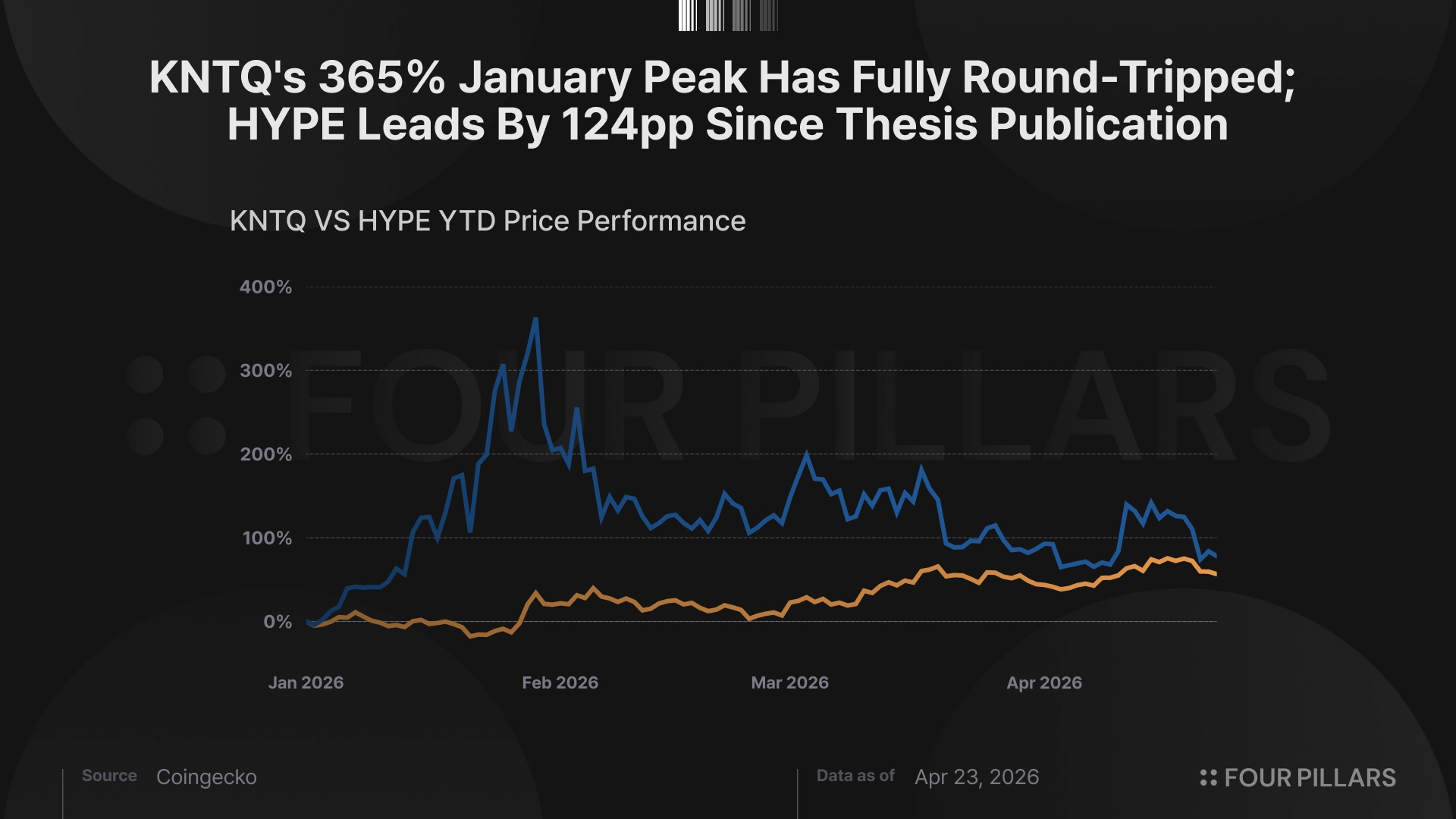

LST dominance validated (77% to 81.2% share, KIP-1/KIP-2 shipped), but the leveraged beta thesis hasn’t played out. KNTQ underperformed HYPE by 124 percentage points from thesis date, and the FDV ratio widened from 142x to 367x.

