Investment in cryptocurrencies remains complex and carries high entry barriers. Existing ETFs or financial firm models only allow exposure to a single asset, failing to meet the demand of investors who seek diversification or additional yield.

Mantle Index 4 (MI4) is designed as an institution-friendly product to fill this gap, holding major assets such as Bitcoin, Ethereum, Solana, and Stablecoins, while leveraging staked tokens to automatically generate yield.

Previous index tokens failed due to low yields and poor targeting of the right customer base. MI4 addresses this by adopting a built-in yield structure and an institution-focused design aligned with regulations.

If MI4 succeeds, it could become the blueprint for a “crypto index with yield.” For investors, this would provide a stable and efficient investment tool, and for the industry, it would bring long-term, reliable institutional capital.

For many investors, building a cryptocurrency portfolio is still a challenging task. In traditional finance, exchange-traded funds (ETFs) have made it possible to invest in a basket of assets with just one click, but crypto investors must self-custody their assets and sift through thousands of cryptocurrencies on their own. Constructing and managing a stable and diversified portfolio out of these thousands of tokens remains a highly complex task for most investors.

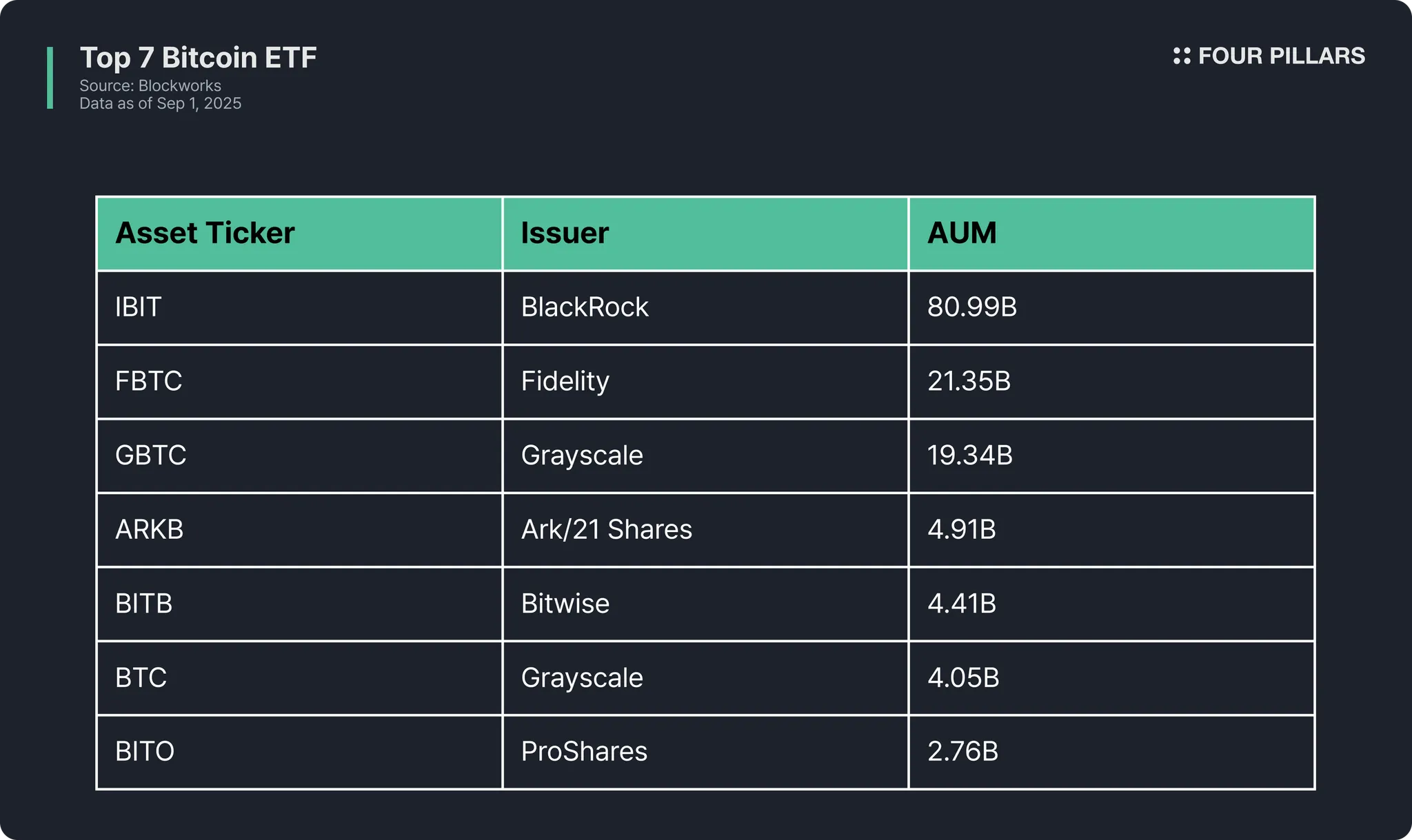

While traditional finance has simplified investing through index funds and ETFs, the crypto market still lacks proper alternatives. Recently launched ETFs such as BlackRock’s spot Bitcoin ETF (IBIT) or ProShares’ futures ETF (BITO) only provide exposure to a single asset, without additional yield or diversification benefits. Nevertheless, their success demonstrates the tremendous demand for regulated crypto investment. BlackRock’s IBIT, for instance, surpassed $52 billion in assets under management within just 18 months of launch. Still, these ETFs remain limited to tracking the price of a single cryptocurrency.

