In the past, banks relied on physical certificates and suffered large-scale bankruptcies due to inefficient intermediary structures. Today’s financial system still inherits this complexity, operating under an indirect ownership model. As tokenized assets and stablecoins emerge as a new core of global finance, banks are approaching a moment where transformation is no longer optional but necessary.

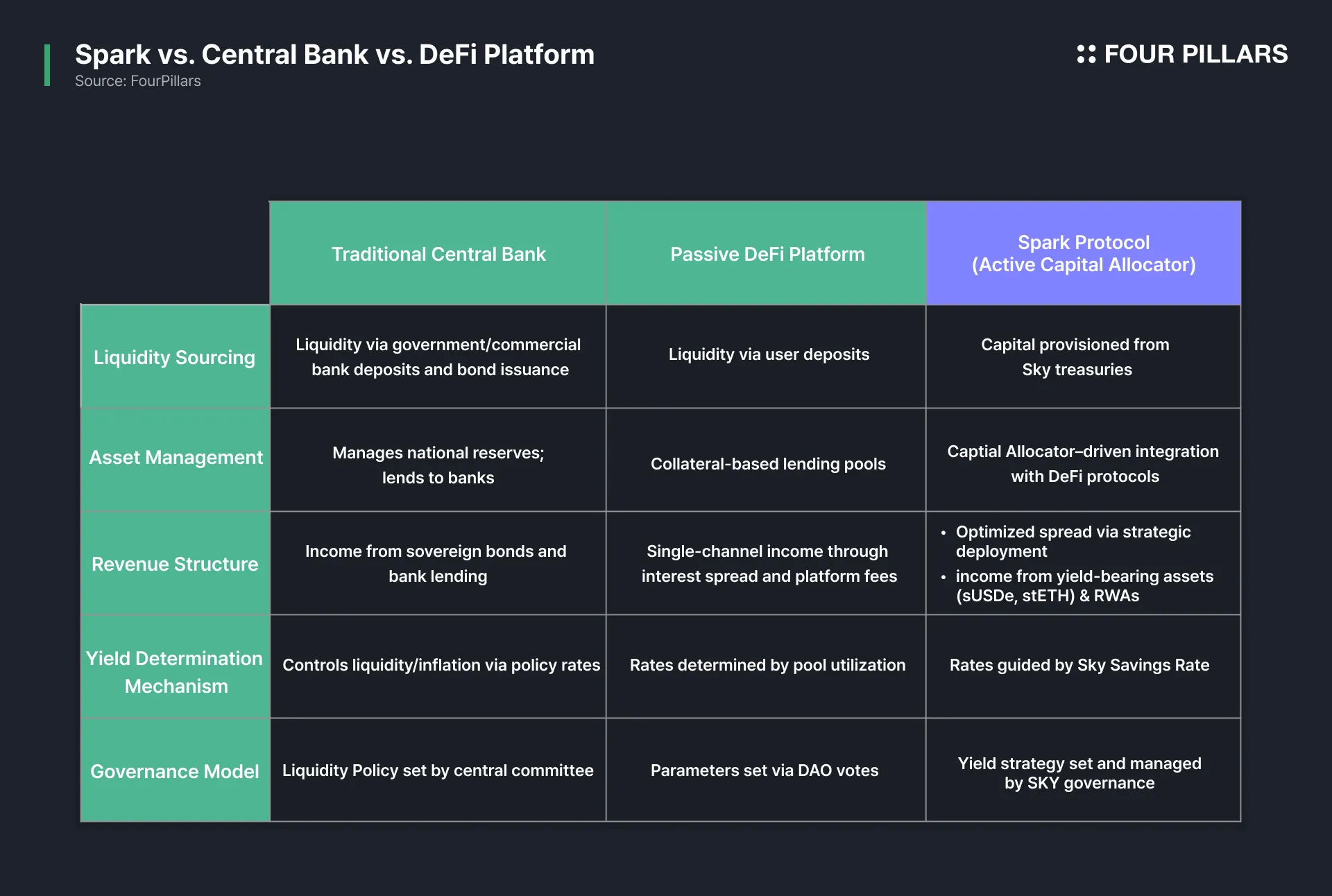

Spark’s vision is to address the inefficiencies of traditional banking and the scalability constraints of existing DeFi money markets, positioning itself as the most advanced on-chain yield engine. To realize this vision, Spark operates the Spark Liquidity Layer (SLL), which automates asset allocation, and SparkLend, a low-cost, high-liquidity lending market.

The Spark Liquidity Layer (SLL) functions as an on-chain asset management engine that continuously monitors liquidity conditions, DeFi protocol yields, and reserve levels in real time, executing automated rebalancing. Spark currently allocates capital strategically across both DeFi protocols (Morpho, Aave, Ethena) and RWAs (BUIDL, Superstate), managing over $4.1 billion in assets and generating more than $190 million in cumulative returns.

SparkLend operates a fixed-rate lending market backed by capital sourced from Sky, enabling high capital efficiency through the use of sUSDS as collateral. Under this structure, SparkLend has surpassed $3.4 billion in TVL.

Spark’s strategy is not necessarily groundbreaking, but it creates a structural advantage that is difficult to replicate through low-cost capital sourcing and sophisticated capital deployment. As demonstrated by the stable yield payout of sUSDS, its ability to consistently deliver high rewards helps establish a favorable environment for attracting large-scale capital.

The banking industry is once again at a structural turning point. To understand this moment, it's worth revisiting the history of banks. Banks emerged during the rise of commercial capitalism. In 17th-century England, goldsmiths stored customers’ gold and issued deposit receipts, which began to circulate as money. These receipts eventually served as collateral for credit creation, laying the foundation for the modern banking system. With the establishment of central banks, financial institutions became the core infrastructure for asset custody, lending, and payments. Later, the Industrial Revolution led to the separation of commercial and investment banking, and by the late 20th century, the role of banks expanded from physical branches to digital banking and global financial networks.

Despite these changes, the core function of banks has remained the same: to serve as intermediaries that store surplus capital and redistribute it to areas of demand, thereby maximizing capital efficiency. However, the methods and tools have continuously evolved to match the prevailing technologies and financial environment.

Now, as tokenized assets and stablecoins reshape the financial landscape, is it time for banks themselves to undergo another transformation?

"Yes, you can save, borrow, and lend with Spark. No, it’s not a bank."

— Spark

This article introduces the Spark Protocol, which presents an on-chain capital allocator optimized for the evolving financial landscape of DeFi. In the following sections, we take a closer look at how Spark operates and explore how it differentiates itself from traditional banking models in terms of capital efficiency.

Source: Market Memoir - the floor of the New York Stock Exchange after closing

In the 1960s, Wall Street experienced a major boom. Low interest rates, attractive dividends, and increased institutional participation led trading volumes to quadruple between 1960 and 1968. Yet by 1969, many brokerages were on the verge of collapse, even as the bull market continued. The reason was surprisingly simple: the paper-based infrastructure could no longer keep up.

