer protection requirements. This provided the legal foundation for institutions and corporations in the U.S. to issue stablecoins. Effectively, Circle’s internal operating guidelines were codified as legal standards, granting Circle legitimacy and compliance.

Pro-crypto policies of the Trump administration: From before his inauguration, the Trump administration declared strong support for crypto. On July 30, 2025, the President’s Working Group on Digital Asset Markets under the administration released a 160-page policy report on crypto. The report presented a concrete roadmap to position the United States as the global capital of crypto.

SEC: Paul Atkins, the new SEC chair, has also taken a pro-crypto stance, adopting a much more relaxed regulatory position compared to Gary Gensler. Following the White House’s release of its crypto policy roadmap, the SEC quickly announced an initiative called Project Crypto, which is making regulations in the U.S. crypto industry much clearer.

Market share: Circle issues USDC, the world’s second-largest stablecoin. Currently, USDC’s supply stands at around $63B, accounting for about 30% of the total stablecoin market. Considering that USDT, due to its collateral composition, cannot comply with the GENIUS Act regulations, USDC is by far the largest compliant stablecoin under U.S. regulation.

Business model: Circle’s primary revenue comes from managing USDC reserves through treasuries, repos, and similar instruments. In Q2 2025, Circle recorded $658M in revenue and an adjusted EBITDA of $126M, showcasing an attractive revenue structure and a solid operating margin.

The current U.S. political environment provides the perfect setting for Circle to gain attention, while also laying the foundation for the rapid growth of the entire stablecoin industry.

