Thanks to advances in digital technology, the world is more connected than ever before. However, international remittance still relies on outdated networks. A prime example is SWIFT, the global standard, which takes anywhere from 1 to 5 business days to complete a cross-border transfer and involves numerous intermediary fees.

On April 22, 2025, Circle, the issuer of USDC, announced the launch of the Circle Payments Network (CPN). CPN leverages institutions and service provider networks, along with stablecoins and blockchain infrastructure, to enable individuals and businesses to send and receive cross-border payments quickly and at low cost.

The announcement of CPN came shortly after the launch of Plasma, a blockchain specialized in USDT. As stablecoin-related legislation in the US is expected to pass soon and the market continues to grow rapidly, both USDC and USDT seem to share a common goal but are taking different paths to reach it.

“Ignoring technological change in a financial system based upon technology is like a mouse starving to death because someone moved their cheese” - Chris Skinner

SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. It is a network founded in Belgium in 1973 that enables international money transfers through secure and standardized message transmission between financial institutions around the world. One common misconception is that SWIFT does not actually move money itself. Instead, it facilitates the secure delivery of payment instructions between banks.

In the early 1970s, international payments were mostly conducted through Telex—a text communication system that operated via telephone lines and was originally used for military communication. Telex was slow, prone to errors, and lacked security. To address this, 239 banks came together in Brussels in 1973 to create SWIFT, with the goal of establishing a standardized messaging system for global financial transactions.

Since then, SWIFT has rapidly expanded across Asia, Africa, and Latin America. Along the way, it has improved member institution security and adopted modern message standards such as ISO 20022, which enables structured data and automation for greater efficiency. Today, SWIFT handles over 50 million messages per day across more than 200 countries.

So, how exactly does a SWIFT-based international remittance work? Throughout the process, messages are secured via encryption and authentication, and the system adheres to anti-money laundering (AML) and counter-terrorism financing (CFT) regulations.