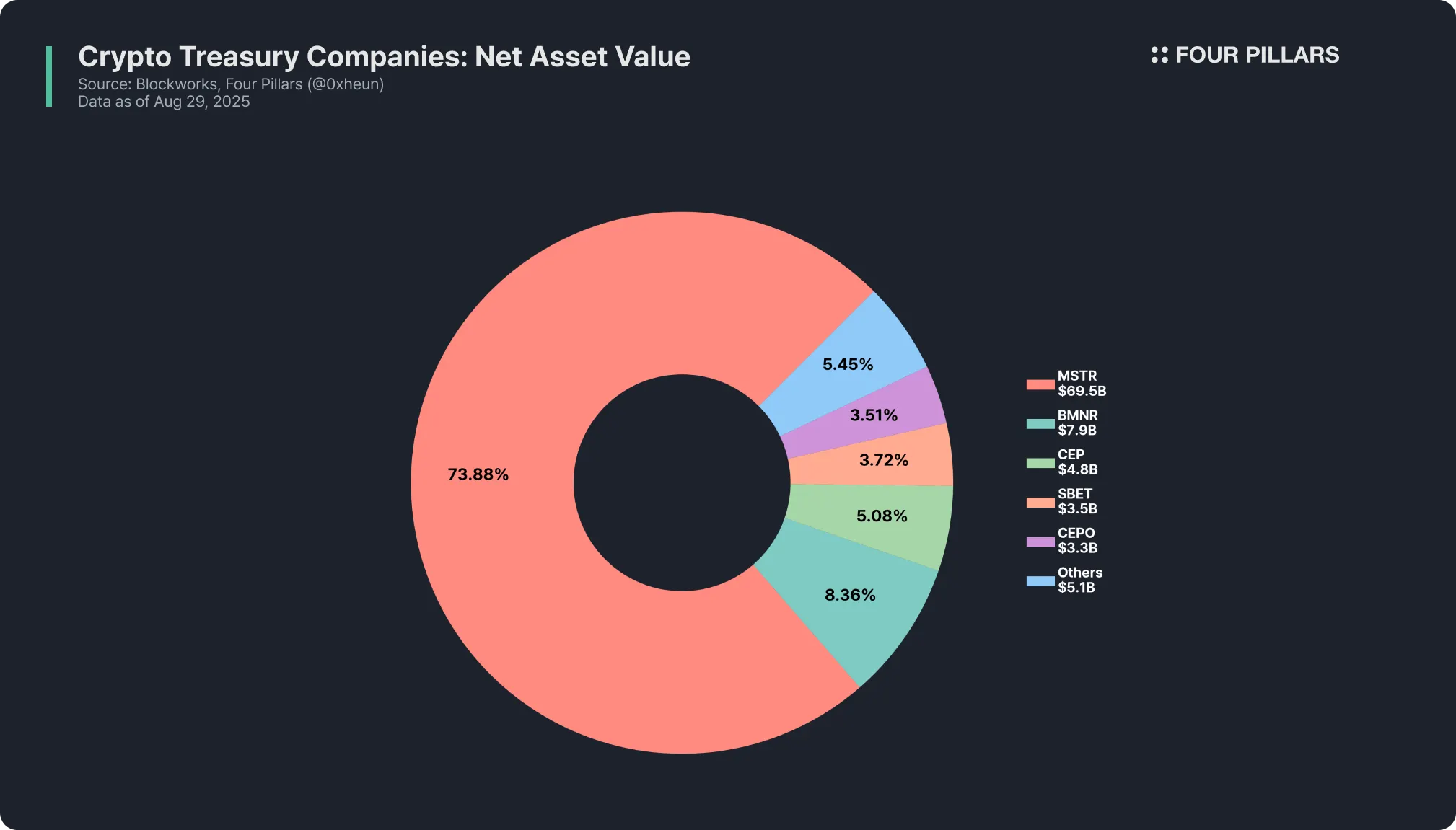

This thirst for regulated crypto exposure can also be seen in the rise of “crypto treasury companies.” Just as Strategy accumulated $70 billion worth of Bitcoin, effectively becoming a proxy stock for Bitcoin, other listed companies have begun accumulating alternative cryptocurrencies as treasury assets—for example, BMNR and SBET holding ETH, or UPXI holding SOL. By buying shares in these companies, investors can indirectly gain exposure not only to Bitcoin but also to major altcoins such as Ethereum and Solana through traditional markets. This trend highlights the market’s growing desire for crypto investment avenues beyond single-asset exposure.

