Polymarket FDV predictions begin converging toward actual values approximately one week before TGE. Analysis of 10 token launches revealed that average prediction error decreased from 128% one month before TGE to 44% one week prior, and further to 21% three days before launch.

Tokenomics announcements have a profound impact on price discovery. Across seven projects with sufficient pre- and post-announcement data, the average error reduction was 113 percentage points.

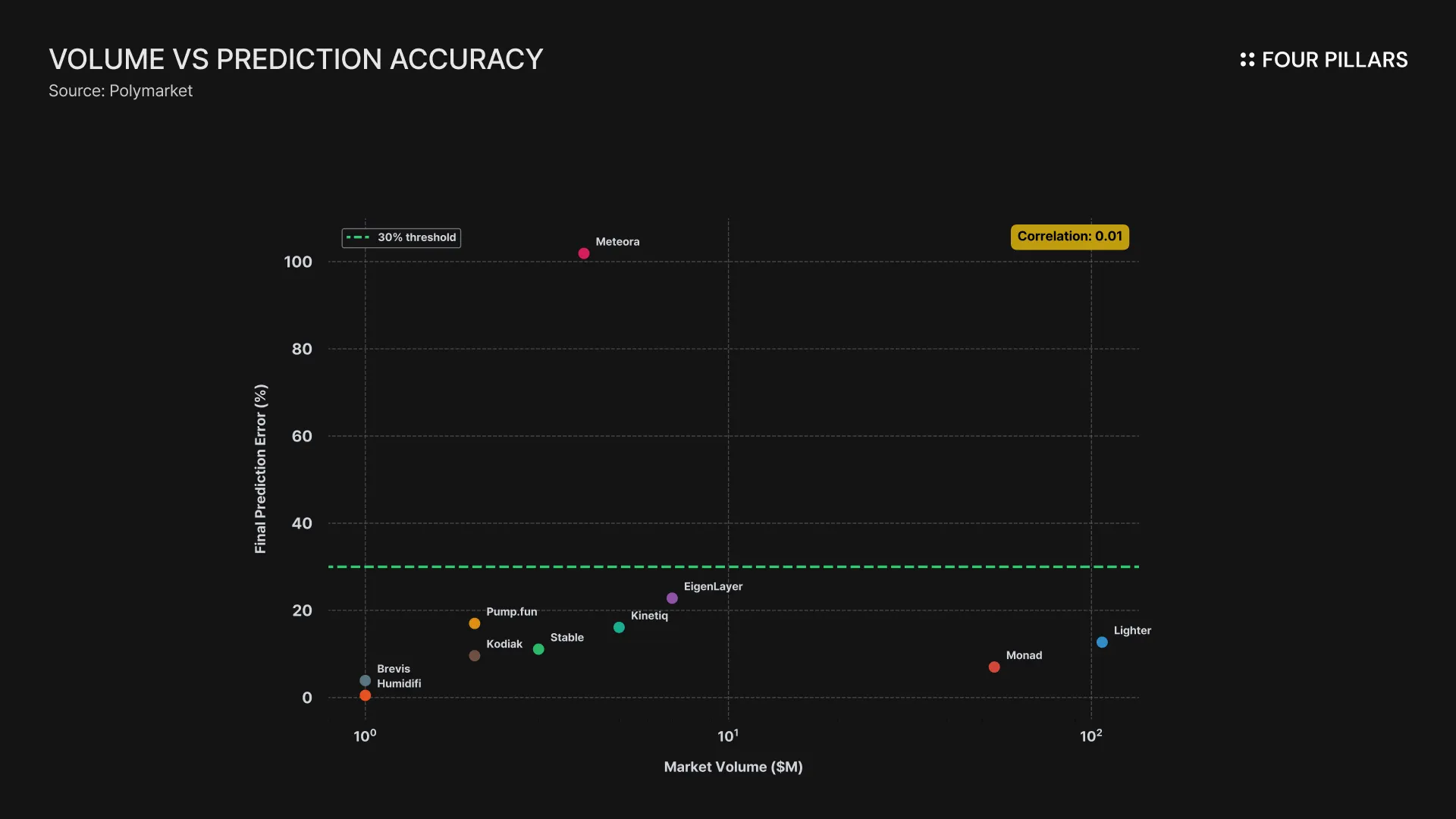

No significant correlation was found between prediction market volume and accuracy. While high-volume markets (≥$50M) showed an average final error of approximately 10% using the median FDV methodology, low-volume markets (<$5M) demonstrated comparable accuracy at around 8% when excluding Meteora as an outlier.

