The supply and utilization of stablecoins has exploded in recent years. In 2024, on-chain stablecoin transaction volume was estimated to be approximately $27.6 trillion, surpassing the combined payments volume of Visa and Mastercard (approximately $23.8 trillion) during the same period. As of March 2025, the top 10 stablecoins had a combined market capitalization of approximately $221.2 billion, of which Tether USDT and Circle USDC accounted for approximately $143 billion and $58 billion, respectively, accounting for more than 90% of the total market. In addition to providing liquidity in the crypto trading market, stablecoins are increasingly being used in the real economy for international remittances, trade payments, and store of value.

The rise of stablecoins is driven by their value stability and transaction efficiency. Unlike assets like Bitcoin, which are prone to price fluctuations, stablecoins peg their value to the dollar or euro, providing a relatively stable unit of account. This allows global users to transfer value quickly and inexpensively without the delays and high fees of traditional finance, and in emerging markets, it enables international trade payments and salary payments without the need for a bank account. For example, SpaceX uses stablecoins to send Starlink sales from Argentina and Nigeria, and AI data company ScaleAI pays its contractors around the world in stablecoins to avoid currency exchange and delays. While stablecoins have the potential to transform global financial infrastructure and payment systems, they also present challenges, such as the transparency of reserve assets and regulatory gaps.

This report examines stablecoin issuance pipelines by analyzing issuance models, regulatory frameworks, and key cases to provide strategic insights. The focus is on fiat-linked, asset-backed stablecoins, excluding non-regulated variants like algorithmic stablecoins. First, we summarize the stablecoin issuance pipeline structure and participant roles, followed by an examination of regulatory and experimental trends across major countries. We then study leading stablecoin issuers and infrastructure companies, concluding with an analysis of stablecoin adoption in traditional finance and fintech in each countries.

Stablecoins have become a key asset in the crypto ecosystem, especially in the form of digital dollars, which serve as the underlying asset that enables fast on-chain payments. However, in order for stablecoins to become more than just a means of securing value and become sustainable and institutionally compatible assets, there needs to be a fundamental discussion about their issuance structure and how the underlying assets are managed.

So far, the regulatory debate has been centered on the bank-based centric, in which a bank or a separate issuer deposits all the cash into a bank account and then issues stablecoins. While this approach has contributed to the initial market establishment by linking with institutional finance, it is likely to face structural limitations in terms of global scalability, asset management efficiency, and liquidity.

An emerging trend in this context is the capital market-centric stablecoin issuance model. This is a structure that goes beyond the deposit-oriented stablecoin structure operated by banks and pursues profitability, liquidity, and institutional compliance based on a variety of assets, such as MMFs, short-term government bonds, and tokenized capital market instruments, while managing the stablecoin's collateral assets.

In this chapter, we will compare these two issuance models from a structural perspective and consider why the capital markets-centric model is emerging as the more important option for stablecoin design today and in the future.

The bank-centric stablecoin issuance model can be described as a form of transferring the structure of the existing financial system to the digital asset space. A typical example is the EURCV issued by SG-Forge, a subsidiary of Societe Generale, which is digitized by matching customer deposits with the bank's internal system on a 1:1 basis. EURCV is a euro-based stablecoin issued within the regulatory framework of the French central bank and financial supervisory authorities, and operates in a closed structure accessible only to authorized institutional investors. Although the stablecoin is issued on a public blockchain (Ethereum), its actual use is limited to euro transactions between institutions authorized by SG-Forge, with funds deposited and settled on a 1:1 basis in Societe Generale's internal system. In this structure, issuance and repurchase are driven by the bank's internal compliance and settlement systems, making it a model with low legal risk and high security and internal controls.

This model is highly compatible with the regulatory environment of traditional financial institutions and can be seamlessly integrated with regulatory frameworks such as MiCA in Europe. From a customer or institutional investor's point of view, it provides high reliability and predictability, as deposited funds are always managed under a regulated infrastructure. At the same time, however, connectivity with public blockchain ecosystems is limited, and functional constraints are inevitable when it comes to participating in dapps, distributing to a global audience, and providing liquidity. As a result, while EURCV is a tokenized digital representation of the euro, it is an institutionally-focused, closed financial token designed to be far removed from the collateral diversity, decentralized distribution, and on-chain asset management.

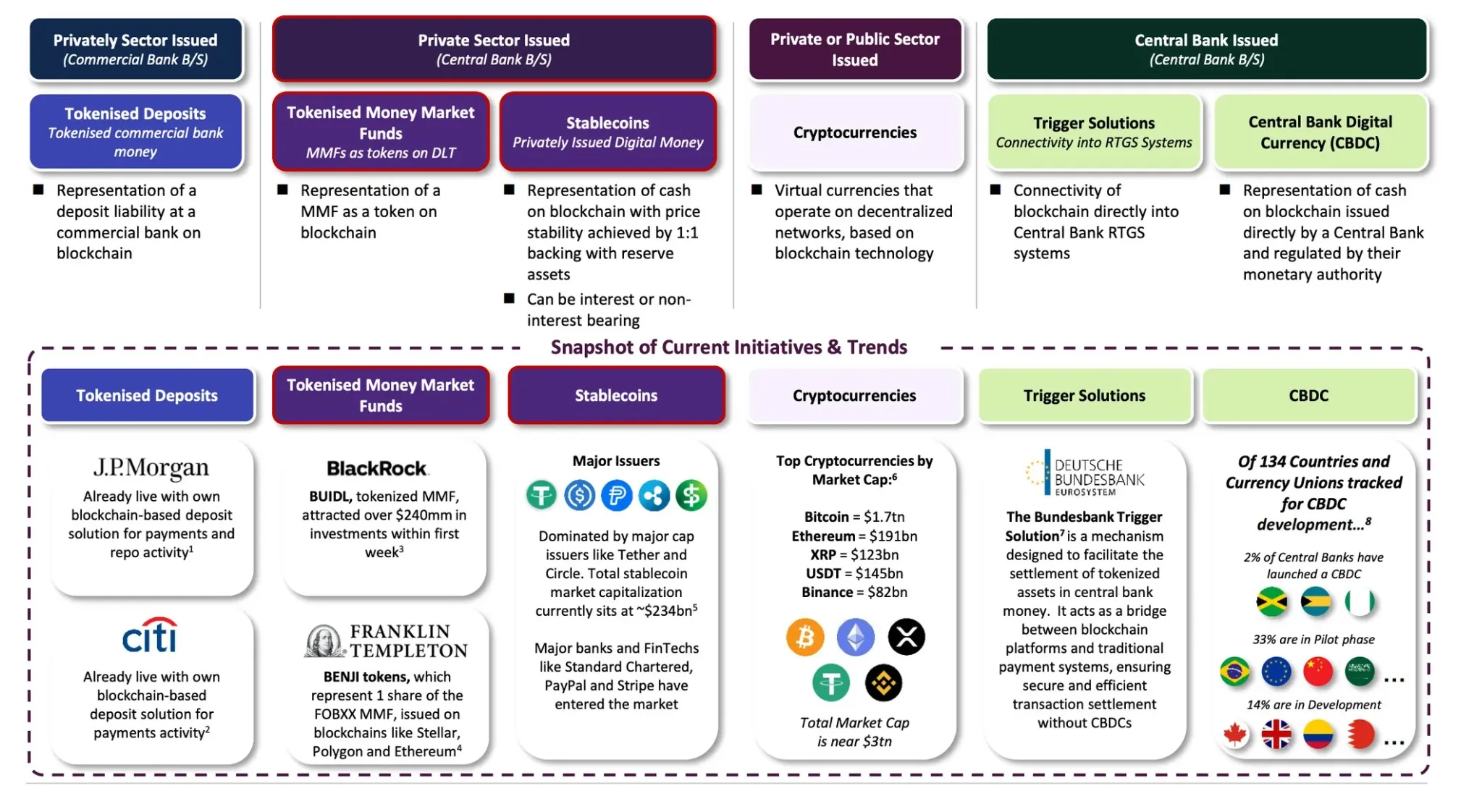

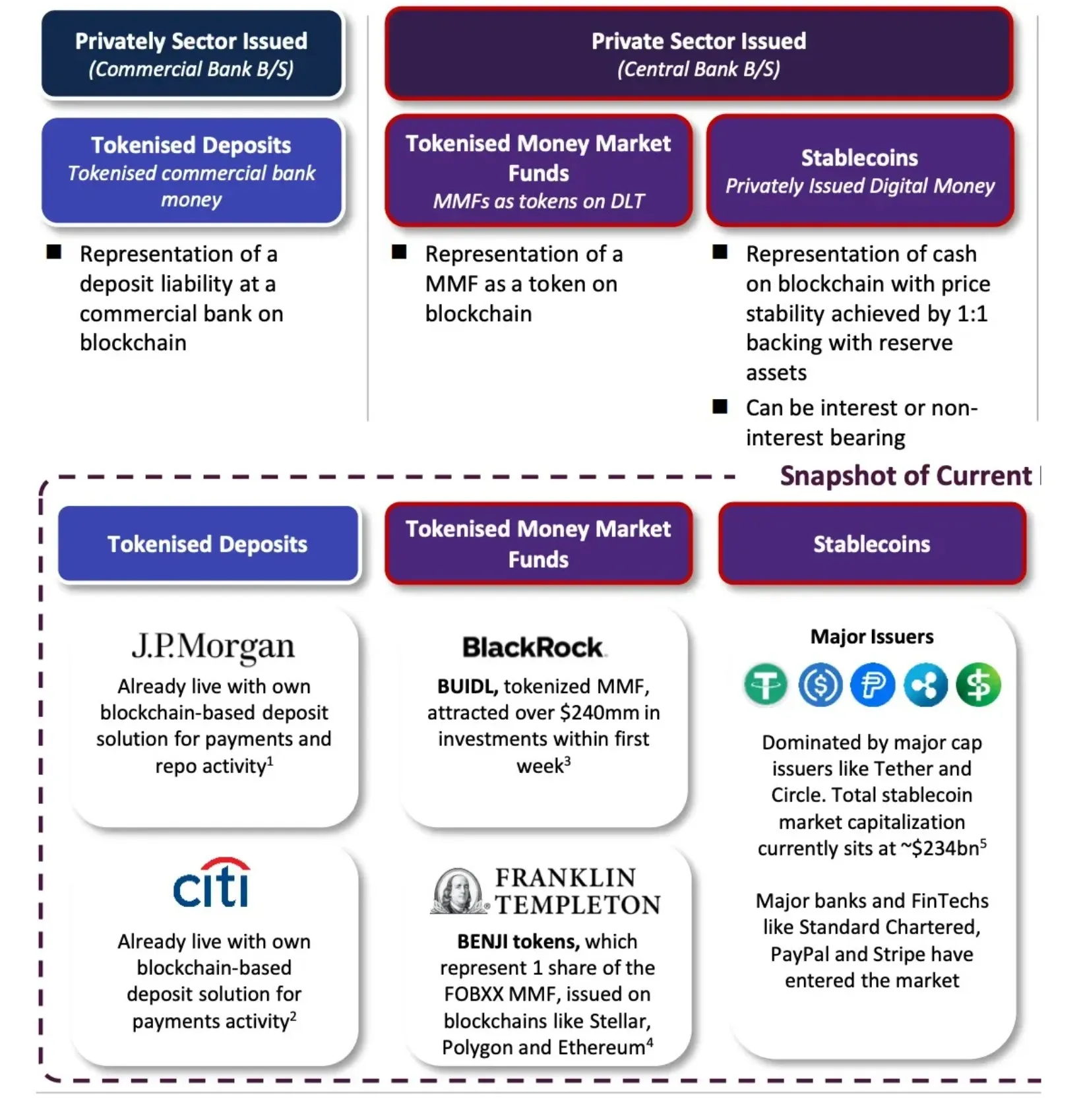

There is a Wide Spectrum of Digital Money Implementations

Source: TBACCharge2Q22025

A capital market-centric stablecoin issuance model is designed to go beyond the simple storage of reserve assets in banks and invest or manage them directly in capital market instruments. This can include money market funds (MMFs), short-term Treasury bills (T-bills), repurchase agreements (repos), and even tokenized securitized assets. This model is characterized by the issuer's ability to partner with an asset manager or brokerage firm to convert the stablecoin into a revenue-based structure.

Circle's USDC and Tether's USDT fall into the market-driven issuance model. They invest the deposits they receive from users, partly in cash and partly in capital market instruments such as short-term US Treasuries, money market funds (MMFs), and commercial paper. Rather than simply holding deposits, they generate management fees and those fees become the issuer's primary source of income. For example, Circle allocates a portion of its reserve assets to the Circle Reserve Fund managed by Blackrock, and Tether invests in U.S. Treasury bonds and MMFs.

This structure is advantageous because it allows reserve assets to generate income while maintaining a certain level of liquidity and safety. However, this model can raise market confidence and regulatory concerns if some of the assets are located outside of banks and the investment strategy or collateral composition is not fully transparent to users.

The main advantages of this model are profitability and scalability. Whereas traditional bank deposits earn little or no interest, or are held solely by the issuer, a capital markets-based model can be designed to distribute a fixed return to holders. This is a key factor in expanding the function of stablecoins from a simple means of transferring money to a yielding asset or digital sovereign bond.

However, the capital market-centric model is not without its drawbacks. The biggest issue is regulation. If the deposited assets are securities, such as government bonds or MMFs, there is a possibility that the stablecoin issued will be classified as a security token. This means that it will be subject to regulation by the SEC or national financial authorities, and will have to meet complex regulations, including asset disclosure, performance reporting, and investor protection requirements. In addition, the issuer itself may need to qualify as an asset manager or broker/dealer, which creates a relatively high barrier to entry, requiring sophisticated institutional analysis and preparation when designing the structure.

