Rapidly Expanding Use Cases of Stablecoins

Source: Big Ideas 2025, ARK Invest, Feb 4, 2025

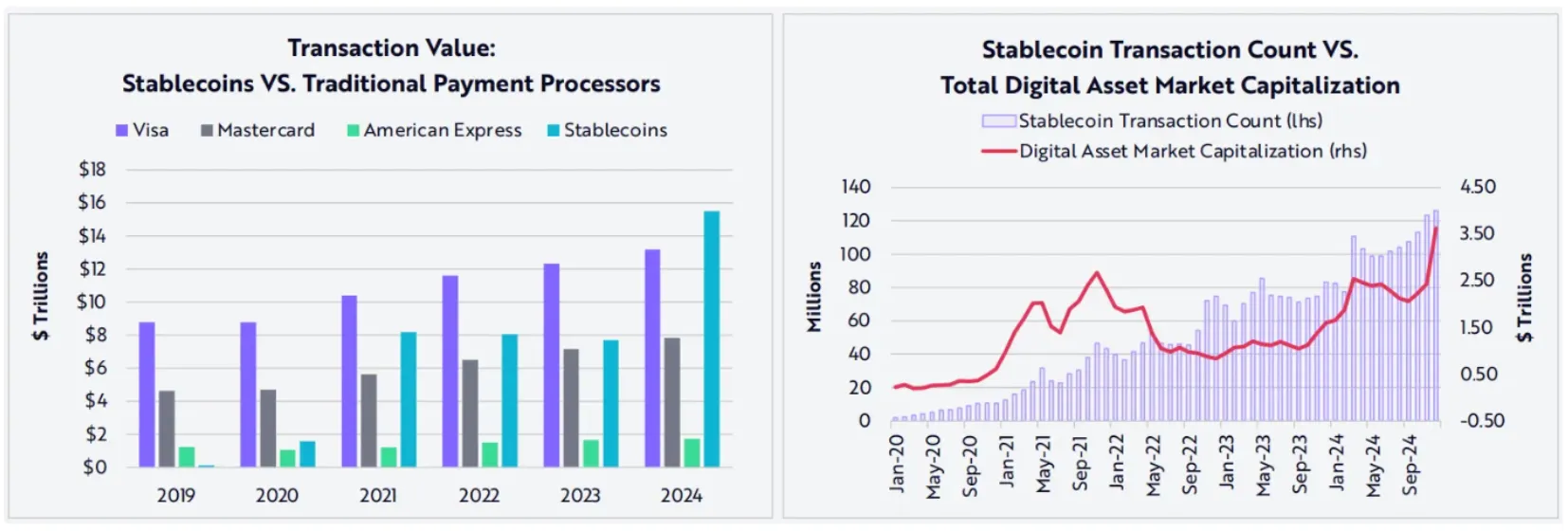

Stablecoins are an unstoppable trend. According to data from ARK Invest, the transaction volume of stablecoins reached $15.6T in 2024, which corresponds to 119% and 200% of Visa’s and Mastercard’s transaction volumes, respectively. Despite the crypto market downturn in 2023–2024, the number of stablecoin transactions continued to grow steadily. The fact that stablecoins surpassed the processing volume of traditional payment systems in 2024 is a highly encouraging development.

Stablecoin Market Share

Source: Artemis Terminal

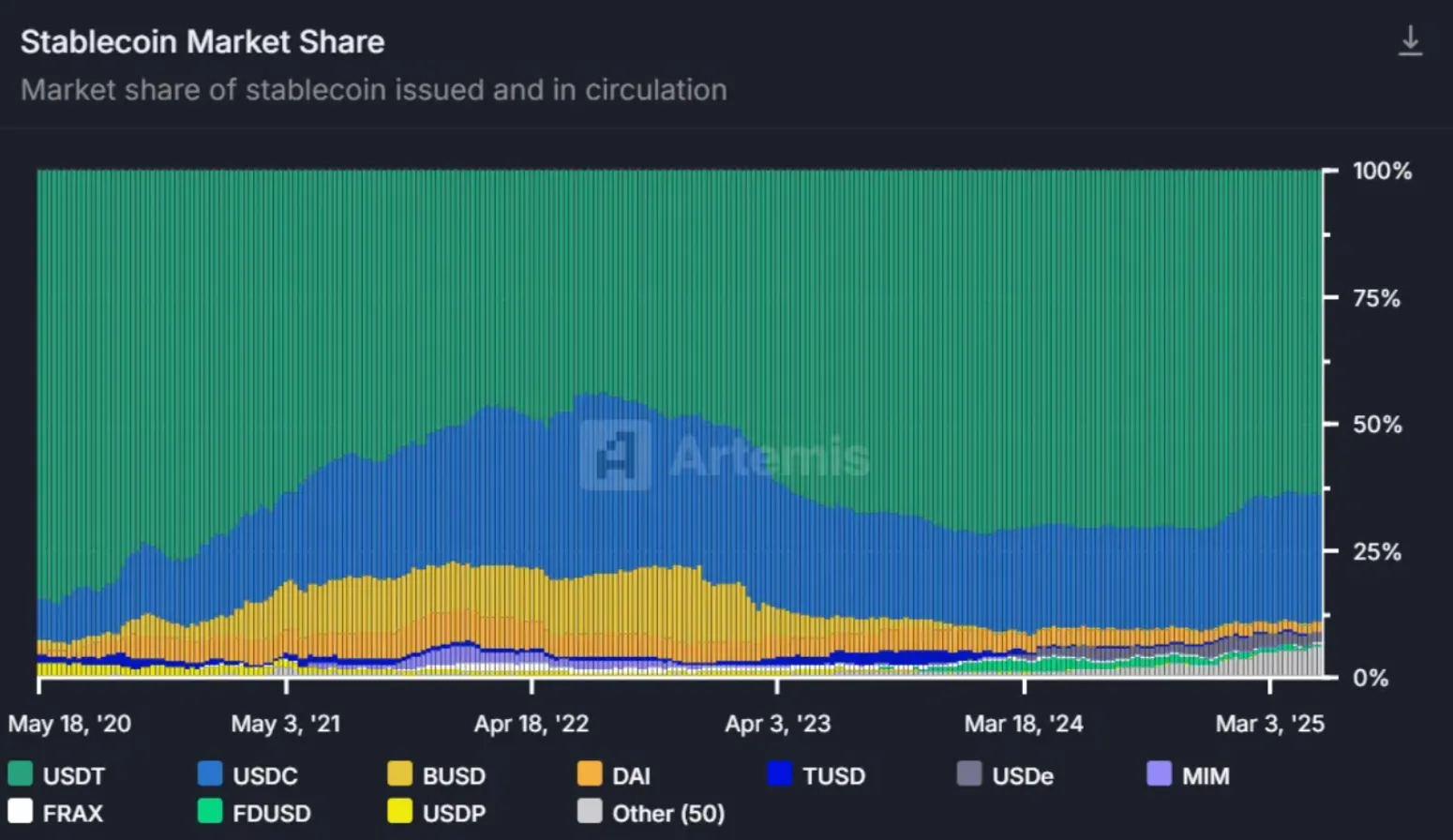

In this era of rapid change, while it is critically important to design and issue stablecoins in compliance with regulation, it is equally important to consider how to make stablecoins truly useful. The stablecoin market is growing at a fast pace, but the majority of current stablecoin supply is still dominated by Tether’s USDT and Circle’s USDC, which together account for nearly 90% of market share.

Beyond USDT and USDC, a variety of fiat-backed stablecoins exist in the market. However, compared to the market capitalizations of USDT ($150B) and USDC ($60B), most other stablecoins have seen very limited adoption. This implies that beyond issuance, ensuring real-world utility and driving user adoption are essential for stablecoin success.

FDUSD (~$1.5B): A USD-backed stablecoin issued by First Digital Labs, a subsidiary of First Digital Group based in Hong Kong. While it currently does not fall under a defined regulatory regime, it is being prepared to comply with Hong Kong’s upcoming regulatory framework.

PYUSD (~$900M): A USD-backed stablecoin issued by PayPal in collaboration with Paxos, under the regulatory oversight of the New York Department of Financial Services (NYDFS).

TUSD (~$500M): Initially issued by TrueCoin LLC under the supervision of Nevada’s Financial Institutions Division (FID), TUSD is now managed by Techteryx, a Singapore-based company registered in the British Virgin Islands, and currently operates without clear regulatory supervision.

RLUSD (~$300M): A USD-backed stablecoin issued by a subsidiary of Ripple, also under the regulatory oversight of NYDFS.

USDG (~$270M): A USD-backed stablecoin issued by Paxos Digital Singapore, regulated by the Monetary Authority of Singapore (MAS).

EURC (~$230M): A euro-backed stablecoin issued by Circle, which complies with the European Union’s MiCA regulatory framework.

USDP (~$70M): A USD-backed stablecoin issued by Paxos, also regulated by NYDFS.

For example, both USDP and PYUSD are issued by Paxos, but PYUSD benefits from PayPal’s branding and distribution. As a result, PayPal’s large user base has easy access to PYUSD for payments and transfers, leading to a significantly larger market capitalization for PYUSD compared to USDP.

In the case of FDUSD, the stablecoin experienced rapid user and liquidity growth after being listed by Binance—one of the world’s largest exchanges—in July 2023. Notably, Binance included FDUSD in its Launchpool platform (where users lock up crypto to receive new project tokens as rewards). This incentivized a large number of users to trade FDUSD in order to earn rewards from newly launched projects, which in turn helped FDUSD achieve its current large market capitalization.

Global Dollar(USDG) Network

Source: Global Dollar Network

There are also cases where incentive structures have accelerated stablecoin adoption. USDG is a prime example, having expanded its use cases by offering incentives to services in multiple countries through the Global Dollar Network. Issued in Singapore and regulated by the Monetary Authority of Singapore (MAS), USDG has quickly grown into one of the leading stablecoins, with a market capitalization of approximately $270 million.

Conversely, some stablecoins have seen sluggish adoption due to a lack of real-world utility. EURCV, a euro-backed stablecoin issued by SG Forge—the digital asset division of France’s major bank Société Générale—in compliance with MiCA regulations, was launched in April 2023. However, due to limited exchange listings and a narrow focus on institutional use, its market capitalization remains at around $46 million. Similarly, Japan’s JPYC stablecoin has a market cap of only about $15 million, primarily due to limited use cases.

In other words, no matter how well governments and public institutions establish regulatory frameworks, and no matter how strictly issuers comply with them, the most crucial factor for stablecoin success is securing strong and practical avenues for real-world adoption. In this context, the following section will explore how stablecoins are actually being used—focusing on four categories: (1) payments, (2) remittances, (3) interbank settlement, and (4) exchanges. It will also examine which industries stand to benefit as stablecoin adoption continues to grow across these domains.

Stablecoin Adoption in Real-World Use Cases

Source: Four Pillars

In April 2025, Visa and Mastercard each announced new initiatives just two days apart, both positioning stablecoins as the core of next-generation payment systems and outlining plans to actively expand their businesses in this area. Was it merely a coincidence? Both companies highlighted four initiatives: 1) stablecoin-based settlement infrastructure, 2) global remittances, 3) enterprise tokenization platforms, and 4) payment cards integrated with stablecoins.

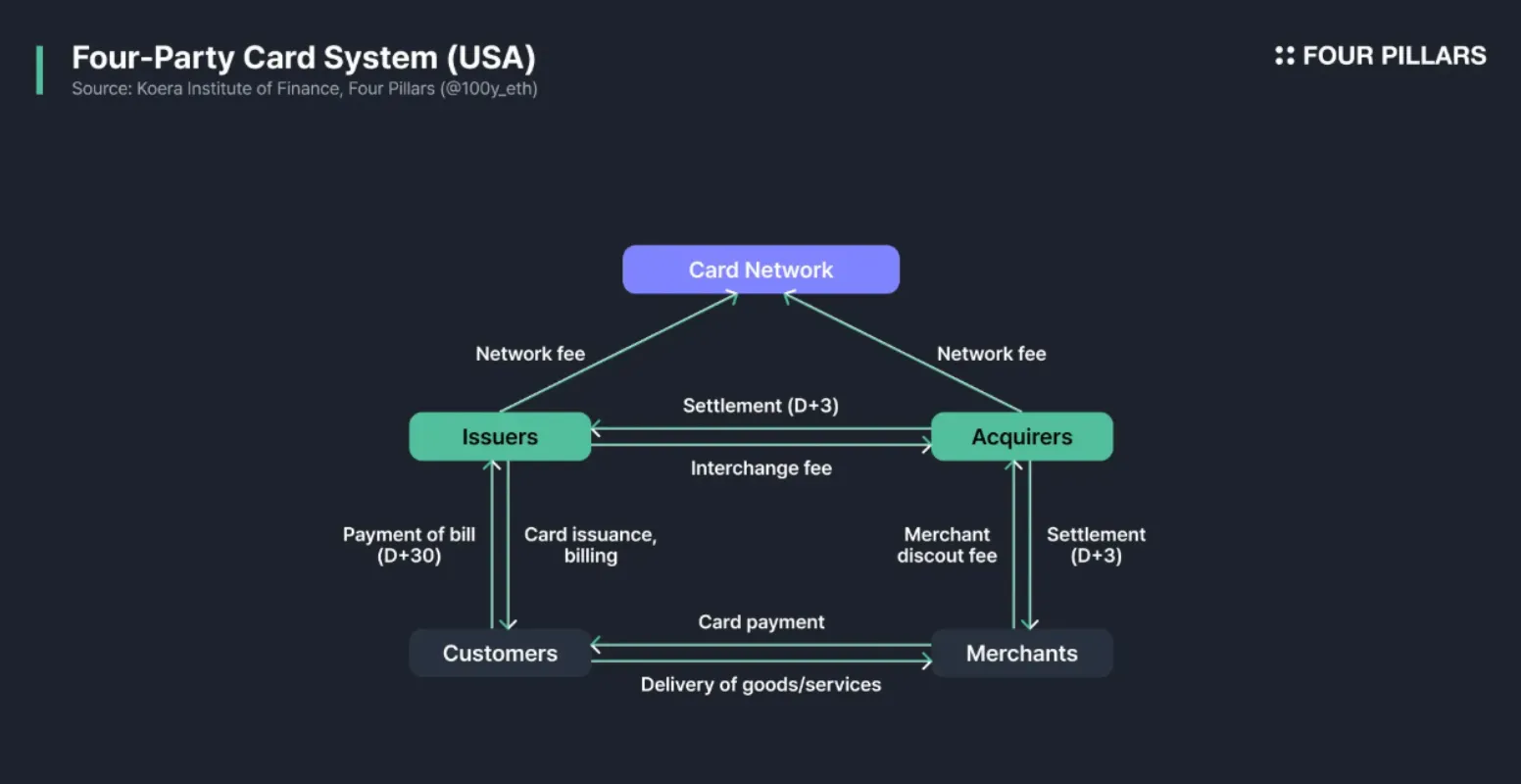

As such, stablecoins and blockchain have emerged today as key concepts in the transformation of existing payment systems. Of course, thanks to decades of effort by various fintech companies, the front end of payments has already become highly digitized, enabling users and merchants to use payment systems with ease. Nevertheless, the actual movement and settlement of funds still remain outdated. Let us first take a look at the four-party model, which is the most commonly used structure in credit card payments.