The median FDV methodology provides a reliable single-point estimate. FDV estimates derived through linear interpolation to find the 50% probability threshold across binary options consistently showed high accuracy, with a median final prediction error of just 12%.

When evaluating the valuation of newly launching tokens, market participants increasingly reference both pre-markets and Polymarket in tandem. While pre-markets offer more visible estimates of expected token value, users must bear the risks of wide spreads and liquidation exposure, and these markets tend to predict ultra-short-term prices immediately following TGE. In contrast, Polymarket's FDV markets settle based on the value "24 hours after launch," approximating fair value after initial volatility subsides.

How reliable are these predictions, and when do they become meaningful signals? This question matters to traders positioning for token launches, projects benchmarking market expectations, and anyone interested in the efficiency of crypto prediction markets.

This article analyzes data from 10 projects launched between 2024 and 2025, examining prediction accuracy across different time horizons, the impact of information events such as tokenomics announcements, and the relationship between market volume and prediction quality.

This analysis covers 10 projects that had FDV prediction markets operating on Polymarket prior to TGE. The sample spans a diverse spectrum of market volumes ($1M to $107M), actual FDVs ($37M to $7.85B), and project types (L1s, DEXs, DeFi protocols, and launchpads).

*In case of Lighter, some critical tokenomics-related information, such as initial airdrop portion, was revealed during 12/27 AMA.

Settlement timing varied depending on resolver configurations. Some markets settled exactly 24 hours after TGE, while others settled at 4:00 PM ET on the day following launch. "Actual FDV" refers to the FDV at each market's respective settlement time.

Polymarket's FDV prediction markets consist of binary options in the format "FDV > $XB." To convert probability data across multiple thresholds into a single FDV estimate, we adopted the median methodology. This approach uses linear interpolation to find the point where P(FDV > X) = 50%.

A simple example illustrates this method. Suppose a Polymarket prediction market at a given time shows the following probability distribution for FDV:

$2B: 90%

$3B: 58%

$4B: 31%

$5B: 15%

The median FDV represents the value that the market believes has exactly a 50% probability of being exceeded. Since P(>$3B) = 58% and P(>$4B) = 31%, the 50% threshold lies between $3B and $4B. Applying linear interpolation yields:

Median FDV = $3B + ($4B - $3B) × (58% - 50%) / (58% - 31%) = $3.30B

This methodology was chosen because it is less sensitive to extreme values than simply integrating the probability distribution, offers an intuitive interpretation of "50% probability of exceeding this value," and enables consistent estimation across projects with different threshold configurations.