However, the treasury company model is essentially nothing more than indirect exposure to a single asset and carries the structural risk of net asset value (NAV) premium collapse. This is not so different from the limitations of spot Bitcoin and Ethereum ETFs. In short, current alternatives still fail to meet the explosive demand from investors. With more than 80 cryptocurrencies exceeding $1 billion in market capitalization, the next step the market truly demands is the emergence of a genuine crypto index fund—one that offers diversified exposure across multiple assets, generates on-chain yield, and provides institutional-grade security.

Mantle Index Four (MI4) was designed to fill this gap in the market. According to Mantle, MI4 is an “institution-grade crypto product capable of generating its own yield within a traditional fund structure.” In other words, MI4’s mission is to act as a bridge between DeFi and traditional finance, offering investors both broad exposure (beta) to the crypto market and additional yield opportunities.

Supporting this vision and stability, Mantle Treasury committed up to $400 million as an anchor investor in MI4 through a governance proposal. The newly established investment firm Mantle Guard Ltd. will manage these assets, while global real-world asset (RWA) tokenization platform Securitize is responsible for tokenizing the fund’s shares. Through this setup, MI4 ensures the level of trust and transparency required by institutional investors.

MI4 offers a passive investment (set-it-and-forget-it) solution that allows investors to build and hold a diversified crypto portfolio without the burden of managing private keys or hand-picking individual cryptocurrencies. Beyond simply tracking the market, MI4 incorporates DeFi-native yield-bearing assets such as mETH, bbSOL, and sUSDe, aiming to capture potentially higher interest rates.

Moreover, share tokenization via Securitize goes beyond mere proof of ownership. Tokens issued on the Mantle Network could eventually be used in on-chain collateralized lending or compliant secondary trading among qualified participants. Ultimately, MI4 seeks to become a “new financial primitive” that bridges traditional and decentralized finance, positioning itself as a yield-enhanced benchmark for the crypto market.

2.1.1 Composition of the Index Fund

Source: Mantle Index Four Fund

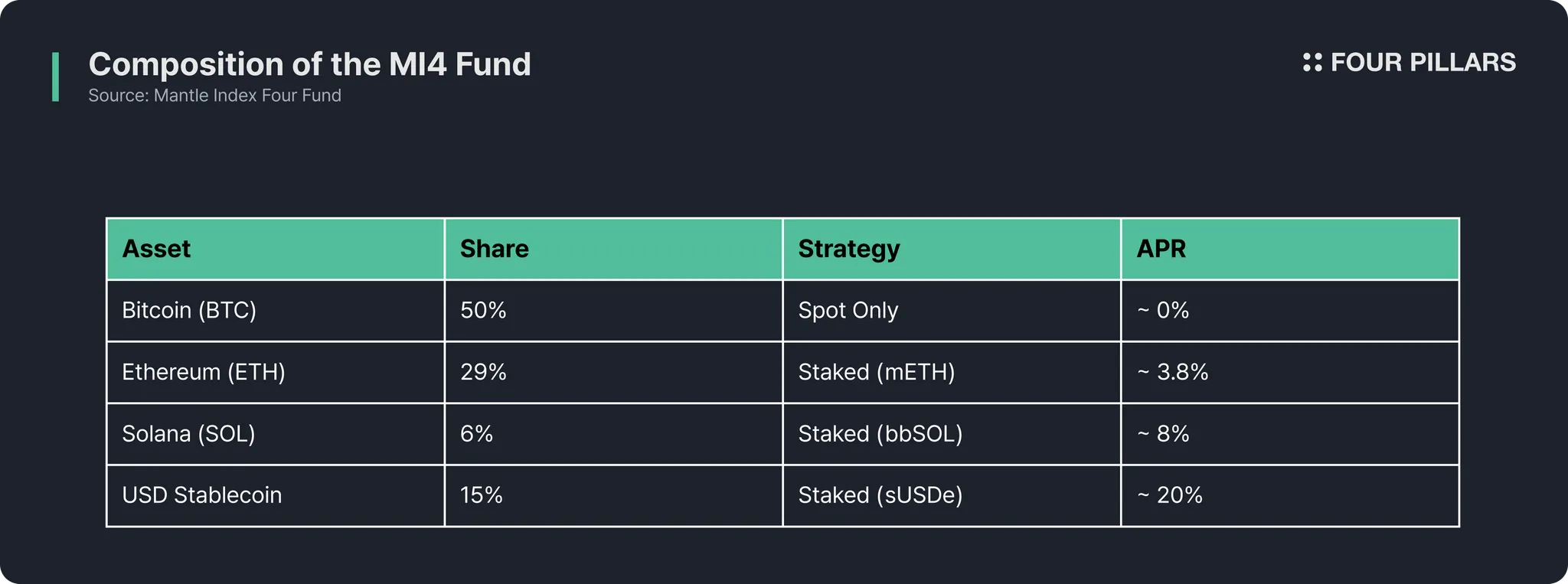

MI4 follows a traditional fund structure (BVI Limited Partnership) while internally employing on-chain strategies to maximize yield. The fund is composed of four major crypto assets selected based on market capitalization and risk factors. With the exception of BTC, all assets are held in yield-bearing token form. In other words, instead of simply holding spot assets, MI4 holds Mantle’s mETH (staked ETH derivative), Bybit’s bbSOL (staked SOL), and Ethena’s sUSDe (yield-bearing USD stablecoin). This approach not only generates stable staking income but also addresses liquidity and compliance concerns.