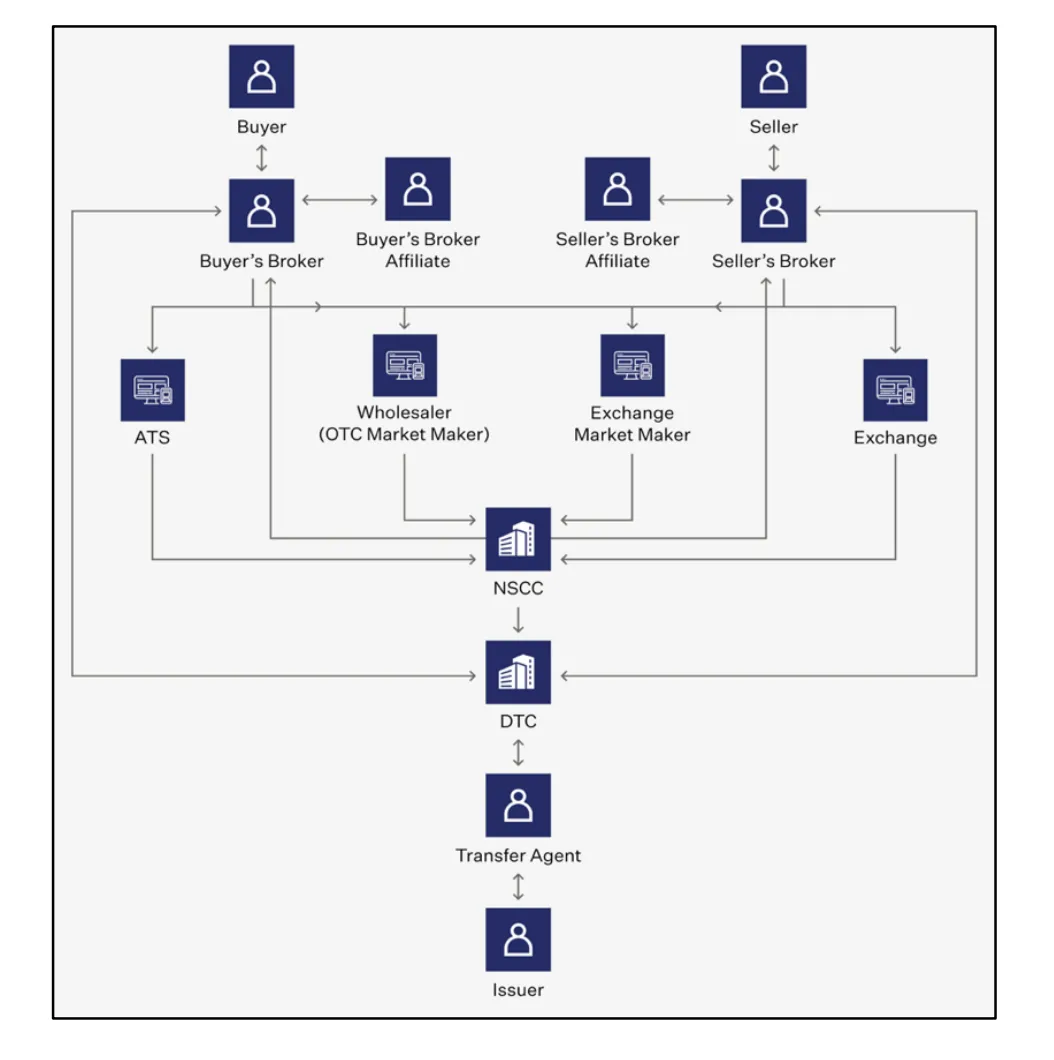

Before modern settlement systems, stock ownership was transferred through the physical exchange of paper certificates. Sellers would hand certificates to their broker, who would pass them to the buyer’s broker, who would then forward them to the issuing company’s transfer agent. The agent would record the change in its shareholder registry, cancel the old certificate, and issue a new one. This multi-step process could involve up to 68 discrete actions and take around four business days to complete.

As trading volumes soared, the settlement process fell behind. The result was billions of dollars in unsettled trades, millions in lost certificates, and failures to pay out dividends. Several brokerage firms suffered severe liquidity crises, with some misappropriating client assets to meet obligations or repurchasing shares in the open market to cover gaps. These practices were overlooked during the bull market, but once the market declined in the late 1960s, fee revenue collapsed and many firms were unable to manage the accumulated burden. The Paperwork Crisis became one of the most severe post-Depression financial infrastructure failures, eventually triggering a shift to the indirect ownership model that prevails today.

Source: Crypto and the Evolution of the Capital Markets

Following the Paperwork Crisis, the capital markets moved away from physical certificates and adopted the indirect ownership model. In this system, securities are not legally owned by investors themselves, but by brokers or custodians. Ownership transfers are recorded not by changing the name on a physical certificate, but by updating internal ledgers within intermediaries.

While this system improves transactional efficiency, it also entrenches structural complexity and intermediated control.

First, the process of settlement is no longer straightforward. What could be a direct transaction between buyer and seller now involves multiple parties such as brokers, dealers, market makers, exchanges, clearinghouses, and central depositories. Each performs a narrow function, often in a siloed or overlapping manner, increasing friction and cost. Moreover, these intermediaries extract fees, spreads, and data rents at multiple points along the transaction path.

Second, the indirect model consolidates the flow and control of transaction data into the hands of a few intermediaries, introducing informational asymmetry and opacity. Since investors are not the legal owners, they often lack real-time visibility into their holdings or execution pathways. Meanwhile, intermediaries can commercialize this information by limiting access or monetizing it through premium services.

In this architecture, intermediaries are no longer just service providers. They become economic stakeholders embedded within the structure of the transaction itself. The result is a financial system where intermediated complexity and value extraction increase transaction costs and reduce overall efficiency.

Spark was created to solve the systemic inefficiencies and opacity of traditional banking. However, the idea of overcoming the limitations of legacy financial systems through DeFi is not entirely new. Since the early days of DeFi, countless protocols have pursued common goals such as peer-to-peer transactions, automated settlement, and transparent data access.

However, existing money market models are structurally limited. They primarily serve as intermediaries between borrowers and lenders without integrating finanical hub functions such as yield rate policy, capital allocator management, or risk diversification into a unified system. As a result, it becomes difficult to design a cohesive flow between yield and borrowing costs or to enhance return on capital. For users, this often translates to limited access to predictable and sustainable yields.

Spark differentiates itself by implementing a unified financial architecture built around its own on-chain capital allocator, designed to improve both capital efficiency and system stability. Spark sources low-cost capital from Sky and allocates it strategically across major protocols such as Morpho, Aave, Ethena, BUIDL, and SparkLend. These assets are autonomously managed through off-chain monitoring software that evaluates yield, risk, and efficiency. Revenue generated from these deployments compounds to sUSDS holders, a yield-bearing stablecoin minted through Spark Savings using USDS, USDC, or DAI.

This architecture enables Spark to transcend the passive role of traditional money markets and operate as an active capital allocator across DeFi. This, in turn, brings in more liquidity, attracts institutional capital, and realizes economies of scale. As of Q2 2025, Spark has reached over $7.5 billion in TVL.

The following sections explore the relationship between Sky and Spark as its Stars (aka SubDAOs) and provide a detailed look at SparkLend and the Spark Liquidity Layer (SLL), the core engines that power Spark’s on-chain financial stack.

Source: X (SkyEcosystem)

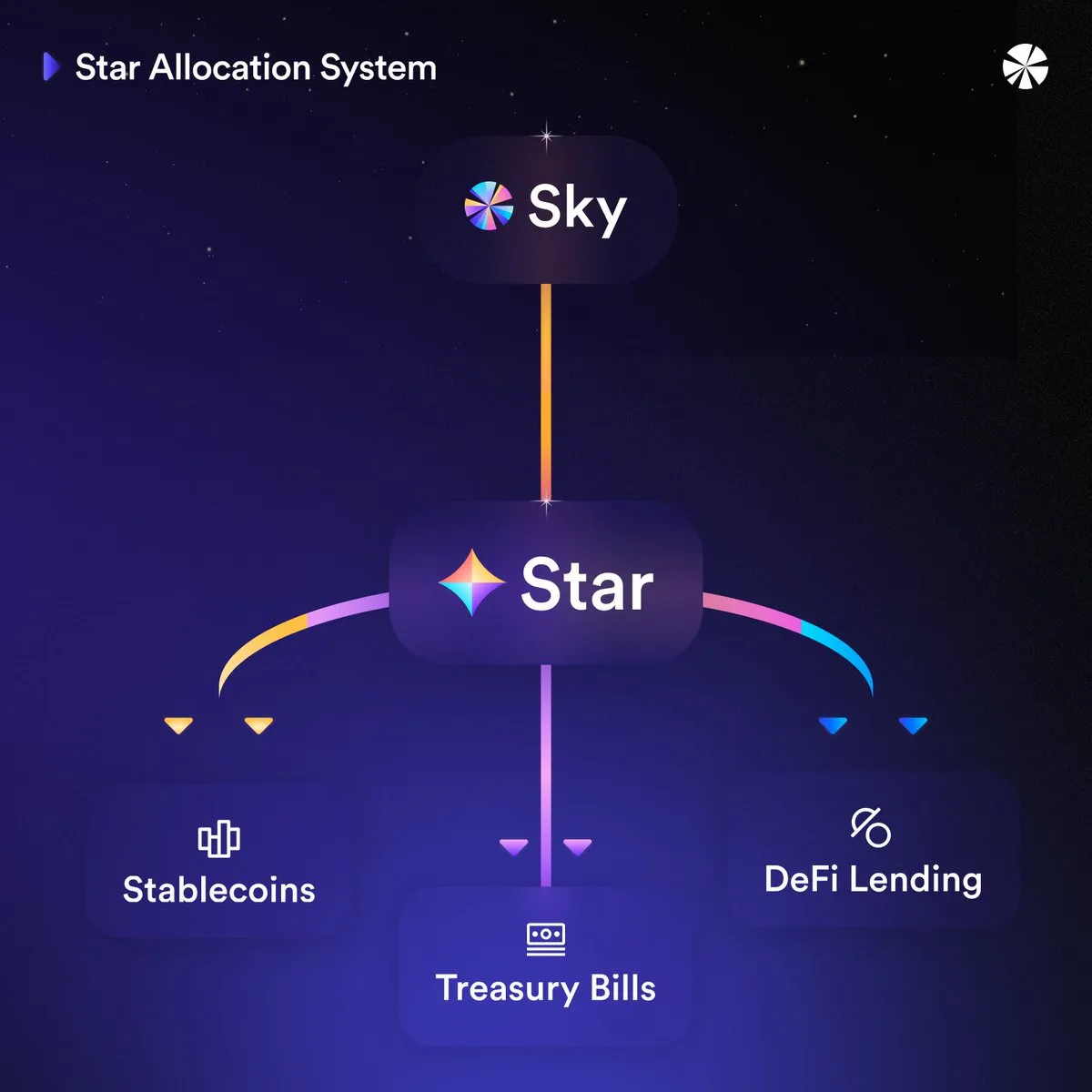

Spark functions as a Star within Sky (formerly MakerDAO) and serves as the first Star, an autonomous unit in Sky’s broader ecosystem of Stars. Sky is a decentralized, reserve-backed protocol that has issued USDS (formerly DAI) and governed rates since 2017. As part of its effort to diversify asset deployment and revenue generation, Sky launched the Star initiative with Spark leading as the inaugural Star responsible for deploying capital into both on-chain and off-chain assets, including RWAs, to generate yield.

