Aave(@aave) launched the Aave App on November 17, 2025, opening the door to mass adoption. Traditional DeFi platforms have largely been limited to users familiar with on-chain activity, which has reduced accessibility for the general public. To overcome this limitation and reach a broader audience, Aave integrated its high APY on-chain deposit infrastructure into an accessible, app-based platform.

ith this accessibility in place, Aave is now positioned to compete directly with low-risk traditional financial assets such as T-bills, MMFs, and bank deposits.

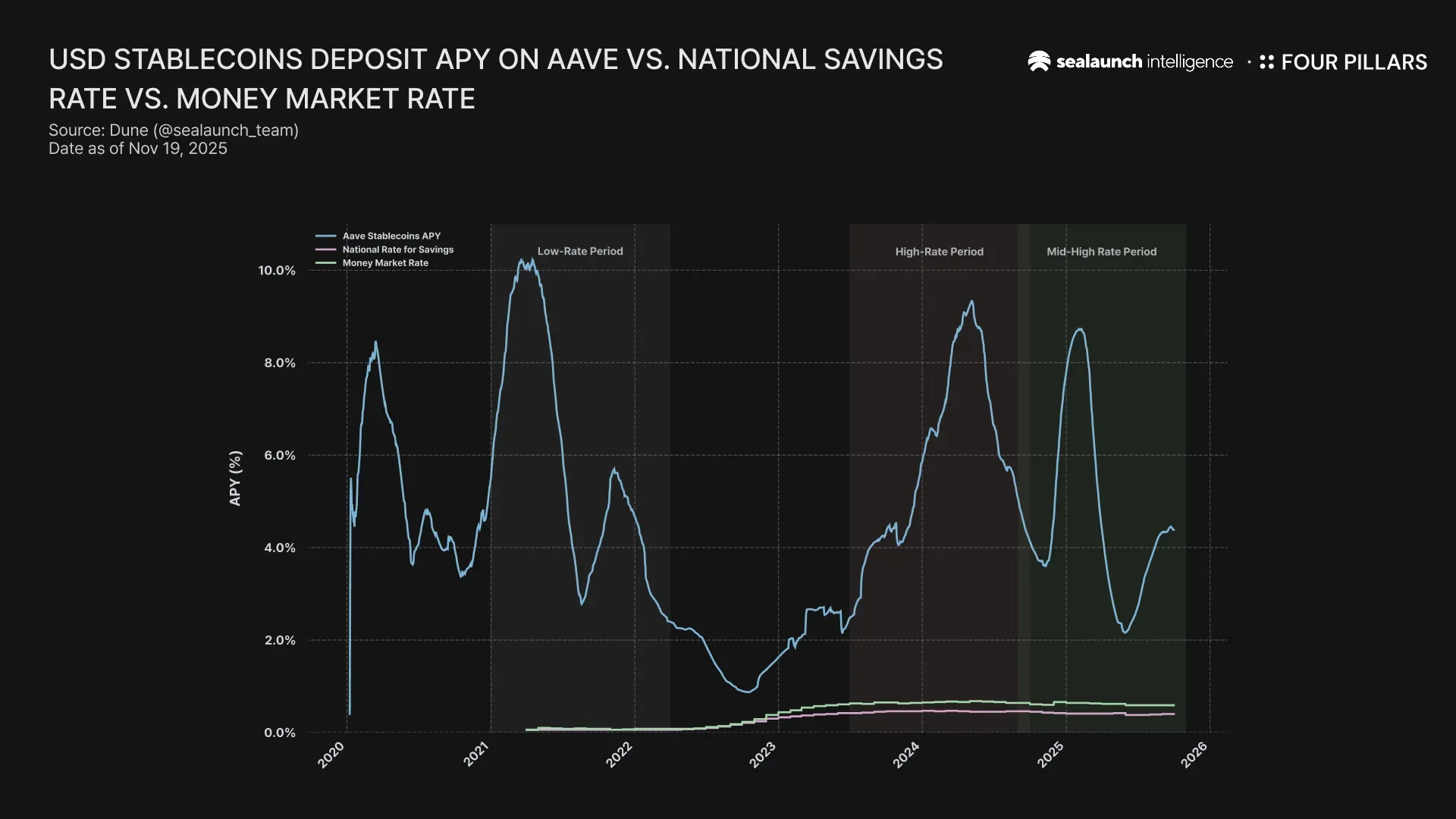

How competitive have Aave’s deposit yields actually been versus those TradFi’s low-risk instruments? We analyzed Aave stablecoin APY and, based on the policy-rate backdrop, divided the data into three regimes, then compared it with short-term T-bills:

Low-rate period (January 2021 to March 2022): the federal funds rate was effectively near zero.

