$1.4B spent. One flat. Twenty-seven underwater. This isn't cherry-picking — this is the entire dataset. CoinGecko tracked 28 buyback programs in 2025. Combined spend exceeded all prior DeFi buybacks in history. Result: HYPE flat, everyone else down 65-89%.

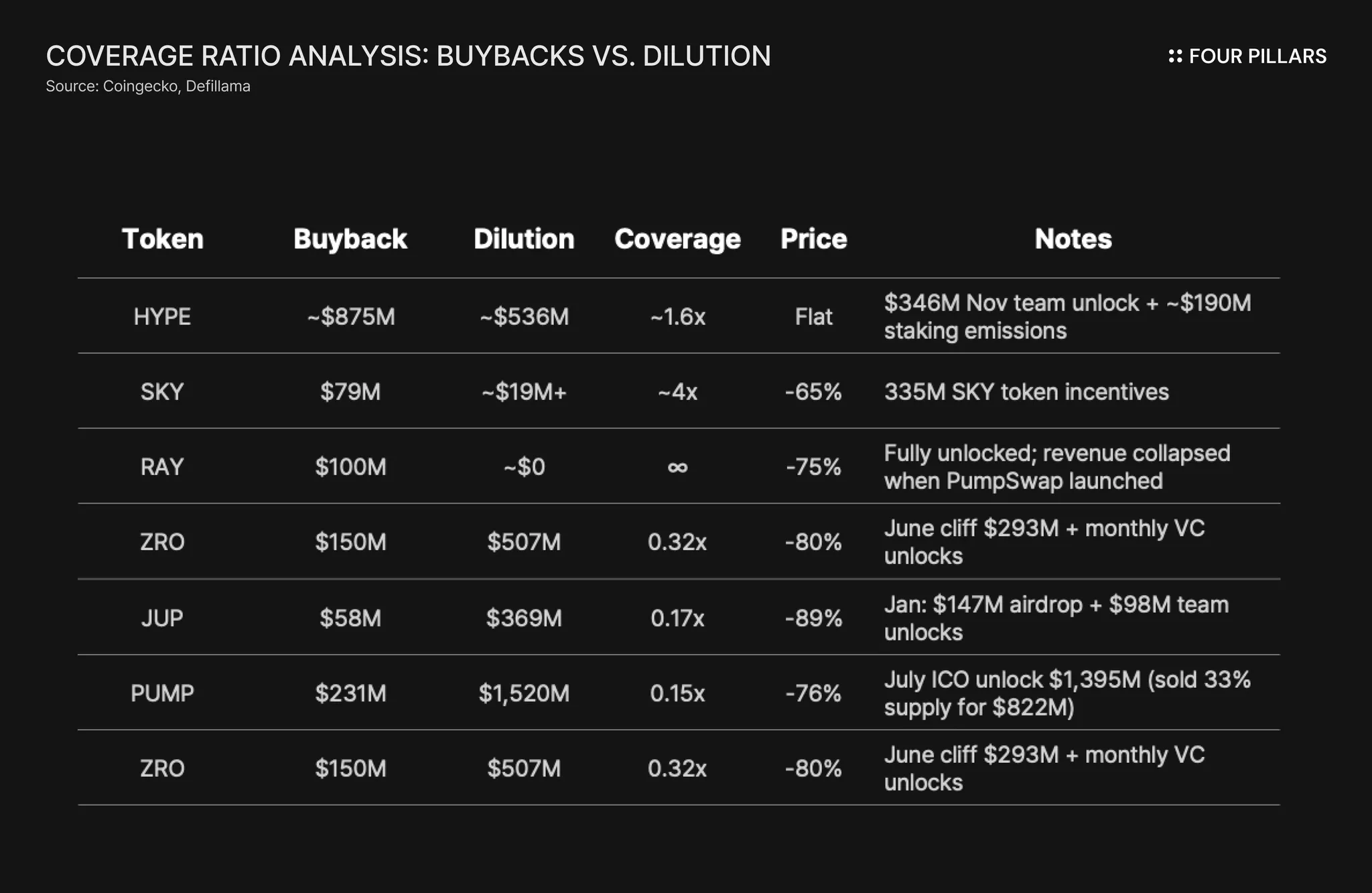

Coverage ratio <1x failure. JUP (0.17x), PUMP (0.15x), and ZRO (0.32x) all dropped 76-89%. PUMP looked like a high-coverage success story until you account for the $1.4B ICO unlock in July.