The core of MI4 lies in enabling investors to diversify into market-leading assets while earning additional on-chain yield—without the need to self-custody private keys or manually select tokens. In practice, this means that rather than just tracking the prices of Bitcoin and Ethereum, MI4 can generate an additional 5–6% annual yield through staking.

In this sense, MI4 fundamentally differs from a “vanilla ETF,” which merely holds assets without producing extra returns and therefore misses out on significant opportunities. MI4 systematically captures these opportunities and converts them into investor profits, making it a more active and efficient crypto investment solution.

2.1.2 Fund Operators

To ensure trust and stability, Mantle has partnered with top-tier institutions:

Mantle Guard Ltd.: Investment manager, strategy execution, and quarterly rebalancing

Securitize: Regulated tokenization platform, responsible for fund administration and tokenization of fund shares on the Mantle Network (allowing investors to hold their shares in digital token form)

KPMG: Auditor, ensuring transparency and credibility

Fireblocks: Digital asset custody solutions

Securitize brokerage & transfer agents: Investor onboarding and regulatory compliance (participation limited to accredited/non-U.S. investors)

Notably, the Mantle DAO Treasury has committed $400 million in seed investment to bootstrap MI4’s AUM, demonstrating strong confidence in the fund while providing large-scale liquidity from day one.

2.1.3 The Role of Securitize

Securitize plays the most critical role in MI4’s operation. Far beyond being a mere technology provider, Securitize is a fully regulated financial institution registered with the U.S. SEC as a Broker-Dealer and authorized Alternative Trading System (ATS) operator.

Source: Ethereum X

As of August 2025, Securitize holds roughly 25% market share of the entire RWA (real-world asset) tokenization sector. It cemented its leadership by partnering with BlackRock to tokenize the $2.4 billion money market fund “BUIDL,” a case so significant that it was even spotlighted by Ethereum’s official account. MI4’s choice of Securitize as a partner ensures that every stage—from issuance to secondary trading—is conducted transparently under institutional regulatory standards.

This regulatory foundation provides real advantages to MI4 investors. Shares of the fund are tokenized using the standardized “DS Protocol,” enabling investors not only to hold their shares but also to access compliant secondary markets for liquidity or even use their holdings as on-chain collateral assets.

In short, Securitize is the central pillar that makes MI4 a true hybrid financial product—combining the trust and security of traditional finance with the efficiency and composability of decentralized finance.

