On August 13, 2025, Circle unveiled Arc, a purpose-built L1 blockchain for USDC that it has been developing in-house. In the midst of the recent surge of stablecoin networks, Arc’s launch attracted significant attention as Circle joined the trend of releasing its own blockchain.

Arc aims to enable enterprises and institutions to leverage blockchain infrastructure more seamlessly while remaining compliant with regulations by providing 1) USDC as a gas token, 2) high scalability and instant finality through the Malachite consensus algorithm, and 3) optional opt-in privacy features.

Circle’s Arc employs a playbook that is both similar to and different from USDT-focused networks like Stable and Plasma, which are backed by Tether. Arc’s differentiators include 1) integration with Circle’s extensive suite of products, 2) a regulation-friendly approach, and 3) a built-in FX engine.

The emergence of Arc offers significant implications for the industry. This article examines 1) the differing directions of Tether and Circle in the realm of stablecoin networks, 2) whether the competition between Circle and Tether will intensify, 3) the moves of other networks such as Codex and 1Money Network, and 4) whether Arc’s real competitor will be Tempo rather than Stable or Plasma.

Source: Circle

On August 13, 2025, Circle announced Arc, a USDC-focused L1 blockchain it developed in-house, in its Q2 Earnings Report, and soon after released its Litepaper. On the same day, just a few hours earlier, the world’s largest PSP company, Stripe, also unveiled its own L1 blockchain called Tempo, making August 13, 2025, an interesting day when two major fintech giants each launched their own L1 blockchains.

The reason Circle’s launch of Arc drew so much attention is that the stablecoin network sector has recently become one of the hottest topics in the crypto community. Led by Stable and Plasma, USDT-focused networks backed by Tether’s CEO and Bitfinex’s investment, numerous new L1 networks such as Codex and 1Money Network are currently being built to be optimized for stablecoins. In the midst of this, there has been growing anticipation within the crypto community about whether Circle would pursue a related initiative, and now Circle has finally unveiled Arc.

So is Arc, which Circle announced today, simply another USDC-specialized L1 network no different from the recently emerging stablecoin networks, or does it present a differentiated playbook from the others?

Source: Arc

Before exploring how Arc is similar to or different from other stablecoin networks, let’s first take a look at Arc itself.

Arc is a purpose-built, EVM-compatible blockchain specialized for USDC. It aims to enable enterprises and institutions to pay predictable network fees in stablecoins while conducting various financial activities on scalable infrastructure with optional opt-in privacy features. To achieve this, Arc offers the following core features:

USDC as native gas: Allows users to pay low-volatility, predictable fees by using USDC as the default gas token for all transactions.

Deterministic instant finality: Provides highly scalable infrastructure by granting transaction finality in under one second through the Malachite consensus algorithm.

Opt-in Privacy: Integrates privacy-preserving technology to provide optional transparency. This is essential for sensitive transactions and is designed to align with compliance and transaction monitoring requirements for enterprises and regulators.

