We often take “money” for granted. Yet money has always been a product of political, technological, and institutional design. In the industrial era, money was issued by governments and central banks and distributed by commercial banks, forming a two-tier monetary structure. In other words, the monetary system was fundamentally built on a dual framework involving the state and financial institutions. However, this structure is beginning to fracture in the digital age.

Markus Brunnermeier, an economist at Princeton University, notes:

“The ongoing digital revolution may lead to a radical departure from the traditional model of monetary exchange. We may see an unbundling of the separate roles of money, creating fiercer competition among specialized currencies. On the other hand, digital currencies associated with large platform ecosystems may lead to a re-bundling of money in which payment services are packaged with an array of data services,...”[1]

In essence, Professor Brunnermeier argues that the architecture of monetary systems can no longer be completed solely by the state and banks. He anticipates an inevitable transition toward a tripartite structure involving governments, banks, and technology companies. This does not necessarily mean that tech companies will directly issue money, but it signals a fundamental shift in the structure of monetary systems.

First, the design and operation of monetary infrastructure are becoming increasingly diversified. What was once monopolized by the state and banks is now being partially taken over by private technology firms.

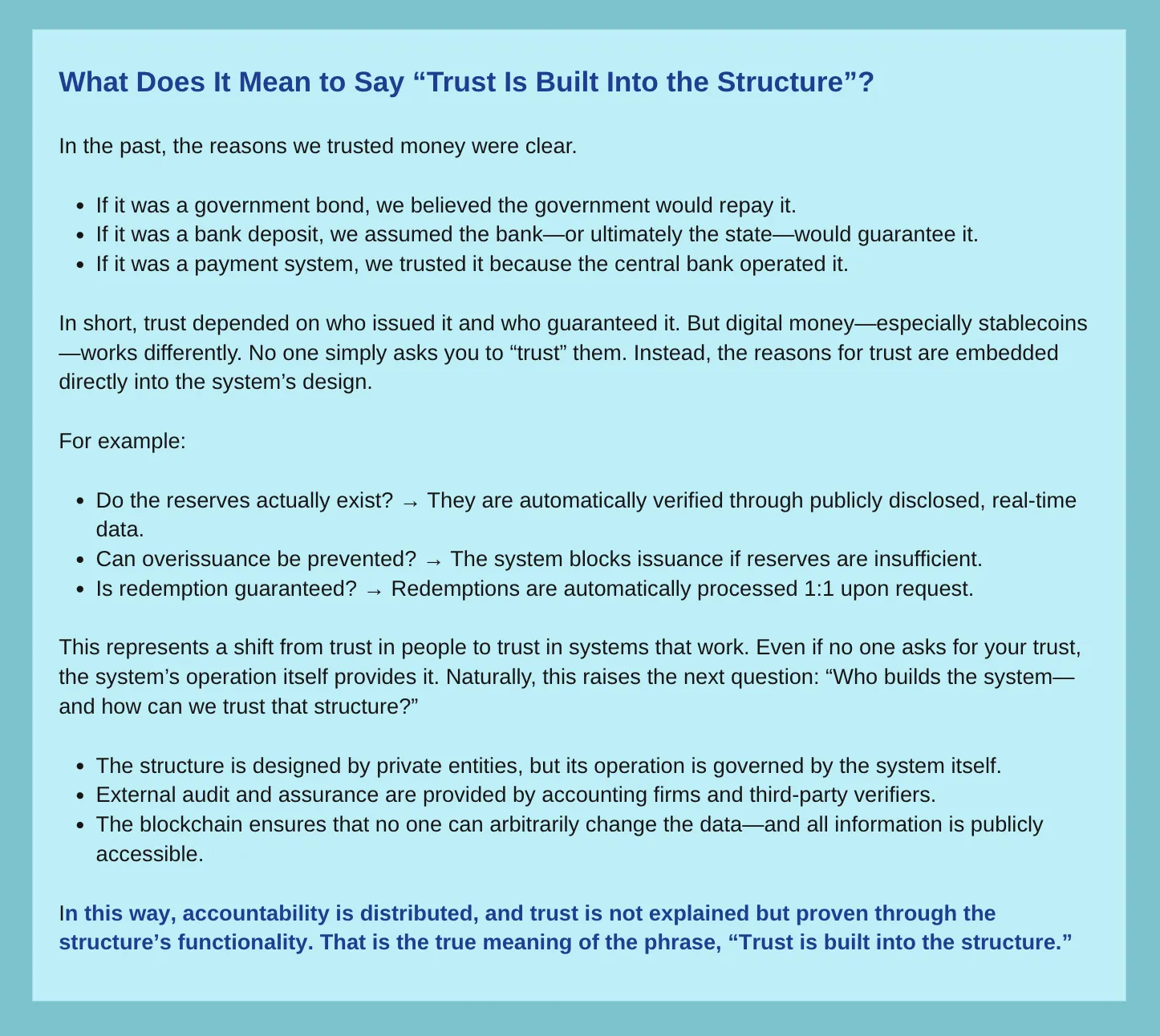

Second, the foundation of trust is shifting from institutions to structures. Trust, which used to rely on centralized institutions, is now being replaced by decentralized technical architectures and network-based systems. These new mechanisms are redefining how trust is formed and sustained.

In the past, trust was built on legal and institutional guarantees—central bank backing, banking licenses, deposit insurance. In today’s digital monetary landscape, however, trust is derived from the architecture itself: smart contracts, real-time reserve disclosures, on-chain audits, and automated redemption mechanisms. This shift is not a mere technical experiment; it reflects a deeper structural debate about what money is and how monetary infrastructure should be designed. At the center of this transformation is the stablecoin. A stablecoin is not simply another type of cryptocurrency. It represents a proposal—and an experiment—for how to design money and engineer trust in the digital era. Its reserve structure, issuance and redemption logic, code-based trust mechanisms, and decentralized operational models are all critical components of a new infrastructure for “digital money.”