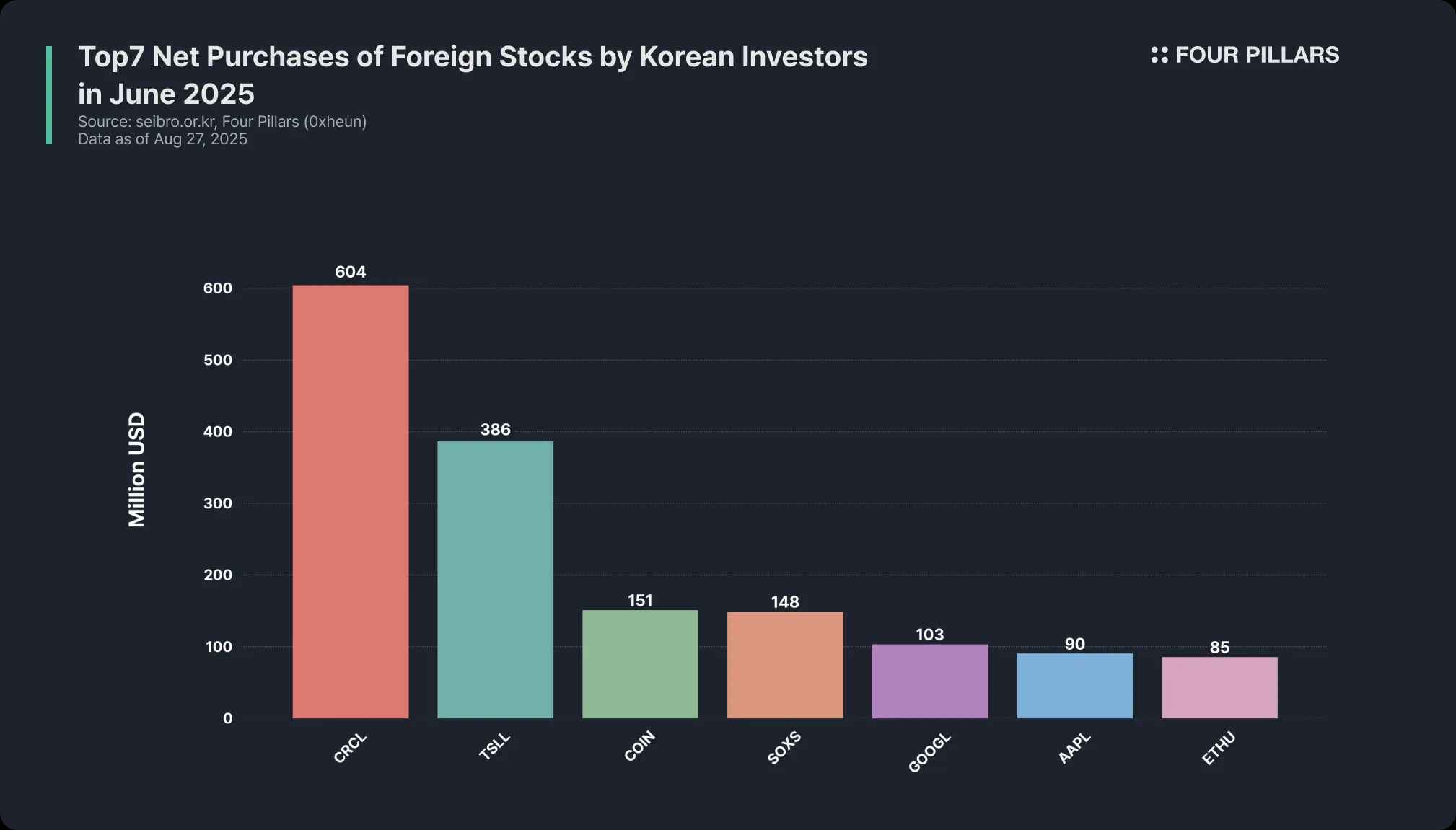

Interestingly, Circle’s popularity has been extremely strong not only in the U.S. but also in other countries. In fact, when looking at the ranking of overseas stocks most purchased by Koreans in June 2025, Circle (CRCL) took the top spot, with net purchases exceeding $600M. This was 1.6 times the volume of Tesla 2X ETF in second place, four times that of Coinbase in third, and far higher than Alphabet ($100M) and Apple ($90M).

Why is Circle attracting such intense interest in Korea? Of course, many Korean investors actively trade U.S. stocks, but the deeper reason is that the Korean market itself is experiencing a heated wave of interest in stablecoins. In June 2025, President Lee was inaugurated and he declared strong support for the legalization of stablecoins. This became a powerful trigger for Koreans to take interest in the stablecoin industry.

Of course, Korea still faces many barriers before the full legalization of a won-based stablecoin due to strict foreign exchange laws, the conservative stance of the Bank of Korea, and the small size of the short-term bond market. Nevertheless, whenever a specific company or institution files a trademark related to stablecoins, its stock price surges, showing that the interest in stablecoins extends not only across the blockchain industry but also among general stock market investors.

With Circle’s successful debut, companies and investors naturally turned their attention to the stablecoin industry and began searching for the companies and protocols that could benefit most from the GENIUS Act after Circle. Coinbase has often been mentioned as a beneficiary, as Circle shares nearly half of its USDC reserve revenue with Coinbase. In Q2 2025, Circle’s total reserve revenue was $634M, of which more than half, $332.5M, was paid to Coinbase.

Aside from companies like Coinbase that benefit indirectly, are there any publicly listed companies that issue GENIUS Act–compliant stablecoins and receive direct benefits like Circle? Unfortunately, there are none. Among companies listed in the U.S. stock market, none issue GENIUS Act–compliant stablecoins. Paxos is the second-largest U.S.-based stablecoin issuer, but it is a private company.

Even if the next Circle cannot be found in the stock market, there is no need to be disappointed. This is because there are stablecoin protocols on-chain that issue dollar-based stablecoins compliant with the GENIUS Act. Currently, only two protocols in the market aim to issue GENIUS Act–compliant stablecoins. One is Ethena, and the other is Frax Finance.

Source: Ethena

Ethena offers two types of stablecoins: USDe and USDtb. USDe does not comply with the GENIUS Act because its reserves are based on delta-neutral positions in the futures market. However, USDtb’s reserves are composed of the MMF fund BUIDL and stablecoins. Moreover, the issuance of USDtb, which was previously done in the BVI, transitioned in July 2025 to issuance through Anchorage Digital Bank, thereby preparing for GENIUS Act compliance.

Source: X(@samkazemian)