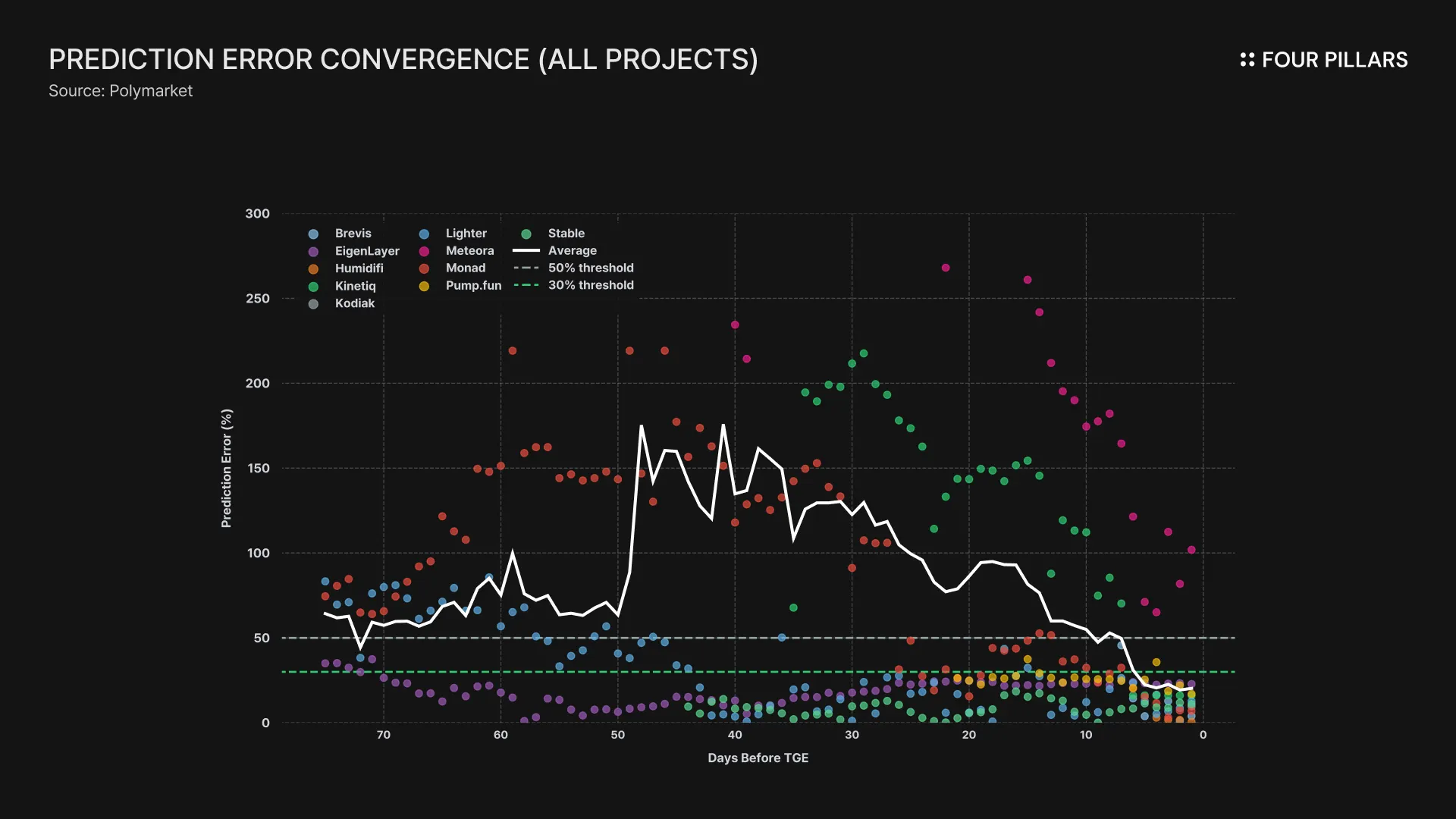

3.1.1 Error Convergence Pattern

A systematic convergence of prediction error as TGE approaches was observed. Starting from one to two months before TGE, a clear trend of improving accuracy over time was evident across all projects.

The average error of 128% one month before TGE indicates that markets were, on average, more than double the actual valuation. This reflects the high uncertainty in early stages when fundamental information about tokenomics, initial circulating supply, and market conditions is absent.

The inflection point appears at the one-week mark, where error tends to drop below 50% for the first time. By three days before TGE, average error decreases to 21%, at which point predictions become practically useful for valuation benchmarking.

3.1.2 Project-Level Variation

While the overall pattern shows clear convergence, some projects exhibited significant deviation from this trajectory.

EigenLayer and Stable stood out as remarkably stable cases. EigenLayer maintained error levels of approximately 17-24% throughout the entire prediction period, likely because tokenomics were announced five months before TGE, giving the market ample time to reach consensus. In Stable's case, despite limited token-related details, the market itself showed minimal volatility from early prices. Interpretations may vary, but we attribute this to the market tracking the FDV of Plasma, a competing project with nearly one-to-one correspondence.

Kinetiq and Meteora represent the opposite extreme. Both projects had prediction errors exceeding 200% one month before TGE, with markets tending to overestimate valuations. Meteora's final error of 102% stands as the only case where predictions remained significantly divorced from reality even immediately before TGE.