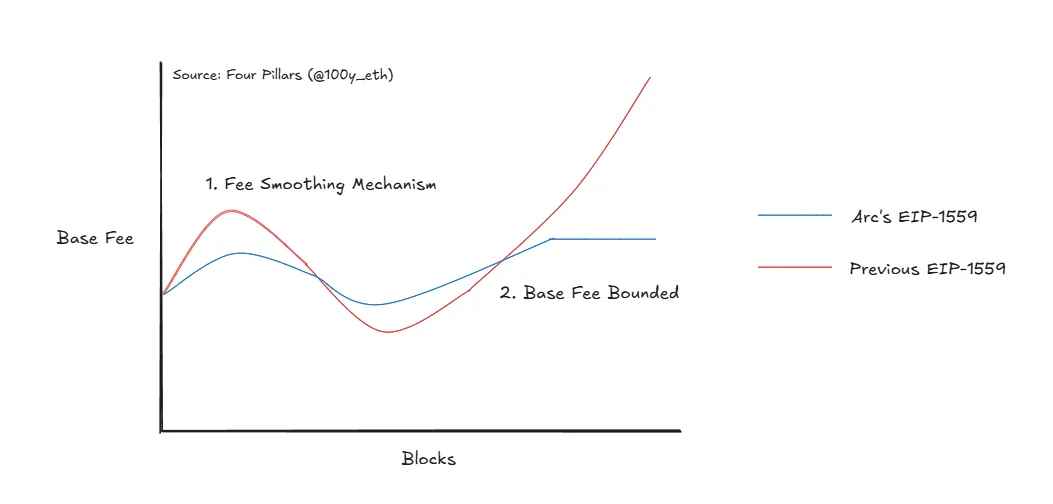

All transaction fees on Arc are set to USDC by default, and it adopts the EIP-1559 fee model.

Arc has made several modifications to the EIP-1559 model. The first is the introduction of a “Fee Smoothing Mechanism,” which uses an Exponentially Weighted Moving Average (EWMA) to determine the next block’s fee by considering fee data from both past and recent blocks (older data receives exponentially decreasing weights while more recent data is weighted more heavily). Whereas traditional EIP-1559 considers only the usage of the previous block when determining the base fee for the next block, Arc’s EIP-1559 smooths base fee volatility by factoring in the usage of multiple past blocks including the previous one. The second modification is the “Base Fee Bounded” feature, which sets a fixed upper limit on the base fee. This prevents fees from increasing without limit even when the Arc network is congested.

Circle Paymaster | Source: Circle

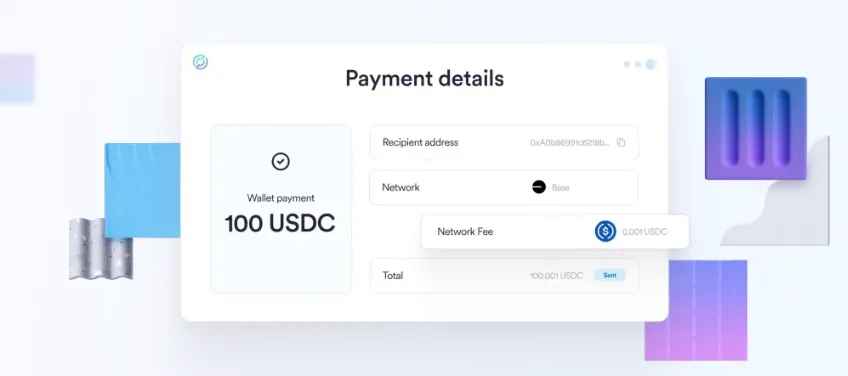

Arc allows not only USDC but also a variety of stable-value tokens such as stablecoins pegged to other national currencies, deposit tokens, and CBDCs to be used as fee tokens. This is related to Circle’s paymaster function.

The Circle Paymaster is originally an ERC-4337-based feature that enables paying transaction fees in USDC instead of the native token on other EVM blockchains. However, since Arc uses USDC as the default fee token, using the paymaster enables transaction fee payments with tokens other than USDC.