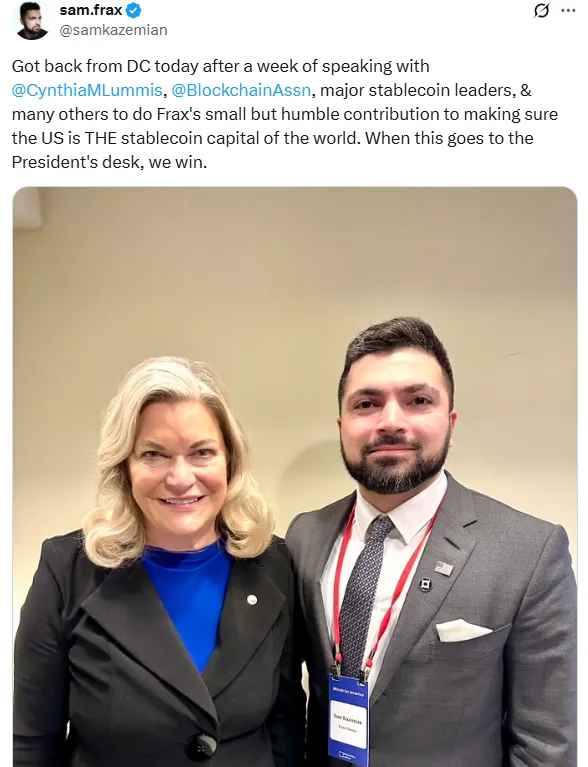

Frax Finance issues the frxUSD stablecoin, whose reserves are composed of various dollar-based MMF tokens and U.S. treasury fund tokens. Notably, Frax Finance’s founder, Sam Kazemian, was one of the key figures who helped bring the monumental GENIUS Act stablecoin legislation into existence.

In March of this year, Sam met with Senator Cynthia Lummis, a co-sponsor of the GENIUS Act, and provided advice and support in drafting the bill, contributing to the successful establishment of a legal framework for the digital dollar.

Unlike other protocols, Frax Finance not only built products to advance its core business but also actively engaged in regulatory discussions, working closely with lawmakers to shape the regulatory framework. This represents a proper example of policy entrepreneurship. Since the founder himself contributed to the drafting of the bill, Frax Finance understands the GENIUS Act better than anyone else and was able to design frxUSD in alignment with it.