Four-Party Card System (USA)

Source: Four Pillars

The four-party model involves the card issuer, acquirer, merchant, and consumer (cardholder). Card networks such as Visa and Mastercard provide the payment network but do not issue cards or extend credit themselves. The basic process of the four-party model is as follows:

Payment Request (D+0): When the cardholder makes a purchase at a merchant using their card, a payment request is initiated. The payment information is transmitted in the order of merchant → acquirer → card network → issuer.

Authorization (D+0): The issuer checks the cardholder’s credit limit, validity, and potential fraudulent activity, then decides whether to approve the transaction. The approval is relayed back in reverse order to the merchant, completing the card payment.

Settlement (D+3): The issuer pays the acquirer after deducting an interchange fee. The acquirer then pays the merchant after deducting a merchant discount rate (MDR). The card network receives a network fee from both the issuer and acquirer for each transaction.

Billing and Repayment (D+30): The cardholder receives a bill from the issuer the following month and makes the payment for the amount due.

There are several problems with this traditional payment system. The first is high fees. The payment process involves multiple intermediaries, all of whom collect service fees from the merchant. Out of the total payment made by the customer, approximately 0.5–2% goes to the issuer, 0.1–0.3% to the card network, and 0.2–0.5% to the acquirer. This can be a significant burden for merchants operating on thin margins.

Stablecoin Payment Systems vs. Traditional Payment Systems

Source: a16z

Another issue arising from the numerous intermediaries in traditional payment systems is the slow settlement time. While some large merchants or those with special agreements with card issuers may be eligible for D+1 settlement—receiving funds the day after the transaction—most merchants typically receive settlement 2 to 5 days after providing goods or services to the customer. The longer the settlement period, the greater the burden on the merchant’s cash flow. For this reason, some merchants opt to pay additional fees to use D+1 settlement services for faster access to funds.

Blockchain-based stablecoin payment systems can address both the high fee structures and delayed settlements of traditional systems. As we will see in the examples of PayPal and Stripe below, if payments are processed via blockchain-based stablecoins, acquirers can complete the transactions without relying on intermediary banks or card networks. This simplifies the fee structure, shortens the settlement cycle, and enables merchants to improve profitability and secure better cash flow.

Let us now examine several real-world examples of how stablecoins are being integrated into payment systems.

2.2.1 Visa

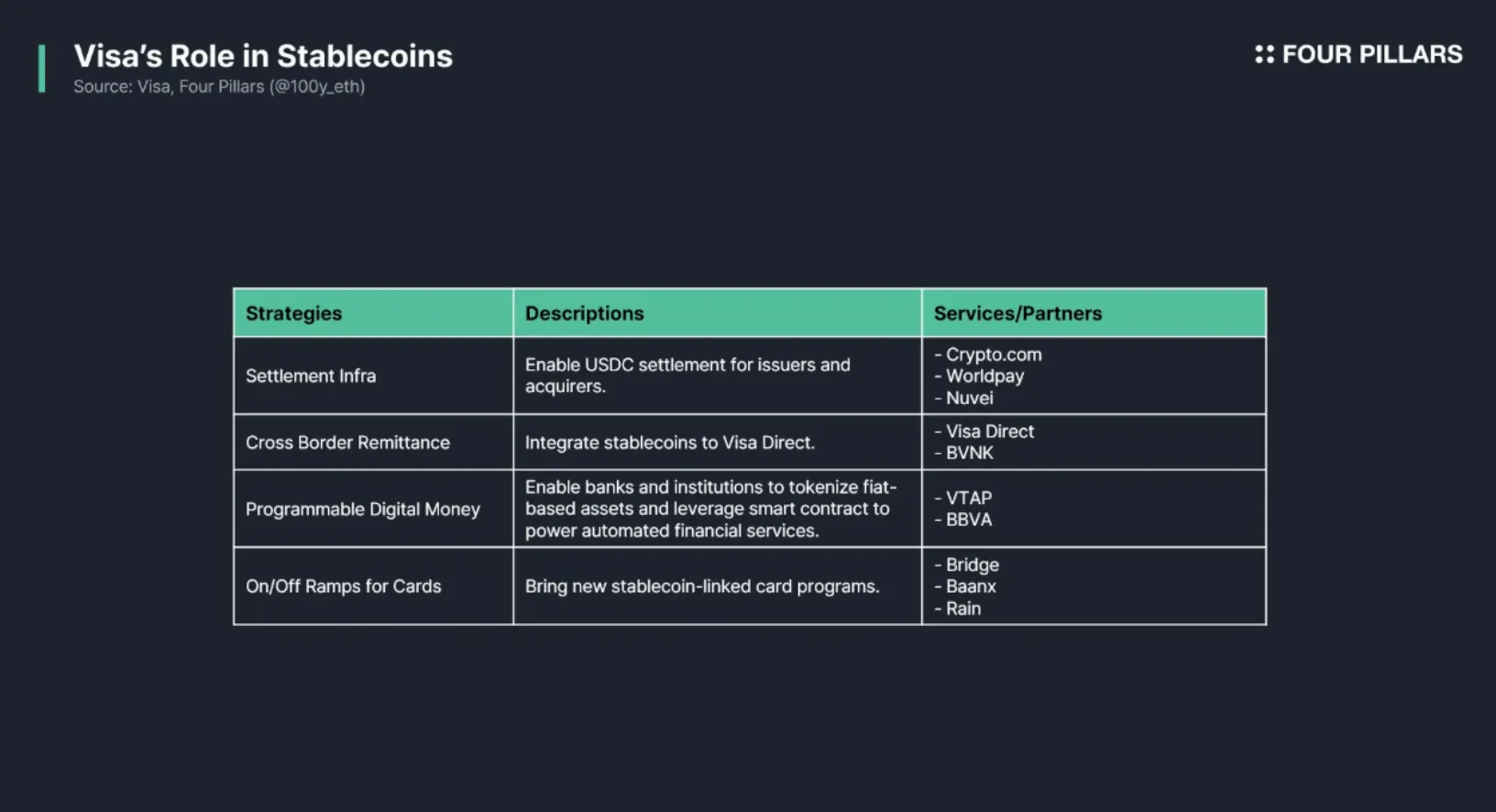

Visa, through its global payment network VisaNet—one of the largest in the world—can process up to 65,000 transactions per second and supports payments at over 150 million merchants in more than 200 countries worldwide. Visa views stablecoins as a core component of future digital payment systems and, in April 2025, announced four specific strategic initiatives for integrating stablecoins into its existing network ("Visa’s Role in Stablecoins," Apr 30, 2025, Visa Perspectives).

Visa’s Role in Stablecoins

Source: Four Pillars

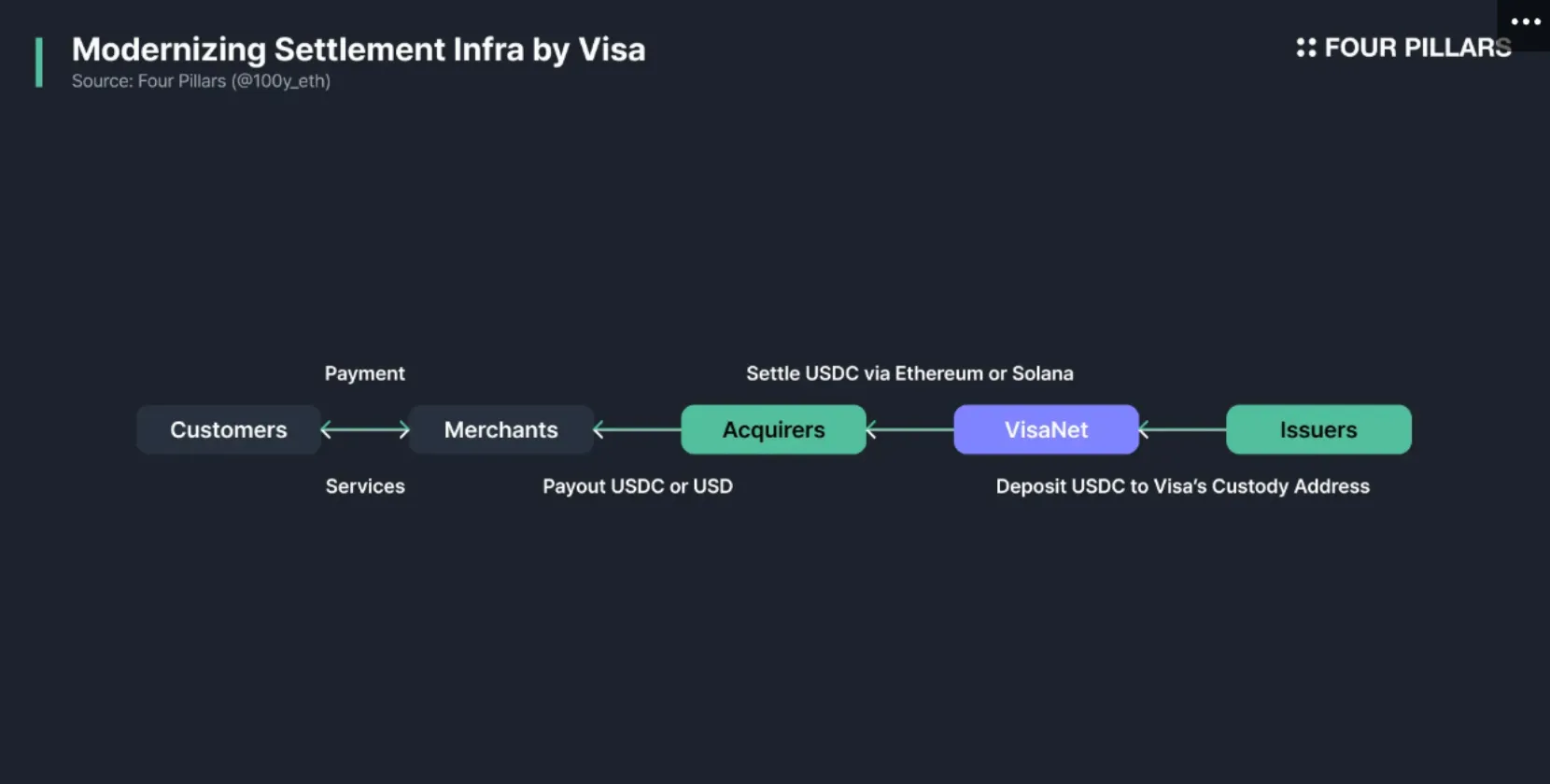

The first initiative is the modernization of its settlement infrastructure. Since 2021, Visa has been running a pilot to settle transactions using USDC on VisaNet and has settled more than $225 million to date. Traditionally, card issuers had to remit settlement funds to Visa in U.S. dollars. Now, however, they can send funds not only in dollars but also directly in USDC ("Digital Currency Comes to Visa’s Settlement Platform," Mar 29, 2021).

For example, Crypto.com issues Crypto.com Visa cards that allow customers to pay directly from their crypto accounts. Previously, crypto-native companies like this had to convert their digital assets to fiat currencies such as USD to process payments, which incurred time and costs. But with Visa’s new system, they can now use USDC for direct settlement. In collaboration with Anchorage, Visa created secure custody accounts for holding stablecoins. Card issuers like Crypto.com can send USDC to these accounts over the Ethereum network to complete settlements.

By adopting the USDC settlement system, Crypto.com reduced the average pre-funding time from 8 days to 4 and lowered FX fees to 20–30 basis points ("By Settling in USDC, Crypto.com Is Setting a New Course," 2023). Visa has enabled not only issuers but also acquirers to settle in USDC. In September 2023, Visa built settlement infrastructure for acquirers Worldpay and Nuvei to accept USDC over Ethereum and Solana. These acquirers can then either pass the USDC directly to merchants or convert it to fiat as needed.

Modernizing Settlement Infra by Visa

Source: Four Pillars

In summary, Visa has successfully established a pipeline that allows settlement between card issuers and acquirers through the Visa network using USDC instead of dollars. Looking ahead, Visa plans to expand its stablecoin settlement system to more partners and regions, introduce 24/7 real-time settlement, and support a broader range of blockchains and stablecoins.

The second initiative is strengthening global remittance infrastructure. Visa already supports large-scale cross-border payments through the VisaNet infrastructure. One of its services, Visa Direct, allows users to send funds peer-to-peer to cards, wallets, and bank accounts via VisaNet. Visa plans to enhance the efficiency of global remittances by adding stablecoin support to Visa Direct. Additionally, Visa recently invested in BVNK, a startup building enterprise-grade stablecoin infrastructure ("Visa Doubles Down on Stablecoins With Investment in Blockchain Payments Firm BVNK," May 7, 2025, CoinDesk), aiming to strengthen its stablecoin capabilities not only in retail but also across the enterprise ecosystem.

The third initiative is the implementation of programmable digital money. One of the major advantages stablecoins have over traditional cash is the ability to leverage blockchain-based smart contracts. Visa sees significant potential in smart contract-enabled automated financial services and, in October 2024, launched the "Visa Tokenized Asset Platform (VTAP)" to lead this innovation.

VTAP is a blockchain-based financial infrastructure that enables banks and financial institutions to issue and manage fiat-backed digital tokens (e.g., stablecoins, tokenized deposits). These capabilities are provided via Visa’s APIs, making it easy to integrate with existing financial systems. Tokens issued through VTAP can also leverage smart contracts, allowing complex processes such as conditional payments and customer lending to be automated and handled efficiently.