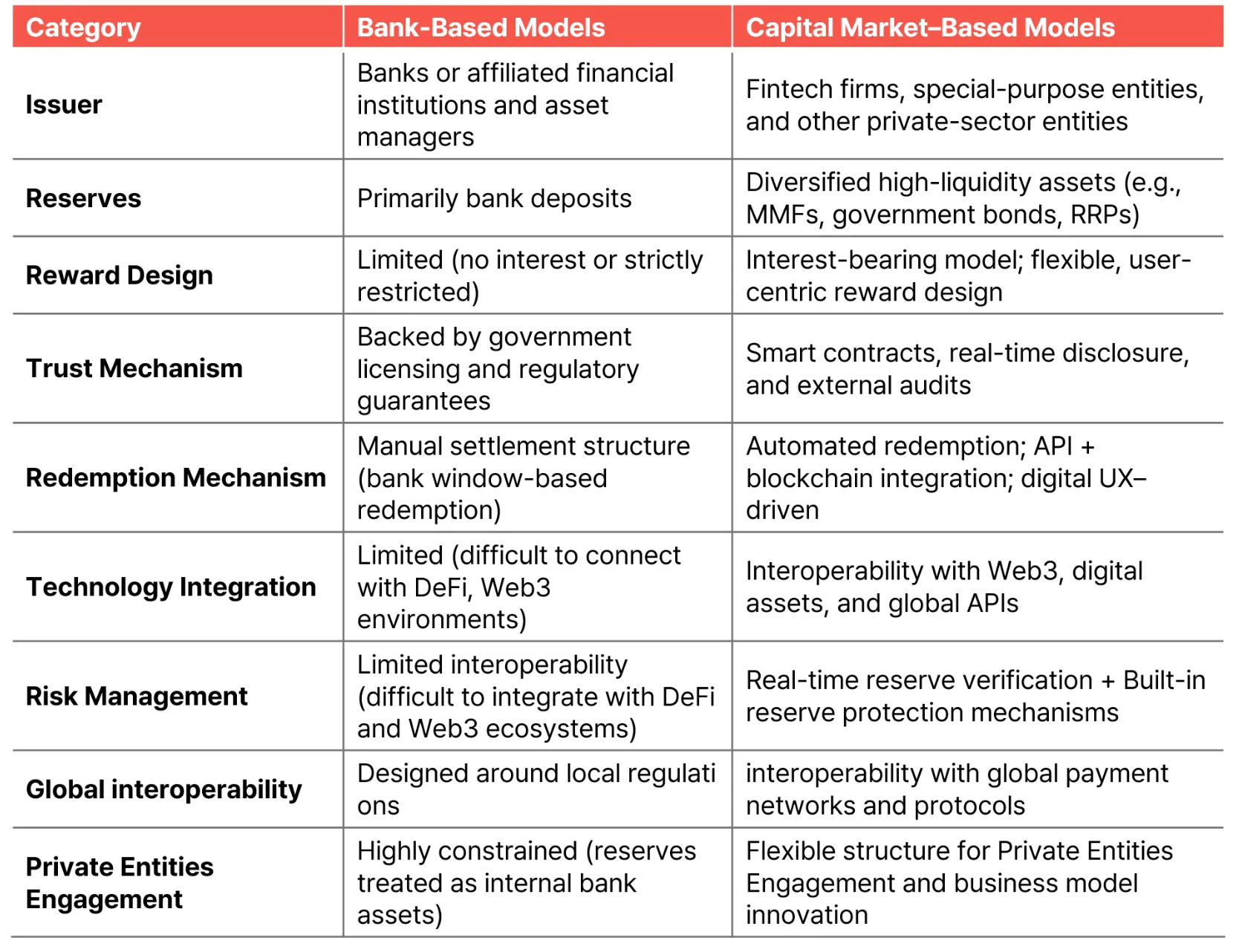

Structural Comparison: Bank-Based Models vs. Capital Market–Based Models

Source: Hashed Open Research

To date, regulators have sought to regulate the stablecoin market through a bank-centric model. However, this model is increasingly showing its limitations in terms of profitability, operational flexibility, and compatibility with global financial flows. Especially when considering cross-border distribution, and asset management revenue allocation, a structure that relies solely on the existing banking system has clear limitations.

A capital markets-centric model, on the other hand, provides the foundation for stablecoins to evolve into a “digital asset management platform”. From issuance structure to investment, distribution, and redemption, it is highly compatible with the on-chain financial system and, in the long run, better positioned to connect to the global liquidity network. In the real market, the share of bank-based models is close to 0%, and the share of capital market-based models such as Tether USDT and Circle USDC is overwhelming, so the foundation of innovation has been capital market-based models.

In the discussion of stablecoin institutionalization and infrastructure building, a key challenge will be to actively embrace capital market-driven models and create regulatory and technical frameworks that can legally support them. This is not just about expanding the diversity of financial products, but also a strategic choice for national economies and global digital currency competitiveness.

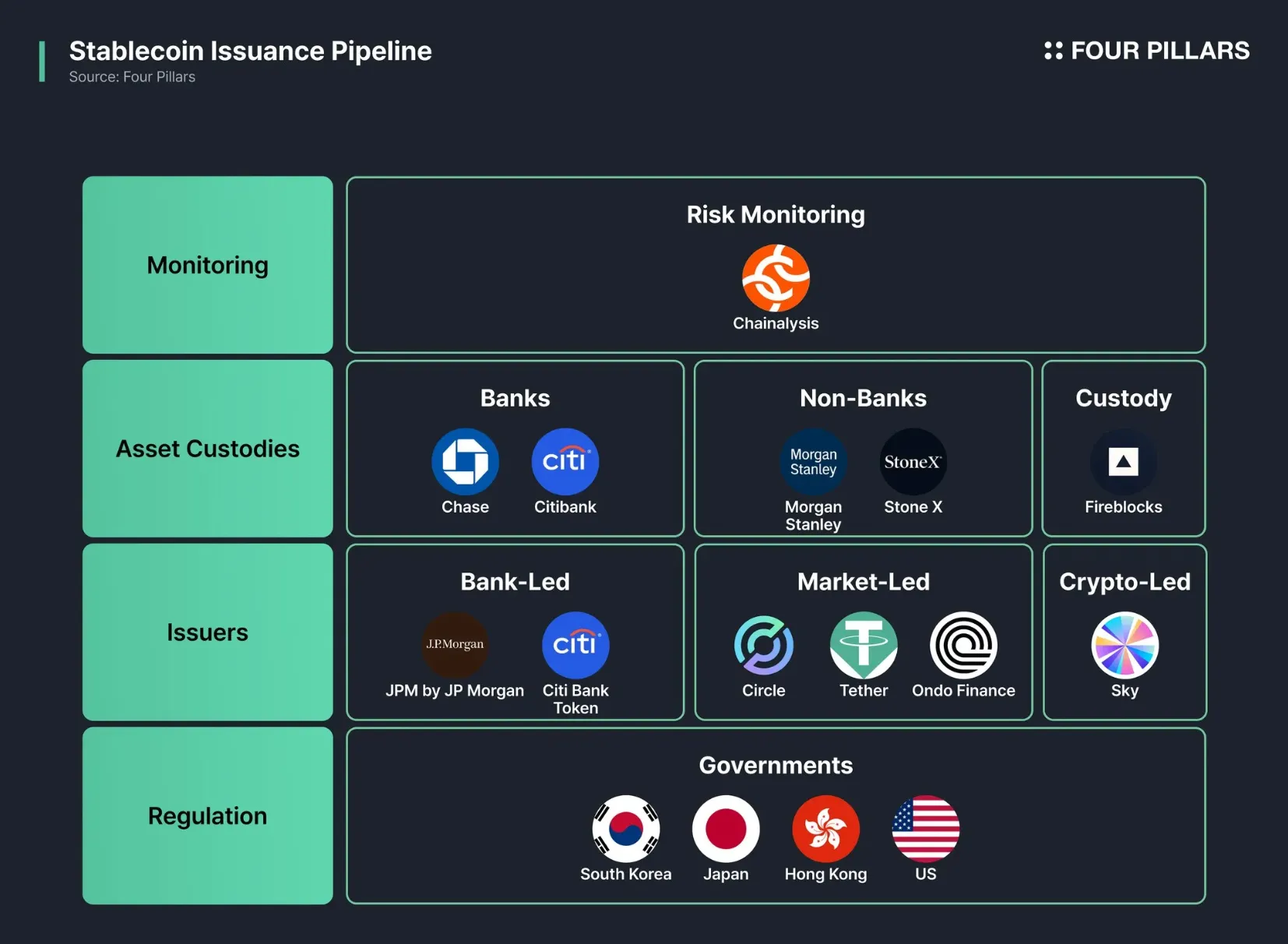

In order to issue and distribute a stablecoin, an infrastructure (both on-chain and off-chain) and a legal and technical framework are required. To make it easier to understand, we can categorize it into a few models, with different actors responsible for each step. The key elements of the issuance pipeline include (i) the legal and regulatory framework, (ii) the types and models of issuing entities, (iii) the role of banks/intermediaries in managing reserve assets, and (iv) the technical infrastructure and operational role of the issuer. These factors are explored below.

Stablecoin Issuance Pipeline

Source: Four Pillars

Stablecoin issuance is subject to institutional requirements, including incorporation and licensing. The issuing entity must be incorporated in the jurisdiction and obtain the relevant licenses or registrations. For example, Circle has obtained a money transmitter business (MSB) license in each state in the U.S. to issue USDC as a prepaid product. Paxos and Gemini, on the other hand, issue dollar-pegged stablecoins through BitLicense or trust authorization in New York State. Regulatory requirements for stablecoins include (i) minimum capitalization requirements, (ii) safe custody of reserve assets, and (iii) regular reporting obligations.

For example, Hong Kong's proposed regulations require a minimum capitalization of HKD 25 million, the maintenance of reserve assets equal to the token issuance at all times, and no redemption restrictions. In the U.S., the GENIUS Act (2025), which recently passed the Senate and is now in the legislative stage, requires issuers to maintain 1:1 reserve assets (cash, bank deposits, short-term Treasury securities, etc.) and publish monthly audited reserve asset reports. As such, the issuer must operate in an authorized form (bank subsidiary, trust company, etc.) under the jurisdiction's financial legal framework and have reporting and monitoring arrangements in place through regulations such as AML/KYC (anti-money laundering).

The above approaches are “capital markets-centric,” allowing non-bank financial institutions to issue, while bank-centric models have been discussed to limit issuers to FDIC-insured banks, and in the case of Custodia Bank, compliance was achieved by redesigning all relevant policies and procedures under banking regulation. Custodia Bank, along with Vantage Bank in the U.S., issued a stablecoin called AVIT, which is backed by actual bank dollar deposits and issued on a public blockchain like Ethereum. When a customer deposits money in the bank, they are issued a certain number of tokens, which can be freely traded on the blockchain or stored in an external wallet.

Currently, the regulatory frameworks for stablecoins in major jurisdictions are capital market-centric in the U.S. and Hong Kong, while Europe and Japan are more conservative and have proposed bank-centric legislation. These regulatory frameworks provide an important foundation for stablecoin operators to develop their businesses.

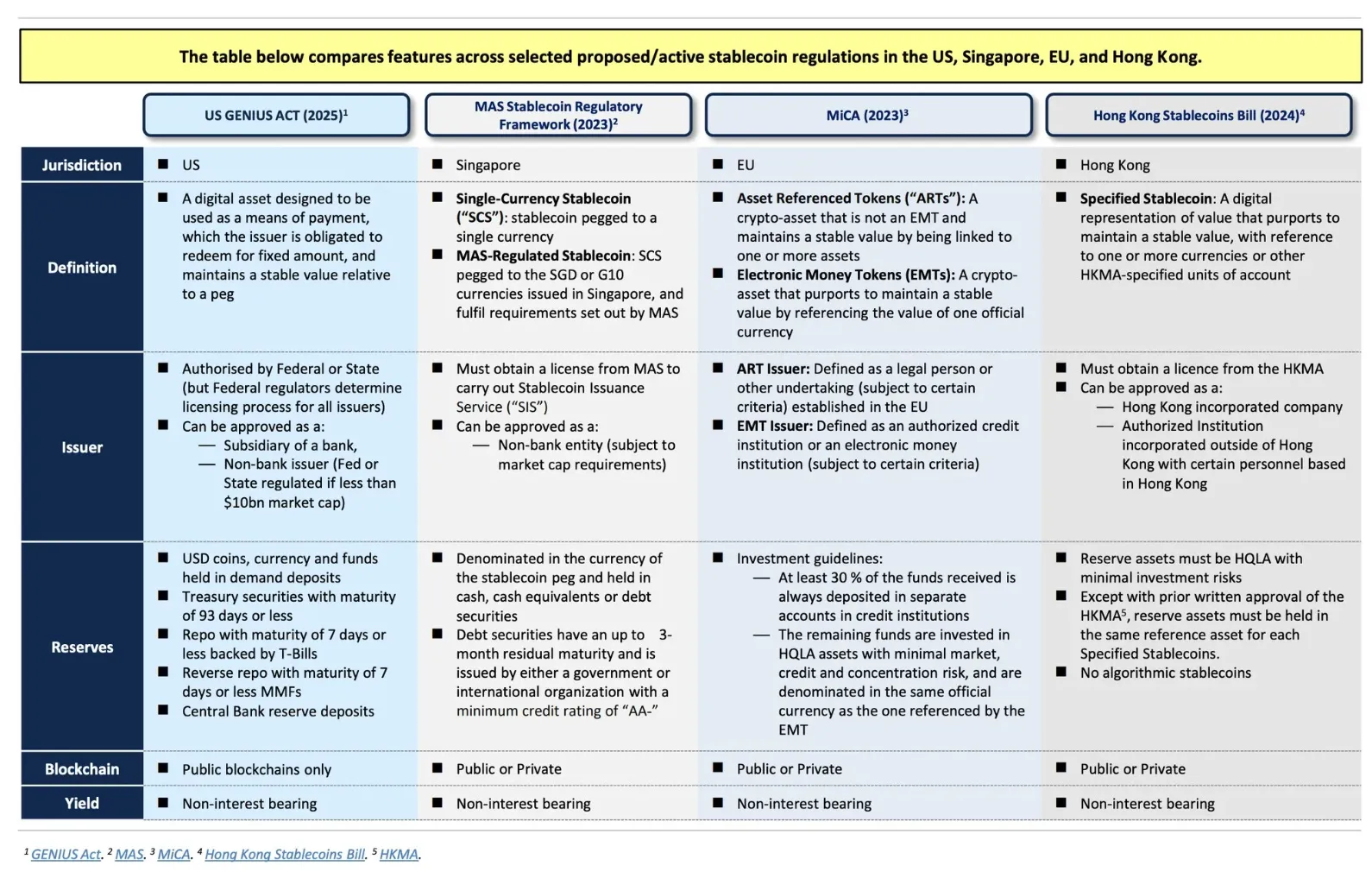

Jurisdictional Comparison on Proposed Stablecoin Regulations

Source: TBACCharge2Q22025

Once the regulatory framework for stablecoins is clear, the next step is to issue a stablecoin. Stablecoin issuance structures can be categorized into three main models

Bank-centric model: A bank, such as a commercial bank, directly leads the issuance of a stablecoin, which can be seen as a tokenized deposit backed by bank deposits or reserves. It is characterized by the fact that the bank already has the credit and regulatory requirements in place, so it operates like a digital version of a bank deposit. Examples include JPMorgan's JPM Coin and the recent issuance of the Avit token by Custodia Bank in the US.