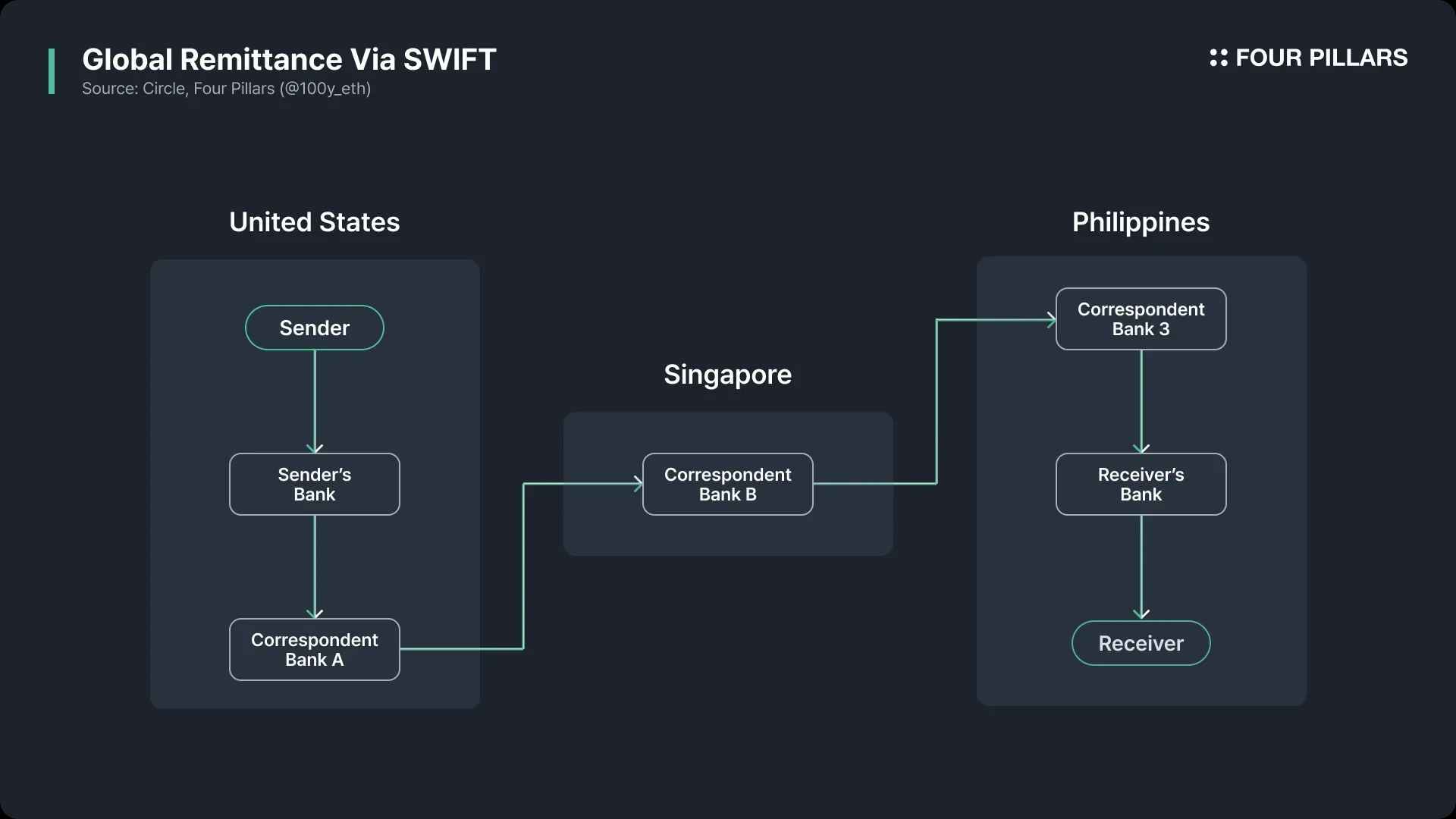

Initiation of Transfer Request: The sender provides their bank with the recipient’s bank information (including SWIFT code) and account number to initiate an international transfer.

Transmission of SWIFT Message: The sender’s bank sends a payment instruction via the SWIFT network to the recipient’s bank.

Fund Movement via Intermediary Banks: If there is no direct account relationship between the sender’s and recipient’s banks, the transfer goes through one or more intermediary banks.

Receipt and Deposit by Recipient Bank: The recipient bank receives the SWIFT message and deposits the funds into the recipient’s account.

This process typically takes between 1 and 5 business days, and it costs significantly more than a domestic transfer. Sending money abroad through a bank or fintech platform usually involves fees ranging from a few to several dozen dollars. Why is this the case?

Let’s start with the slow speed. If the sender’s and recipient’s banks don’t have a direct relationship, the transfer must pass through intermediary banks. Each intermediary may have its own processing steps, extending the timeline. Differences in operating hours and time zones, along with weekends and holidays across countries, can also cause unnecessary delays.

Costs are high for similar reasons. Each intermediary may charge a fee. In addition, many international transfers require currency conversion, which often comes with a foreign exchange fee and less favorable exchange rates than the market rate.

While SWIFT is the global standard for international transfers, several other cross-border payment systems also exist around the world:

CIPS (Cross-Border Interbank Payment System): Developed by the People’s Bank of China, CIPS supports yuan-based international transactions. It aims to offer functions similar to SWIFT and expand yuan usage in Asia.

SPFS (System for Transfer of Financial Messages): Created by the Central Bank of Russia, this system is used by financial institutions in and around Russia that are restricted from using SWIFT due to sanctions.

ACUMER: Developed by Iran, this alternative system was introduced to bypass U.S. sanctions and serve as a substitute for SWIFT.

CIPS and SPFS generally offer lower fees and faster transaction speeds compared to SWIFT. This is largely due to the smaller number of participating countries and banks, which allows for more centralized management. However, these systems also suffer from a major drawback—limited global interoperability and adoption.

Besides international networks, many domestic payment systems also operate around the world. Examples include the U.S.'s ACH, the European Union’s SEPA, Brazil’s PIX, and India’s UPI. These systems are much more efficient than SWIFT in terms of cost and speed, but they lack interoperability with each other and have limited international usage.

With advances in transportation and digital technology, the world is more interconnected than ever, and cross-border economic activity is accelerating as market barriers continue to fall. Ironically, however, most systems for moving money still rely on outdated infrastructure. This isn’t due to a lack of technology but rather stems from the fundamental nature of money itself. For money to retain its value, it requires trust and consensus among members of society. This is why trusted entities like banks, institutions, and governments have always played a central role.

Fortunately, as we enter the era of digital transformation, humanity has invented a financial system well-suited for this new age: blockchain. Blockchain is a decentralized network maintained by servers incentivized to keep it running. Its permissionless and trustless nature makes it an ideal foundation for global financial transactions.