VTAP has not yet been rolled out publicly and is currently operating in a sandbox environment. Initially, Visa partnered with Spanish bank BBVA to test features such as token issuance, transfer, and redemption. According to the roadmap, a pilot program targeting real customers on the Ethereum public blockchain is planned for launch starting in 2025.

The fourth initiative is the development of stablecoin on/off-ramp cards. Visa’s stablecoin-linked cards allow issuers to provide on/off-ramp services. To date, Visa has facilitated over $100 billion in crypto purchases and $25 billion in crypto spending through its card network. To expand this ecosystem, Visa is collaborating with stablecoin card infrastructure companies such as Bridge, Baanx, and Rain.

Bridge is a stablecoin infrastructure platform acquired by Stripe, and it recently partnered with Visa to launch a card issuance solution that enables real-world payments using stablecoins. Fintech companies can use Bridge’s simple API solutions to offer stablecoin-linked card services to their customers. Cardholders can make purchases using their stablecoin balances, and Bridge converts the stablecoin into cash and settles the payment with the merchant. Initially, the service is available in Argentina, Colombia, Ecuador, Mexico, Peru, and Chile, with plans to gradually expand to Europe, Africa, and Asia.

Baanx is a London-based fintech company founded in 2018 that provides a range of crypto services connecting traditional finance and digital assets. In April 2025, Baanx announced a partnership with Visa to launch a stablecoin payment card that allows users to pay with USDC directly from their self-custody crypto wallets. At the time of payment, USDC is sent to Baanx in real time via smart contract, and Baanx converts it into fiat to settle with the merchant.

Rain is a New York-based fintech company founded in 2021 that operates a global card issuance platform using stablecoins. Rain also provides APIs to easily issue Visa cards linked to stablecoins and offers a wide range of financial services, including 24/7 settlement using USDC, tokenization of credit card receivables, and automated settlement processes via smart contracts.

2.2.2 Mastercard

Mastercard, alongside Visa, is one of the world’s leading global payment networks. Unlike VisaNet, which boasts high processing capabilities through a centralized network, Mastercard processes payments through Banknet—its globally distributed infrastructure of over 1,000 data centers—making it highly resilient to outages. On April 28, 2025, Mastercard announced that it had established an end-to-end stablecoin-based payment infrastructure covering everything from wallets to checkout.

The first initiative is the issuance of cards and support for payments integrated with cryptocurrency wallets. Mastercard is collaborating with cryptocurrency wallets like MetaMask, exchanges such as Kraken, Gemini, Bybit, Crypto.com, Binance, and OKX, as well as fintech startups like Monavate and Bleap to provide such services.

MetaMask, in partnership with Mastercard and Baanx, launched the MetaMask Card, which allows users to make card payments using crypto assets held in the MetaMask wallet. For settlement, the backend leverages Monavate’s solution, which converts users’ crypto into fiat currency and connects the Ethereum network to Mastercard’s Banknet. The MetaMask Card will initially be available in Argentina, Brazil, Colombia, Mexico, Switzerland, the UK, and the US.

Mastercard also works with the aforementioned crypto exchanges to support cards that allow payments directly from users’ stablecoin balances.

Recently, Mastercard partnered with MoonPay, one of the world’s largest on/off-ramp service providers, to issue cards via Iron’s API—Iron being a company acquired by MoonPay—that can be used at Mastercard-accepting merchants.

The second initiative is supporting USDC settlements for merchants. While most stablecoin-based payments are ultimately settled in fiat, Mastercard enables merchants to receive settlements in USDC if desired, in collaboration with Nuvei and Circle. Beyond USDC, Mastercard also works with Paxos to support settlements in stablecoins issued by Paxos.

The third initiative is enabling on-chain remittances. Stablecoin remittances over blockchain are simple, fast, and low-cost. However, real-world adoption faces challenges around user experience, security, and regulatory compliance. To address this, Mastercard introduced the Mastercard Crypto Credential service, which allows users of cryptocurrency exchanges to complete a verification process, create aliases, and send stablecoins using those aliases.

This eliminates the need to input complex wallet addresses, significantly improving the user experience. Moreover, the system can block transactions if the recipient wallet does not support the specified crypto asset or blockchain, preventing loss of funds.

From a regulatory standpoint, Mastercard enables automatic exchange of Travel Rule information for international remittances, helping to meet compliance requirements and enhance transparency.

Exchanges currently supporting Mastercard Crypto Credential include Wirex, Bit2Me, and Mercado Bitcoin. The service is available in Latin American countries such as Argentina, Brazil, Chile, Mexico, and Peru, as well as in several European countries including Spain, Switzerland, and France.

The fourth initiative is providing tokenization platforms for enterprises. Mastercard’s Multi-Token Network (MTN) is a private blockchain-based service that enables financial institutions and enterprises to issue, burn, and manage tokens, facilitating fast, round-the-clock cross-border transactions without relying on traditional financial infrastructure.

Ondo Finance has tokenized its short-term bond fund (OUSG), backed by U.S. Treasuries, and integrated it into MTN. This allows companies to purchase and redeem OUSG in real time, 24/7, without using traditional financial systems, while earning stable yields.

JPMorgan has integrated its own blockchain-based payment system, Kinexys, with MTN to support real-time intercompany payments.

In May 2024, Standard Chartered conducted a proof-of-concept project using MTN to tokenize and trade carbon credits.

2.2.3 PayPal

PayPal is a global fintech company founded in the United States in 1998 and is a pioneer in online payments and money transfers. PayPal offers users a digital wallet-based online payment system. Users can link their bank accounts or credit cards to their PayPal accounts to either fund their digital wallets or use them directly as a payment method. Transfers can be made using just an email address or mobile number, and users can make fast online purchases simply by logging into their PayPal accounts. In addition, PayPal provides user-friendly features such as hiding the buyer’s financial information from sellers and intermediating between merchants and card issuers/banks, along with buyer protection policies.

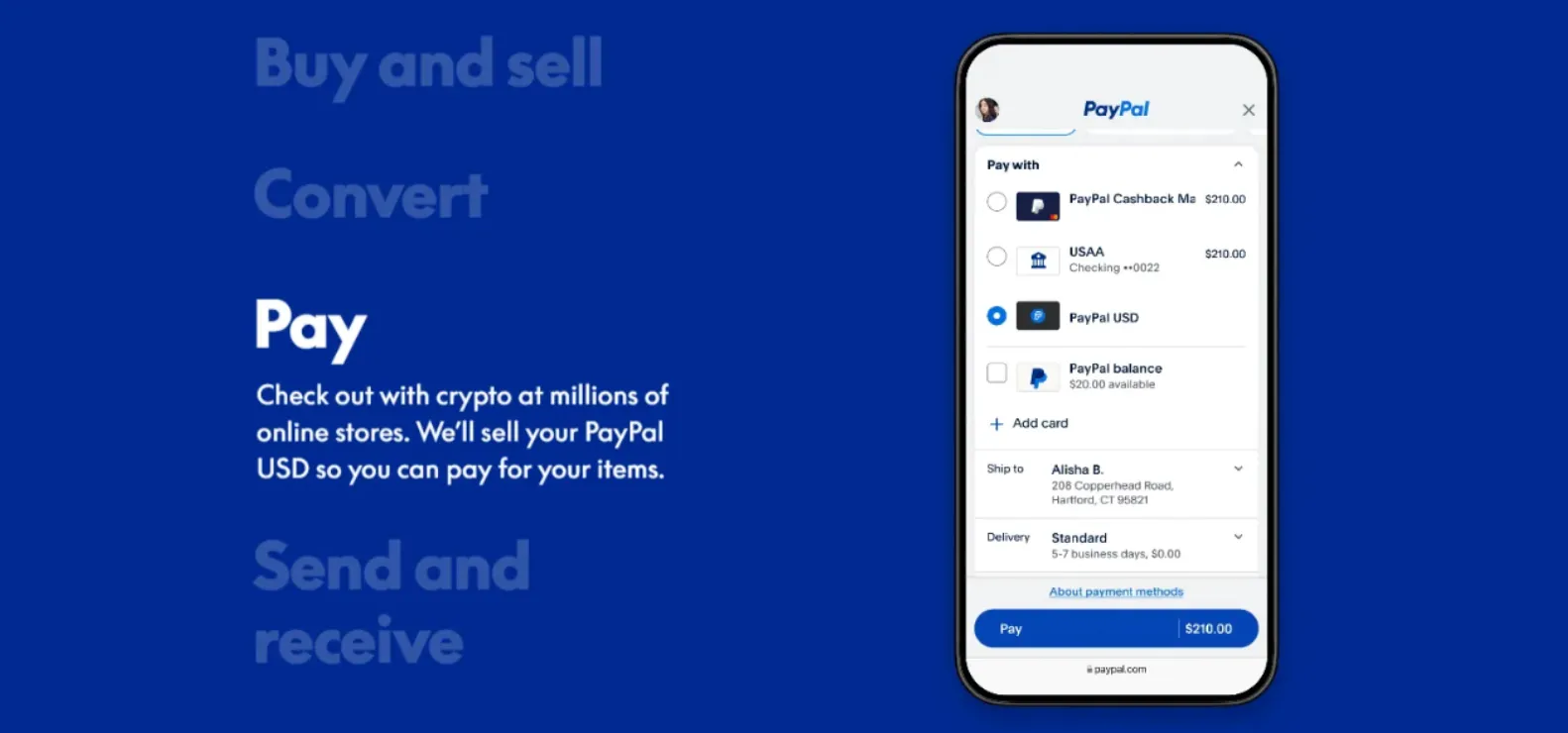

What differentiates PayPal from other fintech companies is that, in addition to offering stablecoin-based services, it directly issues a stablecoin—PYUSD—in partnership with Paxos, a stablecoin issuer. PYUSD is fully backed to maintain a stable value of one U.S. dollar and is collateralized by reserves consisting of U.S. dollar deposits, U.S. Treasuries, Treasury repurchase agreements (repos), and cash equivalents.

PYUSD is integrated into the PayPal app, making it easily accessible to all PayPal users. Users can purchase PYUSD using their PayPal balance or linked bank accounts/cards, and they can convert PYUSD back into dollars or other crypto assets. One of the key benefits is that PayPal users in the U.S. can send PYUSD to each other instantly and without fees.

PayPal UI

Source: PayPal

PYUSD can also be used as a payment currency, allowing users to pay with PYUSD at online merchants. When a user makes a payment using PYUSD, PayPal automatically converts it into U.S. dollars and settles the amount with the merchant. Unlike traditional card payments, this process does not involve acquirers, card networks, or card issuers, making the overall flow simpler and the fees lower. Additionally, users who are familiar with on-chain or DeFi environments can also transfer PYUSD to their personal wallets via the Ethereum or Solana networks.

2.2.4 Stripe

Stripe is a comprehensive Payment Service Provider (PSP) that fulfills the roles of a payment gateway, payment processor, and acquirer. It encrypts customers’ payment information and transmits it to card networks and issuing banks, communicates the approval result back to the merchant, and also handles settlement by transferring the received funds from the issuer to the merchant.

Stripe recently held its 2025 annual event, “Sessions,” where it identified AI and stablecoins as key themes and announced related initiatives. As mentioned in the Visa example above, Stripe acquired the stablecoin infrastructure startup Bridge in early 2025 and collaborated with Visa to launch a stablecoin-based Visa card.

In addition, Stripe recently launched Stablecoin Financial Accounts, allowing businesses in 101 countries to hold USDC and USDB (issued by Bridge), and to send and receive those stablecoins across crypto networks as well as traditional financial rails like ACH and SEPA. This will enable businesses in countries with high currency volatility to gain easier access to the U.S. dollar.

Beyond this, Stripe also offers the following stablecoin-related services:

Stablecoin Payments: When a customer pays in USDC or USDP via Stripe, Stripe automatically converts it into U.S. dollars and settles the payment with the merchant.

On-Ramp Service: Stripe provides a gateway that allows users to purchase cryptocurrencies directly on the Stripe platform using credit cards, Apple Pay, ACH, and other methods. Stripe assumes the role of the seller of record and handles transaction responsibility, fraud management, dispute resolution, KYC/AML compliance, and sanctions screening.

2.2.5 RedotPay

RedotPay is a Hong Kong-based fintech company founded in 2023 that provides a platform enabling the use of cryptocurrencies for everyday payments. RedotPay offers users both virtual and physical crypto payment cards, allowing them to make payments using various tokens such as BTC, ETH, USDC, and USDT. These cards are compatible with Apple Pay, Google Pay, and PayPal, and also support ATM withdrawals.

RedotPay users can store and manage their crypto assets through two options. The first is RedotPay’s own custodial wallet, where user assets are segregated and held in trust by Cactus Custody, a subsidiary of Matrixport. These assets are insured with a $42 million policy provided by OneDegree. Cactus Custody is a licensed trust company in Hong Kong and has passed the SOC2 Type 1 audit. The second option is an external wallet, such as MetaMask. Users may deposit funds from their external wallets into a smart contract vault for use in payments; however, these deposits are not covered by Hong Kong’s deposit protection scheme or insurance.

The specific settlement process is as follows: when a user pays a merchant using the RedotPay card, the cryptocurrency is instantly converted by RedotPay into the corresponding fiat currency. This fiat currency is then transferred to the merchant’s account via VisaNet, in collaboration with Visa. RedotPay works with StraitsX, a BIN sponsor, which allows it to access the Visa network without holding a direct license.

RedotPay’s backend settlement engine, called PayFi, provides instant settlement for merchants. Recently, RedotPay has also expanded support for crypto payment cards in South Korea, attracting attention in the media.

2.2.6 Worldpay

Worldpay is a leading acquirer in the payment processing industry and, as of 2024, ranked as the third-largest merchant acquirer globally by transaction volume. Among acquirers, Worldpay—alongside Nuvei—has been one of the most active in adopting stablecoins.

Historically, Worldpay has supported merchants in accepting and settling payments using USDG, a stablecoin issued by Paxos Digital Singapore. More recently, with Visa’s expansion of USDC-based settlement capabilities, both Worldpay and Nuvei can now receive settlements in USDC.

In addition, Worldpay has launched various blockchain-related initiatives, such as participating as a validator on multiple public blockchains, and building its settlement infrastructure by integrating payment engine technology from Fireblocks, a leading crypto custody provider.

2.2.7 JD.com

JD.com is one of China’s leading comprehensive e-commerce companies. Initially focused on selling electronics through its online marketplace, JD.com has since evolved into a full-scale platform offering a wide range of products, including home appliances, food, apparel, and cosmetics. In 2024, JD.com achieved $160.8 billion in revenue and, as of 2023, had approximately 588.3 million annual active customer accounts, making it a massive platform.