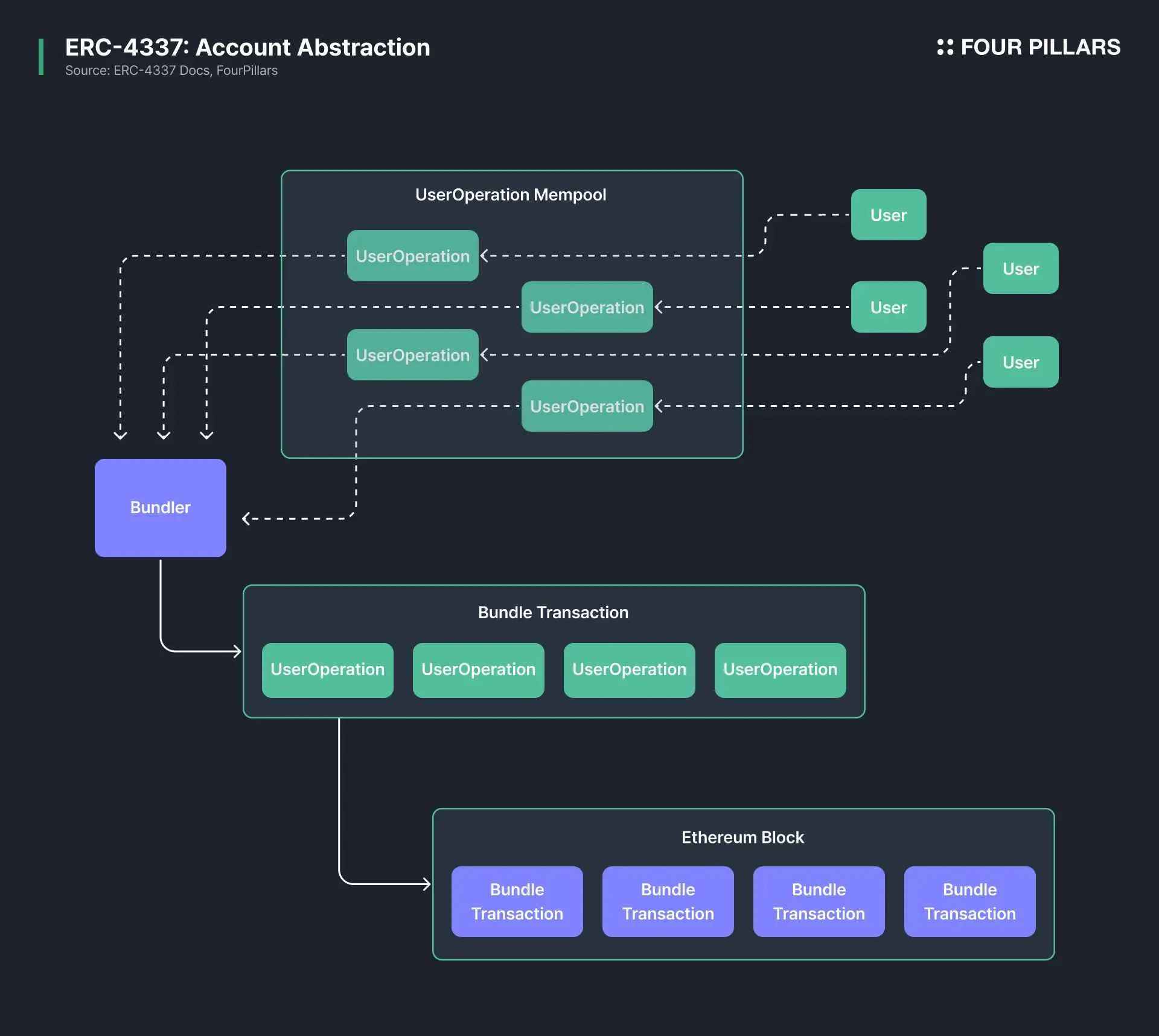

The ERC-4337 standard is the most widely used account abstraction protocol, which adds Entrypoint, Bundler, and Paymaster functions without changing the Ethereum protocol, making account abstraction easier to implement. In ERC-4337, instead of signing transactions, users sign a separate object called a UserOp, which is stored in a separate off-chain mempool (UserOp Mempool) rather than Ethereum’s official mempool. A bundler verifies these UserOps and packages them into a single bundled transaction, which is then sent to a smart contract called the Entrypoint. The Entrypoint verifies and executes the UserOps and performs gas settlement in one go, at which point the Paymaster is used to allow gas fees to be paid in other tokens.

Personal speculation: After Ethereum’s Pectra upgrade, Circle introduced the ability to use the EIP-7702 feature together with the Circle Paymaster function. Based on this, it is expected that Arc will also provide EIP-7702 functionality so that users can fully utilize the Paymaster feature even when using a regular EOA wallet instead of a smart contract wallet.

As we have seen, Arc’s fee model eliminates the need for enterprise and institutional users to hold highly volatile tokens like ETH or SOL to pay transaction fees, while also greatly reducing transaction fee volatility. This increases business predictability and significantly simplifies accounting for enterprises and institutions.