While Spark is independently managed, its capital structure and strategic direction are closely linked to Sky. For instance, the initial capital used to power Spark’s lending markets and capital allocation engine was sourced directly from Sky. As such, Spark’s borrowing rates, fee structures, and revenue flows are fundamentally tied to Sky’s reserves. To understand Spark's architecture, it is essential to first examine SSR and the mechanics of USDS.

3.1.1 SSR & Spark Savings

The Sky Savings Rate (SSR) is the base deposit rate defined by Sky governance, representing the annual yield rate applied to USDS deposits. Unlike the variable rates common across DeFi, which fluctuate based on liquidity conditions, SSR is set through governance voting.

Specifically, Sky’s risk management team proposes adjustments to SSR based on market conditions and protocol revenue. These proposals are reviewed and ratified by the community through on-chain voting. This process gives Sky flexibility to align its rate policy with macroeconomic conditions, independent of short-term liquidity pressures.

Source: Spark Data Hub – Savings

The SSR is funded by Sky’s protocol revenue, which is generated from a combination of RWA investments (e.g., U.S. Treasuries) and DeFi deployments through Spark. This clearly illustrates the link between Sky and Spark: Spark is not only a yield-enhancing engine within DeFi but also a crucial revenue source supporting Sky’s SSR. In fact, Sky currently generates over $400 million annually from its reserves, with 25% of that revenue originating from SparkLend and SLL, and the remainder from RWA strategies like Treasuries.

Source: Spark Data Hub – Savings

While SSR serves as the yield source, Spark Savings acts as the front-end interface for users. Users can deposit USDS or USDC and receive sUSDS or sUSDC in return, which are yield-bearing assets that automatically compound yield based on the SSR. This means the value of sUSDS increases continuously in real time, reflecting the accrued yield. Spark Savings currently holds over $3.1 billion in total deposits.

3.1.2 USDS & Spark PSM: Multichain Peg-Stability Swap

As previously mentioned, USDS is the stablecoin issued by Sky. The relationship between USDS and Spark is defined by Spark’s role in expanding USDS utility. Specifically, Spark functions both as the conversion gateway that transforms USDS into sUSDS, a yield-bearing stablecoin, and as the deployment layer that allocates USDS into lending markets and its on-chain assets. This process generates yield and helps reinforce the stability of the USDS peg.

Spark also plays a critical role in maintaining USDS’s peg through the Spark PSM (Peg Stability Module). This module enables instant, slippage-free swaps between USDS, sUSDS, and USDC across multiple chains, including Ethereum, Base, and Arbitrum. For example, when a user redeems sUSDS for USDC, the PSM facilitates a 1:1 swap on the backend using pooled reserves, ensuring immediate access to USDC liquidity.

By supporting large-scale redemptions and seamless cross-chain asset transfers, Spark PSM mitigates slippage and liquidity fragmentation across networks. This is essential to maintaining stablecoin price parity during periods of volatility or high withdrawal demand.

Here’s how Spark PSM operates in detail:

Reserve Allocation: Large USDC reserves sourced from Sky are deposited into PSM contracts deployed across supported chains such as Base and Arbitrum.

sUSDS to USDC Redemption: When a user redeems sUSDS for USDC, the PSM burns the sUSDS and delivers the equivalent value in USDC from its reserves. The exchange rate reflects the SSR-accumulated yield, as determined by Sky’s Cross-Chain Savings Rate Oracle (e.g., 1 sUSDS = 1.05 USDC).

USDC to sUSDS Minting: When a user deposits USDC to mint sUSDS, the PSM receives the USDC and mints new USDS at a fixed 1:1 rate.

All conversions are executed at a fixed $1 peg, eliminating slippage and minimizing exposure to market volatility. Spark currently maintains over $100 million in USDC/USDS liquidity on Base through the PSM. With more than $1.3 billion in USDC reserves held by Sky, Spark plans to expand its multichain redemption infrastructure across additional networks. This will support seamless capital movement and uphold USDS peg stability as the SLL continues to scale and facilitate cross-chain liquidity allocation.

Source: SparkLend

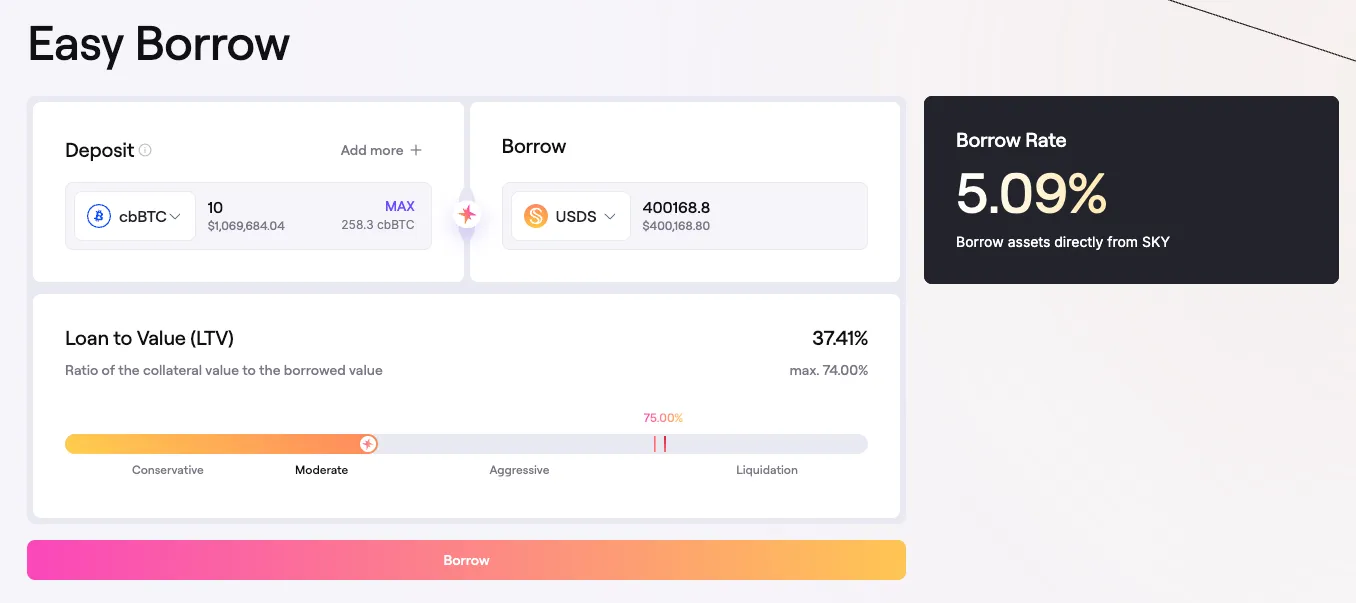

SparkLend is a lending protocol built as a fork of Aave v3, optimized to support large-scale borrowing through Spark’s Liquidity Layer (SLL) and its integration with Sky. Backed by low-cost USDS liquidity supplied by Sky, SparkLend is designed to offer highly competitive borrowing rates.

As with other overcollateralized lending protocols, SparkLend allows users to supply assets and earn yield, or post collateral and borrow assets. The borrow rate for each asset is determined algorithmically based on utilization: higher demand for borrowing pushes rates up, while lower demand causes them to fall. This inertia-based rate model enables autonomous balancing of liquidity across pools. (For USDS specifically, a fixed rate based on SSR is applied, as discussed below.)

While SparkLend structurally resembles other DeFi lending markets, it introduces unique elements through tight integration with Sky and customized collateral settings:

First, SparkLend limits supported collateral assets to enhance stability and reduce volatility risk. For example, SparkLend on Ethereum Mainnet supports only high-liquidity assets such as ETH, stETH, WBTC, USDC, USDS, and sUSDS. Each asset is subject to conservative loan-to-value (LTV) and borrow limits defined by Spark’s risk parameters. By narrowing the collateral universe, SparkLend reduces the chance of liquidation cascades or collateral failure during sharp market downturns, reinforcing protocol-wide stability.