JD.com is participating in the Hong Kong Monetary Authority (HKMA)'s stablecoin regulatory sandbox program, and through its subsidiary Jingdong Coinlink, it is testing the issuance of a stablecoin pegged 1:1 to the Hong Kong dollar on a public blockchain. The stablecoin will be backed by high-liquidity and highly trusted assets, which will be held in a segregated account managed by a licensed financial institution. JD.com aims to leverage stablecoins to improve the efficiency of cross-border payments.

2.2.8 Rain

Rain is a card issuance infrastructure platform that enables businesses to easily issue and manage stablecoin-linked payment cards. Rain holds a Visa principal membership, giving it the authority to issue cards that operate on the Visa network.

Rain provides APIs that allow fintech companies and wallet service providers to issue co-branded cards. In addition to card issuance, Rain supports regulatory compliance and operational needs including KYC/KYB management, transaction monitoring, and dispute resolution—making it possible for businesses to launch stablecoin-linked cards without in-house expertise.

Rain is part of Visa’s experimental program, enabling issuers to settle with the Visa network using USDC. Previously, settlements were limited to traditional banking hours, but now, with stablecoins, issuers can settle 365 days a year. Merchant settlements are still handled by Visa, allowing merchants to receive funds in fiat currency.

2.2.9 Bridge

Bridge is a fintech company that provides global payment infrastructure based on stablecoins. In early 2025, it was acquired by Stripe for approximately $1.1 billion and now operates as a Stripe subsidiary. Bridge offers a wide range of stablecoin-based products, including:

Orchestration: The orchestration API allows stablecoin payments to be integrated into existing financial flows, enabling seamless interoperability with multiple currencies across countries.

Issuance: Companies can issue stablecoins via a single API and earn yield from the underlying collateral backing those stablecoins.

Wallets: Enables businesses to offer wallet solutions on their platforms via a simple API—without needing to manage transaction monitoring, wallet maintenance, or blockchain infrastructure. Combined with the orchestration and card APIs, users can easily send, store, and spend stablecoins.

Cards: Allows businesses to issue stablecoin-linked cards within a few weeks. These cards are available in regions such as Asia, Latin America, and the United States.

Cross-border Transfers: Users can send and receive stablecoins globally 24/7 with instant settlement.

2.2.10 Others

In addition to the major players introduced above, many payment companies are adopting stablecoins to build next-generation payment systems. Several global corporations are already using stablecoins in their actual payment processes.

Meta: After halting its Diem cryptocurrency project three years ago, Meta is once again exploring the adoption of stablecoins. Instead of launching its own coin, the company is now considering the use of proven market stablecoins such as USDC and USDT to facilitate global payments and reduce cross-border transaction fees.

Revolut: A fintech company based in London, Revolut operates a financial super app that offers services including foreign exchange, remittance, investment, savings, payments, and insurance. Revolut plans to launch a stablecoin compliant with Europe’s MiCA regulations, and already provides virtual payment cards that allow users to spend their crypto balances.

Block: The parent company of Square (a leading POS system provider) and Cash App, Block has recently formed a Payment Rails team to build a stablecoin-based payment network.

StraitsX, Alipay+, GrabPay: This collaboration enables tourists using Alipay+-affiliated apps to make payments at GrabPay merchants in Singapore via the XSGD stablecoin, issued by StraitsX on the Avalanche blockchain—bypassing traditional networks like Visa and Mastercard for faster settlement.

Checkout.com: A London-based PSP that functions as a payment gateway, processor, and acquirer like Stripe. In 2022, it launched a USDC-based settlement solution through a partnership with Fireblocks.

Fireblocks: Through its Digital Asset Payments Engine, Fireblocks enables businesses to easily adopt stablecoin-based real-time settlement, global payments, and automated token conversion. Worldpay used this technology to cut its settlement time by 50% for clients such as Crypto.com and Banxa.

Baanx: A UK-based fintech company focused on stablecoin-powered payment and financial solutions. Baanx partnered with Visa to launch a USDC payment card, allowing users to spend directly from their self-custody wallets. Baanx converts the USDC into fiat for settlement via the Visa network. It is also collaborating with Mastercard sponsor Monavate and wallet provider MetaMask to issue a Mastercard that enables users to pay directly from their MetaMask wallets.

BVNK: A London-based fintech company that provides global stablecoin payment infrastructure. BVNK offers multi-currency virtual accounts, stablecoin payment and remittance rails, embedded and self-custody wallet infrastructure, and a full-suite platform called Layer1 for custody, payments, liquidity, and compliance across multiple networks. BVNK recently received investment from Visa.

2.3.1 Merchant

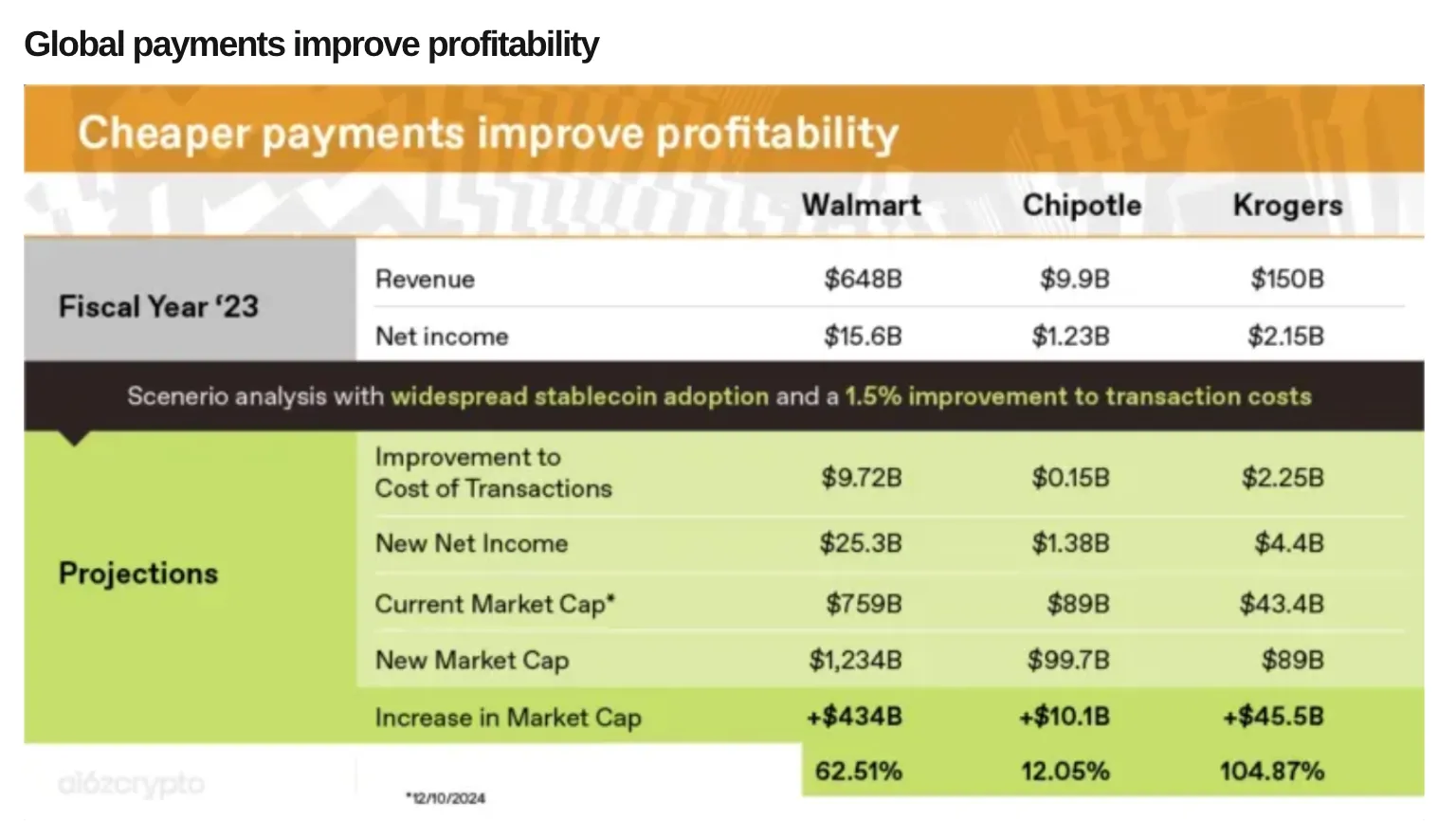

In traditional payment systems, merchants have long borne the burden of high fees and slow settlement times. If stablecoin-based payment systems become more widely adopted, both profitability and cash flow for merchants are expected to improve—especially for those with low margins and high sensitivity to transaction fees.

a16z simulated the impact on profitability for Walmart, Chipotle, and Kroger—assuming that stablecoins could reduce total payment processing fees from 1.6% to 0.1%. These companies represent typical low-margin businesses in the supermarket and food service sectors, where net income is extremely low relative to revenue. Unsurprisingly, the simulation showed that a significant reduction in payment fees would dramatically enhance profitability: net income increased by 65% for Walmart, 12% for Chipotle, and doubled for Kroger.

Global payments improve profitability

Source: a16zcrypto

Nevertheless, there are still factors that may discourage merchants from adopting stablecoins. These include the difficulty of handling payment cancellations or refunds due to the irreversible nature of blockchain transactions, the existence of additional off-ramp fees, and the lack of strong incentives for consumers in regions without significant currency instability to choose stablecoins for payments.

2.3.2 Acquirers and Payment Service Providers (PSPs)

This sector stands to benefit significantly from the expansion of stablecoin-based payment systems. In traditional payment processing, the majority of transaction fees incurred during customer payments are directed toward card networks and issuers, leaving acquirers and PSPs—who handle processing and merchant settlement—with relatively low margins.

In stablecoin payments, as seen in the case of PYUSD, PSPs can bypass card networks and issuers entirely and process payments directly, avoiding additional fees. This increases the relevance and potential profitability of acquirers and PSPs within the payment ecosystem.

2.3.3 Card Networks

As stablecoin-based payments leverage blockchain networks for settlement, the role of traditional card networks may diminish. Interestingly, unlike banks—which often resist the growth of stablecoins due to potential threats to their dominance—card networks like Visa and Mastercard have embraced stablecoins as a core part of next-generation payment systems and are proactively preparing for the transition.

Visa and Mastercard are building systems that allow issuers to settle with acquirers, and acquirers to settle with merchants, using stablecoins. They are also partnering with companies to issue stablecoin-linked cards that allow users to spend their stablecoin balances in daily life.

Given the massive global infrastructure already established through VisaNet and Banknet, Visa and Mastercard are unlikely to be easily displaced even as stablecoin adoption grows. In fact, their aggressive integration of stablecoins suggests they are well-positioned to retain dominance in the future payments landscape.

2.3.4 Card Issuers and Banks

As stablecoin payments become more prevalent, the traditional revenue models of card issuers and banks may come under pressure. Historically, bank deposits have served as the primary source of payment funding and credit card billing. But if consumers start storing value in crypto exchanges, fintech apps, or stablecoin wallets instead of bank accounts—and use those directly for payments—this could lead to deposit outflows and fee revenue decline for banks.

Nonetheless, rather than being rendered obsolete, many experts believe banks will evolve and coexist with stablecoins Credit cards are not just payment tools but bundled financial products offering interest-free loans, rewards, and consumer protection—features that are not easily replicated by stablecoins alone. For example, credit cards provide short-term credit for about 30 days, rewards such as points and miles, and protections like chargebacks for fraudulent transactions.

By contrast, stablecoin wallet-based cards are prepaid and do not extend credit to consumers. They also lack robust consumer protection in the event of accidental payments or unauthorized transfers. Therefore, card issuers and banks should leverage their existing strengths and integrate them into digital asset payments to offer differentiated services.

Another advantage banks have is their potential to bridge existing card/bank infrastructure with blockchain infrastructure. For example, Cross River Bank provides Circle’s on/off-ramp services for USDC, and BNY Mellon serves as a custodian for a significant portion of USDC reserves. In the future, banks could play a key role in providing secure conversion between fiat and stablecoins, as well as in custodianship of reserve assets.

Initially threatened by the rise of fintech, traditional banks survived by launching new ventures and partnering with fintech firms. Similarly, card issuers and banks must view stablecoins not as a threat but as an opportunity—to offer new services like custody, on/off-ramps, and compliance support that stablecoins alone cannot fully provide.

2.3.5 Cryptocurrency Exchanges

Many global crypto exchanges have already launched crypto debit cards that allow users to spend their holdings in real-life transactions. These exchanges can now act as a new class of card issuers in stablecoin payment systems, offering strong incentives for users to remain engaged with their platforms.

2.3.6 Platform Businesses

Large online platforms with substantial user bases can adopt stablecoin payment systems to help merchants receive settlements faster and at lower cost, while also enabling creators to unlock new revenue streams. This is one reason why companies like Meta have long considered stablecoin integration.

Such platforms may also take a step further by issuing their own stablecoins, as JD.com is testing. One of the greatest challenges in the stablecoin business is acquiring users and generating liquidity. Platform companies already have massive user bases, making adoption easier. By issuing their own stablecoins, they can provide integrated on/off-ramp services to users and merchants, and generate additional income from collateral yields—thereby creating a more resilient platform ecosystem.

2.3.7 Stablecoin Infrastructure Providers

While fintech companies revolutionized the front end of financial services, stablecoin-based payments are expected to transform the back end, fostering the growth of stablecoin infrastructure providers. Emerging players like Bridge, Rain, Redot Pay, BVNK, and Baanx are offering end-to-end services—including on/off-ramps, APIs, wallet solutions, and more—allowing users and businesses to adopt stablecoin payments with ease.

Just like global payments, international remittances are one of the key use cases where blockchain technology and stablecoins can provide real value to users. Today, domestic transfers in many countries are almost free for users, thanks to technological advancements and public sector support. Representative examples include ACH in the U.S., SEPA in Europe, FPS in the UK, and IMPS in India.

However, international remittances still typically involve high fees. Services like Wise, Western Union, and MoneyGram are commonly used, but users often have to pay several dollars to as much as $10–20 per transfer. One key reason for these high fees is that most international remittance services still rely on the SWIFT network.

SWIFT—the Society for Worldwide Interbank Financial Telecommunication—is a network established in Belgium in 1973 that enables international money transfers through the secure and standardized exchange of financial messages between institutions. One common misconception is that SWIFT moves money itself, when in fact it merely serves as a secure communication system for transmitting payment instructions between banks.