In Arc’s early growth stage, collected fees will go into the Arc on-chain treasury to support the network’s long-term growth.

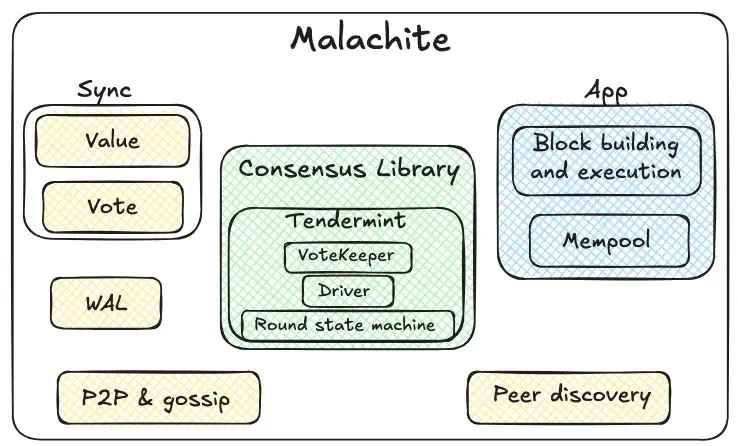

There are two main conditions a blockchain network must meet to become a real-world financial system. The first is high scalability to handle a large number of transactions, and the second is instant transaction finality that does not rely on probability. To achieve this, Arc brought developers from Informal Systems onto its team and adopted the Malachite consensus algorithm.

Informal Systems is a Canada-based infrastructure company that has been deeply involved in the Cosmos ecosystem for a long time, leading protocol design and development. In particular, the company’s co-founders previously worked together at Tendermint and the Interchain Foundation, giving them deep expertise in technologies based on Tendermint BFT. In other words, Informal Systems is the core team that has carried on the technical lineage of Tendermint and is now advancing its successor, CometBFT.

Malachite is a high-performance, Rust-based BFT consensus engine developed by Informal Systems. The Malachite team at Informal Systems has joined Circle to build the consensus algorithm that underpins Arc.

Source: Informal Systems

Compared to the existing CometBFT, Malachite removes unnecessary components and minimizes the core, simplifying modules. As a result, the core library of Malachite is composed of three modules:

Vote Keeper: Collects votes from network participants and tracks quorum

Round State Machine: Implements the internal logic of Tendermint voting rounds

Driver: Operates the state machine over multiple rounds

Because this library makes no assumptions about the execution environment or the type of application it will connect to, it offers the advantage of providing a highly generic consensus API.

Malachite not only provides a simple consensus library but also offers an engine that allows developers to easily build production-grade nodes. It additionally includes features such as:

Sync: Synchronization of block proposal and voting data during the consensus process

WAL: Failure recovery and data integrity assurance

P2P & Gossip: Propagation of blocks, transactions, and vote messages between nodes