Coverage ratio >1x is necessary but not sufficient. RAY had infinite coverage (fully unlocked) and dropped 75% when PumpSwap collapsed its revenue. SKY had ~4x coverage and dropped 65% on sector rotation. HYPE had ~1.6x coverage and was flat. High coverage sets a ceiling on outcomes, not a floor.

Buybacks in crypto operate under opposite conditions to TradFi. Traditional buybacks signal undervaluation and return excess cash to shareholders who own future earnings. Crypto buybacks signal desperation — price down 80%, still emitting heavily. Same mechanism, opposite context, divergent results.

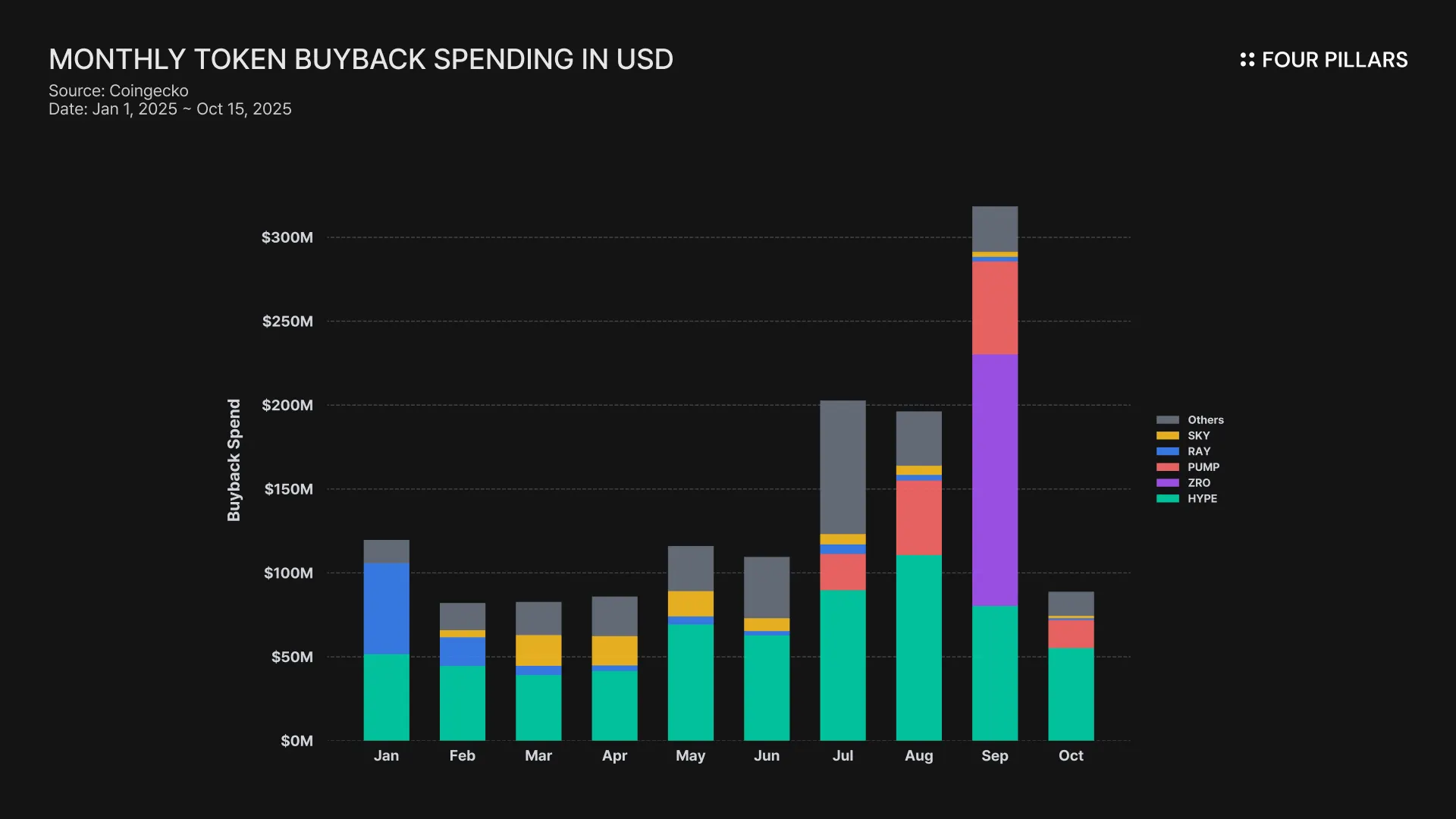

CoinGecko tracked every major buyback program from January 1 through October 15, 2025, and the results are unambiguous.

Twenty-eight protocols. $1.4 billion deployed. One flat. Twenty-seven underwater.

The top 10 programs alone account for 92% of total spend: $1.29 billion combined, representing the largest coordinated attempt at programmatic demand creation in DeFi history. Across different chains, verticals, revenue models, and execution strategies, the exposed returns converged toward the same place: underwater.

Note: Buyback data covers Jan 1 ~ Oct 15, 2025. Price performance extends through Jan 13, 2026. Additional buybacks occurred in the interim — HYPE alone added ~$230M in Q4. If anything, these figures understate total spend relative to outcomes shown.

The distribution of spend reveals concentration risk the market largely ignored. HYPE alone represents 46% of all buyback volume ($644.6M). The next four, ZRO ($150M), PUMP ($138M), RAY ($100M), SKY ($79M), account for another 33%. Below rank 10, programs drop to single-digit millions: GMX at $21M, AERO at $17M, LINK at $10M. The long tail of sub-$10M programs, 18 protocols splitting $72M combined, never had the firepower to matter. They were buying back 0.3-0.5% of supply against unlock schedules that dwarfed their capacity.