Capital market-centric model: Non-bank financial institutions lead the issuance, with individual companies managing reserve assets in conjunction with banks and non-banks to issue stablecoins based on market demand. Examples include Tether (USDT), Circle's USD Coin (USDC), and PayPal's PYUSD, which currently dominate the stablecoin market.

Crypto-native model: Stablecoins that are algorithmically or collaterally generated on-chain by decentralized protocols and issued directly on the blockchain, such as MakerDAO's DAI or Ethena's USDe. In this case, issuance/redemption is done through smart contracts without the involvement of traditional financial institutions, but it is often far from regulated.

Stablecoin issuers manage the minting and burning of tokens on-chain, and operate real-time balance monitoring and security management systems. Issuers build their own blockchain node infrastructure to monitor transactions, detect anomalies, and take action if necessary, such as freezing (blacklisting) wallet addresses. In fact, Tether and Circle have built into their smart contracts the ability to freeze assets in fraudulent accounts when requested by regulators. Issuers also receive and process new issuance/redemption requests from customers via API servers and web interfaces, where it is important to maintain the integrity of off-chain funds flows and on-chain token flows. For example, if a customer transfers $1 million to the issuer's bank account, the issuer will confirm this and call a smart contract to mint an equivalent amount of new stablecoins and send them to the customer's wallet. Conversely, when a redemption request is made, the tokens are reclaimed (burned) from the customer and fiat is paid.

It is essential that all of this is recorded in a double-entry ledger to maintain a 1:1 correspondence between the total amount of tokens in circulation and the total amount of reserves. Some projects introduce a Proof of Reserve Collateral (PoR) system to verify this on-chain as well. The BIS's Pyxtrial project has piloted a data pipeline that collects on-chain and off-chain data from major stablecoin issuers to monitor for reserve anomalies. The issuer's operational infrastructure also includes custody and key management systems. Key private keys used for issuance are securely stored using HSMs (hardware security modules) or solutions from specialized custodians (such as Fireblocks) to prevent hacking or insider misuse.

2.3.1 Managing Collateral Assets

The stability of the value of the issued stablecoins depends on what collateral assets they are backed by and the safe custody of the collateral assets. To this end, banks, trust companies, investment banks, etc. are entrusted with the custody and storage of reserve assets.

In a bank-centric model, the issuing entity, the bank itself, holds the reserve assets as deposits and may not need an additional custodian. However, as in the Custodia/Vantage case, two or more banks may collaborate to share the role, with one holding the reserves and settling payments (e.g., Fedwire/ACH connectivity) and the other managing token issuance/redemption on the blockchain.

In a capital markets-driven model, the issuer manages its reserves by depositing cash from customers into trust accounts at partner banks, or by investing in short-term government bonds and money market funds. For example, USDC holds its cash reserves at banks such as BNY Mellon, while the rest is held in BlackRock's Circle Reserve Fund, a short-term government bond fund. Tether (USDT) also has a portfolio of cash and Treasuries held in multiple banks, and has been earning significant interest income from investments in short-term U.S. Treasuries.

In addition, for market-centric models with smaller cash holdings, a broker is used to purchase Treasuries and hold the assets on their behalf. For example, Ondo Finance's stablecoin, USDY, buys short-term government bonds from brokers with customer dollars and issues tokens as collateral, with more than 95% of its collateral being short-term government securities. Securing/managing such stable and liquid assets is the core of the stablecoin issuance infrastructure, and partnerships with various financial institutions are essential.

2.3.2 Managing Issued Stablecoins

Custody infrastructure to securely manage stablecoins on the blockchain is also important. After issuance, individual users hold the stablecoins in their wallets, but institutional investors or companies with large funds often contract with specialized custodians to manage their assets. Custody services go beyond simple wallet storage to include multisig, cold wallet security, permission controls, auditing capabilities, and some even offer smart contract-based automation. Some of the leading custody providers include Coinbase Custody, Anchorage, BitGo, and Fireblocks, which act as the infrastructure that enables institutional demand for stablecoins and large-scale fund management by providing a consistent payment scheme and security monitoring system. Some examples include

Circle's USDC works closely with Fireblocks to enable institutions and partners to issue, transfer, and store USDC securely on an API basis. Circle uses Fireblock's secure transport network to move assets, especially in cross-chain transfers (CCTP) and large trading environments.

Anchorage also served as the initial infrastructure partner for Ondo Finance's USDY. As Ondo Finance is issuing tokens backed by government bonds, a custodial structure was needed to securely segregate and manage both the underlying assets and the on-chain tokens, and Anchorage was the right security and legal compliance organization for the job. **Anchorage is a digital asset bank authorized by the U.S. Office of the Comptroller of the Currency (OCC), providing institutional partners with legal certainty and regulatory familiarity.

Coinbase Custody provides an offline key custody and audit trail system for institutional investors in the U.S. to hold USDC in bulk, and recently began custody of assets under management for U.S. Treasury-backed money market funds linked to Circle.

The issuance of a stablecoin begins with the creation of tokens based on reserve assets, but what is actually more important is the ongoing monitoring and risk management system after issuance. This goes beyond the simple aggregation of circulating supply or technical operations, and implies the operation of a multi-layered infrastructure that includes legal and financial stability, technical security, and global regulatory responsiveness.

The most basic role is to track and disclose in real-time the circulating supply of issued stablecoins and the 1:1 matching of reserve assets. Most issuers do this by linking their accounting systems with blockchain-based dashboards to transparently share their issuance volume, reserve total, and asset composition. Circle, for example, not only discloses the composition and audit results of its reserve assets on a monthly basis. Tether has also been increasing its transparency in recent years, publishing quarterly reports on its reserve portfolio of cash, short-term U.S. Treasuries, gold, BTC, and more, which are regularly verified by external auditors. This disclosure is not just a marketing gimmick, but a key way to assess a stablecoin's reliability and de-pegging risk.

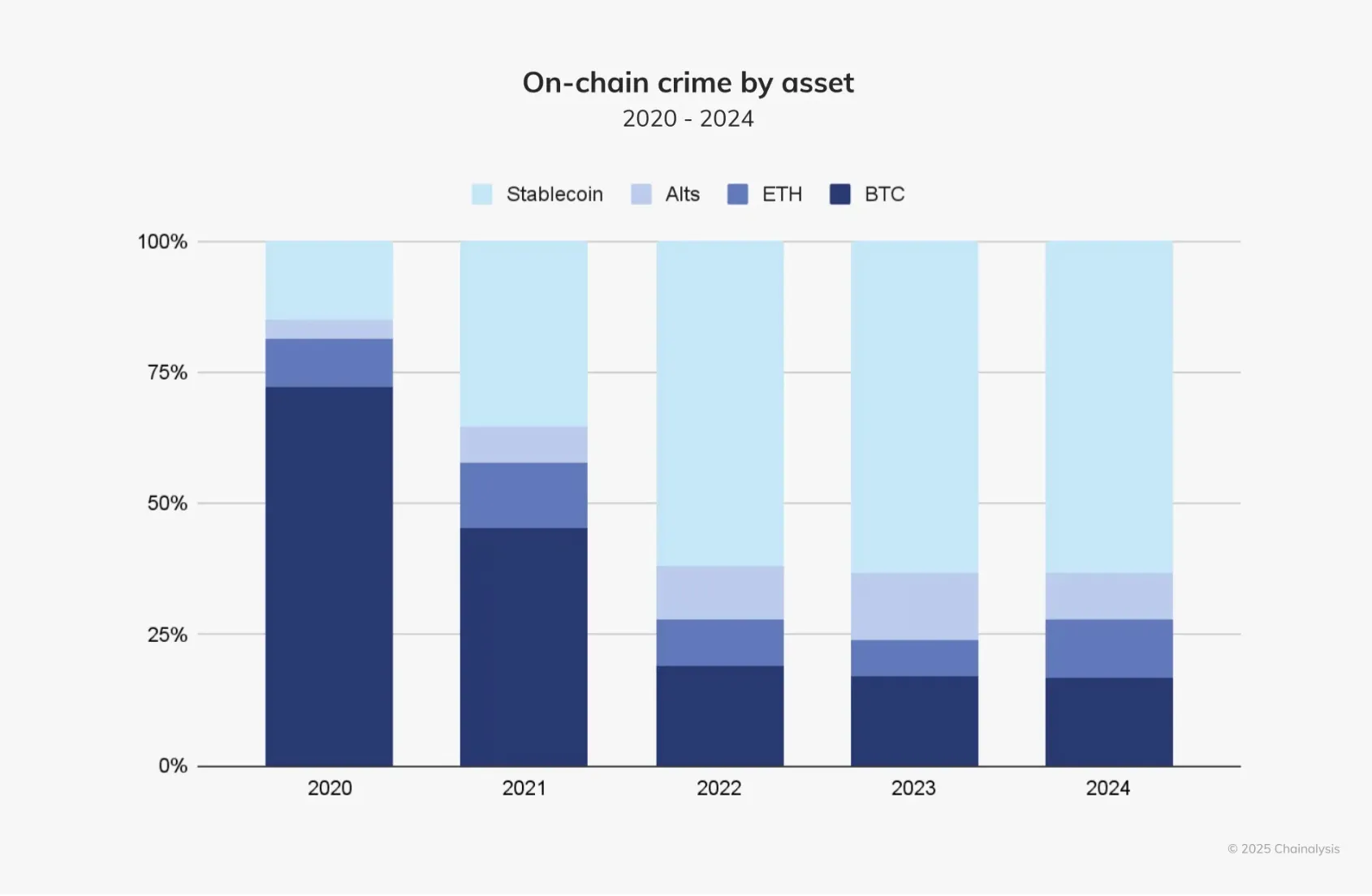

In addition, since stablecoins circulate on multiple blockchains simultaneously, it is essential to have an on-chain tracking system that can precisely analyze the distribution structure and flow of funds between chains and identify anomalies. This is where collaboration with external partners like Chainalysis, a company specializing in blockchain analytics, comes into play. Chainalysis analyzes the distribution channels of major stablecoins such as USDC and USDT in real-time, helping to identify risks such as money laundering, sanctions evasion, and hacktivism at an early stage. Through their machine learning-based transaction analysis system, they recognize sudden liquidity movements at specific addresses or chains as warning signs and take immediate action with issuers and exchanges. According to a 2024 report, there are cases where USDT and USDC have been detected moving through unusual channels, which has led to issuers taking action to freeze assets or blacklist accounts.

On-chain crime by asset

Source: 2025 Crypto Crime Trends from Chainalysis

In fact, most regulatory-friendly stablecoin issuers have built blacklisting and asset freezing capabilities into their smart contracts. Circle has the technical capability to instantly freeze addresses associated with U.S. Treasury sanctioned entities, which it utilized during the Tornado Cash scandal in 2022 to block approximately 75+ addresses. Tether has similar capabilities, and has frozen assets in hundreds of cases to help recover assets related to hack victims or in response to legal requests. While these features have been criticized by some as an invasion of privacy, they are seen as essential tools for financial regulation and law enforcement.

Issuers also need to be able to manage liquidity to stabilize the market when demand for stablecoins fluctuates. For example, in 2023, Circle took action when the Silicon Valley Bank (SVB) crisis threatened to freeze some of its reserves, immediately transferring deposited assets to other banks and reorganizing its entire liquidity. They worked closely with Fireblocks, Chainalysis, Anchorage, and others to set up a real-time response system, and through transparent information disclosure, they were able to restore market confidence. This case highlights the importance of crisis response capabilities and partnerships for issuers to operate large-scale assets.

After all, stablecoins are structured to require ongoing management at the intersection of complex financial, technical, and legal risks, even after issuance. It's not just about issuing an asset, it's about a sustainable governance system designed to ensure that it is trusted by the market and can withstand crises, which is the real competitive advantage and infrastructure capability of stablecoins. Collaborations with external analysts like Chainalysis, institutional custodians, auditors, and security technology companies are key partners in supporting these governance frameworks, and are an important foundation for stablecoins to harmonize with the global financial system.

Currently, various organizations and companies are involved in issuing stablecoins around the world, and each project is differentiated by its issuer, operating method, banking and regulatory structure. In this part, we analyze the key players that provide the issuance infrastructure for three leading bank-centric stablecoins, Tether USDT, Circle USDC, and the emerging Ondo USDY. We will analyze the actual operation of issuance infrastructure and project-specific features.

Bank-centric stablecoins operate in a “Deposit-Backed Token” structure, which is bank-centric or based on bank deposits, as opposed to the more common market-driven types (USDC, USDT, etc.). These models are often bank-centric and emphasize stability and regulatory compliance rather than profitability through asset management. Some examples include