Peer Discovery: Finding other nodes in the network

App: Block creation and execution logic, as well as a mempool for transactions

Source: Arc

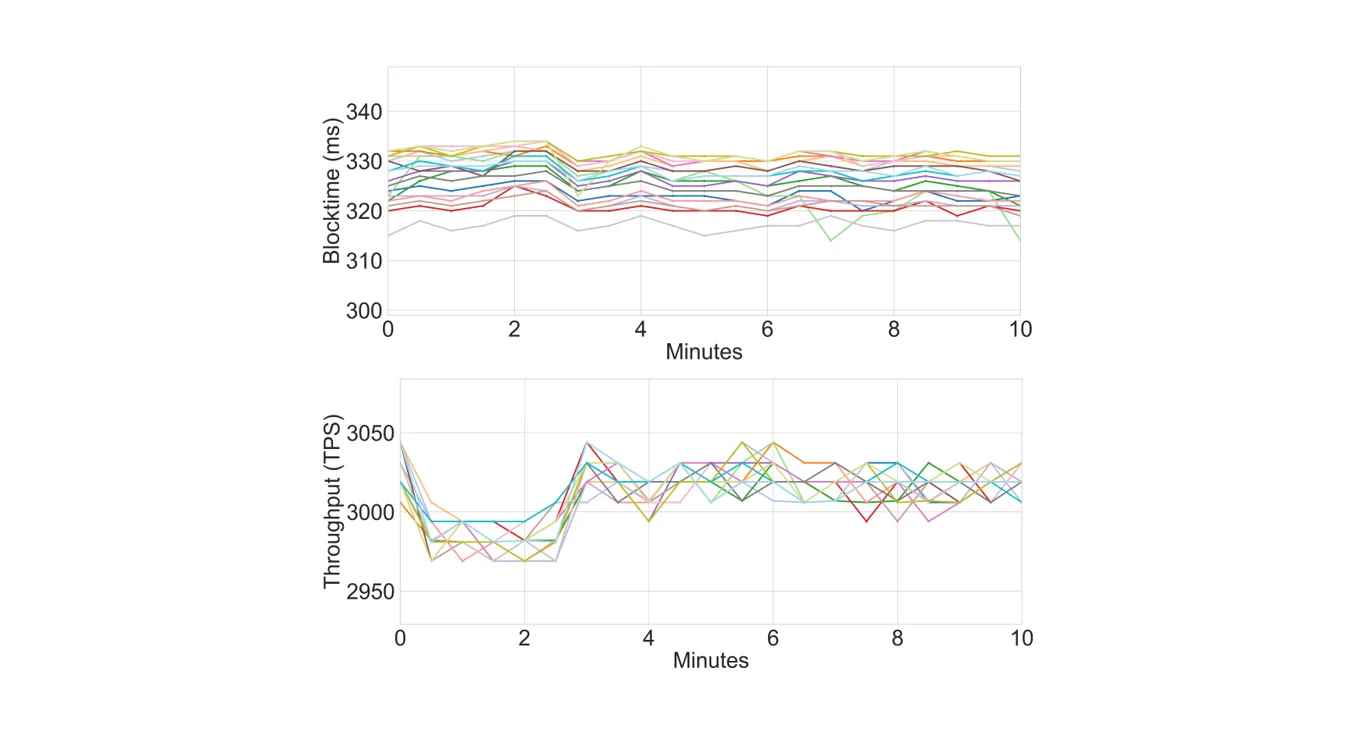

Due to its Rust-based implementation and simplified modular design, Malachite has achieved very high performance in benchmarks, forming the foundation of Arc’s scalability. In a test with 20 geographically distributed validators, Arc achieved 3,000 TPS and finality in under 350 ms. Furthermore, since Malachite is fundamentally based on Tendermint BFT, it can provide instant finality.

A privacy feature that can protect users’ sensitive transaction information while still allowing regulators to view transaction records when necessary is essential for real-world financial infrastructure. To achieve this, Arc plans to add an opt-in privacy feature in an upgrade after its mainnet launch.

In the early privacy roadmap, Arc will introduce a “confidential transfer” function. This will hide transaction amounts but disclose addresses so that regulators and analytics tools can trace them, with the goal of remaining compatible with existing blockchain analysis and monitoring systems. In particular, by introducing View Keys — a mechanism that grants read-only access to specific transaction data to approved third parties such as auditors and regulators — Arc can ensure compliance. For institutions, this allows full visibility into all transactions conducted by their customers, enabling them to meet regulatory requirements such as transaction monitoring and the Travel Rule.

To implement this, Arc will provide an EVM precompile that will allow smart contracts to interact with a cryptographic backend. Initially, this backend will leverage TEE to enable fast and verifiable privacy transactions, unlike many other privacy solutions. In the future, Arc aims to integrate a variety of cryptographic technologies beyond TEE, including ZKP, FHE, and MPC.

In the later privacy roadmap, Arc plans to go beyond simple confidential transfers to support “Private State” and “Confidential Computation,” enabling advanced privacy use cases such as:

Private order book: Maintaining an exchange’s order book state without disclosing it externally

Trade finance agreement: Keeping the contents of trade agreements private

Automated treasury: Keeping corporate treasury management logic hidden from outside parties

The Arc unveiled by Circle this time shows a playbook that is very similar yet different from USDT-focused networks supported by Tether, such as Stable and Plasma.