This structure-based approach to trust is not just a technological or industrial initiative—it has attracted serious attention from academia and international policy bodies as a core component of future monetary systems. The traditional approach to trust, grounded in institutional authority, is increasingly giving way to trust rooted in technological and structural design.

Brunnermeier’s analysis illustrates this point. He emphasizes that in the digital era, the functions of money are becoming unbundled, and a tripartite structure—comprising states, banks, and tech companies—is emerging as the foundation of monetary order. Money can no longer be fully realized by the state and banks alone; various actors will assume independent roles in the monetary ecosystem[1].

Similarly, researchers at the Centre for Economic Policy Research (CEPR) have proposed the concept of Digital Currency Areas (DCAs) to describe the reorganization of monetary systems in digital ecosystems. This concept highlights a shift from traditional monetary areas—defined by legal tender and national borders—to platform-based ecosystems, where technology and economic activity are tightly integrated, giving rise to new forms of monetary sovereignty.[2]

The Bank for International Settlements (BIS) has analyzed how this structural transformation directly affects regulatory models. The BIS observes that the spread of stablecoins is facilitating a shift from external supervision to embedded supervision—a regulatory paradigm in which oversight is built directly into the technical architecture through blockchain and smart contracts, allowing for real-time, automated compliance.[3]

The National Institute of Standards and Technology (NIST) in the U.S. has also provided a systematic analysis of the technical trust architecture of stablecoins. NIST highlights how mechanisms such as real-time disclosures, automated auditing of reserves, and smart contract-based redemption systems can either replace or complement traditional banking functions. These mechanisms demonstrate how trust can be engineered without the need for centralized institutional intervention.[4]

Collectively, these developments point to a fundamental transformation: the monetary order in the digital age can no longer be sustained by institutional authority alone. It is moving toward a new architecture in which trust is engineered through code and design. This transformation goes beyond technology; it reconfigures the political economy and challenges existing notions of monetary sovereignty.