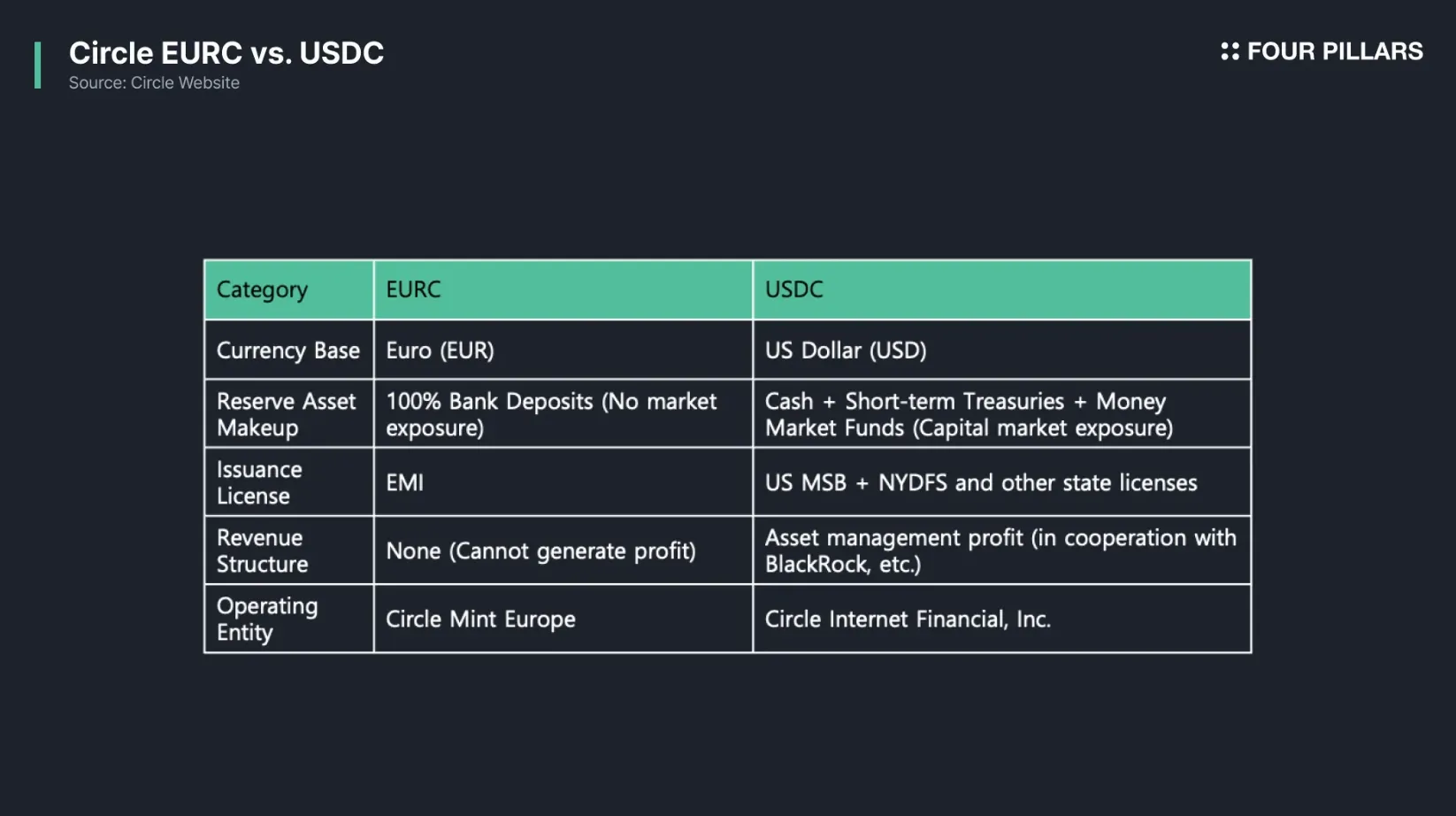

3.1.1 European Bank-Centric Stablecoins: Circle's EURC.

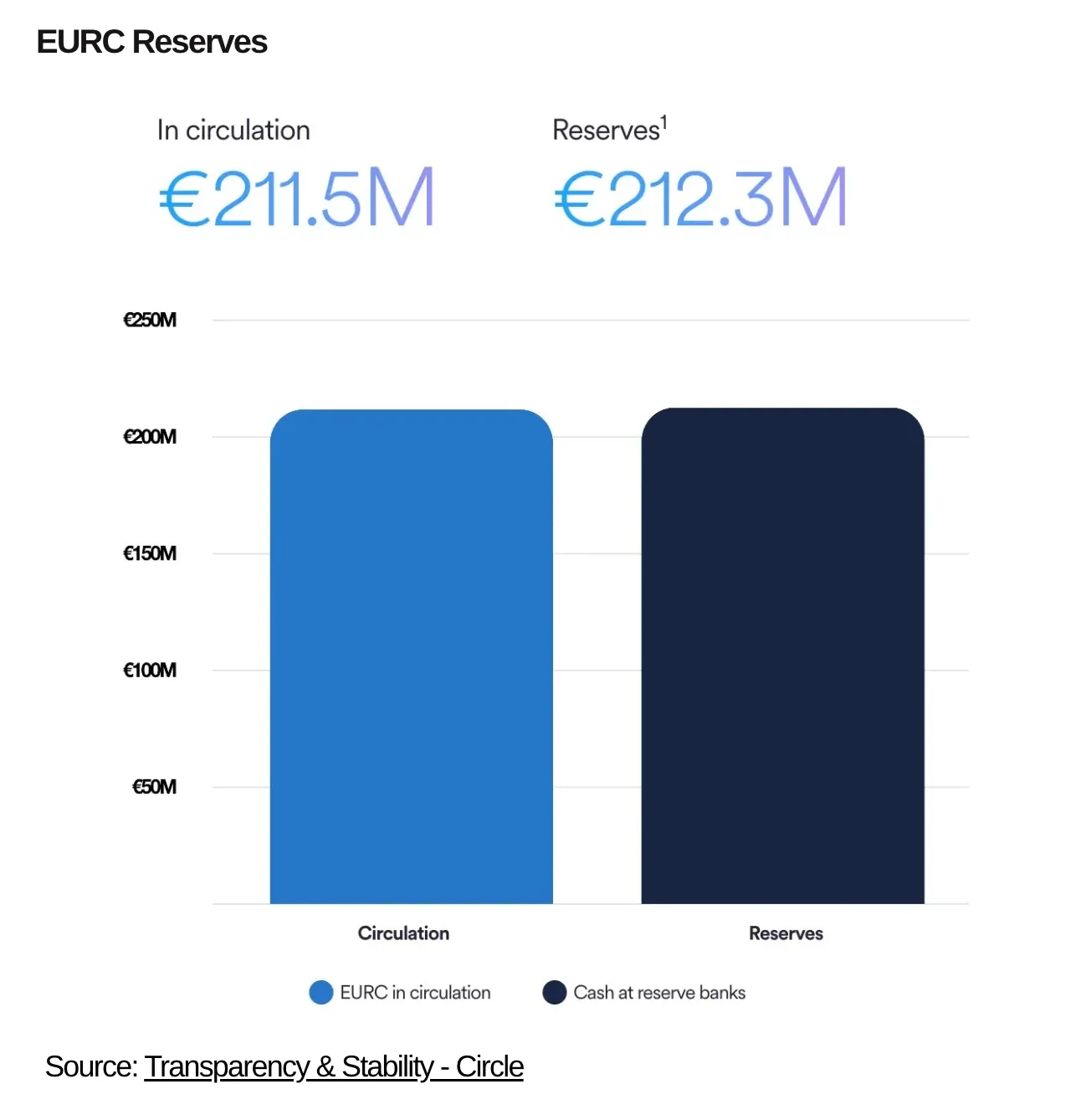

EURC, issued by Circle, is a euro-based stablecoin that is pegged to the euro at a 1:1 ratio. While this asset may appear similar to the US dollar-backed USDC, there are clear differences in the issuance structure, asset mix, revenue model, and regulatory response. In particular, EURC differs from USDC, which is a capital markets-focused stablecoin, by having a bank-based structure.

First, EURC is issued under European e-money regulations and operated by Circle's Irish subsidiary, Circle Mint Europe, through an Electronic Money Institution (EMI) license. This means that when a customer deposits Euros with Circle, the amount is deposited in full by Circle with a credit institution (i.e. a bank) in Europe, and the corresponding EURC is issued. In this process, Circle does not invest the deposited funds in financial assets such as money market funds or short-term government bonds, nor does it employ a return-seeking asset management strategy.

This structure contrasts sharply with the USDC. USDC is registered as a money services business (MSB) in the U.S., holds money transmission licenses in each U.S. state, and manages a portion of its reserves through BlackRock's short-term government bond fund (Circle Reserve Fund). This gives it exposure to capital markets and a structure to generate management fees. In contrast, the EURC prioritizes the stability and protection of customer assets and does not manage assets other than bank deposits, so its focus is on regulatory compliance and risk minimization rather than profitability. From a regulatory perspective, EURC is also designed to be compliant with Europe's MiCA regulation. MiCA is a unified regulatory framework for the issuance and operation of cryptoassets across the EU, and specifically distinguishes between Asset-Referenced Tokens and E-Money Tokens, stipulating that the latter must be issued by a bank or e-money institution. Circle is therefore operating EURC under the existing regulatory framework for E-Money Tokens and is preparing to align its reporting and disclosure obligations with that framework when MiCA is fully implemented.

EURC is a stablecoin that is not 100% bank backed and reserve backed, which distinguishes it from USDC, which is capital market backed with a yield structure. This is a strategic response by Circle to the European regulatory environment and is a prime example of how stablecoin structures can vary depending on the financial infrastructure and regulatory approach of each country.

Circle’s EURC vs. USDC: A Comparative Overview

Source: Four Pillars

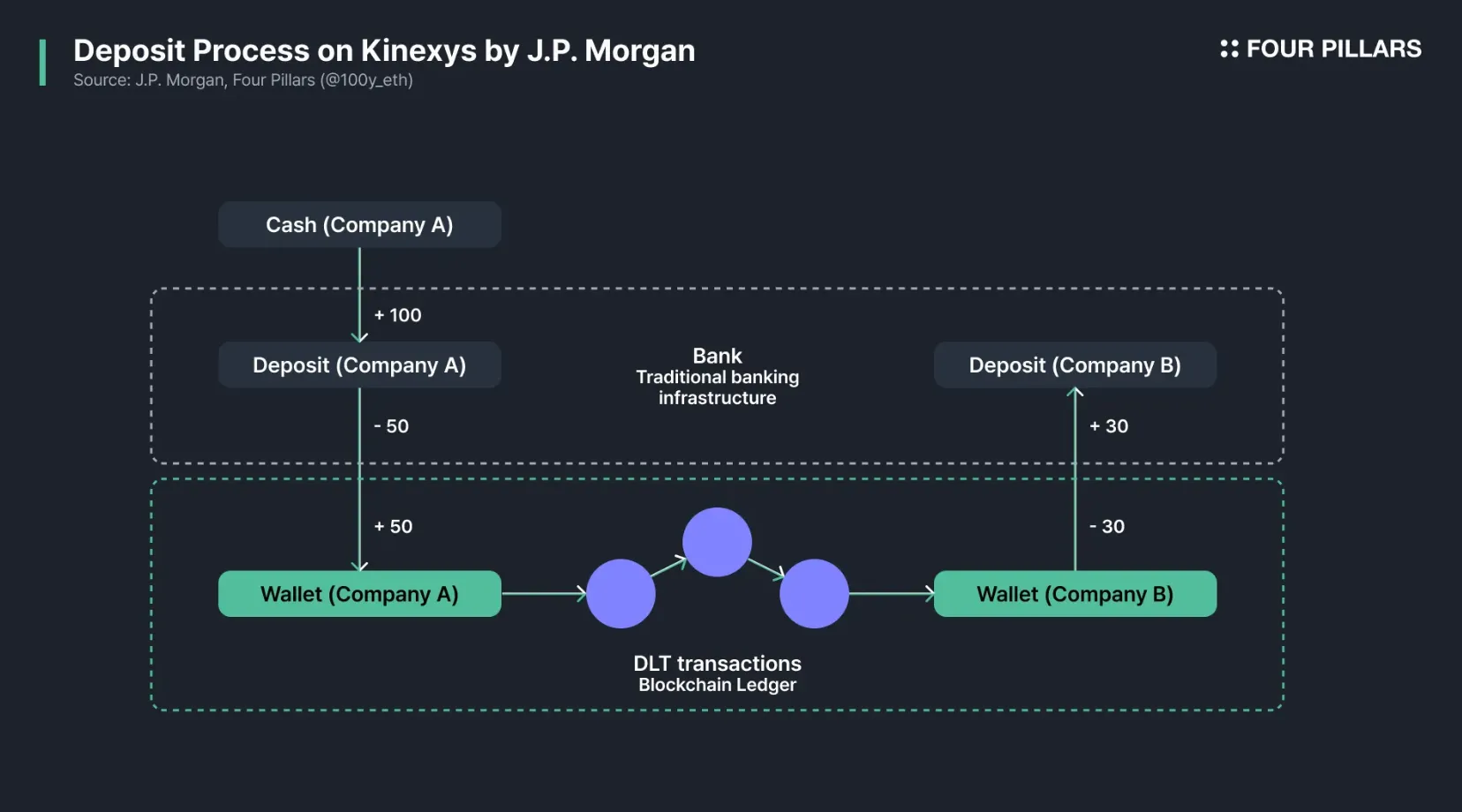

3.1.2 JPMorgan's JPM Coin in the U.S.

JPM Coin, operated by JPMorgan Chase, is a digital asset designed to support real-time payments and fund movement between institutional clients. The stablecoin is pegged 1:1 to the U.S. dollar and runs on JPMorgan's blockchain platform, Kinexys (formerly known as Onyx). JPM Coin processed approximately $1 billion in transactions per day and is utilized by corporate clients in more than 30 countries around the world.

Technically, JPM Coin was initially launched on Quorum, a private Ethereum-based blockchain, and later expanded to the Kinexys platform. The platform supports a number of financial services, including cross-border payments, securities settlement, and liquidity management. Notably, JPM Coin has also introduced support for the euro, enhancing its multi-currency payment capabilities. One of the key features of JPM Coin is its programmable payments feature. This allows payments to be automatically executed based on pre-defined conditions, automating the flow of funds for businesses and increasing efficiency. For example, companies like Siemens are utilizing this feature to automate the movement of funds between global subsidiaries.

On the regulatory front, JPM Coin is fully compliant with U.S. and international financial regulations. JP Morgan monitors all payment information in accordance with U.S. Treasury Department Office of Foreign Assets Control (OFAC) regulations and other international sanctions and anti-money laundering laws. In addition, JPM Coin is considered a bank deposit for legal purposes and operates within the existing financial regulatory framework.

JPM Coin is a prime example of a stablecoin issued and regulated directly by a bank, and is expected to play an important role in the future development of digital asset-based financial infrastructure. Like Kinexys' recent transfer of assets to Ondo Finance's public blockchain, JPM Coin has the potential to be linked to a public blockchain.

Deposit Process on Kinexys by J.P. Morgan

Source: Deposit Tokens | Kinexys by J.P.Morgan

3.1.3 Tochituka Coin by Fukuoka Bank in Japan

Hokkoku Bank launches Japan's first deposit-backed stablecoin

Tochituka Coin is Japan's first deposit-based stablecoin, launched in 2024 by Hokkoku Bank, a regional bank in Ishikawa Prefecture, Japan. The digital currency is backed by existing bank deposits on a 1:1 basis, and customers of Hokkoku Bank can top up their tokens through the Tochituka app and use them as a form of payment at local stores. The app was originally developed in collaboration with Suzu City and designed to allow citizens to earn and redeem “Tochituka” points through volunteer activities, and now serves as a wallet for Tochika.

Technically, Tochituka operates on a private blockchain infrastructure developed by Japanese blockchain company Digital Platformer. Tochituka is currently only available within Ishikawa Prefecture, and users can exchange up to one currency for free per month, after which a fee of 110 yen will be charged. Hokkoku Bank plans to expand its reach by collaborating with other local banks and introduce person-to-person remittance functions within the app in the future.

One of Tochituka’s main goals is to “digitize Japan's cash-centric payment culture.” Hokkoku Bank is offering a low fee rate of 0.5% for Tochituka payments to help small businesses avoid paying high card payment fees. It is also encouraging businesses that issue paper gift certificates to switch to a digital points-based payment system. This approach is contributing to the digital transformation of the local economy and providing an efficient payment method for both consumers and businesses.

On the regulatory front, Japan's revised Payment Services Act (PSA) of 2023 defines stablecoins as “Electronic Payment Instruments” and allows only three types of institutions to issue stablecoins: banks, money transmitters, and trust companies. Since Tochka is issued using bank deposits as collateral, it operates legally under this law.