Second, SparkLend applies a customized rate model to the USDS market that is directly linked to SSR. Unlike most markets where borrowing costs fluctuate with short-term liquidity conditions, SparkLend offers USDS borrowing at the fixed SSR rate set by Sky governance. This ensures predictable and consistently low borrowing costs for users who borrow USDS.

Third, SparkLend receives direct liquidity injections from Sky’s vaults. In practice, this means SparkLend’s USDS pool is continuously supplied with freshly minted USDS from Sky. These funds can be withdrawn or re-supplied dynamically, based on protocol demand. Moreover, when users deposit USDS into SparkLend, it is automatically converted into sUSDS, allowing users to simultaneously earn rewards through both the lending yield and SSR.

Source: Spark Data Hub – SparkLend

By leveraging its structural connection with Sky, SparkLend provides a highly predictable and capital-efficient borrowing market. The use of SSR-based fixed rate in the USDS market reduces uncertainty and supports long-term planning. Additionally, because sUSDS continues to earn yield even while being used as collateral, users can maximize capital efficiency without sacrificing yield.

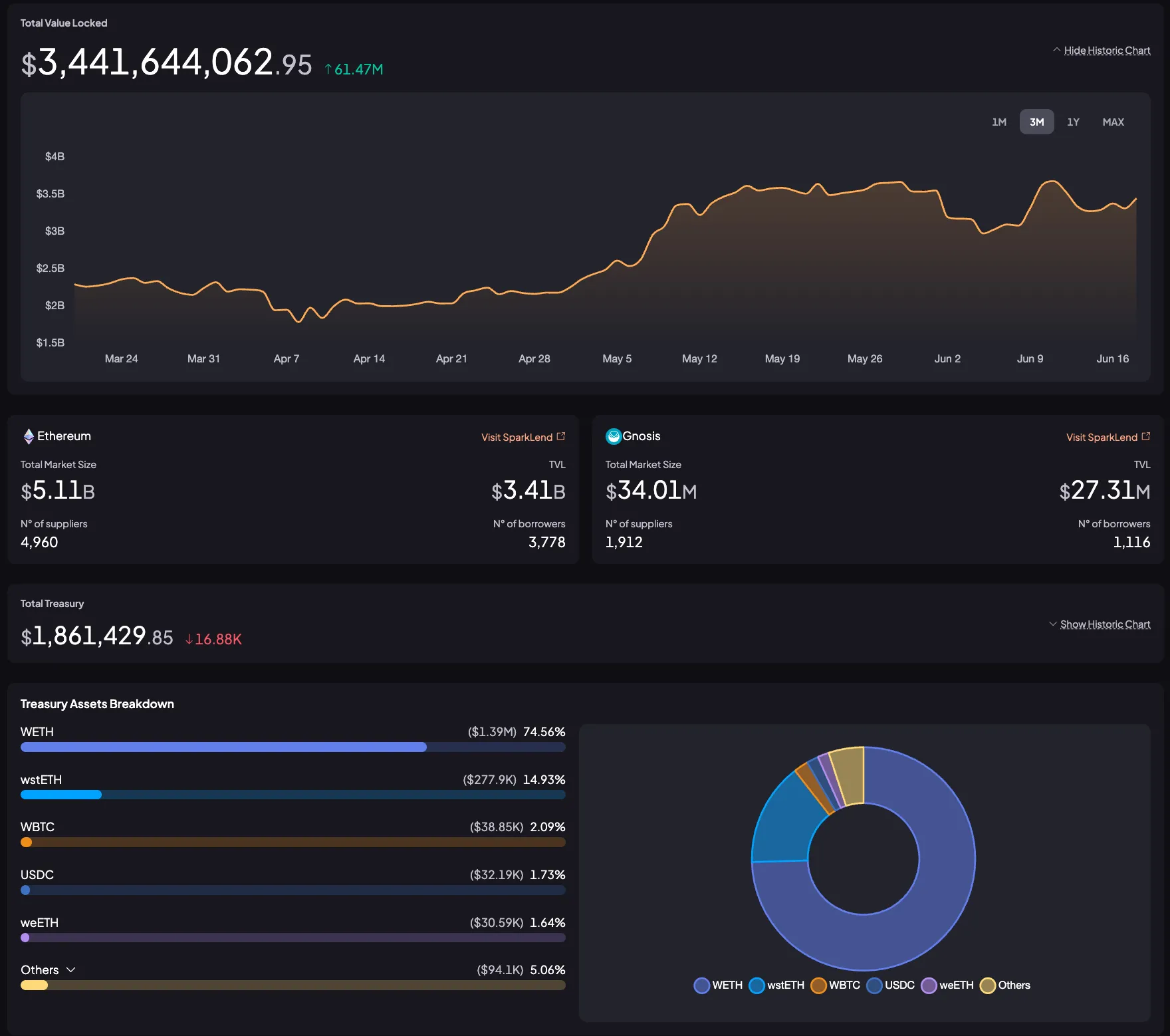

As of Q2 2025, SparkLend has reached over $3.4 billion in TVL, and the Treasury holds approximately $1.8 billion. Notably, the SLL—the capital allocation engine behind Spark—has generated over $190 million in cumulative revenue, with SparkLend contributing 62% (approximately $120 million), making it the single largest source of earnings within the Spark ecosystem.

3.3.1 How SLL Works

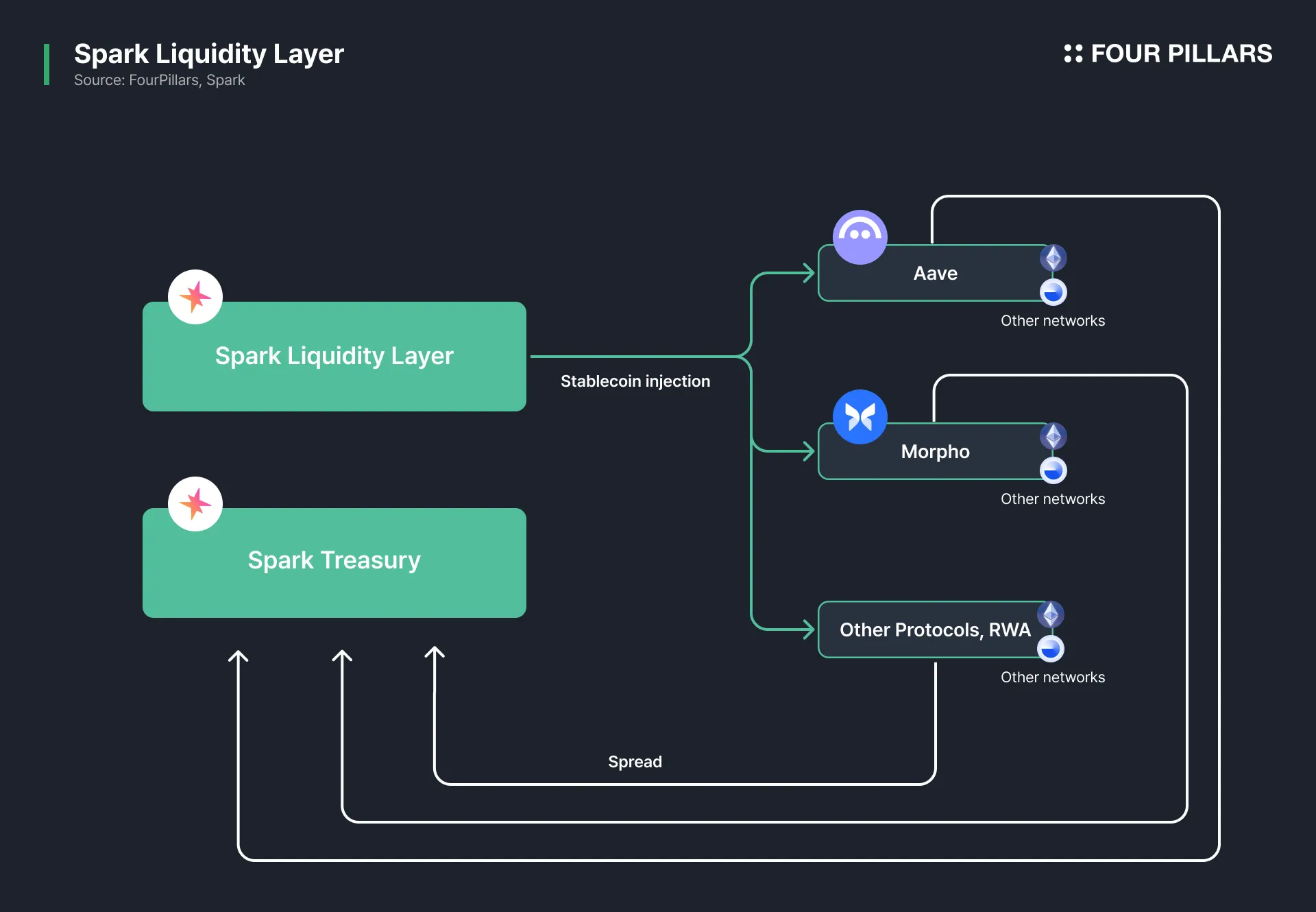

The SLL is the core system that defines Spark’s role as an “active capital allocator for DeFi.” It serves as Spark’s on-chain capital allocation engine, sourcing low-cost liquidity from Sky and deploying it across multiple chains and DeFi protocols. The yield generated through these deployments is returned to Sky’s treasury, which means that SLL functions as both the funding source for yields on USDS and sUSDS and the financial foundation that supports SSR payouts.