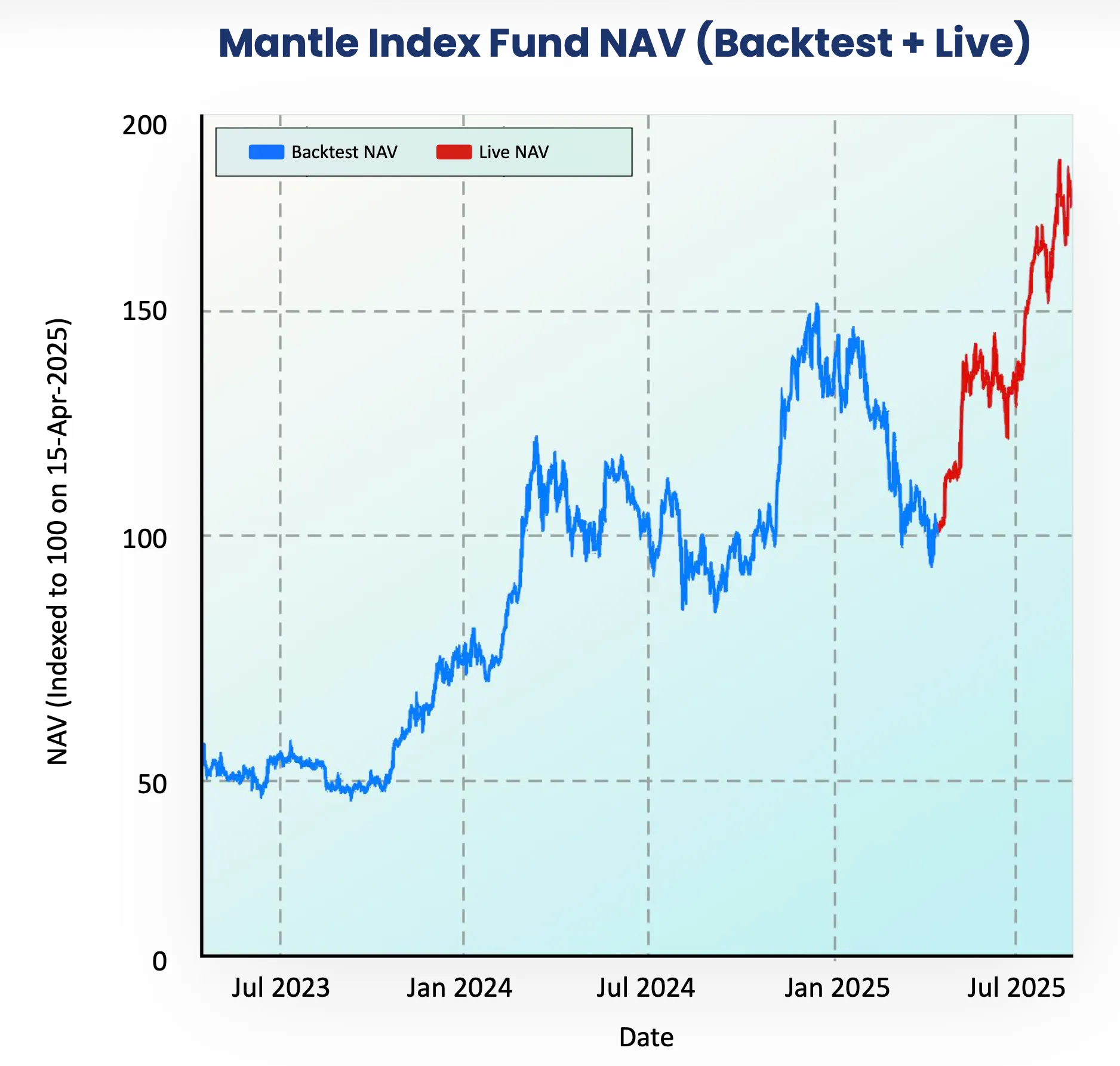

Source: Mantle Index Four

Launched in Q2 2025, MI4 does not yet have a long operational track record, but its potential can be examined by applying the fund’s strategy to historical data. The chart above shows backtesting results of a synthetic portfolio constructed according to MI4’s asset allocation and yield model over the past two years.

The steady upward trajectory in the chart reflects the combination of MI4’s two core strengths: a diversified portfolio and built-in yield. Let’s explore how these elements work in practice.