Tochituka is seen as a leading example of the convergence of Japan's traditional financial system and blockchain technology to drive digital transformation in local communities. Hokkoku Bank's initiative demonstrates the practical applications of stablecoins and is expected to serve as an important reference model for other financial institutions in Japan to adopt digital currencies in the future. In particular, Tochituka’s role in revitalizing the local economy and promoting financial inclusion is noteworthy.

USDCs are legally issued by Circle, which has substantial operations and is licensed as a money transmitter and money service business (MSB) in several U.S. states. Reserves are maintained at 100% cash and short-term U.S. Treasuries, with all reserves held at U.S. regulated financial institutions. After 2023, a significant portion of the reserves are invested in BlackRock's Circle Reserve Fund (an SEC-registered money market fund), and cash is held at BNY Mellon Bank. The issuer publishes a monthly reserve certification report through its accounting firm (formerly Grant Thornton), which provides transparency by detailing the breakdown of reserve assets and the duration of government bonds.

Stablecoin Issuance Pipeline - Circle USDC

Source: Four Pillars

3.2.1 Operating Entity and Related Legal Framework.

Initially governed through the Centre Consortium, which was co-founded by Circle and Coinbase Exchange in 2018, a restructuring in August 2023 resulted in Circle taking full responsibility for USDC issuance and operations. The Center Foundation no longer exists as a separate entity, with Circle bringing all USDC-related governance and smart contract key management in-house. Coinbase maintains an equity investment in Circle and a revenue-sharing partnership, but the issuing entity is now clearly Circle as a company.

Circle is a private, for-profit company (in the form of a corporation) and is not a bank. Instead, it is regulated and compliant with Money Transmitter licenses in each U.S. state and operates as a cryptocurrency business (BitLicense) in New York and elsewhere. There are several regulated entities under the Circle umbrella, and they are issued through regulated entities.

Regulators are likely to recognize USDC as a “payment stablecoin” or a payment instrument similar to e-money. In fact, in the US, USDC is classified as a prepaid stored value, not a security or fund, and is subject to state-by-state money transmitter regulation. The legal gray area is that in the US, USDCs function similarly to banks, even though they are not bank deposits. There is no deposit insurance protection and they don't fit neatly into the existing banking legal framework, leaving a gap in federal law. In response, Circle has voluntarily disclosed its reserve information and is cooperating with authorities, but ultimately is in a state of interim compliance until future legislation clarifies.

USDCs are not deposits, so they are not FDIC insured and there is no government guarantee of the collateral. While Circle is 100% reserve funded, which is fine for now, there are few protections in the event of unexpected losses (e.g., loss of some deposits due to bank failure). During the SVB crisis in 2023, Circle responded by declaring that it would cover the shortfall with corporate funds, but this was a voluntary measure, not a legal obligation. The fact that Circle is not legally obligated to do so is also a potential risk.

3.2.2 Collateral Validation and Proof of Reserve Structure

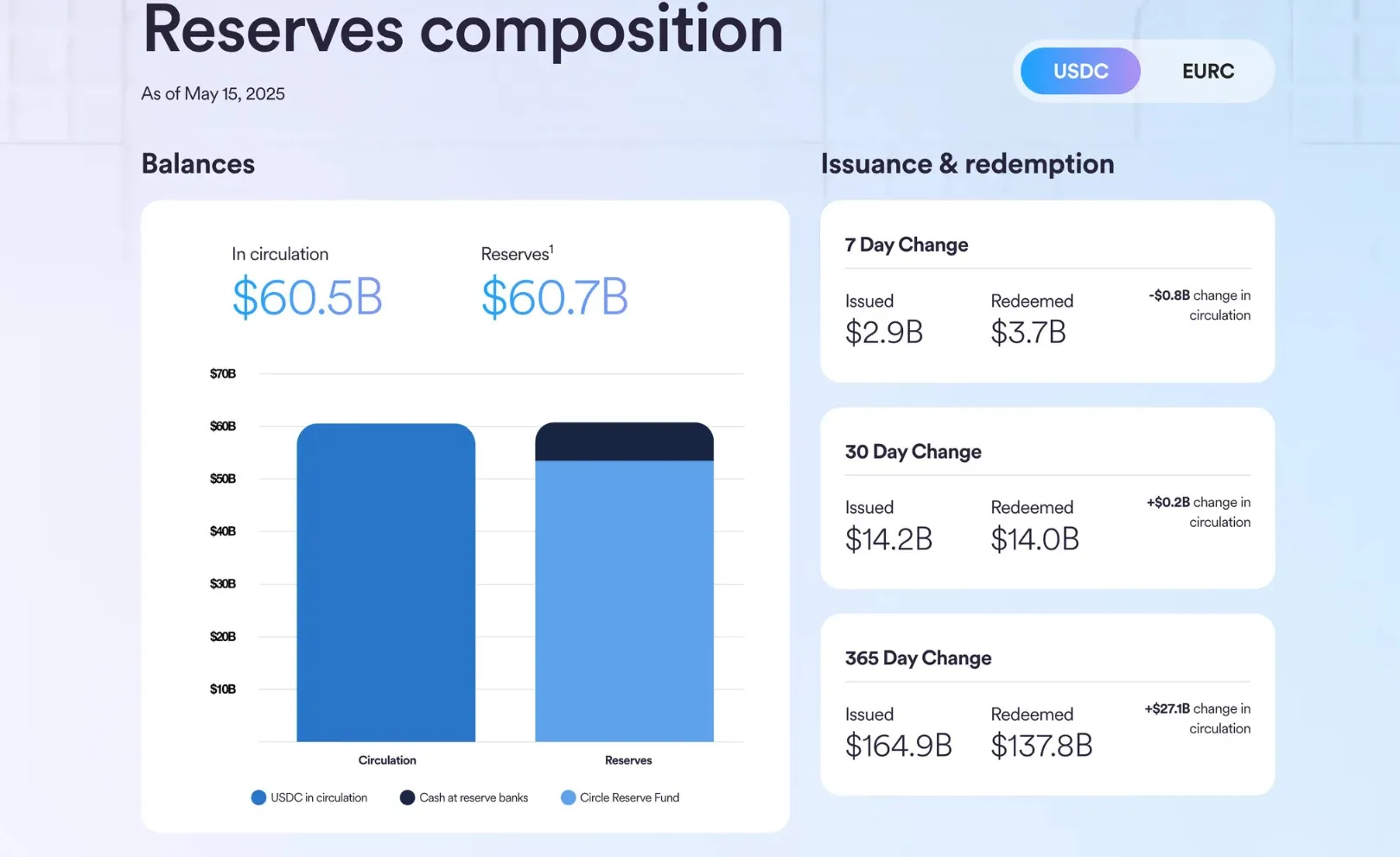

The collateral for USDC consists of cash and cash equivalents, including short-term U.S. Treasuries. Since September 2021, Circle has simplified its collateral portfolio, moving to a policy of backing 100% of USDCs with cash or cash equivalents with maturities of 90 days or less. Currently, about 90% of the reserve is held in short-term U.S. Treasury securities (Treasuries) and overnight repurchase agreements (repos), with the remaining 10% held in cash to provide immediate liquidity. According to Circle, as of early 2025, short-term Treasuries/Repos account for about 90% of total reserve assets and cash accounts for 10%, with about 90% of the cash held at global systemically important banks such as JPMorgan and BNY Mellon.

USDC's transparency data is available via weekly updates and monthly reserve reports and audit opinions on the Transparency page of Circle's homepage. As of 2025, Circle publishes its reserves on a weekly basis, with monthly assurance reports from Big 4 accounting firms such as Deloitte. In addition, the Circle Reserve Fund, managed by BlackRock, publishes a daily list of government bonds held through the Circle Reserve Fund, providing a high level of transparency into its reserve assets.

In March 2023, Circle temporarily lost access to some of its reserves due to the bankruptcy of Silicon Valley Bank (SVB), which caused the value of USDC to fall below $1 for a short period of time, but was restored to normalization following deposit protection measures by U.S. authorities. This prompted Circle to shift to a more conservative approach to reserve management.

USDC Reserves composition

Source: Transparency & Stability - Circle

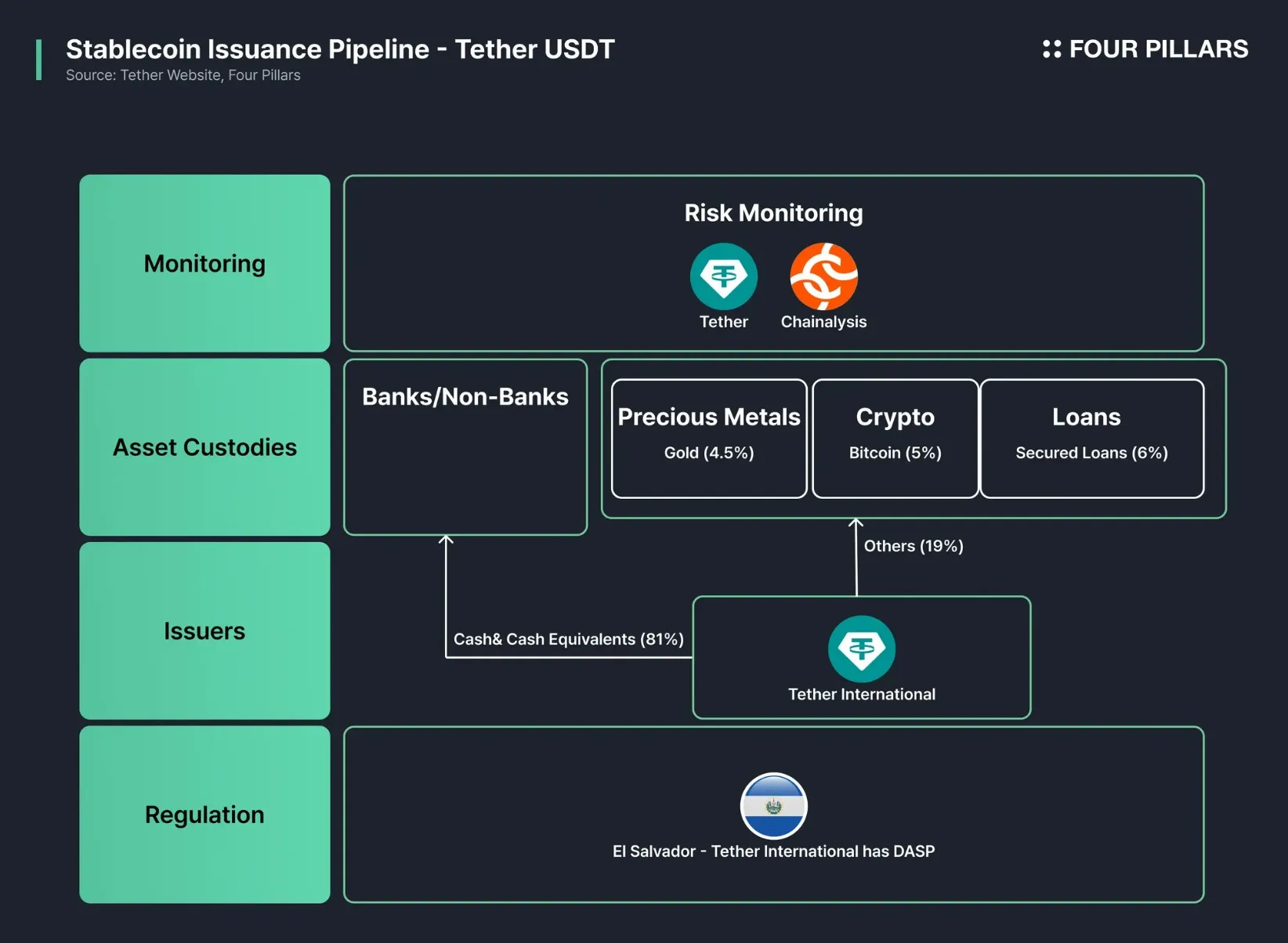

Tether USDT, the #1 stablecoin by market capitalization, was launched in 2014 and currently has over $150 billion in tokens in circulation. USDT is issued on a total of 12 blockchains (Ethereum, Tron, Solana, etc.) and holds approximately 85% of its reserves as of 2023 in cash, cash equivalents, and U.S. Treasuries. Tether was once controversial for its reserve transparency, but it now regularly discloses its collateralized assets and has said it will release audit reports from a Big 4 accounting firm.