Institution-Based Trust vs. Structure-Based Trust

Source: Hashed Open Research

In Korea, regulatory discussions on stablecoins have yet to be finalized, and no specific issuance model has been officially adopted. Nevertheless, there is a strong likelihood that the policy direction will lean toward a bank-based model. This tendency stems from both the nature of global reference models currently available and institutional inertia toward regulatory acceptability.

Two of the most prominent reference cases are the European Union’s MiCA (Markets in Crypto-Assets Regulation) framework and Japan’s stablecoin legislation. Both regulatory regimes permit stablecoin issuance and circulation under certain conditions, but they presuppose a model where issuance is handled either by banks, bank-equivalent institutions, or qualified private entities under strict requirements. In particular, Japan has allowed stablecoin issuance exclusively by banks since 2023, imposing strong regulatory constraints on the custody and management of reserve assets. While MiCA permits issuance by private sector entities, both the reserve requirements and the qualifications for issuers are structured to integrate with traditional financial infrastructure.

Korea is still in the process of drafting its Basic Act on Digital Assets and related legislation for stablecoins. In these early stages of policy formation, it is highly likely that Korean regulators will refer to these foreign precedents. In contrast, the United States has explored a private-issuer model, such as in the STABLE Act, but no federal-level framework has been enacted. Multiple models currently coexist in the U.S., contributing to regulatory ambiguity.

Although Korea has not formally adopted a bank-based model, it is structurally inclined in that direction due to several underlying conditions—namely, regulatory acceptability, alignment with the existing financial supervisory framework, and the perceived legitimacy of aligning with international legislative trends.

This tendency is shaped by several key factors:

First, the foundational premise of Korean policy design emphasizes regulatory integration and financial stability.

Second, a preference exists for models that can be governed within the existing financial supervisory system.

Third, the MiCA and Japanese models are seen as realistic and institutionally stable references for Korean policymakers.

In this sense, the bank-based model, while not yet officially adopted, effectively functions as the default path with the highest probability of being chosen.

However, as discussed in Section 1.1, the architecture of trust in the digital currency era is increasingly shifting toward functionally distributed and technically structured systems. This is not a hypothetical shift—it is already manifesting in the global convergence of technological and regulatory developments.

Ultimately, Korea now faces a critical policy choice:

Will it build a regulatory framework as an extension of existing institutional models, or will it seize this opportunity to redesign monetary infrastructure tailored to the digital environment from the ground up?

As discussed in Section 1.2, while Korea has not yet finalized a regulatory framework for stablecoins, the policy discourse is implicitly gravitating toward a bank-based model as the default assumption. This inclination reflects a pragmatic choice, drawing from precedent frameworks such as the EU’s MiCA (Markets in Crypto-Assets Regulation) and Japan’s stablecoin law. Both are meaningful references in that they offer regulatory clarity: Japan, in 2023, became the first country in the world to formally codify a legal framework for stablecoin issuance, while MiCA provides a unified regulatory regime applicable across the European Union.

What is particularly noteworthy, however, is that despite being regulatory front-runners, neither Europe nor Japan has witnessed significant growth in their domestic stablecoin ecosystems. In the EU, euro-pegged stablecoins remain marginal in global circulation, with weak usage foundations. In Japan, despite being the earliest to implement a legal framework, the number of issued stablecoins remains extremely limited, and their use in global exchanges or decentralized finance (DeFi) ecosystems is minimal.

This stagnation cannot be explained solely by market conservatism or the early stages of policy rollout. Rather, it suggests that structural constraints inherent in the regulatory design may be limiting adoption. Heavy reliance on banks for issuance, a regulatory focus on minimizing institutional risk, and a prioritization of stability over innovation appear to have collectively failed to attract active private sector participation.

1. Lack of Scalability: Bank-centric models tend to face difficulties in integrating with private-sector platforms, digital asset services, and global blockchain infrastructure. For example, decentralized finance (DeFi), Web3 wallets, and international payment applications are typically built on blockchain APIs and smart contract environments—areas where bank-based systems struggle to adapt flexibly.