2.2.1 Better than Vanilla

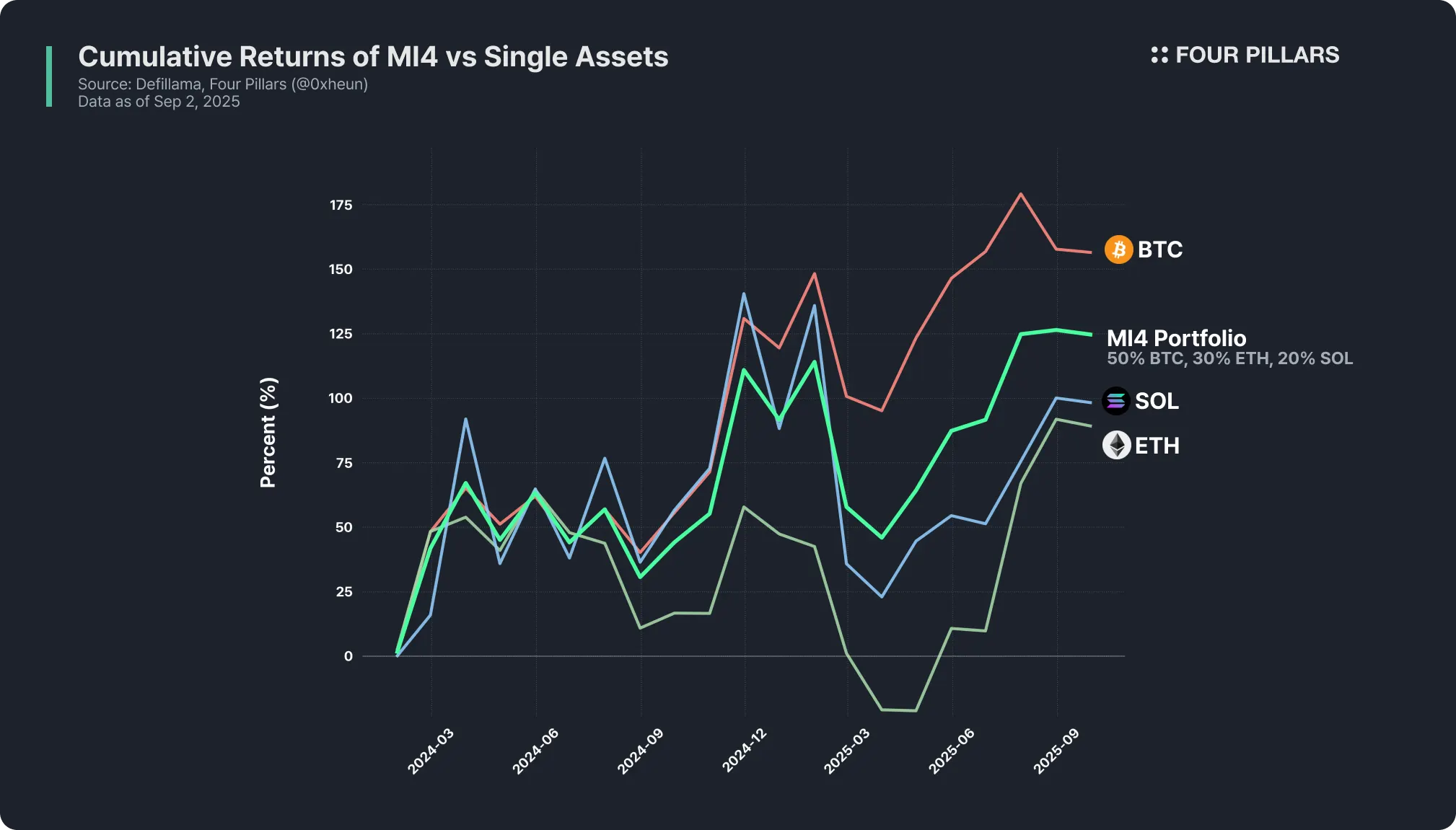

One of MI4’s greatest advantages is its ability to smooth out the volatility of individual asset bets while still capturing the overall growth of the crypto market. Consider a scenario where BTC moves sideways, ETH rises modestly, and SOL rallies sharply:

BTC-only investors: Miss out on the upside of other assets.

SOL-only investors: Enjoy strong gains in an uptrend but face outsized risk of heavy losses in a downturn.

By weighting assets proportionally to market capitalization, MI4 balances exposure—capturing part of SOL’s upside while BTC and ETH provide stability. Instead of depending on the performance of a single token, investors gain broad market beta exposure, benefiting from compounding growth over the long run without needing to predict which asset will lead the next cycle.

2.2.2 Higher Yields

Another key differentiator of MI4 is that it doesn’t merely mix assets together—it generates additional yield directly within the portfolio. Previous crypto index products simply held the underlying assets, missing out on staking and other on-chain income opportunities.

MI4 overcomes this by incorporating yield-bearing tokens such as mETH, bbSOL, and sUSDe. This design provides two major advantages:

Downside protection: Even in market downturns, staking and DeFi strategies deliver around 5–6% annual yield, acting as a cushion to mitigate losses.

Upside acceleration: In bull markets, yields are reinvested, compounding alongside price appreciation to significantly amplify total returns.

