*Special thanks to @OxOmnia for feedback and review.

Capital requirements under HIP‑3 limit who can launch new markets; Kinetiq’s Launch solves this by crowdfunding the 1m HYPE bond.

Kinetiq started as Hyperliquid’s liquid staking protocol and now manages about 36m HYPE, making it the network’s leading financial hub through vkHYPE yield aggregation and the institutional iHYPE pool.

Unlike most LST protocols, Kinetiq’s value capture is uncapped because every HIP‑3 market deployed through Launch becomes a new fee stream; exLSTs function like micro‑exchange equity and can outperform base staking yields if volumes scale.

kHYPE doesn’t yet share in Launch fees, but illustrative scenarios show that even a handful of few dozen exchanges could generate tens of millions in revenue; actual upside depends on future token value accrual mechanism, sustained trading volume, oracle reliability and competitive dynamics.

Most crypto experiments are still searching for product–market fit, but a few stand out as undeniable winners: stablecoins, payments, and especially perpetual futures (perps) trading.

The growth of perps has been astonishing. Monthly perp trading volumes have grown from about $35b in 2018 to $6.4t in May 2025, and they now represent over 90% of all crypto derivatives volume.

Traders worldwide gravitate to perps for their high leverage and continuous trading (no expirations), making them the go-to instruments for speculation and hedging in crypto. Perpetuals have essentially become crypto’s equivalent of stock market indices or FX pairs—massive, liquid, and always in demand. Now, the question isn’t whether perps will matter, but who will build the infrastructure to capture their next wave of growth.

Hyperliquid’s HIP‑3 is the breakthrough that makes it possible for anyone to launch their own perp markets on-chain. Instead of rebuilding an exchange, teams can plug into Hyperliquid’s matching engine and orderbook. As Alvin Hsia (co-founder of Ventuals) explained, HIP‑3’s recipe is market + oracle + demand. If you can find a number people want to bet on (up or down) and provide a credible price oracle for it, you can create a market for it.

Source: X (@alvinhsia)