3.1.1 Stablecoin-focused features

Stable and Plasma are USDT-focused networks that allow USDT to be used as the default gas token, provide high scalability through core optimizations, and plan to offer optional privacy features. In addition, they provide zero transaction fees for simple USDT transfer transactions.

For readers familiar with Stable and Plasma, a quick look at Circle’s Arc might immediately prompt the thought, “Wait, isn’t this just Stable or Plasma but for USDC?” This is because Arc’s main features — 1) USDC as the gas token, 2) optional privacy, and 3) high scalability — are almost identical to the key characteristics offered by Stable and Plasma.

One major difference here is that Circle’s Arc only supports using USDC as the fee token and does not offer a zero-fee option for USDC transfer transactions.

3.1.2 Privacy still takes a back seat

Not only Circle’s Arc, but also Stable and Plasma plan to provide optional privacy features for user data protection and regulatory compliance. However, these are still under active research and will not be supported at the initial mainnet launch. This is because introducing privacy features right away is technically challenging. It remains to be seen which stablecoin network will be the first to implement optional privacy features and, if implemented, what the actual user experience will be like from the perspective of users, businesses, and regulators.

At first glance, Arc may seem like just another stablecoin network for USDC, but it has a playbook that differentiates it from existing stablecoin networks.

3.2.1 Integration with Circle Products

Source: Circle

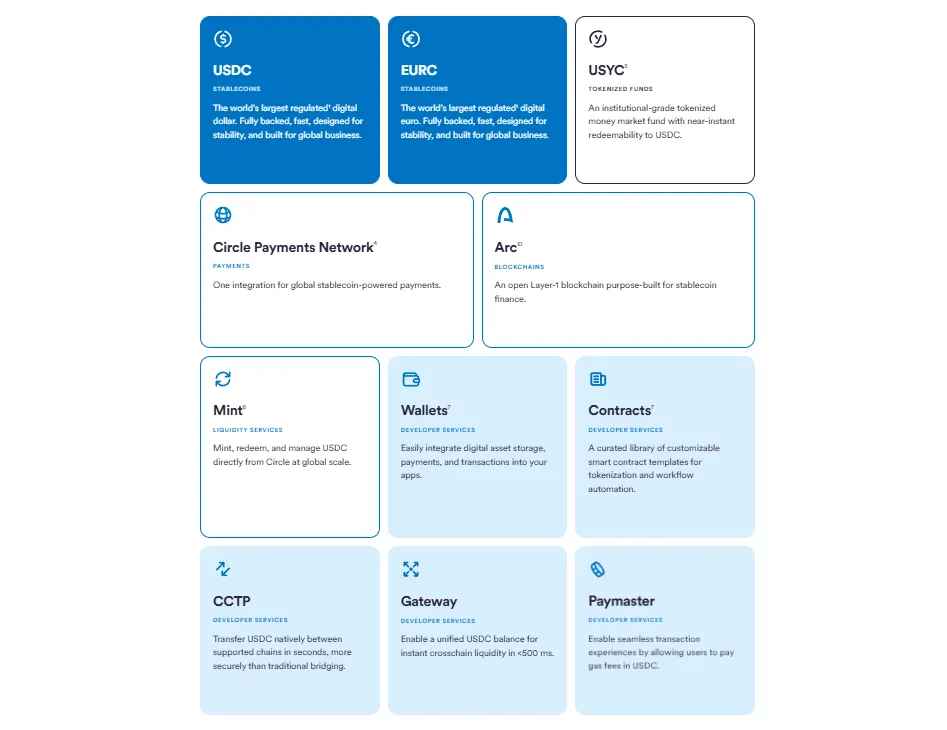

Arc’s biggest strength compared to other stablecoin networks is its flexible integration with other services offered by Circle. Circle is known among stablecoin issuers for vertically integrating a wide range of stablecoin-related services. Arc can integrate with the following features to deliver a highly enhanced user experience for USDC and EURC holders:

USYC: An institutional-grade MMF token backed by U.S. short-term treasuries. USYC will be supported from Arc’s launch day, allowing users to leverage not only USYC but also various types of yield-bearing institutional-grade tokens on Arc.