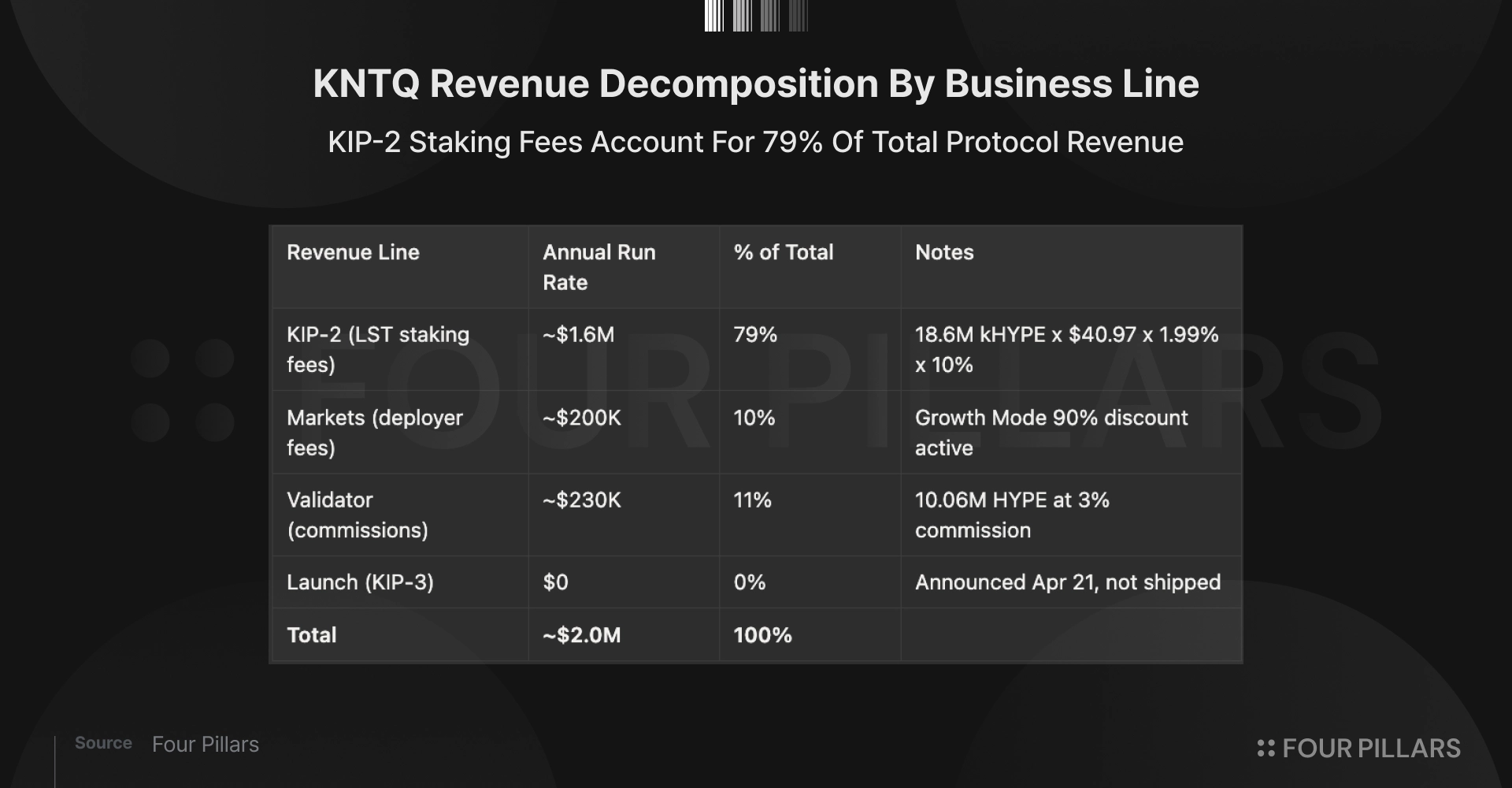

Revenue run rate (~$2.0M/yr) tracks the original “Current” scenario, not the base case. Staking revenue held close to projections. Markets is the entire gap, and that gap is a USDH adoption timeline question.

54x on $2.0M isn't paying for an LST at 4.3% penetration. It's paying for the infrastructure position underneath HIP-3 and HIP-4. LST dominance (81%) is the moat. Markets and KIP-3 (Launch) adoption is the ceiling.

Scenarios span $30-40M (bear) to $600M-1.5B (bull). Same infrastructure thesis, wider surface area with HIP-4 on testnet. Three months is too early to grade infrastructure, but November 2026's vesting cliff sets the deadline.

KNTQ trades at roughly $0.11 at time of writing. Three months ago (Jan 22) I published my KNTQ thesis paper “KNTQ Thesis: 17x, Heavily Coded.” The piece argued that KNTQ was 142x smaller than HYPE with operating leverage that amplified every dollar of HYPE appreciation, that equity perps were coming through HIP-3, and that Kinetiq was building the infrastructure to capture them.

Since January 22, HYPE is up 88%. KNTQ is down 36%. That’s a 124 percentage point spread, and the FDV ratio widened from 142x to 367x. KNTQ did run to $0.302 within a week of the thesis, before giving back the entire move and then bottoming at $0.0886 on April 8.

If you bought KNTQ on thesis date instead of HYPE and held to today, you underperformed by every measure. I don’t want to bury that number in caveats or explain it away with macro or timing. The market had the same macro thesis available in both tokens and it chose HYPE decisively.

The infrastructure KNTQ sits on is healthy and growing. Hyperliquid’s 30-day revenue was $41.3M with $889.6M all-time, the Assistance Fund grew from 39.28M to 43.48M HYPE over the period, and market share against Bybit sits at 41.81%. The AF also holds 516.10K KNTQ worth $54,368, small but the protocol itself owns the token. Whatever went wrong with KNTQ didn’t go wrong because Hyperliquid stumbled.

The infrastructure half of the thesis (LST dominance, product shipping, Hyperliquid ecosystem growth) validated. The leverage half (KNTQ outperforms HYPE, HIP-3 captures equity perps through Markets, ) hasn’t yet. The rest of this piece walks through each line item.