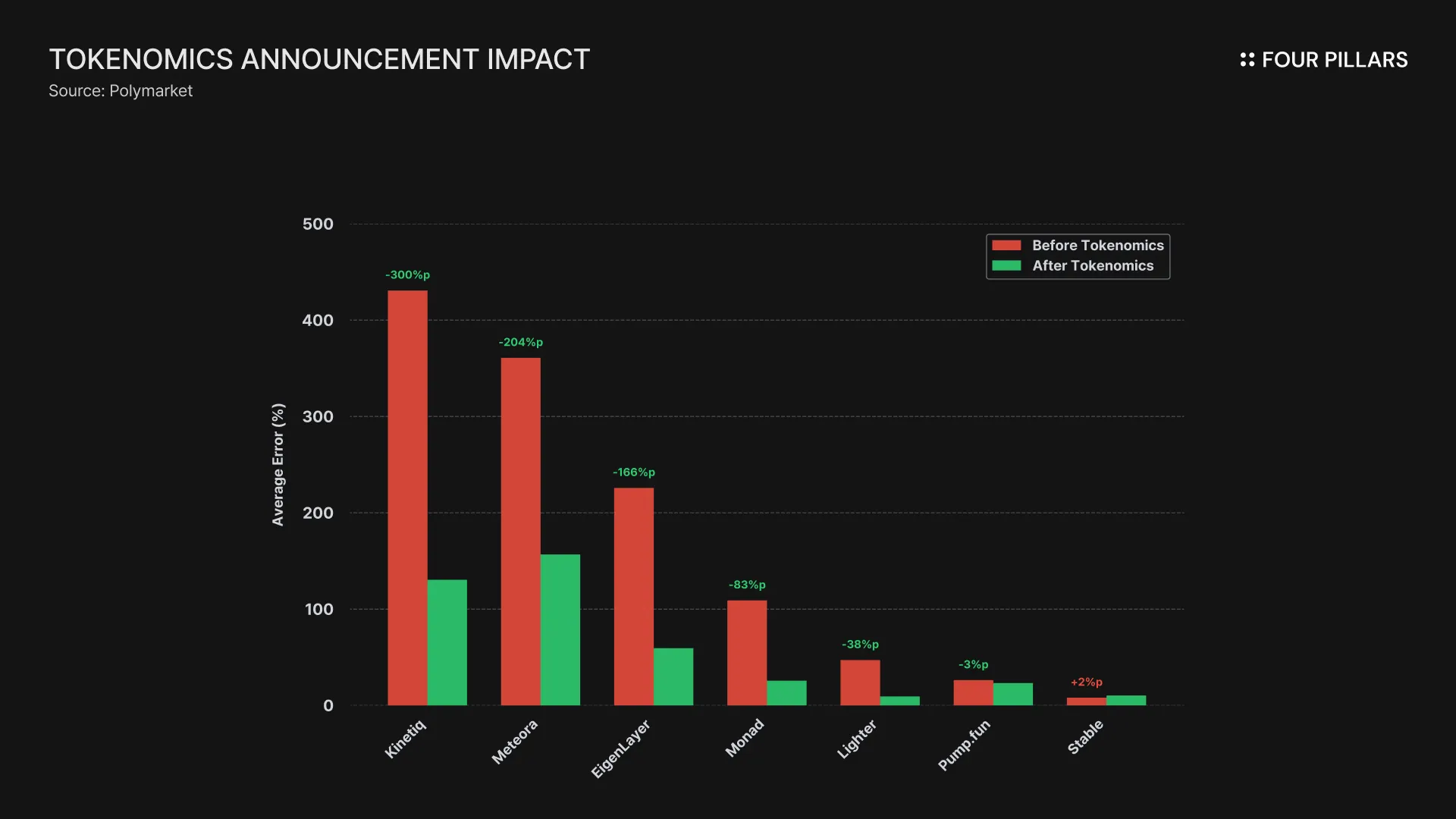

Given that tokenomics announcements can substantially resolve information asymmetry between insiders and retail participants, we hypothesized that such announcements would serve as critical inflection points for prediction accuracy. Comparing average prediction error before and after tokenomics disclosure across seven projects with sufficient data revealed the following changes.

Projects with limited prior information showed particularly large swings. Kinetiq exhibited the largest change (-300%p), implying that the market held high expectations for potential valuation before concrete tokenomics data was released. Meteora (-204%p), EigenLayer (-166%p), and Monad (-83%p) also underwent substantial adjustments to expected FDV following tokenomics disclosure.

Some may question why tokenomics disclosure would affect the total value of tokens, that is, the expected value of the project itself. We agree that project tokenomics do not fundamentally determine value to such a degree. However, it is essential to recognize that Polymarket's FDV prediction markets aim to estimate value "24 hours after TGE," meaning that who receives the initial circulating supply can significantly influence predictions.