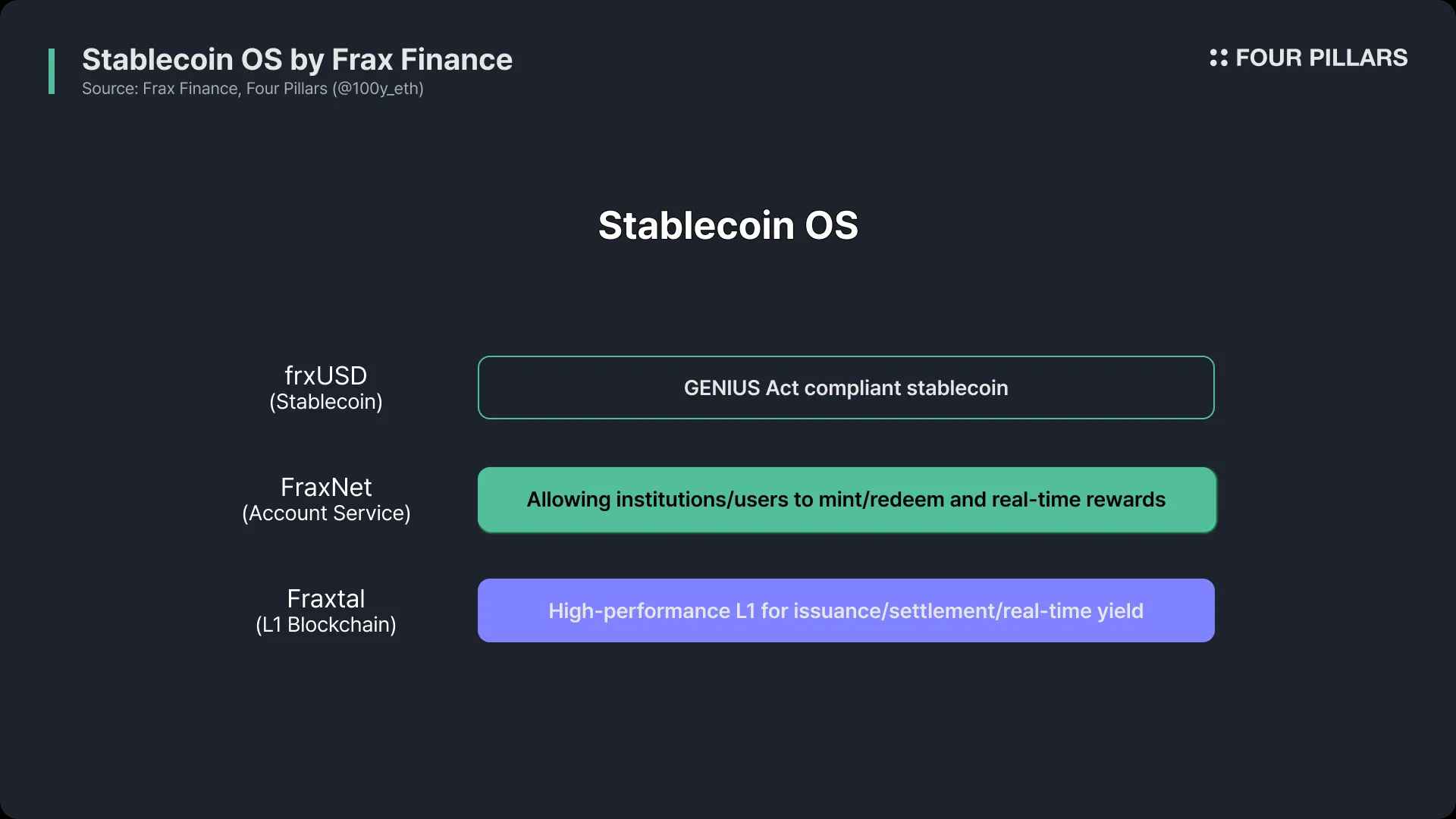

Frax Finance’s goal is to issue stablecoins in a reliable way and to build scalable infrastructure that allows them to be widely used. To achieve this, Frax Finance presents the Stablecoin OS, offering its three core products: frxUSD, FraxNet, and Fraxtal.

frxUSD: A GENIUS Act–compliant stablecoin and the core asset of liquidity in the Frax ecosystem.

FraxNet: A platform where users can issue and redeem frxUSD in various ways and earn stable returns from non-custodial holdings of stablecoins in compliance with the GENIUS Act.

Fraxtal: A high-performance EVM L1 blockchain built for frxUSD, using the FRAX as its gas token.

While issuance is important, utility is even more critical for stablecoins. Frax Finance not only issues frxUSD in compliance with regulations but also provides FraxNet, a frontend where users can easily use frxUSD, and Fraxtal, an ecosystem built specifically for frxUSD.

In this structure, frxUSD serves as money, FraxNet takes on the role of fintech and banks, and Fraxtal serves as the backend of the financial system. The harmony of these three products functions as the core engine of the frxUSD ecosystem.

In addition, Frax Finance offers various services such as Fraxswap for trading, Fraxlend for lending, and frxETH, an Ethereum liquid staking protocol, thereby building a full-stack stablecoin and DeFi ecosystem. The full story of the Frax Finance ecosystem and how it has grown to its current position will be introduced in the next article.

Source: GovInfo

Sam Kazemian, the founder of Frax Finance, participated in drafting the GENIUS Act, and as a result Sam and the Frax team have a deep understanding of it. Based on this regulatory expertise, Frax Finance began issuing frxUSD, a stablecoin compliant with regulatory requirements, in February of this year. But what exactly qualifies a stablecoin as GENIUS Act–compliant? And does frxUSD truly comply with the GENIUS Act?

The full text of the GENIUS Act is easily accessible online, but since it is lengthy, the key points are summarized below. For a stablecoin to be issued in compliance with the GENIUS Act, it must meet the following requirements.

(Aside from the items listed below, there are also requirements such as external accounting audits, capital adequacy, AML compliance, and priority of repayment in bankruptcy. Since these are related to internal operations, they will not be discussed here.)

3.2.1 Issuance Qualification

Only authorized issuers within the U.S. are allowed, and there are three types of authorized issuers. The first is subsidiaries of banks or credit unions, the second is institutions approved by the OCC, and the third is institutions approved by state financial regulators.

Through the approval of the FIP-432 governance proposal, all responsibilities related to the issuance of frxUSD, reserve management, and regulatory compliance were transferred to FRAX Inc. FRAX Inc. is a Delaware-registered corporation in the U.S. and must obtain approval either from the OCC or from state financial regulators to issue a GENIUS Act–compliant stablecoin. According to the FIP-432 document, FRAX Inc. is currently preparing to acquire a stablecoin issuer license.