Circle Payments Network: A global payment system based on stablecoins and blockchain, easily understood as the Web3 version of SWIFT. Once Arc launches, organizations connected to CPN will be able to settle stablecoin transactions on Arc.

Circle Mint: A platform that enables USDC and EURC issuers to easily mint and redeem stablecoins. In the future, users will be able to mint and redeem USDC and EURC directly on Arc via Circle Mint in the fastest and most efficient way.

Circle Wallets: Infrastructure that enables businesses to easily integrate Web3 wallets into their products, with Arc-based assets also set to be integrated.

Circle Contracts: A platform for deploying, managing, and monitoring smart contracts for various services based on stablecoins. Since Arc is an EVM network, it can immediately leverage this functionality.

CCTP: A bridging infrastructure that enables easy cross-chain transfers of USDC and EURC across multiple networks. Arc will also be able to interact with dozens of blockchains and facilitate fund transfers through CCTP. Especially with Arc’s sub-one-second finality, bridging to other networks can be much faster.

Circle Gateway: A service that aggregates USDC balances scattered across different networks into one unified balance and allows instant usage on any chain when needed. This enables users to easily manage balances between Arc and other blockchains.

Circle Paymaster: As discussed earlier, Circle Paymaster enables users to pay fees in tokens other than USDC or use gas sponsorship features on Arc.

3.2.2 Regulatory-friendly approach

Unlike USDT, Circle’s USDC complies with the U.S. GENIUS Act and conducts business targeting the U.S. market. However, this is not just about the obvious facts everyone knows — reading Arc’s litepaper reveals that Circle has paid significant attention to regulatory considerations when building Arc.

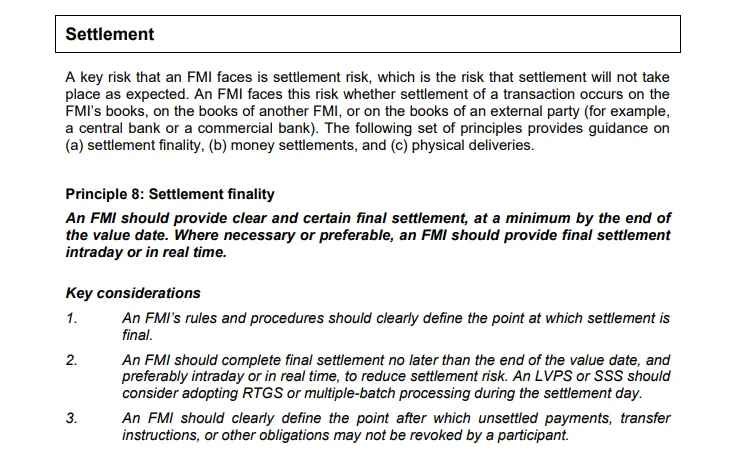

Source: BIS

For example, the Arc litepaper cites BIS reports twice. The first reference emphasizes that Arc transactions are all instantly final, aligning with Principle 8: Settlement finality of the “Principles for financial market infrastructures” published by BIS in 2012. The second points out that Arc’s permissioned validator set could be advantageous under the “Basel Committee on Banking Supervision’s Prudential Treatment of Cryptoasset Exposures” framework published by BIS in 2022.

Thus, it is clear that Arc has been designed not merely as a Web3 network for USDC, but with numerous regulatory elements carefully considered.

3.2.3 Built-in FX engine

Arc’s technical roadmap includes embedding an institutional-grade FX engine directly into the network. This engine will enable secure and efficient foreign exchange settlements between counterparties 24/7.

In addition to smart contract-based transactions, it will incorporate an off-chain RFQ system that allows institutional investors to obtain FX quotes from market makers, compare prices, and execute trades quickly. Such an FX engine will make possible a wide range of FX-related services, including cross-border payments, FX hedging, automated on/off-ramping, and stablecoin futures markets.