High-rate period (July 2023 to September 2024): the policy rate peaked at 5.25 to 5.50 percent.

Mid-to-high rate period (September 2024 to October 2025): rates began to decline but remained elevated.

Although the on-chain deposit market remains at an early stage, several interesting patterns emerge from the data.

Source : Dune(@sealaunch)

The APY of Aave USD stablecoins consistently exceeded the US National Rate for Savings and the Money-Market Rate across all three interest rate segments. In other words, whether in a low-rate environment where rates were near zero, a high-rate environment where the benchmark rate surpassed 5%, or a transition period of medium-to-high rates in between, Aave has structurally maintained a higher APY compared to the corresponding low-risk products in traditional finance.

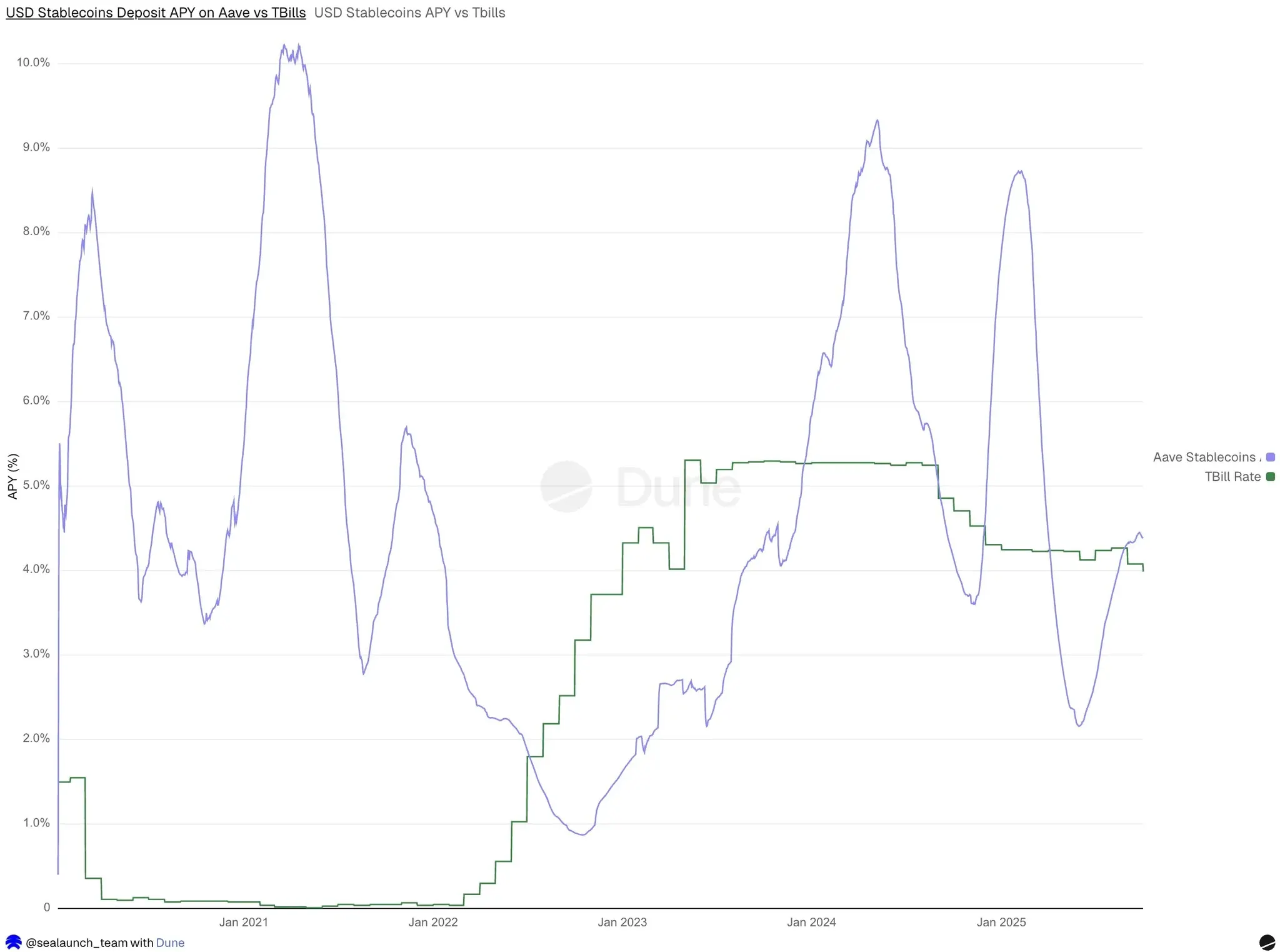

Source : Dune(@sealaunch)

Let's compare Aave to another low-risk traditional finance product: 4-week T-Bills. There have been periods where the 4-week T-Bill Rate did temporarily exceed Aave's APY. However, a closer examination of the data reveals a clear pattern, as follows:

T-bill outperformance is short in duration, infrequent, and limited in spread.