3.2.2 Reserve Requirements

The core principle of reserves under the GENIUS Act is full 1:1 backing. In other words, the total supply of issued stablecoins must be supported by at least an equal amount of reserves. The composition of reserves is restricted to the following highly liquid assets:

U.S. currency or balances in Federal Reserve accounts

Demand deposits or withdrawable deposits, or insured deposits and credit union shares

U.S. treasuries with a remaining or original maturity of 93 days or less

Overnight repos entered into by the issuer as the seller, collateralized by treasuries with a remaining maturity of 93 days or less

Overnight reverse repos entered into by the issuer as the buyer, collateralized by U.S. treasuries

Registered government money market funds or securities registered under the Investment Company Act of 1940 that hold only the assets listed in (i) to (v)

Other assets directly issued by the U.S. federal government with a similar level of liquidity and stability as those listed above

Tokenized forms of assets in (i), (ii), (iii), (vi), and (vii)

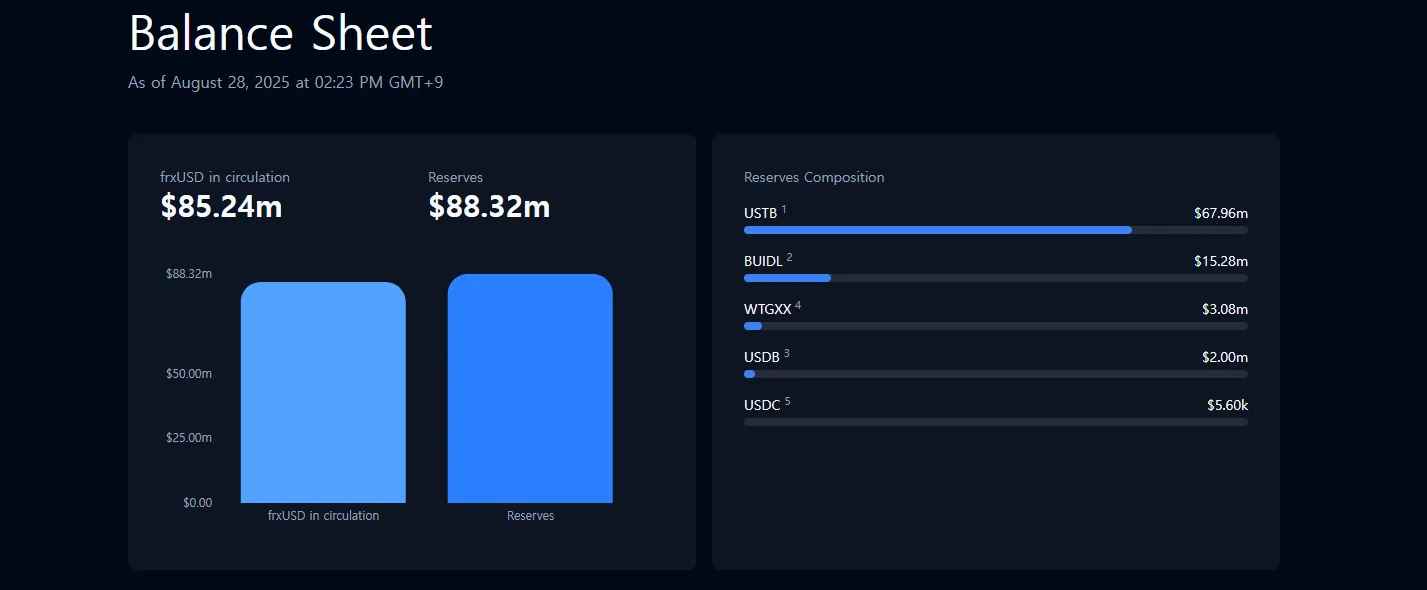

Source: Frax Finance

The reserves backing frxUSD issued by Frax Finance are entirely composed in tokenized form. The RWA tokens constituting frxUSD’s reserves are as follows:

USTB: A tokenized form of the Superstate Short Duration US Government Securities Fund, which invests in short-term U.S. treasuries, issued through Superstate. It is issued under Reg. D Rule 506(c) and Investment Company Act 3(c)(7).

BUIDL: A tokenized form of the BlackRock USD Institutional Digital Liquidity Fund, which invests in U.S. treasuries, cash equivalents, and repos, issued through Securitize. It is issued under Reg. D Rule 506(c) and Investment Company Act 3(c)(7).

WTGXX: A tokenized form of the WisdomTree Government Money Market Digital Fund, which invests in short-term U.S. treasuries and U.S. government agency bonds. It is an officially registered government money market fund issued under Investment Company Act 2a-7.

USDB: A stablecoin issued by Bridge, acquired by Stripe.

USDC: A stablecoin issued by Circle.