Different directions of Tether and Circle in stablecoin networks: Tether has chosen to support external projects like Stable and Plasma in building networks for USDT, while Circle has chosen to build its own network for USDC. Both approaches have clear pros and cons. In Tether’s case, USDT-focused networks can expand their ecosystems quickly without being heavily influenced by Tether’s corporate governance, but they may not be perfectly aligned with Tether’s direction and the ecosystem may become somewhat fragmented. In contrast, Circle’s approach can deliver a more complete user experience through vertically integrated products, but the Arc ecosystem’s growth may be slower due to movements aligned with Circle’s governance and regulatory compliance. Which direction is correct will ultimately be decided by time and the market.

Will competition between Circle and Tether intensify?: Some may view the launch of Circle’s USDC-focused blockchain as a sign that the competition between Circle and Tether will intensify. While this is a reasonable argument, it is somewhat one-dimensional. Arc’s launch is less about entering an entirely new ecosystem and more about more seamlessly connecting and strengthening Circle’s existing products. Competition between Circle and Tether has already been strong, and Arc’s launch is not expected to significantly deepen it. Arc’s real competitor may be closer to Stripe’s Tempo than to Stable or Plasma.

What’s next for Codex and 1Money Network?: Before Circle announced Arc, there was no specific stablecoin network dedicated solely to USDC, which allowed Codex and 1Money Network to attract considerable attention. Both are stablecoin-focused blockchains — Codex has received investment from Circle Ventures and supports native issuance of USDC, while 1Money Network is a Circle Alliance partner and uses the Circle Mint function. However, with Circle’s official entry, these projects will likely be at a disadvantage in terms of mindshare within the crypto community, and it remains to be seen what GTM strategies they will adopt going forward.

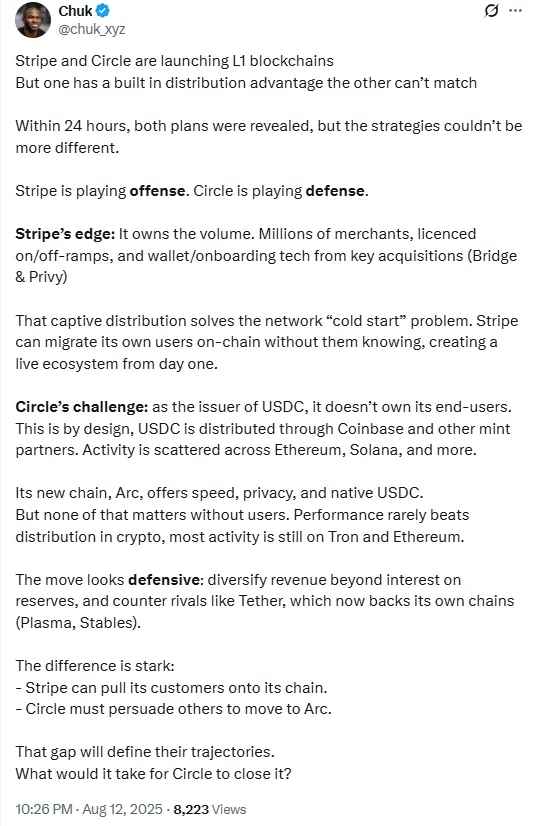

Is Arc’s competitor Tempo?: Chuk from Paxos, offered an interesting insight that I would like to share here. His tweet compared Circle’s Arc to Stripe’s Tempo, highlighting that the two have entirely different approaches and factors that increase their chances of success. Stripe’s strategy is offense — it already has a massive base of users, merchants, and transaction volume, making it possible to seamlessly move its existing network effects on-chain and avoid the cold start problem. In contrast, Circle’s strategy is defense — since Circle does not directly own end users, it must persuade existing users to migrate, starting from a less advantageous position. As I have always emphasized in my previous writings, stablecoins are a game entirely about distribution. The question is whether Arc can successfully build its initial ecosystem and flagship use cases to convince existing USDC holders.

Dive into 'Narratives' that will be important in the next year