In the early 1970s, international remittances were primarily conducted via Telex, a text-based communication system that operated over telephone lines and was originally used for military communication. However, Telex was slow, prone to errors, and lacked adequate security. To address these issues, 239 banks came together in Brussels in 1973 to establish SWIFT, with the goal of creating a standardized messaging system for international financial transactions.

Since then, SWIFT has rapidly expanded its network from Europe and North America to Asia, Africa, and Latin America. Over time, it has strengthened member institution security, introduced modern messaging standards like ISO 20022, and improved data structure and automation to enhance efficiency. Today, SWIFT processes over 50 million messages per day across more than 200 countries, making it a critical component of the global financial system.

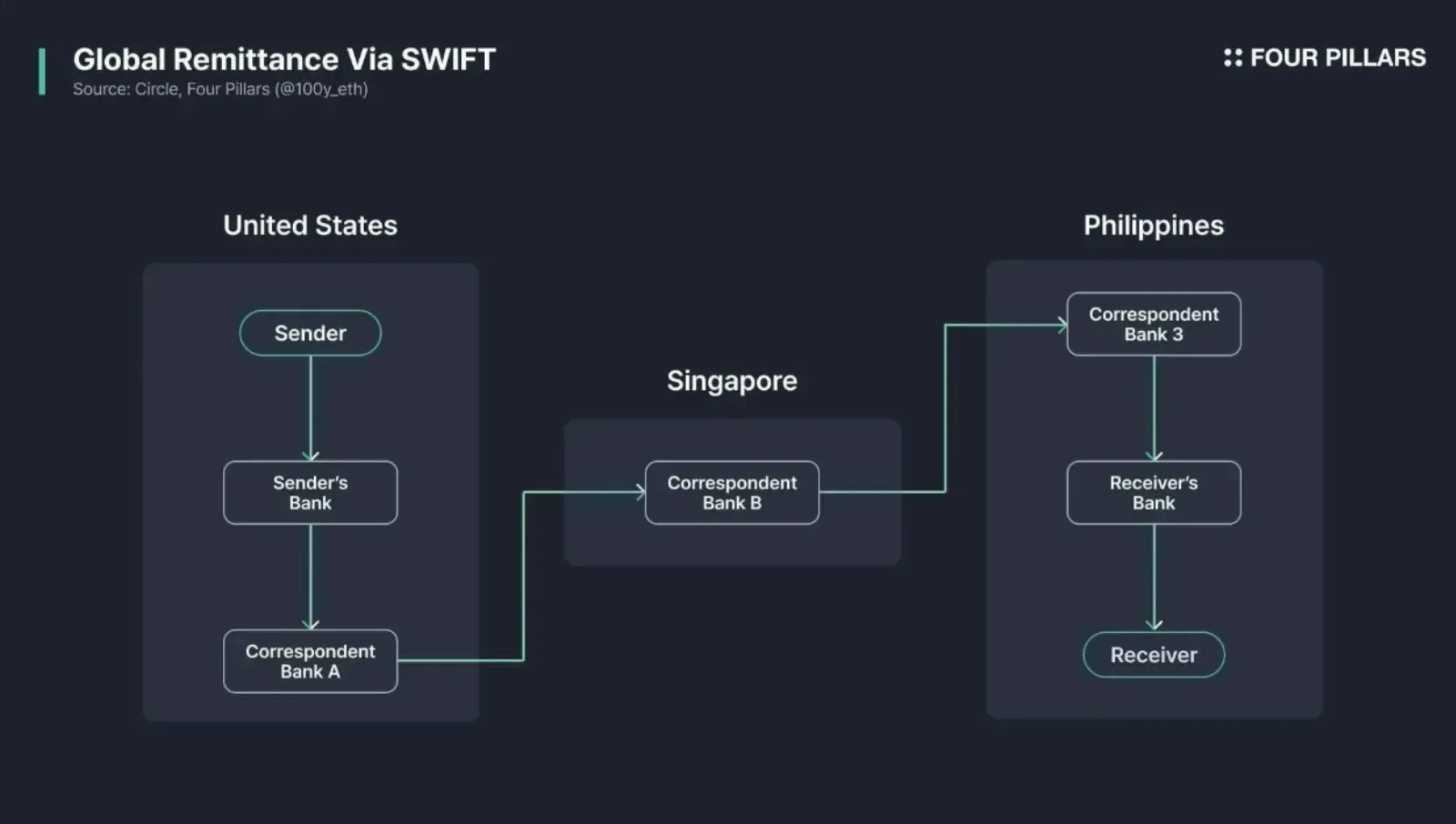

Global Remittance Via SWIFT

Source: Four Pillars

So how does international remittance via SWIFT actually work in practice? It’s important to note that SWIFT messages in the following process are secured through encryption and authentication and comply with Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) regulations.

Initiating the Remittance Request: The sender provides the originating bank with the recipient's bank details, including the SWIFT code and account number, to initiate the international transfer.

Sending the SWIFT Message: The originating bank sends a payment instruction message to the recipient bank via the SWIFT network.

Funds Transfer via Intermediary Banks: If the originating and recipient banks do not have a direct account relationship, the funds are routed through one or more intermediary banks.

Receipt and Deposit by Recipient Bank: The recipient bank receives the SWIFT message and deposits the funds into the recipient's account.

This process typically takes 1 to 5 business days and is significantly more expensive than domestic transfers. When using a bank or fintech service to send money internationally, fees often range from a few to several dozen dollars. Why is this the case?

Let’s start with slow transfer speeds. If there is no direct account relationship between the sending and receiving banks, the funds must be routed through intermediary banks. This introduces additional layers of processing, each with its own procedures and timelines. Moreover, banks across different countries operate in different time zones and have different working days and public holidays, which can further delay the transaction.

As for high costs, each intermediary bank involved in the transaction may charge a fee. In many international transfers, currency conversion is also required, which incurs foreign exchange fees, often at exchange rates less favorable than the market rate.

In contrast, stablecoin-based remittance offers several advantages due to the nature of blockchain technology: there are no borders, network fees are minimal, and settlement is nearly instantaneous. Let’s now explore how businesses and fintech services are leveraging stablecoin remittances in the real world.

3.2.1 SWIFT

SWIFT has also recognized the importance of stablecoins and blockchain technology and is preparing for the future. Its vision is to build an infrastructure where, in the future, financial institutions can freely exchange traditional assets (such as fiat currencies and securities) and digital assets (such as CBDCs and stablecoins) through existing SWIFT connections.

In fact, SWIFT has already conducted experiments in 2024 to connect blockchain networks with its infrastructure, successfully testing token transfers between public and private blockchains and collaborating with central and commercial banks in several countries to explore CBDC interoperability. Starting in 2025, SWIFT plans to move beyond the experimental phase and launch pilot programs for real transactions of digital assets and currencies over the SWIFT network with banks in North America, Europe, and Asia.

Several central banks are already testing digital methods for international foreign exchange transactions. The Hong Kong Monetary Authority (HKMA) and the Bank of France, for example, are conducting FX trials using SWIFT. These efforts are part of a broader project led by the European Central Bank (ECB) to explore next-generation technologies in wholesale settlement. As of now, technical details on how these experiments and pilots are being conducted have not yet been publicly disclosed.

3.2.2 ScaleAI (feat. Airtm)

ScaleAI is a San Francisco–based AI data labeling and infrastructure company co-founded by Alexandr Wang and Lucy Guo. The company provides high-quality data essential for training AI models. Given the nature of the data labeling industry, which involves a globally distributed workforce, a reliable and efficient payment system is critical to ensure workers are paid smoothly.

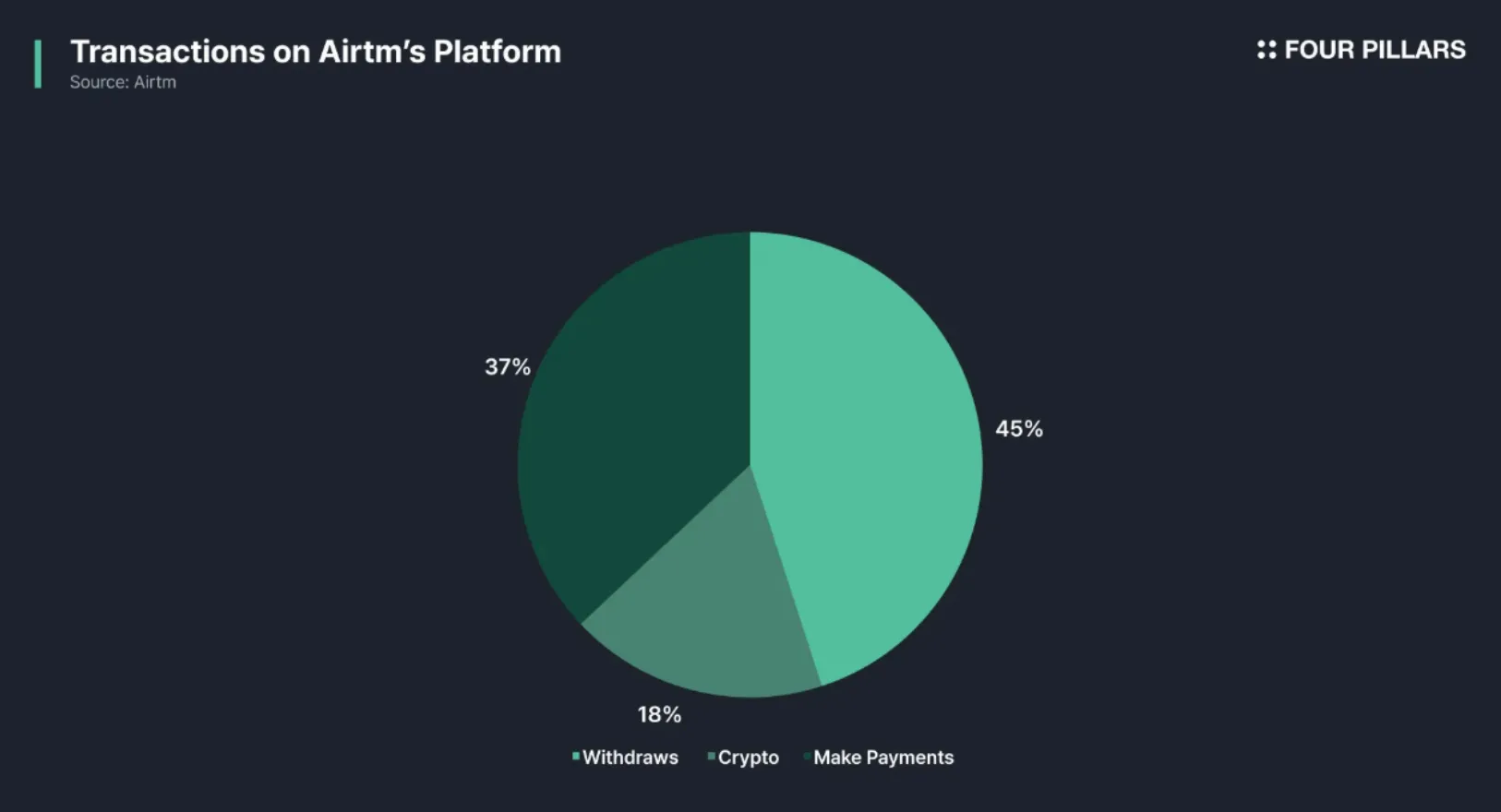

To facilitate this, ScaleAI uses the services of Airtm, a payments and community platform that connects global workers with companies needing AI data labeling services. Airtm supports fast payments, multiple currency options, peer-to-peer transfers, and crypto withdrawals, all designed to make it easy for workers to receive compensation.

Global Remittance Via SWIFT

Source: Airtm, Four Pillars

Airtm surveyed how data labeling workers receive their payments: 45% withdrew in their local currency, 37% transferred the funds to other users within Airtm, and 18% withdrew in cryptocurrency. Airtm users can select stablecoins as their withdrawal method, choose the type of stablecoin (e.g., USDC, USDT, DAI, PYUSD), and then select their preferred network (e.g., Ethereum, Solana, Avalanche, Optimism) to easily withdraw their funds.

3.2.3 Bitso

Bitso is the largest crypto and fintech company in Latin America, headquartered in Mexico, with over 9 million individual users and more than 1,900 business clients across Mexico, Brazil, Argentina, and Colombia. Bitso provides a wide range of services including crypto trading and blockchain-based financial infrastructure for payments and remittances.

Bitso is directly connected to local payment networks such as SPEI in Mexico and Pix in Brazil, allowing users to deposit funds into their Bitso wallets via bank accounts or cards (on-ramp). Bitso supports 24/7 real-time transfers using USDC, USDT, and its own Mexican peso–pegged stablecoin MXNB. A real-world example is Felix, a WhatsApp-based remittance service that collaborates with Bitso to enable fast, seamless transfers from the U.S. to Mexico using USDC on the Stellar network.

3.2.4 Others

SpaceX: Starlink, SpaceX’s global internet service, is especially in demand in regions with limited connectivity. Because it accepts payments in various currencies, SpaceX converts local currency payments into stablecoins immediately to hedge against FX risk, and later converts them back into USD in the U.S.

Venmo and XOOM: Both are subsidiaries of PayPal and allow users to send money easily using PayPal’s stablecoin PYUSD.

MoneyGram: A major U.S.-based global remittance service that now supports USDC transfers over the Stellar network in addition to traditional remittance methods.

Afriex: A remittance service targeting African and diaspora communities, offering international transfers and on/off-ramp services using USDC.

Stables: A digital currency exchange and remittance company registered with AUSTRAC in Australia. Stables enables global remittances using stablecoins such as USDC, USDT, DAI, and PYUSD, with a particular focus on remittances between Australia and the Philippines. Stables also provides virtual bank accounts, allowing users to deposit USD, AUD, EUR, and more.

As covered in section 2.1, Visa, Mastercard, Stripe, and PayPal all already support or are preparing to support P2P remittances using stablecoins.

Stable: With the majority of stablecoin transfers and trading now taking place on TRON, Ethereum, and Solana, networks optimized specifically for stablecoin transfers are beginning to emerge. A leading example of this trend is the network Stable, designed specifically for stablecoin-focused use cases.