Aave’s outperformance is longer in duration, more frequent, and wider in spread.

Visually, the valleys are shallow and the peaks are high. This asymmetry explains Aave’s advantage in long-run average yields, and it becomes even more important given projections that short-term T-bill yields may enter their lowest range of the past two to three years next year. As rates decline, the perceived value of excess yield at similar risk levels increases.

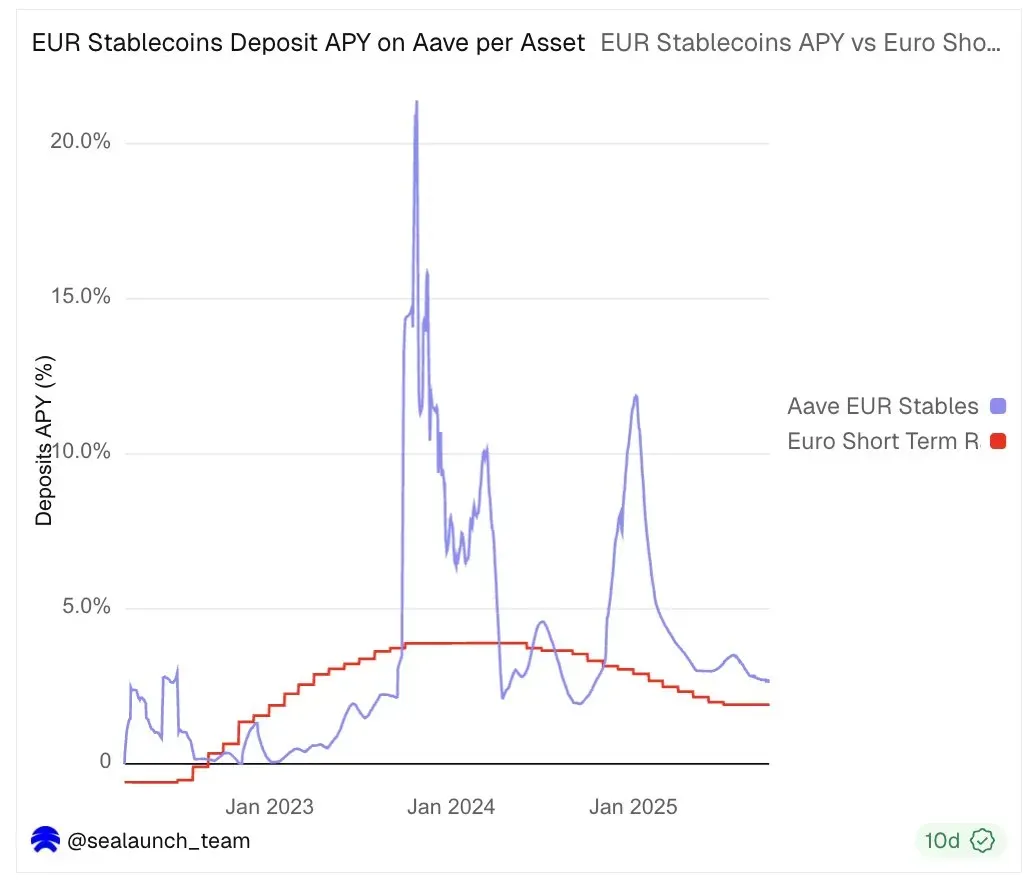

Source : Dune(@sealaunch)

A similar story holds when comparing Aave’s euro stablecoin APY with the Euro Short-Term Rate (ESTR). Although euro stablecoins were added to Aave relatively recently and thus have a shorter data window than USD, Aave’s euro APY has consistently remained about 1 to 2 percentage points above ESTR.

In short, the premium structure observed in USD is replicated in EUR. Even when both the currency and the benchmark change, on-chain deposit rates maintain a consistent premium over traditional low-risk reference rates.

Across different policy regimes, regions, and benchmarks, the pattern is consistent:

Aave has provided structurally higher average APY than short-term T-bill, money-market funds, and bank deposits.

A similar premium pattern appears not only in USD but also in EUR stablecoins.

DeFi is competing by offering higher yields and broader accessibility than traditional low-risk products. As rates move into a downward cycle, more capital seeking even slightly better deposit returns is likely to flow on-chain. Whether protocols like Aave can become the new default choice for depositors is a test that is only just beginning.