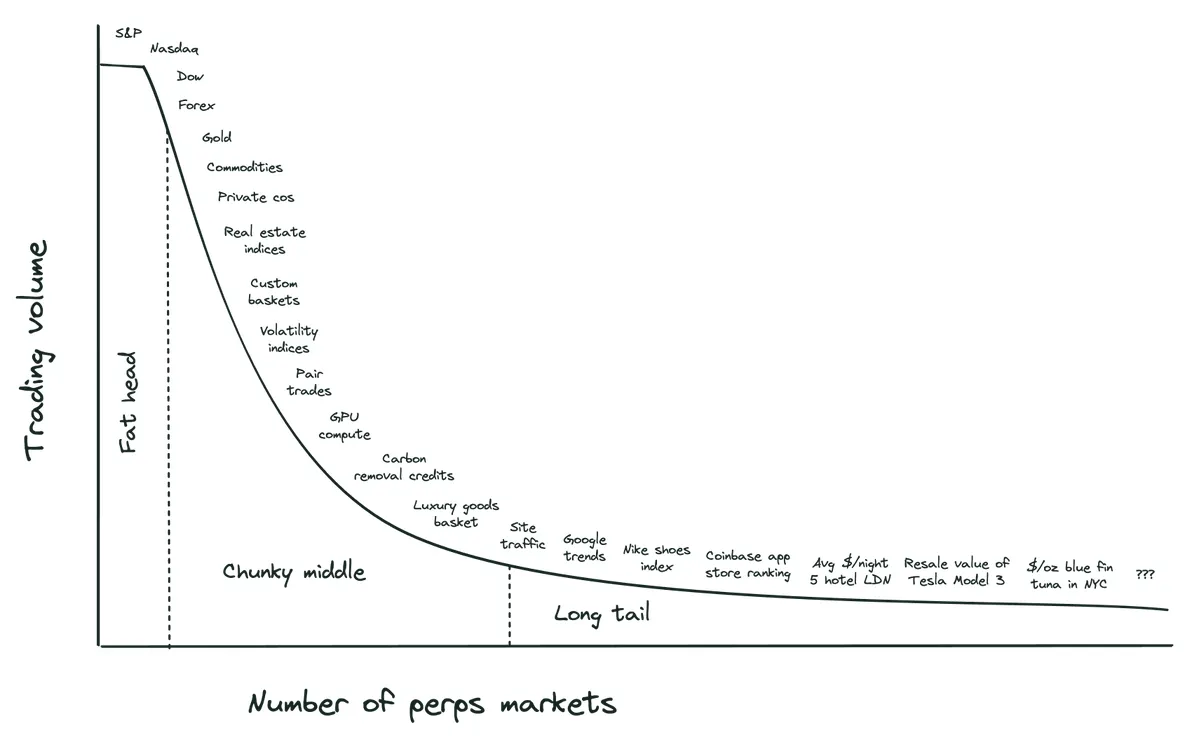

Practically anything that can be measured and has people who want to speculate on it is fair game. Markets can range anywhere from the “fat head” like S&P or FX pairs to the “chunky middle” like pre‑IPO equities, all the way to long‑tail experiments like tuna per ounce in NYC.

As an example, Ventuals is working on pre‑IPO perp markets, using HIP‑3 to list equity like instruments that don’t exist anywhere else. Prediction markets too—@footballdotfun and @noise_xyz are early examples that can be made via HIP‑3.

But deploying a HIP‑3 exchange requires staking 1m HYPE ($40~50m at current prices). That’s a very high barrier, especially for startups. Without a way around that, HIP‑3 would remain accessible only to very large players.

Kinetiq launched as Hyperliquid’s native liquid staking protocol. HYPE has a 7 day unbonding period, so liquid staking was an obvious need. Stake via Kinetiq and you receive kHYPE, a yield bearing token that represents your staked HYPE.

Adoption was immediate. Within two weeks of launch, Kinetiq passed $750m TVL, and it now secures over $1.7b HYPE from ~12k holders. Currently kHYPE is widely integrated across Hyperliquid defi, from lending to AMMs. It also delegates across validators via StakeHub, a performance based scoring system, eliminating bias in validator selection entirely, reducing centralization and aligning with Hyperliquid’s ethos.

Where most LST protocols stop at staking yield, Kinetiq built an Earn vault in partnership with Veda’s Seven Seas. Deposit kHYPE (or HYPE) and you receive vkHYPE, a share token that tracks your principal plus compounded yield and earns kPoints. Veda deploys the vault across lending, LPing and leverage strategies on HyperEVM, charging a performance fee only on profits. In essence, Kinetiq bootstraps a low maintenance yield aggregator on top of the base staking rate, similar in spirit to stETH’s integration in Curve or Jito’s MEV auctions, but native to Hyperliquid.

For institutions, Kinetiq has created iHYPE, a KYB/KYC compliant pool with its own isolated validator delegation and custom LST tickers. iHYPE gives professional allocators the same yield benefits as kHYPE while meeting regulatory requirements and offering more control over validator selection. Hyperion DeFi, the first public company to adopt it, has amassed over 1.5 million HYPE and staked through iHYPE, demonstrating institutional appetite.

This alone made Kinetiq the largest liquid staking protocol on HyperEVM. But the real potential comes from what came next: Kinetiq Launch.

Launch is an Exchange‑as‑a‑Service platform built on HIP‑3. Instead of a single operator staking $40~$50m (as of Aug 26, 2025), Kinetiq crowdsources the capital into isolated pools. Each pool backs one exchange, and contributors receive exchange specific LSTs (exLSTs) entitling them to trading fees and governance. Risk is segregated, so a slashing event in one market doesn’t spill over to others.

This architecture is powerful for several reasons:

Exchange deployers no longer need tens of millions of dollars to experiment. They define the market, oracle and margin parameters, plug into Kinetiq’s dashboard and HyperCore handles execution. That lowers the barrier for venture funds, trading desks or domain experts to launch bespoke perps.

HYPE holders gain new yield primitives. Instead of simply staking, they can back specific exchanges they believe will generate flow and earn exLSTs on top of kHYPE staking rewards.