2. Limitations on Reward Mechanisms: Bank deposit-based models typically operate under a non-interest-bearing reserve principle. Profits generated from reserve assets are mostly retained by the issuing banks. In contrast, private stablecoins like USDC and PYUSD can offer on-platform rewards or interest tied to collateral assets, providing a stronger incentive for users to adopt and hold them.

3. Distance from Technological Innovation: The core innovation of stablecoins lies in trust through code and programmable finance. While bank-based models may ensure security and accounting transparency, they are often poorly suited to implement technological trust mechanisms such as smart contract-based automatic redemptions, on-chain disclosures, or real-time reserve verification.

4. Lack of Global Interoperability and Competitiveness: The stablecoin market is currently dominated by USD-pegged private stablecoins such as USDT and USDC, which have captured the market by combining capital market structure with code-based trust models. By contrast, bank-centered and state-backed models struggle to incentivize private-sector participation and often lack compatibility with global digital asset ecosystems.

These observations from Europe and Japan offer critical lessons for any jurisdiction pursuing stablecoin regulation. Regulatory clarity and legal formalization are necessary conditions for industry development—but they are not sufficient on their own. Without alignment between legal frameworks and the technological evolution of the market, user behavior, and interoperability with global financial infrastructure, regulation may fail to function effectively in practice.

This suggests that Korea, in pursuing the institutionalization of stablecoins, cannot rely solely on a “regulation-first” approach. When designing the regulatory framework, it is essential to consider which structural model will serve as the reference point, and whether that structure can offer a practically viable environment for market participants. The objective of regulation must go beyond formal codification; it should aim to establish a framework that functions effectively within the broader context of technology, market dynamics, and global interoperability

As examined in the previous sections, while the bank-based model may offer intuitive advantages in terms of regulatory acceptability and supervisory alignment, it reveals structural limitations when it comes to scalability, interoperability, and the implementation of technological trust. This raises a key question: What alternative models can overcome these constraints?