3.3.1 Individuals and Businesses

The primary reason individuals have avoided international remittances has been high fees, but as stablecoin-based remittance services become more widespread, individuals may begin to use international transfers as frequently and easily as domestic ones. Businesses as well can benefit—similar to the case of ScaleAI, which uses stablecoins for global compensation, or SpaceX, which utilizes stablecoins to reduce foreign exchange risk—thereby lowering operational costs related to cross-border transactions.

3.3.2 Fintech Services

Fintech companies like Venmo, XOOM, and MoneyGram, which already provide international remittance services, now support transfers using stablecoins. This allows them to offer faster and cheaper services to users, reduce intermediary bank fees incurred through the SWIFT system, and presents an opportunity to attract a larger user base.

3.3.3 Blockchain Infrastructure Providers

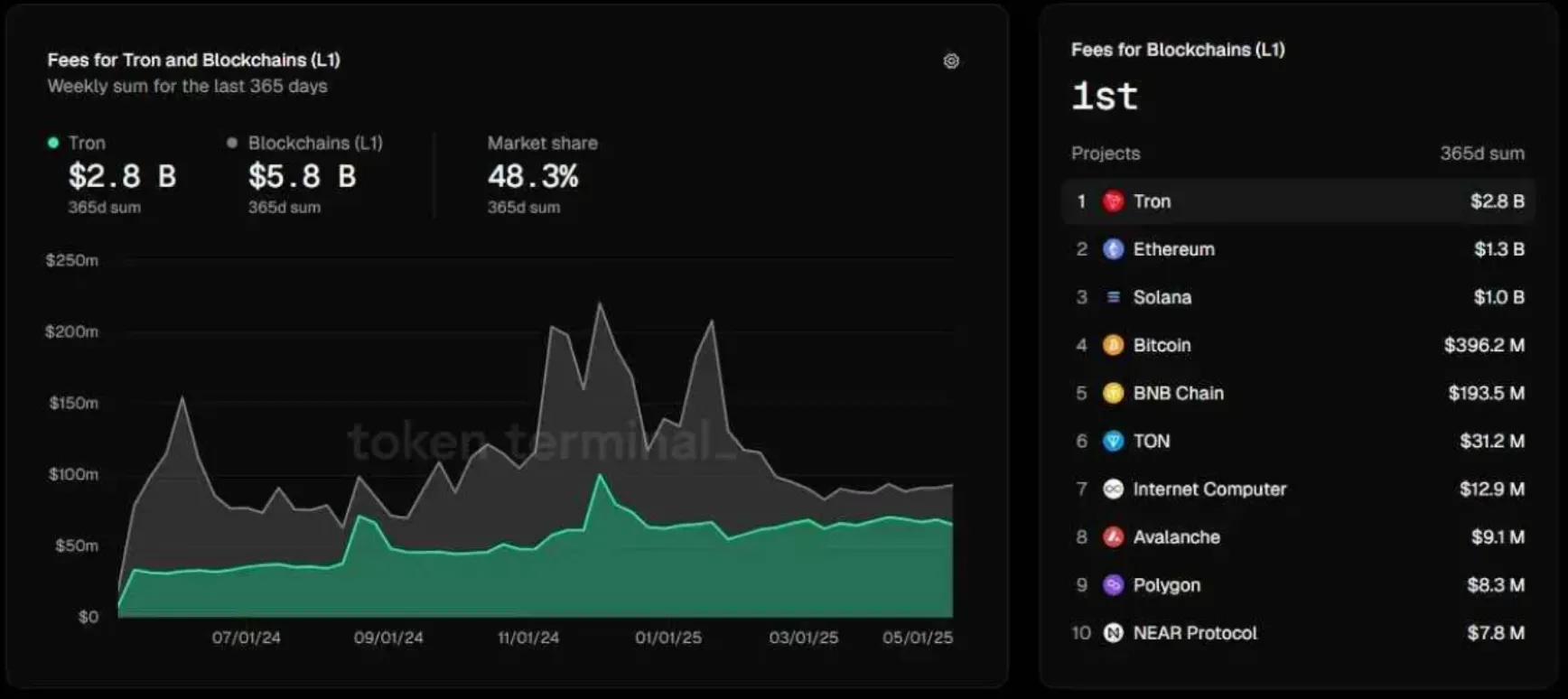

In traditional cross-border transfers, fees mostly flowed to intermediary banks participating in SWIFT. In stablecoin-based remittances, though the fees are significantly lower, they are instead distributed to blockchain infrastructure providers such as validators and token stakers.

Fees for Tron an Blockchains (L1)

Source: Token Terminal

Despite the low cost of blockchain remittances, the total fee revenue is still substantial. Last year, the TRON network generated $2.8 billion in fee revenue—more than Ethereum and Solana combined. Since over 98% of transactions on the TRON network are related to USDT transfers, it highlights the massive scale of the stablecoin transfer market. As stablecoin-based remittances continue to grow, blockchain infrastructure providers are expected to benefit significantly.

3.3.4 On/Off-Ramp Services (+ Banks)

As stablecoin remittances increase, demand will rise for converting between cash and stablecoins. On/off-ramp service providers can charge fees for facilitating these conversions, opening up a new revenue stream. Even beyond specialized on/off-ramp providers, traditional banks could expand into this business. On/off-ramp infrastructure requires regulatory components such as KYC/AML, fraud prevention, and risk management—areas where banks already have strong capabilities.

Interbank settlement refers to the process by which multiple banks calculate and transfer funds to settle obligations arising from financial transactions between customers. Typically, the settlement process involves three steps:

1. Payment: This is the act of a person or business paying for goods or services. At this stage, funds are not yet actually moved from the payer’s account to the recipient’s account—instead, the transaction is recorded in the bank’s system.

2. Clearing: This involves aggregating transaction data across financial institutions and calculating the amounts owed between them.

3. Settlement: This is the final step, where actual fund transfers are made between financial institutions to eliminate the net obligations.

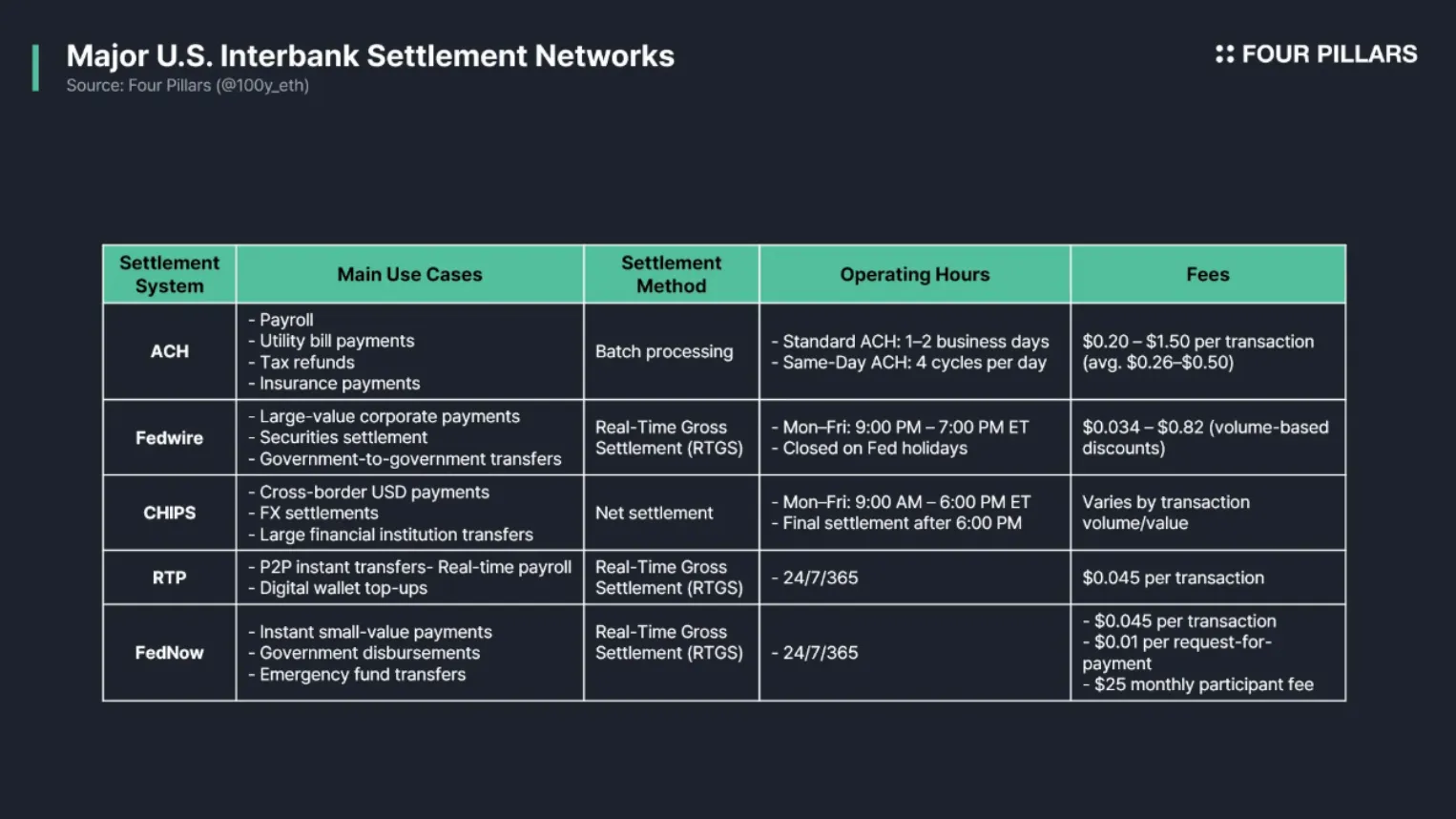

In the U.S., different types of interbank settlement networks are used depending on the nature of the transaction.

Major U.S. Interbank Settlement Networks

Source: Four Pillars

ACH: Operated by FedACH and EPN, this batch-processing system is suited for high-volume, low-value transactions like payroll deposits, utility payments, tax refunds, and insurance premiums. It is cost-efficient but typically takes 1–2 business days to process.

Fedwire: Suitable for large corporate transactions, securities settlement, and government transfers, Fedwire is a real-time gross settlement system processed through Federal Reserve accounts. Transactions are processed instantly but only operate on business days from 9:00 p.m. the previous day to 7:00 p.m. Eastern Time.

CHIPS: A net settlement system operated by The Clearing House, CHIPS is used for large-value payments such as international trade and FX settlements. It offsets multiple transactions throughout the day so that only the net amount is settled between participating institutions. It operates from 9:00 p.m. to 6:00 p.m. ET on business days.

RTP: Also operated by The Clearing House, the RTP system is a real-time gross settlement network suitable for instant low-value transactions like peer-to-peer transfers and real-time payroll payments. It operates 24/7, but payments are irreversible once completed, increasing fraud risk and requiring transaction limits for safety.

FedNOW: Operated by the Federal Reserve, FedNow is also a real-time gross settlement system designed for small-value payments and operates 24/7, similar to RTP.

Although traditional interbank settlement systems have long served as core financial infrastructure, they also come with structural limitations and inefficiencies. The first issue is transaction delays and restricted operating hours. Systems like ACH require 1–2 days for processing, and many settlement networks only operate during business hours. If international transfers are involved, using SWIFT may add another 2–5 days. The second issue is high fees. B2B cross-border transactions often incur fees ranging from tens to over a hundred dollars.

As discussed in the payments and remittance sections, introducing blockchain-based stablecoins into interbank settlement can resolve both issues. Because the underlying infrastructure is blockchain-based, transactions can be settled in real-time, operate 24/7, and provide very low fees even for international transfers. In fact, many banks are actively exploring or already using blockchain and stablecoins for interbank settlement. Let’s look at several examples in the following section.

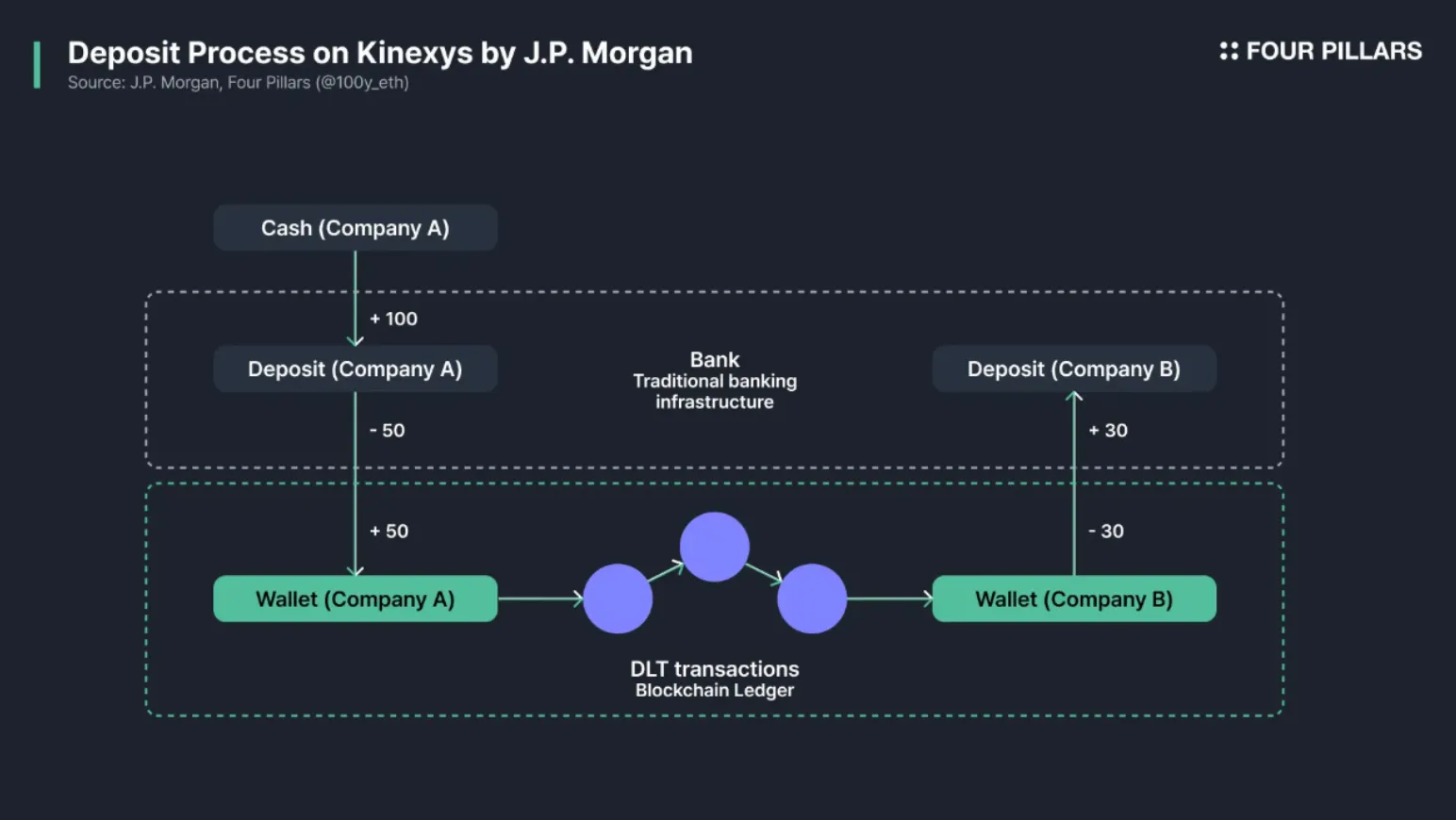

4.2.1 JPM Coin by JPMorgan Chase

JPM Coin is an institution-only digital currency introduced in 2019 by JPMorgan Chase, one of the largest investment banks in the U.S. JPM Coin operates as a stablecoin pegged 1:1 to fiat currency and functions on JPMorgan’s proprietary private blockchain platform, Kinexys.