One company seeking to leverage these advantages to reinvent global payments and remittance infrastructure is Circle, the issuer of the USDC stablecoin.

“By orchestrating stablecoin payments, Circle Payments Network enables payment providers to unlock new markets and new business models faster than ever before.” - Nikhil Chandhok

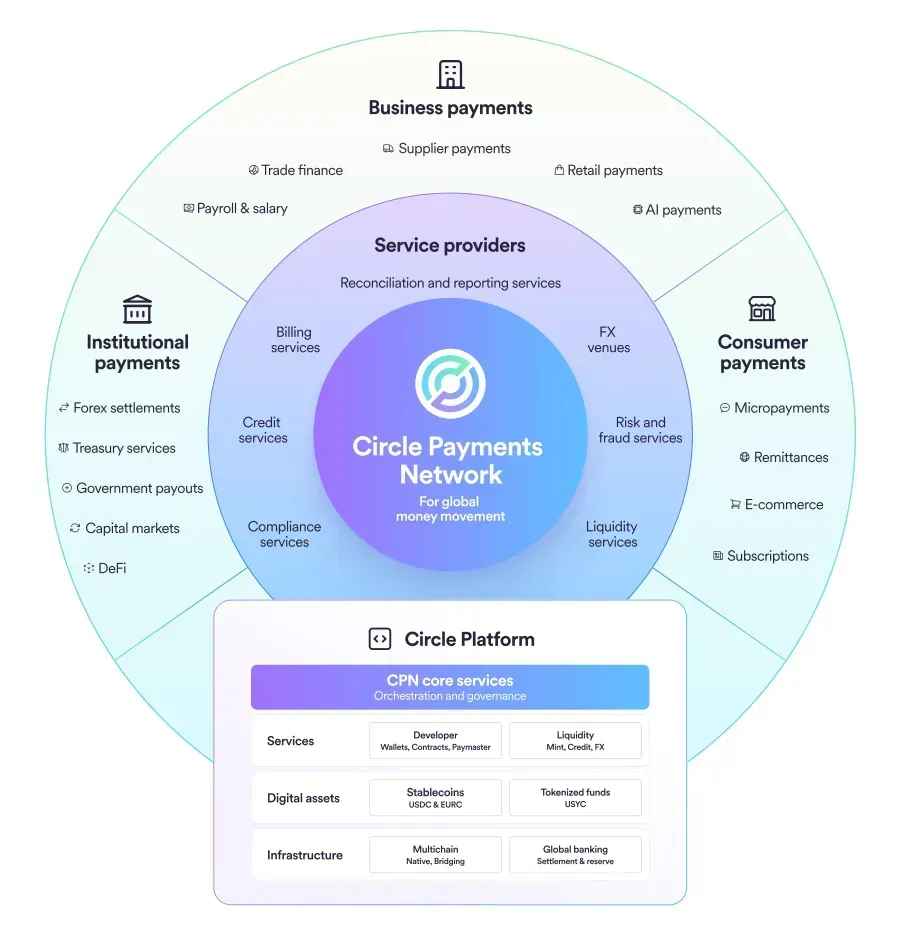

On April 22, 2025, Circle announced the launch of the Circle Payments Network (CPN). Built on blockchain and stablecoin infrastructure, CPN introduces a new standard for cross-border capital movement. It brings together global banks, payment service providers, and digitally native financial institutions.

CPN is the first initiative to combine regulated stablecoins with a governance layer tailored for traditional financial institutions. It connects stablecoins to existing payment systems and creates a trusted settlement layer between institutions. Since the settlement takes place on secure, always-on public blockchains using stablecoins, transactions can occur in real time across borders, time zones, and currencies.