Stablecoin Issuance Pipeline - Tether USDT

Source: Four Pillars

3.3.1 Operating Entities and Related Legal Frameworks.

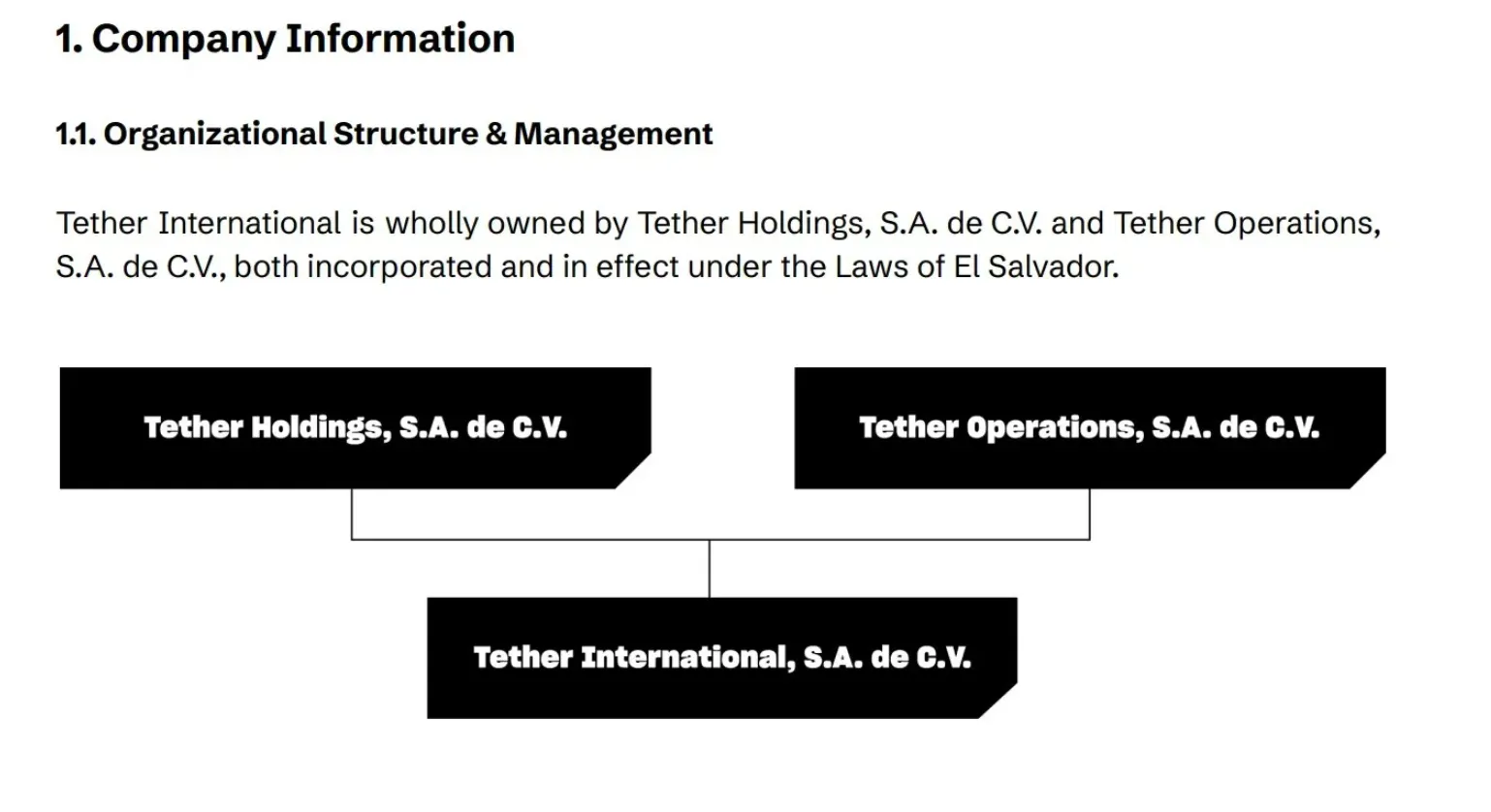

In January 2025, Tether (USDT) reorganized its legal structure by relocating its headquarters and principal operating entities to El Salvador. Previously headquartered in the British Virgin Islands (BVI), Tether established its physical headquarters in El Salvador after obtaining a Digital Asset Service Provider (DASP) and Stablecoin Issuer license in El Salvador. Being licensed as a digital asset service provider and stablecoin issuer means that a company is officially authorized by the El Salvadoran government to legally provide a range of services for digital assets (e.g., Bitcoin, Ethereum, etc.) and stablecoins. This authorization allows companies to operate a range of financial services, including spot and derivatives trading in cryptocurrencies, staking, savings and investment products, and stablecoin issuance and distribution, in a transparent manner and in compliance with local regulations.

The entity responsible for operating Tether has now transitioned to Tether International S.A. de C.V., a company incorporated in El Salvador. The company is listed in the El Salvador Commercial Registry, is licensed as a Digital Asset Service Provider (DASP) and Stablecoin Issuer, and serves as the issuing entity for Tether's dollar, renminbi, and peso-linked tokens (USDT, CNHT, MXNT). Tether International is wholly owned by two El Salvadoran entities, Tether Holdings S.A. de C.V. and Tether Operations S.A. de C.V., collectively referred to as the Tether Group. The structure is organized with a parent company (Tether Holdings) and an operating company (Tether International) in El Salvador.

Company Information - Tether

Source: Relevant Information Document - Tether International S.A. de C.V.

However, in the eyes of regulators in other countries, Tether is recognized as a foreign entity outside of traditional financial regulation. In 2021, a U.S. CFTC investigation found that Tether-related entities had been fined in the past for violating the Commodity Exchange Act (CEA), and that Tether had been operating in the U.S. without a specific financial regulatory license. In a settlement with the New York State Attorney General (NYAG), Tether agreed to cease operations in New York and to submit regular reports. In short, the regulator's view is that it is not fully integrated into the regulatory framework of any major country. S&P Global has assigned Tether a stability rating of “Constrained (Grade 4)”, citing the “lack of a regulatory framework” and “the issuer's opaque risk appetite.

However, Tether's approval by the El Salvadoran government under the country's new Digital Assets Law of 2023 could be seen as a step toward filling the regulatory gap. Outside of El Salvador, however, Tether is still considered an unauthorized private stablecoin, and regulators in other countries have limited monitoring and indirect sanctions without a full understanding of its structure. Most regulators view Tether as a de facto unregulated entity operating under a complex governance structure of international entities, which is a risk factor.

3.3.2 Collateral Verification and Proof of Reserve Structure

Tether Reserves

Source: Tether Transparency

Tether (USDT) is a capital markets-based stablecoin that holds at least 100% of its tokens in a variety of collateralized assets of equal value for every token issued, meaning that it is designed to maintain the value of $1 USDT by holding the equivalent of USDT in circulation in reserve. Tether discloses the status of these reserves through daily balances and quarterly reports. Recent publicly available data shows that Tether holds the majority of its reserves in cash and cash equivalents, and reports that its actual reserves are greater than the total value of its issued tokens. For example, as of March 2025, approximately 81% of Tether's reserves consisted of highly liquid assets such as cash and short-term government bonds.

Tether has yet to undergo a formal audit, but instead releases quarterly Attestation reports from accounting firms such as BDO Italy to provide third-party verification of its reserves. Beginning in Q1 2023, Tether will introduce a new categorization to further transparently disclose its reserves, breaking them down into gold holdings, Bitcoin holdings, corporate bonds, and repos. Tether claims to have internally verified the stability of its reserves through market stress tests, and in response to community requests, the company has revamped its structure to reduce risk factors such as collateralized debt obligations and ensure that reserves are fully covered by excess capital. On the other hand, there is no cryptographic Proof of Reserve (PoR) system that users can verify directly on-chain in real-time.

3.3.3 Tether's Risks

There are several gray areas in Tether's legal status and structure.

First, investor rights are unclear. It is not clear what legal claims Tether holders have against the company. While bank deposits have depositor protections and securities have legal rights, USDT token holders have no direct rights to reserves, only a contractual relationship that allows them to “request a one-for-one exchange” with Tether. However, even this commitment is limited by the user agreement, and according to the New York Agreement, Tether has the right to refuse or delay redemptions at its discretion. This creates a gray area where stablecoin holders are not legally protected.

Second, the reserve is bankruptcy-insulated. S&P and legal experts point out that in the event of Tether's bankruptcy, token holders may not be protected in favor of general creditors because the reserves are not sequestered in a separate trust structure. This remains a legal void.

Third, oversight blind spots can be exploited. For example, there have been concerns about Tether being used to launder criminal money around the world or to evade sanctions, which Tether has responded to by self-regulating itself by freezing transactions (and in some cases blacklisting suspicious addresses), but law enforcement ambiguities remain.

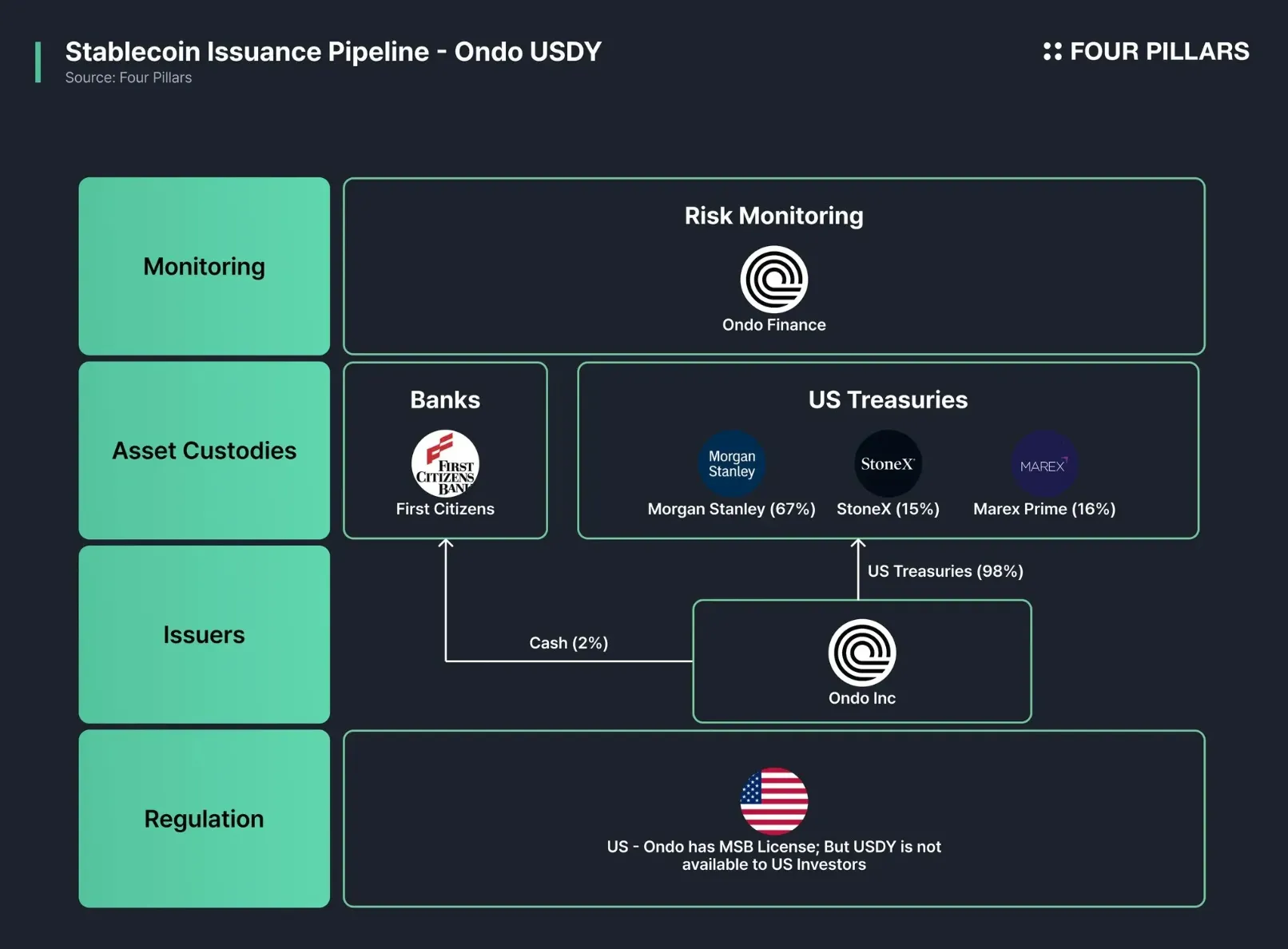

Stablecoin Issuance Pipeline - Ondo USDY

Source: Four Pillars

3.4.1 Operating Entity and Relevant Legal Framework.

Ondo USDY LLC is incorporated and operated in the United States, but is not selling to U.S. persons pursuant to Reg S requirements. We are only selling tokens to non-residents of the United States to comply with U.S. securities laws. The parent company, Ondo Finance, Inc. is a technology company headquartered in New York, USA and was founded in 2021. Ondo has also established the Ondo Foundation for decentralization, and a subsidiary of the foundation has announced that it holds a 99% stake in Ondo USDY LLC. However, day-to-day USDY issuance/redemption and collateral management will be performed by Ondo Inc.

From a U.S. Treasury perspective, USDY is issued and exchanged in the form of virtual assets and therefore requires registration as a money transmitter (MSB). In fact, Ondo USDY LLC is federally registered as an MSB to comply with anti-money laundering (AML) regulations. For example, under the EU's MiCA regulation, USDY may qualify as an asset reference token (ART) or an electronic money token (EMT), but this is open to interpretation as USDY is structured as a security, which distinguishes it from a typical stablecoin.

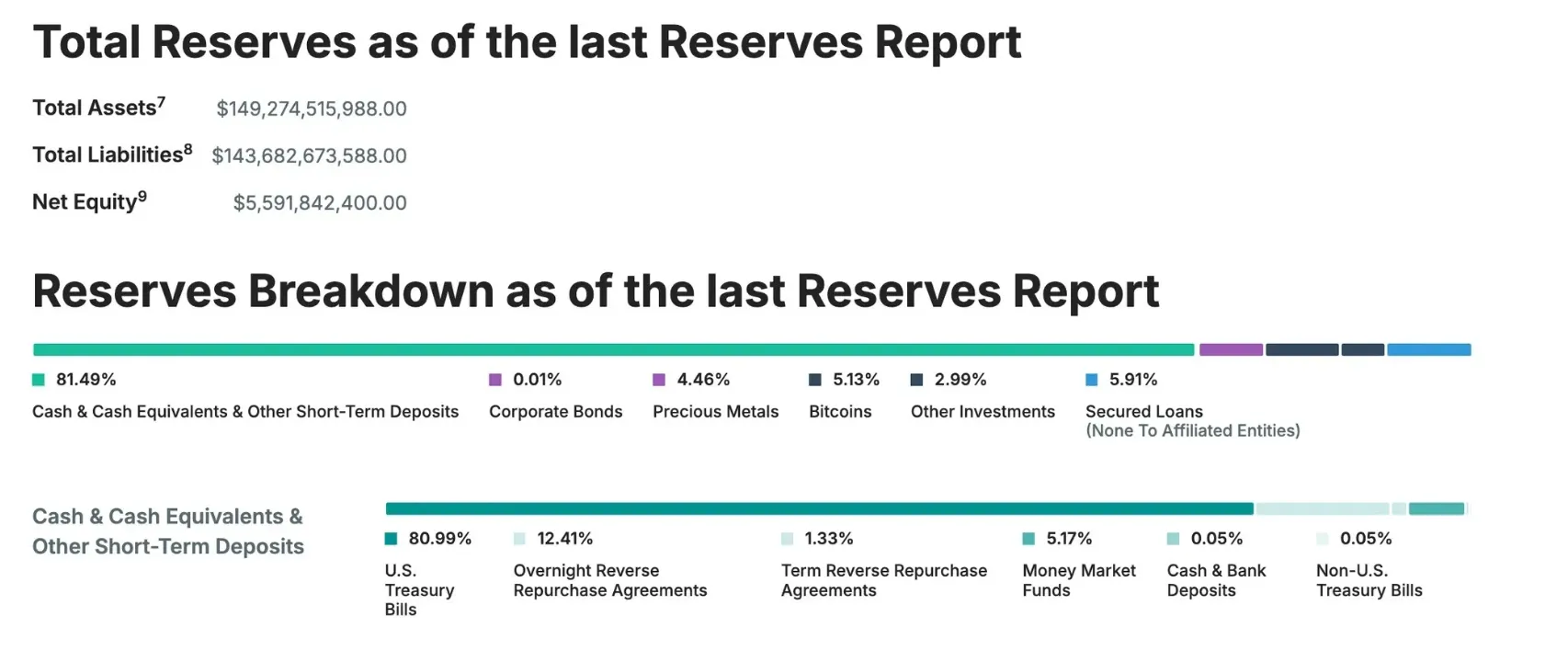

3.4.2 Collateral Verification and Proof of Reserve Structure

Ondo has implemented several measures to increase the transparency of USDY reserve assets and protect investors. First, all USDY tokens are issued with at least 100% overcollateralization (approximately 3-4% overcollateralization), meaning that for every $100 worth of tokens issued, at least $103 of underlying assets are secured, and this collateralization ratio is checked at the end of each quarter for any abnormalities. We have also engaged an independent third-party organization, Ankura Trust, to verify and report on the collateral every business day. At the end of each month, we provide a detailed metrics report, which is also verified by Ankura. Collateralization is publicly available on the Ondo website, where users can track the size of U.S. Treasury holdings and deposits in real-time.