Deposit Process on Kinexys by J.P. Morgan

Source: Deposit Tokens | Kinexys by J.P.Morgan, restructured by Four Pillars

Institutional clients who wish to transfer funds deposit USD or EUR into a designated JPMorgan account, and the equivalent amount of JPM Coin is issued. The coins are transferred in real time over JPMorgan’s blockchain network and can be redeemed back into USD or EUR by the recipient. Compared to the traditional banking system, this enables fast and efficient 24/7 real-time fund transfers.

Since its launch in 2019, JPM Coin has processed over $1.5 trillion in transactions and now facilitates an average daily volume of $2 billion. Notable institutional users include Brevan Howard, Goldman Sachs, and Axis Bank.

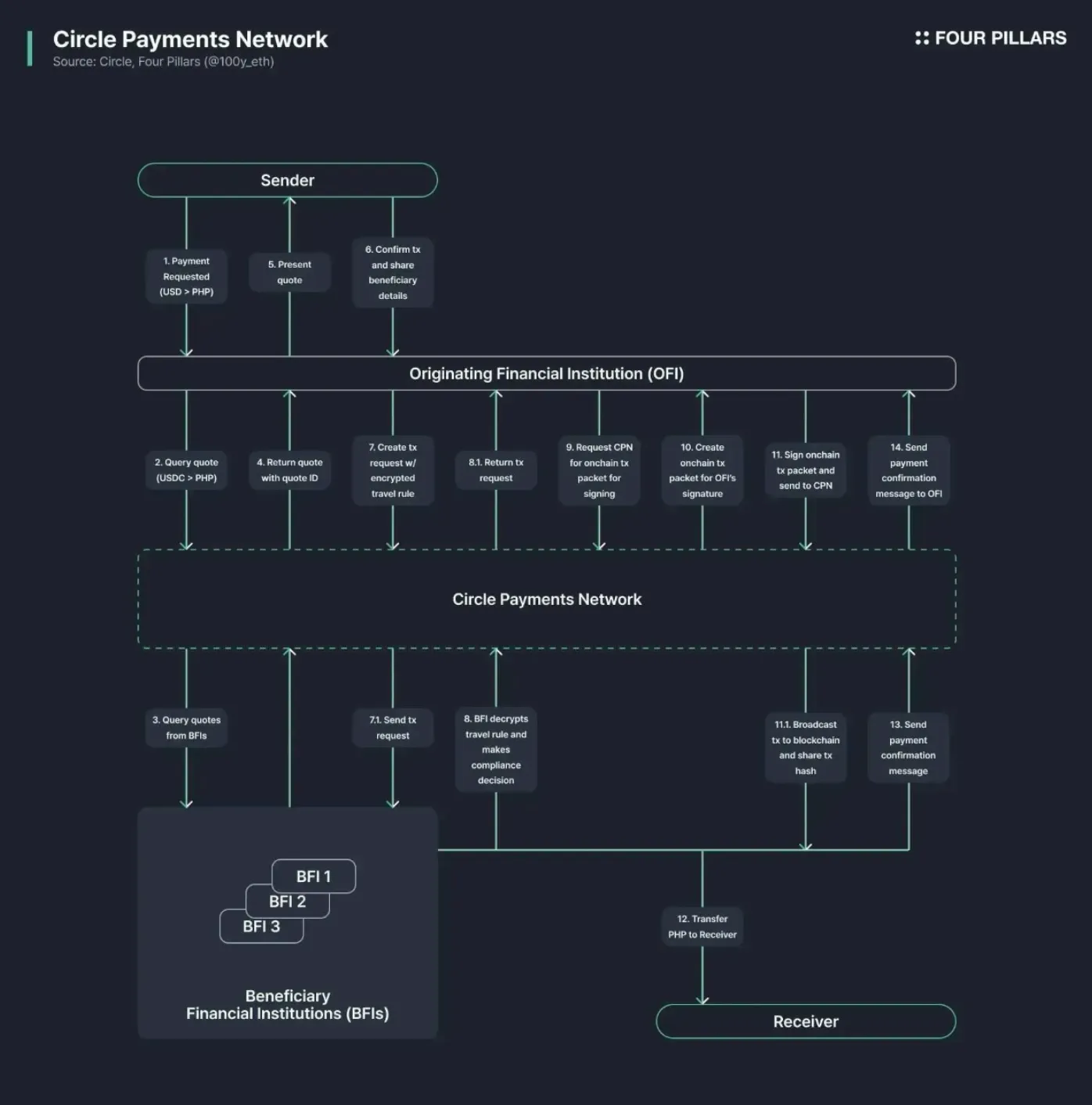

4.2.2 Circle Payment Network (CPN)

On April 22, 2025, Circle launched the Circle Payment Network (CPN). CPN is positioned as a new global standard for value transfer using blockchain and stablecoins, with participation from global banks, payment service providers, and digital asset-native financial institutions.

CPN is the first attempt to combine regulated stablecoins with a governance layer tailored for traditional financial institutions. It connects existing payment infrastructure with stablecoins and provides a trusted settlement layer for regulated financial entities. Because settlement occurs on a secure and continuously operating blockchain, CPN enables real-time cross-border payments across currencies and time zones.

Importantly, CPN is not a new blockchain network; it utilizes regulated stablecoins such as USDC and EURC, and runs on public blockchain infrastructure. Similar to SWIFT, CPN does not move funds directly but instead functions as a coordination protocol and marketplace for financial institutions to manage global transfers.

Circle Payments Network

Source: Circle, Four Pillars

CPN operates as follows (note: OFI = Originating Financial Institution; BFI = Beneficiary Financial Institution):

The sender asks the OFI to send USD to the Philippines in PHP.

The OFI requests a quote from CPN, including expected FX rates and fees.

CPN forwards the request to BFIs.

CPN returns BFI quotes to the OFI along with a quote ID.

The OFI presents the quote to the sender.

The sender confirms the transaction and shares recipient info with the OFI.

The OFI initiates a transaction request with recipient details, quote ID, and encrypted Travel Rule data via CPN, which is forwarded to the BFI.

The BFI decrypts Travel Rule data and determines whether to accept the transaction per compliance requirements, then sends its response to the OFI.

The OFI requests an on-chain transaction packet from CPN.

CPN generates the transaction packet for the OFI.

The OFI signs the transaction and sends it back to CPN, which broadcasts it to the blockchain.

Once the BFI receives the USDC on-chain, it delivers PHP to the recipient.

The BFI confirms completion to CPN.

CPN notifies the OFI that the transfer is complete.

Because CPN utilizes public blockchains for settlement, it is always accessible and globally interoperable. Beyond settlement, CPN also aims to optimize regulatory information exchange and payment routing. For example, it can automatically select the BFI offering the lowest fees. In the long term, developers will also be able to build modules and applications on top of CPN.

Initially, CPN uses a hybrid on-chain/off-chain architecture. The OFI generates and signs a transaction request via CPN's API (off-chain), Circle then broadcasts the transaction to a public blockchain, and funds are settled on-chain. In the future, however, CPN plans to transition from off-chain API interactions to fully on-chain smart contract execution, improving accuracy, automation, and security.

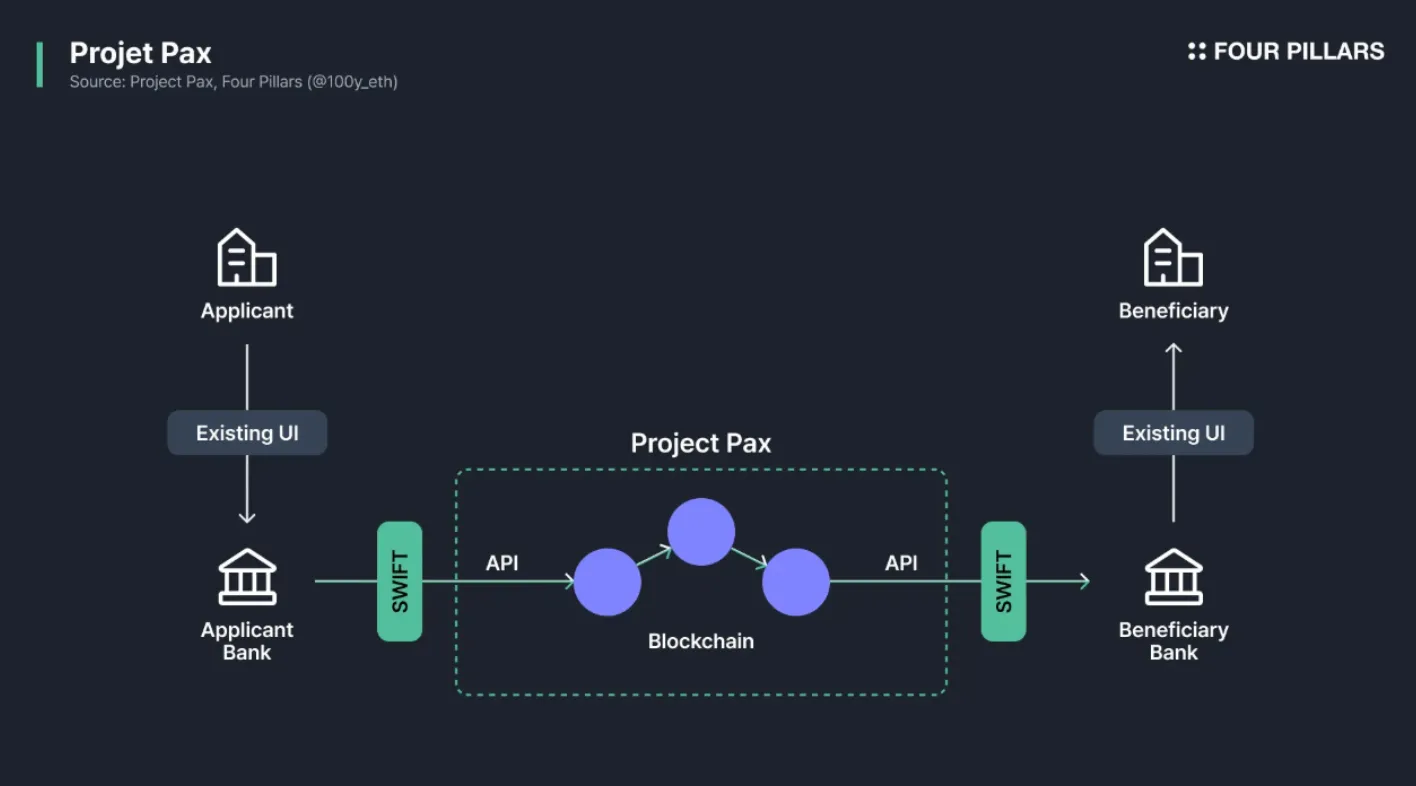

4.2.3 Project Pax

Project Pax is a cross-border stablecoin remittance infrastructure initiative led by major Japanese banks including MUFG, SMBC, and Mizuho. The project aims to integrate traditional financial systems with blockchain technology to enable efficient international money transfers.

A key feature of Project Pax is that from the user’s perspective—whether a bank, corporate, or institutional client—remittance is conducted via familiar SWIFT messaging, preserving user experience. However, on the backend, transactions are executed using blockchain and stablecoins for speed. The system is designed so that users do not need to understand blockchain technology like wallets or private keys.

Project Pax

Source: Project Pax, Four Pillars

The blockchain underpinning Project Pax is Progmat, a digital asset infrastructure platform led by MUFG. Progmat supports the issuance and management of stablecoins and security tokens. For stablecoins, it offers trust-based issuance compliant with Japanese regulation. Progmat runs on Corda, a private blockchain developed by R3, and supports interoperability with various public blockchains including Ethereum, Polygon, Avalanche, and Cosmos.

In April 2025, Project Pax entered Phase 2 of testing, simulating real-world remittance scenarios. Shoko Chukin Bank, a Japanese bank specializing in small- and medium-sized businesses, is participating in this phase.

4.2.4 Fnality

Fnality is a blockchain-based wholesale payment system jointly developed by global financial institutions. It tokenizes funds held by member banks at central banks on a 1:1 basis, enabling those tokens to be used for settlement on the network. This system allows participating banks to execute settlements 365 days a year without delays using blockchain technology.

Since its inception, Fnality has attracted collaboration from major financial institutions. Key investors and partners include: Banco Santander, BNY Mellon, Barclays, CIBC, Commerzbank, Credit Suisse, ING, KBC Group, Lloyds Banking Group, Mizuho Financial Group, MUFG Bank, Nasdaq, Nomura, SMBC, State Street Corporation, and UBS.

4.3.1 Banks

Currently, banks pay substantial fees to use interbank settlement networks. For example, as of 2024, ACH processed approximately 33 billion transactions, with an average fee of $0.20–$1.50 per transaction. Even at the lowest rate of $0.20, this amounts to $6.6 billion in fees.

In addition, Fedwire charges between $0.034–$0.82 per transaction, RTP charges $0.75, and FedNow charges $0.043. Since all three are real-time gross settlement (RTGS) systems, the total fee burden can be significant for institutions processing large transaction volumes.

By adopting blockchain-based stablecoin settlement systems, banks can dramatically reduce these fees while benefiting from real-time and 24/7 operational capabilities.