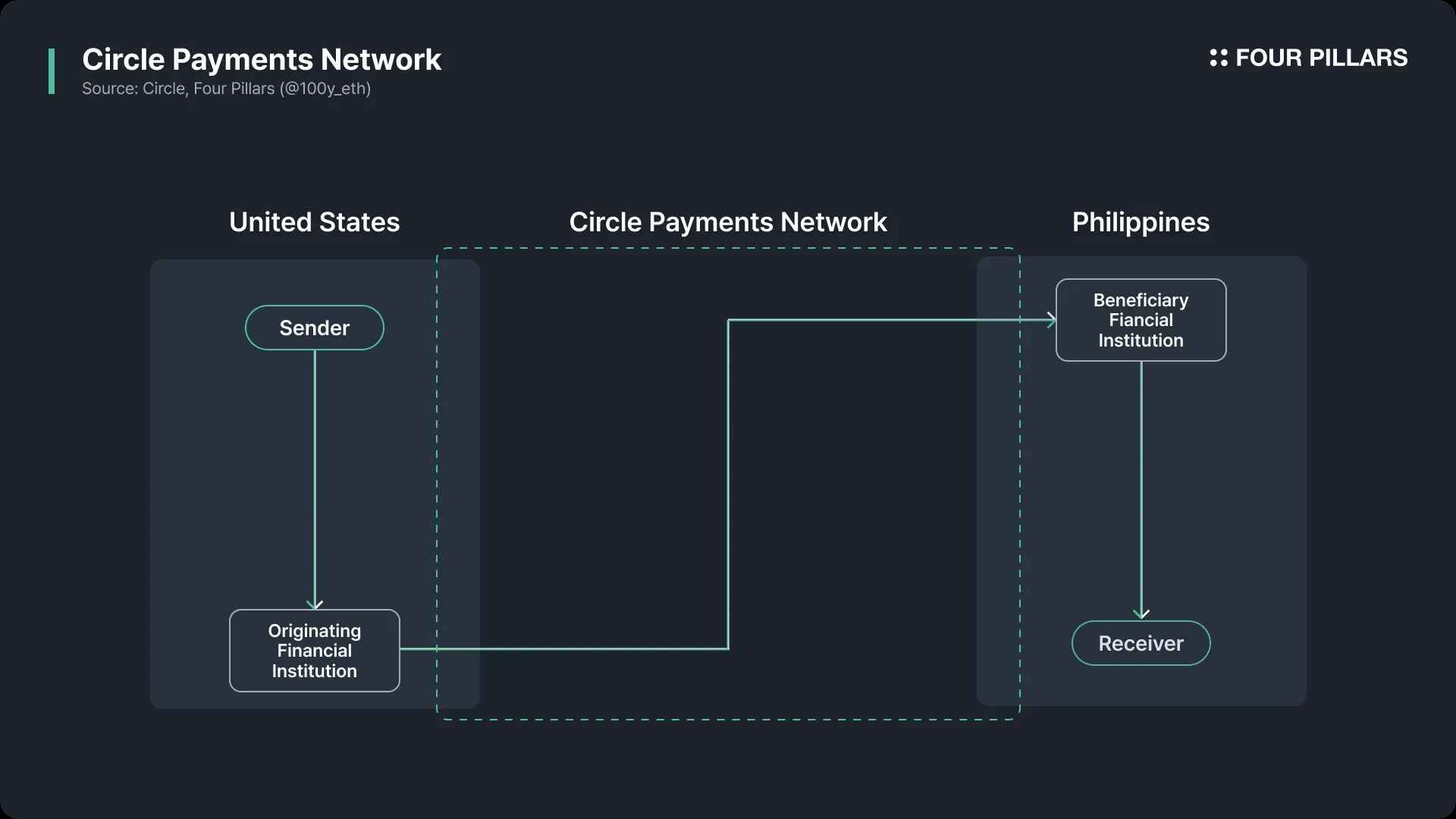

It’s important to note that CPN is not a new blockchain network. Instead, it uses compliant stablecoins like USDC and EURC alongside public blockchains as infrastructure. Also, like SWIFT, CPN does not move funds directly. Rather, it acts as a marketplace for financial institutions. In essence, CPN is a coordination protocol for global capital movement.

Unlike SWIFT, cross-border transactions through CPN involve just two parties—an OFI (Originating Financial Institution) and a BFI (Beneficiary Financial Institution). Since funds are transferred via stablecoins and public blockchains, the process is significantly faster and more cost-efficient.

There are four main types of participants in the Circle Payments Network (CPN):

2.2.1 Governing Body

Circle serves as the primary governing body of CPN and is responsible for the following:

Establishing and maintaining rules: Defines the “CPN Rules,” which govern participant eligibility, operations, and compliance.

Core infrastructure development: Builds and maintains the smart contracts, APIs, SDKs, and other technical components.

Third-party module onboarding: Approves and integrates vetted third-party services and applications into the CPN ecosystem.

Network security: Ensures system reliability and handles incident response and platform security.