Thus, frxUSD’s reserves are composed of tokenized versions of (i) and (vi) in accordance with (viii), and with more than 100% overcollateralization, they satisfy the reserve requirements of the GENIUS Act and can maintain stable value.

3.2.3 Yield Distribution?

Under the GENIUS Act, stablecoin issuers are not allowed to pay interest to stablecoin holders simply for holding or using them. This provision is intended to prevent similarities with deposits, avoid misinterpretation as investment assets, and ensure financial stability.

Because frxUSD complies with the GENIUS Act, users cannot earn interest just by holding frxUSD. However, if a user holds frxUSD within FraxNet, they can receive stable yields generated from bonds. At first glance, this may appear to violate the GENIUS Act, but it does not. How is this possible?

It is possible because the issuer is not directly paying interest to stablecoin holders. Instead, the distribution platform provides the rewards. FraxNet is operated by Frax Network Labs Inc., a Delaware-based legal entity distinct from the issuer. Therefore, only users who hold frxUSD within FraxNet can receive yield rewards.

Naturally, users holding frxUSD in personal wallets like MetaMask or in exchanges that support frxUSD cannot receive interest, in accordance with the GENIUS Act. This structure is not unique to Frax Finance but is also used without issue in Circle’s USDC and PayPal’s PYUSD.

Coinbase pays approximately 4.1% interest to users holding USDC within the Coinbase app, while PayPal pays about 3.7% interest to users holding PYUSD within the PayPal app. This is possible because Coinbase and PayPal are separate legal entities from the issuers Circle and Paxos.

So far, we have looked at how Circle was able to make its successful debut and explored Frax Finance’s frxUSD. But wait, did you feel a sense of déjà vu while reading about Frax Finance? The direction Frax Finance is taking to build its stablecoin ecosystem looks very similar to Circle’s.

The first déjà vu lies in the way stablecoins are issued. Both Circle and Frax Finance aim to issue GENIUS Act–compliant stablecoins backed by reserves consisting of cash, short-term U.S. treasuries, and repos. These stablecoins maintain stable value and serve as the lubricant for the next-generation financial system as money.

In terms of how interest income from reserves is used, Frax Finance may have more room to create a virtuous cycle within its ecosystem compared to Circle. While all the interest income from USDC reserves goes to Circle, the interest income from frxUSD reserves is used for FraxNet holders of frxUSD and team operations, with the remaining amount distributed to FRAX stakers, the core token holders of the Frax ecosystem.

This structure means that as more frxUSD is issued, the Frax ecosystem grows, which in turn increases the issuance of frxUSD, creating a positive feedback loop.

Circle provides frontends with high user experience that make it easy for USDC holders to use their stablecoins, such as 1) Circle Mint for easy issuance and redemption, 2) Circle Wallet for easy wallet integration, and 3) Circle Gateway for managing balances across multiple chains.