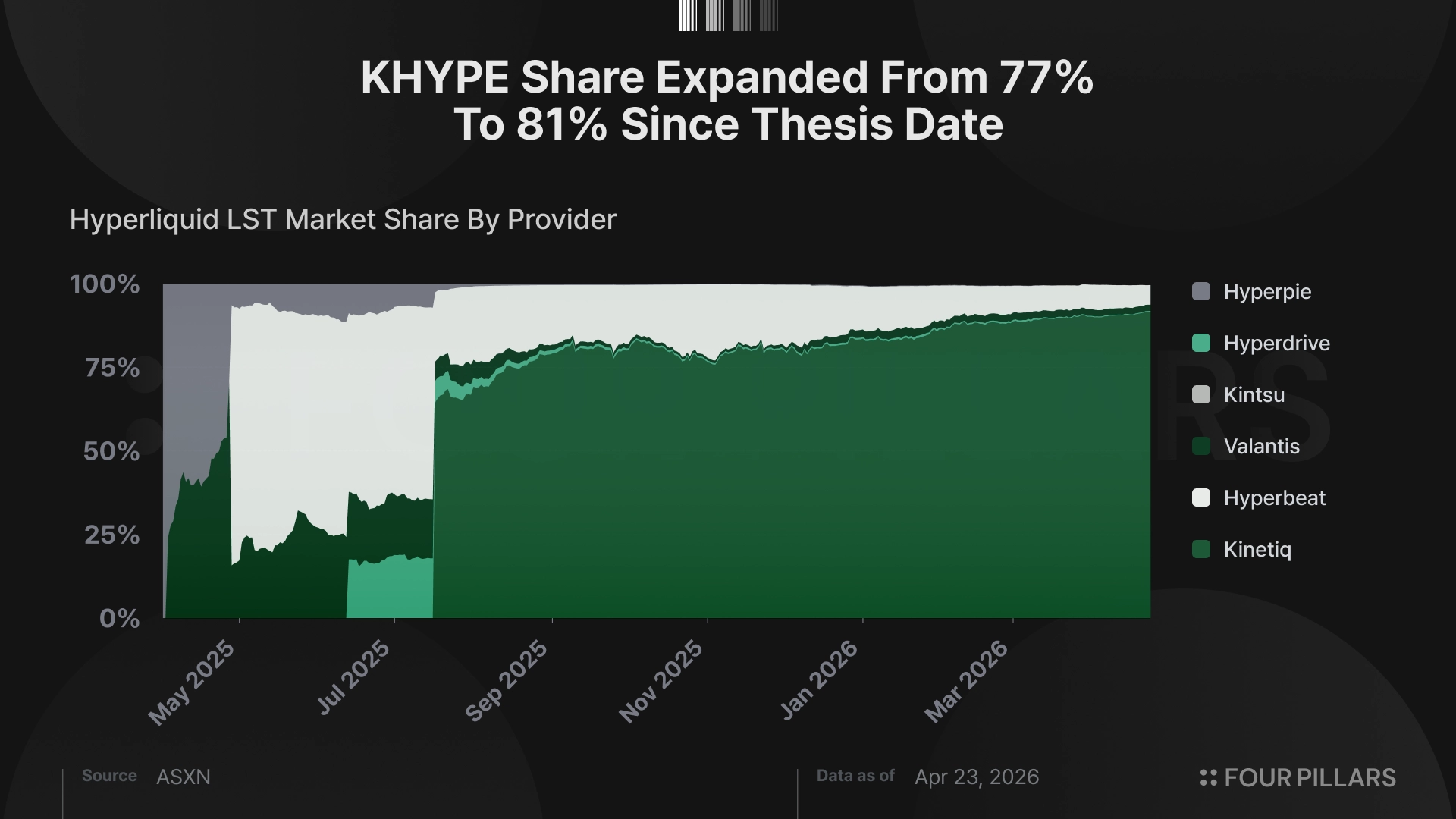

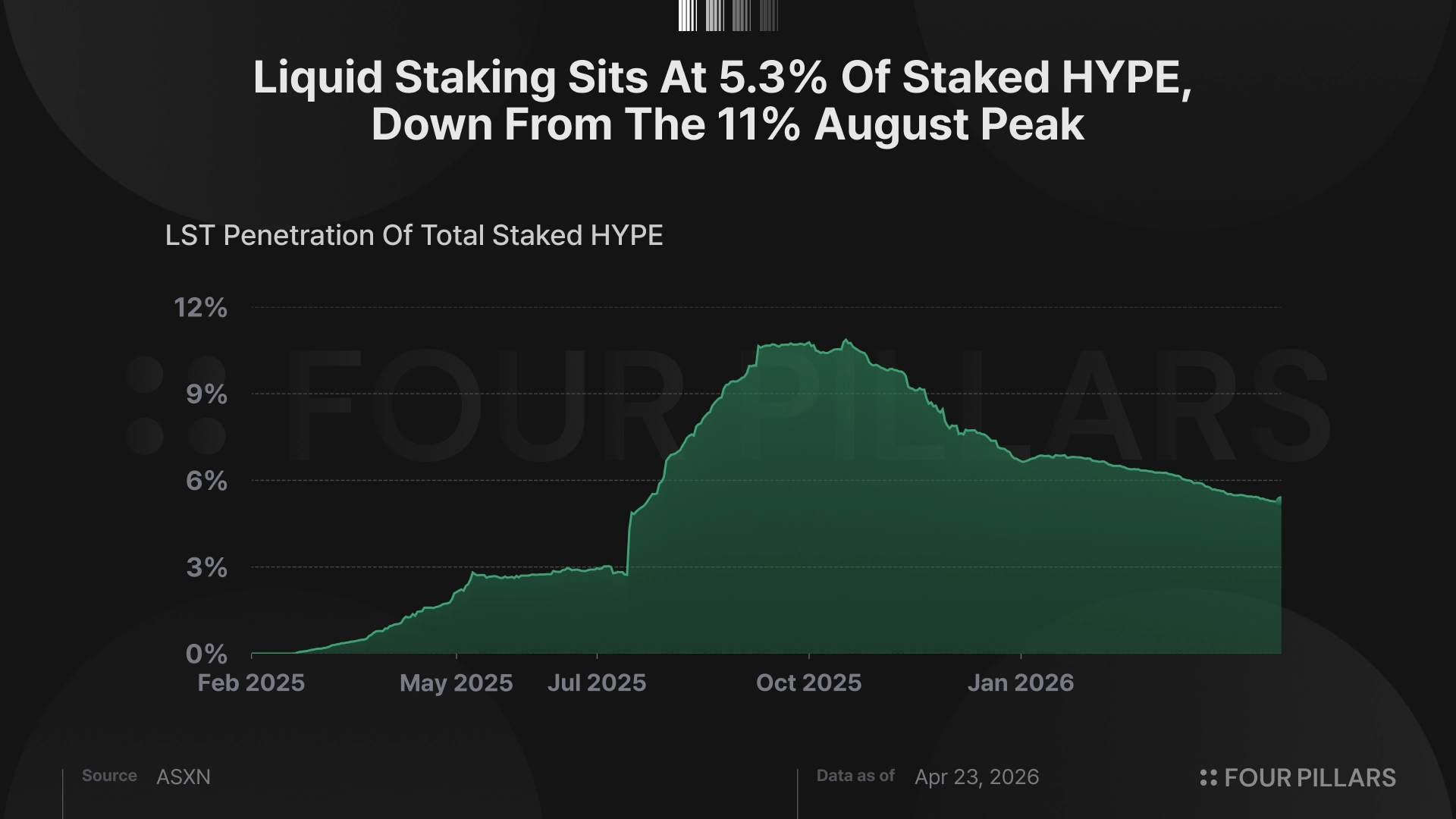

Kinetiq’s liquid staking dominance is the part of the thesis that worked. kHYPE holds 81.2% of the $1.05B LST market on Hyperliquid, up from 77% at thesis time, gaining 4.2 percentage points while already dominant. TVL sits at $843M, down from a $2.65B peak in early October 2025, but that drawdown tracked HYPE’s price, not organic outflows. The $2.65B peak coincided with HYPE around $49, the trough hit $548M in late January when HYPE bottomed near $21, and the recovery to $843M at HYPE $40.80 follows the same price-driven pattern.

kHYPE has 18.6M tokens outstanding at a $40.97 price, 28,000 holders, ~1.99% APY, and an exchange rate of 1 HYPE = 0.984 kHYPE as of April 22. The product works. KIP-1 shipped (sKNTQ staking with revenue distribution is live) and KIP-2 shipped (kHYPE v2 with validator selection and a 10% staking fee, immediately generating the protocol’s primary revenue line).

But 18.6M kHYPE out of 434.5M total staked HYPE is 4.3%. Kinetiq dominates liquid staking. Liquid staking is 5.3% of native staking. The “dominant monopolist” framing from my original thesis overstated the market captured and understated the market remaining.

KIP-2 revenue runs at roughly $1.6M per year: 18.6M kHYPE times $40.97 times 1.99% APY times the 10% fee. It scales linearly with three variables (kHYPE supply, HYPE price, and staking APY) and all three can move. At HYPE $60 with kHYPE at 10% of staked HYPE, that same formula produces ~$5.4M per year.

The composability moat is building in ways that should make a penetration bet more comfortable. Kinetiq runs vkHYPE (Kinetiq Earn) at $49.82M TVL with a 20% performance fee, powered by Veda across Hyperlend, Project X, Felix, and Pendle. kmHYPE sits at $32.04M TVL with an 888,888 supply cap and USDH collateral priced by Kaiko oracles. Across the broader DeFi ecosystem, kHYPE has 12 integrations spanning DEXes (Curve, Project X, Hyperswap, Hybra, Ramses, Ultrasolid), yield protocols (Pendle, Harmonix), and lending (Felix, HypurrFi, Hyperlend, Sentiment). Each integration raises switching costs.

KIP-2’s validator selection is working too. kHYPE delegates across 9+ validators, with HyperStake at 5.3M, Kinetiq x Hyperion at 4.26M, and Nansen, infinitefield, Bitwise, Imperator, USDT0, ASXN, and HypurrCorea each around 689K, at 2~5% commission. Not a single-validator risk concentration.