In contrast, Pump.fun and Stable showed minimal effect from tokenomics disclosure.

Pump.fun had already operated for a relatively long period (18 months) before token launch, recording over $400M in documented revenue. The market already possessed extensive operational metrics including daily active users, trading volume, and fee revenue to anchor valuation expectations. The tokenomics announcement merely confirmed what could already be inferred from business fundamentals. As mentioned earlier, Stable appears to have reached early consensus due to clearly corresponding peer valuations.

This confirms that for projects with established operational track records or clear institutional backing, the informational value of tokenomics announcements is limited, and the market treats them accordingly.

3.3.1 Analysis by Volume Tier

To examine whether deeper liquidity correlates with better predictions, we analyzed the relationship between each project's prediction market volume and final error. (Final error refers to the difference between median FDV immediately before TGE and actual FDV at settlement.)

Markets with overwhelmingly high trading volume, such as Lighter and Monad, showed average final errors around 10%. Interestingly, excluding Meteora as an outlier, medium and low-volume markets below $10M also demonstrated respectable average final errors around 8%. While it seems self-evident that deeper liquidity attracts more informed participants and generates more efficient price discovery on average, the reality reveals that markets are discovering prices more efficiently than one might expect.

Notably, low-volume markets around $1M, such as Humidifi and Brevis, achieved errors below 5%, contrasting sharply with Meteora despite its roughly four times higher volume.