USDY's Treasury and deposit collateral is held off-chain in accounts with large U.S. financial institutions. Ondo USDY LLC holds U.S. Treasuries on deposit with Morgan Stanley and StoneX, and has opened a depository account with First Citizens Bank for depository operations. The Treasury securities are held in “cash custody” accounts at Morgan Stanley and StoneX, where they are not recycled and are safely segregated. Ankura Trust, as the collateral management organization, has control agreements with these custodians and banks and has established a legal security interest in the collateral assets. This ensures that if anything goes wrong on the Ondo side, we have the legal right to freeze/recover the collateral assets and repay token holders.

The global stablecoin market is dominated by U.S. dollar-based issued coins, while some countries, such as Japan and Europe, are approaching stablecoins led by traditional financial institutions such as banks. The two models differ greatly in terms of issuers, regulatory frameworks, and scope of use, with the U.S. model being considered superior in terms of flexibility and scalability.

With the rapid growth of stablecoins, governments and regulatory authorities are also working on regulatory frameworks and pilot projects for issuance infrastructure. In Asia and Europe, a variety of approaches are emerging, from introducing regulatory sandboxes to formalizing legislation, which are aligned with national financial strategies. This part of the report highlights key trends in Hong Kong, Japan, and the European Union (EU).

4.1.1 Progress on stablecoin legislation in the U.S.

In the U.S., federal legislative discussions on stablecoins have been in full swing since 2023, and by early 2025, the results are beginning to be seen. The “Clarity for Payment Stablecoins Act”, introduced in the House of Representatives, is the first bill to clarify the legal status of privately issued stablecoins, limiting their distribution to licensed issuers under the supervision of the Federal Reserve. The bill aims to bring stablecoins into the traditional financial system through a conservative regulatory framework, including a 100% reserve requirement, transparent disclosure requirements, and a prohibition on the inclusion of risky assets.

In the first half of 2025, a companion bill, the Genius Act, gained traction in the Senate. The bill would give the Fed and the Office of the Comptroller of the Currency (OCC) licensing and supervisory authority over stablecoin issuers, and would create a dedicated licensing regime for “payment stablecoin issuers” separate from the existing banking licensing regime. Notably, the bill also allows for issuance by non-banking entities, while strengthening anti-money laundering (AML) and counter-terrorism financing requirements, as well as mandating monthly audits and reserve transparency, which opens up new opportunities for fintech and blockchain companies. In fact, major players such as PayPal, Circle, and Coinbase have lobbied heavily in support of the bill. The bill has been delayed due to some opposition from Democrats (including former President Trump's ties to crypto businesses and concerns about lack of consumer protections), but with additional amendments (including AML enhancements and limits on big tech issuance), another vote is expected after Memorial Day (May 26).

However, the U.S. legislative debate still faces structural challenges of political compromise and state-federal authority alignment. For example, some states, such as New York and Wyoming, already have their own regulatory frameworks for stablecoin issuance, and there is no consensus on whether the federal bill would supersede or parallel these state licenses. As a result, the final implementation phase will require more sophisticated design, including avoiding legal duplication, overhauling authorities, and providing grace periods for existing issuers. Overall, however, there is a strong will to institutionalize the stablecoin market, and the US regulatory framework is likely to serve as a global reference point in the future.

4.1.2 Banking and Institutional Investors

Bank of America (BoA), whose CEO stated in early 2025 that the bank is ready to launch its own dollar coin if stablecoin legislation passes, and other global banks such as Standard Chartered and HSBC are also researching tokenized deposit and payment coins. In March 2025, U.S. banks Custodia and Vantage became the first U.S. banks to issue and redeem bank deposit tokens (Avit) on the public Ethereum network, demonstrating the potential for bank-led stablecoins. During the pilot's eight experimental transactions, the two banks confirmed low fees, fast settlement, and programmable money features, and announced that they worked closely with regulators to create legal best practices, including compliance with BSA/AML requirements.

Meanwhile, asset managers are also innovating with stablecoins. BlackRock, the world's largest asset manager, has been a strategic investor in Circle since 2022, managing USDC reserves, and in 2023 launched a tokenized money market fund (BUIDL), distributing $1.7 billion in fund shares as tokens across seven blockchains, including Ethereum and Solana. BUIDL will allow institutional liquid funds to be traded and redeemed directly on the blockchain, and investors will also be able to exchange their fund shares for USDC. Larry Pink, CEO of BlackRock, said, “The next financial market disruption is the tokenization of securities,” and is looking to strengthen the link between stablecoins and traditional finance by tokenizing short-term assets such as MMFs.

As such, banks and other large financial institutions are leveraging the potential of stablecoins to streamline payments (international remittances, internal capital flows), securitize assets (fund tokenization), and manage liquidity. However, regulatory uncertainties have not been fully resolved, so most of these programs are piloted and limited in scope.

There is a Wide Spectrum of Digital Money Implementations(institutional investors)

Source: : TBACCharge2Q22025

4.1.3 Fintech and Big Tech

Fintechs in the payments and remittance space are actively adopting stablecoins as a means to improve user experience and reduce costs. The aforementioned Stripe began utilizing USDC to settle in-store payments in 2022, and in 2023, it began offering USDC payouts to platform workers in African and Asian countries. In 2024, Stripe acquired the Bridge platform, integrating stablecoin support into its core infrastructure and working with Visa to implement direct card payment integration to accelerate cross-border transfers.

Paypal launched its own stablecoin, PYUSD, in 2023, enabling its 250 million users to send and receive dollar tokens and pay for goods. It's the first consumer-facing stablecoin issued by a traditional payments company, and it's freely convertible to $1 within the Paypal wallet and compatible with the Ethereum network. Crypto platforms such as Robinhood and Kraken have gone a step further, announcing the formation of the Global Dollar Network (GDN) and the joint launch of the USDG stablecoin in 2024. The USDG will be issued in Singapore by Paxos and will be designed to benefit the partners economically through the formation of a governance board by the participating companies. This is an example of a consortium approach to stablecoins, rather than a single company, and contrasts with the approach of individual companies such as PayPal. Social media companies, including Meta, are also exploring the adoption of stablecoins to facilitate payments.

Meanwhile, crypto exchanges are building 24/7 payment networks using stablecoins. Coinbase, for example, offers USDC-based cross-border money transfers, and card companies are also getting into the stablecoin space with Mastercard's Crypto Card program and Visa's USDC payment settlement pilot. Payment processors like Stripe and Square are using stablecoins as back-end settlement currencies to enable low-cost cross-border payments that bypass the card networks.

As such, the fintech industry is embracing stablecoins as part of the next-generation financial infrastructure, creating more convenient services for users and lower cost structures for themselves.

4.1.4 Future Directions

In the U.S., traditional financial institutions are currently adopting stablecoins mainly for internal efficiency and asset tokenization, while fintech companies are adopting them to innovate global remittance and payment services. The actions of JPMorgan, BlackRock, and others show that stablecoins are evolving into financial market infrastructure rather than just crypto products. On the other hand, fintech examples show how stablecoins are being integrated into the daily lives of ordinary consumers and merchants. For example, shoppers in South America are using stablecoins to pay for Visa cards, and online freelancers are getting paid in USDC without a bank account. While these changes are positive in terms of expanding financial access and reducing costs, they also increase the potential for illegal activities (e.g., money laundering, tax evasion) to take advantage of regulatory gaps and need to be managed.

In addition, the recent passage of the Genius Act in the U.S., which has passed the Senate and is now in the final legislative stages, will provide a clear federal regulatory framework for the U.S. stablecoin market and significantly improve institutional stability. However, political issues and further debate on detailed regulations remain, and further adjustments will be necessary before the Act is actually implemented.

4.2.1 Japan - Bank-Based

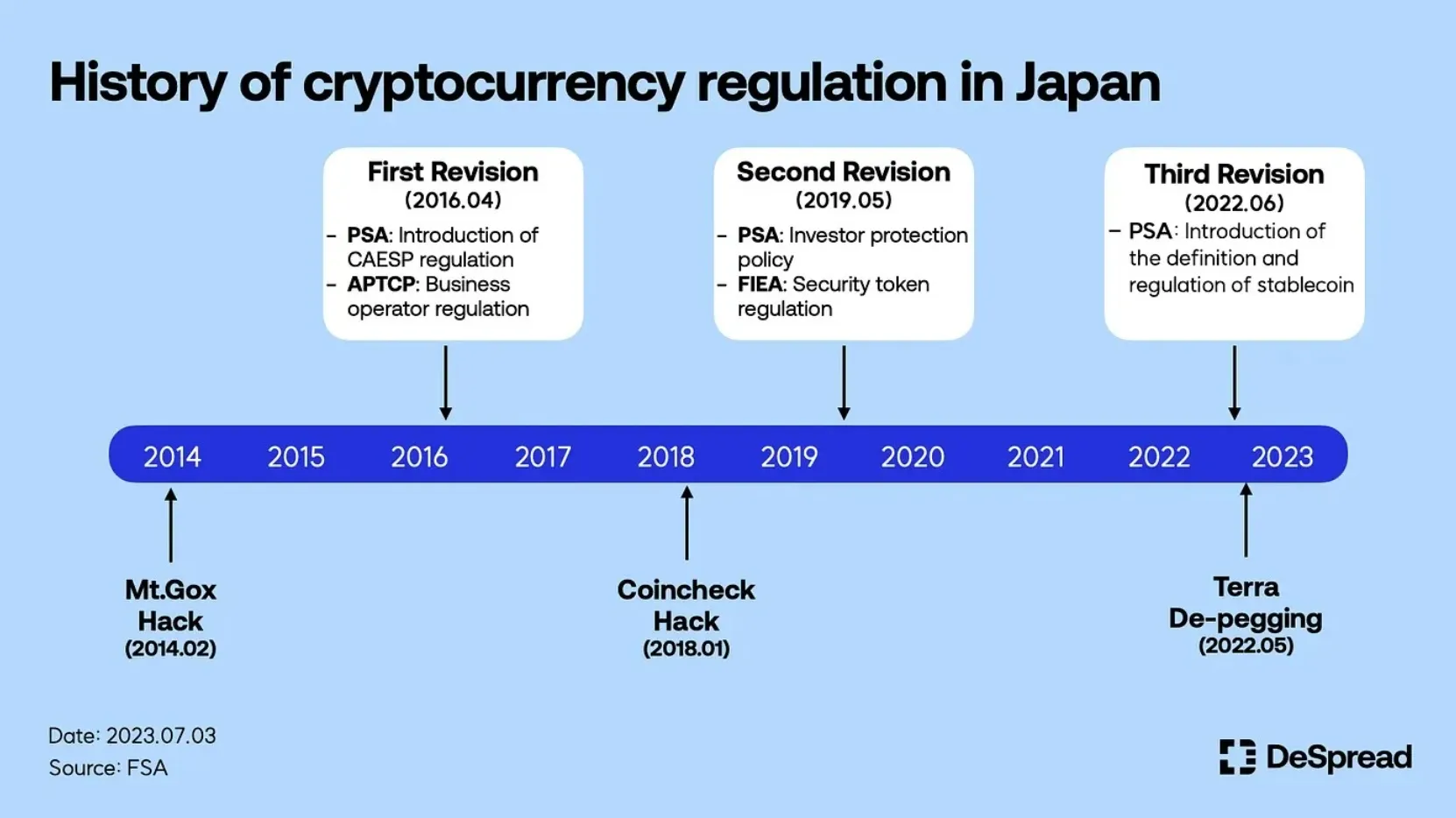

History of cryptocurrency regulation in Japan

Source: An Overview of Japanese Stablecoin Regulation | by Declan Kim | DeSpread Blog

Japan is leading the way in terms of regulation, passing a stablecoin law in June 2022 that will take effect in June 2023. The revised Financial Instruments and Exchange Act defines stablecoins as “electronic payment instruments” and strictly limits issuance qualifications. The issuer requirements stipulate that only general banks, registered money transmitters, and trust companies can issue yen-linked stablecoins, which ensures that only authorized financial institutions can be the issuing entity. It also stipulates a 1:1 par value redemption right guarantee, allowing users to exchange their tokens for fiat at any time. The reserve assets were also limited to safe assets, and accounting and reporting requirements were imposed.

After the law was enacted, Japanese banks and companies began preparing to issue stablecoins. Mitsubishi UFJ Financial Group (MUFG) has developed its own “Progmat Coin” platform to enable banks to issue stablecoins in yen and other currencies, while Sumitomo Mitsui Banking Corporation (SMBC) and Mizuho Banking Corporation (MBC) are also participating in cross-border stablecoin payment pilots. Japan also plans to allow the distribution of foreign stablecoins, such as USDT and USDC, issued overseas, and in 2023, regulations were revised to allow domestic companies to register as distribution entities and sell them if they meet certain requirements. Overall, Japan is implementing regulations that limit issuers to licensed institutions and prioritize user protection and redemption guarantees, while simultaneously experimenting with market activation (such as the banking union project).