The market's verdict came quickly. By the first week of January 2026, two founders publicly called their programs failures:

"We spent more than $70M... the price obviously didn't move much."

- Siong (Jupiter)

"The market doesn't seem to care... we're going to stop wasting our money."

- Haleem (Helium)

They're half right. The market does care, just not about the buyback itself. It cares about what the buyback reveals. A protocol executing buybacks while insiders dump unlocks is providing exit liquidity with institutional legitimacy. The mechanism is working exactly as designed, just not for the people who thought they were the beneficiaries.

The differentiator isn't commitment, execution, or supply retired. The variable that actually matters is how much you buy versus how much you emit.

Coverage Ratio = Buyback $ / (Unlocks $ + Emissions $ + Token Incentives $)

The pattern separates cleanly at the 1x threshold. Below 1x, buyback failure is arithmetic. ZRO spent $150M against $507M in 2025 unlocks (coverage ratio 0.32x). LayerZero has real bridging volume, real revenue, real usage. None of it mattered. The June cliff alone ($293M) exceeded two years of buyback capacity in a single month. You cannot outbuy a denominator three times your size.

PUMP is the most instructive case because it looked like a counterexample. The narrative: 98% revenue commitment, aggressive execution, minimal unlocks until July 2026. The reality is a $1.4B ICO unlock in July 2025 that wasn't in most analyses. They sold 33% of supply during ICO for $822M cash. Those holders have been selling into every buyback since.

JUP had the clearest arithmetic failure. $58M in buybacks against $369M in unlocks (0.17x coverage). January alone dumped $245M onto the market ($147M airdrop + $98M team).