On Solana, Jito flipped Marinade from roughly 60% share to dominance in about four months, but Marinade had minimal DeFi integrations when the flip happened. Kinetiq is building the composability moat, which should make displacement harder if a competitor emerges. Whether liquid staking penetrates total staking on Hyperliquid the way it did on Ethereum isn’t obvious. Ethereum DeFi needed stETH for capital efficiency across Aave, Maker, and Curve at scale, and Hyperliquid’s DeFi ecosystem is younger. The “DeFi needs kHYPE” moment hasn’t arrived yet. That’s an open question.

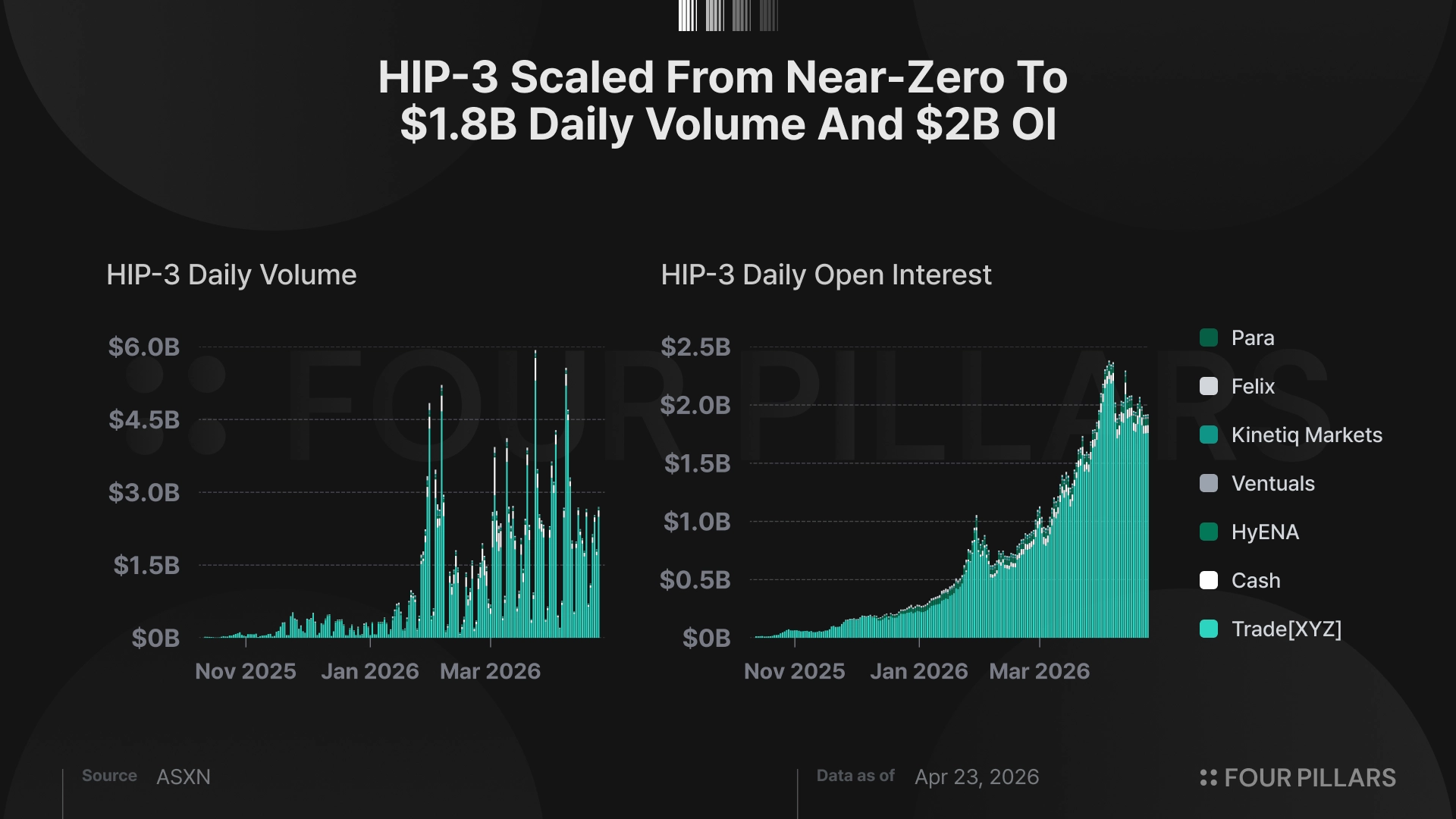

HIP-3 as a category validated massively. At thesis date it was processing $226B in cumulative volume with $512M in open interest. Today it runs $1.78B in daily volume, $1.97B in OI, 8 DEXes, 164 assets. As a share of total Hyperliquid perps it grew from roughly 15% to a Q1 average of 21.5%, hitting 33.6% by March and representing 28.7% of OI. The category bet was right.