Compliance supervision: Verifies that participating institutions comply with AML/CFT and sanctions regulations.

Participant qualification: Reviews and approves financial institutions for network participation.

Travel rule data sharing: Facilitates travel rule compliance through standardized, secure data exchange systems.

Orchestration: Operates the coordination protocol that handles price discovery, routing, and settlement between participants.

2.2.2 Participating Financial Institutions (PFIs)

These institutions process global payments on behalf of users while complying with both CPN Rules and regulatory requirements. PFIs include Virtual Asset Service Providers (VASPs), Payment Service Providers (PSPs), and both traditional and digital banks. PFIs can act as either:

OFIs (Originating Financial Institutions): institutions initiating the transfer

BFIs (Beneficiary Financial Institutions): institutions receiving the transfer

2.2.3 End Users

End users do not interact with CPN directly. Instead, they access international remittance services through financial institutions connected to CPN (i.e., OFIs or BFIs). In most cases, users may not even realize their transfers are being routed through CPN—yet they benefit from faster and cheaper remittances.

2.2.4 Service Providers

These entities provide technical and financial services to CPN. Their roles include foreign exchange, market making, stablecoin issuance, risk management, wallet infrastructure, custody, and compliance monitoring.

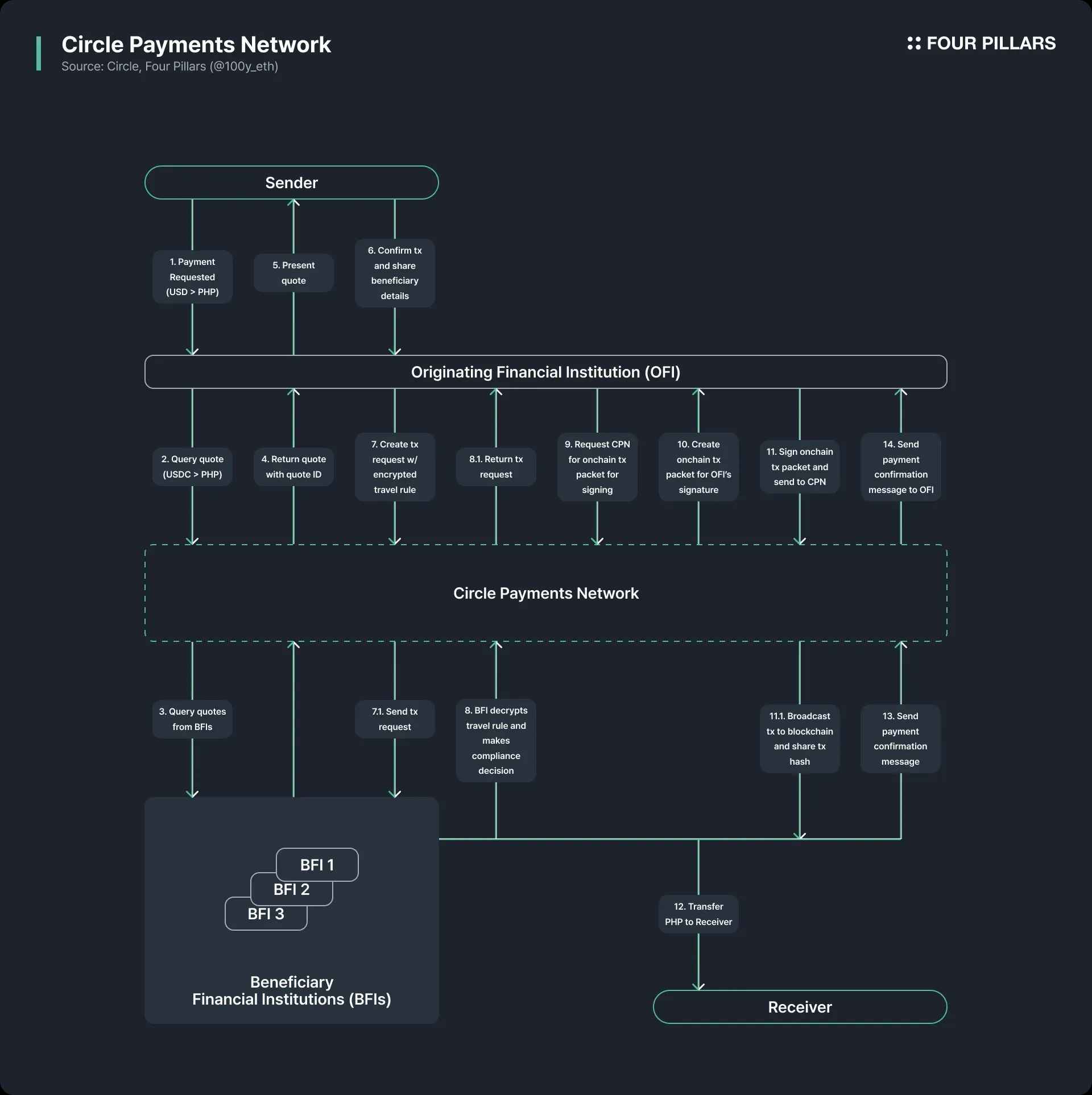

Here’s how a transaction flows through CPN:

The sender requests a remittance from an OFI to send USD to the Philippines in PHP.

The OFI requests a quote from CPN that includes the estimated exchange rate and fees.

CPN queries BFIs for quotes.

CPN returns quotes from the BFIs along with a quote ID to the OFI.

The OFI presents the quote to the sender.

The sender confirms the transaction and provides the recipient’s information to the OFI.

The OFI initiates a transaction request to CPN including recipient details, quote ID, and encrypted travel rule data. This is forwarded to the BFI.

The BFI decrypts the travel rule data, evaluates the request for compliance, and sends back an approval or rejection to the OFI.

The OFI requests an on-chain transaction packet from CPN.

CPN generates the on-chain transaction packet.

The OFI signs the transaction and submits it to CPN, which then broadcasts it to the blockchain.

Once the BFI receives the USDC on-chain, it delivers PHP to the recipient.

The BFI confirms settlement to CPN.

CPN notifies the OFI that the transaction is complete.

Since CPN uses public blockchains for settlement, it is globally accessible and operates 24/7. Beyond just settlement, CPN aims to optimize compliance data sharing and payment routing. For instance, it can automatically identify the BFI offering the lowest fees. Looking ahead, developers will be able to build modules and applications on top of CPN.