Above 1x, the math is necessary but not sufficient. RAY had infinite coverage (fully unlocked since February 2024, zero scheduled dilution) and still dropped 75%. PumpSwap launched in March 2025 and broke Raydium's pump.fun-derived fee revenue within weeks.

SKY had ~4x coverage and dropped 65%. The most favorable math in the dataset outside HYPE. Governance tokens for mature protocols may simply lack the reflexivity that makes buybacks effective — there's no growth narrative to amplify.

HYPE had ~1.6x coverage and the best structural conditions in crypto. No VC allocation, airdrop recipients with zero cost basis (no "get back to even" selling pressure), 70%+ market share in perp DEXs, and stable fee revenue.

Coverage ratio is predictive, not descriptive. Below 1x, you can calculate failure before the program launches. Above 1x, you need everything else to break right — clean cap table, durable revenue, market leadership, sector tailwinds. Even then, you're playing defense. The best possible outcome could be a floor, not a flywheel.

The mechanism is identical. The conditions are opposite. That's why results diverge.

When Apple or Microsoft announces a buyback, they're communicating a specific signal: management believes shares are undervalued, excess cash has no better reinvestment opportunity, and the business has matured past its high-growth phase. The S&P 500's aggregate buyback spend exceeded $900 billion in 2024 — capital returned to shareholders because these companies have already won their markets. Buybacks reduce share count, mechanically increasing remaining shareholders' claim on future earnings. It's tax-efficient relative to dividends and transmits value directly: company earns $100, you now own a larger percentage of it.

When crypto protocols announce buybacks, they're communicating something else entirely — usually that price is down 80%+ and the team is out of ideas. The protocol is still emitting tokens heavily, often 5-15% annual inflation through staking rewards, liquidity mining, or team vesting. There's no tax advantage. And critically, tokens don't represent ownership of future cash flows. You're not increasing your claim on anything because there's nothing to claim.

Anatoly Yakovenko framed it precisely: "In markets with heavy emissions, short-term buybacks do not reset how sellers price risk." Sellers don't price tokens based on buyback announcements. They price based on their own unlock schedules, their own cost basis, their own liquidity needs. A protocol buying $10M monthly doesn't change the calculus for a VC sitting on $50M in unlocking tokens. It just provides a more liquid exit.

The narrative says: Revenue → buying pressure → reflexive flywheel → price appreciation.

The mechanism actually delivers: Revenue → absorb selling pressure → if everything else goes right, prevent collapse.

TradFi buybacks are a mature-company capital return tool deployed when growth opportunities are exhausted and excess cash has no productive use. Crypto protocols are attempting to use them as growth-stage demand creation while still in land-grab mode, still emitting tokens to attract users, still paying liquidity incentives, still vesting team allocations. They're deploying a tool designed for equilibrium during a phase that demands expansion.

As a result, buybacks become a treadmill. Revenue that could fund growth instead funds absorption of the protocol's own dilution. The token doesn't appreciate because there's no net demand increase — just capital cycling from the protocol's revenue line to its token holders' exit liquidity. The mechanism works exactly as designed. It's just designed for a different context.

This explains why coverage ratio >1x is necessary but not sufficient. Even when buybacks exceed emissions, you're still playing defense, absorbing supply rather than creating demand.

No configuration in the 2025 dataset produced positive returns. The ceiling is flat. The floor is -89%. The key takeaway here is to fade buyback announcements from protocols with coverage ratio <1x. These programs are more exit liquidity infrastructure with institutional PR than value accraual mechanisms. When a protocol announces buybacks while staring down a 5x larger unlock schedule, they're telling you exactly who the beneficiary is. It's not you.

The watch is HYPE through 2026. Coverage ratio inverts from ~1.6x to ~0.29x as team vesting kicks in — $237M monthly unlocks + additional staking emissions against $73M monthly buybacks. If HYPE holds, something beyond the buyback mechanism is carrying it: brand, ecosystem expansion, genuine product-market fit. That would confirm what the data already suggests. Buybacks are defense, not offense. Fundamentals are signal.

Dive into 'Narratives' that will be important in the next year