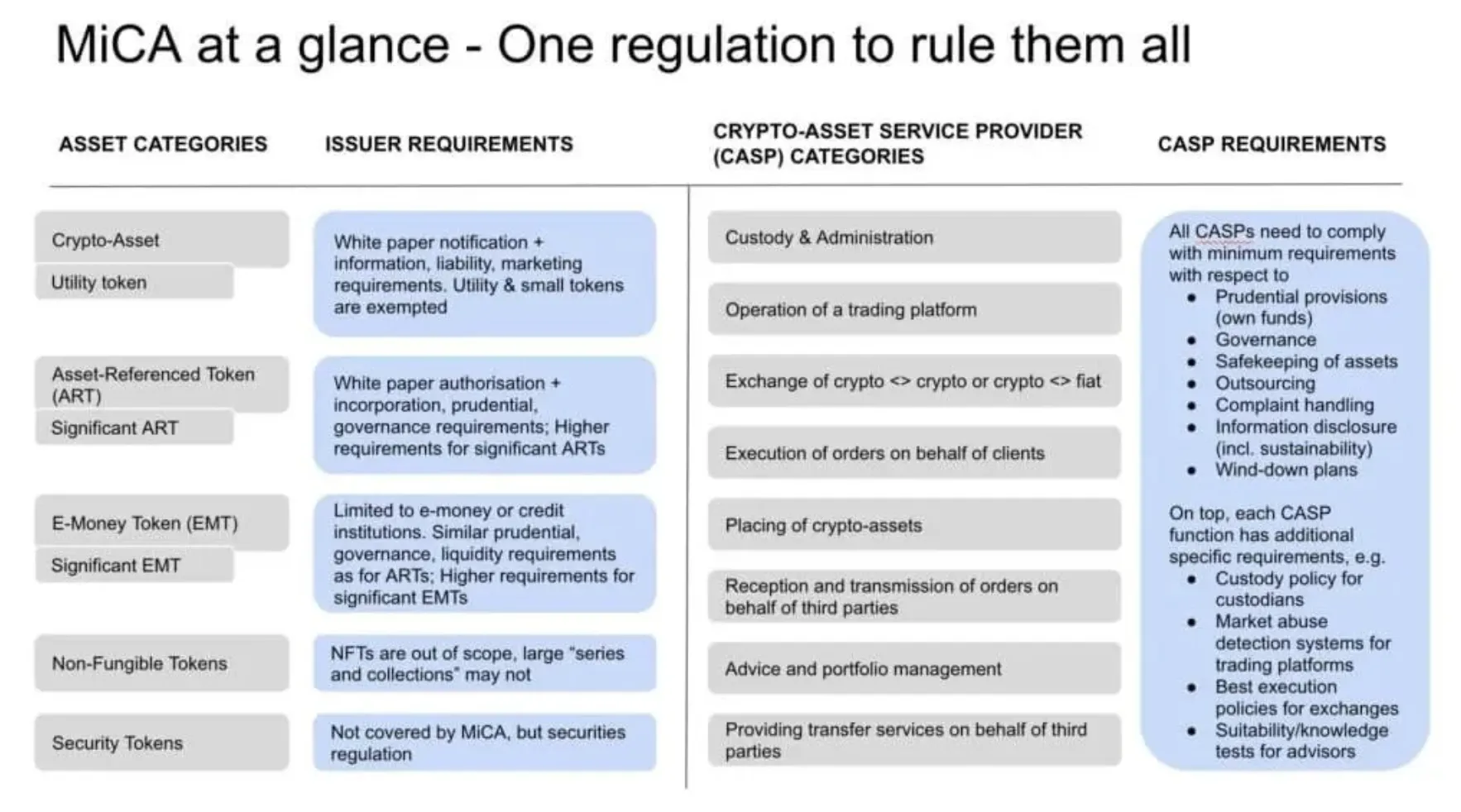

4.2.2 The European Union (EU): Unified regulatory framework with MiCA

MiCA at a glance - One regulation to rule them all

Source: MiCA goes live in Europe as the crypto regulatory framework starts with stablecoins

In June 2023, Europe finalized the Markets in Crypto-Assets (MiCA), a pan-EU crypto-asset regulation bill, establishing a harmonized stablecoin regulatory framework across member states. MiCA came into effect in phases starting in late 2024 and divides stablecoins into two categories: e-money tokens (EMTs) and asset reference tokens (ARTs). EMT (E-money Token) is a stablecoin pegged to a single fiat currency, with a structure of 1 euro = 1 token. Asset-Referenced Tokens (ARTs) are a type of multi-collateralized stablecoin that can be pegged to multiple currencies or non-currency assets (such as commodities).

In both cases, they are considered “cryptoassets intended to maintain stable value” and are subject to extensive issuance regulations. The key requirements are that the issuer must be authorized in advance (white paper submitted and approved) and incorporated in the EU. There are capitalization requirements, maintenance of 100% liquid assets in reserve, transparent white paper disclosure and real-time reserve reporting, and reserve assets must be deposited in a safe haven on a 1:1 basis.

In addition, designation as a “significant stablecoin” with large trading volumes (e.g., €200 million or more in daily trading volume, 10 million or more users, etc. In particular, non-euro-based EMTs will be subject to a daily trading limit, which will take into account the impact on euro sovereignty. MiCA creates a single passport for stablecoin issuers in Europe, allowing them to be authorized in one member state and offer services across the EU.

As a result, existing stablecoin players are preparing for the transition to regulatory compliance, and new players are emerging. For example, Circle has been issuing EURC (Euro-linked stablecoins) since 2023 with a temporary regulatory authorization in France, and is in the process of obtaining full authorization in Luxembourg and other countries in anticipation of MiCA. In addition, some countries, such as Germany, are discussing amending their domestic laws to treat stablecoins as e-money separately from MiCA. Overall, the EU's MiCA seeks to promote investor protection and financial stability while providing clear rules to encourage the growth of legitimate stablecoin businesses.

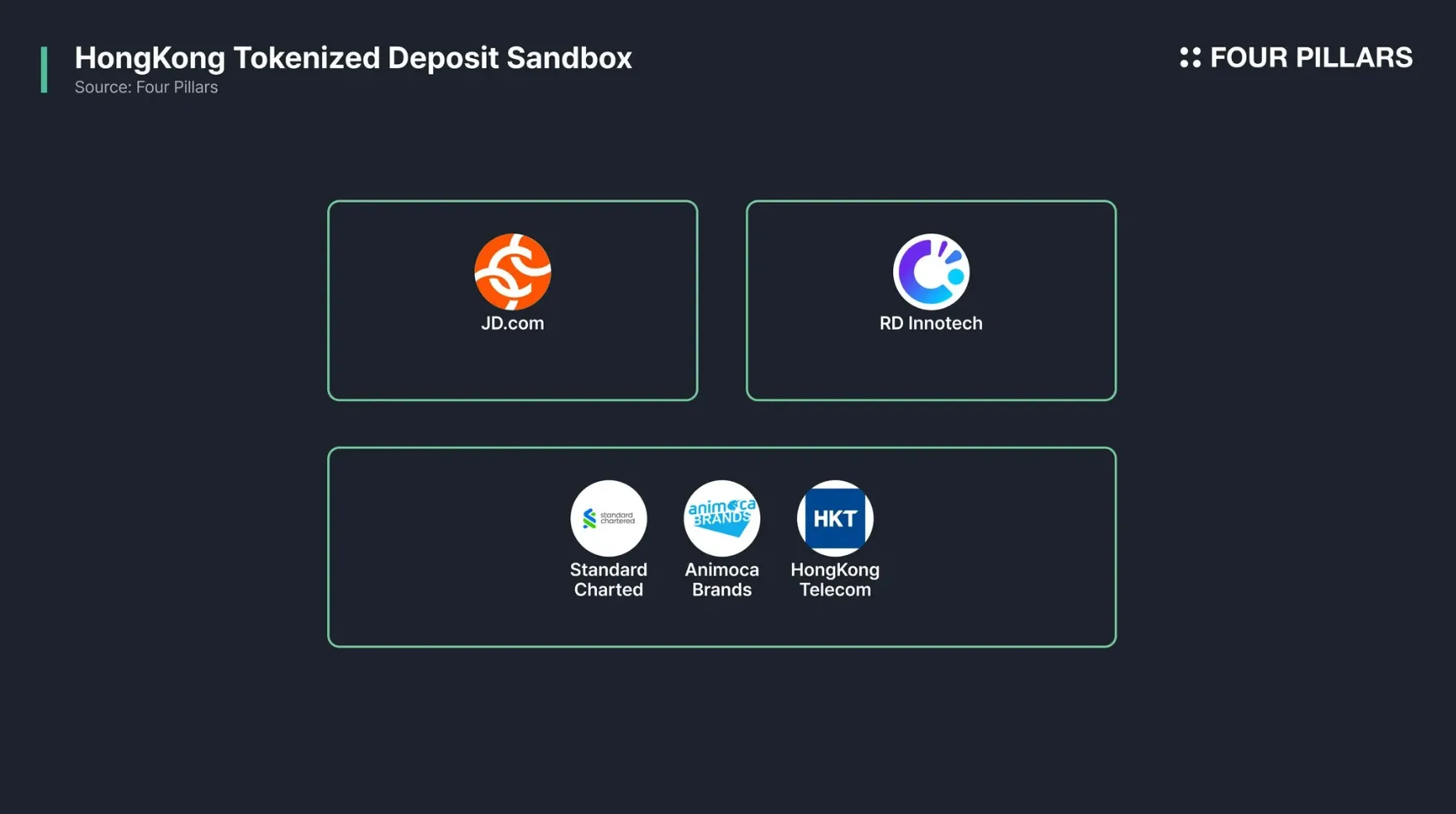

Hong Kong, one of the world's leading financial hubs, is a prime example of a jurisdiction that has moved relatively quickly to regulate stablecoins. In 2022, the Hong Kong Monetary Authority (HKMA) conducted a public consultation on stablecoins and announced its intention to introduce a licensing scheme for issuers. In 2023, the HKMA allowed stablecoin experimentation in a limited environment through a regulatory sandbox program, and in December 2024, it submitted a formal Stablecoin Bill to the Legislative Council.

With the passage of the bill on May 21, non-banking entities, as well as banks, will be able to issue fiat-linked stablecoins with the approval of the HKMA. The main requirements set out in the bill include the aforementioned minimum capitalization of HK$25 million, maintaining reserve assets of 100% of the issuance volume, and prohibiting redemption restrictions. In preparation for this regulatory framework, private preparations are also underway, with Standard Chartered Bank, Hong Kong Telecom (HKT), Animoca Brands, and others forming a joint venture to issue a Hong Kong dollar-based stablecoin in late 2023.

With this combination of sandbox testing and rapid legislation, Hong Kong is aiming to become Asia's stablecoin hub while Singapore falters. The HKMA aims to foster a “healthy and orderly stablecoin market” with the new licensing regime coming into effect as early as 2025.

HongKong Tokenized Deposit Sandbox

Source: Hong Kong Monetary Authority - HKMA announces stablecoin issuer sandbox participants

Currently, there are no cases of domestic institutions directly issuing or utilizing stablecoins in South Korea. There is no clear legal status for stablecoins within the framework of virtual asset regulation, so institutions such as banks and securities are not actively trying. However, considering that major overseas countries are developing related systems and that dollar coins such as Tether are already being utilized in Korea, it is necessary for Korea to take the initiative. The following strategic directions are suggested:

In reality, the safest approach is a bank-led stablecoin based on bank deposits. Currently, MiCA-compliant stablecoins in the European Union, such as Circle's EURC and Societe Generale's EURCV, are bank-backed. However, Circle's USDC and Tether's USDT, which are currently being adopted by the market, are both capital market-oriented stablecoins, with non-bank issuers and collateral consisting of US short-term bonds. In order to operate a sustainable stablecoin, a stablecoin with only cash as collateral is unattractive from an operational perspective and from a user perspective, because the only way to make a profit is to earn interest on the collateral.

Korea currently has no stablecoin legislation at all, and if we only discuss bank-centered stablecoins, it will be difficult to be competitive when they are launched. Korea should either enact capital market-based legislation immediately or allow capital market-oriented stablecoins to be issued in stages.

In Korea, a stablecoin issuance consortium can be formed by combining the credibility of banks, the technology of fintechs, and the digital asset management capabilities of custodians. As in the case of Japan, it is too burdensome for a commercial bank to proceed alone, so it is preferable for multiple banks + fintechs / securities + technology companies to jointly participate. For example, a role-sharing model such as domestic commercial bank A trusting KRW 10 billion in deposits, fintech B operating the blockchain issuance system, and custodian C managing and monitoring smart contract keys can be envisioned.

This allows each participant to play to their strengths, while spreading out the risk more than if each company went it alone. While Korea's banking and electronic finance laws make it difficult for financial firms to handle crypto assets directly, it may be possible to pilot such a model by establishing a special purpose corporation (SPC) within a consortium or utilizing overseas subsidiaries. As domestic crypto custodians are currently accumulating technology and some banks are exchanging information through the Digital Asset Council (DAXA), it is necessary to open a public-private dialogue channel to seek concrete cooperation. More details will be discussed in the following report.

Real-time transparency and monitoring systems are key to securing trust. Korean stablecoin projects should internalize external monitoring and information disclosure from the very beginning. For example, all issuance and redemption transactions and reserve asset details should be disclosed in a real-time dashboard, and smart contract code should be open-sourced and verified by external experts.

It could also allow financial authorities or chartered accounting firms to operate supervisory nodes that can access the nodes in real time to verify balance data. (Similar to the BIS Pyxtrial model, a dedicated dashboard could be provided for supervisors to monitor the liquidity/reserve status of stablecoins). In addition, an anomaly monitoring system should be in place so that the consortium and authorities can trigger response scenarios together in the event of large redemption requests or concentrations at specific addresses.

Safeguards should also be put in place for reserve asset management. In the case of KRW-based stablecoins, cash equal to the issuance amount can be deposited separately with the cooperation of the Bank of Korea, or a 1:1 exchange with CBDCs issued by the Bank of Korea can be considered (to ensure interchangeability with private stablecoins when CBDCs are introduced in the future).

If it is dollar-based, it is possible to acquire U.S. Treasury bonds through overseas branches or foreign branches of domestic banks and issue tokens as collateral. The important thing is to have a combination of legal mechanisms and technical means to ensure that “1 stablecoin = 1 won (or 1 dollar) at all times”.

To this end, Korea can first utilize the regulatory sandbox system to test small-scale pilot stablecoins. For example, as a special case of the financial regulatory sandbox, a certain amount of KRW-linked tokens (e.g., KRW 10 billion) can be issued and used for actual interbank or overseas remittances, and technical and institutional issues can be identified. This will help identify necessary legal amendments (such as amendments to the Electronic Financial Transactions Act) and risk management requirements. It is also possible to simulate stablecoin transactions between banks in a specific closed network environment to assess the impact on the existing payment and settlement network. This step-by-step validation and trust-building will increase stakeholder acceptance when formalization occurs.

As stablecoins are cross-border, it is important to benchmark international examples of advanced infrastructure. For example, the concept of a “supervised open market” could be considered, where multiple private issuers participate but are supervised in real-time by regulators. This would allow authorized foreign private issuers to issue competitively, with the authorities monitoring and intervening to ensure reserve disclosure, liquidity coverage, etc. South Korea could move toward such an open market issuance system to encourage competition and innovation, while allowing the central bank/financial authorities to control systemic risk. In terms of technical standards, it is necessary to ensure interoperability and linkage of multiple chains.

In addition, if Korean stablecoins are privately issued, they should follow internationally standardized token standards (e.g., ERC-20, etc.) and consider utilizing cross-chain protocols (e.g. LayerZero) in order to be linked to blockchains other than Ethereum in the future.

Dive into 'Narratives' that will be important in the next year