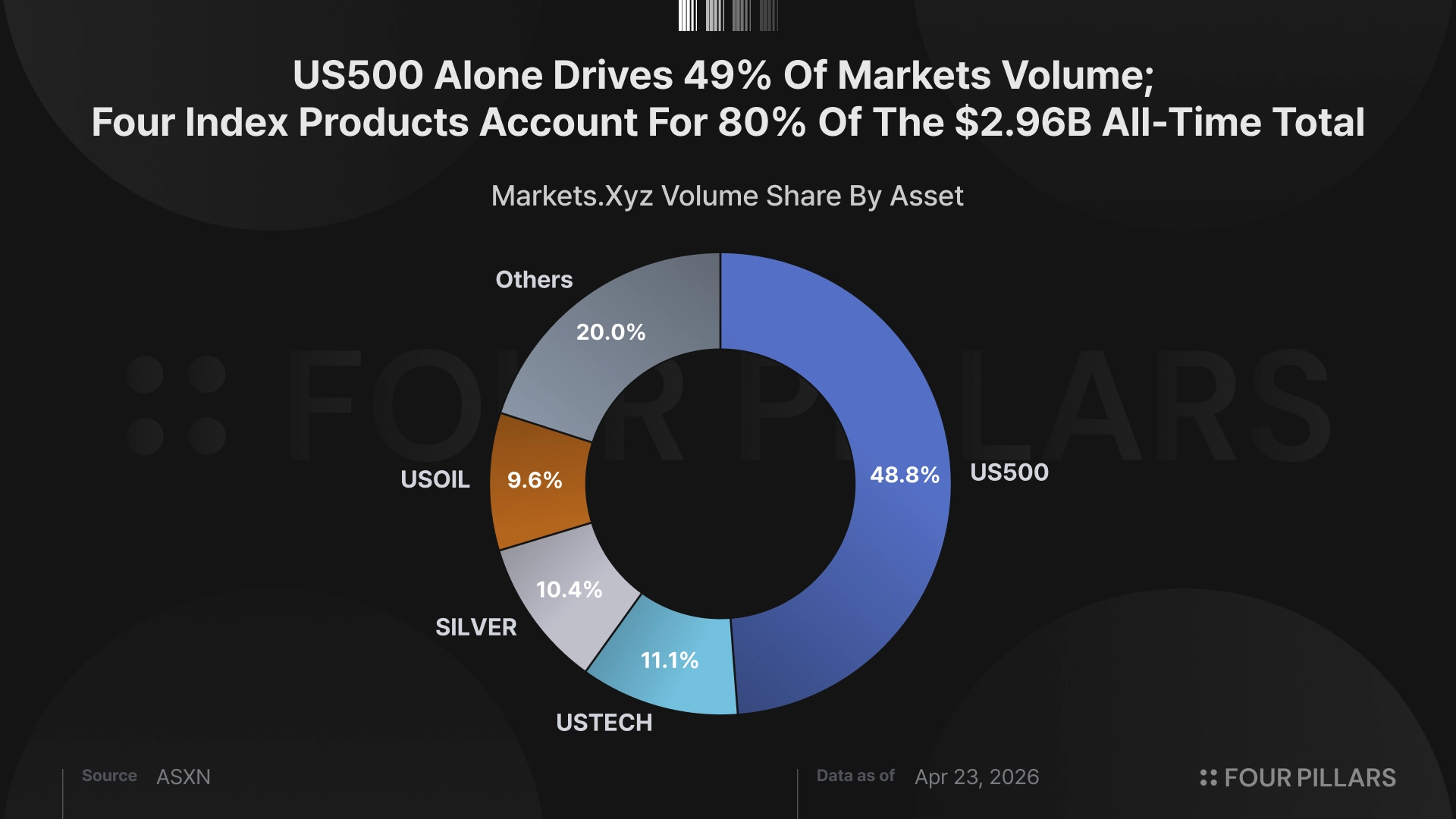

The KNTQ-captures-it bet was not. Markets runs roughly ~$25M per day in volume, 1.2% of HIP-3. TradeXYZ runs $1.63B per day, 91.6%.

Markets has 6,572 all-time users, 2,334 in the past 30 days, and 405 daily. Volume is $2.95B all-time, $695M over 30 days. New user growth peaked at 395-490 per day in January and March, now running 14-60 per day. Open interest across 21 listed markets totals $15.33M with US500 at $5.01M, SMALL2000 at $2.80M, USOIL at $2.00M, USBOND at $1.74M. The equity perps thesis from the original piece IS materializing, just at a smaller scale than I projected. Liquidity quality on the deeper markets is tight: US500 spreads at 0.10bps, slippage at $10K of 0.64bps, $100K of 2.12bps. Tail markets are thin, but the core products are liquid for HIP-3.

Deployer revenue runs at roughly $200K per year from $514K in all-time fees. The fee structure layers 3.5bps taker and 2.0bps maker as builder fees on top of an 0.81bps HIP-3 protocol fee (after Growth Mode’s 90% discount, full rate is ~8.1bps). When Growth Mode ends, the effective taker fee jumps from roughly 4.3bps to 11.6bps, and volume likely collapses at full rates. That’s a cliff in the fee structure.

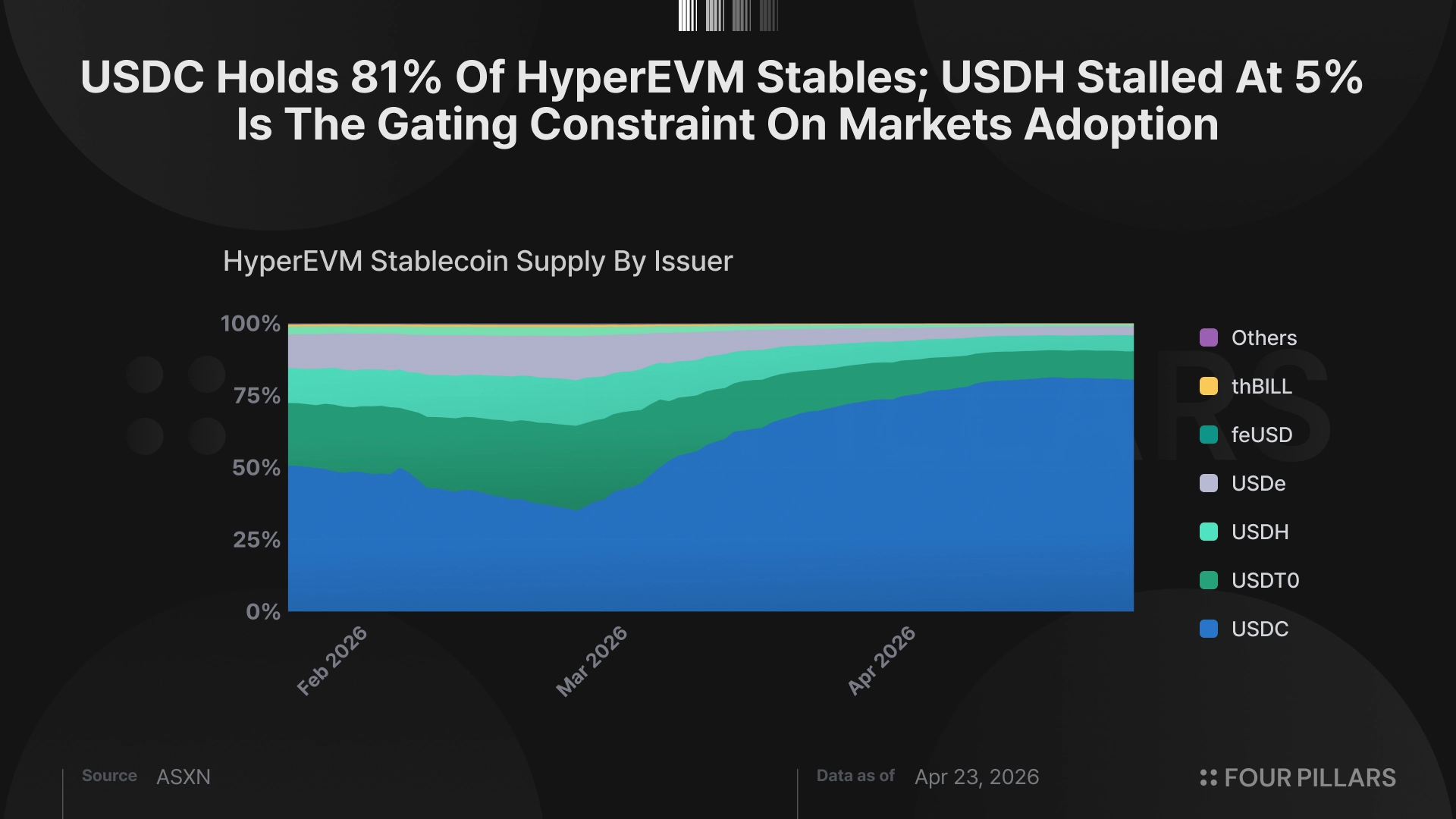

The structural problem sits upstream, and I want to state it once because I’m not going to repeat the diagnosis in later sections. All Markets are USDH-denominated. USDH has $98.3M in supply, 5.36% of HyperEVM stables, versus USDC at $1.48B and 80.82%. USDH friction IS Markets friction. Not two separate problems.