SLL does more than allocate capital. It is integrated with off-chain monitoring software that continuously observes liquidity conditions across chains, yield performance from external DeFi protocols, and Sky’s reserve levels. Based on these metrics, SLL automatically rebalances liquidity in real time. For instance, if deposits into the PSM on Base increase sharply and the USDC balance becomes insufficient, the system will bridge additional USDC from Ethereum mainnet using CCTP. If there is excess idle USDC on a layer 2 network, a portion is withdrawn and reallocated to mainnet.

SLL operates through three main components:

Sky Allocation Vault: This vault serves as a credit facility that allows Stars, including Spark, to mint USDS against Sky’s collateral. Currently, more than 4.5 billion dollars worth of USDS (formerly DAI) has been issued through Spark’s vault. The funds secured at low cost are then used by SLL for strategic capital allocation across DeFi.

SkyLink: SkyLink is a native cross-chain bridge developed by Sky. It facilitates the transfer of USDS and sUSDS across supported networks. This enables SLL to automate fund movement between chains quickly and securely, without relying on intermediaries. For the movement of external stablecoins such as USDC, SLL uses Circle’s Cross-Chain Transfer Protocol (CCTP) to ensure efficient liquidity routing.

Spark PSM: As previously explained, the Spark Peg Stability Module allows instant and slippage-free swaps between USDS, sUSDS, and USDC on each chain. During the rebalancing process, it helps SLL execute asset conversions without price deviations, preserving peg stability and minimizing liquidity loss.

Source: Spark Data Hub - Spark Liquidity Layer

Spark uses this infrastructure to deploy billions of dollars across a wide range of DeFi protocols and asset types. These deployments are fully transparent, and information such as asset allocation, SparkLend TVL, and protocol-level revenue is available through the Spark Data Hub.

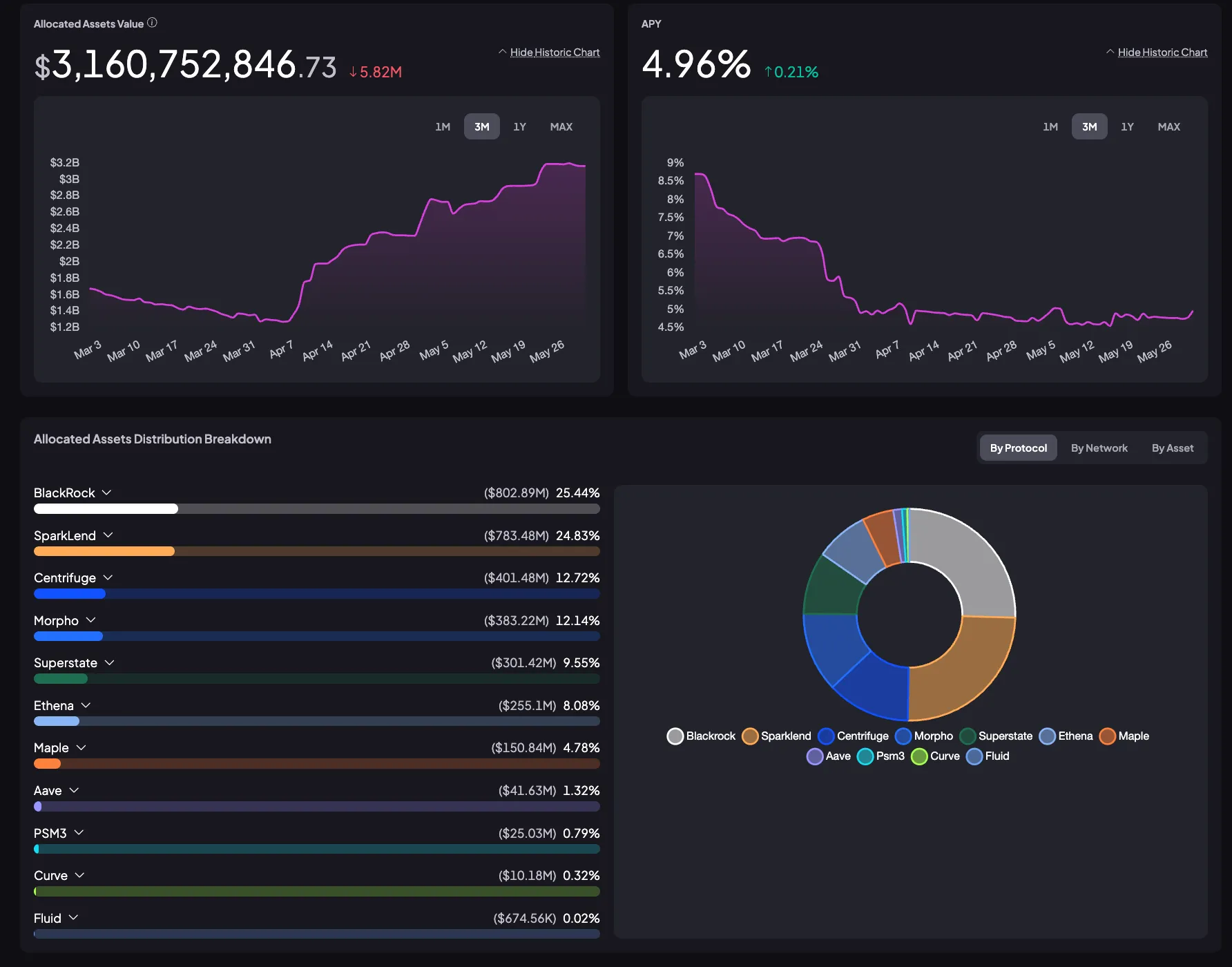

According to the latest data, over 3.1 billion dollars has been allocated across DeFi strategies. Among these, BlackRock (via BUIDL) accounts for $800 million and SparkLend for $900 million, representing the largest shares. Spark allocates liquidity to BUIDL to access Treasury-backed yields and generates additional revenue through deposit yield on SparkLend, its own lending platform.

SLL’s revenue sources are well diversified. Rather than depending on a single stream, it combines stable returns from real-world assets with higher-yield strategies native to DeFi. On the RWA side, Spark provides liquidity to tokenized Treasury products such as Superstate, Centrifuge, and Maple. These positions generate reliable income based on U.S. government bonds. On the DeFi side, Spark partners with protocols like Ethena, Morpho, and Aave to pursue yield opportunities with higher upside potential. These include direct exposure to synthetic yield-bearing assets such as sUSDe, as well as more complex vault-based deployments through Morpho.

Source: Spark Data Hub - Spark Liquidity Layer

As a result of this multi-pronged strategy, SLL has generated more than 190 million dollars in cumulative revenue. Among that revenue, SparkLend accounts for approximately 62%. This demonstrates that Spark has built an internal yield engine that does not rely solely on external protocols.

Morpho vaults represent the second-largest contributor, generating 29% of total revenue. This performance confirms that Spark is functioning effectively as an active central bank for DeFi. The next section will explore how Spark integrates with a wider range of protocols and expands its role within the broader ecosystem.