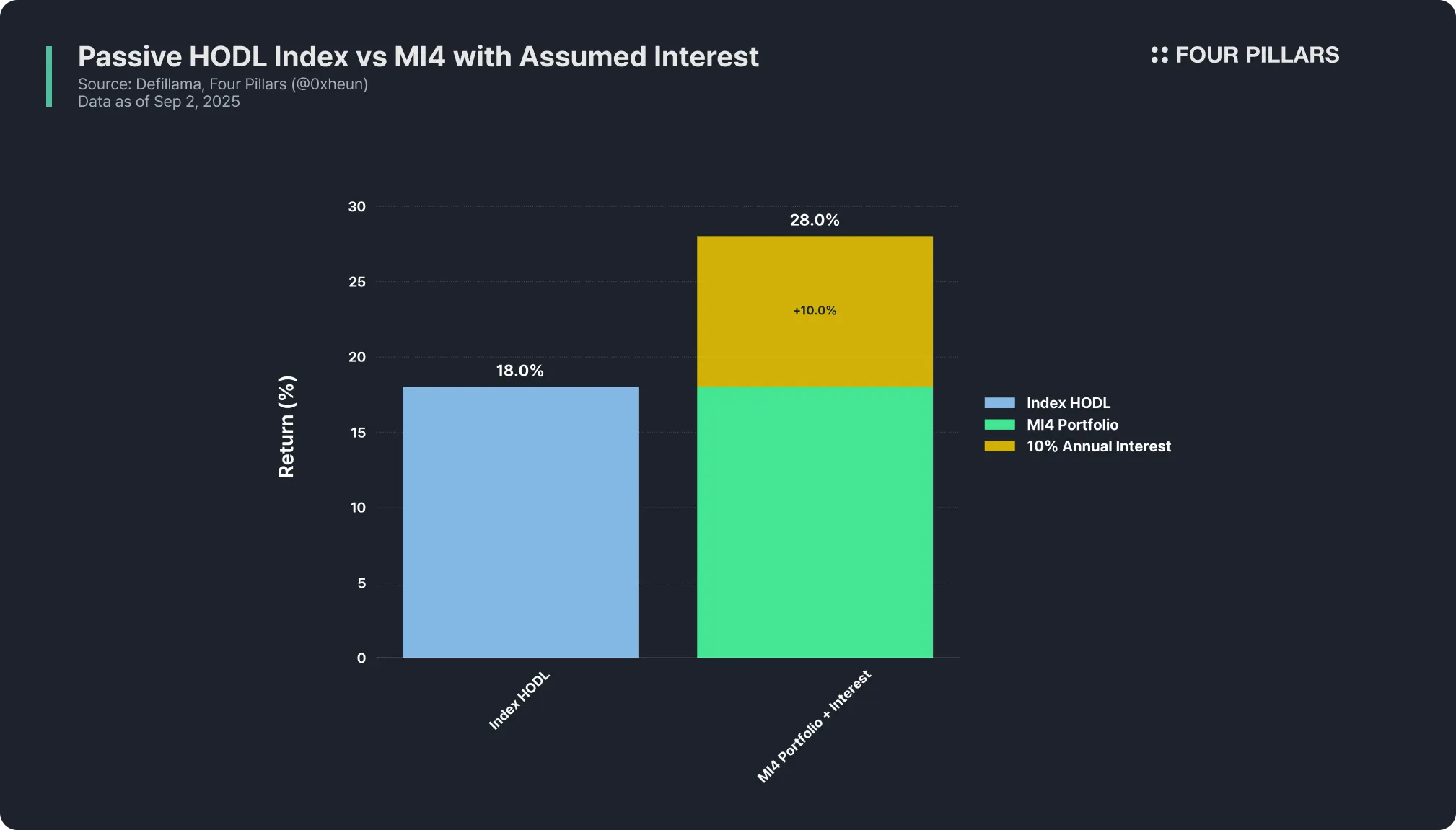

For example, if the overall fund value drops 10% due to falling asset prices, accumulated yield amounting to ~5% of fund value could cut the net loss roughly in half.

In short, MI4 functions as a smart index fund that automatically farms yield, offering a structural advantage that simple HODL strategies cannot match. For long-term holders, this translates into far stronger financial benefits.

The DeFi boom of 2020 gave rise to on-chain index tokens targeting crypto-native investors. Issued as ERC-20 tokens, these products relied on smart contracts to automate rebalancing and portfolio management.

The goal of crypto index tokens was to simplify exposure to multiple assets in the otherwise complex crypto market—similar in spirit to stock indexes or ETFs in traditional finance. These came in various forms, from on-chain index tokens to off-chain index funds and exchange-traded products (ETPs).

Even before MI4, several crypto index fund experiments took place, with on-chain index tokens gaining particular attention. A notable example was the DeFi Pulse Index (DPI) launched by Index Coop in 2020. DPI bundled major DeFi governance tokens such as Uniswap (UNI), Aave (AAVE), MakerDAO (MKR), and Compound (COMP) using market-cap-weighted allocation, allowing investors to gain sector-wide DeFi exposure through a single token.

Although these products generated excitement at launch, most struggled to attract or retain significant capital. DPI’s assets under management (AUM), for example, climbed to around $150 million during the 2021 bull run but fell to roughly $14 million by mid-2024. Two major reasons explain this failure:

Early index tokens simply held the underlying assets without generating additional returns, effectively ignoring crypto’s unique yield opportunities. Proof-of-stake assets like Ethereum could earn ~4% annually through staking, and stablecoins deposited into DeFi protocols could generate 5–10% or more. By not capturing this, index tokens left investors with pure price exposure and nothing else.

CoinDesk argued that staking the assets inside an index could prevent dilution and provide dividend-like rewards, much like traditional equity index funds do. But DPI and its peers ignored this, leaving holders with zero income.

Meanwhile, the protocols included in these indexes distributed rewards to other investors through token issuance, creating a structural disadvantage for index holders. With no incentive to hold long-term—especially in bearish markets—value eroded even faster.

Most index tokens were issued on-chain as ERC-20s, targeting DeFi-savvy retail investors with high risk tolerance. However, this approach lacked the regulatory and legal safeguards institutions required—missing the most important customer base.

Crypto-native investors: Preferred chasing short-term gains from new tokens rather than holding broad-market exposure.

Institutional investors: Had demand for diversified products but could not commit capital to unregulated, self-custodied tokens.

In 2021, there were effectively no regulated crypto index products. The few available—like Grayscale trusts or early ETFs—focused only on single assets such as Bitcoin or Ethereum, offering limited product–market fit.

For an index fund to succeed, it needed to target institutions with real capital and provide structures they could legally invest in. At the same time, it had to deliver added value beyond mere price exposure, such as yield strategies that even seasoned crypto investors would find difficult to implement themselves.

Traditional finance underscored this reality. The Bitcoin futures ETF BITO, launched in 2021, raised over $1 billion within days precisely because it was regulated and infrastructure-ready, even though it only offered one-dimensional Bitcoin exposure.

As a result, on-chain index tokens failed to attract either DeFi enthusiasts or cautious institutions. The key lesson: a successful crypto index product must be institution-ready in structure while delivering tangible added value, such as systematic yield generation, beyond just tracking prices.

Not only projects like MI4 but also traditional financial institutions are increasingly interested in crypto index-based products. At the end of 2024, U.S. regulators approved the first hybrid crypto index ETF combining Bitcoin and Ethereum, though initial inflows were modest. Still, as regulations evolve, broader crypto index ETFs, including altcoins, are likely to emerge.

The entry of Wall Street giants like BlackRock and Fidelity through ETF filings and partnerships shows that professionally managed index products are gaining ground in a space where decentralized experiments previously failed. Lessons from the 2020–2022 wave of index token experiments have strongly influenced this new wave of products, which now prioritize compliance, risk management, and investor needs (such as stable returns and lower volatility).

MI4 solves the “lack of yield” problem that crippled earlier index tokens. Instead of simply holding ETH, SOL, and USD, it incorporates their yield-bearing equivalents, mETH, bbSOL, and sUSDe, so that the portfolio automatically accrues rewards. This is similar to how traditional equity index funds automatically reinvest dividends.