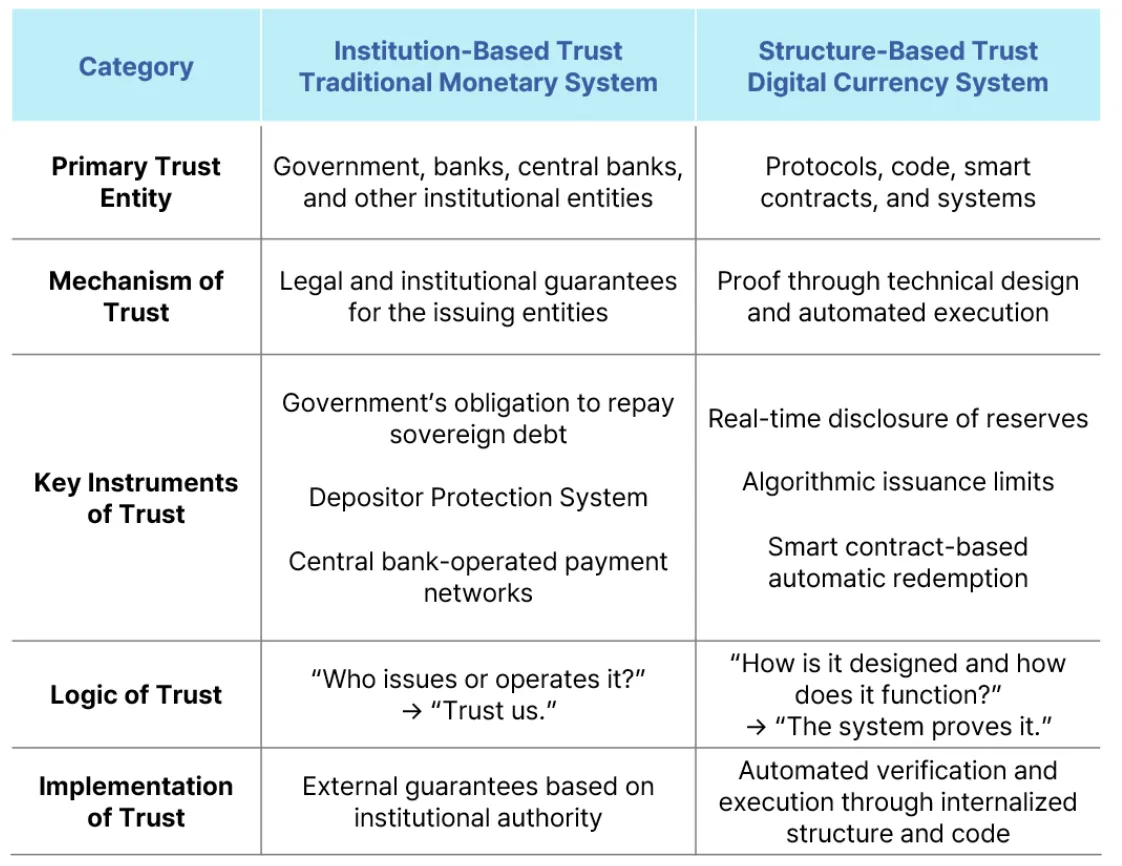

In practice, the stablecoin structures that have gained real traction in global markets are increasingly aligned with capital market-based models. In these models, issuance is led by private-sector entities—particularly asset managers and fintech firms. Reserve assets typically consist of money market funds (MMFs), government bonds, and reverse repurchase agreements (RRPs). Redemption mechanisms, audits, and disclosures are designed around smart contract-based automation and external third-party verification.

Structure of Circle (USDC)

Source: Hashed Open Research

Circle (USDC) Market Overview (as of 2024)

This architecture is not only thriving within the United States but is also widely utilized across global payment networks, decentralized finance (DeFi), NFTs, and Web3 services. It represents a compelling example of how trust can be structurally embedded and sustained without reliance on traditional banking infrastructure.

Among all stablecoin projects, Tether (USDT) stands out as the one that has dominated the market the longest. Launched in 2014, USDT has survived numerous controversies—including opaque reserve disclosures, lack of formal audits, disconnection from the banking system, and ongoing legal disputes—yet it continues to hold over 60% of the global stablecoin market.

Tether(USDT) Market Overview (as of 2024)

Source: Hashed Open Research

In its early stages, Tether relied on a mixed reserve structure, consisting of cash, commercial paper, and other short-term assets. Over time, however, it evolved toward a portfolio centered on U.S. Treasury securities, introduced third-party attestation reports, and adopted a multi-bank custody strategy to distribute risk across multiple institutions. In effect, it shifted closer to a capital market-based model.

What is noteworthy is that this transformation was not part of a strategic master plan but occurred “by necessity” - an adaptive response to being effectively cut off from the traditional banking system. Tether’s survival illustrates an important reality: it has proven, in practice, the viability of capital market-based structures in sustaining trust without institutional backing. It is, in essence, an experimental case study in structural resilience under adverse conditions.