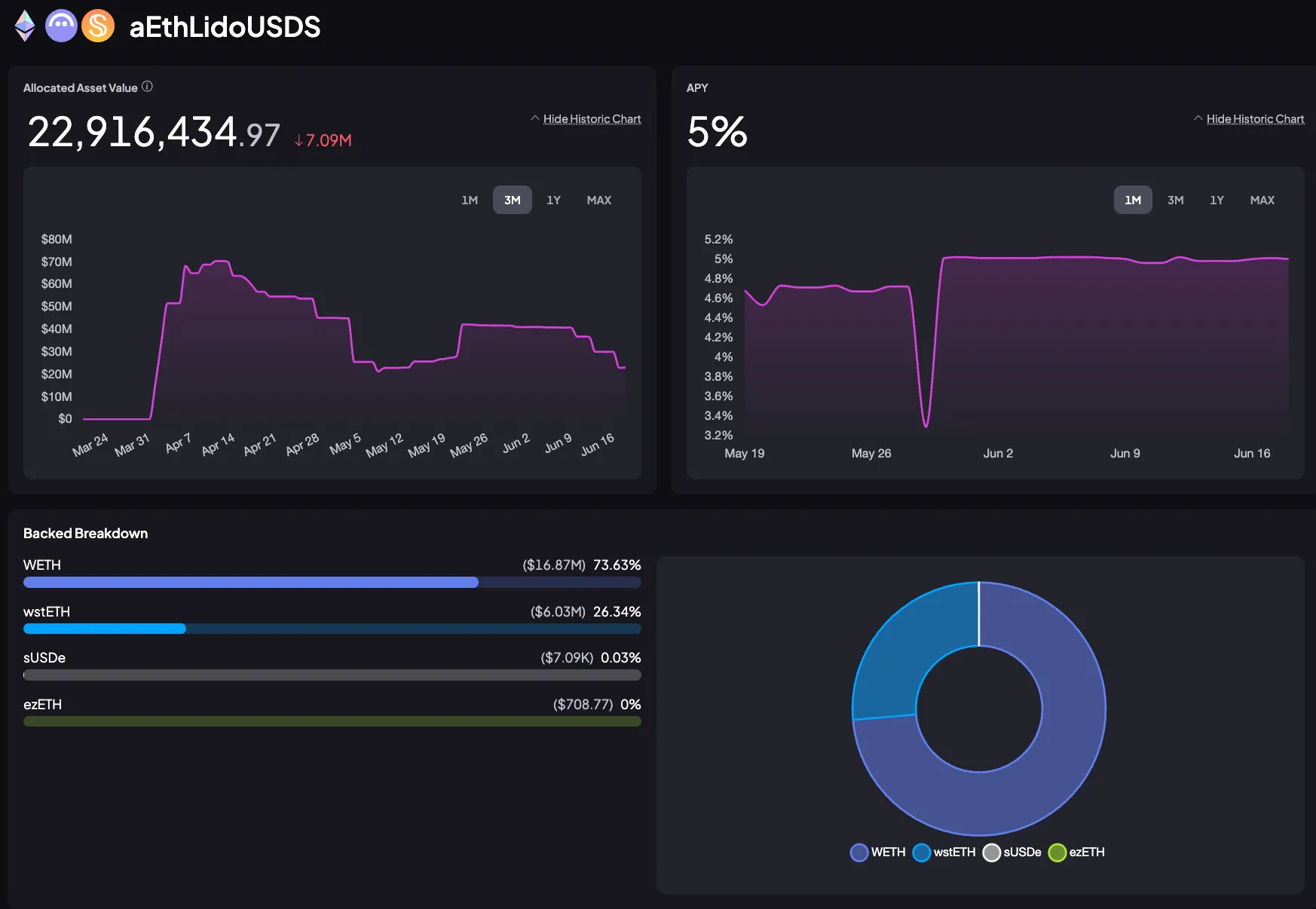

Source: Spark Data Hub - aEthLidoUSDS

Through SLL, Spark supplies USDS liquidity to Aave’s Lido market. This allows users to borrow against assets such as WETH and wstETH. In this process, Spark acts as the liquidity provider and earns yield on loans. Currently, approximately $20 million worth of ETH-based assets are deployed in the Aave market, generating a cumulative yield of $400K.

One of the core advantages of SLL integration is its ability to stabilize stablecoin borrowing rates across Aave’s Core, Prime, and Base markets. When borrowing rates rise in a particular market, SLL dynamically rebalances liquidity to reduce rate disparities. This mechanism increases rate predictability and stability across Aave, while enabling Spark to earn sustainable yields through active liquidity provisioning.

Spark leverages the Morpho protocol to maximize returns from liquidity provision. Liquidity is directly supplied to MetaMorpho vaults, creating a variety of lending markets. Currently, approximately 400 million dollars in USDC and 500 million dollars in DAI have been deposited into Spark-managed vaults.

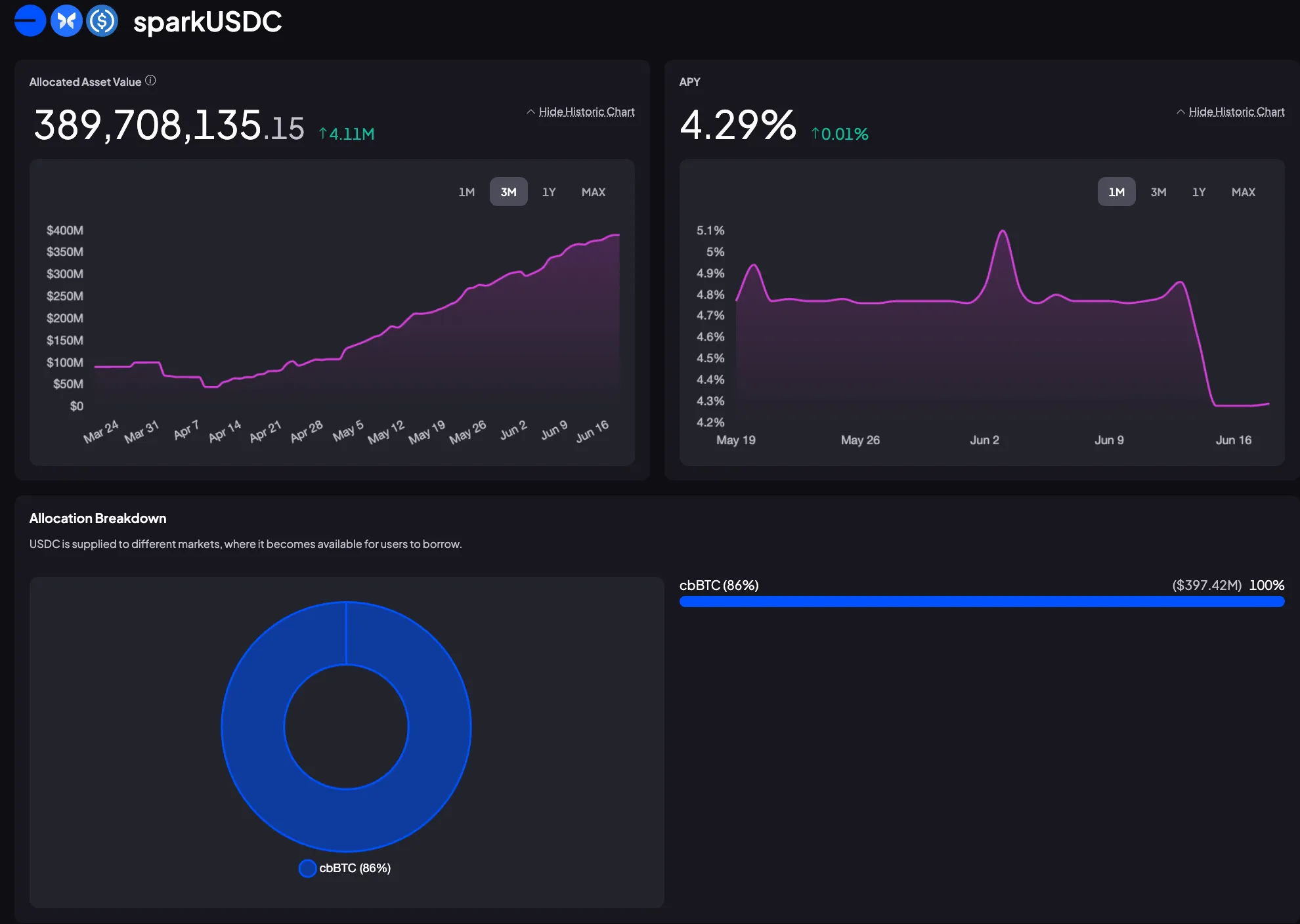

Source: Spark Data Hub - sparkUSDC

Most of the USDC liquidity is allocated to the cbBTC/USDC market, where users can borrow USDC against cbBTC (Coinbase Wrapped BTC) as collateral. Through this market, Spark earns yield on its deployed USDC, generating around 1.5 million dollars in revenue over the past year.