For example, imagine two indexes with the same asset composition. If crypto prices rise 20% in a year, a plain index would return 20%. But MI4, with an average 6% APY from staking and yield strategies, would deliver ~26%. Over time, compounding makes this gap even wider.

Crucially, this yield doesn’t come from leverage or excessive risk. ETH and SOL staking provide stable returns while securing their networks, and sUSDe generates income from staking rewards and funding rate arbitrage. MI4’s yield is therefore native to the crypto ecosystem and aligned with its underlying strengths.

This design directly addresses past missteps. With MI4, capital is no longer left “sitting idle.” Even in sideways markets, the fund collects steady yield from ETH (~3.5–4%), SOL (~7%), and stablecoin strategies (10%+ APY). Over the long term, these embedded returns turn mediocre years into decent ones, and decent years into excellent ones. This stickiness keeps capital anchored in the fund, positioning MI4 as an institutional-grade product that fuses ETF-style security with DeFi-native yield strategies.

MI4 was designed from the ground up for institutional adoption, addressing precisely where earlier index tokens failed on product–market fit. It is not just another token for traders but a regulated fund structure operated with licensed service providers:

Investors must be accredited or otherwise qualified (non-U.S. or Reg D U.S. investors).

The minimum subscription is $100,000, clearly targeting institutions and professional investors, not retail.

Investor onboarding and share tokenization are handled via the Securitize platform, integrating smoothly with traditional workflows (KYC/AML → subscription → tokenized securities as fund shares).

Fund administration, auditing, and custody follow controls equivalent to hedge funds or ETFs.

This structure removes the institutional barriers that on-chain indexes previously faced.

MI4’s investment approach also matches institutional demand. Instead of betting on a single asset, institutions can gain exposure to a basket of leading cryptocurrencies while capturing built-in yield. Mantle describes MI4 as aiming to become the “S&P 500 of crypto”. Particularly when traditional rates are low, MI4 offers a regulated, secure way to access broad crypto exposure plus steady income.

“MI4 and associated future products will become the de facto SPX or S&P 500 of crypto – our basket of the major cryptocurrencies aims to capture all capital on-chain looking for smart beta with income, and is a set-it-and-forget-it solution for institutions without the complexities of direct custody.”

— Timothy Chen, Global Head of Strategy at Mantle

This value proposition is especially attractive to family offices, funds, and corporate treasuries that want crypto exposure but lack the expertise to run staking and DeFi strategies themselves. MI4 outsources this complexity while maintaining transparency and professionalism, making institutional entry into crypto far easier.

Source: mantleguard.com

The fund’s early performance also supports this. Mantle Treasury has already committed an initial investment of $400 million, and the partnership with Securitize is strengthening market confidence in the inflow of institutional capital. Through this, it is currently showing a performance with about $220M in AUM.

As the market matures, the idea of a crypto index fund is becoming increasingly attractive. A diversified crypto index functions as a “set-it-and-forget-it” investment solution, ideal for investors who want broad market exposure without active trading. But to succeed, it must overcome the challenges that plagued earlier attempts—low liquidity, high fees, lack of yield, and weak marketing.

MI4 addresses these pitfalls by combining institutional-grade trust with on-chain yield mechanisms. If successful, it could achieve the vision that early projects like DPI and C20 never realized. As of 2025, most crypto index initiatives remain experimental, but with improved design, they are once again catching investors’ attention. The coming years will determine whether crypto indexes can evolve from experiments into core investment vehicles within the digital asset market.

The timing of MI4’s launch is also well-calibrated. Institutional interest in crypto is growing, but so are demands for simplicity and safety. Products like BlackRock’s IBIT and Nasdaq’s custody services show that major financial players are preparing for broader adoption. Yet institutions still face key hurdles when entering the market directly:

Which assets should be included?

How should staking and yield management be handled?

Who takes responsibility for custody and regulatory compliance?

MI4 provides a solution by enabling institutions to allocate into a diversified crypto basket as easily as they would into a stock index fund—while also capturing DeFi yield. This lowers entry barriers, channels more capital into the crypto ecosystem, and in turn boosts liquidity, efficiency, and even network security. It represents a fundamentally different proposition than ETFs that merely store Bitcoin.

If MI4 succeeds, it could serve as the blueprint for yield-generating crypto index funds. Just as dividend equity funds or bond index funds hold a place in traditional portfolios, “crypto beta with yield” could become a core allocation. Mantle envisions MI4 as a starting point for more products and deeper on-chain financial integration, framing it as a new financial primitive. As regulation clarifies and institutions grow more familiar with tokenized assets, models like MI4 are likely to become a driving force behind institutional crypto adoption.

In conclusion, this creates a win–win scenario for both investors and the industry. Investors gain easier access, improved risk-adjusted returns, and yield; the industry secures stable institutional capital and stronger legitimacy in traditional finance. By combining investor convenience with the strengths of crypto, MI4 positions itself as a key milestone in bridging traditional and decentralized finance—opening the door to the next wave of crypto investment.

Dive into 'Narratives' that will be important in the next year