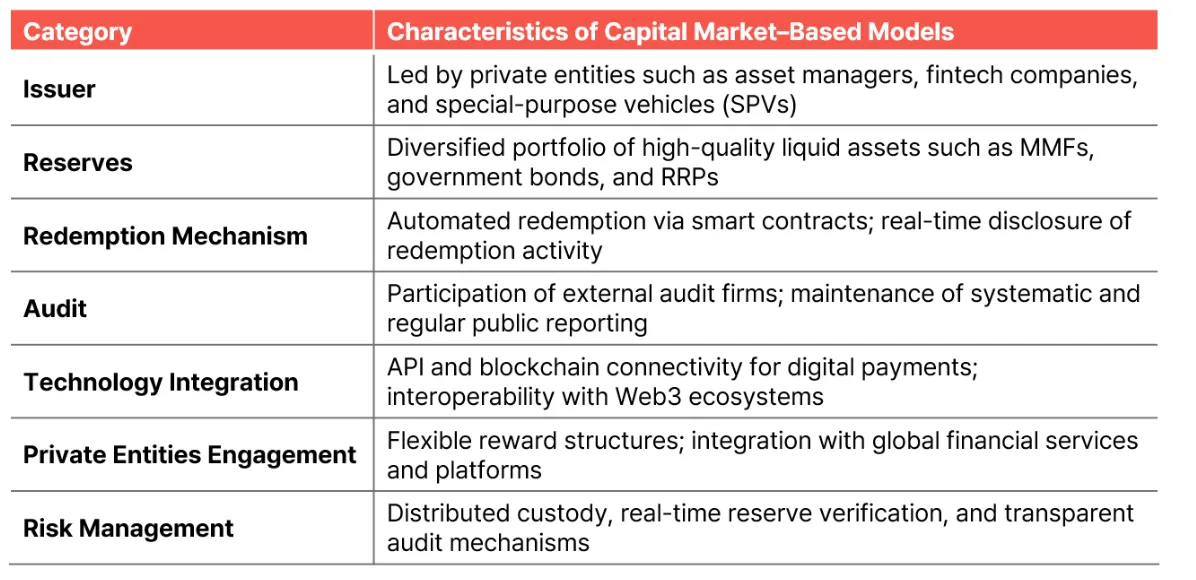

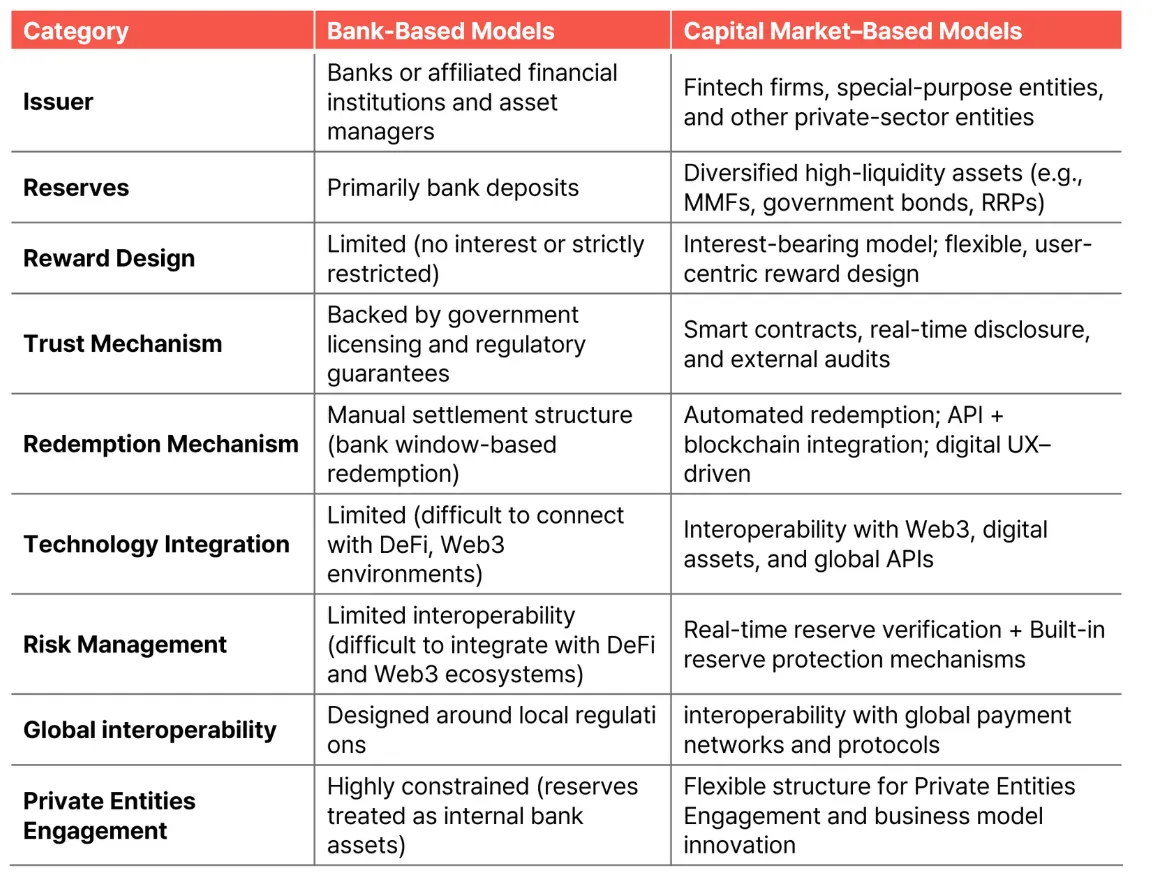

Characteristics of Capital Market–Based Models

Source: Hashed Open Research

Capital market-based models make stablecoins functionally viable by combining technology-driven trust with market flexibility.

In the previous sections, we examined how the bank-based model is increasingly misaligned with the technological trajectory and global architecture of the digital currency era, while the capital market-based model has demonstrated viability and growth in real-world markets. Now, it is time to systematically compare the structural differences between the two models across key dimensions such as policy design, technological implementation, and market interoperability.

The following comparison table provides a framework for policy evaluation, organized around the core architectural elements of each model.

Structural Comparison: Bank-Based Models vs. Capital Market–Based Models

Source: Hashed Open Research

The bank-based model prioritizes regulatory alignment and conservative financial stability. While this approach may be effective in the early stages of regulatory adoption and within traditional financial stability frameworks, it presents clear limitations in areas central to digital currencies: scalability, decentralization, transparency, flexible reward mechanisms, and global interoperability.

In contrast, the capital market-based model is already operational in real-world markets. Projects such as Circle, Tether, and TUSD have each demonstrated, in their own way, the viability of functional trust architectures. In nearly every dimension—technical implementation, market fit, private-sector incentives, and global integration—this model exhibits structural superiority.

Therefore, the guiding question for policy should shift from “Who is the issuer?” to “Which structure actually works?”

This comparison is not merely about stablecoins—it reflects a strategic choice for Korea:

Which structural model will position the country for international competitiveness in the emerging digital financial order?

Which system should serve as the foundation for future financial infrastructure design?

Despite Korea’s strong advantages in technological infrastructure, capital markets, digital asset demand, and global connectivity, discussions around stablecoin institutionalization remain in the early stages. Financial regulators have tended to prioritize risk containment, and the preference for bank-based models continues to reflect a kind of institutional inertia.

However, this is precisely the moment for Korea to move beyond regulatory acceptance and actively define the direction of its policy architecture. Choosing a capital market-based framework is not merely about permitting private-sector participation—it represents a strategic opportunity to enhance economic sovereignty and global competitiveness in the era of digital currency.

Korea already possesses globally competitive digital finance infrastructure. The country is home to a meaningful number of blockchain technology firms, digital asset exchanges, custody providers, and Web3-based startups. Additionally, a rapidly growing user base is emerging across sectors such as tokenization, NFTs, and real-world assets (RWAs).

In this context, adopting a capital market-based stablecoin framework could yield several benefits:

First, it would allow private-sector entities to participate as issuers, enhancing interoperability with global stablecoin networks.

Second, it could catalyze the development of a broader digital finance ecosystem by linking issuance to industries such as custody, external auditing, and reserve asset management.

For example, one could envision a “Korean model” scenario:

Private financial institutions or fintech companies could serve as issuers, subject to registration and disclosure requirements. Reserve assets would follow a diversified structure, including money market funds (MMFs), government bonds, and cash-equivalent instruments, underpinned by an external oversight framework.