The incentives are well-designed: 20% lower taker fees, 50% better maker rebates, 20% more volume contribution toward fee tiers on USDH-quoted pairs. The problem is demand. Nothing compelling exists to hold USDH for. No canonical perp markets on the HL frontend use it. Even sophisticated traders I’ve spoken with describe the friction as “much higher than we think.”

Exchange stablecoin precedent is clear. Only Binance has ever crossed $1B (BUSD at $23.5B, FDUSD at $4B), and both required forced adoption. Every exchange stablecoin that tried organic growth (Huobi’s HUSD, OKX’s USDK, Gemini’s GUSD) capped below $600M.

The friction is being addressed from multiple angles. USD mode (launched April 20) lets traders use USDC on Markets with auto-routed margin, a native on/off ramp reduces USDH minting friction, HIP-4 creates structural USDH demand through outcome market settlement, and Native Markets at USDH.com adds a dedicated venue. These help traders get in and give USDH incremental use cases, but none of them solve the core demand problem. The catalyst that would move USDH supply at scale is canonical USDH-denominated perps on the HL frontend, and that requires the HL team and the validators. No timeline.

Beyond LST and Markets, Kinetiq runs three additional revenue lines. Two are live and small. One is imminent.

Kinetiq x Hyperion validates 10.06M HYPE at a 3% commission rate, producing roughly $230K per year. That’s 2.3% of total staked HYPE across 17+ active validators, a fraction of the top slots held by Hyper Foundation validators at 53-57M each, or Anchorage/Figment at 34.84M, or Nansen at 24.51M. The revenue is linear, scales with HYPE price, carries zero marginal cost, and is immaterial to the investment thesis at current scale.

sKNTQ is where all revenue lines converge. 106M KNTQ is staked (39.31% of the 270M circulating supply) at $11.16M in TVL. The tier system runs from 50K KNTQ for a 10% fee discount up to 2.5M KNTQ for a 30% discount plus priority kmHYPE access. 100% of Markets income, 100% of Launch revenue, validator commission shares, and 70% of KIP-2 staking revenue all flow into KNTQ buybacks on HyperCore and get distributed to sKNTQ stakers.

At current scale, estimated buyback flow runs roughly $1.55M per year ($1.12M from KIP-2, $200K from Markets, $230K from validators) which produces about 13.9% yield on the $11.16M sKNTQ staked. That’s 1.4% of FDV in annual buyback pressure. At current revenue, the numbers are insignificant. It becomes a value accrual engine at $5-10M or more in revenue, and the 39.31% stake ratio does reduce effective circulating supply in the meantime.

KIP-3 Launch is what matters. It introduces permissionless LST deployments on Hyperliquid. Prospective HIP-3 deployers can crowdsource the HYPE needed to launch their own DEX through Kinetiq, without deploying or managing their own LST infrastructure. It’s not limited to HIP-3 or HIP-4: validators, communities, and DeFi protocols can all launch LSTs to unlock capital efficiency for HYPE sitting idle on HyperCore.

The revenue model is the important part. Kinetiq earns 10% of the deployer share from every bonded DEX. The protocol generates no returns unless deployers do, which aligns the incentive cleanly. 100% of Launch revenue flows into programmatic KNTQ buybacks and gets distributed to sKNTQ. Launch eliminates the roughly $15M HYPE staking requirement to deploy a HIP-3 DEX directly, positioning Kinetiq as the cheapest and fastest path to market for any deployer.

perps.fun is the first proof of demand. It’s the first perpetual futures launchpad on Hyperliquid via HIP-3, anyone can deploy a HIP-3 market for $0 (versus the ~$15M in HYPE to deploy directly), and deployers earn 50% of fees in perpetuity. It’s powered by kpHYPE, an LST deployed through Kinetiq Launch. A third party built a product on Kinetiq’s LST infrastructure, creating a new HIP-3 DEX without deploying their own LST.

Source: X (@Perpsdotfun)

Nova Markets is building on the same infrastructure, a HIP-3 exchange with a "conviction markets" model where traders validate demand before markets get full CLOB listings. That's two deployers (perps.fun + Nova) building on Kinetiq Launch before KIP-3 has shipped. Revenue is $0 today, but the demand signal is there.

HIP-4 extends the surface area. Hyperliquid's native prediction market protocol is live on testnet with no mainnet timeline. KIP-3 enables HIP-4 deployers alongside HIP-3. Same infrastructure, same 10% toll. Prediction markets on Hyperliquid would flow through Kinetiq's LST layer the same way perps.fun does today. HIP-3 and HIP-4 don't need to flow through one Kinetiq product. They need to flow through Kinetiq's infrastructure.

Start with where the $2.0M in annual revenue actually comes from:

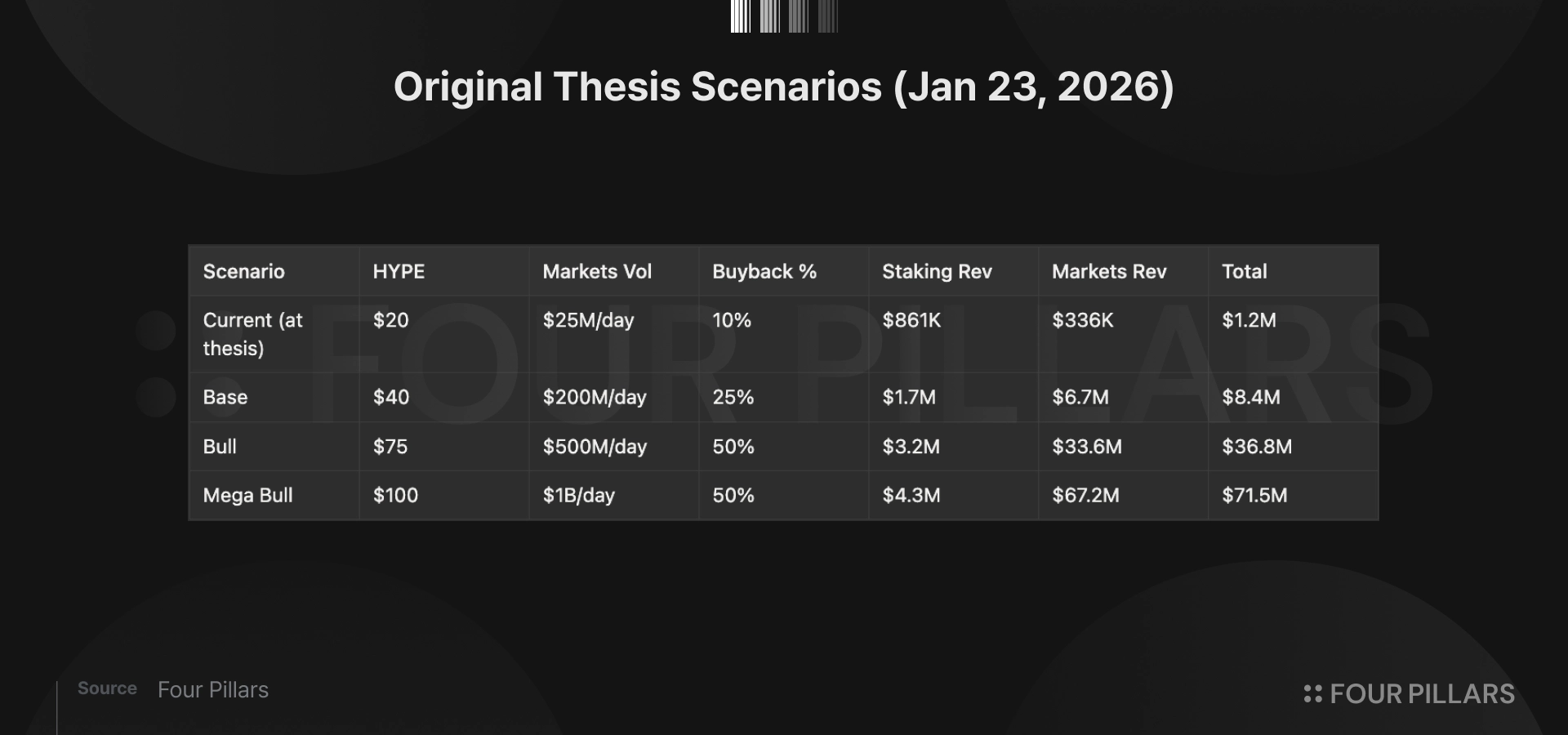

The original thesis projected four scenarios. The base case assumed $200M per day in Markets volume, a 25% buyback rate, and HYPE at $40, producing $8.4M in annual revenue at mature state. These were not three-month forecasts. The buyback rate is now fixed at 10% deployer share, not the variable 25% I originally modeled. Staking revenue ($1.6M) tracks close to the base case staking line ($1.7M at HYPE $40). The entire gap between current revenue and the base case is Markets, and per the USDH analysis above, that gap depends on USDH adoption measured in years, not months.

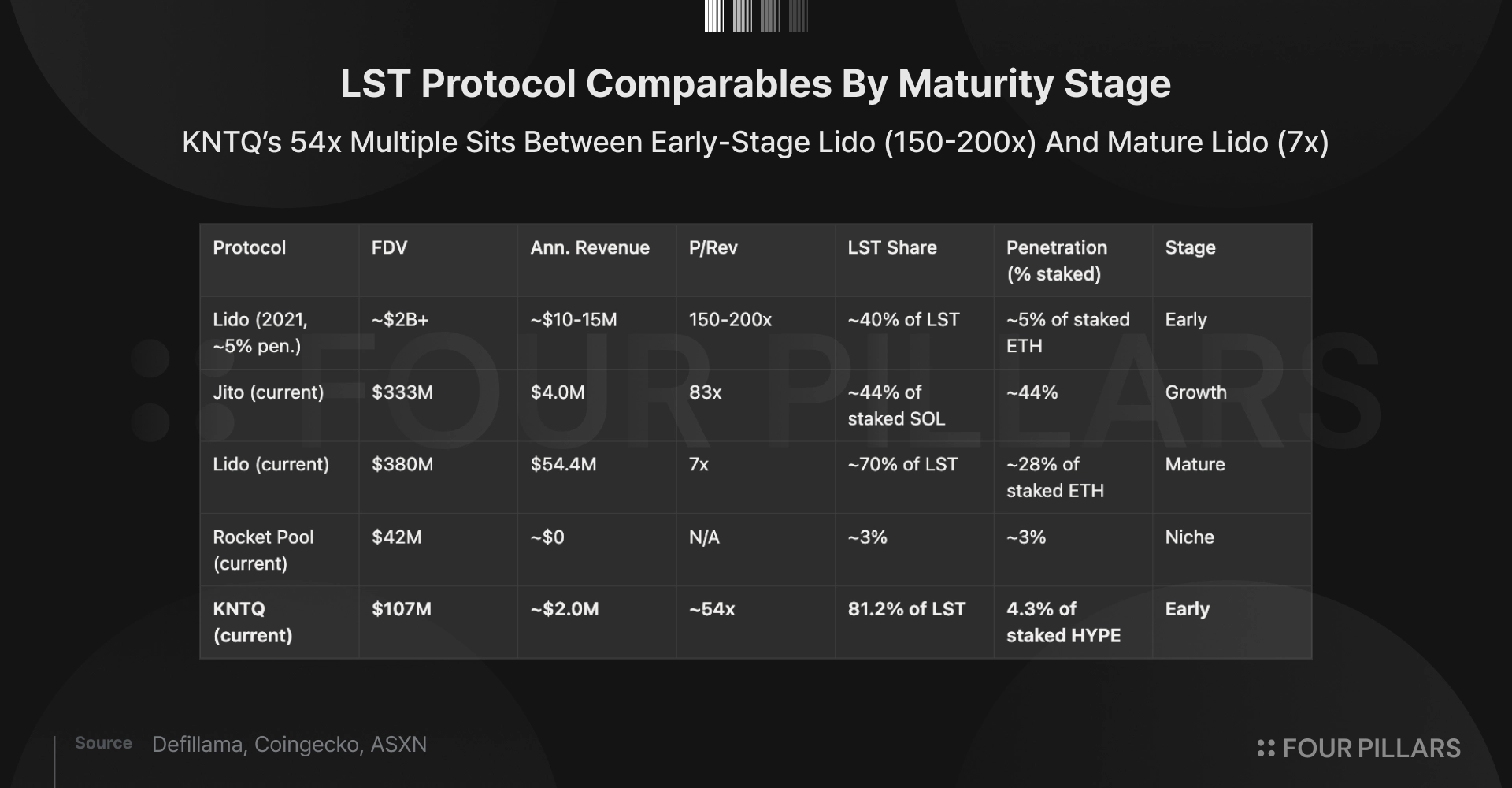

The comp table is where the Lido comparison gets quantified:

KNTQ’s 54x sits between mature Lido (7x) and early Lido (150-200x). At 4.3% penetration with 81% dominance, the maturity stage reads closer to early Lido than anything else in the comp set. Whether 54x is defensible depends on whether you believe the penetration curve bends up. The key difference: Ethereum DeFi needed stETH for capital efficiency because it was collateral across Aave, Maker, and Curve at scale. Hyperliquid’s DeFi ecosystem is building those integrations but the structural necessity hasn’t arrived.