Initially, CPN uses a hybrid architecture involving both off-chain and on-chain components. Off-chain, the OFI submits and signs transaction requests via API, and Circle then broadcasts the request on-chain. On-chain, the funds are transferred and settled. In the long term, CPN plans to transition from off-chain APIs to fully on-chain smart contracts, which will improve accuracy, automation, and security.

Source: Circle

Based on everything we've seen, CPN can be understood as a financial network where institutions settle payments using stablecoins like USDC and EURC on public blockchains, enabling international transfers and payments to be processed quickly and cheaply. If such a system sees widespread adoption, anyone will be able to send money and make payments across borders instantly and affordably. This would fundamentally transform the global payments and remittance market.

For example, businesses engaged in international trade could make cross-border payments more efficiently and at lower costs, helping streamline global supply chains. With fewer payment delays, they would also avoid unnecessary interest expenses on bridge loans. For individual users, travel payments or peer-to-peer transfers on internet platforms would become significantly cheaper. For fintech developers, CPN would unlock the ability to build and offer services that were previously unfeasible.

Circle’s launch of CPN came shortly after the debut of Plasma, a blockchain optimized for USDT remittances. Built as a sidechain to the Bitcoin network, Plasma stands out by offering zero transaction fees for USDT transfers. It has also gained significant attention from the community and investors, particularly due to backing from Bitfinex, which shares a parent company with Tether.

To end users, USDC and USDT may seem nearly identical—but behind the scenes, the two operate with very different philosophies. USDC strictly adheres to U.S. regulatory frameworks, while USDT has grown its influence in regulatory gray zones. This difference is reflected in how they manage their treasuries: USDC operates conservatively, while USDT takes a more aggressive approach, generating significantly higher revenues.

Although CPN and Plasma share a common goal of transforming outdated global payment systems, their approaches diverge. USDT is building an entirely new blockchain optimized for stablecoin use, whereas USDC is leveraging existing public blockchain infrastructure and institutional networks.

With new stablecoin legislation like the GENIUS and STABLE Acts expected to pass in the U.S., the stablecoin market is entering a phase of rapid, unprecedented growth. All eyes will be on how these two giants—USDC and USDT—compete to build the future financial empire of the digital economy.

Related Articles, News, Tweets etc. :

Dive into 'Narratives' that will be important in the next year