Audits would be conducted periodically by designated third-party firms, with results disclosed transparently to the public. Redemption would be enabled through a combination of API-based automated clearing systems and smart contract-driven buyback mechanisms, creating a technological trust architecture embedded in the system design.

Korea’s financial markets are already experiencing a widespread influx of dollar-denominated private stablecoins, and in global exchanges and DeFi environments, assets are routinely managed using foreign currency-pegged stablecoins such as USDT and USDC. This reality suggests that, if Korea delays the development of its own regulatory framework, the domestic market may ultimately be shaped by a stablecoin order led by other jurisdictions.

A capital market-based framework offers the most flexible path for aligning with the evolving global financial structure. It enables Korea to establish mutual verification systems with major global issuers such as Circle, Paxos, MakerDAO, and PayPal, and to adopt on-chain reserve verification mechanisms, integration with global payment networks, and other interoperability features. These capabilities would allow Korean services to maintain genuine international competitiveness.

In this context, the capital market-based structure should not be viewed merely as one policy option among many. Rather, it represents what is effectively the only viable choice if Korea seeks to ensure compatibility with the global stablecoin infrastructure.

The question facing Korea is not simply whether to permit stablecoins. At a more fundamental level, we are confronted with a set of structural questions:

First, how should trust in monetary infrastructure be designed in the digital era?

Second, who holds sovereignty over money and payments—and through what structures should that authority now be shared or distributed?

Third, what principles and mechanisms will enable Korea to position itself at the center of the emerging global digital currency order?

To respond to these questions, this report began in Chapter 1 with a conceptual reframing around the architecture of trust, and in Chapters 2 through 4, provided comparative and empirical analyses of global regulatory directions and structural models. Chapter 5 presented a concrete proposal for why a capital market-based stablecoin framework is strategically significant for Korea and outlined a viable path for its implementation.

In doing so, this report goes beyond regulatory evaluation—it calls for a paradigm shift in policy thinking, toward the design of a new monetary order.

Although Korea’s legislative timeline for stablecoins trails that of the European Union (MiCA) and Japan, this may in fact serve as a strategic advantage in regulatory design. The early adopters largely pursued bank-centric trust frameworks, yet these models have fallen short in delivering real market adoption.

By thoroughly analyzing these early missteps and structural limitations, Korea is uniquely positioned to leverage a second-mover advantage—not by replicating existing models, but by building something better.

In the digital era, trust is no longer guaranteed by licenses or administrative approvals alone. It must be designed, implemented in code, and verified through system architecture. We are now entering an era in which trust is built on technology and structure.

Korea now stands at a crossroads—not as a passive regulatory adopter, but with the opportunity to become an active architect of the digital currency order. The country already possesses the technological capacity and private-sector engagement needed to support such a role. What remains is the assertion of directional leadership in regulatory design and structural architecture.

The foundation of that leadership lies in the design of a trust framework rooted in capital market principles. This model represents the only structural solution capable of simultaneously meeting the demands of domestic financial scalability and global system compatibility. Today’s policy choice, therefore, is not simply about regulation—it is a strategic decision on whether Korea will merely accommodate the new monetary order, or actively shape and lead it.

All of these discussions rest on a single premise:

“Trust can be designed. And that structure—we can build it now.”

[1] Brunnermeier, M. K., James, H., & Landau, J. P. (2019). The Digitalization of Money. NBER Working Paper No. 26300. National Bureau of Economic Research.

[2] Eichengreen, B., et al. (2019). Digital Currency Areas. CEPR Discussion Paper No. DP14065. Centre for Economic Policy Research (CEPR).

[3] Auer, R. (2019). Embedded Supervision: How to Build Regulation into a Blockchain. BIS Working Papers No. 811. Bank for International Settlements.

[4] NIST (2023). Stablecoin Systems and Trust Architecture: An Overview. U.S. National Institute of Standards and Technology, Technical Note.

Dive into 'Narratives' that will be important in the next year