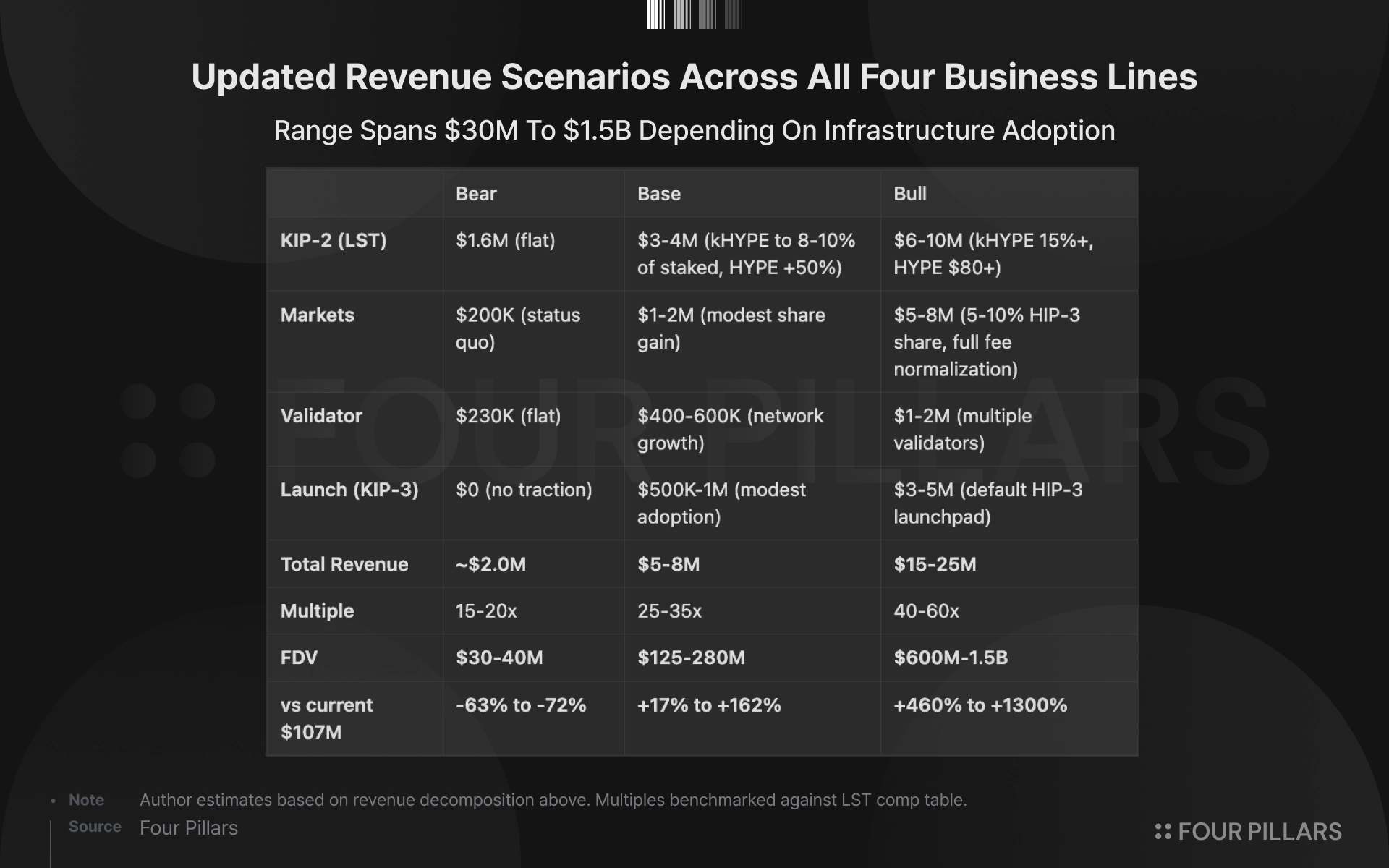

Updated scenarios incorporating all four revenue lines:

Bear case first — Nothing works, penetration stalls, USDH stays stuck, KIP-3 finds no traction. The floor at $30M reflects a protocol that has users, revenue, and dominance, not a zero, but painful from $107M. In a true bear, HYPE itself declines and compresses KIP-2 revenue directly through price. At $30-40M FDV, that's $0.03-0.04 per KNTQ.

The base case requires kHYPE penetration to grow organically to 8-10% of staked HYPE as HyperEVM DeFi matures, HYPE to appreciate roughly 50%, USD mode to add modest Markets traction, and KIP-3 to ship with early adoption. Each is individually plausible, and together they produce $125-280M in FDV (~$0.13-0.28).

The bull case needs the full stack to fire. kHYPE as default collateral at 15%+ penetration, Markets capturing meaningful share, KIP-3 becoming the canonical launchpad, and HYPE past $80. At $600M-1.5B, that's $0.60-1.50 per KNTQ.

KIP-2 is 80% of revenue today because KIP-3 is unshipped and Markets is early — that's the floor, not the thesis. You're not paying 54x for an LST at 4.3% penetration. You're paying for the infrastructure position underneath HIP-3 and HIP-4, where Markets captures volume, KIP-3 turns every deployer into a revenue source, and 81% LST dominance is the moat that makes displacement hard.

Three months of price action went against me, and none of the catalysts have fired yet. Three months is too short to grade an infrastructure thesis. But the clock doesn’t care. 730M KNTQ tokens vest with a one-year cliff in November 2026, followed by 73M per month for two years. That gives KIP-3 roughly six months to show something before the unlock math starts dominating the supply picture.

Here’s what I’m watching:

kHYPE supply growth: 18.6M toward 30M+ (4.3% to ~7% of staked HYPE) means the penetration thesis is working.

Markets HIP-3 share: 1.2% toward 5%+ suggests denomination friction was the bottleneck.

KIP-3 adoption: deployer count and revenue from the 10% perpetual share in the first three months post-launch.

HIP-4 mainnet progress: testnet today, no timeline. Mainnet launch = new deployer surface area for KIP-3.

sKNTQ staking ratio: currently 39.3%. Below 25% means loss of faith ahead of the unlock.

KNTQ vs HYPE relative performance: continued underperformance by more than 50 percentage points on a 90-day rolling basis triggers a hard position review.

I’ll be back when the data updates the thesis again.

Dive into 'Narratives' that will be important in the next year