Source: Matteo’s X

Once regarded as part of Mega Mafia, a core group of builders within the MegaETH ecosystem, GTE announced in August last year that it would exit the MegaETH ecosystem, stating that it had “grown enough.”

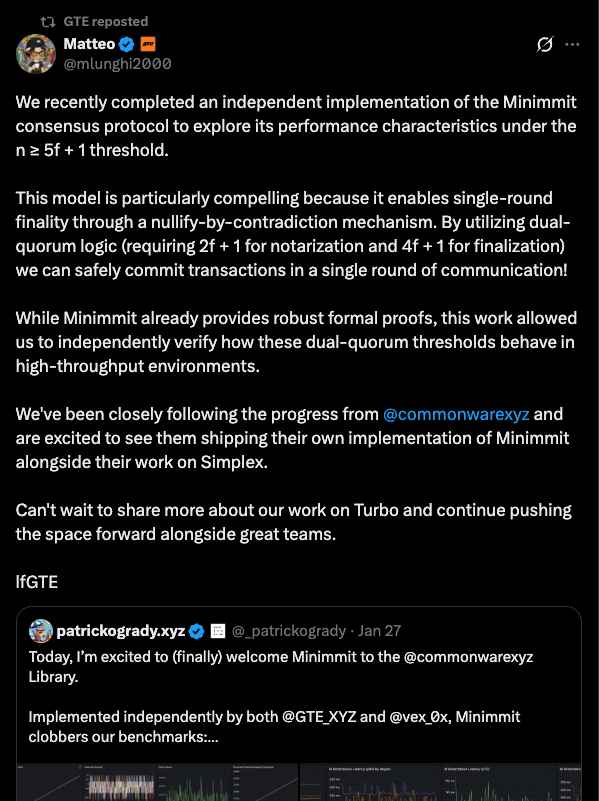

Since then, the market has speculated extensively about GTE’s next direction. Recently, however, GTE unveiled its own independent implementation of Minimmit, the consensus protocol developed by Commonware, making it increasingly clear that the team is not positioning itself within an existing ecosystem, but is instead moving decisively toward building its own Layer 1 blockchain.

What makes this development particularly interesting is that, while GTE is leveraging Commonware’s consensus design, it has not merely forked an existing implementation. Instead, the team independently implemented and validated Minimmit on its own. Moreover, by contributing this implementation directly to the Commonware repository, GTE effectively signaled that its ambitions extend beyond building a single application—such as an exchange—and toward deeper involvement at the infrastructure and protocol layer.

Why, then, is GTE focusing so heavily on Minimmit? The answer is straightforward: the team appears to believe that Minimmit offers meaningful technical advantages over existing blockchain consensus mechanisms.

The most notable feature is its single-round finality. Traditional consensus protocols such as Tendermint or HotStuff typically require at least two to three rounds of voting (i.e., multiple communication rounds) to finalize a transaction. In contrast, Minimmit can finalize transactions in a single round, provided that approximately 80% of the total nodes reach agreement.

At first glance, reducing the number of rounds may raise concerns about weakened safety. Minimmit addresses this trade-off through a dual-quorum design. Under normal network conditions, transactions are finalized in a single round with an 80% quorum. However, when the network becomes unstable or sufficient quorum cannot be reached, Minimmit switches to a Mini-Notarization (M-notarization) mode. In this mode, the chain can continue producing blocks with agreement from only around 40% of nodes, ensuring that progress does not halt entirely.

In other words, assuming honest nodes, a Minimmit-based chain can continue producing blocks even if up to 60% of nodes go offline. Compared to traditional BFT-style consensus systems—which typically require at least 67% (2/3) of nodes to remain online to preserve liveness—Minimmit offers significantly stronger resilience under adverse network conditions.

Tempo, Noble, and now GTE.

As more chains signal their intent to build independently using Commonware, the question of how investors should position themselves remains far from clear.

The core issue lies in the lack of clarity around Commonware’s business model. This situation closely resembles the Cosmos ecosystem, where the proliferation of Cosmos-based chains did not necessarily translate into value accrual for the Cosmos Hub itself. As an open-source protocol, Commonware does not automatically capture economic value when new chains adopt its technology. Even if a chain is built entirely on Commonware, that usage alone does not directly generate revenue for the development entity, Commonware, Inc.(Tempo represents a partial exception, as it has both invested in Commonware and contributed technically, creating a more direct alignment of incentives.)

From an investor’s perspective, this creates structural ambiguity. Even if Commonware succeeds in becoming a next-generation blockchain framework, there are limited and indirect ways to translate that success into a clear investment thesis. For institutional investors who have invested directly in Commonware, Inc., the path from protocol adoption to sustainable revenue and long-term business viability remains uncertain.

That said, the most pragmatic strategy at this stage may simply be to closely monitor the chains being built on top of Commonware. If Commonware does emerge as a foundational layer for next-generation blockchains, then the chains built using it are likely to attract disproportionate attention in their early stages—potentially offering more tangible opportunities for investors than the framework itself.