Source: FraxNet

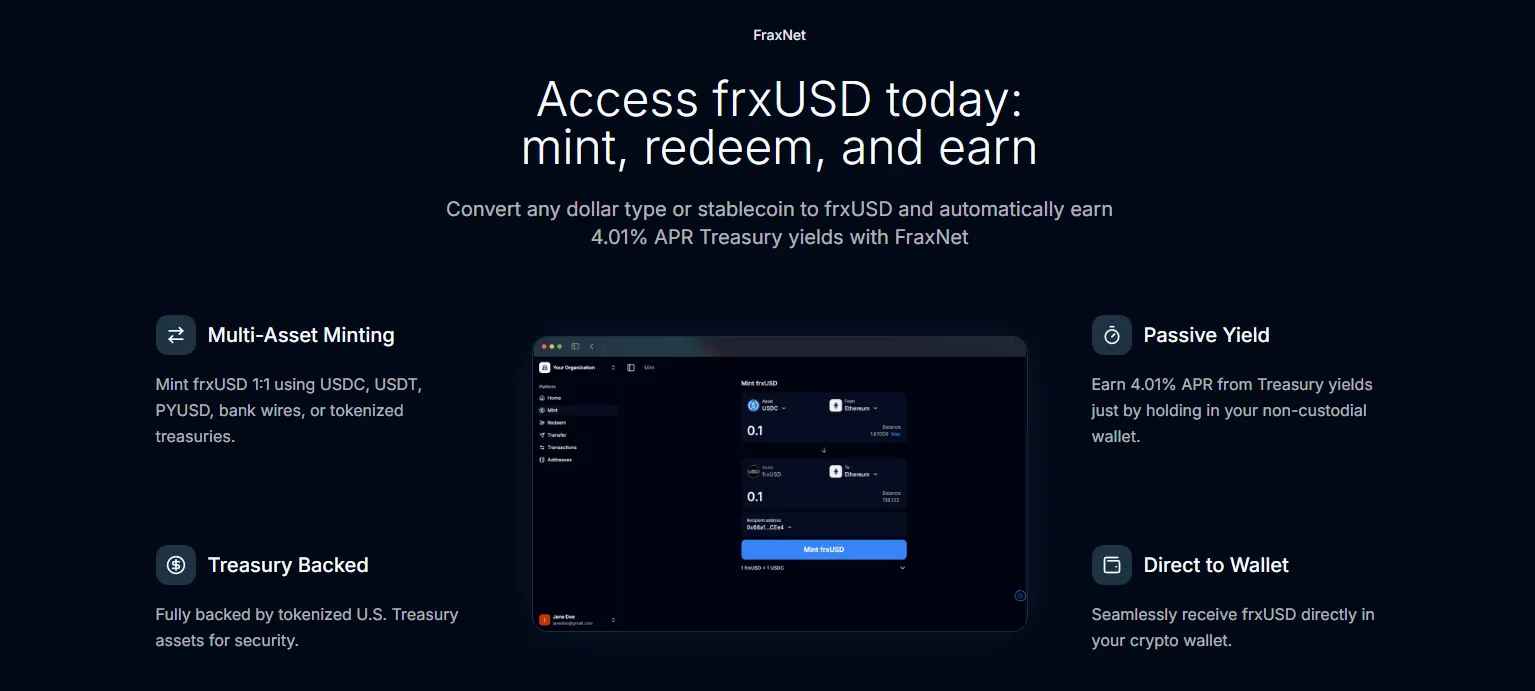

Similarly, Frax Finance provides a user-friendly frontend called FraxNet, which allows frxUSD holders to easily access various financial activities:

Multi-asset issuance: Users can issue frxUSD not only with stablecoins such as USDC, USDT, PYUSD, and USDB but also with bank wires and even RWA tokens like USTB and WTGXX. This is similar to Circle Mint.

Embedded wallet: Users can log into FraxNet with accounts such as Google, and a blockchain wallet is automatically created for them. This allows even users unfamiliar with blockchain to easily access frxUSD. This is similar to Circle Wallet.

Dashboard: FraxNet provides a dashboard that displays a wide range of assets across multiple networks at a glance and enables easy transfers. This is similar to Circle Gateway.

Passive yield: Users holding frxUSD within FraxNet can automatically earn stable interest income from bonds. Just like users holding USDC in the Coinbase app can earn yield, Frax Finance provides interest income to frxUSD holders on FraxNet.

While multi-asset issuance or passive yield are indeed powerful features, the four functions mentioned above can be considered fairly basic capabilities that modern financial services must have. FraxNet takes this a step further by aiming to deliver a much stronger vertically integrated product and user experience than Circle Mint through the following roadmap.

Virtual Visa Card: In collaboration with Stripe and Bridge, FraxNet plans to launch a virtual Visa card connected to the Visa network. This will enable users to utilize FraxNet assets for real-world payments.

Virtual Bank Accounts: Frax Finance is working with Lead Bank to provide each user with a virtual bank account, enabling deposits and withdrawals through the traditional banking network. This integration with existing infrastructure can improve the onboarding experience for users.

FraxNet Mobile: In 2026, FraxNet will launch an app that allows users to easily access FraxNet on mobile, providing them with a full mobile banking experience.

The goal is not just for the stablecoin issuance protocol to offer simple wallet, trading, monitoring, and yield opportunity services, but to build a complete user interaction lifecycle by supporting cards, banking, and mobile services that can be applied in real life.

In financial systems, the backend is just as important as the frontend. No matter how user-friendly the frontend is, if the backend where money actually moves is inefficient, users cannot be provided with a good experience.

To achieve this, in February 2024 Frax Finance launched its own high-performance blockchain network, Fraxtal. Fraxtal is designed to be optimized for the Frax ecosystem, with the goal of serving as the rail for frxUSD.

In fact, providing a backend optimized for its ecosystem makes Frax Finance a pioneer in the industry. Following Fraxtal, many stablecoin projects began to launch their own blockchains optimized for their stablecoins:

Converge: Ethena is developing Converge, a high-performance blockchain in collaboration with Securitize, to bridge DeFi and traditional finance around ENA and USDe.