Traders gain access to a flood of specialized markets built on Hyperliquid’s high performance infrastructure. Launch democratizes exchange building, but it also acts as a filter: only markets with real demand and credible oracles will sustain themselves.

Hyperliquid expands its market set without monopolizing listings. Each new market increases trading fees routed back to the network, reinforcing the HYPE buyback flywheel. HIP‑3 commoditizes the exchange layer; Launch commoditizes the capital layer.

As Kinetiq puts it, this is the Shopify x Kickstarter analogy: plug‑and‑play infrastructure married with community driven funding.

To understand why Kinetiq could command a fat premium, it helps to benchmark against peers. Lido’s stETH captures the 3~4% ETH staking rate and takes a 10% cut of rewards. Jito’s jitoSOL earns staking plus MEV yield, boosting net APY to ~7% and justifying a higher multiple.

Kinetiq’s kHYPE base yield is comparable to Hyperliquid staking (around 2.3% with current supply), but its value capture is uncapped: every HIP‑3 market deployed through Launch is a new revenue stream. Think of exLSTs as synthetic equities in microexchanges. If even a handful of markets clear daily volumes comparable to Hyperliquid’s main perps, fee flows to Kinetiq backers could dwarf staking rewards.

There’s also a network effects angle. Builder codes (Hyperliquid’s referral/fee‑sharing IDs) have generated over US $32 million in revenue as of August 26, 2025, signalling a growing ecosystem of wallets, bots and frontends that steer order flow. HIP‑3 markets created via Launch can tap into that distribution by being supported on builder code enabled frontends such as Phantom, Axiom or pvp.trade, which helps accelerate liquidity uptake. Competitors like beHYPE or stHYPE operate as pure LSTs; they lack this capital allocation layer.

Source: Hypeburn.fun

Right now, kHYPE accrues staking yield and kPoints, but it doesn’t yet share in Launch fees. To sketch a credible bull case you need to run some back‑of‑the‑envelope numbers. The figures below are purely hypothetical and deliberately simple.

Hyperliquid sets the baseline fee for each trade. For most traders, it’s roughly 0.045% for takers and 0.015% for makers. A HIP‑3 deployer can (a) add their own surcharge on top of that base and (b) take up to 50% of the total fee (base plus extra) as revenue.

For example, if the base taker fee is 0.045% and you add a 0.005% surcharge, the all‑in taker fee becomes 0.05%. Under HIP‑3, you could choose to pocket anywhere between 0% and 50% of that 0.05% (up to 0.025%) and whatever you don’t take flows back to the HLP/Assistance Fund.

Now assume Launch brings ten exchanges online in its first year, each doing roughly US $10b in annual trading volume (about what Dexari or Merkle Trade would do if you annualize their last 30 days of volume as of 26 Aug 2025). A 0.05% fee on that flow yields US $5m in gross fees per exchange. If each deployer takes half, they’d collect $2.5m each, or $25m in total across the ten exchanges.

If Kinetiq directs 40% of that fee pool to exLST holders, 40% to the deployers and 20% to its treasury, the treasury would earn about $5m in the first year. Scale up to 100 exchanges and you get $50m. Applying a 20~30× multiple to that revenue (which is pretty conservative in an industry where token valuations can run well ahead of revenue) implies a valuation around current TVL.

Of course, these outcomes depend on real trading demand, reliable oracles and sound validator management. But fee optionality and scalability is what separates Kinetiq from pure liquid staking plays like Lido.

Perpetual futures are crypto’s clearest product–market fit. Hyperliquid is the largest perpetuals DEX to date and the first true Binance competitor to have cleared more than US$2.4t in trading volume. Kinetiq sits at the intersection, securing billions of dollars in HYPE, offering yield aggregation, onboarding institutions and enabling permissionless perps through Launch. Its combination of base yield, vault yield and exLST fee flows gives it a broader value capture surface than typical LSTs. My conviction is high that this platform will be a major coordination layer for new perps markets.

Dive into 'Narratives' that will be important in the next year