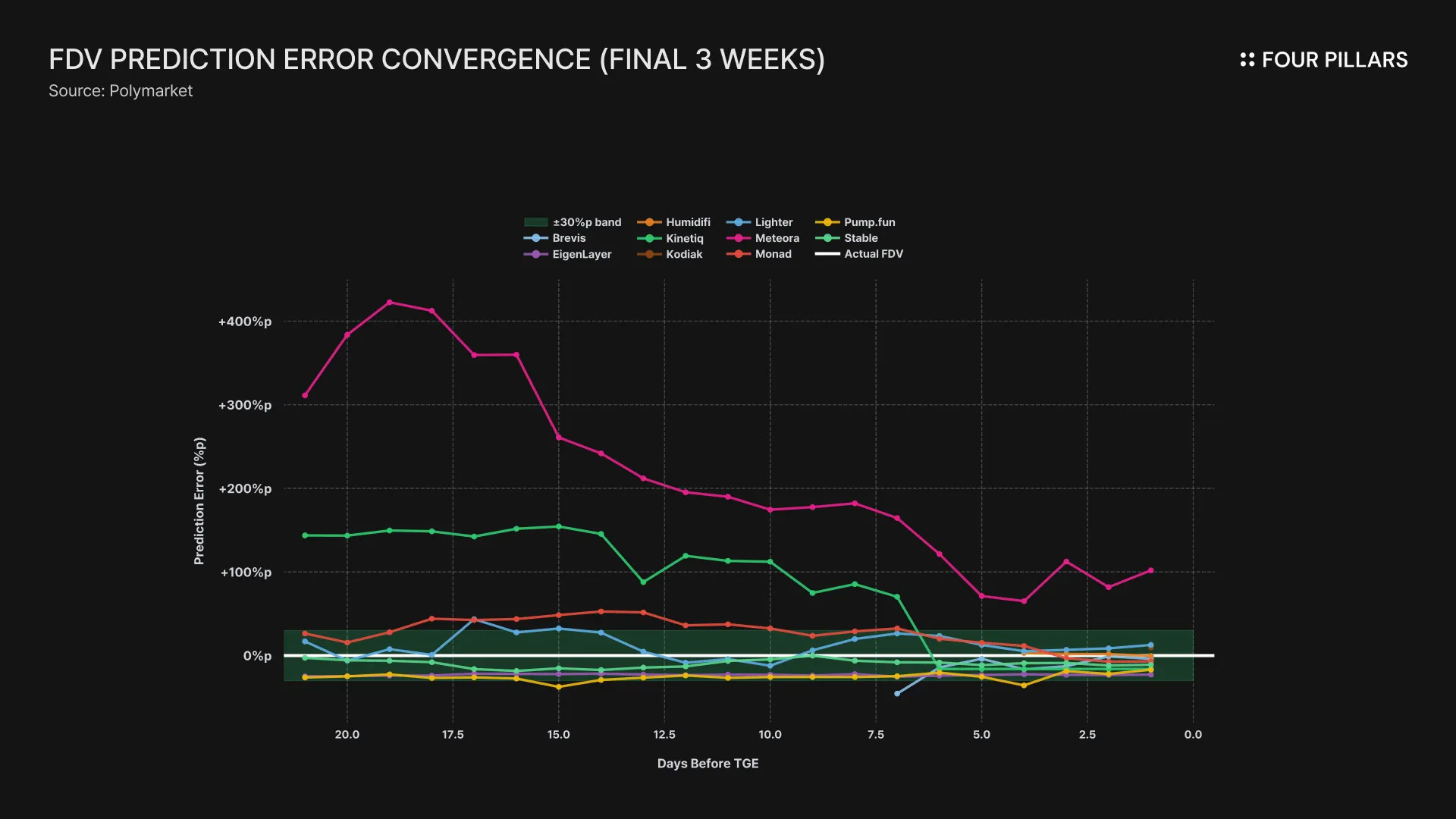

By D-1, most information including tokenomics, team background, and initial circulating supply has already been disclosed. If significant error still occurs, the cause may lie not in lack of information but in "how accurately the market predicted supply-demand dynamics during the 24 hours immediately following TGE."

In Meteora's case, a very high initial circulating supply of 48% was released to the market simultaneously with TGE. Despite knowing this information, the market predicted $1.11B at D-1, but selling pressure from airdrop recipients proved far stronger than anticipated, driving the price down to $550M.

This suggests that the magnitude of post-TGE supply-demand uncertainty may be more closely related to final error. Projects with high initial circulating supply and large airdrop allocations tend to experience greater price volatility in the 24 hours following TGE, which can serve as a primary factor reducing D-1 prediction accuracy.

If prediction markets are efficient, would changes in overall market trends, as represented by Bitcoin, be reflected in individual token FDV predictions?

To investigate this, we compared BTC and FDV changes across 96 weeks for seven projects with sufficient data. Correlation was defined as "FDV prediction rising when BTC rose" or "FDV prediction falling when BTC fell." The results were unexpected: prediction markets moved independently of BTC trends.

Analysis showed that the correlation rate between BTC price and expected FDV was only 43%, with a correlation coefficient of -0.04, indicating virtually no correlation. Furthermore, during 39 weeks when BTC rose, median FDV declined by an average of 6.8%, while during 57 weeks when BTC fell, FDV predictions rose by an average of 2.1%, supporting these findings.

This result can be interpreted in two ways.

First, the information convergence effect may operate more strongly than market trends. Most projects were initially overvalued, and as TGE approached and information became clearer, FDV predictions converged toward actual values. This downward adjustment process proceeded regardless of BTC fluctuations.

Second, prediction market participants may have responded more to project-specific information than to macro factors. Individual events such as tokenomics announcements, airdrop condition disclosures, and competing project developments may have influenced predictions more than BTC price movements.

This analysis identified several clear patterns regarding the reliability of Polymarket FDV prediction markets.

First, prediction error converges systematically. Average error decreased from 128% one month before TGE to 44% one week prior, and 21% three days before. This pattern appeared consistently across projects. This means predictions more than one month before TGE should serve only as directional references for gauging market sentiment, predictions from one to two weeks prior can be used as proxies for fair value, and predictions within one week achieve sufficient reliability for trading decisions.

Second, tokenomics announcements represent the single most important inflection point for prediction accuracy. They produced an average error reduction of 88 percentage points, with particularly dramatic effects for projects lacking prior information. However, the informational value of tokenomics announcements was limited for projects with abundant existing operational metrics or established competing projects.

Third, no significant correlation between market volume and accuracy was confirmed. High-volume markets showed sufficiently low error levels, but this was not substantially different from average errors in low-volume markets. This suggests that predictability of post-TGE supply-demand dynamics, rather than volume itself, is the key variable determining final error. Projects like Meteora with high initial circulating supply and large airdrop allocations may be difficult to predict regardless of volume.

As prediction markets continue to mature, we expect accuracy to improve further through deeper liquidity, more sophisticated participants, and enhanced market design. While only around 10 FDV prediction markets have shown meaningful volume, indicating an early stage, knowing how to interpret this data presents an opportunity, given that 47 FDV prediction markets are currently active on Polymarket.

Dive into 'Narratives' that will be important in the next year