Stable and Plasma: Tether has made strategic investments in Stable and Plasma, blockchain networks specialized for USDT transfers and payments.

Arc: Circle recently unveiled its own blockchain, Arc, optimized for USDC.

Ultimately, Frax Finance foresaw where the industry was headed. The launch of Fraxtal was not merely the release of another blockchain but a pioneering move pointing to the future of financial infrastructure.

The three elements of today’s financial system are money, frontend, and backend. We can engage in economic activities easily because fintech companies provide convenient frontends that connect us to complex payment, securities, and remittance backends.

From the perspective of financial industry development, today’s complex and inefficient backends will gradually transition to blockchains. In this trend, the three essential elements of blockchain-based financial systems are stablecoins, frontends, and blockchain networks. This is the stablecoin trinity, and Frax Finance is one of the few projects building all three, presenting a vertically integrated direction.

Source: Frax Finance

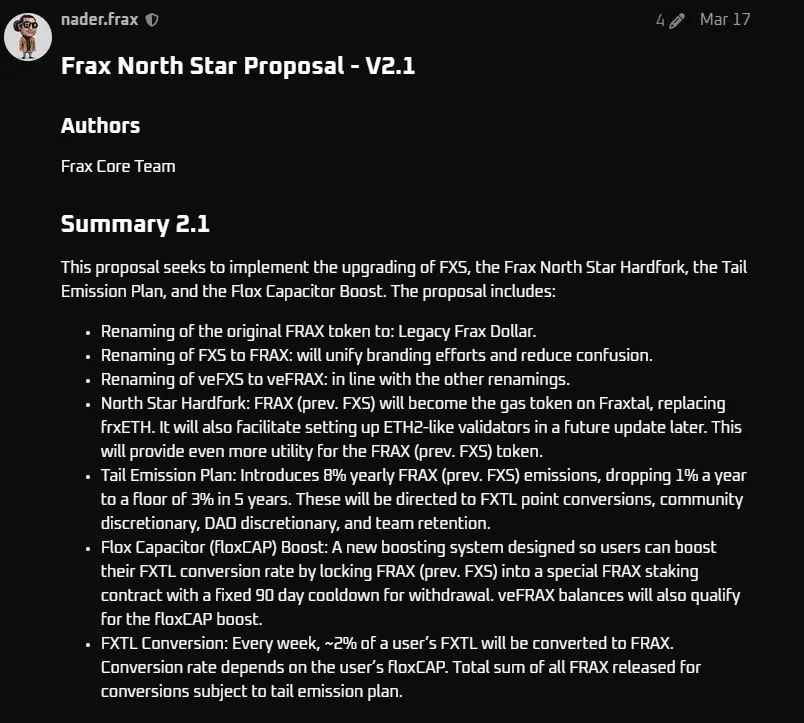

Since March of this year, Frax Finance has been preparing for the GENIUS Act and working on the North Star upgrade, which will transform the protocol accordingly. This upgrade includes rebranding the legacy Frax protocol tokens FRAX and FXS into frxUSD and FRAX respectively, changing the gas token of Fraxtal from frxETH to FRAX, and making other significant adjustments such as token incentive structures.

Frax Finance now stands at a major turning point for the next chapter. From the founder’s political leadership in contributing to the original GENIUS Act draft, to its vertically integrated product vision through the Stablecoin OS, and now to a sweeping transformation of the protocol through the North Star upgrade, Frax Finance is preparing for the future envisioned by the GENIUS Act more thoroughly than anyone else.

Some may argue that Frax Finance is merely following Circle’s roadmap. However, the reality is quite the opposite. By introducing FraxNet, an all-in-one platform for frontend, alongside Fraxtal, a blockchain purpose-built to serve as the backend infrastructure, Frax Finance has demonstrated that it is not just keeping pace but actively shaping the trajectory of the stablecoin industry. These innovations highlight Frax Finance’s role as a pioneer, setting the direction that the broader ecosystem is likely to follow.

Just as navigators once followed the North Star to find their way, Frax Finance too is setting the course for the industry through the North Star upgrade. This is more than just an upgrade. It is the act of establishing a new reference point for the entire industry, and ultimately Frax Finance will position itself as the guiding light at the forefront, like the North Star.

Dive into 'Narratives' that will be important in the next year