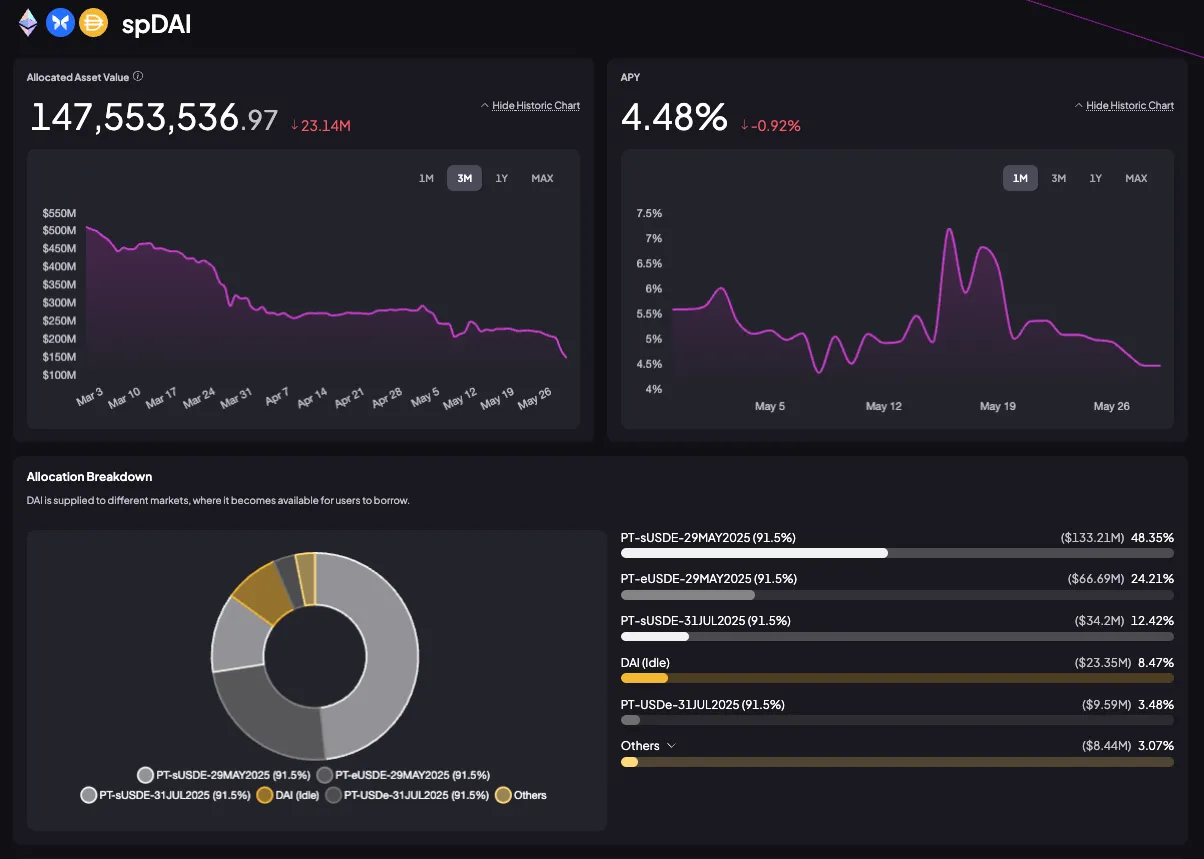

Source: Spark Data Hub - spDAI

Meanwhile, DAI liquidity is deployed on Morpho Blue, Morpho’s lending platform, alongside Pendle-based PT-USDS and other Ethena-based assets. Through this setup, users can borrow DAI using USDe or sUSDe as collateral. Since Ethena provides yield to USDe through delta-hedging strategies and RWA-based income, this pairing enables diverse yield strategies for DAI. Spark earns lending yield by supporting these high-yield collateral pools and has generated approximately 50 million dollars in cumulative revenue through these positions.

In the Ethena-integrated market on Morpho Blue, Spark accepts Pendle’s Principal Tokens (PT-sUSDe and PT-USDe) as collateral and supplies DAI liquidity accordingly. This lending structure was established by Spark assigning DAI to Pendle positions using capital sourced from Sky, as described in this governance post. This allows users to borrow DAI against PT-sUSDe and access fixed-yield collateral for capital-efficient borrowing.

This strategy enables users to earn staking yields from sUSDe, benefit from enhanced fixed yields via PTs, and simultaneously access leverage by unlocking additional liquidity. For Spark, this approach improves flexibility in capital allocation and improves protocol-level returns.

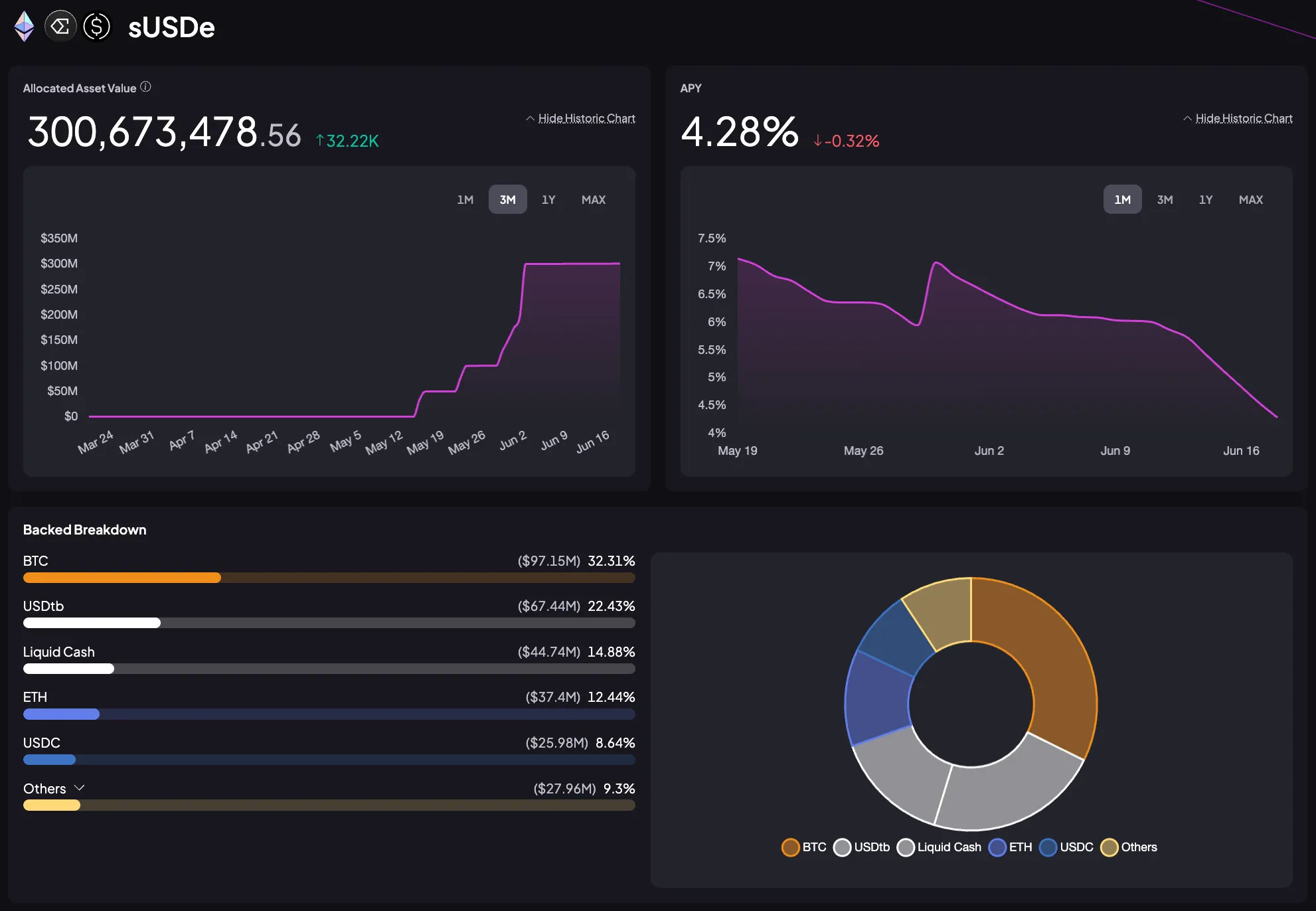

Source: Spark Data Hub - sUSDe

Spark is also expanding its direct exposure to Ethena’s USDe and sUSDe through SLL. The protocol plans to allocate up to 1.1 billion dollars to this strategy, and currently holds approximately 300 million dollars in USDe and sUSDe directly on its capital allocator. These high-yield assets, which have delivered an average APY of 18% in 2024, are being added alongside existing holdings like USDC, USDS, and sUSDS to enhance SLL returns.

Unlike indirect exposure through lending markets such as Morpho, this strategy allows Spark to receive rewards from Ethena directly without intermediaries. As a result, Spark can strengthen potential returns while minimizing external dependency. The cumulative yield generated so far amounts to approximately 1.5 million dollars.

As previously discussed, Spark functions as a unified financial hub through SparkLend and the SLL, addressing the limitations of both traditional banks and legacy DeFi money markets. But where does Spark derive its competitive moat that enables sustainable expansion? The answer lies in its integrated relationship with Sky, its competitiveness in yield-bearing stablecoins, and its operational efficiency through the SLL.