4.3.2 Blockchain Infrastructure Providers

As seen in use cases such as JPM Coin’s Kinexys, Circle’s CPN, Progmat (used in Project Pax), and Fnality, many stablecoin-based interbank settlement systems are being built on custom-optimized blockchain networks or messaging protocols. This trend demonstrates that blockchain infrastructure companies have a major opportunity to grow by providing settlement-focused infrastructure for financial institutions.

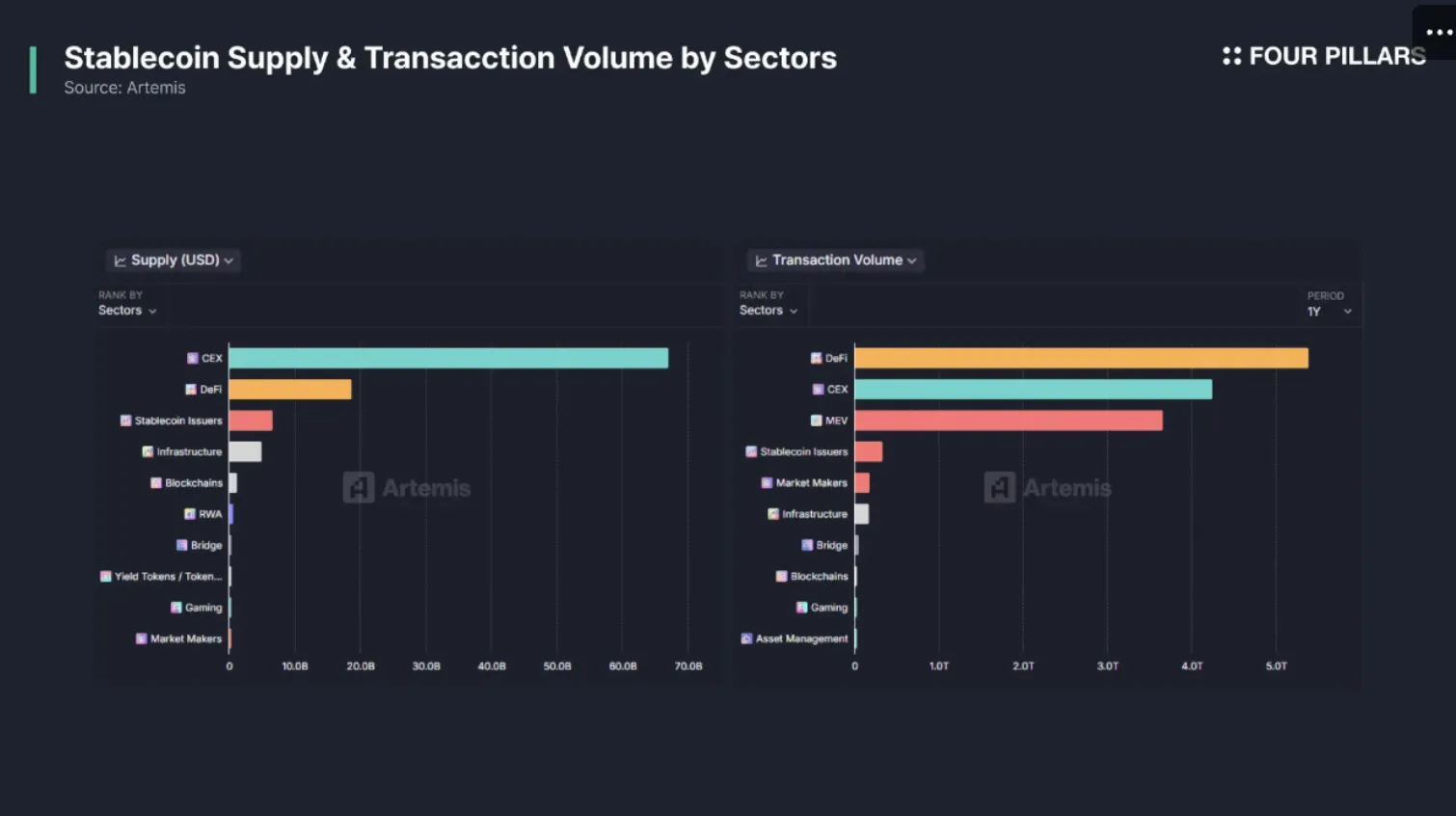

Stablecoin Supply & Transaction Volueme by Sectors

Source: Artemis, Four Pillars

As mentioned in the first installment of the stablecoin report, the most prominent use case for stablecoins today is within cryptocurrency exchanges. According to the Artemis stablecoin dashboard, massive amounts of stablecoin liquidity are deposited in centralized exchanges such as Coinbase, Binance, and Upbit. In addition, we see enormous trading volume occurring on decentralized exchanges as well. This indicates that regardless of whether the exchange is centralized or decentralized, stablecoins play a central role in crypto trading.

Globally, numerous CEXs now use stablecoins as a trading currency. Not only do exchanges operating in regulatory gray zones like Binance, Bybit, and OKX support stablecoins, but so do regulated exchanges like Coinbase and Kraken. These exchanges support stablecoins like USDC and USDT as quote currencies. Notably, Coinbase has even merged the USD and USDC order books to allow seamless trading within the same trading pair.

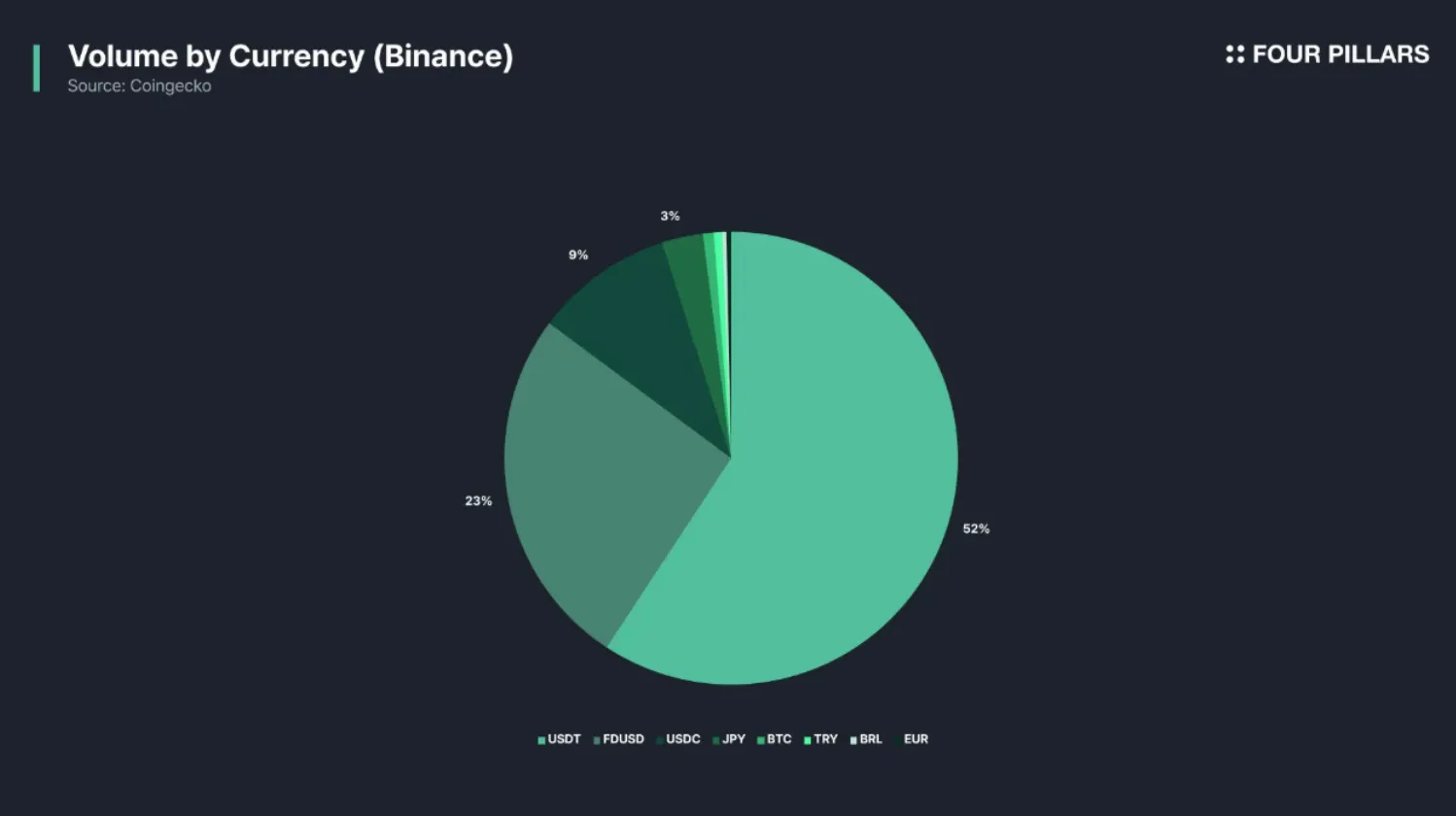

Volume by Currency (Binance)

Source: Coingecko, Four Pillars

Regulated exchanges such as Coinbase and Kraken have a relatively high share of fiat currency trading pairs, but in the case of Binance, nearly 90% of trading volume is conducted using stablecoins. Given that Binance’s daily trading volume is around $20 billion, stablecoins already process an enormous volume of crypto trades as the primary trading currency.

When a crypto exchange adopts stablecoins as a trading currency, both users and the exchange benefit in the following ways:

Stable Unit of Trade: In countries with volatile fiat currencies, crypto prices can show greater fluctuations compared to global prices. For example, in Turkey, political instability and depreciation of the lira have led to greater volatility and premium in the BTC/TRY market. Stablecoins allow users in such markets to trade with greater price stability.

Reduced Need for FX Conversion: In fiat-only exchanges, users must undergo cumbersome fiat-to-crypto conversion during deposits and withdrawals. If an exchange supports stablecoins, users can avoid unnecessary currency conversion steps.

Global Accessibility: In regions with limited access to traditional financial services or restricted use of USD, stablecoins allow users to access global exchanges without needing to open overseas bank accounts.

Simplified Payment Processing: Unlike fiat, stablecoins do not require integration with banks, account management, or remittance processing—dramatically reducing operational cost and complexity. Settlement is straightforward.

On-Chain Ecosystem Integration: When users want to transfer funds to use on-chain applications, they can easily withdraw in stablecoins.

24/7 Access: Unlike fiat transactions that depend on bank operating hours and may be unavailable during system maintenance, stablecoin deposits and withdrawals are available 24/7.

Exchange Independence: If an exchange issues its own KRW stablecoin, either independently or via a consortium, it can reduce fees related to bank integration (e.g., real-name account fees, fast withdrawal fees) and increase financial independence.

Throughout this report, we have examined how stablecoins are being utilized across four major use cases—payments, remittances, interbank settlement, and exchanges—and what kind of impact their adoption is having on both existing and emerging industries. Across all four categories, blockchain technology and stablecoins have consistently demonstrated the ability to reduce settlement times, lower intermediary fees, and improve global accessibility.

On May 15, 2025, at the Consensus 2025 event in Toronto, Jose Fernandez da Ponte, Senior Vice President of Digital Currencies at PayPal, delivered two key messages:

First, that the participation of banks is essential for the stablecoin industry to grow, and second, that there won’t be just two stablecoins left in the market, but there also won’t be 300.

In the past, as fintech companies emerged and rapidly grew, they directly targeted core banking sectors such as remittances, lending, payments, and wealth management—posing a serious threat to traditional banks’ customer bases and revenue streams. In response, banks employed three key strategies: build their own tech innovations, acquire fintech firms, or collaborate with them.

Building Innovation: Major U.S. banks like Bank of America, Chase, and Wells Fargo launched Zelle, a P2P payments network that successfully competed with Venmo.

Fintech Acquisitions: Examples include JPMorgan Chase acquiring WePay, Goldman Sachs acquiring Clarity Money and GreenSky, Morgan Stanley acquiring E*TRADE, and BBVA acquiring Simple.

Fintech Partnerships: Collaborating with fintechs to offer services like microloans or partnering with firms that don’t hold licenses themselves.

As this report has shown, the expansion of stablecoin-based payments and remittances could reduce the market share of traditional banks. However, this is no different from the fintech challenge banks have already faced. Banks are uniquely positioned to address limitations that stablecoins cannot easily solve—such as credit provisioning, fraud detection, and financial compliance.

Just as banks have coexisted with fintech companies, they can also coexist with a stablecoin-based financial system. Banks can:

Build technological innovation in areas like interbank settlement (e.g., JPMorgan’s Kinexys),

Acquire stablecoin issuers or infrastructure providers,

Expand into areas like on/off-ramps and custody, offering compliance support and infrastructure to stablecoin payment providers.

As Jose Fernandez da Ponte noted, it is unlikely that only USDT and USDC will remain. Since distribution is the most critical factor in stablecoin adoption, fintech and platform companies with large user bases and active economies will have strong incentives to issue their own stablecoins.

What must be considered is interoperability among stablecoins. It’s not just about making different versions of USDC on Ethereum, Solana, or Base compatible—it’s also about making different types of regulated stablecoins interoperable.

In the real economy, dollars held at Wells Fargo and dollars held at Chase are interchangeable because interbank settlement exists. If in the future we see a proliferation of stablecoins—such as USDC, PYUSD, MetaUSD, GoogleUSD—then new forms of settlement layers or liquidity distribution infrastructure will be required to enable smooth interoperability among different types of stablecoins.

Ultimately, utility is the key to a stablecoin’s survival. Even if issuance is tightly regulated, if the coin isn’t used in the market, it is worthless. We’ve already seen this play out—Japanese bank-issued stablecoins have extremely low usage, and even within the MiCA framework, Societe Generale’s EURCV sees far less adoption compared to Circle’s EURC.

Bank-issued stablecoins often suffer from limited scalability across international and on-chain environments due to excessive regulatory constraints. As a result, they fail to fully leverage the fundamental strengths of stablecoins and are often seen merely as digital extensions of bank deposits—resulting in slow adoption.

To ensure success, stablecoin issuance should be capital markets–oriented. If issued by non-bank entities, the regulatory frameworks of MiCA, MAS, and the Genius Act should be referenced to ensure user protection. Stablecoins should then be deployed in use cases that capitalize on their inherent advantages, enabling genuine market utility and growth.

Dive into 'Narratives' that will be important in the next year