Source: SKY Ecosystem

Spark’s core advantage stems from Sky’s vast capital base and the low-cost funding structure it enables. As of now, Sky maintains approximately $11 billion in total collateralized assets, with $8.3 billion in USDS liabilities, maintaining an over-collateralization ratio of around 131%. This translates to $2.7 billion in excess collateral, which reinforces the financial soundness of the Sky ecosystem and underpins the capital operations of Stars like Spark.

This low-cost capital sourced from Sky is actively utilized across SparkLend and the SLL. SparkLend offers stable, fixed rates through the SSR, establishing a strong foundation for long-term user retention. Meanwhile, the SLL allows Spark to operate its capital allocator with high capital efficiency and minimal reliance on external liquidity.

The income generated through yield spreads and yield-generating asset exposure flows back to Sky’s SSR module as a financial backbone. A portion is also retained as Spark’s protocol revenue. This structure enables Spark to minimize its cost of capital while maintaining a stable revenue base, giving it a fundamental advantage over conventional DeFi protocols in both sustainability and asset efficiency.

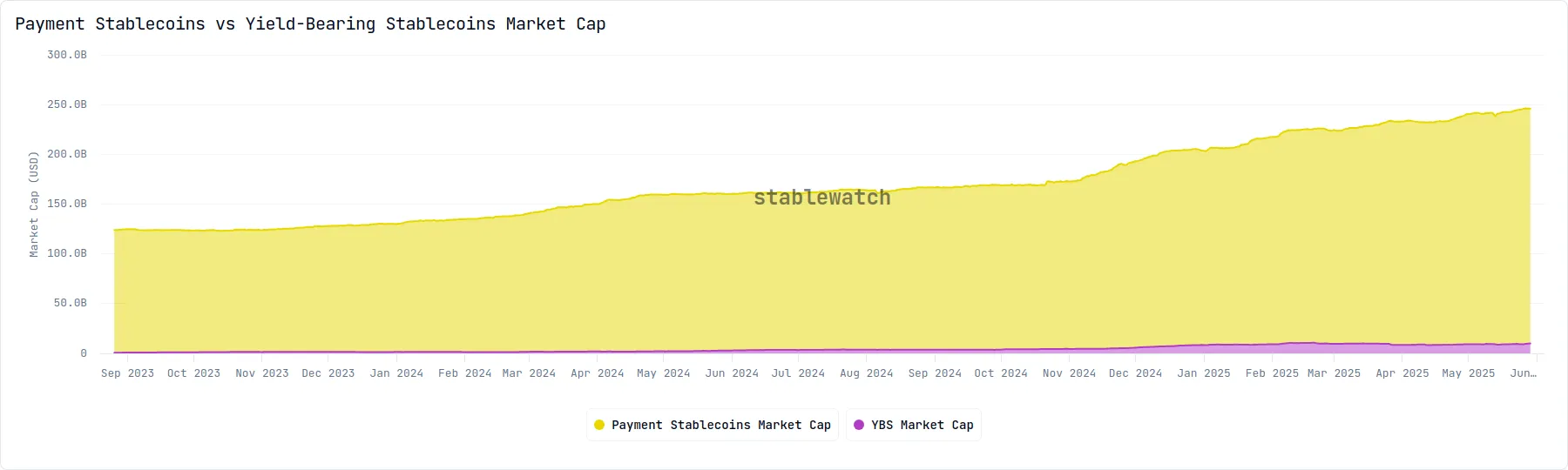

Source: Stablewatch

Yield-bearing stablecoins have emerged as an effective tool for enhancing capital efficiency in the stablecoin market. Since late 2023, the market has experienced rapid growth and reached approximately 10 billion dollars by the second quarter of 2025. This represents a nearly threefold increase in market capitalization over the past year.

In this fast-growing category, Sky’s sUSDS is demonstrating strong competitiveness in terms of yield distribution. According to Stablewatch, sUSDS has distributed over $82 million in yield to date, ranking second only to Ethena’s sUSDe in cumulative yield paid.

The key factor behind this performance is Sky’s rate competitiveness. The APY offered by sUSDS has typically ranged between 5 and 8%, which is comparable to the average 6% range offered by sUSDe during the same period. This attractive rate continues to drive demand for sUSDS deposits and in turn benefits Spark’s financial structure.

5.2.1 Enhanced Capital Capacity through sUSDS Demand

sUSDS is a yield-bearing token issued to users who deposit USDS into the SSR. As demand for sUSDS increases, more USDS is deposited into the SSR, leading to an expansion of Sky Treasury’s assets and an increase in SDS issuance. As the treasury grows, Sky gains greater capacity to supply low-cost capital to Spark, further strengthening Spark’s SSR-based lending capacity. This foundation enables SparkLend to offer below-market borrowing rates, reinforcing its rate competitiveness.

5.2.2 Expanded SparkLend Demand through Collateralization of sUSDS

SparkLend accepts sUSDS as collateral. This allows users to continue earning SSR yield while maintaining liquidity on their deposited assets. The dual benefit of yield and liquidity provides a strong incentive to use SparkLend.

As SparkLend incentivizes borrowing against sUSDS and sUSDS finds utility through SparkLend, a mutually reinforcing loop is created. An increase in users depositing sUSDS as collateral leads to higher TVL for SparkLend, which expands the protocol’s lending capacity. In turn, SparkLend can issue more loans and generate more revenue.

Ultimately, this feedback loop between sUSDS and Spark creates a virtuous cycle. Higher sUSDS deposits expand Spark’s treasury assets, which increases Spark’s capacity to access low-cost funding. This enables SparkLend to offer competitive lending rates, boost utilization, and increase protocol revenue. The resulting income flows back into the SSR, which can then offer more attractive APYs, further increasing demand for sUSDS and completing the cycle.

As real-world assets (RWAs) become tokenized and crypto assets integrate with traditional financial systems, the boundary between DeFi and TradFi continues to dissolve. Spark aims to achieve both high yield and low risk by balancing DeFi-native revenues with RWA-based returns.

5.3.1 DeFi-native Revenues

In the money market sector, Aave, and in the yield-bearing stablecoin space, Ethena, have emerged as formidable players. So how does Spark compete? Rather than entering direct competition, Spark adopts a capital-allocator-driven approach that reduces the need for head-to-head rivalry.

Today’s DeFi is increasingly characterized by what can be called “Fat DeFi,” where protocols focus on increasing composability. Spark aligns with this trend through the SLL, which is designed for optimal integration. It supplies liquidity to vaults such as Morpho, directly acquires yield-bearing assets from protocols like Ethena, and strategically exposes itself to Aave’s deep liquidity pools and large user base. This multi-channel strategy enhances Spark’s capital efficiency.

5.3.2 RWA Revenues

While DeFi’s open-source nature allows easy replication of code, the most defensible moats often stem from non-programmatic advantages. Spark’s deep alignment with traditional finance represents such a moat. While other protocols may replicate the technical infrastructure, replicating Spark’s revenue structure is far more difficult.

Spark’s Tokenization Grand Prix is a prime example of this. The initiative marked a major milestone in the convergence of DeFi and TradFi. Under the program, Sky committed $2 billion to purchase the most competitive tokenized short-term U.S. Treasury products. A total of 39 teams, including BlackRock, Janus Henderson, and Superstate, submitted proposals. The SLL ultimately purchased BUIDL, USTB, and JTRSY.

(For more details, see “Spark’s $2B Tokenization Grand Prix Redefines RWA in DeFi”)

The funds acquired by Sky consist of low-volatility, highly liquid assets backed by short-term U.S. Treasuries and comply with U.S. and European securities regulations. This provides a framework for institutional capital inflows into DeFi and strengthens the USDS peg and liquidity defense in the long run.

Spark’s strength lies in integrating DeFi’s flexible yield-generating strategies with the stability of RWAs through the SLL. On one hand, it seeks to increase revenue by engaging with external DeFi protocols. On the other, it reduces volatility by incorporating real-world assets such as U.S. Treasuries. In doing so, Spark redefines the relationship between DeFi and traditional finance as a continuous yield-stability spectrum, rather than two separate domains.

Spark’s north star is clear. It aims to become the most advanced yield engine in DeFi at scale, with the explicit goal of overcoming the opacity and inefficiency of traditional banking, as well as the scalability limitations of legacy money markets.

While Spark’s approach may not appear novel at first glance, its focus on mitigating capital costs and precisely managing exposure to yield-generating assets enables it to offer competitive rates and stable income. However, the ability to combine large-scale capital sourced through SSR with a capital-allocator-driven model across both DeFi and TradFi results in a structural moat that is difficult to replicate. As capital markets continue their on-chain transition, Spark may very well emerge as a hub for on-chain capital. It is worth closely observing how this thesis plays out.

Dive into 'Narratives' that will be important in the next year